Financial Management: Investment Appraisal and Valuation Methods

VerifiedAdded on 2023/06/18

|15

|3884

|413

Report

AI Summary

This report provides a comprehensive analysis of capital appraisal techniques and valuation methods in financial management. It evaluates the economic feasibility of acquiring machinery using methods such as payback period, accounting rate of return, net present value, and internal rate of return, recommending the adoption of the machine based on positive cash inflows and economic benefits. The report also assesses the effects of capital structuring proposals, particularly repurchasing equity versus paying cash dividends, using the net operating income approach. Furthermore, it discusses the benefits and drawbacks of investment appraisal techniques like net present value, payback period, IRR, and accounting rate of return, highlighting their strengths and limitations in decision-making. Finally, the report examines valuation methods, including the price/earning ratio, discounted cash flow method, and dividend valuation method, critically discussing their issues and applications in valuing stocks and making investment decisions. Desklib offers a wealth of similar resources for students seeking to enhance their understanding of financial management concepts.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 2 ..................................................................................................................................1

a) calculating capital appraisal techniques and providing recommendation for economic

feasibility for acquiring machine ...........................................................................................1

b) Evaluating the effects of proposal on company................................................................4

Explaining benefits & drawbacks of investment appraisal techniques..................................5

QUESTION 3...................................................................................................................................6

a) Price/earning ratio..............................................................................................................6

b) Discounted Cash Flow method .........................................................................................7

c) Dividend valuation method ...............................................................................................8

d) Critically discussing the issues concerned with mentioned valuation methods................9

REFERENCES..............................................................................................................................13

QUESTION 2 ..................................................................................................................................1

a) calculating capital appraisal techniques and providing recommendation for economic

feasibility for acquiring machine ...........................................................................................1

b) Evaluating the effects of proposal on company................................................................4

Explaining benefits & drawbacks of investment appraisal techniques..................................5

QUESTION 3...................................................................................................................................6

a) Price/earning ratio..............................................................................................................6

b) Discounted Cash Flow method .........................................................................................7

c) Dividend valuation method ...............................................................................................8

d) Critically discussing the issues concerned with mentioned valuation methods................9

REFERENCES..............................................................................................................................13

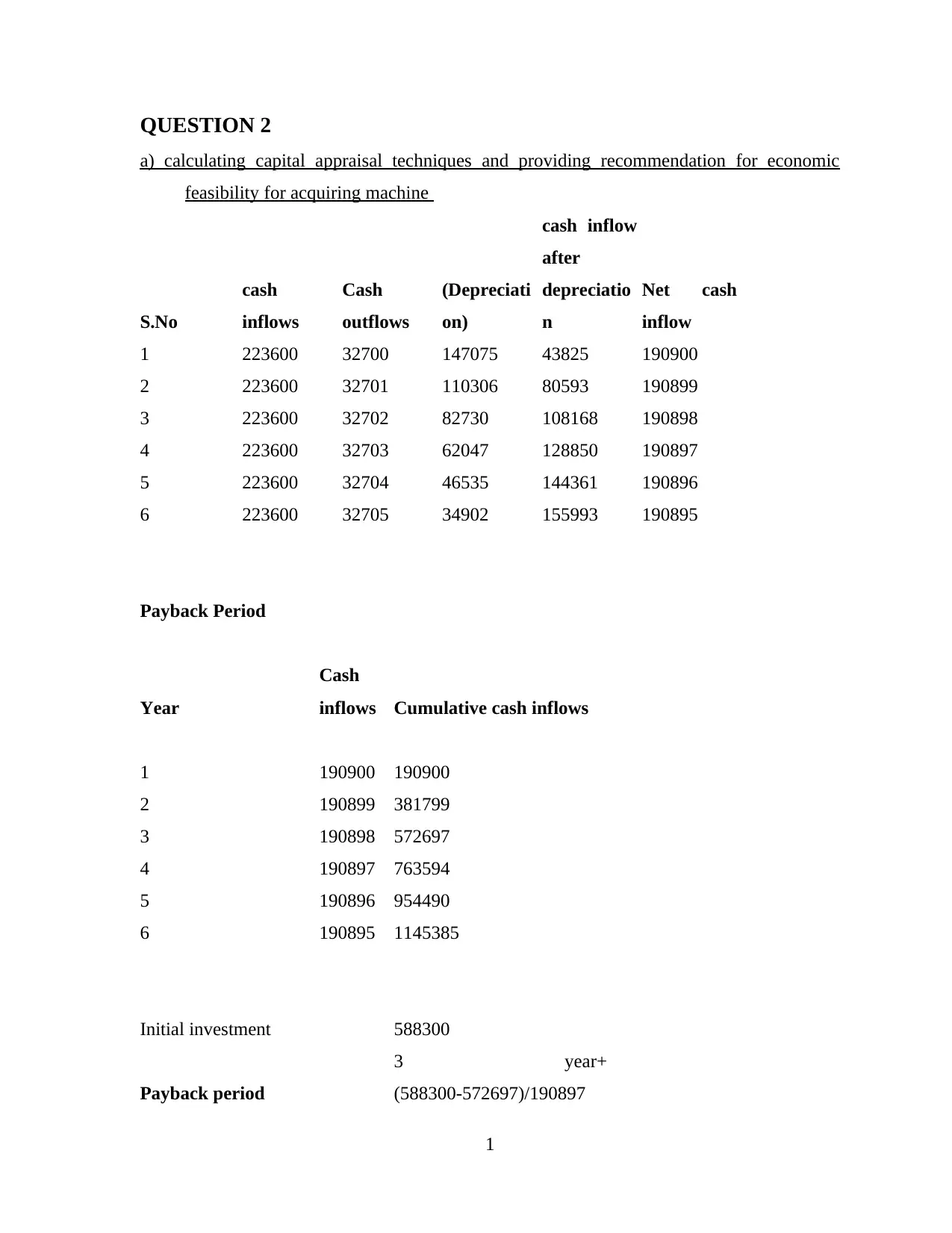

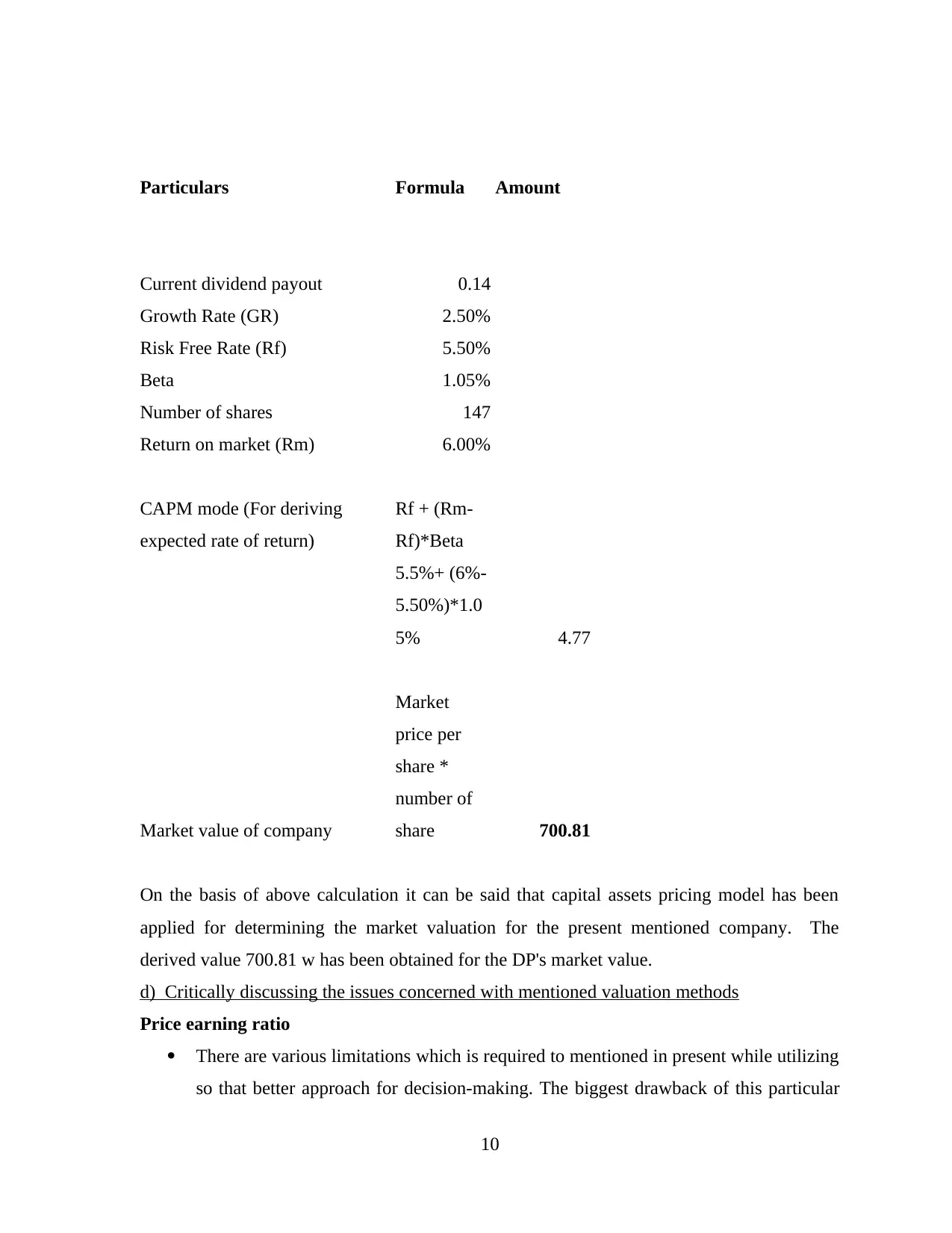

QUESTION 2

a) calculating capital appraisal techniques and providing recommendation for economic

feasibility for acquiring machine

S.No

cash

inflows

Cash

outflows

(Depreciati

on)

cash inflow

after

depreciatio

n

Net cash

inflow

1 223600 32700 147075 43825 190900

2 223600 32701 110306 80593 190899

3 223600 32702 82730 108168 190898

4 223600 32703 62047 128850 190897

5 223600 32704 46535 144361 190896

6 223600 32705 34902 155993 190895

Payback Period

Year

Cash

inflows Cumulative cash inflows

1 190900 190900

2 190899 381799

3 190898 572697

4 190897 763594

5 190896 954490

6 190895 1145385

Initial investment 588300

Payback period

3 year+

(588300-572697)/190897

1

a) calculating capital appraisal techniques and providing recommendation for economic

feasibility for acquiring machine

S.No

cash

inflows

Cash

outflows

(Depreciati

on)

cash inflow

after

depreciatio

n

Net cash

inflow

1 223600 32700 147075 43825 190900

2 223600 32701 110306 80593 190899

3 223600 32702 82730 108168 190898

4 223600 32703 62047 128850 190897

5 223600 32704 46535 144361 190896

6 223600 32705 34902 155993 190895

Payback Period

Year

Cash

inflows Cumulative cash inflows

1 190900 190900

2 190899 381799

3 190898 572697

4 190897 763594

5 190896 954490

6 190895 1145385

Initial investment 588300

Payback period

3 year+

(588300-572697)/190897

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

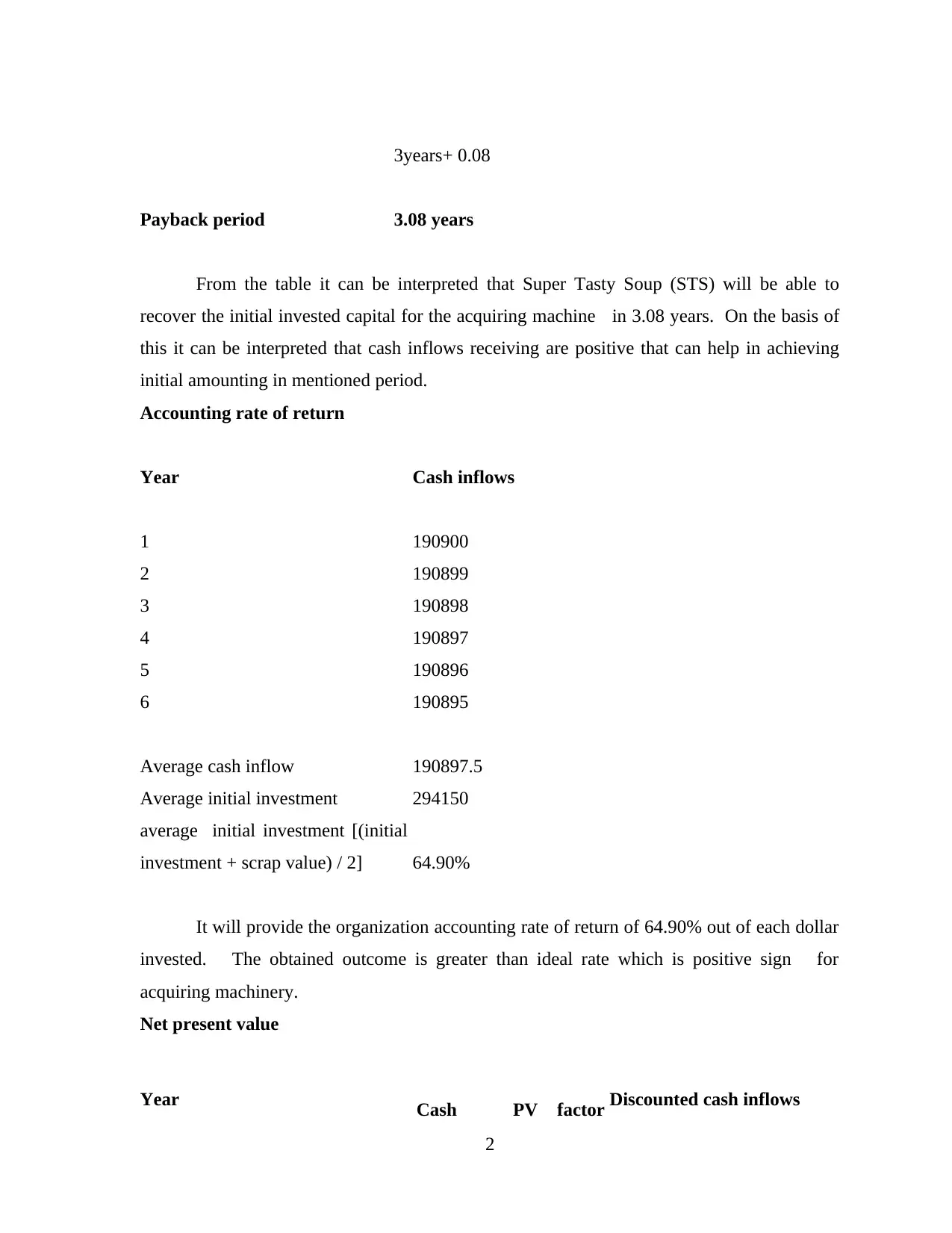

3years+ 0.08

Payback period 3.08 years

From the table it can be interpreted that Super Tasty Soup (STS) will be able to

recover the initial invested capital for the acquiring machine in 3.08 years. On the basis of

this it can be interpreted that cash inflows receiving are positive that can help in achieving

initial amounting in mentioned period.

Accounting rate of return

Year Cash inflows

1 190900

2 190899

3 190898

4 190897

5 190896

6 190895

Average cash inflow 190897.5

Average initial investment 294150

average initial investment [(initial

investment + scrap value) / 2] 64.90%

It will provide the organization accounting rate of return of 64.90% out of each dollar

invested. The obtained outcome is greater than ideal rate which is positive sign for

acquiring machinery.

Net present value

Year Cash PV factor Discounted cash inflows

2

Payback period 3.08 years

From the table it can be interpreted that Super Tasty Soup (STS) will be able to

recover the initial invested capital for the acquiring machine in 3.08 years. On the basis of

this it can be interpreted that cash inflows receiving are positive that can help in achieving

initial amounting in mentioned period.

Accounting rate of return

Year Cash inflows

1 190900

2 190899

3 190898

4 190897

5 190896

6 190895

Average cash inflow 190897.5

Average initial investment 294150

average initial investment [(initial

investment + scrap value) / 2] 64.90%

It will provide the organization accounting rate of return of 64.90% out of each dollar

invested. The obtained outcome is greater than ideal rate which is positive sign for

acquiring machinery.

Net present value

Year Cash PV factor Discounted cash inflows

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

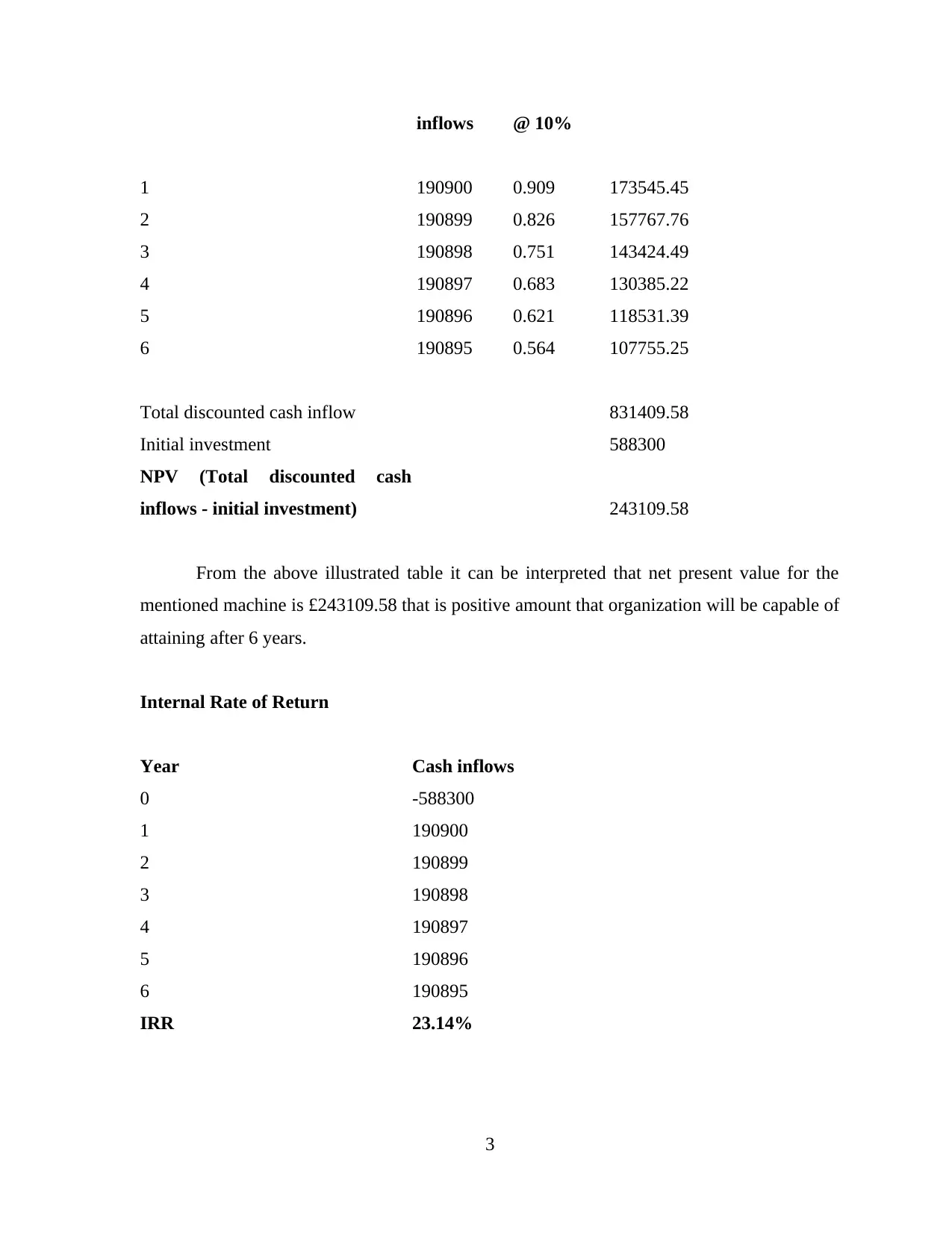

inflows @ 10%

1 190900 0.909 173545.45

2 190899 0.826 157767.76

3 190898 0.751 143424.49

4 190897 0.683 130385.22

5 190896 0.621 118531.39

6 190895 0.564 107755.25

Total discounted cash inflow 831409.58

Initial investment 588300

NPV (Total discounted cash

inflows - initial investment) 243109.58

From the above illustrated table it can be interpreted that net present value for the

mentioned machine is £243109.58 that is positive amount that organization will be capable of

attaining after 6 years.

Internal Rate of Return

Year Cash inflows

0 -588300

1 190900

2 190899

3 190898

4 190897

5 190896

6 190895

IRR 23.14%

3

1 190900 0.909 173545.45

2 190899 0.826 157767.76

3 190898 0.751 143424.49

4 190897 0.683 130385.22

5 190896 0.621 118531.39

6 190895 0.564 107755.25

Total discounted cash inflow 831409.58

Initial investment 588300

NPV (Total discounted cash

inflows - initial investment) 243109.58

From the above illustrated table it can be interpreted that net present value for the

mentioned machine is £243109.58 that is positive amount that organization will be capable of

attaining after 6 years.

Internal Rate of Return

Year Cash inflows

0 -588300

1 190900

2 190899

3 190898

4 190897

5 190896

6 190895

IRR 23.14%

3

The upper reflected table helps in achieving the knowledge regarding internal rate of

return derived from the invested capital. The particular machinery will provide the

significant value of return at rate of 23.14%.

Recommendation

From the evaluation for acquiring the machine on the basis of capital appraisal

techniques firm can obtain significant knowledge regarding its economic feasibility. In

addition to this, the firm will reach position to ascertain benefits & drawbacks for the

purpose making effective decision for accomplishing purpose of having positive cash

inflows.

It is suggested to the organization to identify the risk associated with monetary

outcomes of assets. Super Tasty Soup is advised to adopt the particular mentioned

technique from the perspective of risk as it will help in obtaining positive discounted

cash flow (Siziba, and Hall, 2019). This indicates that firm will be able to achieve

more than invested amount which that indicates its cost of manufacturing will be

recovered.

In order to increase profitability firm should adopt asset so that higher average rate of

return will allow firm to get economic feasibility in terms availability of liquidity

(Kengatharan, 2018). Implementing this technique can allow STS to be effectual in

overcoming cost related obligations so that smooth functioning can be obtained.

On the basis of payback period it is advised to Super Tasty Soup (STS) to have this

machine in company's operational practices. The mentioned course of action will

permit STS to become able to recover initial invested capital within 3.08 year that is

less than the life span stated in case. From this it is advised to STS to have this in

adopts the machine into organizational processing.

Super Tasty Soup is recommended to organization to adopt the particular technique in

its operational activities for having economic feasibility in terms of declined cost of

production, increased positively, etc. it will help in getting competitive advantages to

lead in industry for better progress.

b) Evaluating the effects of proposal on company

Capital structuring method adopted by organization highly affects the functioning &

processing that contribute in attaining success. Liquidity management becomes essential for

4

return derived from the invested capital. The particular machinery will provide the

significant value of return at rate of 23.14%.

Recommendation

From the evaluation for acquiring the machine on the basis of capital appraisal

techniques firm can obtain significant knowledge regarding its economic feasibility. In

addition to this, the firm will reach position to ascertain benefits & drawbacks for the

purpose making effective decision for accomplishing purpose of having positive cash

inflows.

It is suggested to the organization to identify the risk associated with monetary

outcomes of assets. Super Tasty Soup is advised to adopt the particular mentioned

technique from the perspective of risk as it will help in obtaining positive discounted

cash flow (Siziba, and Hall, 2019). This indicates that firm will be able to achieve

more than invested amount which that indicates its cost of manufacturing will be

recovered.

In order to increase profitability firm should adopt asset so that higher average rate of

return will allow firm to get economic feasibility in terms availability of liquidity

(Kengatharan, 2018). Implementing this technique can allow STS to be effectual in

overcoming cost related obligations so that smooth functioning can be obtained.

On the basis of payback period it is advised to Super Tasty Soup (STS) to have this

machine in company's operational practices. The mentioned course of action will

permit STS to become able to recover initial invested capital within 3.08 year that is

less than the life span stated in case. From this it is advised to STS to have this in

adopts the machine into organizational processing.

Super Tasty Soup is recommended to organization to adopt the particular technique in

its operational activities for having economic feasibility in terms of declined cost of

production, increased positively, etc. it will help in getting competitive advantages to

lead in industry for better progress.

b) Evaluating the effects of proposal on company

Capital structuring method adopted by organization highly affects the functioning &

processing that contribute in attaining success. Liquidity management becomes essential for

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the firm to get higher profitability & sustainability. The proposal of utilizing investment to

repurchase equity in proportion of 40% which is 235320 and paying rest as cash dividend

will affect organization in getting good reputation through attaining higher level of

satisfaction among investors.

According to the net operating income approach which allows firm to establish

optimum capital structure (Capital Structure Theory – Net Operating Income Approach,

2021). This is concerned with making appropriate value of firm depends on the operating

income & concerned business risk. In these suitable proportion is allowed to adopted in form

of equity & debt. From the evaluation of given proposal it can be articulated that having 40%

invested in equity capital & paying remaining amount as cash dividend to investors can

enable firm to earn less operating income as cost of capital will remain constant. In addition

to this, the particular theory assumes that there is no taxes which can enable the organization

to be prompt in having significant benefit in earning higher profitability.

From the proposed proposal company can obtain much benefits as compared to

investing in equity shares. In addition to this, it will provide different competitive

advantages than investing in machinery. This includes fixed cost unchanged by the equity

capital as well theory articulates that there will be no change sin cost of capital. It will allow

organization to meet its operating expenditure in effectual manner. The firm becomes

possible to have collateral free equity financing that will permit the specified organization to

be had constant level of risk that is one the significant benefit attained by firm while giving

emphasis on this particular capital structure. This theory of financial management will

provide mentioned level of significance for smooth functioning.

Explaining benefits & drawbacks of investment appraisal techniques

According to Knoke, Gosling and Paul, (2020) net present value is one of the viable

technique used for discounted cash flow tool for decision making. There are various benefits

of this particular technique which allows organization to implement strategic decision. It

includes unambiguous measure that estimates wealth creation of particular project. It largely

pays attention on measuring the time value of money. These benefits are crucial for

company while evaluating any option in turn better profitability can be attained. In against to

this, Gaspars-Wieloch (2019) articulated that discount rate is same over the life of particular

investment that does not provide appropriate knowledge. This drawback is one of the

5

repurchase equity in proportion of 40% which is 235320 and paying rest as cash dividend

will affect organization in getting good reputation through attaining higher level of

satisfaction among investors.

According to the net operating income approach which allows firm to establish

optimum capital structure (Capital Structure Theory – Net Operating Income Approach,

2021). This is concerned with making appropriate value of firm depends on the operating

income & concerned business risk. In these suitable proportion is allowed to adopted in form

of equity & debt. From the evaluation of given proposal it can be articulated that having 40%

invested in equity capital & paying remaining amount as cash dividend to investors can

enable firm to earn less operating income as cost of capital will remain constant. In addition

to this, the particular theory assumes that there is no taxes which can enable the organization

to be prompt in having significant benefit in earning higher profitability.

From the proposed proposal company can obtain much benefits as compared to

investing in equity shares. In addition to this, it will provide different competitive

advantages than investing in machinery. This includes fixed cost unchanged by the equity

capital as well theory articulates that there will be no change sin cost of capital. It will allow

organization to meet its operating expenditure in effectual manner. The firm becomes

possible to have collateral free equity financing that will permit the specified organization to

be had constant level of risk that is one the significant benefit attained by firm while giving

emphasis on this particular capital structure. This theory of financial management will

provide mentioned level of significance for smooth functioning.

Explaining benefits & drawbacks of investment appraisal techniques

According to Knoke, Gosling and Paul, (2020) net present value is one of the viable

technique used for discounted cash flow tool for decision making. There are various benefits

of this particular technique which allows organization to implement strategic decision. It

includes unambiguous measure that estimates wealth creation of particular project. It largely

pays attention on measuring the time value of money. These benefits are crucial for

company while evaluating any option in turn better profitability can be attained. In against to

this, Gaspars-Wieloch (2019) articulated that discount rate is same over the life of particular

investment that does not provide appropriate knowledge. This drawback is one of the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

important limitation of net present value method of capital appraisal which required to be

keep in mind before selecting any project (Net Present Value,2021). On contrast to this,

Abdelhady, (2021) NPV permits the enterprise to get the information regarding risk elements

so that significant formulation of decision can be exerted to achieve larger advantages.

In the views of Verma and et.al., 2021 payback period is concerned with making

proper determination of years within which firm will be able to recover its invested capital.

This specific method allows the company to have certain advantages such as simple to utilize

& understand. In case of uncertainty firm becomes capable to determine the values for the

purpose of decision-making. On the other side, Maheshwari, Maheshwari and Maheshwari,

(2021) said that it ignores time value of money & all cash flow covered is as well neglected

which leads to inappropriate decision formulation. There is no realistic execution of this

particular concept that can negatively affect the functioning & decision making processing

of company. Ignorance of return on investment is found in this particular method of capital

appraisal. In contrast to this, Mollah, Rouf and Rana, (2021) said that there is involvement

of providing preference to liquidity which enable enterprise to get quick solution for the

prevailing circumstances.

In the opinion of Siziba and Hall, (2019) IRR helps in estimating profitability of

particular investment. These has certain advantages which includes its simple nature that is

easy to understand for reaching conclusion. Time value of money is considered while

computing the particular method for drawing decision. Simple interpreting with its presenting

method in percentage saves time for making decision. In contrast to this, Agbeye, (2019)

this includes variety of disadvantages that are important to highlight for having desirable

outcome. Economic of scales is ignored due to dependence on contingent projects.

Increasing wealth is not possible to measure in it. On the other side, DeBoeuf and et.al.,

(2018) said that there is no requirement of calculating required rate of return which bring

effectiveness in this particular project.

According to Casalini and Vecchi (2021) accounting rate of return is widely used

by organization to have sufficient knowledge & efficiency in making decision regarding

capital appraising for achieving objectives. Having clear picture regarding profitability can

enable the firm to get transparent outcome attaining capacity. This as well gives focus on

measuring the current performance of company which helps in comparing present results

6

keep in mind before selecting any project (Net Present Value,2021). On contrast to this,

Abdelhady, (2021) NPV permits the enterprise to get the information regarding risk elements

so that significant formulation of decision can be exerted to achieve larger advantages.

In the views of Verma and et.al., 2021 payback period is concerned with making

proper determination of years within which firm will be able to recover its invested capital.

This specific method allows the company to have certain advantages such as simple to utilize

& understand. In case of uncertainty firm becomes capable to determine the values for the

purpose of decision-making. On the other side, Maheshwari, Maheshwari and Maheshwari,

(2021) said that it ignores time value of money & all cash flow covered is as well neglected

which leads to inappropriate decision formulation. There is no realistic execution of this

particular concept that can negatively affect the functioning & decision making processing

of company. Ignorance of return on investment is found in this particular method of capital

appraisal. In contrast to this, Mollah, Rouf and Rana, (2021) said that there is involvement

of providing preference to liquidity which enable enterprise to get quick solution for the

prevailing circumstances.

In the opinion of Siziba and Hall, (2019) IRR helps in estimating profitability of

particular investment. These has certain advantages which includes its simple nature that is

easy to understand for reaching conclusion. Time value of money is considered while

computing the particular method for drawing decision. Simple interpreting with its presenting

method in percentage saves time for making decision. In contrast to this, Agbeye, (2019)

this includes variety of disadvantages that are important to highlight for having desirable

outcome. Economic of scales is ignored due to dependence on contingent projects.

Increasing wealth is not possible to measure in it. On the other side, DeBoeuf and et.al.,

(2018) said that there is no requirement of calculating required rate of return which bring

effectiveness in this particular project.

According to Casalini and Vecchi (2021) accounting rate of return is widely used

by organization to have sufficient knowledge & efficiency in making decision regarding

capital appraising for achieving objectives. Having clear picture regarding profitability can

enable the firm to get transparent outcome attaining capacity. This as well gives focus on

measuring the current performance of company which helps in comparing present results

6

with previous to interpret end outcome effectively. This method does not allow the external

factors involvement that is one of the major negative factor required to focus. On contrast to

this, Pawlak and Zarzecki (2020) It satisfies the investors as it provide assistance in

measuring the return on investment that is one of the crucial object of investing.

QUESTION 3

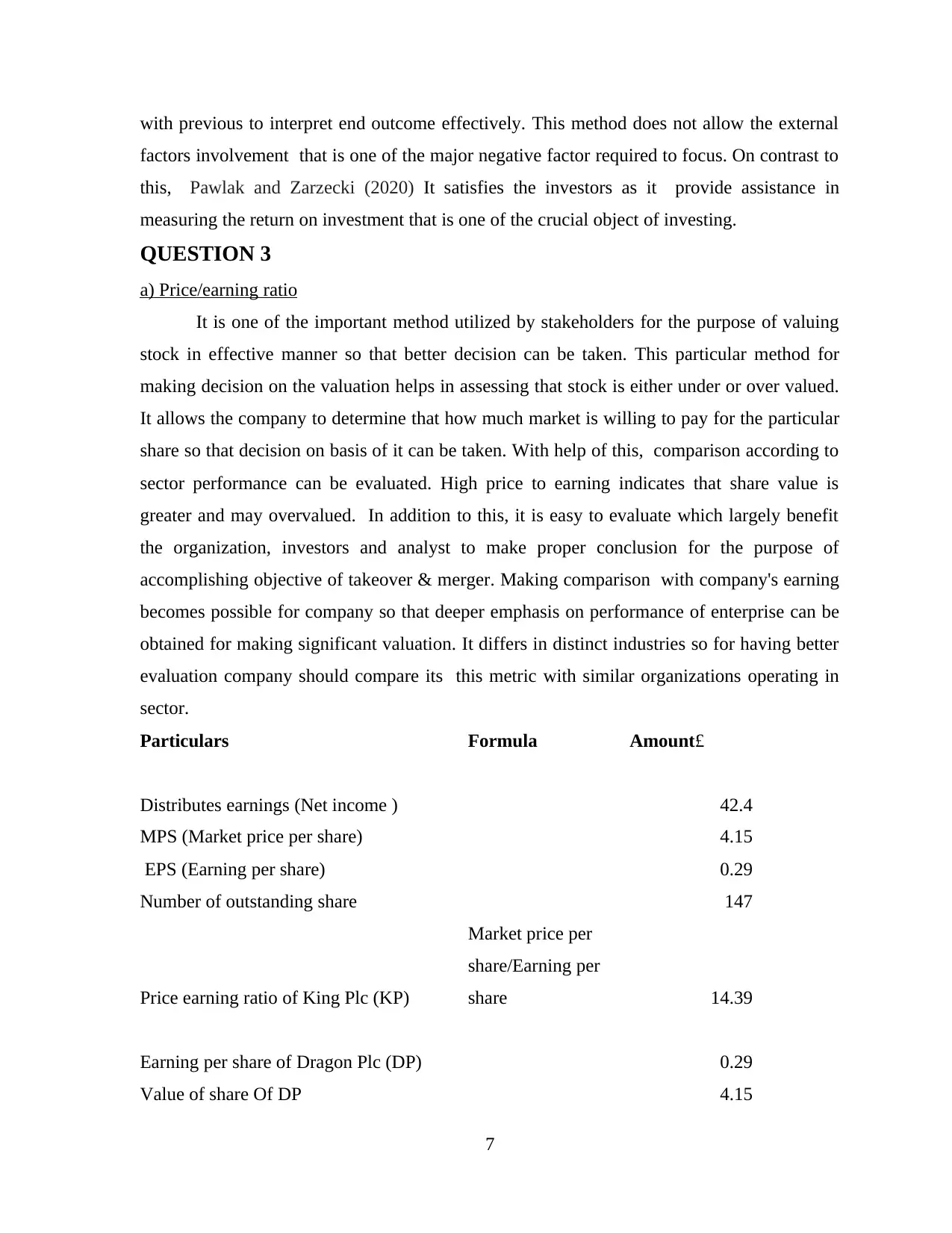

a) Price/earning ratio

It is one of the important method utilized by stakeholders for the purpose of valuing

stock in effective manner so that better decision can be taken. This particular method for

making decision on the valuation helps in assessing that stock is either under or over valued.

It allows the company to determine that how much market is willing to pay for the particular

share so that decision on basis of it can be taken. With help of this, comparison according to

sector performance can be evaluated. High price to earning indicates that share value is

greater and may overvalued. In addition to this, it is easy to evaluate which largely benefit

the organization, investors and analyst to make proper conclusion for the purpose of

accomplishing objective of takeover & merger. Making comparison with company's earning

becomes possible for company so that deeper emphasis on performance of enterprise can be

obtained for making significant valuation. It differs in distinct industries so for having better

evaluation company should compare its this metric with similar organizations operating in

sector.

Particulars Formula Amount£

Distributes earnings (Net income ) 42.4

MPS (Market price per share) 4.15

EPS (Earning per share) 0.29

Number of outstanding share 147

Price earning ratio of King Plc (KP)

Market price per

share/Earning per

share 14.39

Earning per share of Dragon Plc (DP) 0.29

Value of share Of DP 4.15

7

factors involvement that is one of the major negative factor required to focus. On contrast to

this, Pawlak and Zarzecki (2020) It satisfies the investors as it provide assistance in

measuring the return on investment that is one of the crucial object of investing.

QUESTION 3

a) Price/earning ratio

It is one of the important method utilized by stakeholders for the purpose of valuing

stock in effective manner so that better decision can be taken. This particular method for

making decision on the valuation helps in assessing that stock is either under or over valued.

It allows the company to determine that how much market is willing to pay for the particular

share so that decision on basis of it can be taken. With help of this, comparison according to

sector performance can be evaluated. High price to earning indicates that share value is

greater and may overvalued. In addition to this, it is easy to evaluate which largely benefit

the organization, investors and analyst to make proper conclusion for the purpose of

accomplishing objective of takeover & merger. Making comparison with company's earning

becomes possible for company so that deeper emphasis on performance of enterprise can be

obtained for making significant valuation. It differs in distinct industries so for having better

evaluation company should compare its this metric with similar organizations operating in

sector.

Particulars Formula Amount£

Distributes earnings (Net income ) 42.4

MPS (Market price per share) 4.15

EPS (Earning per share) 0.29

Number of outstanding share 147

Price earning ratio of King Plc (KP)

Market price per

share/Earning per

share 14.39

Earning per share of Dragon Plc (DP) 0.29

Value of share Of DP 4.15

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Computation of market value of Dragon

Plc.

Value of shares of

Dragon*Number of

outstanding share 4.15*147

£610.05

From the above table it can be interpreted that specified company Dragon Plc (DP) is

£610.05

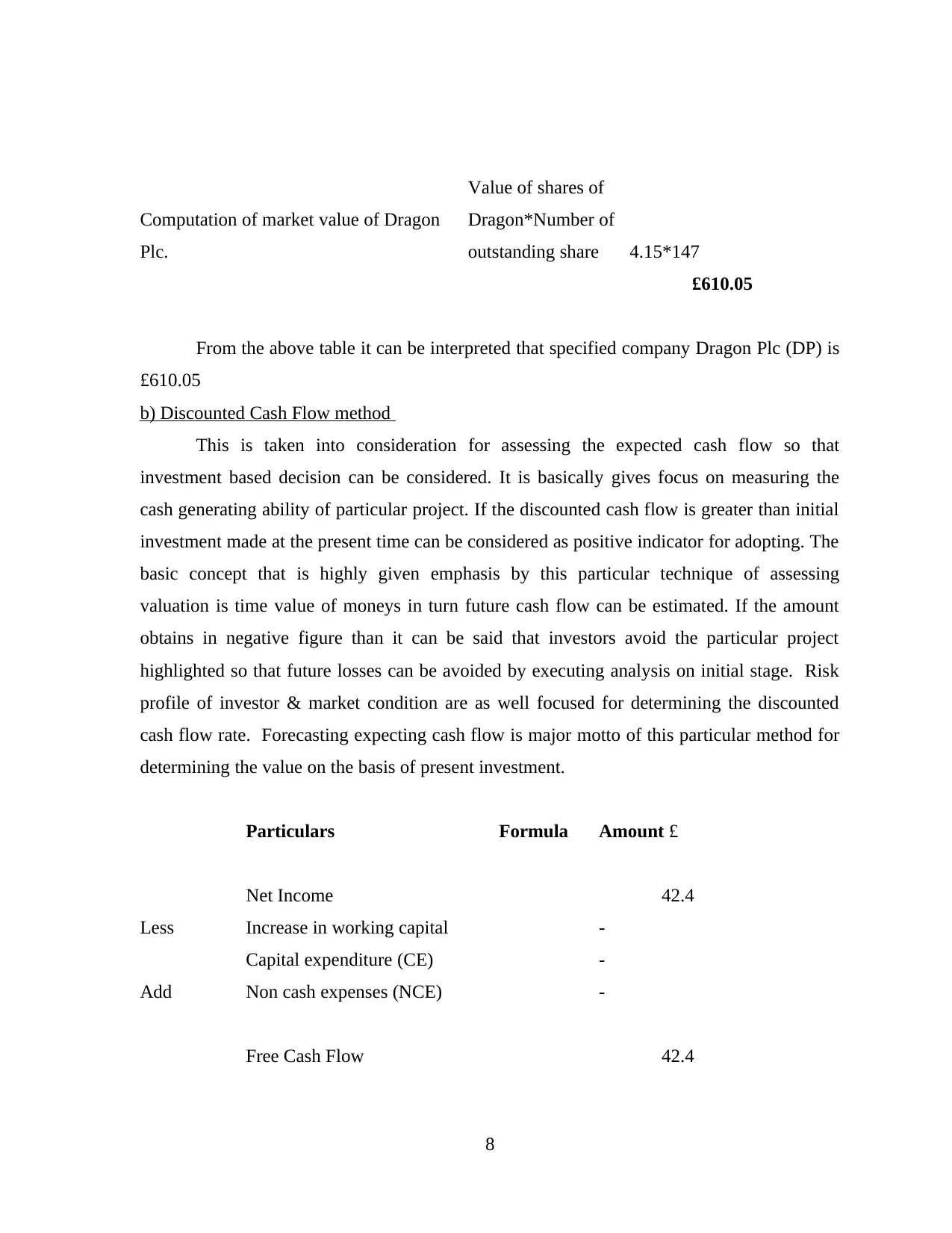

b) Discounted Cash Flow method

This is taken into consideration for assessing the expected cash flow so that

investment based decision can be considered. It is basically gives focus on measuring the

cash generating ability of particular project. If the discounted cash flow is greater than initial

investment made at the present time can be considered as positive indicator for adopting. The

basic concept that is highly given emphasis by this particular technique of assessing

valuation is time value of moneys in turn future cash flow can be estimated. If the amount

obtains in negative figure than it can be said that investors avoid the particular project

highlighted so that future losses can be avoided by executing analysis on initial stage. Risk

profile of investor & market condition are as well focused for determining the discounted

cash flow rate. Forecasting expecting cash flow is major motto of this particular method for

determining the value on the basis of present investment.

Particulars Formula Amount £

Net Income 42.4

Less Increase in working capital -

Capital expenditure (CE) -

Add Non cash expenses (NCE) -

Free Cash Flow 42.4

8

Plc.

Value of shares of

Dragon*Number of

outstanding share 4.15*147

£610.05

From the above table it can be interpreted that specified company Dragon Plc (DP) is

£610.05

b) Discounted Cash Flow method

This is taken into consideration for assessing the expected cash flow so that

investment based decision can be considered. It is basically gives focus on measuring the

cash generating ability of particular project. If the discounted cash flow is greater than initial

investment made at the present time can be considered as positive indicator for adopting. The

basic concept that is highly given emphasis by this particular technique of assessing

valuation is time value of moneys in turn future cash flow can be estimated. If the amount

obtains in negative figure than it can be said that investors avoid the particular project

highlighted so that future losses can be avoided by executing analysis on initial stage. Risk

profile of investor & market condition are as well focused for determining the discounted

cash flow rate. Forecasting expecting cash flow is major motto of this particular method for

determining the value on the basis of present investment.

Particulars Formula Amount £

Net Income 42.4

Less Increase in working capital -

Capital expenditure (CE) -

Add Non cash expenses (NCE) -

Free Cash Flow 42.4

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Weighted average cost of capital 12.00%

Market price per share

Free Cash

Flow/weight

ed average

cost of

capital

353.333333

3333

Computation of market value of

Dragon Plc.

MPS*Numb

er of shares 353*147

£51940

On the basis of above table it can be interpreted market value of Dragon Plc for the

purpose of making investment. £51940 is market value of the organization as per the

discounted cash flow.

c) Dividend valuation method

It is quantitative method used for predicting the price of company's stock based on the

theory that is associated with present day price is total of all future dividend payouts. This

specific method is concerned with evaluating market value according to the divided paid by

organization. This model highlights that capital appreciation is obtain when there is higher

dividend obtained by investors which helps the organization to understand that how much

they are paying to stakeholders. There are two cash flows which includes future dividend

payments & selling prices. Earning growth & dividend growth rate is expected to be

constant according to dividend discount model of valuation. The reason behind this

assumption is that if it will rise will sustain for shorter duration therefore it is as well called

as sustainable rate on the basis of which decision. It is enough accurate tool utilized by

investors & analyst for making decision. In addition to this, it is one of the crucial model

practiced by investors & analyst for the purpose of making judgment regarding company's

market value.

9

Market price per share

Free Cash

Flow/weight

ed average

cost of

capital

353.333333

3333

Computation of market value of

Dragon Plc.

MPS*Numb

er of shares 353*147

£51940

On the basis of above table it can be interpreted market value of Dragon Plc for the

purpose of making investment. £51940 is market value of the organization as per the

discounted cash flow.

c) Dividend valuation method

It is quantitative method used for predicting the price of company's stock based on the

theory that is associated with present day price is total of all future dividend payouts. This

specific method is concerned with evaluating market value according to the divided paid by

organization. This model highlights that capital appreciation is obtain when there is higher

dividend obtained by investors which helps the organization to understand that how much

they are paying to stakeholders. There are two cash flows which includes future dividend

payments & selling prices. Earning growth & dividend growth rate is expected to be

constant according to dividend discount model of valuation. The reason behind this

assumption is that if it will rise will sustain for shorter duration therefore it is as well called

as sustainable rate on the basis of which decision. It is enough accurate tool utilized by

investors & analyst for making decision. In addition to this, it is one of the crucial model

practiced by investors & analyst for the purpose of making judgment regarding company's

market value.

9

Particulars Formula Amount

Current dividend payout 0.14

Growth Rate (GR) 2.50%

Risk Free Rate (Rf) 5.50%

Beta 1.05%

Number of shares 147

Return on market (Rm) 6.00%

CAPM mode (For deriving

expected rate of return)

Rf + (Rm-

Rf)*Beta

5.5%+ (6%-

5.50%)*1.0

5% 4.77

Market value of company

Market

price per

share *

number of

share 700.81

On the basis of above calculation it can be said that capital assets pricing model has been

applied for determining the market valuation for the present mentioned company. The

derived value 700.81 w has been obtained for the DP's market value.

d) Critically discussing the issues concerned with mentioned valuation methods

Price earning ratio

There are various limitations which is required to mentioned in present while utilizing

so that better approach for decision-making. The biggest drawback of this particular

10

Current dividend payout 0.14

Growth Rate (GR) 2.50%

Risk Free Rate (Rf) 5.50%

Beta 1.05%

Number of shares 147

Return on market (Rm) 6.00%

CAPM mode (For deriving

expected rate of return)

Rf + (Rm-

Rf)*Beta

5.5%+ (6%-

5.50%)*1.0

5% 4.77

Market value of company

Market

price per

share *

number of

share 700.81

On the basis of above calculation it can be said that capital assets pricing model has been

applied for determining the market valuation for the present mentioned company. The

derived value 700.81 w has been obtained for the DP's market value.

d) Critically discussing the issues concerned with mentioned valuation methods

Price earning ratio

There are various limitations which is required to mentioned in present while utilizing

so that better approach for decision-making. The biggest drawback of this particular

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.