Comprehensive Report on Investment Appraisal and Budgeting Analysis

VerifiedAdded on 2023/06/17

|19

|3943

|174

Report

AI Summary

This report provides a detailed analysis of accounting and finance principles, focusing on investment appraisal techniques, break-even analysis, and budgetary control. It includes an examination of Tom and Jerry Limited's financial statements, calculating key metrics such as gross profit, net profit, and financial position. The report also assesses Fidel & Ana Limited's break-even point in units and revenue, margin of safety, and profitability with and without advertising. Furthermore, it evaluates investment appraisal techniques like Net Present Value (NPV), payback period, and Accounting Rate of Return (ARR), discussing their merits and demerits. Finally, the report explores the benefits and drawbacks of using budgetary tools for strategic planning, emphasizing the importance of financial management in achieving organizational goals. Desklib provides access to this and other solved assignments to aid students in their studies.

Introduction to

Accounting and Finance

Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1 Tom and Jerry Limited............................................................................................................3

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020................................3

Financial Position of Tom and Jerry Ltd as at 31 December 2020............................................................4

QUESTION 2.................................................................................................................................................5

a).............................................................................................................................................................5

b).............................................................................................................................................................6

c)..............................................................................................................................................................8

d).............................................................................................................................................................9

e) Explaining the assumptions of break even model and its utilization................................................10

QUESTION 3...............................................................................................................................................11

a) Calculating investment appraisal techniques....................................................................................11

b) Explaining key merits and demerits of investment appraisal techniques..........................................13

c) Explaining the benefits and drawback of budgetary tool for strategic planning................................15

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

INTRODUCTION...........................................................................................................................................3

QUESTION 1 Tom and Jerry Limited............................................................................................................3

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020................................3

Financial Position of Tom and Jerry Ltd as at 31 December 2020............................................................4

QUESTION 2.................................................................................................................................................5

a).............................................................................................................................................................5

b).............................................................................................................................................................6

c)..............................................................................................................................................................8

d).............................................................................................................................................................9

e) Explaining the assumptions of break even model and its utilization................................................10

QUESTION 3...............................................................................................................................................11

a) Calculating investment appraisal techniques....................................................................................11

b) Explaining key merits and demerits of investment appraisal techniques..........................................13

c) Explaining the benefits and drawback of budgetary tool for strategic planning................................15

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

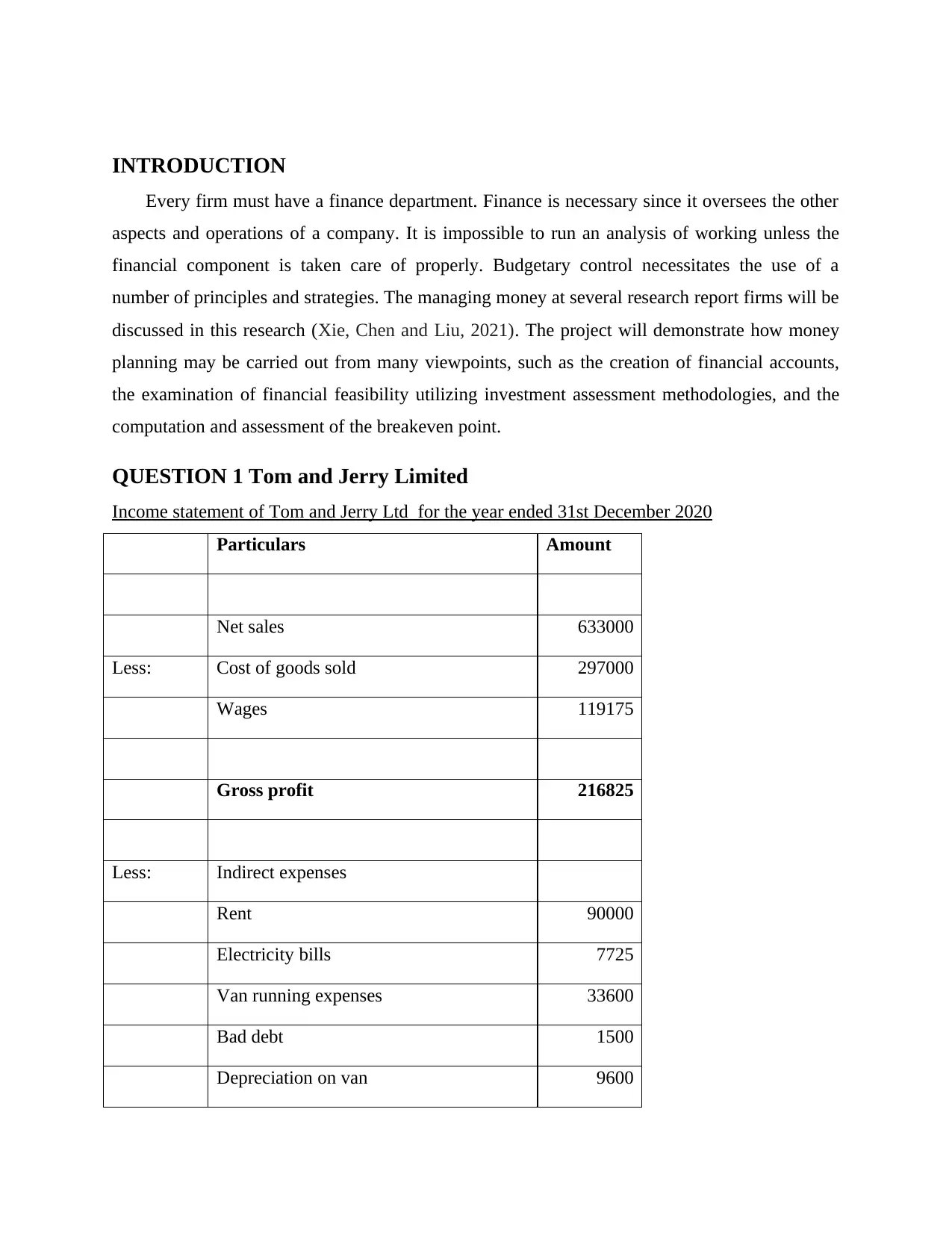

INTRODUCTION

Every firm must have a finance department. Finance is necessary since it oversees the other

aspects and operations of a company. It is impossible to run an analysis of working unless the

financial component is taken care of properly. Budgetary control necessitates the use of a

number of principles and strategies. The managing money at several research report firms will be

discussed in this research (Xie, Chen and Liu, 2021). The project will demonstrate how money

planning may be carried out from many viewpoints, such as the creation of financial accounts,

the examination of financial feasibility utilizing investment assessment methodologies, and the

computation and assessment of the breakeven point.

QUESTION 1 Tom and Jerry Limited

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020

Particulars Amount

Net sales 633000

Less: Cost of goods sold 297000

Wages 119175

Gross profit 216825

Less: Indirect expenses

Rent 90000

Electricity bills 7725

Van running expenses 33600

Bad debt 1500

Depreciation on van 9600

Every firm must have a finance department. Finance is necessary since it oversees the other

aspects and operations of a company. It is impossible to run an analysis of working unless the

financial component is taken care of properly. Budgetary control necessitates the use of a

number of principles and strategies. The managing money at several research report firms will be

discussed in this research (Xie, Chen and Liu, 2021). The project will demonstrate how money

planning may be carried out from many viewpoints, such as the creation of financial accounts,

the examination of financial feasibility utilizing investment assessment methodologies, and the

computation and assessment of the breakeven point.

QUESTION 1 Tom and Jerry Limited

Income statement of Tom and Jerry Ltd for the year ended 31st December 2020

Particulars Amount

Net sales 633000

Less: Cost of goods sold 297000

Wages 119175

Gross profit 216825

Less: Indirect expenses

Rent 90000

Electricity bills 7725

Van running expenses 33600

Bad debt 1500

Depreciation on van 9600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

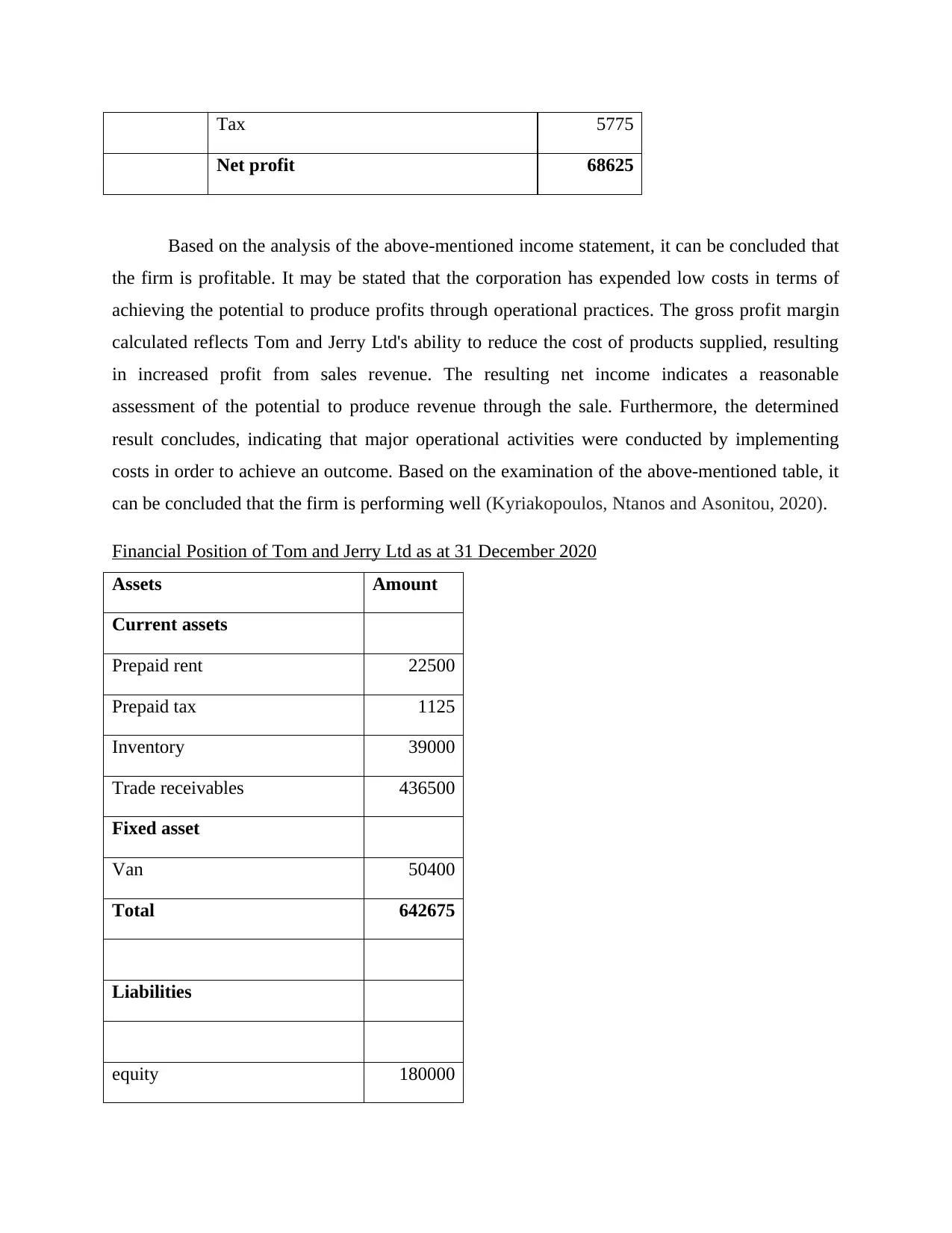

Tax 5775

Net profit 68625

Based on the analysis of the above-mentioned income statement, it can be concluded that

the firm is profitable. It may be stated that the corporation has expended low costs in terms of

achieving the potential to produce profits through operational practices. The gross profit margin

calculated reflects Tom and Jerry Ltd's ability to reduce the cost of products supplied, resulting

in increased profit from sales revenue. The resulting net income indicates a reasonable

assessment of the potential to produce revenue through the sale. Furthermore, the determined

result concludes, indicating that major operational activities were conducted by implementing

costs in order to achieve an outcome. Based on the examination of the above-mentioned table, it

can be concluded that the firm is performing well (Kyriakopoulos, Ntanos and Asonitou, 2020).

Financial Position of Tom and Jerry Ltd as at 31 December 2020

Assets Amount

Current assets

Prepaid rent 22500

Prepaid tax 1125

Inventory 39000

Trade receivables 436500

Fixed asset

Van 50400

Total 642675

Liabilities

equity 180000

Net profit 68625

Based on the analysis of the above-mentioned income statement, it can be concluded that

the firm is profitable. It may be stated that the corporation has expended low costs in terms of

achieving the potential to produce profits through operational practices. The gross profit margin

calculated reflects Tom and Jerry Ltd's ability to reduce the cost of products supplied, resulting

in increased profit from sales revenue. The resulting net income indicates a reasonable

assessment of the potential to produce revenue through the sale. Furthermore, the determined

result concludes, indicating that major operational activities were conducted by implementing

costs in order to achieve an outcome. Based on the examination of the above-mentioned table, it

can be concluded that the firm is performing well (Kyriakopoulos, Ntanos and Asonitou, 2020).

Financial Position of Tom and Jerry Ltd as at 31 December 2020

Assets Amount

Current assets

Prepaid rent 22500

Prepaid tax 1125

Inventory 39000

Trade receivables 436500

Fixed asset

Van 50400

Total 642675

Liabilities

equity 180000

net profit 67500

Out sanding wages 2175

Trade payable 393000

Total 642675

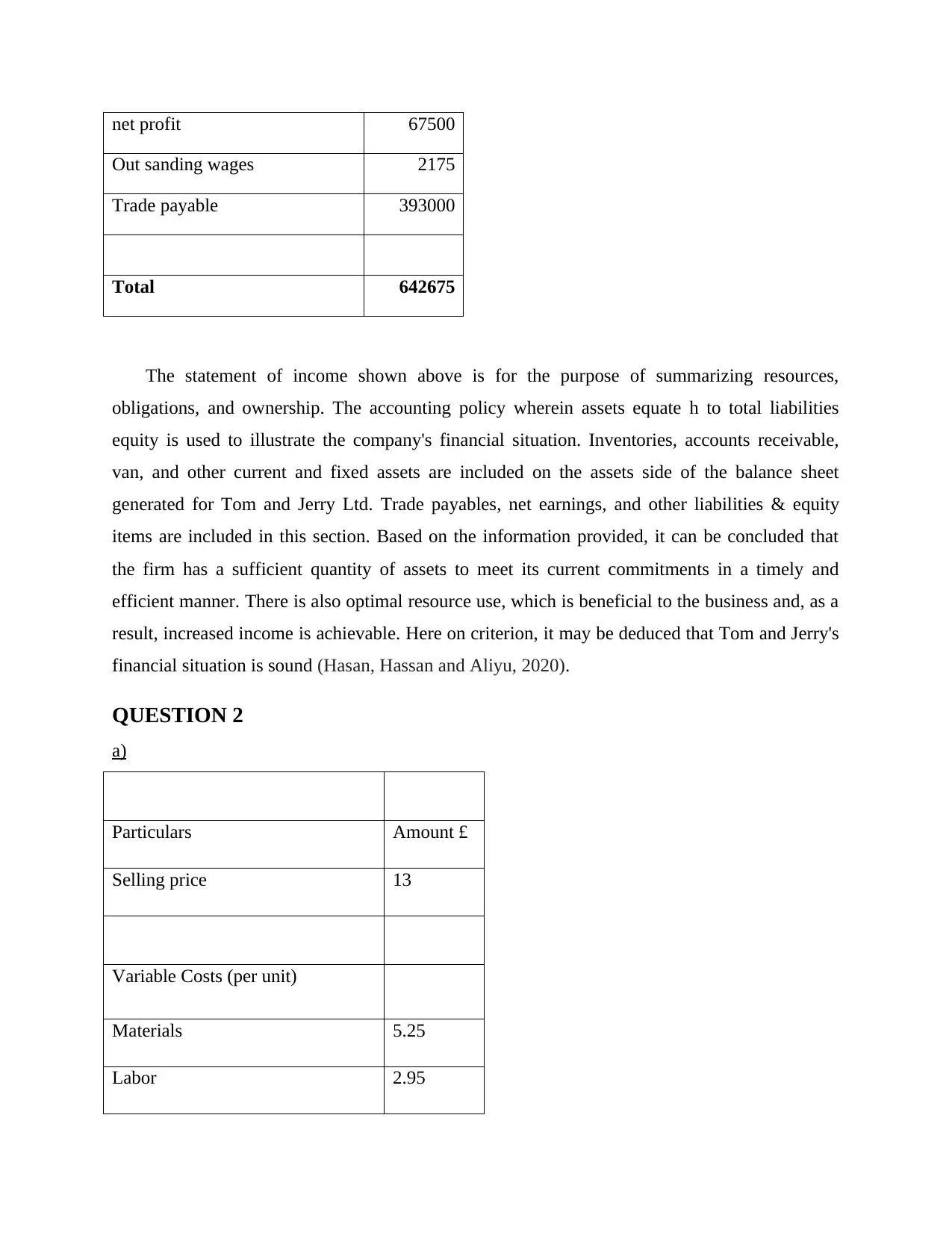

The statement of income shown above is for the purpose of summarizing resources,

obligations, and ownership. The accounting policy wherein assets equate h to total liabilities

equity is used to illustrate the company's financial situation. Inventories, accounts receivable,

van, and other current and fixed assets are included on the assets side of the balance sheet

generated for Tom and Jerry Ltd. Trade payables, net earnings, and other liabilities & equity

items are included in this section. Based on the information provided, it can be concluded that

the firm has a sufficient quantity of assets to meet its current commitments in a timely and

efficient manner. There is also optimal resource use, which is beneficial to the business and, as a

result, increased income is achievable. Here on criterion, it may be deduced that Tom and Jerry's

financial situation is sound (Hasan, Hassan and Aliyu, 2020).

QUESTION 2

a)

Particulars Amount £

Selling price 13

Variable Costs (per unit)

Materials 5.25

Labor 2.95

Out sanding wages 2175

Trade payable 393000

Total 642675

The statement of income shown above is for the purpose of summarizing resources,

obligations, and ownership. The accounting policy wherein assets equate h to total liabilities

equity is used to illustrate the company's financial situation. Inventories, accounts receivable,

van, and other current and fixed assets are included on the assets side of the balance sheet

generated for Tom and Jerry Ltd. Trade payables, net earnings, and other liabilities & equity

items are included in this section. Based on the information provided, it can be concluded that

the firm has a sufficient quantity of assets to meet its current commitments in a timely and

efficient manner. There is also optimal resource use, which is beneficial to the business and, as a

result, increased income is achievable. Here on criterion, it may be deduced that Tom and Jerry's

financial situation is sound (Hasan, Hassan and Aliyu, 2020).

QUESTION 2

a)

Particulars Amount £

Selling price 13

Variable Costs (per unit)

Materials 5.25

Labor 2.95

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

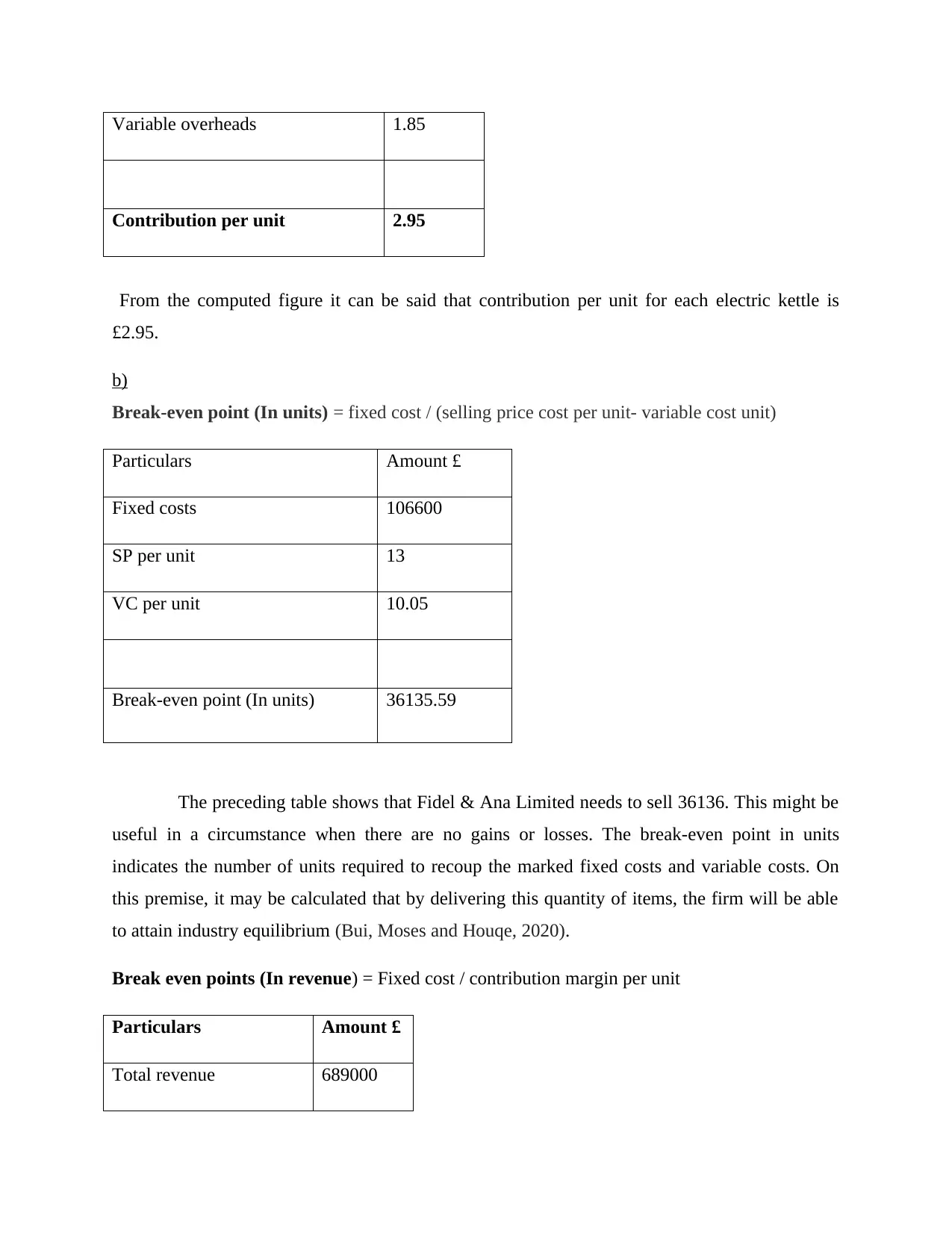

Variable overheads 1.85

Contribution per unit 2.95

From the computed figure it can be said that contribution per unit for each electric kettle is

£2.95.

b)

Break-even point (In units) = fixed cost / (selling price cost per unit- variable cost unit)

Particulars Amount £

Fixed costs 106600

SP per unit 13

VC per unit 10.05

Break-even point (In units) 36135.59

The preceding table shows that Fidel & Ana Limited needs to sell 36136. This might be

useful in a circumstance when there are no gains or losses. The break-even point in units

indicates the number of units required to recoup the marked fixed costs and variable costs. On

this premise, it may be calculated that by delivering this quantity of items, the firm will be able

to attain industry equilibrium (Bui, Moses and Houqe, 2020).

Break even points (In revenue) = Fixed cost / contribution margin per unit

Particulars Amount £

Total revenue 689000

Contribution per unit 2.95

From the computed figure it can be said that contribution per unit for each electric kettle is

£2.95.

b)

Break-even point (In units) = fixed cost / (selling price cost per unit- variable cost unit)

Particulars Amount £

Fixed costs 106600

SP per unit 13

VC per unit 10.05

Break-even point (In units) 36135.59

The preceding table shows that Fidel & Ana Limited needs to sell 36136. This might be

useful in a circumstance when there are no gains or losses. The break-even point in units

indicates the number of units required to recoup the marked fixed costs and variable costs. On

this premise, it may be calculated that by delivering this quantity of items, the firm will be able

to attain industry equilibrium (Bui, Moses and Houqe, 2020).

Break even points (In revenue) = Fixed cost / contribution margin per unit

Particulars Amount £

Total revenue 689000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

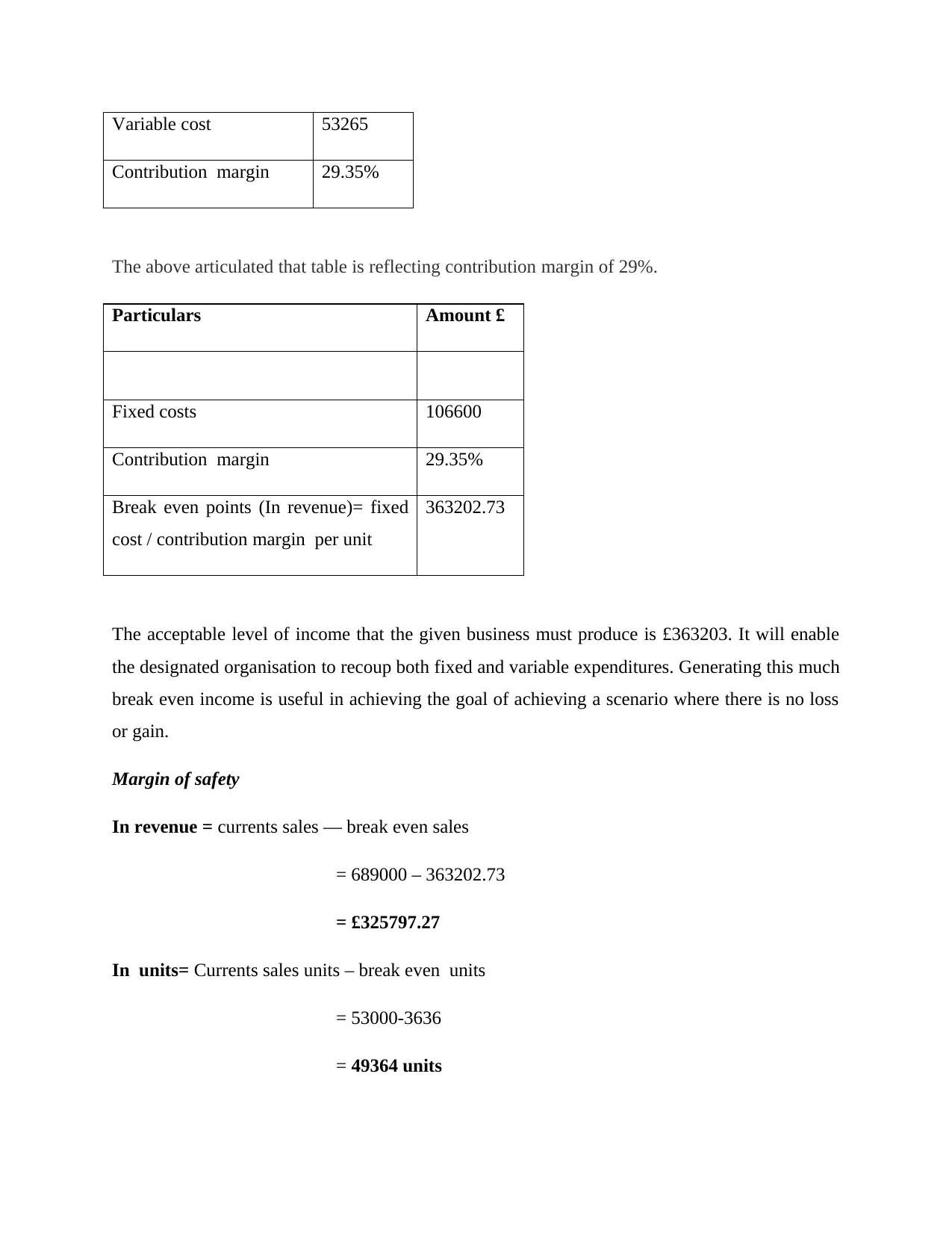

Variable cost 53265

Contribution margin 29.35%

The above articulated that table is reflecting contribution margin of 29%.

Particulars Amount £

Fixed costs 106600

Contribution margin 29.35%

Break even points (In revenue)= fixed

cost / contribution margin per unit

363202.73

The acceptable level of income that the given business must produce is £363203. It will enable

the designated organisation to recoup both fixed and variable expenditures. Generating this much

break even income is useful in achieving the goal of achieving a scenario where there is no loss

or gain.

Margin of safety

In revenue = currents sales — break even sales

= 689000 – 363202.73

= £325797.27

In units= Currents sales units – break even units

= 53000-3636

= 49364 units

Contribution margin 29.35%

The above articulated that table is reflecting contribution margin of 29%.

Particulars Amount £

Fixed costs 106600

Contribution margin 29.35%

Break even points (In revenue)= fixed

cost / contribution margin per unit

363202.73

The acceptable level of income that the given business must produce is £363203. It will enable

the designated organisation to recoup both fixed and variable expenditures. Generating this much

break even income is useful in achieving the goal of achieving a scenario where there is no loss

or gain.

Margin of safety

In revenue = currents sales — break even sales

= 689000 – 363202.73

= £325797.27

In units= Currents sales units – break even units

= 53000-3636

= 49364 units

From the projected data on margin of safety, which is directly associated with predicting

the overall sales or units that surpass the breakeven point. The sales margin of safety indicates

that income from breakeven sales exceeds revenues. Furthermore, the sum indicated in terms of

quantity represents more individuals than the breakeven equivalents. It is mostly carried out to

ensure that market pressures are met with safety.

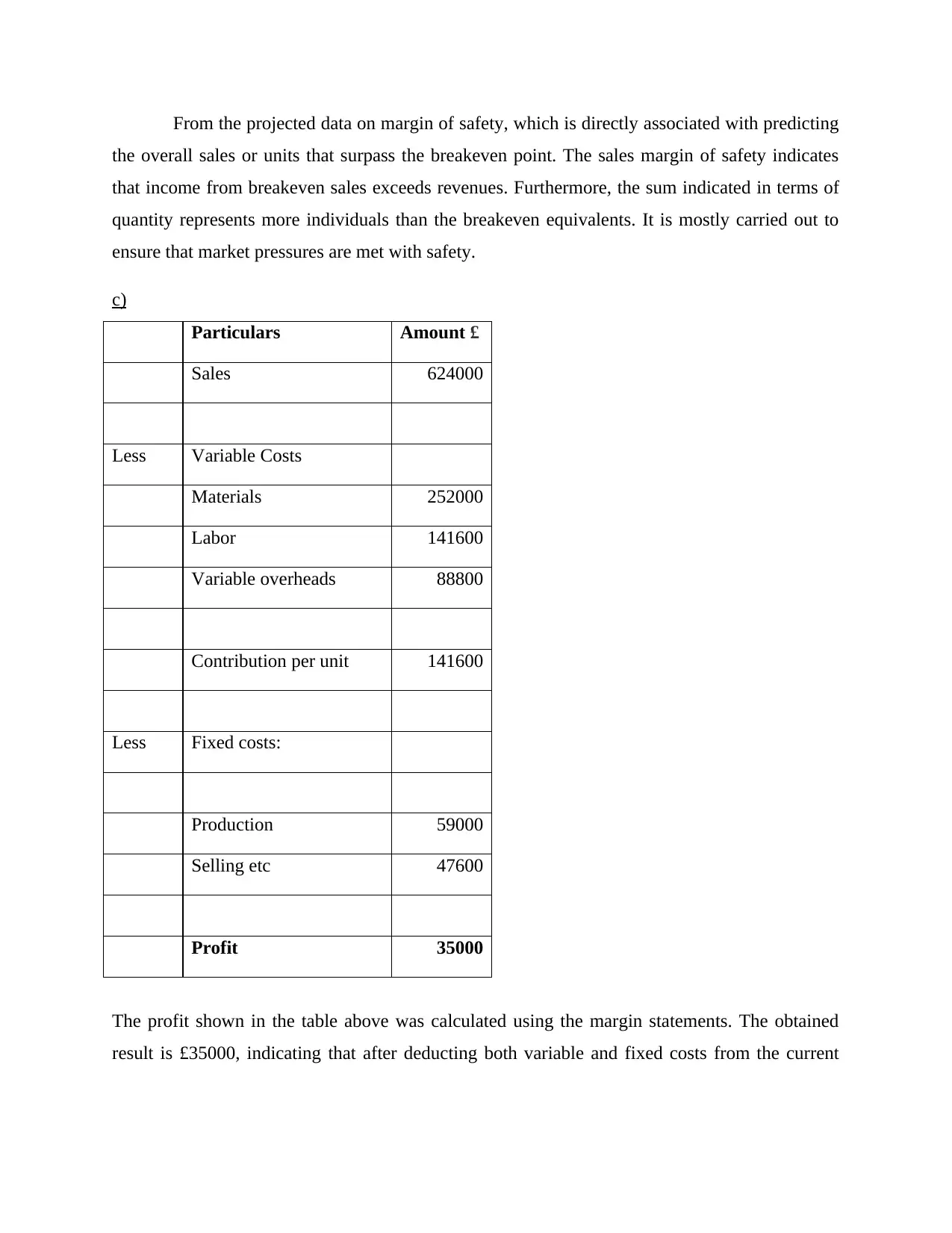

c)

Particulars Amount £

Sales 624000

Less Variable Costs

Materials 252000

Labor 141600

Variable overheads 88800

Contribution per unit 141600

Less Fixed costs:

Production 59000

Selling etc 47600

Profit 35000

The profit shown in the table above was calculated using the margin statements. The obtained

result is £35000, indicating that after deducting both variable and fixed costs from the current

the overall sales or units that surpass the breakeven point. The sales margin of safety indicates

that income from breakeven sales exceeds revenues. Furthermore, the sum indicated in terms of

quantity represents more individuals than the breakeven equivalents. It is mostly carried out to

ensure that market pressures are met with safety.

c)

Particulars Amount £

Sales 624000

Less Variable Costs

Materials 252000

Labor 141600

Variable overheads 88800

Contribution per unit 141600

Less Fixed costs:

Production 59000

Selling etc 47600

Profit 35000

The profit shown in the table above was calculated using the margin statements. The obtained

result is £35000, indicating that after deducting both variable and fixed costs from the current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sales income, Fidel & Ana Limited would be able to achieve such advantages, resulting in

increased flexibility to align with current conditions.

d)

Particulars Amount

(after advertising)

Amount

(Before

advertising)

Sales 878681.7 689000

Less Variable Costs

Materials 325552.5 278250

Labor 182929.5 156350

Variable overheads 114718.5 98050

Contribution per unit 255481.2 156350

Less Fixed costs:

Production 59000 59000

selling etc. 47600 47600

Profit 148881.2 49750

Deep insights may be drawn from the estimated data about before and after alterations. Due to a

increase in the sales price and advertising costs, the income of the mentioned business will grow

from 689000 to 878681.7. The contributions per unit has been raised from 156350 to 255481.2

as a result of the calculated results, indicating that enhanced sales price and advertising costs are

increased flexibility to align with current conditions.

d)

Particulars Amount

(after advertising)

Amount

(Before

advertising)

Sales 878681.7 689000

Less Variable Costs

Materials 325552.5 278250

Labor 182929.5 156350

Variable overheads 114718.5 98050

Contribution per unit 255481.2 156350

Less Fixed costs:

Production 59000 59000

selling etc. 47600 47600

Profit 148881.2 49750

Deep insights may be drawn from the estimated data about before and after alterations. Due to a

increase in the sales price and advertising costs, the income of the mentioned business will grow

from 689000 to 878681.7. The contributions per unit has been raised from 156350 to 255481.2

as a result of the calculated results, indicating that enhanced sales price and advertising costs are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

advantageous. The key reason for this is that it has permitted the operating cash flow to increase

from 49750 to 148881.2. It's an indication of progress and growth.

e) Explaining the assumptions of break even model and its utilization

The break even model enables a company to determine when it will be capable of

achieving a revenue or loss-free state. It enables an organisation to develop successful planning,

allowing it to achieve the company's specified goals. The break-even approach has a few

drawbacks that must be understood in order to produce a new strategy for identifying and

reducing the gaps (Bui and de Villiers, 2021).

This model is constructed on numerous hypotheses in order to achieve the goal effectively.

The fixed and variable costs are separated in this paradigm. Furthermore, the model assumes that

fixed costs would stay unchanged when output levels rise or fall. However, it has been

discovered that the company's variable cost would change over time as the quantity of products

changes. It is also expected that the pricing of overall strategy would remain constant, which is

not true in today's economic climate. There is a presumption that the sale value of the offered

items would stay unchanged, which is impossible to achieve in the marketplace. The

fundamental explanation being that the company's sales price is determined by market factors

including producers and consumers. Based on this evidence, the break-even model may be

considered to present these types of constraints that might impact the firm's judgment procedure.

There are various more advantages that must be considered in order to improve the

efficiency of the firm's management. One of the major advantages that might help you make

strategic decisions is the capacity to monitor earnings and expenditures just at production stage.

It is commonly used to forecast the impact of productivity and time improvements on revenue so

that appropriate initiatives to sophisticated processing may be implemented. The break even

method is used to assess the connection among fixed and variable, allowing for a more efficient

method to reaching the goals. All of information makes it feasible for a certain firm to estimate

costs, profits, and anticipate selling prices, among other things. They help the organisation

achieve its overall goals by defining applicable business processes and implementing

organizational strategies. On this premise, it may be concluded that organizations are capable of

successful preparation and design, resulting in improved production and better coordination with

stated goals (Tokic, 2020).

from 49750 to 148881.2. It's an indication of progress and growth.

e) Explaining the assumptions of break even model and its utilization

The break even model enables a company to determine when it will be capable of

achieving a revenue or loss-free state. It enables an organisation to develop successful planning,

allowing it to achieve the company's specified goals. The break-even approach has a few

drawbacks that must be understood in order to produce a new strategy for identifying and

reducing the gaps (Bui and de Villiers, 2021).

This model is constructed on numerous hypotheses in order to achieve the goal effectively.

The fixed and variable costs are separated in this paradigm. Furthermore, the model assumes that

fixed costs would stay unchanged when output levels rise or fall. However, it has been

discovered that the company's variable cost would change over time as the quantity of products

changes. It is also expected that the pricing of overall strategy would remain constant, which is

not true in today's economic climate. There is a presumption that the sale value of the offered

items would stay unchanged, which is impossible to achieve in the marketplace. The

fundamental explanation being that the company's sales price is determined by market factors

including producers and consumers. Based on this evidence, the break-even model may be

considered to present these types of constraints that might impact the firm's judgment procedure.

There are various more advantages that must be considered in order to improve the

efficiency of the firm's management. One of the major advantages that might help you make

strategic decisions is the capacity to monitor earnings and expenditures just at production stage.

It is commonly used to forecast the impact of productivity and time improvements on revenue so

that appropriate initiatives to sophisticated processing may be implemented. The break even

method is used to assess the connection among fixed and variable, allowing for a more efficient

method to reaching the goals. All of information makes it feasible for a certain firm to estimate

costs, profits, and anticipate selling prices, among other things. They help the organisation

achieve its overall goals by defining applicable business processes and implementing

organizational strategies. On this premise, it may be concluded that organizations are capable of

successful preparation and design, resulting in improved production and better coordination with

stated goals (Tokic, 2020).

QUESTION 3

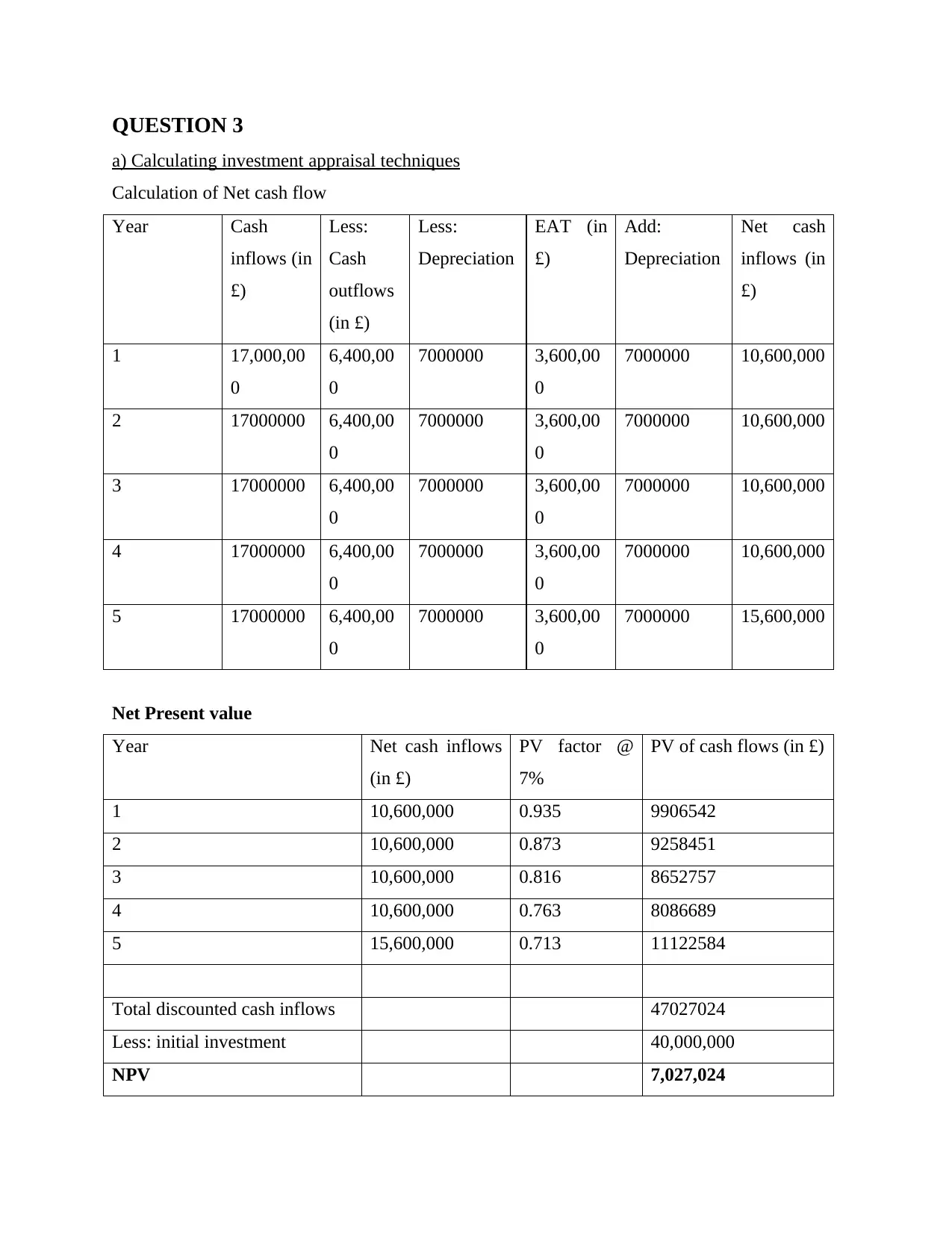

a) Calculating investment appraisal techniques

Calculation of Net cash flow

Year Cash

inflows (in

£)

Less:

Cash

outflows

(in £)

Less:

Depreciation

EAT (in

£)

Add:

Depreciation

Net cash

inflows (in

£)

1 17,000,00

0

6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

2 17000000 6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

3 17000000 6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

4 17000000 6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

5 17000000 6,400,00

0

7000000 3,600,00

0

7000000 15,600,000

Net Present value

Year Net cash inflows

(in £)

PV factor @

7%

PV of cash flows (in £)

1 10,600,000 0.935 9906542

2 10,600,000 0.873 9258451

3 10,600,000 0.816 8652757

4 10,600,000 0.763 8086689

5 15,600,000 0.713 11122584

Total discounted cash inflows 47027024

Less: initial investment 40,000,000

NPV 7,027,024

a) Calculating investment appraisal techniques

Calculation of Net cash flow

Year Cash

inflows (in

£)

Less:

Cash

outflows

(in £)

Less:

Depreciation

EAT (in

£)

Add:

Depreciation

Net cash

inflows (in

£)

1 17,000,00

0

6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

2 17000000 6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

3 17000000 6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

4 17000000 6,400,00

0

7000000 3,600,00

0

7000000 10,600,000

5 17000000 6,400,00

0

7000000 3,600,00

0

7000000 15,600,000

Net Present value

Year Net cash inflows

(in £)

PV factor @

7%

PV of cash flows (in £)

1 10,600,000 0.935 9906542

2 10,600,000 0.873 9258451

3 10,600,000 0.816 8652757

4 10,600,000 0.763 8086689

5 15,600,000 0.713 11122584

Total discounted cash inflows 47027024

Less: initial investment 40,000,000

NPV 7,027,024

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.