Investment Appraisal, Long-Term Finance, and CVP Analysis for S Plc

VerifiedAdded on 2023/06/18

|17

|4210

|490

Report

AI Summary

This business report provides a detailed analysis of investment appraisal techniques, cost-volume-profit (CVP) analysis, long-term finance options, and strategic sourcing for S Plc, a computer game company. It assesses the importance of capital investment appraisal, prepares a cash flow analysis, defines the payback period, determines the net present value (NPV), and calculates the internal rate of return (IRR) for a new product line. The report critically contrasts bank loans with equity issues for long-term financing, computes break-even point (BEP), revenue at desired profit, and margin of safety. It also differentiates strategic, preferred, and transactional suppliers, compares single and multiple sourcing benefits, and explains cross-sourcing with examples. The analysis uses financial data to provide recommendations for S Plc's financial and operational strategies, offering a comprehensive overview of key business decisions. Desklib provides access to solved assignments and resources for students.

Business Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

A......................................................................................................................................................4

1. Assessing the importance of capital investment appraisal in the context of S plc..................4

2. Preparing a cash flow analysis statement for the concerned investment proposal..................4

3. Defining payback period for the new investment....................................................................5

4. Determining the net present value for the new investment.....................................................6

5. Describing net present value approach and its association with cost of capital......................7

6. Calculating internal rate of return and assessing how cost of capital affect IRR....................7

8. Stating why NPV method is better over IRR...........................................................................8

B.......................................................................................................................................................8

Critically contrast bank loan with equity issue in the context of meeting long-term finance

requirements................................................................................................................................8

C.......................................................................................................................................................9

1) Computing BEP, revenue at desired profit and margin of safety............................................9

2) Assessing the consequences when price increase or decrease by 10%.................................10

3. Critically explaining the assumptions of Cost-volume-profit analysis..................................11

D....................................................................................................................................................12

1) Differentiating strategic, preferred and transactional suppliers...........................................12

2) Comparing the benefits of single and multiple sourcing with regards to procurement........13

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

A......................................................................................................................................................4

1. Assessing the importance of capital investment appraisal in the context of S plc..................4

2. Preparing a cash flow analysis statement for the concerned investment proposal..................4

3. Defining payback period for the new investment....................................................................5

4. Determining the net present value for the new investment.....................................................6

5. Describing net present value approach and its association with cost of capital......................7

6. Calculating internal rate of return and assessing how cost of capital affect IRR....................7

8. Stating why NPV method is better over IRR...........................................................................8

B.......................................................................................................................................................8

Critically contrast bank loan with equity issue in the context of meeting long-term finance

requirements................................................................................................................................8

C.......................................................................................................................................................9

1) Computing BEP, revenue at desired profit and margin of safety............................................9

2) Assessing the consequences when price increase or decrease by 10%.................................10

3. Critically explaining the assumptions of Cost-volume-profit analysis..................................11

D....................................................................................................................................................12

1) Differentiating strategic, preferred and transactional suppliers...........................................12

2) Comparing the benefits of single and multiple sourcing with regards to procurement........13

3) Explaining cross-sourcing along with its benefits the buyer ad example.............................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial decision making may be defined as a process of selecting best alternative out of

various options available to business unit. In modern era, it is an accountability of manager of

take appropriate decision about financial, investment and operating aspects by evaluating all the

related factors. Moreover, financial growth and success highly depends on the extent to which

firm makes optimum use of monetary resources. The present is report based on case scenario of

S Plc which deals in computer game. Now, for increasing revenue and profit business unit is

planning to add new line of product in the existing range. In this, report will provide deeper

insight about the manner in which investment appraisal techniques can be used for decision

making. Along with this, report will develop understanding about the concept of CVP and its

contribution in business decisions. Further, it entails sources of finance which S Plc can use for

meeting long term financial requirements. Report also highlights different types of suppliers and

sources which used by organization for procurement purpose.

TASK

A

1. Assessing the importance of capital investment appraisal in the context of S plc

Capital budgeting tools mainly include payback, net present value, average and internal

rate of return which helps in appraising the performance of new project. In the context of S Plc,

investment appraisal techniques are highly significant as it helps in evaluating proposed

investment from different perspectives (Importance of Investment Appraisal, 2021). Along with

this, through applying investment appraisal techniques management team of S Plc can assess

financial feasibility of projects using projected cash flows. Further, it provides assistance in

determining the extent to which available resources make project feasible (Idehen, 2021). By

using tools firm can evaluate which falls under the category of uncertainty such as inflation,

regulatory aspects etc. In this way, capital budgeting tools contribute in project selection for

investment purpose and thereby contributes in organizational success.

Financial decision making may be defined as a process of selecting best alternative out of

various options available to business unit. In modern era, it is an accountability of manager of

take appropriate decision about financial, investment and operating aspects by evaluating all the

related factors. Moreover, financial growth and success highly depends on the extent to which

firm makes optimum use of monetary resources. The present is report based on case scenario of

S Plc which deals in computer game. Now, for increasing revenue and profit business unit is

planning to add new line of product in the existing range. In this, report will provide deeper

insight about the manner in which investment appraisal techniques can be used for decision

making. Along with this, report will develop understanding about the concept of CVP and its

contribution in business decisions. Further, it entails sources of finance which S Plc can use for

meeting long term financial requirements. Report also highlights different types of suppliers and

sources which used by organization for procurement purpose.

TASK

A

1. Assessing the importance of capital investment appraisal in the context of S plc

Capital budgeting tools mainly include payback, net present value, average and internal

rate of return which helps in appraising the performance of new project. In the context of S Plc,

investment appraisal techniques are highly significant as it helps in evaluating proposed

investment from different perspectives (Importance of Investment Appraisal, 2021). Along with

this, through applying investment appraisal techniques management team of S Plc can assess

financial feasibility of projects using projected cash flows. Further, it provides assistance in

determining the extent to which available resources make project feasible (Idehen, 2021). By

using tools firm can evaluate which falls under the category of uncertainty such as inflation,

regulatory aspects etc. In this way, capital budgeting tools contribute in project selection for

investment purpose and thereby contributes in organizational success.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

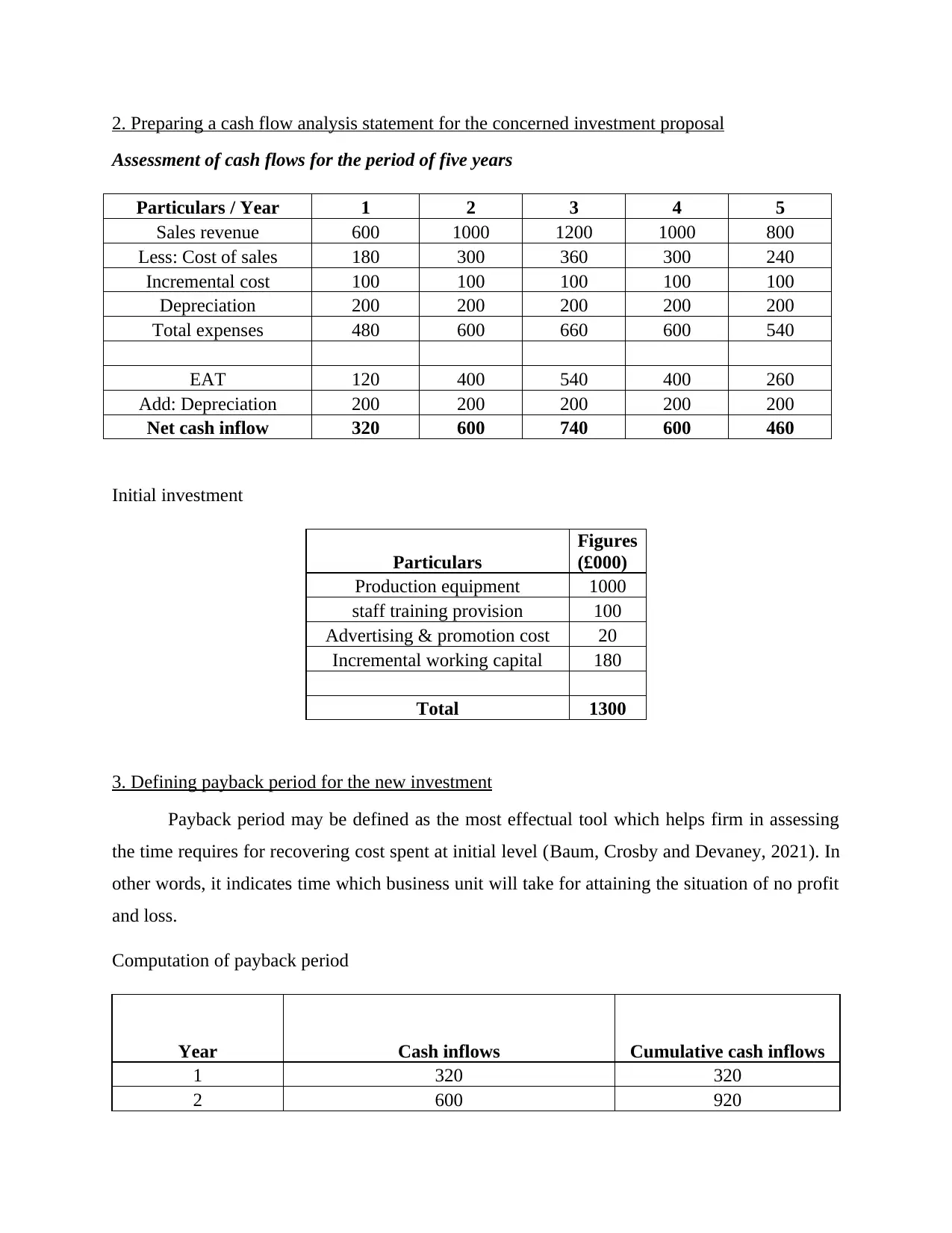

2. Preparing a cash flow analysis statement for the concerned investment proposal

Assessment of cash flows for the period of five years

Particulars / Year 1 2 3 4 5

Sales revenue 600 1000 1200 1000 800

Less: Cost of sales 180 300 360 300 240

Incremental cost 100 100 100 100 100

Depreciation 200 200 200 200 200

Total expenses 480 600 660 600 540

EAT 120 400 540 400 260

Add: Depreciation 200 200 200 200 200

Net cash inflow 320 600 740 600 460

Initial investment

Particulars

Figures

(£000)

Production equipment 1000

staff training provision 100

Advertising & promotion cost 20

Incremental working capital 180

Total 1300

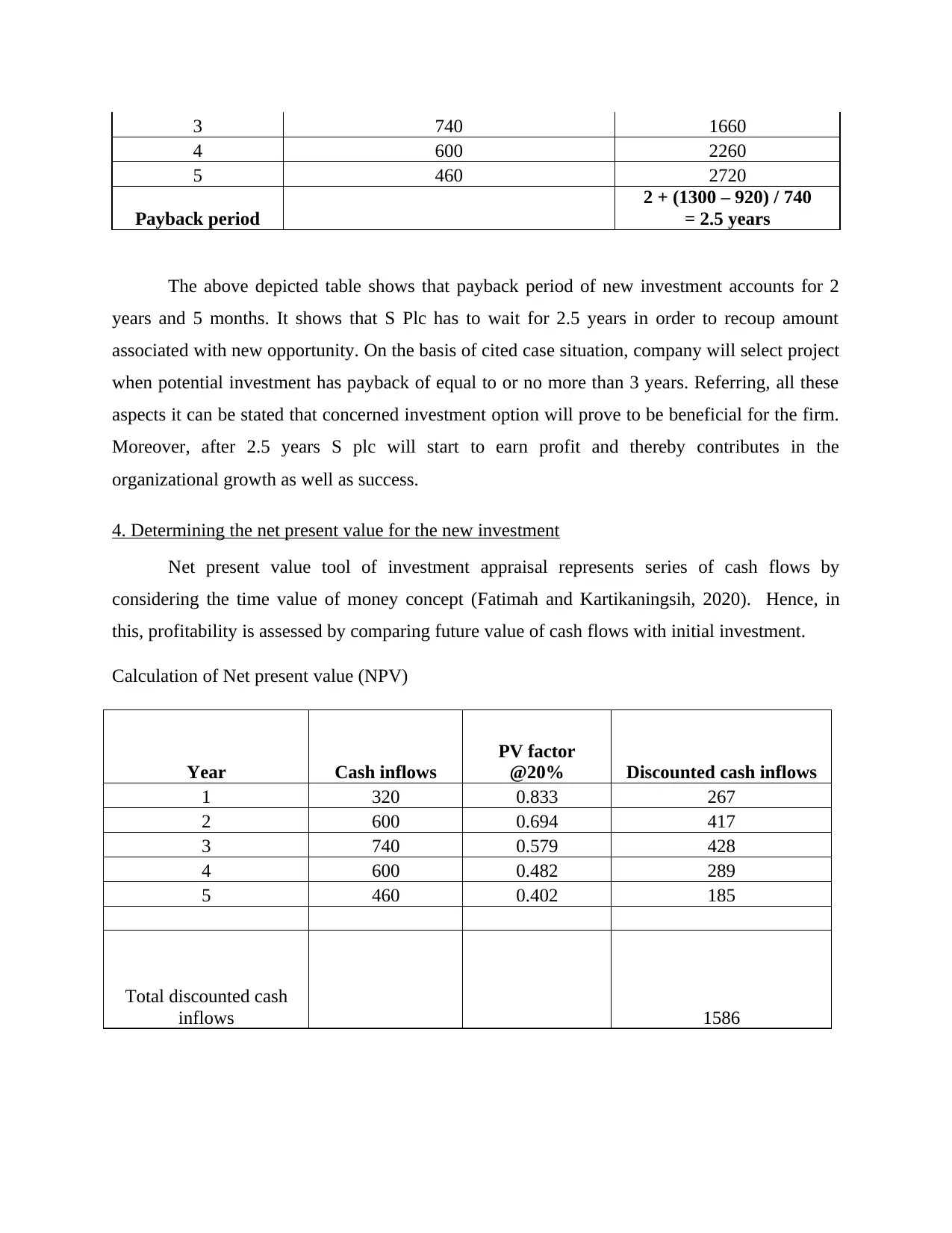

3. Defining payback period for the new investment

Payback period may be defined as the most effectual tool which helps firm in assessing

the time requires for recovering cost spent at initial level (Baum, Crosby and Devaney, 2021). In

other words, it indicates time which business unit will take for attaining the situation of no profit

and loss.

Computation of payback period

Year Cash inflows Cumulative cash inflows

1 320 320

2 600 920

Assessment of cash flows for the period of five years

Particulars / Year 1 2 3 4 5

Sales revenue 600 1000 1200 1000 800

Less: Cost of sales 180 300 360 300 240

Incremental cost 100 100 100 100 100

Depreciation 200 200 200 200 200

Total expenses 480 600 660 600 540

EAT 120 400 540 400 260

Add: Depreciation 200 200 200 200 200

Net cash inflow 320 600 740 600 460

Initial investment

Particulars

Figures

(£000)

Production equipment 1000

staff training provision 100

Advertising & promotion cost 20

Incremental working capital 180

Total 1300

3. Defining payback period for the new investment

Payback period may be defined as the most effectual tool which helps firm in assessing

the time requires for recovering cost spent at initial level (Baum, Crosby and Devaney, 2021). In

other words, it indicates time which business unit will take for attaining the situation of no profit

and loss.

Computation of payback period

Year Cash inflows Cumulative cash inflows

1 320 320

2 600 920

3 740 1660

4 600 2260

5 460 2720

Payback period

2 + (1300 – 920) / 740

= 2.5 years

The above depicted table shows that payback period of new investment accounts for 2

years and 5 months. It shows that S Plc has to wait for 2.5 years in order to recoup amount

associated with new opportunity. On the basis of cited case situation, company will select project

when potential investment has payback of equal to or no more than 3 years. Referring, all these

aspects it can be stated that concerned investment option will prove to be beneficial for the firm.

Moreover, after 2.5 years S plc will start to earn profit and thereby contributes in the

organizational growth as well as success.

4. Determining the net present value for the new investment

Net present value tool of investment appraisal represents series of cash flows by

considering the time value of money concept (Fatimah and Kartikaningsih, 2020). Hence, in

this, profitability is assessed by comparing future value of cash flows with initial investment.

Calculation of Net present value (NPV)

Year Cash inflows

PV factor

@20% Discounted cash inflows

1 320 0.833 267

2 600 0.694 417

3 740 0.579 428

4 600 0.482 289

5 460 0.402 185

Total discounted cash

inflows 1586

4 600 2260

5 460 2720

Payback period

2 + (1300 – 920) / 740

= 2.5 years

The above depicted table shows that payback period of new investment accounts for 2

years and 5 months. It shows that S Plc has to wait for 2.5 years in order to recoup amount

associated with new opportunity. On the basis of cited case situation, company will select project

when potential investment has payback of equal to or no more than 3 years. Referring, all these

aspects it can be stated that concerned investment option will prove to be beneficial for the firm.

Moreover, after 2.5 years S plc will start to earn profit and thereby contributes in the

organizational growth as well as success.

4. Determining the net present value for the new investment

Net present value tool of investment appraisal represents series of cash flows by

considering the time value of money concept (Fatimah and Kartikaningsih, 2020). Hence, in

this, profitability is assessed by comparing future value of cash flows with initial investment.

Calculation of Net present value (NPV)

Year Cash inflows

PV factor

@20% Discounted cash inflows

1 320 0.833 267

2 600 0.694 417

3 740 0.579 428

4 600 0.482 289

5 460 0.402 185

Total discounted cash

inflows 1586

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

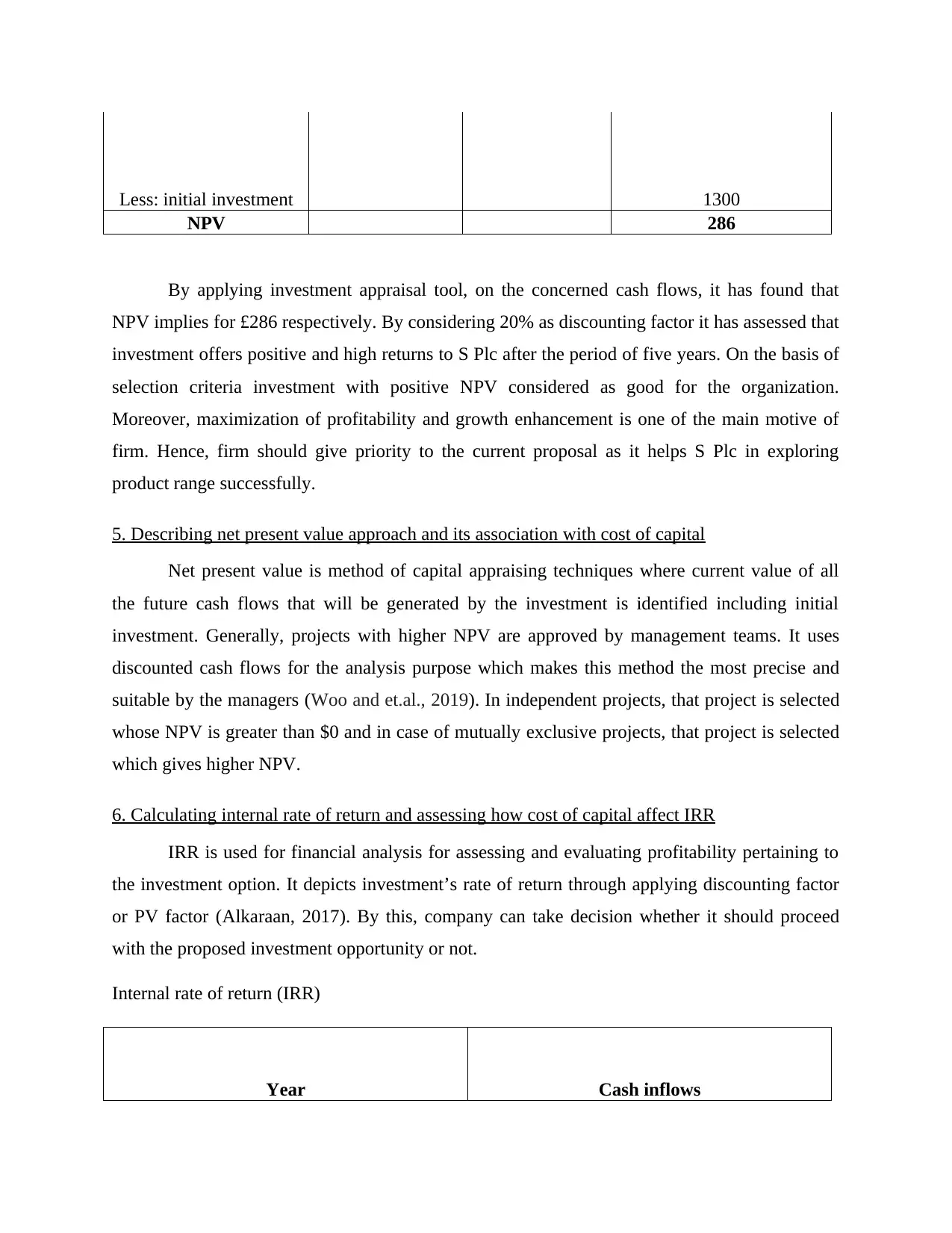

Less: initial investment 1300

NPV 286

By applying investment appraisal tool, on the concerned cash flows, it has found that

NPV implies for £286 respectively. By considering 20% as discounting factor it has assessed that

investment offers positive and high returns to S Plc after the period of five years. On the basis of

selection criteria investment with positive NPV considered as good for the organization.

Moreover, maximization of profitability and growth enhancement is one of the main motive of

firm. Hence, firm should give priority to the current proposal as it helps S Plc in exploring

product range successfully.

5. Describing net present value approach and its association with cost of capital

Net present value is method of capital appraising techniques where current value of all

the future cash flows that will be generated by the investment is identified including initial

investment. Generally, projects with higher NPV are approved by management teams. It uses

discounted cash flows for the analysis purpose which makes this method the most precise and

suitable by the managers (Woo and et.al., 2019). In independent projects, that project is selected

whose NPV is greater than $0 and in case of mutually exclusive projects, that project is selected

which gives higher NPV.

6. Calculating internal rate of return and assessing how cost of capital affect IRR

IRR is used for financial analysis for assessing and evaluating profitability pertaining to

the investment option. It depicts investment’s rate of return through applying discounting factor

or PV factor (Alkaraan, 2017). By this, company can take decision whether it should proceed

with the proposed investment opportunity or not.

Internal rate of return (IRR)

Year Cash inflows

NPV 286

By applying investment appraisal tool, on the concerned cash flows, it has found that

NPV implies for £286 respectively. By considering 20% as discounting factor it has assessed that

investment offers positive and high returns to S Plc after the period of five years. On the basis of

selection criteria investment with positive NPV considered as good for the organization.

Moreover, maximization of profitability and growth enhancement is one of the main motive of

firm. Hence, firm should give priority to the current proposal as it helps S Plc in exploring

product range successfully.

5. Describing net present value approach and its association with cost of capital

Net present value is method of capital appraising techniques where current value of all

the future cash flows that will be generated by the investment is identified including initial

investment. Generally, projects with higher NPV are approved by management teams. It uses

discounted cash flows for the analysis purpose which makes this method the most precise and

suitable by the managers (Woo and et.al., 2019). In independent projects, that project is selected

whose NPV is greater than $0 and in case of mutually exclusive projects, that project is selected

which gives higher NPV.

6. Calculating internal rate of return and assessing how cost of capital affect IRR

IRR is used for financial analysis for assessing and evaluating profitability pertaining to

the investment option. It depicts investment’s rate of return through applying discounting factor

or PV factor (Alkaraan, 2017). By this, company can take decision whether it should proceed

with the proposed investment opportunity or not.

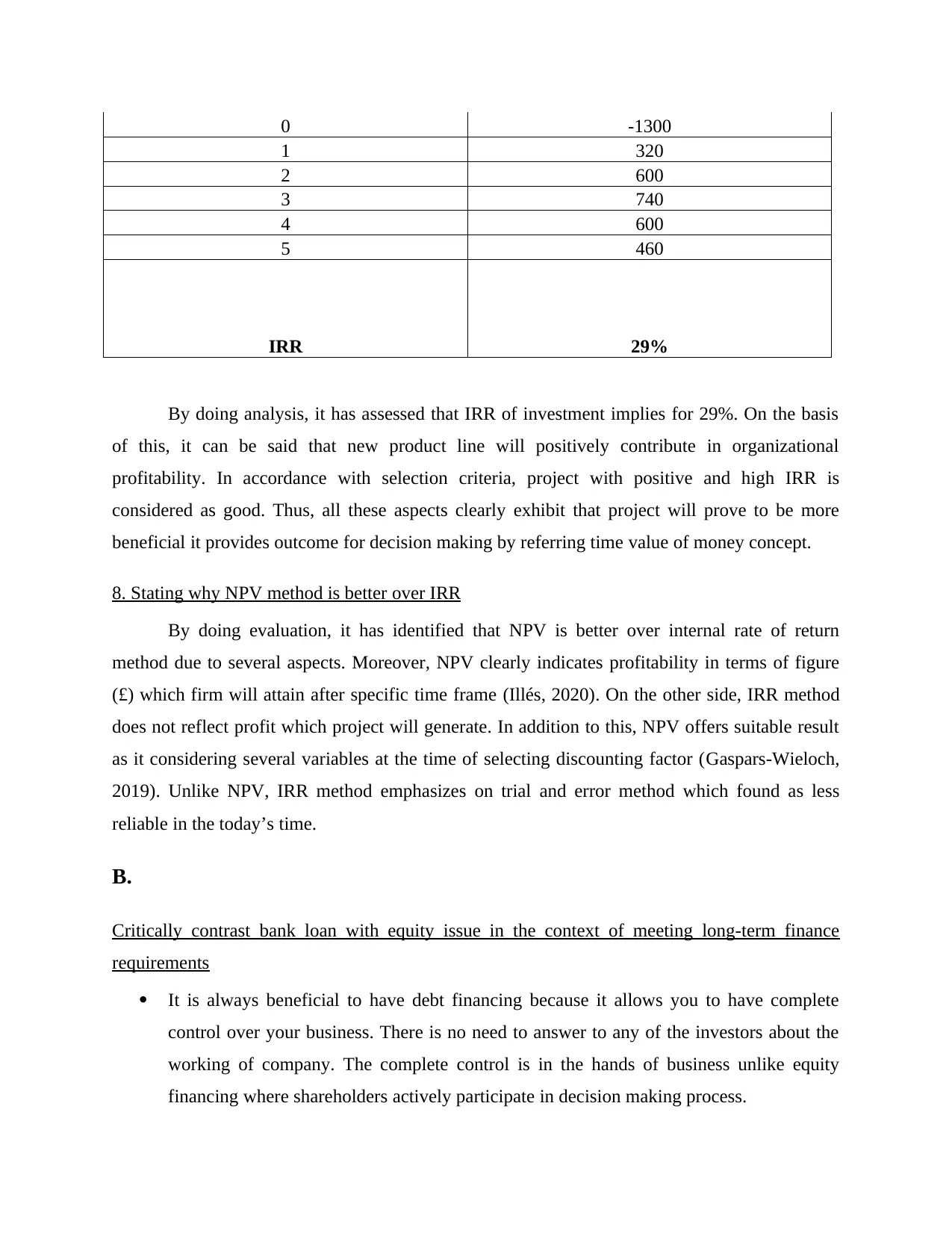

Internal rate of return (IRR)

Year Cash inflows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0 -1300

1 320

2 600

3 740

4 600

5 460

IRR 29%

By doing analysis, it has assessed that IRR of investment implies for 29%. On the basis

of this, it can be said that new product line will positively contribute in organizational

profitability. In accordance with selection criteria, project with positive and high IRR is

considered as good. Thus, all these aspects clearly exhibit that project will prove to be more

beneficial it provides outcome for decision making by referring time value of money concept.

8. Stating why NPV method is better over IRR

By doing evaluation, it has identified that NPV is better over internal rate of return

method due to several aspects. Moreover, NPV clearly indicates profitability in terms of figure

(£) which firm will attain after specific time frame (Illés, 2020). On the other side, IRR method

does not reflect profit which project will generate. In addition to this, NPV offers suitable result

as it considering several variables at the time of selecting discounting factor (Gaspars-Wieloch,

2019). Unlike NPV, IRR method emphasizes on trial and error method which found as less

reliable in the today’s time.

B.

Critically contrast bank loan with equity issue in the context of meeting long-term finance

requirements

It is always beneficial to have debt financing because it allows you to have complete

control over your business. There is no need to answer to any of the investors about the

working of company. The complete control is in the hands of business unlike equity

financing where shareholders actively participate in decision making process.

1 320

2 600

3 740

4 600

5 460

IRR 29%

By doing analysis, it has assessed that IRR of investment implies for 29%. On the basis

of this, it can be said that new product line will positively contribute in organizational

profitability. In accordance with selection criteria, project with positive and high IRR is

considered as good. Thus, all these aspects clearly exhibit that project will prove to be more

beneficial it provides outcome for decision making by referring time value of money concept.

8. Stating why NPV method is better over IRR

By doing evaluation, it has identified that NPV is better over internal rate of return

method due to several aspects. Moreover, NPV clearly indicates profitability in terms of figure

(£) which firm will attain after specific time frame (Illés, 2020). On the other side, IRR method

does not reflect profit which project will generate. In addition to this, NPV offers suitable result

as it considering several variables at the time of selecting discounting factor (Gaspars-Wieloch,

2019). Unlike NPV, IRR method emphasizes on trial and error method which found as less

reliable in the today’s time.

B.

Critically contrast bank loan with equity issue in the context of meeting long-term finance

requirements

It is always beneficial to have debt financing because it allows you to have complete

control over your business. There is no need to answer to any of the investors about the

working of company. The complete control is in the hands of business unlike equity

financing where shareholders actively participate in decision making process.

In taking loans from banks, interest fee and other charges are tax deductible which a

bigger incentive of debt financing. There are no such deductions in case of equity

financing (Ning and Babich, 2018).

There is no need to share the retained profits of business and the only obligation towards

loan payment is of the instalment payments at the agreed time frame. When company

adopts equity financing, it has to pay dividends from profits which reduces the

profitability of company.

However, it is very difficult for a new company to have access to bank loan because there

are a lot of formalities that needs to be done before bank sanctions a loan.

Moreover, company needs to make sure that it generates enough revenue so that it is able

to make repayments on time to the bank. In case of non-payment of dues, company may

have to face serious issues. Failure to make payments on time can also affect negatively

organization’s credit rating.

On the other hand, equity financing places no obligation on regular payments, that is, no

financial burden on company. Therefore, company is left with more funds to invest in

proper manner so that it can expand further.

It is cheap to get loan from bank in case if company expands in future, it is easy to exit

the debt and expand efficiently. But, with shareholder’s fund, company needs to make a

lot of formalities and permissions before expanding further.

Lot of formalities are required in case of equity financing which is not there in raising

loan from bank. Raising money from venture capitalist involves lot of meetings and is

lengthy and complicated process. It is easy and simple process to get a loan from bank.

In debt financing, principal and interest payment is known in advance. So, it becomes

possible for company to plan well in advance and prepare budgets (Aziz and Abbas,

2019).

There is a potential risk in taking loans from banks because banks ask company to keep

collateral. Business entity keeps financial or tangible assets with the banks, thereby

potentially putting the assets at risk.

bigger incentive of debt financing. There are no such deductions in case of equity

financing (Ning and Babich, 2018).

There is no need to share the retained profits of business and the only obligation towards

loan payment is of the instalment payments at the agreed time frame. When company

adopts equity financing, it has to pay dividends from profits which reduces the

profitability of company.

However, it is very difficult for a new company to have access to bank loan because there

are a lot of formalities that needs to be done before bank sanctions a loan.

Moreover, company needs to make sure that it generates enough revenue so that it is able

to make repayments on time to the bank. In case of non-payment of dues, company may

have to face serious issues. Failure to make payments on time can also affect negatively

organization’s credit rating.

On the other hand, equity financing places no obligation on regular payments, that is, no

financial burden on company. Therefore, company is left with more funds to invest in

proper manner so that it can expand further.

It is cheap to get loan from bank in case if company expands in future, it is easy to exit

the debt and expand efficiently. But, with shareholder’s fund, company needs to make a

lot of formalities and permissions before expanding further.

Lot of formalities are required in case of equity financing which is not there in raising

loan from bank. Raising money from venture capitalist involves lot of meetings and is

lengthy and complicated process. It is easy and simple process to get a loan from bank.

In debt financing, principal and interest payment is known in advance. So, it becomes

possible for company to plan well in advance and prepare budgets (Aziz and Abbas,

2019).

There is a potential risk in taking loans from banks because banks ask company to keep

collateral. Business entity keeps financial or tangible assets with the banks, thereby

potentially putting the assets at risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

C

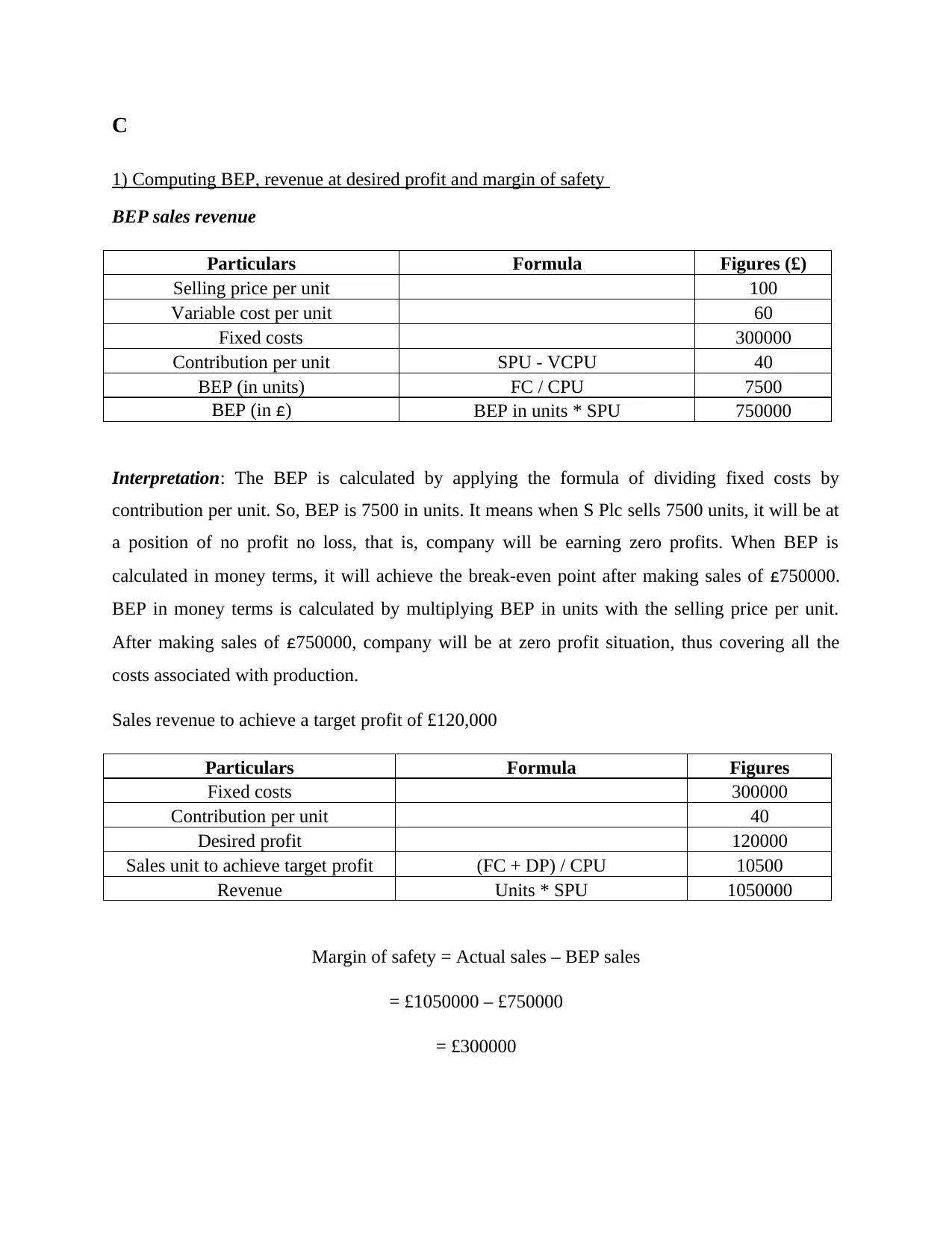

1) Computing BEP, revenue at desired profit and margin of safety

BEP sales revenue

Particulars Formula Figures (£)

Selling price per unit 100

Variable cost per unit 60

Fixed costs 300000

Contribution per unit SPU - VCPU 40

BEP (in units) FC / CPU 7500

BEP (in £) BEP in units * SPU 750000

Interpretation: The BEP is calculated by applying the formula of dividing fixed costs by

contribution per unit. So, BEP is 7500 in units. It means when S Plc sells 7500 units, it will be at

a position of no profit no loss, that is, company will be earning zero profits. When BEP is

calculated in money terms, it will achieve the break-even point after making sales of £750000.

BEP in money terms is calculated by multiplying BEP in units with the selling price per unit.

After making sales of £750000, company will be at zero profit situation, thus covering all the

costs associated with production.

Sales revenue to achieve a target profit of £120,000

Particulars Formula Figures

Fixed costs 300000

Contribution per unit 40

Desired profit 120000

Sales unit to achieve target profit (FC + DP) / CPU 10500

Revenue Units * SPU 1050000

Margin of safety = Actual sales – BEP sales

= £1050000 – £750000

= £300000

1) Computing BEP, revenue at desired profit and margin of safety

BEP sales revenue

Particulars Formula Figures (£)

Selling price per unit 100

Variable cost per unit 60

Fixed costs 300000

Contribution per unit SPU - VCPU 40

BEP (in units) FC / CPU 7500

BEP (in £) BEP in units * SPU 750000

Interpretation: The BEP is calculated by applying the formula of dividing fixed costs by

contribution per unit. So, BEP is 7500 in units. It means when S Plc sells 7500 units, it will be at

a position of no profit no loss, that is, company will be earning zero profits. When BEP is

calculated in money terms, it will achieve the break-even point after making sales of £750000.

BEP in money terms is calculated by multiplying BEP in units with the selling price per unit.

After making sales of £750000, company will be at zero profit situation, thus covering all the

costs associated with production.

Sales revenue to achieve a target profit of £120,000

Particulars Formula Figures

Fixed costs 300000

Contribution per unit 40

Desired profit 120000

Sales unit to achieve target profit (FC + DP) / CPU 10500

Revenue Units * SPU 1050000

Margin of safety = Actual sales – BEP sales

= £1050000 – £750000

= £300000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

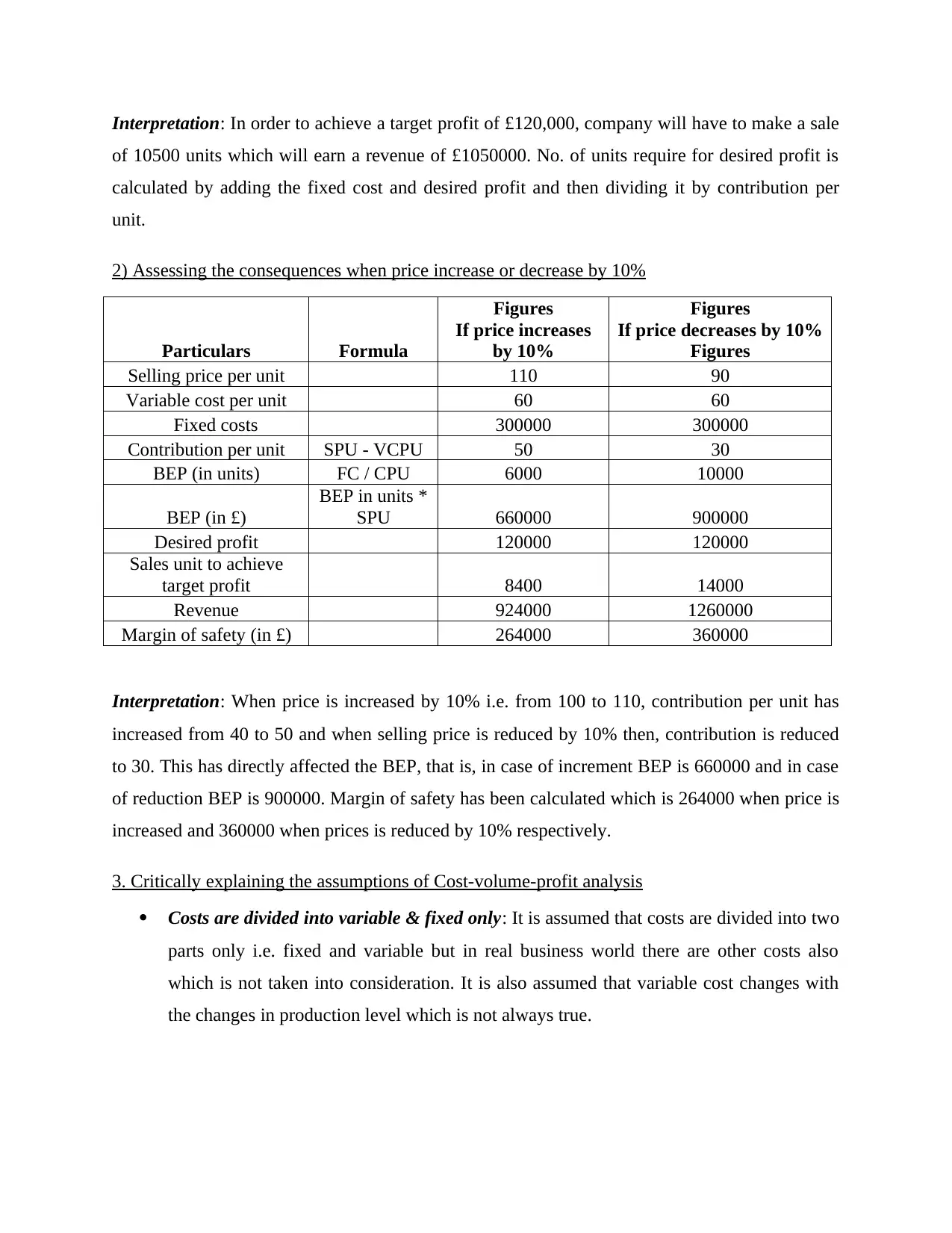

Interpretation: In order to achieve a target profit of £120,000, company will have to make a sale

of 10500 units which will earn a revenue of £1050000. No. of units require for desired profit is

calculated by adding the fixed cost and desired profit and then dividing it by contribution per

unit.

2) Assessing the consequences when price increase or decrease by 10%

Particulars Formula

Figures

If price increases

by 10%

Figures

If price decreases by 10%

Figures

Selling price per unit 110 90

Variable cost per unit 60 60

Fixed costs 300000 300000

Contribution per unit SPU - VCPU 50 30

BEP (in units) FC / CPU 6000 10000

BEP (in £)

BEP in units *

SPU 660000 900000

Desired profit 120000 120000

Sales unit to achieve

target profit 8400 14000

Revenue 924000 1260000

Margin of safety (in £) 264000 360000

Interpretation: When price is increased by 10% i.e. from 100 to 110, contribution per unit has

increased from 40 to 50 and when selling price is reduced by 10% then, contribution is reduced

to 30. This has directly affected the BEP, that is, in case of increment BEP is 660000 and in case

of reduction BEP is 900000. Margin of safety has been calculated which is 264000 when price is

increased and 360000 when prices is reduced by 10% respectively.

3. Critically explaining the assumptions of Cost-volume-profit analysis

Costs are divided into variable & fixed only: It is assumed that costs are divided into two

parts only i.e. fixed and variable but in real business world there are other costs also

which is not taken into consideration. It is also assumed that variable cost changes with

the changes in production level which is not always true.

of 10500 units which will earn a revenue of £1050000. No. of units require for desired profit is

calculated by adding the fixed cost and desired profit and then dividing it by contribution per

unit.

2) Assessing the consequences when price increase or decrease by 10%

Particulars Formula

Figures

If price increases

by 10%

Figures

If price decreases by 10%

Figures

Selling price per unit 110 90

Variable cost per unit 60 60

Fixed costs 300000 300000

Contribution per unit SPU - VCPU 50 30

BEP (in units) FC / CPU 6000 10000

BEP (in £)

BEP in units *

SPU 660000 900000

Desired profit 120000 120000

Sales unit to achieve

target profit 8400 14000

Revenue 924000 1260000

Margin of safety (in £) 264000 360000

Interpretation: When price is increased by 10% i.e. from 100 to 110, contribution per unit has

increased from 40 to 50 and when selling price is reduced by 10% then, contribution is reduced

to 30. This has directly affected the BEP, that is, in case of increment BEP is 660000 and in case

of reduction BEP is 900000. Margin of safety has been calculated which is 264000 when price is

increased and 360000 when prices is reduced by 10% respectively.

3. Critically explaining the assumptions of Cost-volume-profit analysis

Costs are divided into variable & fixed only: It is assumed that costs are divided into two

parts only i.e. fixed and variable but in real business world there are other costs also

which is not taken into consideration. It is also assumed that variable cost changes with

the changes in production level which is not always true.

Relationship between Cost and revenue: Another assumption of CVP analysis is that

there is linear relationship between cost and revenue (Lulaj and Iseni, 2018). It is

assumed that there is one relevant range between cost (fixed and variable) and revenue.

Inventory does not change: CVP analysis is based on assumption that there is no

inventory left at the end of a particular year which means all that is produced is sold

within that year. This does not hold true because it is not necessary that whatever is

produced is sold with that year.

Selling price remains constant: Selling price does not change throughout the life of the

product which is not true because in competitive world, it is not possible to sustain one

price for longer time. Due to tough competition in market, companies are bound to

change their selling price from time to time.

D

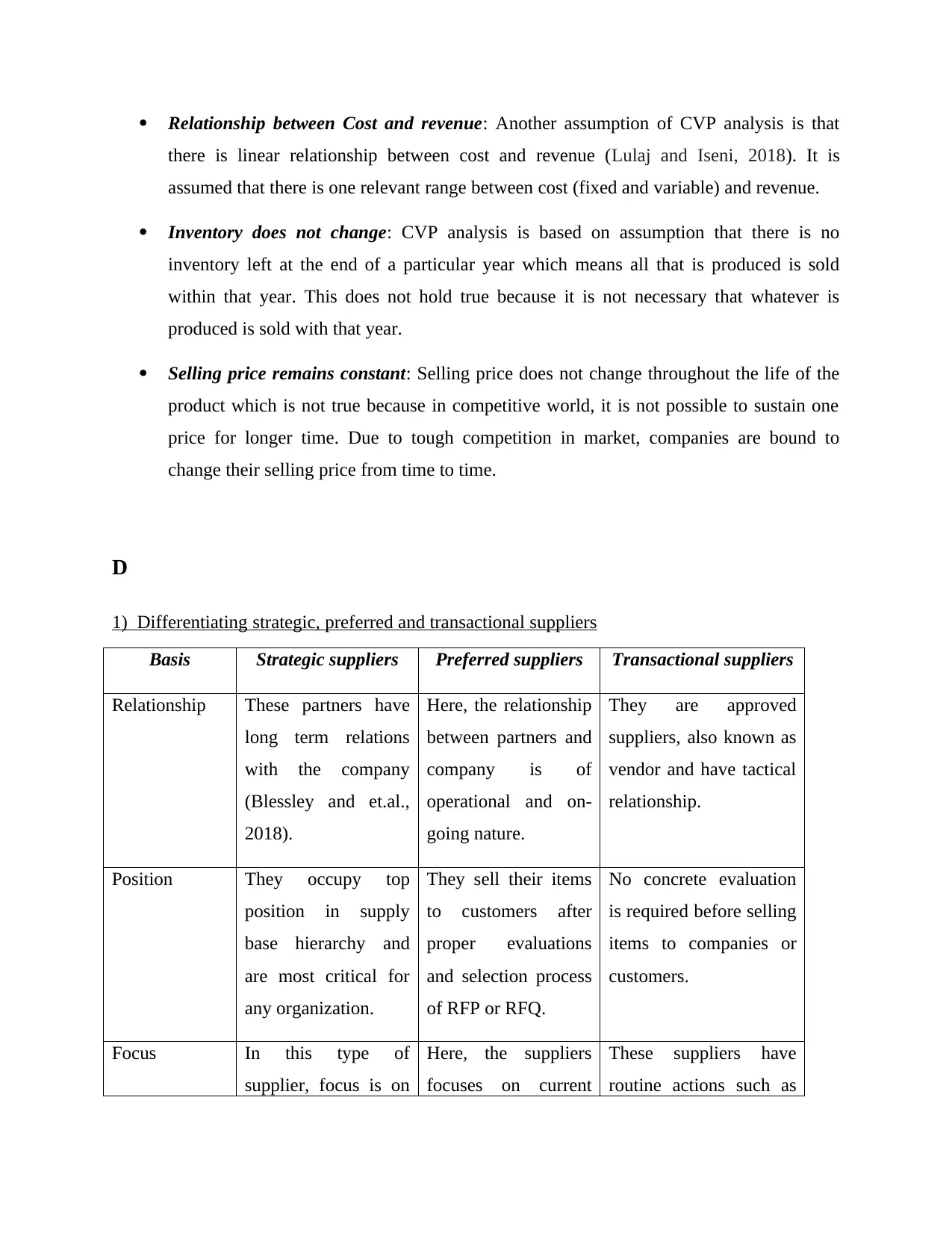

1) Differentiating strategic, preferred and transactional suppliers

Basis Strategic suppliers Preferred suppliers Transactional suppliers

Relationship These partners have

long term relations

with the company

(Blessley and et.al.,

2018).

Here, the relationship

between partners and

company is of

operational and on-

going nature.

They are approved

suppliers, also known as

vendor and have tactical

relationship.

Position They occupy top

position in supply

base hierarchy and

are most critical for

any organization.

They sell their items

to customers after

proper evaluations

and selection process

of RFP or RFQ.

No concrete evaluation

is required before selling

items to companies or

customers.

Focus In this type of

supplier, focus is on

Here, the suppliers

focuses on current

These suppliers have

routine actions such as

there is linear relationship between cost and revenue (Lulaj and Iseni, 2018). It is

assumed that there is one relevant range between cost (fixed and variable) and revenue.

Inventory does not change: CVP analysis is based on assumption that there is no

inventory left at the end of a particular year which means all that is produced is sold

within that year. This does not hold true because it is not necessary that whatever is

produced is sold with that year.

Selling price remains constant: Selling price does not change throughout the life of the

product which is not true because in competitive world, it is not possible to sustain one

price for longer time. Due to tough competition in market, companies are bound to

change their selling price from time to time.

D

1) Differentiating strategic, preferred and transactional suppliers

Basis Strategic suppliers Preferred suppliers Transactional suppliers

Relationship These partners have

long term relations

with the company

(Blessley and et.al.,

2018).

Here, the relationship

between partners and

company is of

operational and on-

going nature.

They are approved

suppliers, also known as

vendor and have tactical

relationship.

Position They occupy top

position in supply

base hierarchy and

are most critical for

any organization.

They sell their items

to customers after

proper evaluations

and selection process

of RFP or RFQ.

No concrete evaluation

is required before selling

items to companies or

customers.

Focus In this type of

supplier, focus is on

Here, the suppliers

focuses on current

These suppliers have

routine actions such as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.