Financial Modeling Project: Investment Appraisal of a Tenant Property

VerifiedAdded on 2022/09/18

|29

|2685

|32

Project

AI Summary

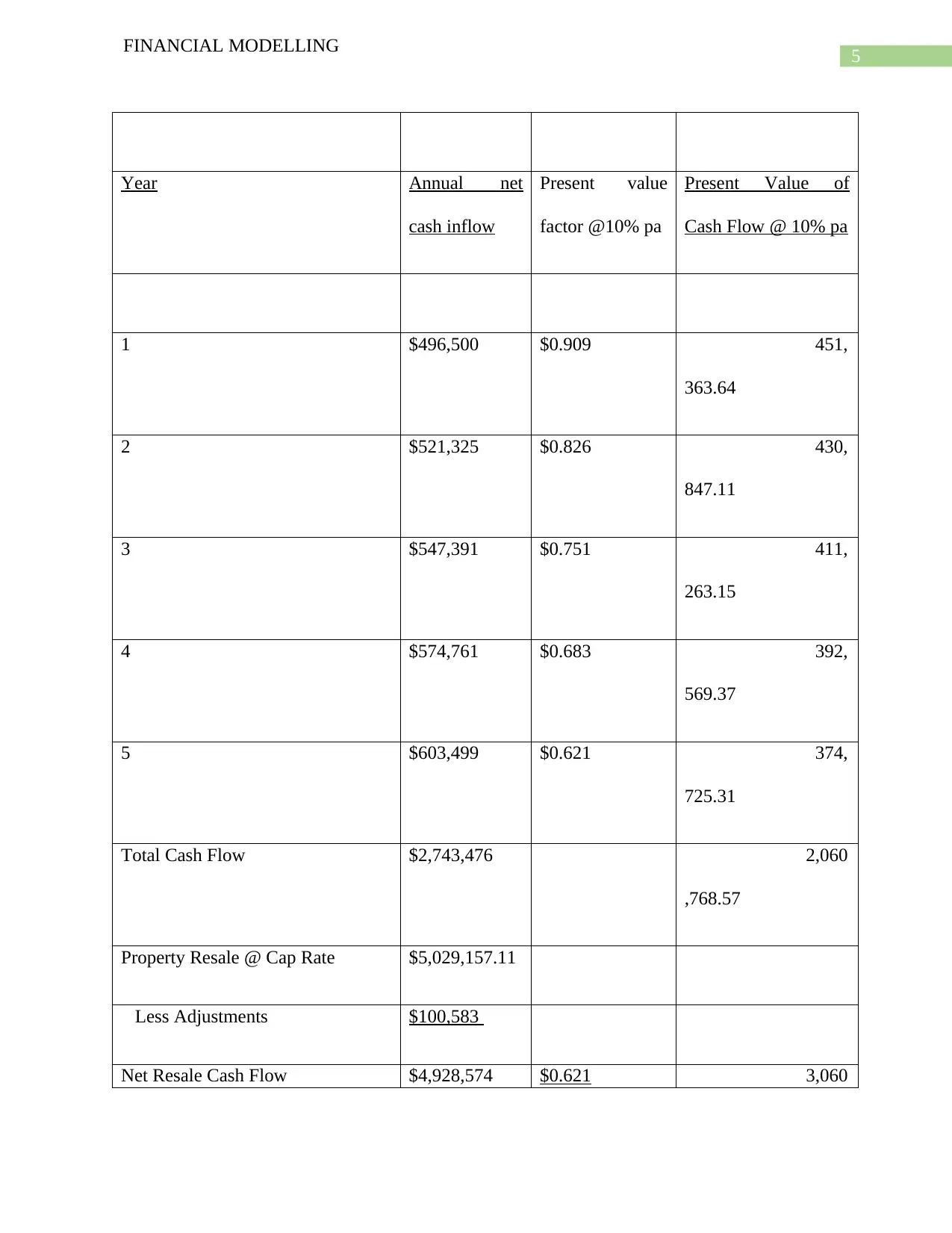

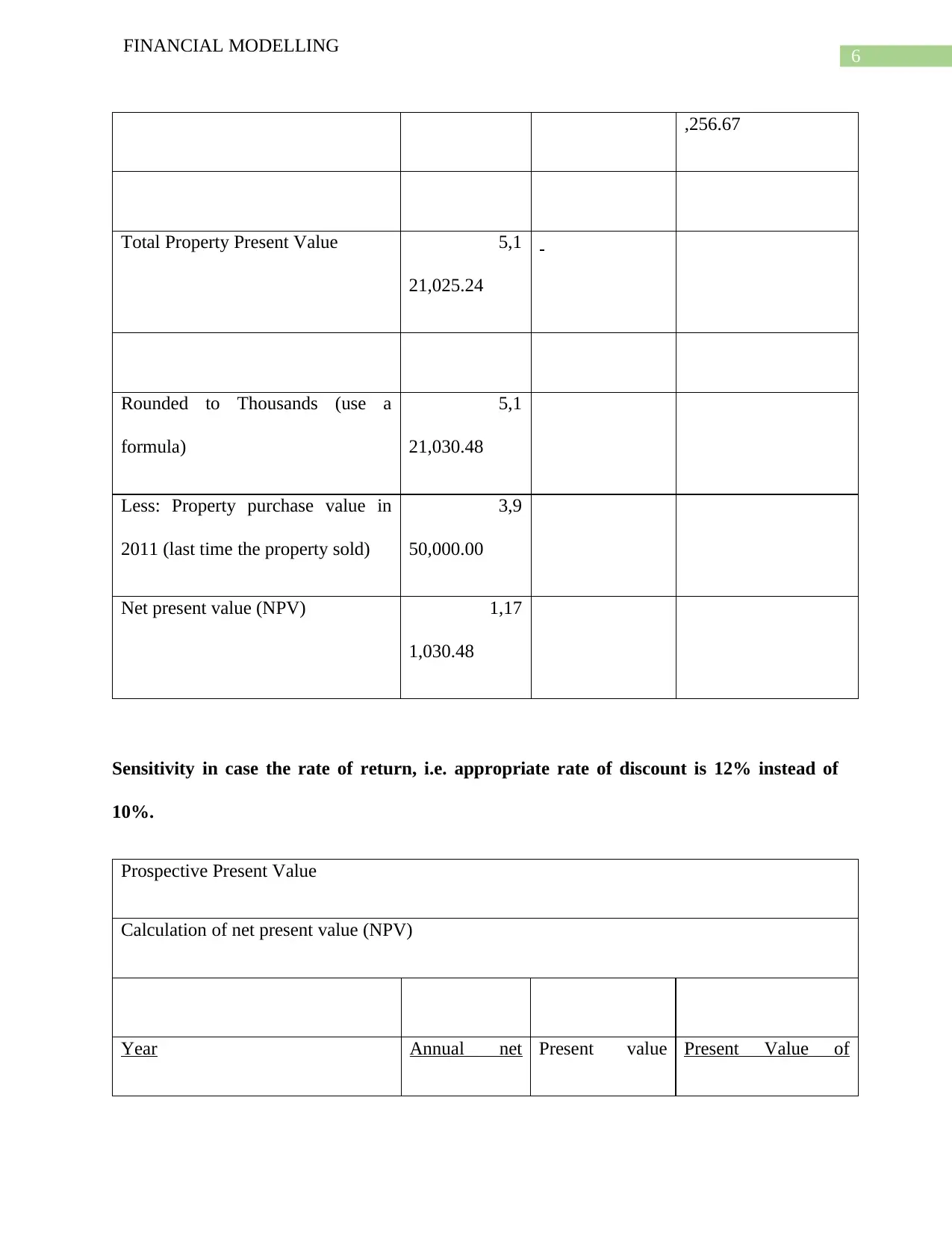

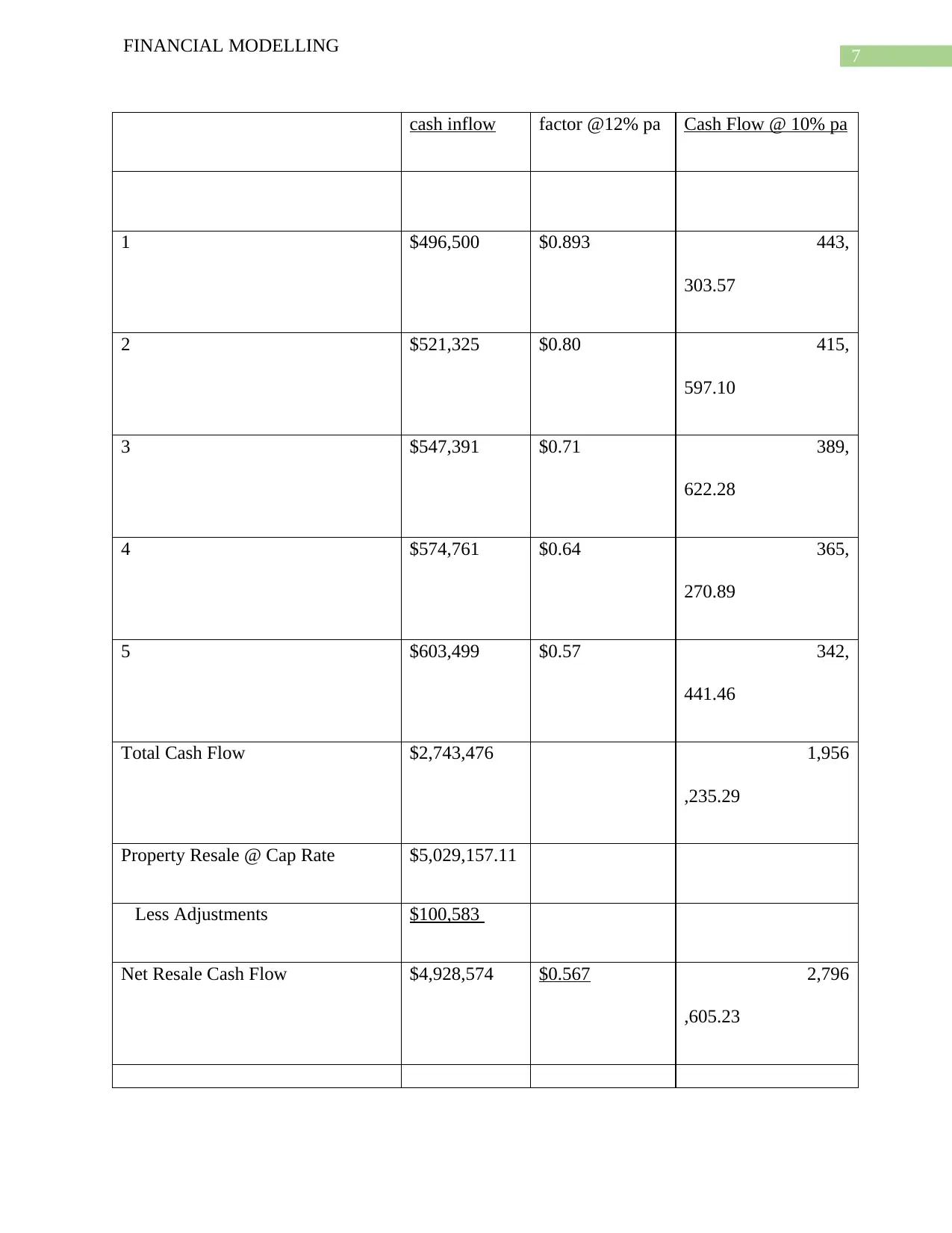

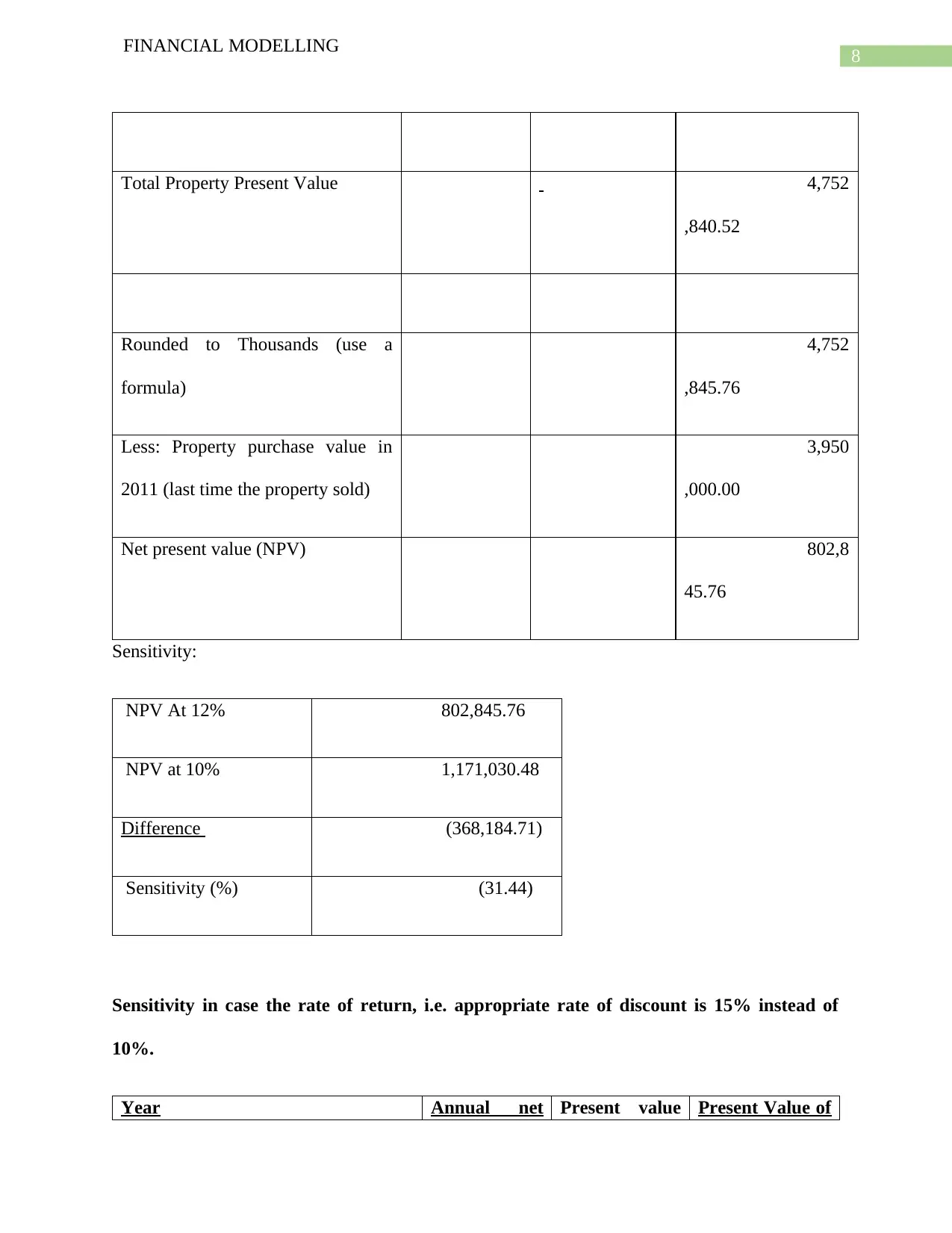

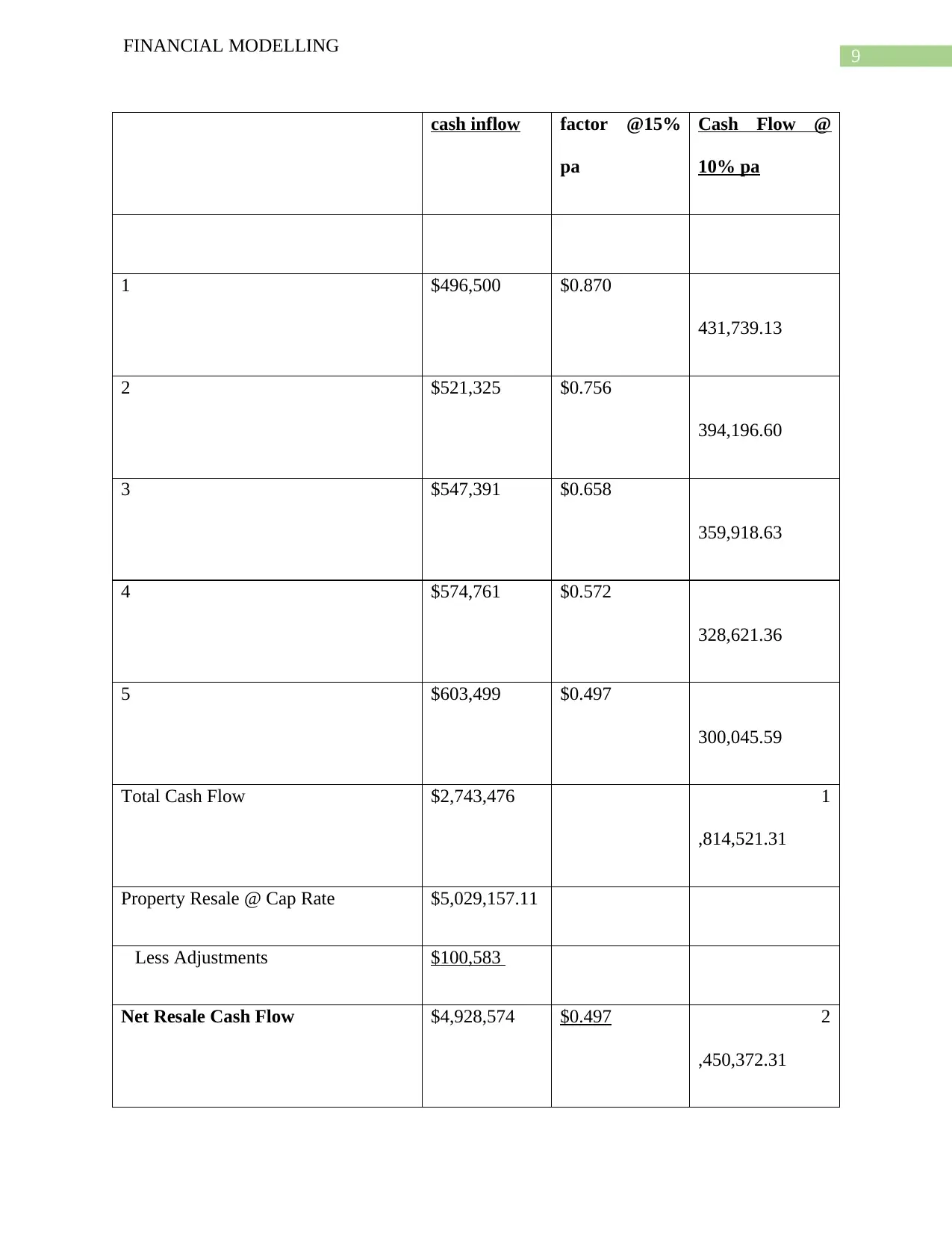

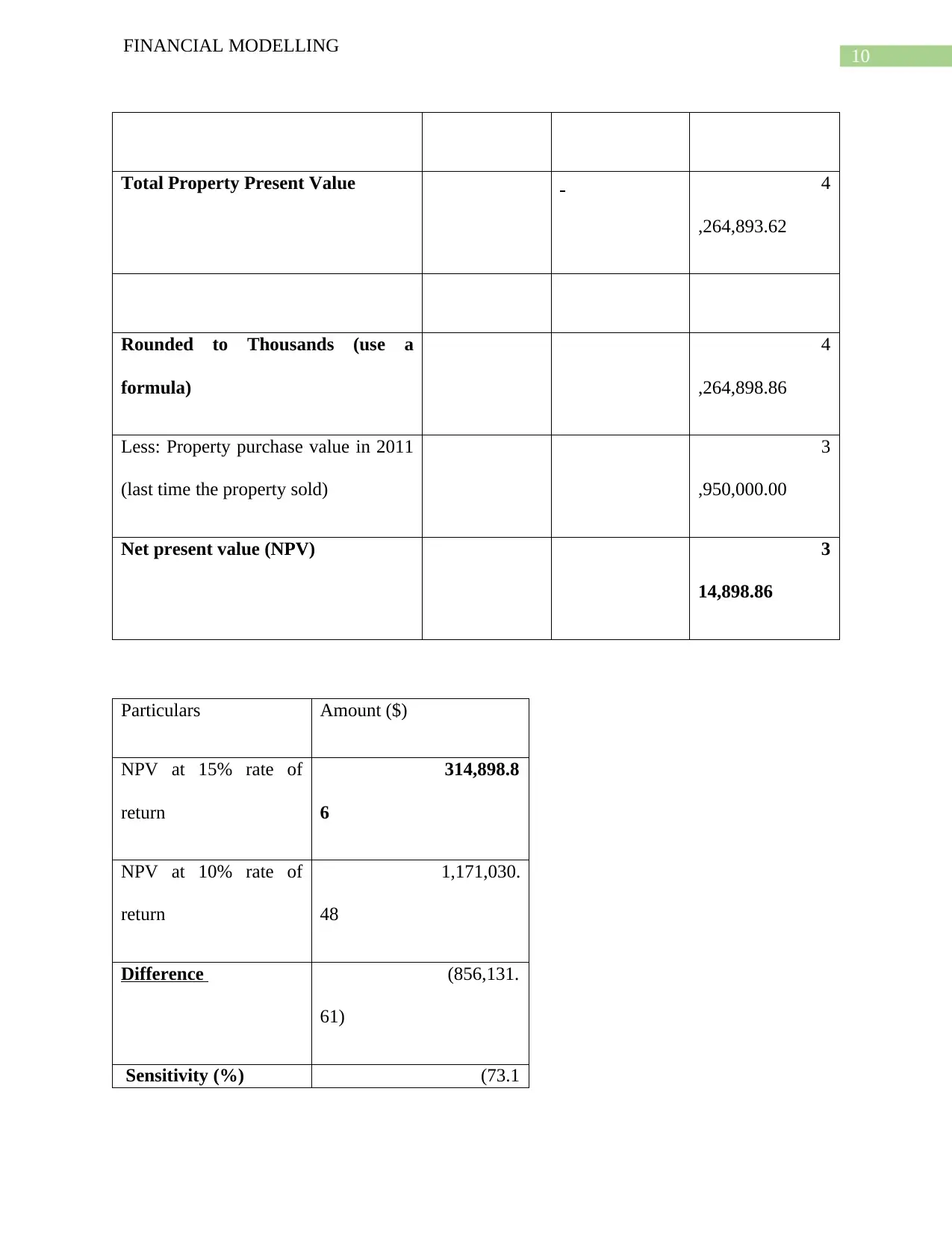

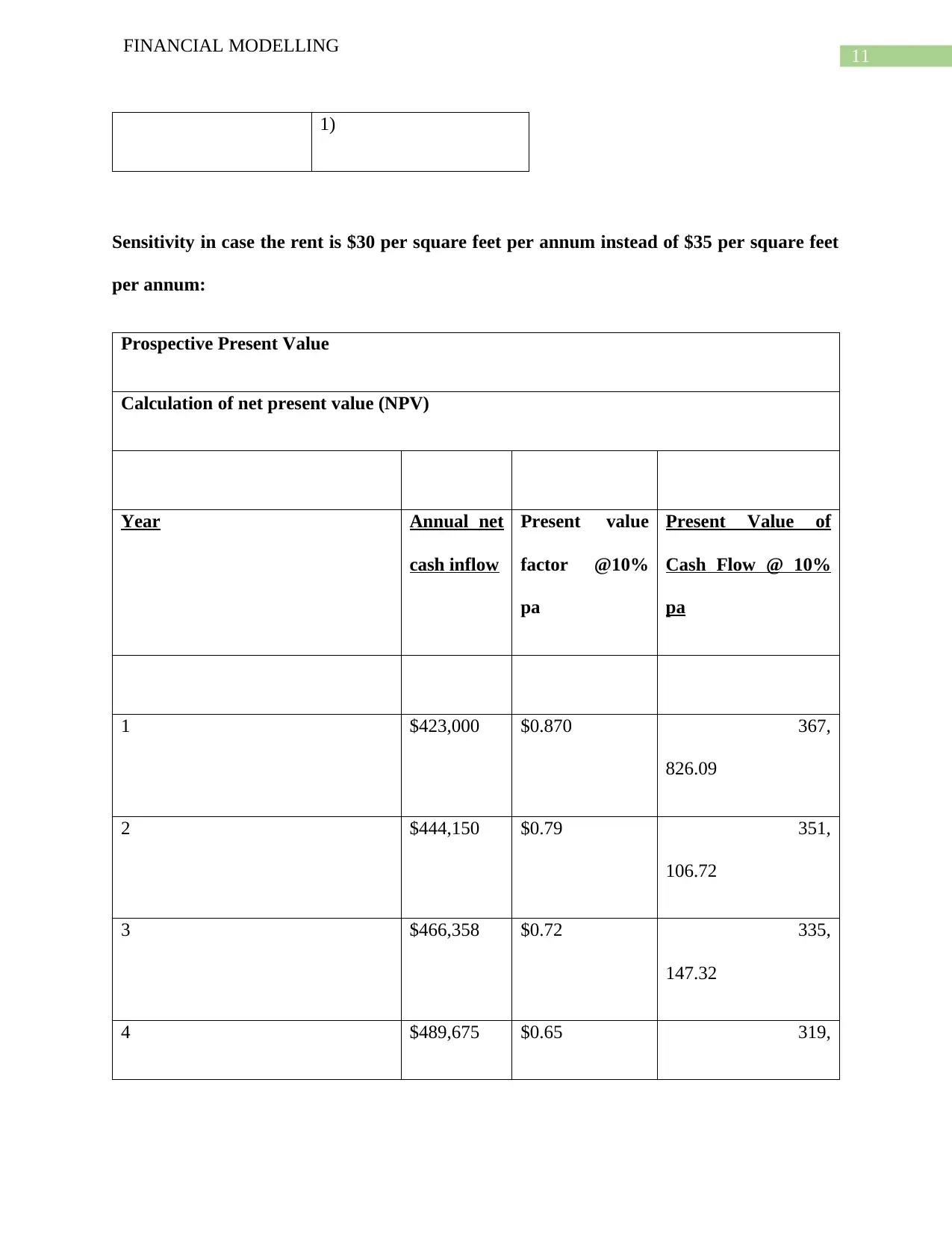

This document presents a comprehensive financial modeling project focused on the investment appraisal of a tenant property located at 104 Lake Popular Street, White City, Israel. The project includes detailed calculations to assess the sensitivity of the Net Present Value (NPV) to various underlying variables. The analysis considers factors such as rent, expenses, and the discount rate. Sensitivity analysis is performed by changing variables like the discount rate and rent per square foot. Simulation of a stochastic variable is used to analyze the impact of uncertain annual cash inflows. The project also covers pricing strategies, optimization using Excel, and the application of the Capital Asset Pricing Model (CAPM) to determine the cost of capital. The document highlights the advantages of financial modeling in making informed investment decisions by assessing potential outcomes under different market conditions. It uses a variety of financial modeling techniques to provide a detailed analysis of the investment's potential.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.