Financial Management: Investment Appraisal and Merger Analysis Methods

VerifiedAdded on 2023/01/09

|14

|3836

|34

Report

AI Summary

This report delves into financial management principles, focusing on investment appraisal methods and merger analysis. It examines the potential acquisition of Trojan plc by Aztec plc, utilizing price earnings ratio, dividend valuation model, and discounted cash flow methods to assess the viability of the merger. The report critically evaluates the advantages and disadvantages of each valuation method. Additionally, it explores investment appraisal techniques, including payback period, accounting rate of return, net present value, and internal rate of return, to evaluate the profitability of a new equipment purchase for Love Well Limited. Recommendations are provided based on the analysis of these methods, offering insights into strategic financial decision-making. Desklib provides access to this and other solved assignments.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

Question...........................................................................................................................................3

Question 2: Merger and takeovers..........................................................................................3

Question 3 Investment appraisal methods..............................................................................7

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

Question...........................................................................................................................................3

Question 2: Merger and takeovers..........................................................................................3

Question 3 Investment appraisal methods..............................................................................7

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

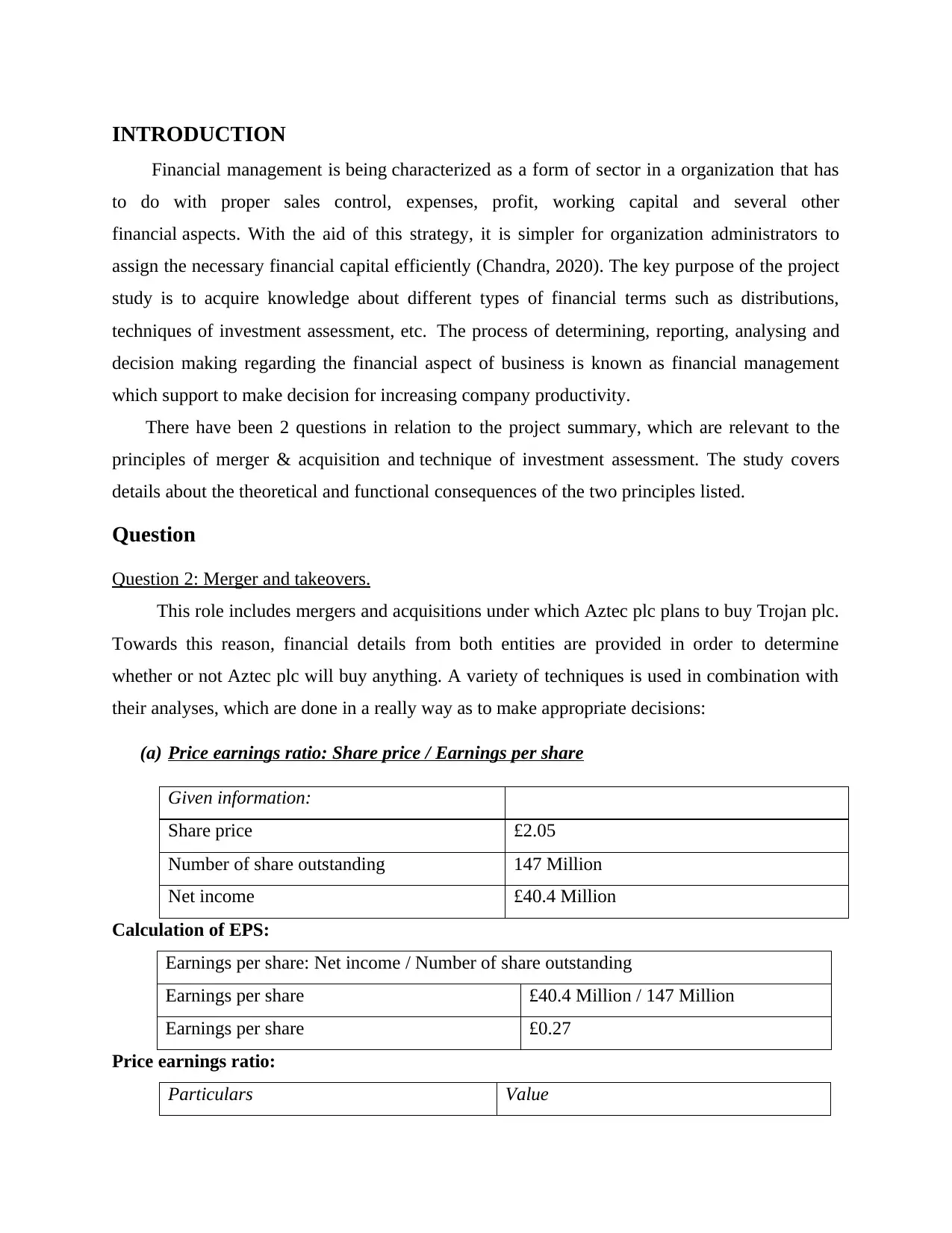

INTRODUCTION

Financial management is being characterized as a form of sector in a organization that has

to do with proper sales control, expenses, profit, working capital and several other

financial aspects. With the aid of this strategy, it is simpler for organization administrators to

assign the necessary financial capital efficiently (Chandra, 2020). The key purpose of the project

study is to acquire knowledge about different types of financial terms such as distributions,

techniques of investment assessment, etc. The process of determining, reporting, analysing and

decision making regarding the financial aspect of business is known as financial management

which support to make decision for increasing company productivity.

There have been 2 questions in relation to the project summary, which are relevant to the

principles of merger & acquisition and technique of investment assessment. The study covers

details about the theoretical and functional consequences of the two principles listed.

Question

Question 2: Merger and takeovers.

This role includes mergers and acquisitions under which Aztec plc plans to buy Trojan plc.

Towards this reason, financial details from both entities are provided in order to determine

whether or not Aztec plc will buy anything. A variety of techniques is used in combination with

their analyses, which are done in a really way as to make appropriate decisions:

(a) Price earnings ratio: Share price / Earnings per share

Given information:

Share price £2.05

Number of share outstanding 147 Million

Net income £40.4 Million

Calculation of EPS:

Earnings per share: Net income / Number of share outstanding

Earnings per share £40.4 Million / 147 Million

Earnings per share £0.27

Price earnings ratio:

Particulars Value

Financial management is being characterized as a form of sector in a organization that has

to do with proper sales control, expenses, profit, working capital and several other

financial aspects. With the aid of this strategy, it is simpler for organization administrators to

assign the necessary financial capital efficiently (Chandra, 2020). The key purpose of the project

study is to acquire knowledge about different types of financial terms such as distributions,

techniques of investment assessment, etc. The process of determining, reporting, analysing and

decision making regarding the financial aspect of business is known as financial management

which support to make decision for increasing company productivity.

There have been 2 questions in relation to the project summary, which are relevant to the

principles of merger & acquisition and technique of investment assessment. The study covers

details about the theoretical and functional consequences of the two principles listed.

Question

Question 2: Merger and takeovers.

This role includes mergers and acquisitions under which Aztec plc plans to buy Trojan plc.

Towards this reason, financial details from both entities are provided in order to determine

whether or not Aztec plc will buy anything. A variety of techniques is used in combination with

their analyses, which are done in a really way as to make appropriate decisions:

(a) Price earnings ratio: Share price / Earnings per share

Given information:

Share price £2.05

Number of share outstanding 147 Million

Net income £40.4 Million

Calculation of EPS:

Earnings per share: Net income / Number of share outstanding

Earnings per share £40.4 Million / 147 Million

Earnings per share £0.27

Price earnings ratio:

Particulars Value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

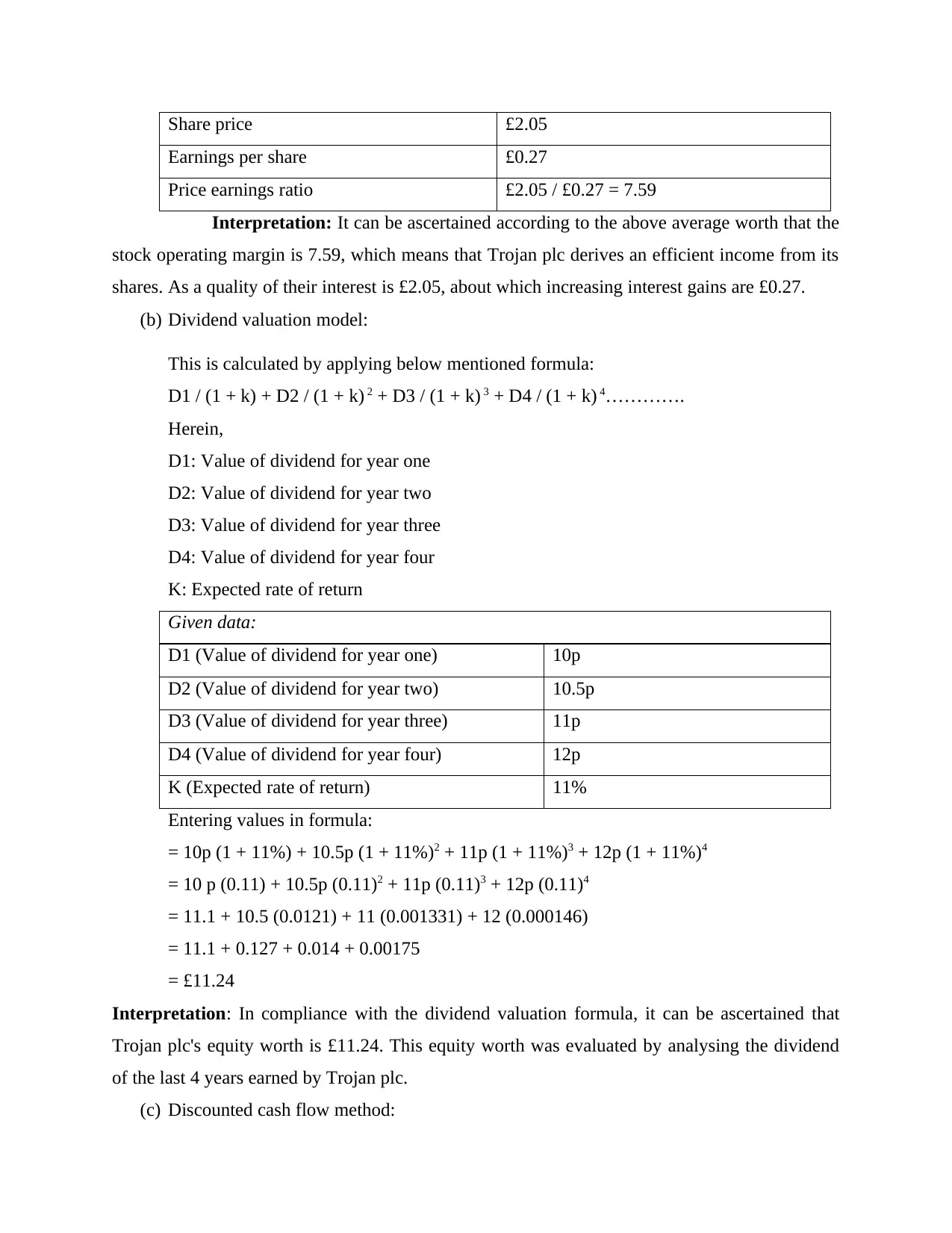

Share price £2.05

Earnings per share £0.27

Price earnings ratio £2.05 / £0.27 = 7.59

Interpretation: It can be ascertained according to the above average worth that the

stock operating margin is 7.59, which means that Trojan plc derives an efficient income from its

shares. As a quality of their interest is £2.05, about which increasing interest gains are £0.27.

(b) Dividend valuation model:

This is calculated by applying below mentioned formula:

D1 / (1 + k) + D2 / (1 + k) 2 + D3 / (1 + k) 3 + D4 / (1 + k) 4………….

Herein,

D1: Value of dividend for year one

D2: Value of dividend for year two

D3: Value of dividend for year three

D4: Value of dividend for year four

K: Expected rate of return

Given data:

D1 (Value of dividend for year one) 10p

D2 (Value of dividend for year two) 10.5p

D3 (Value of dividend for year three) 11p

D4 (Value of dividend for year four) 12p

K (Expected rate of return) 11%

Entering values in formula:

= 10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)3 + 12p (1 + 11%)4

= 10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

= 11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

= 11.1 + 0.127 + 0.014 + 0.00175

= £11.24

Interpretation: In compliance with the dividend valuation formula, it can be ascertained that

Trojan plc's equity worth is £11.24. This equity worth was evaluated by analysing the dividend

of the last 4 years earned by Trojan plc.

(c) Discounted cash flow method:

Earnings per share £0.27

Price earnings ratio £2.05 / £0.27 = 7.59

Interpretation: It can be ascertained according to the above average worth that the

stock operating margin is 7.59, which means that Trojan plc derives an efficient income from its

shares. As a quality of their interest is £2.05, about which increasing interest gains are £0.27.

(b) Dividend valuation model:

This is calculated by applying below mentioned formula:

D1 / (1 + k) + D2 / (1 + k) 2 + D3 / (1 + k) 3 + D4 / (1 + k) 4………….

Herein,

D1: Value of dividend for year one

D2: Value of dividend for year two

D3: Value of dividend for year three

D4: Value of dividend for year four

K: Expected rate of return

Given data:

D1 (Value of dividend for year one) 10p

D2 (Value of dividend for year two) 10.5p

D3 (Value of dividend for year three) 11p

D4 (Value of dividend for year four) 12p

K (Expected rate of return) 11%

Entering values in formula:

= 10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)3 + 12p (1 + 11%)4

= 10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

= 11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

= 11.1 + 0.127 + 0.014 + 0.00175

= £11.24

Interpretation: In compliance with the dividend valuation formula, it can be ascertained that

Trojan plc's equity worth is £11.24. This equity worth was evaluated by analysing the dividend

of the last 4 years earned by Trojan plc.

(c) Discounted cash flow method:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Through applying certain formula, the value of the share is determined according to this

methodology:

CF1 / (1+r) 1 + CF2 / (1+r) 2 + CF n / (1+r) n

r: 5%

= £40.4 / (1 + 5%)

= £808

Interpretation: Stock worth is £808 in discounted cash process. Discounted cost is known as 5

per cent in the estimation of the share interest. Along with income contribution is calculated as

one of £40.4 in cash flow each year.

(d) Analysis of problems associated with above mentioned valuation methods.

Price earnings ratio: This proportion is also called as PER, reflecting the relationship between

the share prices of the company and the earnings of each share (Rahman and Shamsuddin, 2019).

Customers use the formula to render a fair equity assessment, so that they might evaluate if they

are up or down priced. The key aim of using this method is to perform a company's portfolio

valuation so the market price could be measured efficiently. It is useful to investors when

assessing a company's earnings market worth when addition to earnings. Besides these attributes,

there are certain disadvantages throughout this proportion which are discussed follows in this

way:

Demerits

One of the key disadvantages of this formula is it doesn't take account of a company's

debt/income position when reviewing its financial reports.

This measure does not include details on an enterprise's earnings per share production.

Throughout the case of a rapidly growing business, buyers will make purchases even if

the ratio of price earnings is faster or slower.

methodology:

CF1 / (1+r) 1 + CF2 / (1+r) 2 + CF n / (1+r) n

r: 5%

= £40.4 / (1 + 5%)

= £808

Interpretation: Stock worth is £808 in discounted cash process. Discounted cost is known as 5

per cent in the estimation of the share interest. Along with income contribution is calculated as

one of £40.4 in cash flow each year.

(d) Analysis of problems associated with above mentioned valuation methods.

Price earnings ratio: This proportion is also called as PER, reflecting the relationship between

the share prices of the company and the earnings of each share (Rahman and Shamsuddin, 2019).

Customers use the formula to render a fair equity assessment, so that they might evaluate if they

are up or down priced. The key aim of using this method is to perform a company's portfolio

valuation so the market price could be measured efficiently. It is useful to investors when

assessing a company's earnings market worth when addition to earnings. Besides these attributes,

there are certain disadvantages throughout this proportion which are discussed follows in this

way:

Demerits

One of the key disadvantages of this formula is it doesn't take account of a company's

debt/income position when reviewing its financial reports.

This measure does not include details on an enterprise's earnings per share production.

Throughout the case of a rapidly growing business, buyers will make purchases even if

the ratio of price earnings is faster or slower.

Market perceptions will lead to high stock values for business as a whole. That is because

stocks are under calculation in the corresponding P / E ratio throughout contraction. In

the other side, firms' productivity earnings are measured in compliance with a given

nation's currency. This could boost PER’s worth (Itemgenova and Sikveland, 2020).

This approach is not appropriate for all businesses that suffer losses. This is so that in the

early period of market expansion, this framework cannot determine the importance of

losses.

Model of dividend calculation: This can be described as a form of share price income approach

predicated on the notion that the stock is valued the overall modern distribution payments. This

aims to calculate the fair value of a stock regardless of the current market climate, taking into

consideration the metrics of dividends paid and expected yields on the business (Akben-Selçuk,

2020). If the interest generated again from DDM meets the current stock share level, otherwise

the stock is under-priced and must qualify for a transaction, as well as conversely. Dividend

interest is calculated in the calculation that is used in this approach for the years a business pays

in. Like in the above-mentioned business sense, the dividends value from the last 4 years was

used to allow a reasonable assessment. This approach has certain disadvantages that are

described in following way:

Demerits

The biggest downside to this approach is that it should refer to such stocks that pay

dividends. It cannot be extended to certain stocks which pay no premium of any sort.

Throughout the case, this approach cannot be extended where there is a contrast among

small and big businesses and for smaller firms.

There are a variety of considerations that need to be weighed as per stock assessment,

like customer satisfaction, loyalty, capital expenditures etc. Although these are

considerations are neglected in the sense of the latter method as this approach only

recognizes dividend variables (Pinto, Robinson and Stowe, 2019).

In some countries, dividend pay-out is not seen as advantageous from a tax perspective.

Then the value of this template is zero, as investors tend to engage in stock repurchase.

The effectiveness of this approach is dependent entirely on details provided in the

formula. Unless the knowledge is false the stock value would therefore be unreliable. So

it is also a major drawback to use this share price form.

stocks are under calculation in the corresponding P / E ratio throughout contraction. In

the other side, firms' productivity earnings are measured in compliance with a given

nation's currency. This could boost PER’s worth (Itemgenova and Sikveland, 2020).

This approach is not appropriate for all businesses that suffer losses. This is so that in the

early period of market expansion, this framework cannot determine the importance of

losses.

Model of dividend calculation: This can be described as a form of share price income approach

predicated on the notion that the stock is valued the overall modern distribution payments. This

aims to calculate the fair value of a stock regardless of the current market climate, taking into

consideration the metrics of dividends paid and expected yields on the business (Akben-Selçuk,

2020). If the interest generated again from DDM meets the current stock share level, otherwise

the stock is under-priced and must qualify for a transaction, as well as conversely. Dividend

interest is calculated in the calculation that is used in this approach for the years a business pays

in. Like in the above-mentioned business sense, the dividends value from the last 4 years was

used to allow a reasonable assessment. This approach has certain disadvantages that are

described in following way:

Demerits

The biggest downside to this approach is that it should refer to such stocks that pay

dividends. It cannot be extended to certain stocks which pay no premium of any sort.

Throughout the case, this approach cannot be extended where there is a contrast among

small and big businesses and for smaller firms.

There are a variety of considerations that need to be weighed as per stock assessment,

like customer satisfaction, loyalty, capital expenditures etc. Although these are

considerations are neglected in the sense of the latter method as this approach only

recognizes dividend variables (Pinto, Robinson and Stowe, 2019).

In some countries, dividend pay-out is not seen as advantageous from a tax perspective.

Then the value of this template is zero, as investors tend to engage in stock repurchase.

The effectiveness of this approach is dependent entirely on details provided in the

formula. Unless the knowledge is false the stock value would therefore be unreliable. So

it is also a major drawback to use this share price form.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Discounted cash flow method: It is known as a form of valuation system compared to the

cash flows of the determined period of time (Shamsi, Mahdavi and Paydar, 2020). There under,

expenditure is priced for the present period of time according to the potential expectation of how

much revenue will be created there under. This is used by both creditors and company owner,

since this leads successfully to proper assessment. It method has other disadvantages that are as

described in the following way:

Disadvantage

Businesses find it hard to depend on the result extracted from this approach. That is

because different types of assessments are produced under this, like discount price,

pattern of increase, etc.

As well as this pattern, bad investment plans are not appropriate. This can only be

extended to larger-size ventures that contribute (Laitinen, 2019). It is because this

paradigm can be difficult to adopt for short term investments.

This approach only works efficiently where there is profitability for longer than two

years, this system cannot be implemented successfully in the case of severe cash flows.

Recommendation to Aztec plc: Based on the aforementioned analysis of all valuation

approaches, this can be directed to dividend additional value shareholders of the Aztec plc. This

is just so even though it is achieved in an effective way under this equity price. At the other

hand, the assessment of stock and profits that is ideal for internally and externally owners are

performed in the balance of two processes. Throughout the situation that a corporation wishes to

buy another corporation then DVM framework will be extended such that full analysis can be

achieved.

Question 3 Investment appraisal methods

This problem applies to the introduction of different forms of investment assessment in

try to determine out the productivity of modern equipment planned to be acquired by Love well

limited.

1. Calculations and suggestions:

(A) Payback period: The Two calculations are used in connection with the essence of cash flows

to calculate the payback period:

When cash balances are the same: initial investment / cash flow

cash flows of the determined period of time (Shamsi, Mahdavi and Paydar, 2020). There under,

expenditure is priced for the present period of time according to the potential expectation of how

much revenue will be created there under. This is used by both creditors and company owner,

since this leads successfully to proper assessment. It method has other disadvantages that are as

described in the following way:

Disadvantage

Businesses find it hard to depend on the result extracted from this approach. That is

because different types of assessments are produced under this, like discount price,

pattern of increase, etc.

As well as this pattern, bad investment plans are not appropriate. This can only be

extended to larger-size ventures that contribute (Laitinen, 2019). It is because this

paradigm can be difficult to adopt for short term investments.

This approach only works efficiently where there is profitability for longer than two

years, this system cannot be implemented successfully in the case of severe cash flows.

Recommendation to Aztec plc: Based on the aforementioned analysis of all valuation

approaches, this can be directed to dividend additional value shareholders of the Aztec plc. This

is just so even though it is achieved in an effective way under this equity price. At the other

hand, the assessment of stock and profits that is ideal for internally and externally owners are

performed in the balance of two processes. Throughout the situation that a corporation wishes to

buy another corporation then DVM framework will be extended such that full analysis can be

achieved.

Question 3 Investment appraisal methods

This problem applies to the introduction of different forms of investment assessment in

try to determine out the productivity of modern equipment planned to be acquired by Love well

limited.

1. Calculations and suggestions:

(A) Payback period: The Two calculations are used in connection with the essence of cash flows

to calculate the payback period:

When cash balances are the same: initial investment / cash flow

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If investment returns are unbalanced: year since investment return + sum to be regained / cash

flow in next periods.

This can be calculated in compliance with the provided financial information that there is

normal cash flow with all periods, hence:

Initial investment: £275000

Cash inflow: £85000

Less: Cash outflow: £12500

Cash flow: £72500

Payback period: 275000/72500

= 3.79 years

Recommendation: Through estimation of the equipment's payback time, it can be calculated

that the sum of 275000 pounds would be covered in 3.79 years. Although equipment lifetime is 6

years, this machine will be bought above the business as expenses will be protected by the

machinery's lifespan.

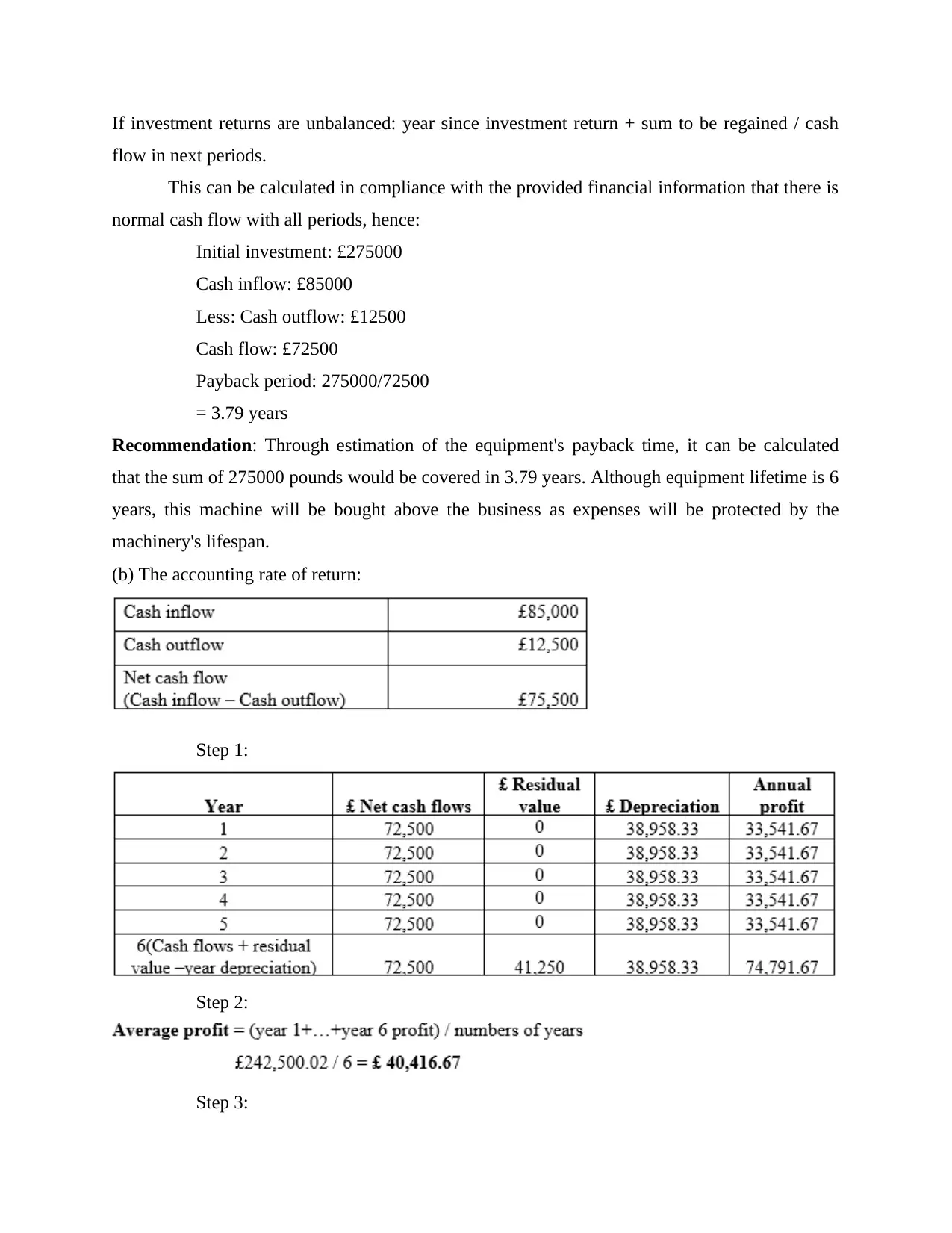

(b) The accounting rate of return:

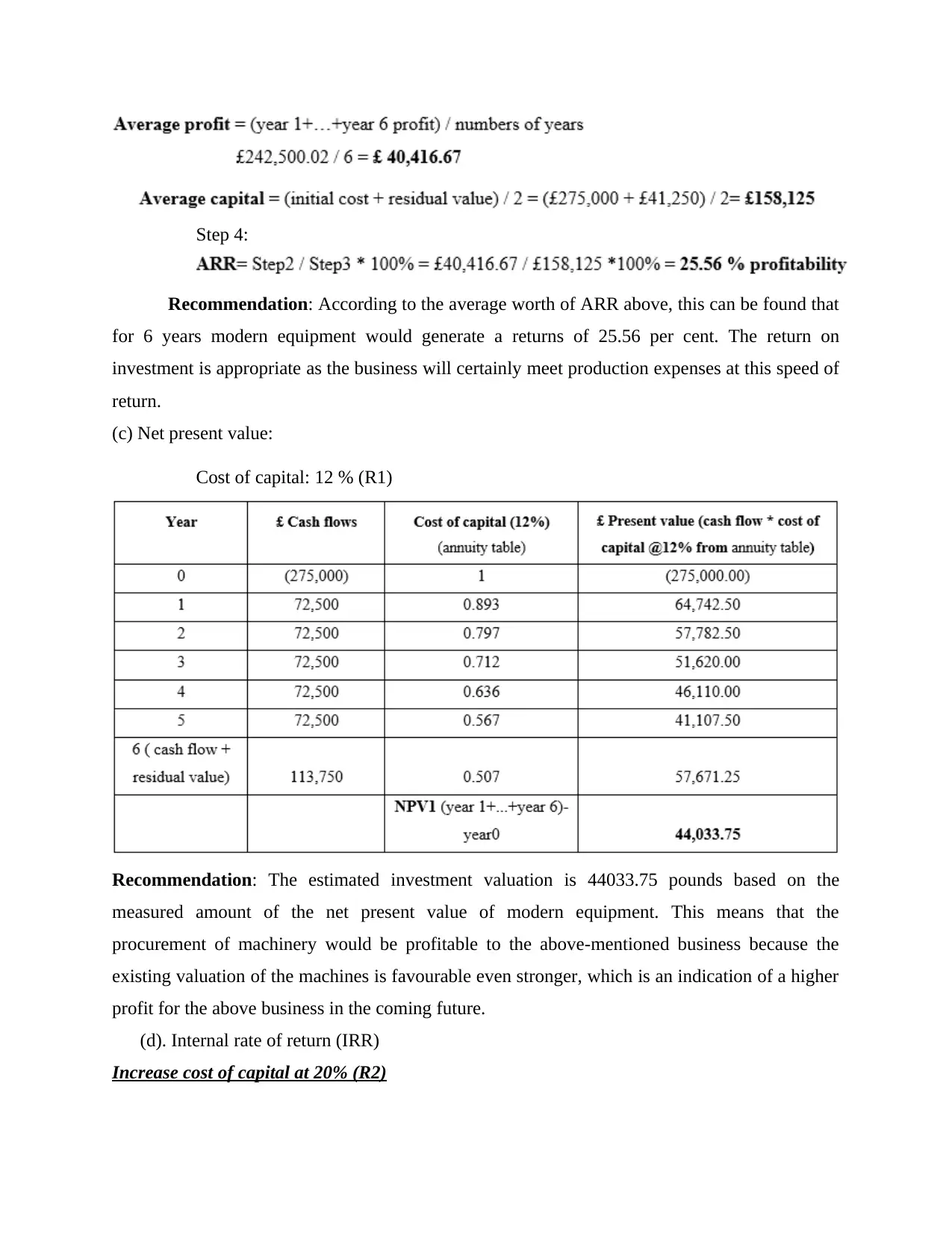

Step 1:

Step 2:

Step 3:

flow in next periods.

This can be calculated in compliance with the provided financial information that there is

normal cash flow with all periods, hence:

Initial investment: £275000

Cash inflow: £85000

Less: Cash outflow: £12500

Cash flow: £72500

Payback period: 275000/72500

= 3.79 years

Recommendation: Through estimation of the equipment's payback time, it can be calculated

that the sum of 275000 pounds would be covered in 3.79 years. Although equipment lifetime is 6

years, this machine will be bought above the business as expenses will be protected by the

machinery's lifespan.

(b) The accounting rate of return:

Step 1:

Step 2:

Step 3:

Step 4:

Recommendation: According to the average worth of ARR above, this can be found that

for 6 years modern equipment would generate a returns of 25.56 per cent. The return on

investment is appropriate as the business will certainly meet production expenses at this speed of

return.

(c) Net present value:

Cost of capital: 12 % (R1)

Recommendation: The estimated investment valuation is 44033.75 pounds based on the

measured amount of the net present value of modern equipment. This means that the

procurement of machinery would be profitable to the above-mentioned business because the

existing valuation of the machines is favourable even stronger, which is an indication of a higher

profit for the above business in the coming future.

(d). Internal rate of return (IRR)

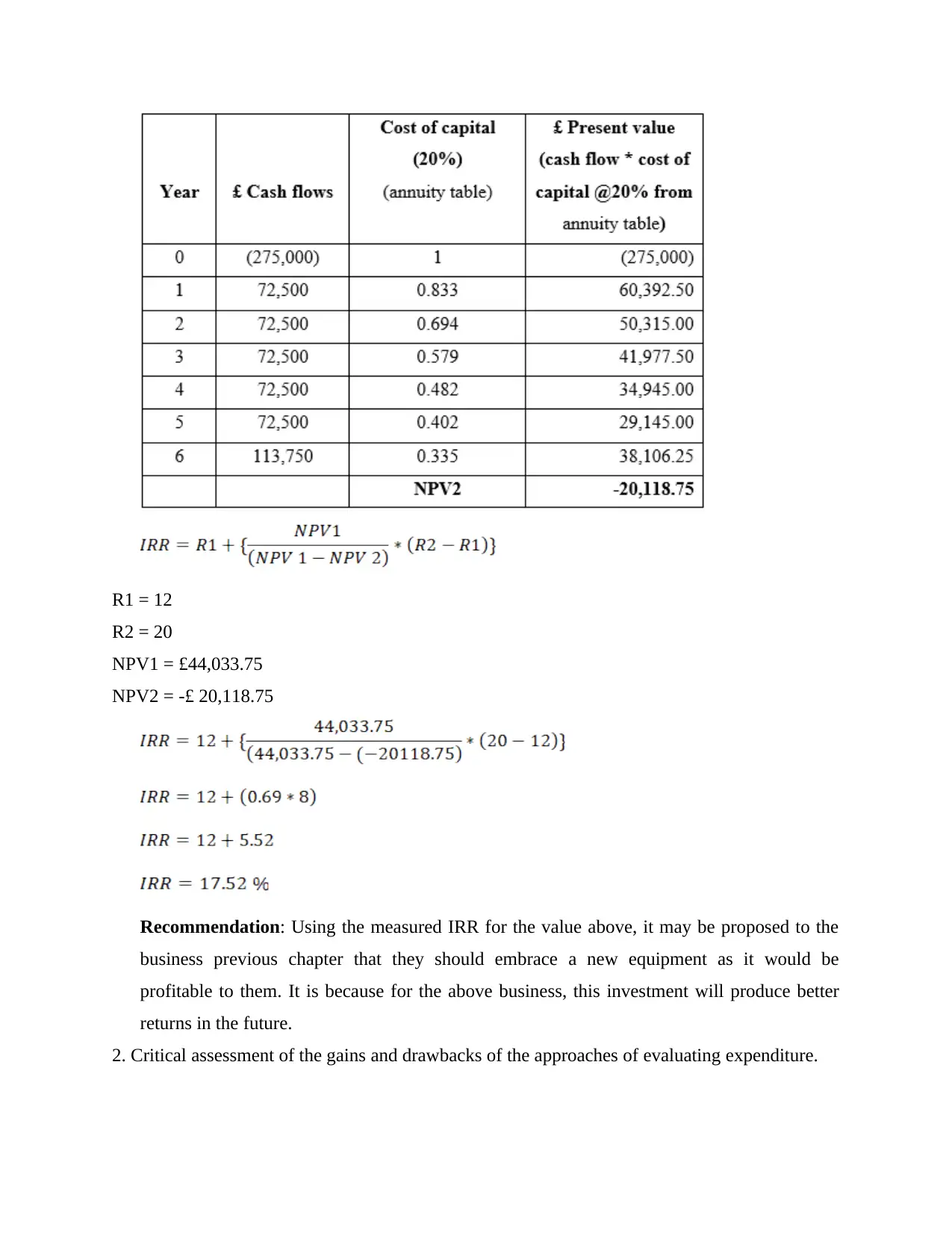

Increase cost of capital at 20% (R2)

Recommendation: According to the average worth of ARR above, this can be found that

for 6 years modern equipment would generate a returns of 25.56 per cent. The return on

investment is appropriate as the business will certainly meet production expenses at this speed of

return.

(c) Net present value:

Cost of capital: 12 % (R1)

Recommendation: The estimated investment valuation is 44033.75 pounds based on the

measured amount of the net present value of modern equipment. This means that the

procurement of machinery would be profitable to the above-mentioned business because the

existing valuation of the machines is favourable even stronger, which is an indication of a higher

profit for the above business in the coming future.

(d). Internal rate of return (IRR)

Increase cost of capital at 20% (R2)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

Recommendation: Using the measured IRR for the value above, it may be proposed to the

business previous chapter that they should embrace a new equipment as it would be

profitable to them. It is because for the above business, this investment will produce better

returns in the future.

2. Critical assessment of the gains and drawbacks of the approaches of evaluating expenditure.

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

Recommendation: Using the measured IRR for the value above, it may be proposed to the

business previous chapter that they should embrace a new equipment as it would be

profitable to them. It is because for the above business, this investment will produce better

returns in the future.

2. Critical assessment of the gains and drawbacks of the approaches of evaluating expenditure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payback period: It can be defined as a form of investment valuation approach that is

associated with the mechanism of determining approximate time period to cover investment

costs. Just two considerations are listed under this approach that is economic resources and

savings (Ndanyenbah and Zakaria, 2019). This function facilitates the implementation of some

kind of proposal in the feature. As for Love well plc, this formula has been implemented and

specifies which certain project costs should be protected in 3.79 years ' time. This offers

administrators an idea of job productivity whether or not they can buy new equipment. This has

some advantages and risks which are:

Merits: As stated in the above section, it is simpler to apply this method which makes it

ideal for all types of businesses, including small or large. Along with under this process, project

effectiveness assessment can be conducted in less expense and time. However, which can be

used by any employee in an organisation, since this will not entail any special experience and

skills in accounting.

Demerits: There have been some disadvantages that make results less accurate, as

variables like net present value are overlooked under this system (Ayodele, 2019). Despite of

this, depending on generated result is problematic for consumers, because time worth of money

is one of the key considerations to remember when assessing a project. But also in this process,

capital expenditures in all periods are not included so cash flows in the existing years following

recovery in investment costs are overlooked.

ARR: This is another easy way of measuring expenditure. A calculation is used to

calculate the rate of return from which a project can deliver return in the future. Businesses take

reasonable steps to obtain any financial initiative on the basis of measured outcomes under this

framework (Godbole and Jayraj, 2019). Similar to the approach mentioned above, this often

requires little knowledge to provide the final result. As for Love-well plc, this approach was used

to calculate the expected yield rate of 25.56 %. This expectation of return directly leads to

executives in deciding whether or not they will consider a plan. Below some of the advantages

and demerits of this approach are described in this way:

Merits: This approach has a number of benefits and makes it common to use as

accounting income are being used under it when net cash flows towards project assessment are

considered in certain methods. This function makes implementation of the system more robust

associated with the mechanism of determining approximate time period to cover investment

costs. Just two considerations are listed under this approach that is economic resources and

savings (Ndanyenbah and Zakaria, 2019). This function facilitates the implementation of some

kind of proposal in the feature. As for Love well plc, this formula has been implemented and

specifies which certain project costs should be protected in 3.79 years ' time. This offers

administrators an idea of job productivity whether or not they can buy new equipment. This has

some advantages and risks which are:

Merits: As stated in the above section, it is simpler to apply this method which makes it

ideal for all types of businesses, including small or large. Along with under this process, project

effectiveness assessment can be conducted in less expense and time. However, which can be

used by any employee in an organisation, since this will not entail any special experience and

skills in accounting.

Demerits: There have been some disadvantages that make results less accurate, as

variables like net present value are overlooked under this system (Ayodele, 2019). Despite of

this, depending on generated result is problematic for consumers, because time worth of money

is one of the key considerations to remember when assessing a project. But also in this process,

capital expenditures in all periods are not included so cash flows in the existing years following

recovery in investment costs are overlooked.

ARR: This is another easy way of measuring expenditure. A calculation is used to

calculate the rate of return from which a project can deliver return in the future. Businesses take

reasonable steps to obtain any financial initiative on the basis of measured outcomes under this

framework (Godbole and Jayraj, 2019). Similar to the approach mentioned above, this often

requires little knowledge to provide the final result. As for Love-well plc, this approach was used

to calculate the expected yield rate of 25.56 %. This expectation of return directly leads to

executives in deciding whether or not they will consider a plan. Below some of the advantages

and demerits of this approach are described in this way:

Merits: This approach has a number of benefits and makes it common to use as

accounting income are being used under it when net cash flows towards project assessment are

considered in certain methods. This function makes implementation of the system more robust

and efficient Along with another good feature of this method is that this is convenient to use as it

is focused on formula estimation that everyone inside the company can execute.

Demerits: The ARR approach does not take into account the time value factor which is a

significant aspect. This renders judgments less successful and accurate (Bakri Bakri, 2019).

Beyond this, capital expenditures underneath it are totally neglected and are not so positive in

terms of a project's computational performance. And these are some of that method’s main

demerits.

Net present value: It is known as a process form which is used to measure a project's

current value. Within it, project current value is calculated by deducting investment balance from

expected cash flows of the respective years (Sinha and Datta, 2020). Under it, the discounted

cash flow valuation is calculated using the expected Present Value (PV) element. The process is

commonly known as NPV. This approach is applied throughout the sense of the aforementioned

business to figure out the total value of their planned machines. A few of the benefits and

demerits of this approach are described in this way below:

Merits: The main advantage of using this approach is that during the course of measuring

project's current valuation it includes time amount of money aspect. This allows it much more

proper and effective approach relative to the methods described above, as this aspect has been

overlooked in the above methods. Big positive point of this approach has been that it takes the

cash balances of all months to figure out the current project interest.

Demerits: The biggest downside to this approach is that it is difficult to implement

because of the capital cost-related assumptions. Including this presumption, the result makes

long-term judgments less accurate and successful. In relation to this, capital expenses for

measuring current project value are not included the same.

Internal return rate: this can be classified as a form of approach related to the process

of determining a project’s real return rate. This technique is called a type of approach that is too

difficult to use since strong accounting information is needed. Along with only those individuals

who have appropriate understanding about accounting will apply this form. With respect to the

above-mentioned business, accountants have made the transition to learn for the future about the

productivity of modern equipment. Many of the method’s benefits and demerits are described

below:

is focused on formula estimation that everyone inside the company can execute.

Demerits: The ARR approach does not take into account the time value factor which is a

significant aspect. This renders judgments less successful and accurate (Bakri Bakri, 2019).

Beyond this, capital expenditures underneath it are totally neglected and are not so positive in

terms of a project's computational performance. And these are some of that method’s main

demerits.

Net present value: It is known as a process form which is used to measure a project's

current value. Within it, project current value is calculated by deducting investment balance from

expected cash flows of the respective years (Sinha and Datta, 2020). Under it, the discounted

cash flow valuation is calculated using the expected Present Value (PV) element. The process is

commonly known as NPV. This approach is applied throughout the sense of the aforementioned

business to figure out the total value of their planned machines. A few of the benefits and

demerits of this approach are described in this way below:

Merits: The main advantage of using this approach is that during the course of measuring

project's current valuation it includes time amount of money aspect. This allows it much more

proper and effective approach relative to the methods described above, as this aspect has been

overlooked in the above methods. Big positive point of this approach has been that it takes the

cash balances of all months to figure out the current project interest.

Demerits: The biggest downside to this approach is that it is difficult to implement

because of the capital cost-related assumptions. Including this presumption, the result makes

long-term judgments less accurate and successful. In relation to this, capital expenses for

measuring current project value are not included the same.

Internal return rate: this can be classified as a form of approach related to the process

of determining a project’s real return rate. This technique is called a type of approach that is too

difficult to use since strong accounting information is needed. Along with only those individuals

who have appropriate understanding about accounting will apply this form. With respect to the

above-mentioned business, accountants have made the transition to learn for the future about the

productivity of modern equipment. Many of the method’s benefits and demerits are described

below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.