Managing Financial Resources: Investment Appraisal for PNJ Ltd

VerifiedAdded on 2023/04/22

|26

|5014

|487

Report

AI Summary

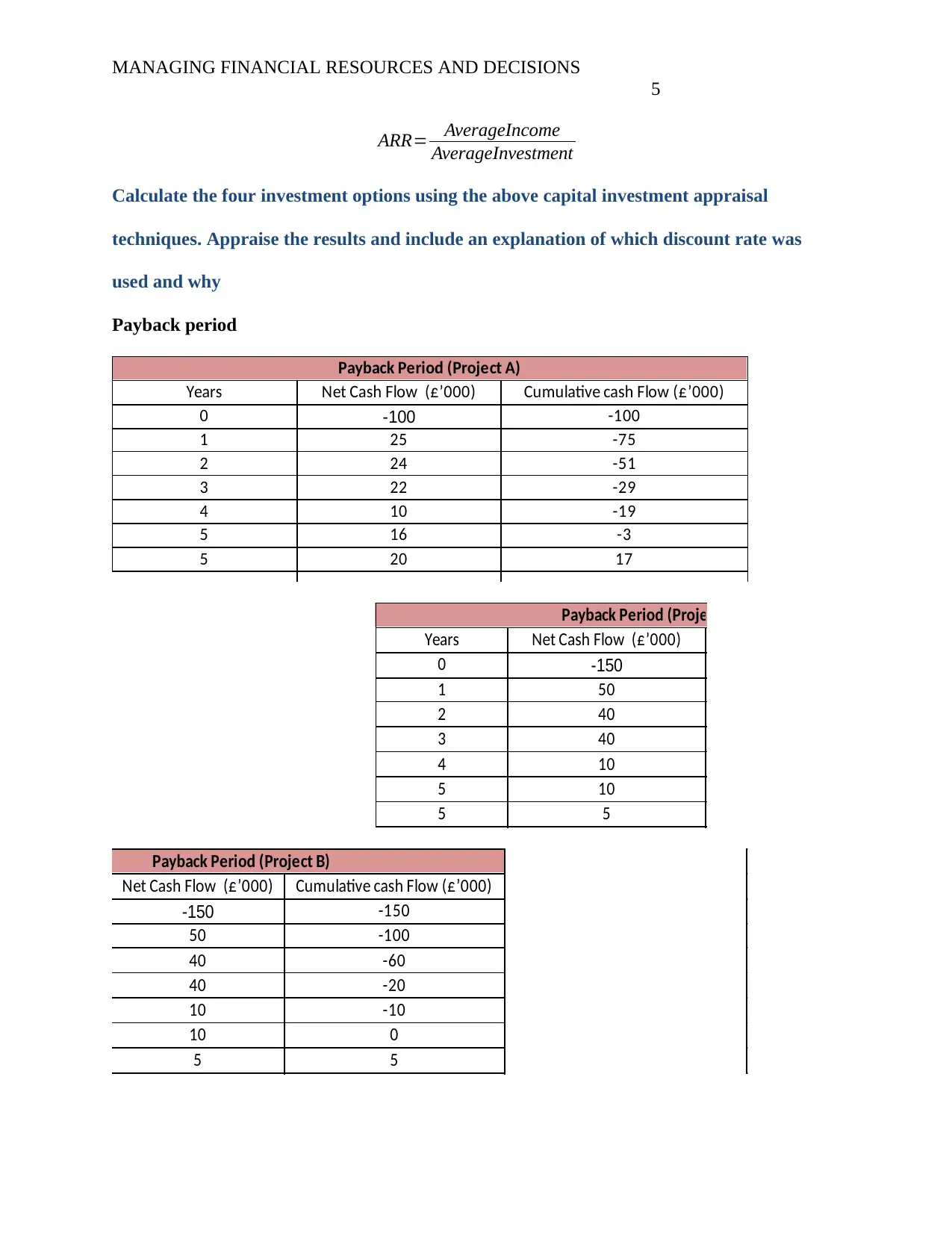

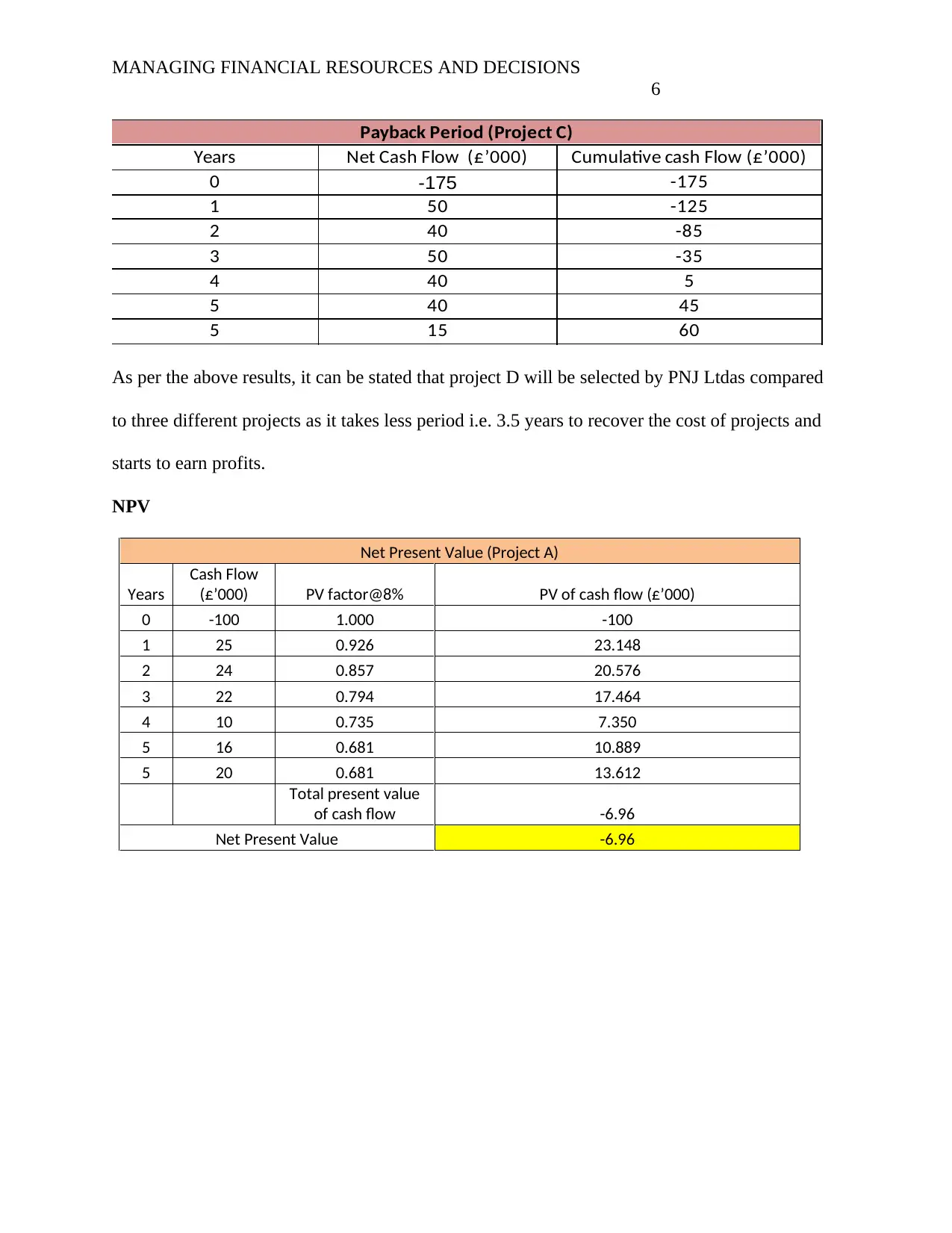

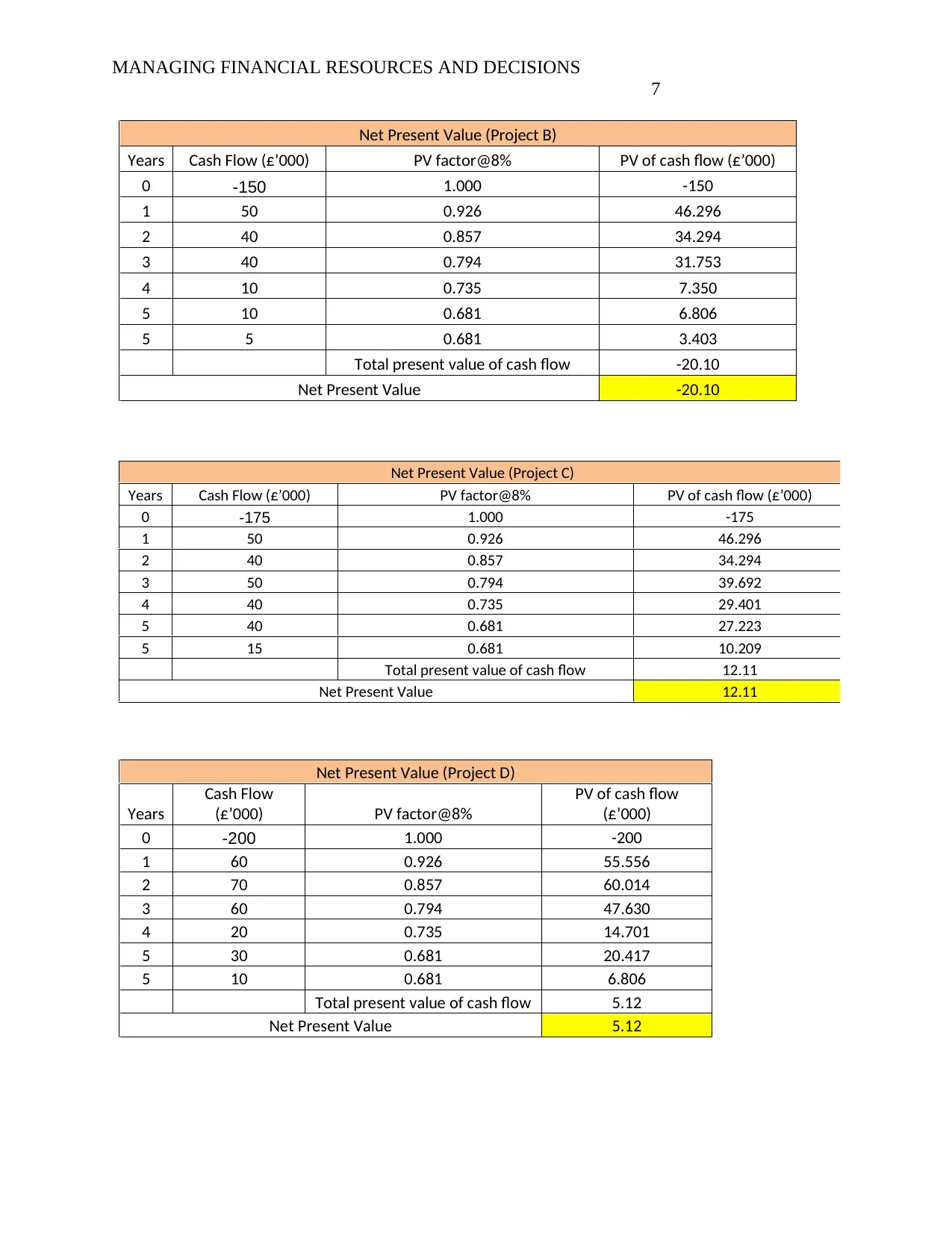

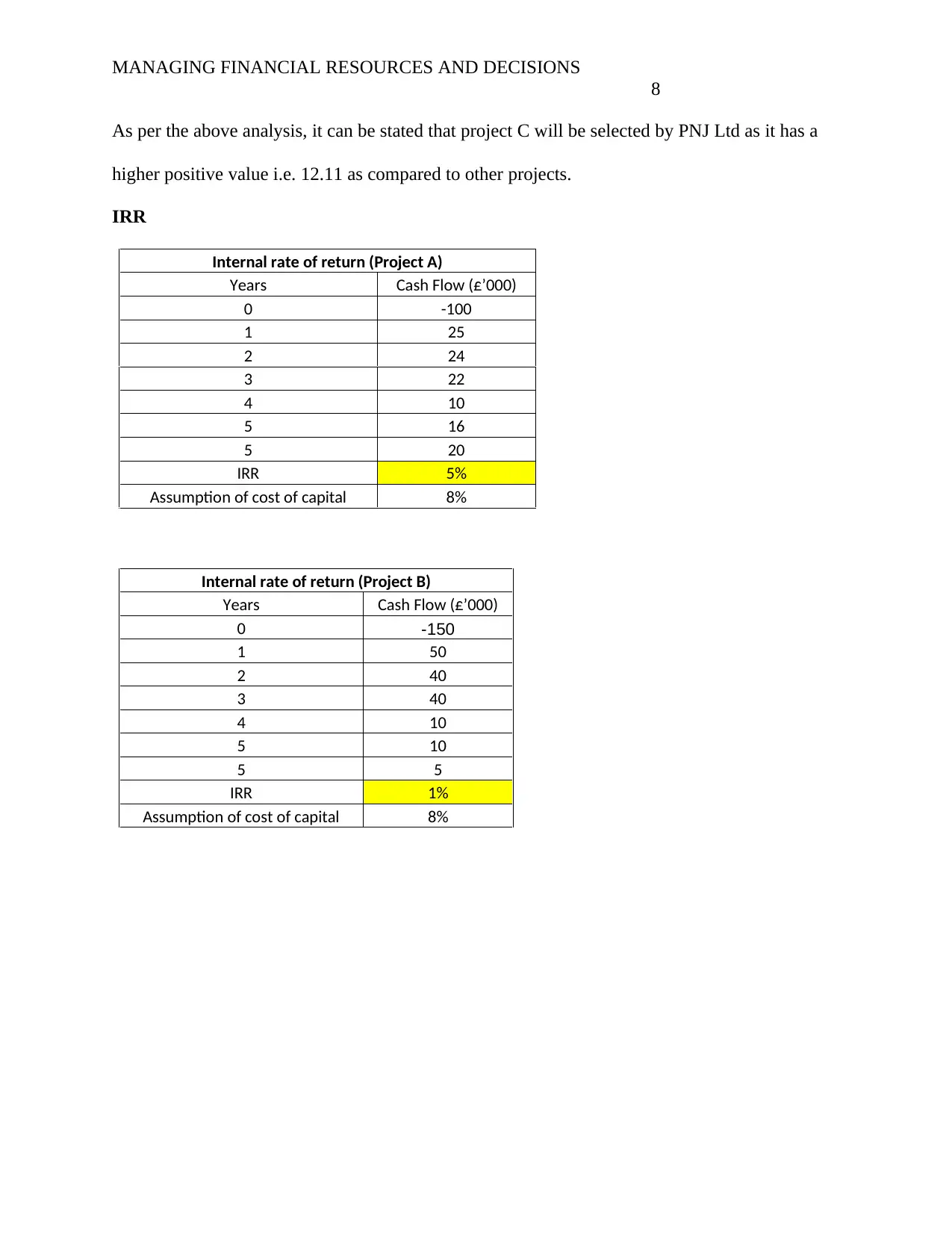

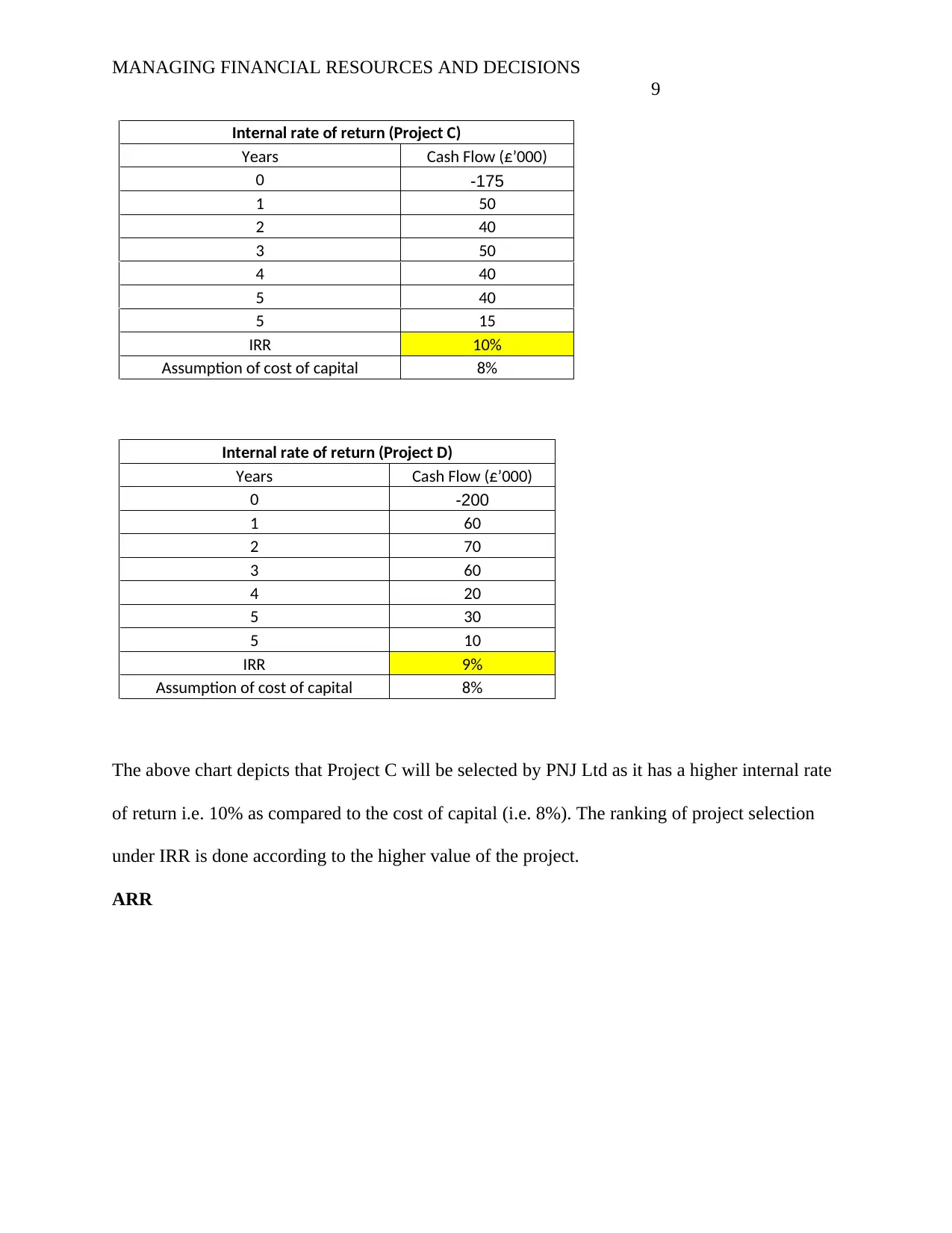

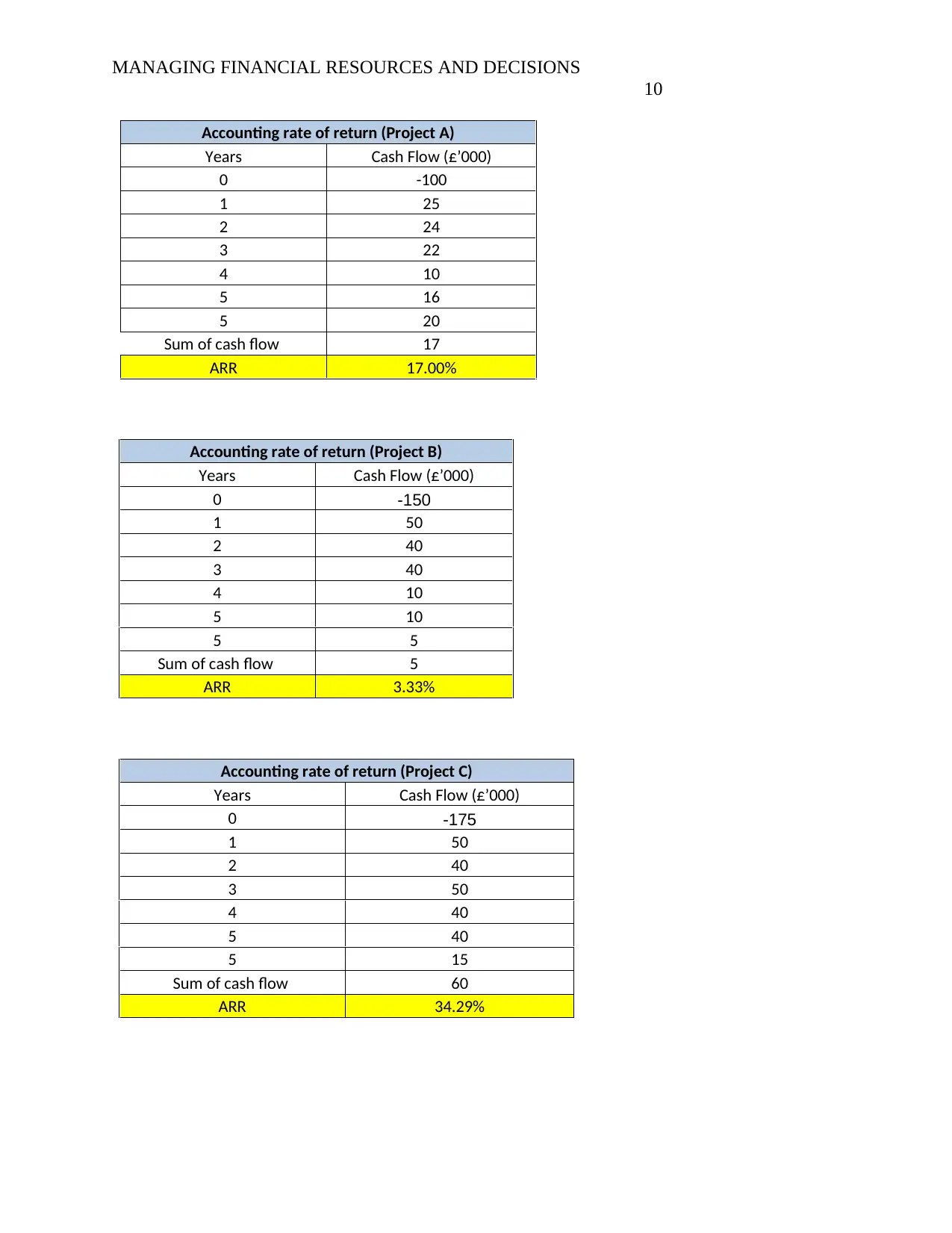

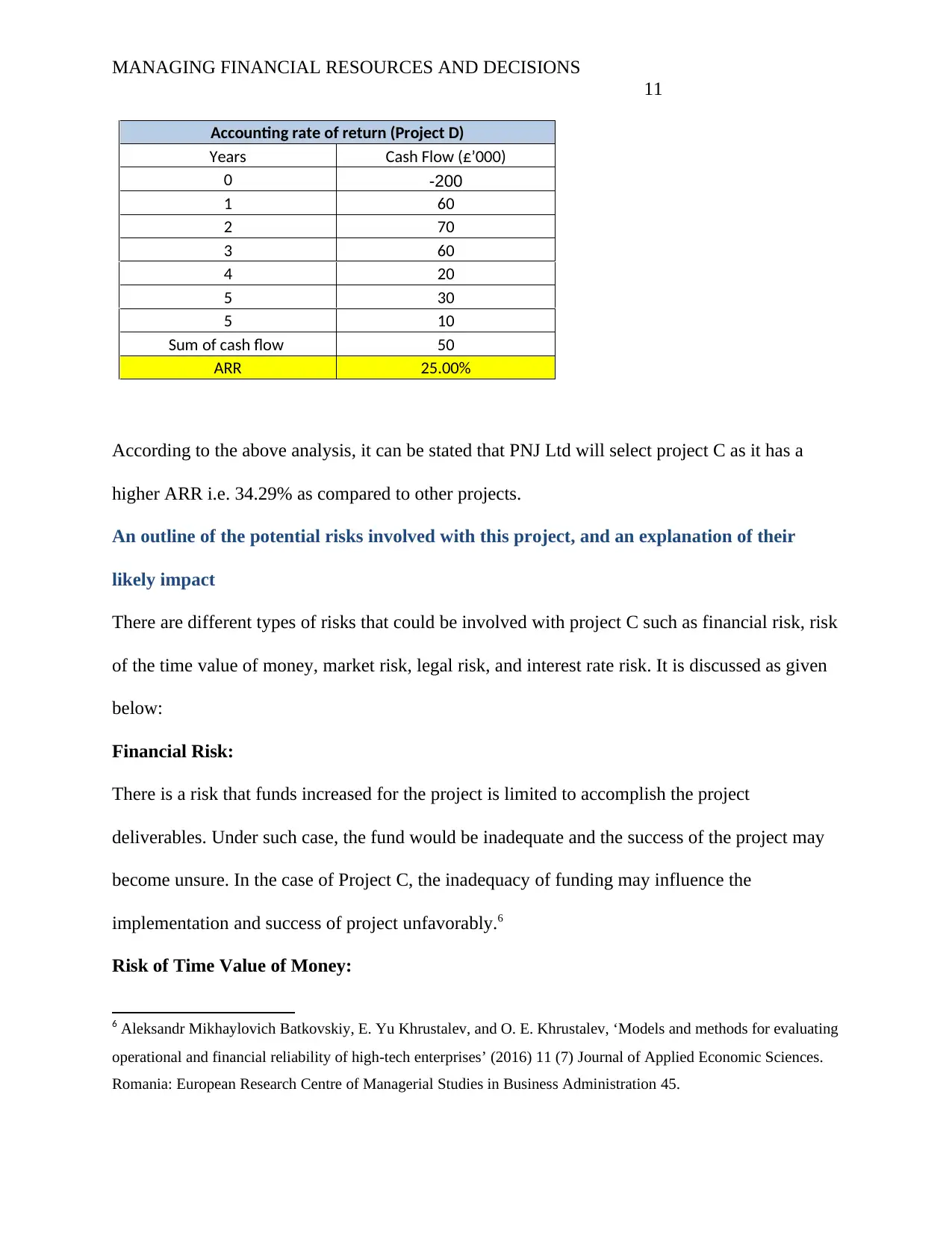

This report assesses capital investment appraisal techniques for PNJ Ltd, a wood products company evaluating replacement equipment. It explains and applies methods like Payback Period, Internal Rate of Return (IRR), Net Present Value (NPV), and Accounting Rate of Return (ARR) to four potential investment options (Projects A, B, C, and D). The analysis includes calculations and appraisals of each project, highlighting the discount rate used and its rationale. Furthermore, the report outlines potential risks associated with Project C, such as financial, market, legal, and interest rate risks, and their likely impact on management. Finally, it summarizes possible sources of funding for the project, detailing the advantages and disadvantages of each option. The document is available on Desklib, a platform offering study tools and solved assignments for students.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.