University Finance Module: Investment Appraisal Techniques Report

VerifiedAdded on 2021/06/17

|17

|4660

|38

Report

AI Summary

This report provides a comprehensive overview of investment appraisal techniques, essential for financial decision-making. It begins with an introduction to the concept of investment decisions and the factors influencing them, including cash flow, project life, and discounting factors. The report then delves into specific techniques such as Accounting Rate of Return (ARR), Payback Period, Net Present Value (NPV), and Internal Rate of Return (IRR), detailing their calculation methods, decision rules, merits, and demerits. A hypothetical investment scenario is presented, and the techniques are applied to determine the viability of the investment. The report concludes with a discussion of ethical considerations in financial decision-making and provides relevant references. The report offers a detailed analysis of each technique, making it a valuable resource for students studying finance and accounting.

Accounting and finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction................................................................................................................................3

Investment appraisal techniques................................................................................................3

Accounting rate of return.......................................................................................................3

Payback Period.......................................................................................................................4

Net present value....................................................................................................................6

Internal Rate of Return...........................................................................................................7

Investment scenario..................................................................................................................10

Application of investment appraisal techniques and conclusions............................................11

Calculations..........................................................................................................................11

Statement showing annual cash flow...............................................................................11

Accounting rate of return.................................................................................................11

Payback period.................................................................................................................11

Net present value..............................................................................................................12

Internal rate of return.......................................................................................................12

Decision................................................................................................................................13

Assumptions.........................................................................................................................13

Ethical considerations..............................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

Introduction................................................................................................................................3

Investment appraisal techniques................................................................................................3

Accounting rate of return.......................................................................................................3

Payback Period.......................................................................................................................4

Net present value....................................................................................................................6

Internal Rate of Return...........................................................................................................7

Investment scenario..................................................................................................................10

Application of investment appraisal techniques and conclusions............................................11

Calculations..........................................................................................................................11

Statement showing annual cash flow...............................................................................11

Accounting rate of return.................................................................................................11

Payback period.................................................................................................................11

Net present value..............................................................................................................12

Internal rate of return.......................................................................................................12

Decision................................................................................................................................13

Assumptions.........................................................................................................................13

Ethical considerations..............................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

INTRODUCTION

It is identified that the investment decision is based on the decision rule that is implemented

under different circumstances. Hence, the decision rule itself incorporated following listed

inputs

1) Cash Flow

2) Project Life

3) Discounting Factor

It is noted that the effectiveness of the decision emphasized on the proper assessment of all

three factors which requires being done in an effective manner. It is analyzed that cash flow

estimation needs an immense project understanding time before its implementation;

specifically the economy macro and micro view, the company, and polity. The life of the

project is essential to focus; because the entire prospect of the project will be affected or

change(Abor, 2017). Thus, a proper determination is needed to focus on having project life

estimation. It is noted that cost of capital is known as the discounting factor which has

determined a change over the years. It is due to the fact that capital cost has different

connotations in the perspective of different philosophies of the economy. Such as; India has

determined a change in the circumstance of Indian economic ideology to open economy from

the closed economy. Thus, it can be stated that capital cost carries out its high influence on

the evaluation of investment.

The present study is based on the description of crucial investment appraisal techniques by

considering its merits and demerits. Further, the hypothetical scenario will be created and

investment appraisal techniques will be applied to determine whether the investment is viable

or not. In the last part of study importance of ethical consideration will be analyzed in

financial decision proposed in the project.

INVESTMENT APPRAISAL TECHNIQUES

Accounting rate of return

It is identified that the investment decision is based on the decision rule that is implemented

under different circumstances. Hence, the decision rule itself incorporated following listed

inputs

1) Cash Flow

2) Project Life

3) Discounting Factor

It is noted that the effectiveness of the decision emphasized on the proper assessment of all

three factors which requires being done in an effective manner. It is analyzed that cash flow

estimation needs an immense project understanding time before its implementation;

specifically the economy macro and micro view, the company, and polity. The life of the

project is essential to focus; because the entire prospect of the project will be affected or

change(Abor, 2017). Thus, a proper determination is needed to focus on having project life

estimation. It is noted that cost of capital is known as the discounting factor which has

determined a change over the years. It is due to the fact that capital cost has different

connotations in the perspective of different philosophies of the economy. Such as; India has

determined a change in the circumstance of Indian economic ideology to open economy from

the closed economy. Thus, it can be stated that capital cost carries out its high influence on

the evaluation of investment.

The present study is based on the description of crucial investment appraisal techniques by

considering its merits and demerits. Further, the hypothetical scenario will be created and

investment appraisal techniques will be applied to determine whether the investment is viable

or not. In the last part of study importance of ethical consideration will be analyzed in

financial decision proposed in the project.

INVESTMENT APPRAISAL TECHNIQUES

Accounting rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The accounting rate of return is also elaborated as ROI (Return on Investment), it is a return

on capital employed consider as ROCE, and it used to follow accounting information instead

of cash flow.

Meaning; It is noted that term ARR is the average ratio focus after-tax profit and divided by

given average investment.

Computing Method;

there has been a number of the method used to compute the ARR. Thus the most used and

common method of computing ARR is done by the given formula;

ARR= Average Annual Profit After Tax/ Average Investment*100

Moreover, average after-tax profit is evaluated by adding Profit after Tax and divides the

total by each year numbers.

Decision Rule; The ARR is also used for the decision criterion in order to select the proposal

of investment (Bierman and Smidt, 2014). The diction rued defines information that if the

determined ARR is not less than the minimum rates set by the high official tends to accept

the project and ARR is not higher than the minimum rates set by the high official tends to

reject the project (Wei, 2018).

Merits:

It is a simple and easy method to compute the value

It is based on the accounting information which is familiar with ventures and information is

easily available

Demerits:

It is not based on the cash flow for project evaluation

It does not consider the valuation of monetary time value. Due to this, the benefits cannot be

valued at the part in early and later years.

It is focusing on profit averaging; however, it is taking into account all years

Payback Period

on capital employed consider as ROCE, and it used to follow accounting information instead

of cash flow.

Meaning; It is noted that term ARR is the average ratio focus after-tax profit and divided by

given average investment.

Computing Method;

there has been a number of the method used to compute the ARR. Thus the most used and

common method of computing ARR is done by the given formula;

ARR= Average Annual Profit After Tax/ Average Investment*100

Moreover, average after-tax profit is evaluated by adding Profit after Tax and divides the

total by each year numbers.

Decision Rule; The ARR is also used for the decision criterion in order to select the proposal

of investment (Bierman and Smidt, 2014). The diction rued defines information that if the

determined ARR is not less than the minimum rates set by the high official tends to accept

the project and ARR is not higher than the minimum rates set by the high official tends to

reject the project (Wei, 2018).

Merits:

It is a simple and easy method to compute the value

It is based on the accounting information which is familiar with ventures and information is

easily available

Demerits:

It is not based on the cash flow for project evaluation

It does not consider the valuation of monetary time value. Due to this, the benefits cannot be

valued at the part in early and later years.

It is focusing on profit averaging; however, it is taking into account all years

Payback Period

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According to the study of Sirinanda, (2018), payback period criterion is an approach to

evaluate and compare the initial cash outlay with the subsequent project annual cash flow. It

is used to determine the number of years requires recovering the starting investments (Jain,

Singh and Yadav, 2013). It is identified that using this approach means that having a payback

period shorter and project to be more attractive. However, the criterion of the project is based

on the project acceptance which is based on the period payable which might not be longer

than the tolerable duration which is decided by the organization at its own

It is determined that this approach is simple for May application, but it can take the

organization into wrong and useless investment decision which eventually causes the

substantial loss to the organization (Tangedahl and Manuel, 2014). One of its main

drawbacks is that the valuation of time money and cash flows after the payback period.

Meaning; it elaborated the number of years need to cover the outlay of original cash invested

in a project

Decision Rule; the payback period is used as a decision to have a selection investment

proposal (Bandy, 2014). It is evaluated that if the payback period less than maximum

acceptable payback period and if the payback period greater than maximum acceptable

payback period than reject the project.

This system can be utilized to contrast actual pay back, and a standard payback set up by the

administration regarding the most extreme time frame amid which the underlying speculation

must be recouped (Das, 2011). The standard PBP is controlled by administration subjectively

based on various factors, for example, the kind of venture, the apparent danger of the task and

so forth. PBP can be even utilized for positioning totally unrelated undertakings. The tasks

might be positioned by the length of PBP and the venture with the briefest PBP will be

chosen.

Merits:

It is a simple concept, and its application is east to consider

This method is cost-effective which does not need a lot of time in financial execution and

data handling

The methods help in managing risk. It focuses those project which generates the level of

substantial cash inflows in the present years and discriminates those project which elaborated

evaluate and compare the initial cash outlay with the subsequent project annual cash flow. It

is used to determine the number of years requires recovering the starting investments (Jain,

Singh and Yadav, 2013). It is identified that using this approach means that having a payback

period shorter and project to be more attractive. However, the criterion of the project is based

on the project acceptance which is based on the period payable which might not be longer

than the tolerable duration which is decided by the organization at its own

It is determined that this approach is simple for May application, but it can take the

organization into wrong and useless investment decision which eventually causes the

substantial loss to the organization (Tangedahl and Manuel, 2014). One of its main

drawbacks is that the valuation of time money and cash flows after the payback period.

Meaning; it elaborated the number of years need to cover the outlay of original cash invested

in a project

Decision Rule; the payback period is used as a decision to have a selection investment

proposal (Bandy, 2014). It is evaluated that if the payback period less than maximum

acceptable payback period and if the payback period greater than maximum acceptable

payback period than reject the project.

This system can be utilized to contrast actual pay back, and a standard payback set up by the

administration regarding the most extreme time frame amid which the underlying speculation

must be recouped (Das, 2011). The standard PBP is controlled by administration subjectively

based on various factors, for example, the kind of venture, the apparent danger of the task and

so forth. PBP can be even utilized for positioning totally unrelated undertakings. The tasks

might be positioned by the length of PBP and the venture with the briefest PBP will be

chosen.

Merits:

It is a simple concept, and its application is east to consider

This method is cost-effective which does not need a lot of time in financial execution and

data handling

The methods help in managing risk. It focuses those project which generates the level of

substantial cash inflows in the present years and discriminates those project which elaborated

the last year substantial inflows(Halpin and Senior, 2011). However, the Payback period

method is a useful method in order to weed out risky projects.

It is a liquidity method. It delivers an explanation to consider a project with a yearly

investment recovery.

Demerits:

It is not useful in the conservation of valuation of money. It is because the calculations in

payback for cash flow are used to add simply without any discount. Thus, in this way, the

most basic financial analysis principles have been violets which stipulate the cash flow and

its occurrence at a different point at the different time that can be added or subtract after the

consideration of suitable discounting or computing.

It used to ignore the cash flows beyond the payback period which leads towards the project

rejection that creates the substantial inflows in further years

Net present value

According to the study of Sirinanda,(2018), the technique of net present value is one of

discounted time-adjusted and cash flow techniques. It determines that the streaming of cash

flow at a different time interval in terms of value and it can be computed when the values are

expressed in terms of common denominator which is known as present value.

Meaning; The Net Present Value is the state of differentiation between the present value of

the future cash inflows and the present value of the initial outlay which is discounted at the

capital cost of organization (Harris and Mongiello, 2012). The process to determine the

present values is consist of two stages; one stage is based on the involvement of appropriate

determination of discount rate, and in the second stage with the selection of discount rate , the

cash flow streams have been converted into present value

The calculation of Net Present Value is done with the help of the following equation

The NPV can be calculated with the help of equation.

NPV = Present value of cash inflows – Initial investment

Decision Rule:

method is a useful method in order to weed out risky projects.

It is a liquidity method. It delivers an explanation to consider a project with a yearly

investment recovery.

Demerits:

It is not useful in the conservation of valuation of money. It is because the calculations in

payback for cash flow are used to add simply without any discount. Thus, in this way, the

most basic financial analysis principles have been violets which stipulate the cash flow and

its occurrence at a different point at the different time that can be added or subtract after the

consideration of suitable discounting or computing.

It used to ignore the cash flows beyond the payback period which leads towards the project

rejection that creates the substantial inflows in further years

Net present value

According to the study of Sirinanda,(2018), the technique of net present value is one of

discounted time-adjusted and cash flow techniques. It determines that the streaming of cash

flow at a different time interval in terms of value and it can be computed when the values are

expressed in terms of common denominator which is known as present value.

Meaning; The Net Present Value is the state of differentiation between the present value of

the future cash inflows and the present value of the initial outlay which is discounted at the

capital cost of organization (Harris and Mongiello, 2012). The process to determine the

present values is consist of two stages; one stage is based on the involvement of appropriate

determination of discount rate, and in the second stage with the selection of discount rate , the

cash flow streams have been converted into present value

The calculation of Net Present Value is done with the help of the following equation

The NPV can be calculated with the help of equation.

NPV = Present value of cash inflows – Initial investment

Decision Rule:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The acceptance and rejection criterion of the project can be done by using the present value

method. The present value of the future cash inflows has been determined by the present

value of the initial outlay. Henceforth, the present value outlay is the same as the investment

at the initial stage (Tantisuvanichkul, 2014). However, if Net Present Value that is greater

than zero than project will be accepted and f Net Present Value that is less than zero than

project will be rejected. The accept and reject criterion can symbolically be shown as follows

PV > C → Accept [NPV > 0]

PV < C → Reject [NPV < 0]

Where the term C is denoted as outlay and PV is the present value

This strategy can be utilized to choose between mutually exclusive projects. With the

utilizing NPV, the task with the most elevated positive NPV would be positioned first, and

that venture would be chosen accordingly (Collier, 2015). The market estimation of the

association's offer will increment if ventures with positive NPVs are acknowledged.

Merits:

The most significant advantage of the net present value method comprised of the idea that the

receiving of dollars in future are worth less than today dollars rate saved in banks. The cash

flow from future years has been back to the stage to find out the present years’ worth

The dollar amount has been produced by NPV method which demonstrates that how much

value is created by the project for the organization (Droms and Wright, 2015). It will also

help stockholder to determine that how much a project will contribute to greater value

The Net Present Value Calculation uses a company capital cost as the discounted rate which

is considered as the minimum return rate that is the essential requirement of the company

investment

Demerits:

The main issue with the utilization of NPV is that it needs to guess the amount of future cash

flows and estimation for the company capital cost.

It is not an applicable method in order to compare the projects having a different amount of

investment. A larger project that requires more money they demonstrate the higher Net

method. The present value of the future cash inflows has been determined by the present

value of the initial outlay. Henceforth, the present value outlay is the same as the investment

at the initial stage (Tantisuvanichkul, 2014). However, if Net Present Value that is greater

than zero than project will be accepted and f Net Present Value that is less than zero than

project will be rejected. The accept and reject criterion can symbolically be shown as follows

PV > C → Accept [NPV > 0]

PV < C → Reject [NPV < 0]

Where the term C is denoted as outlay and PV is the present value

This strategy can be utilized to choose between mutually exclusive projects. With the

utilizing NPV, the task with the most elevated positive NPV would be positioned first, and

that venture would be chosen accordingly (Collier, 2015). The market estimation of the

association's offer will increment if ventures with positive NPVs are acknowledged.

Merits:

The most significant advantage of the net present value method comprised of the idea that the

receiving of dollars in future are worth less than today dollars rate saved in banks. The cash

flow from future years has been back to the stage to find out the present years’ worth

The dollar amount has been produced by NPV method which demonstrates that how much

value is created by the project for the organization (Droms and Wright, 2015). It will also

help stockholder to determine that how much a project will contribute to greater value

The Net Present Value Calculation uses a company capital cost as the discounted rate which

is considered as the minimum return rate that is the essential requirement of the company

investment

Demerits:

The main issue with the utilization of NPV is that it needs to guess the amount of future cash

flows and estimation for the company capital cost.

It is not an applicable method in order to compare the projects having a different amount of

investment. A larger project that requires more money they demonstrate the higher Net

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Present Value, but it is not necessary that it will be a better investment as compared to other

small projects. In this case, the organization may have other quality factors to be considered.

It is not easy to implement Net Present Value approach when comparing the projects having

different life spans (Ricmand, 2018).

Internal Rate of Return

The internal rate of return is also considered as the investment yield, marginal capital

efficiency, marginal capital productivity, time adjusted rate of return, return rate and so on. It

is also known as the time valuation money by focusing the discounted streams of cash flow

such as Net Present Value. In addition to this, in order to compute the required rate of return

and to find out the cash flows and inflows present value and the outflow are not kept under

consideration (DeFusco, 2015). In any case, the IRR depends totally on the underlying cost

and the money continues of the ventures which are being assessed for acknowledgement or

dismissal. It is, subsequently, alluded to as the inner rate of return. The IRR is generally the

rate of restore that a venture acquires or acknowledged.

Meaning

The internal rate of return (IRR) is the rebate rate that compares the NPV of a speculation

opportunity with Rs.0 (in light of the fact that the present estimation of money inflows

measures up to the underlying venture). It is the compound yearly rate of restore that the firm

will procure in the event that it puts resources into the task and gets the given inflows of cash

Criteria Explanations

IRR = r

Where IRR represents the internal rate of

project

And,

Ris equal to the required return of the firm

Project acceptance

The Net Present Value of Project is equal to

the 0

It is noted that by the time the IRR of the

project equal to the required rate of an

organization (r) the project acceptance will

neither increase and decrease the value of

the organization

small projects. In this case, the organization may have other quality factors to be considered.

It is not easy to implement Net Present Value approach when comparing the projects having

different life spans (Ricmand, 2018).

Internal Rate of Return

The internal rate of return is also considered as the investment yield, marginal capital

efficiency, marginal capital productivity, time adjusted rate of return, return rate and so on. It

is also known as the time valuation money by focusing the discounted streams of cash flow

such as Net Present Value. In addition to this, in order to compute the required rate of return

and to find out the cash flows and inflows present value and the outflow are not kept under

consideration (DeFusco, 2015). In any case, the IRR depends totally on the underlying cost

and the money continues of the ventures which are being assessed for acknowledgement or

dismissal. It is, subsequently, alluded to as the inner rate of return. The IRR is generally the

rate of restore that a venture acquires or acknowledged.

Meaning

The internal rate of return (IRR) is the rebate rate that compares the NPV of a speculation

opportunity with Rs.0 (in light of the fact that the present estimation of money inflows

measures up to the underlying venture). It is the compound yearly rate of restore that the firm

will procure in the event that it puts resources into the task and gets the given inflows of cash

Criteria Explanations

IRR = r

Where IRR represents the internal rate of

project

And,

Ris equal to the required return of the firm

Project acceptance

The Net Present Value of Project is equal to

the 0

It is noted that by the time the IRR of the

project equal to the required rate of an

organization (r) the project acceptance will

neither increase and decrease the value of

the organization

It is observed that the project rejection will

lead into the opportunity loss of the unused

fund of an organization which causes the

comparable decrease in the value of the firm

within the market (Chen and et al., 2018).

However, the opportunity loss of the unused

fund of an organization is equal to the

required return rate of an organization

IRR greater than r Project acceptance

The Net Present Value of Project is greater

than to the 0

Project acceptance will lead to the better

market value and also the better shareholder

value

The increase in magnitude value of the

organization is equal to the NPV of the

projects

IRR greater than r Project rejected

The Net Present Value of Project is less than

to the 0

The project rejection will in favour of the

organization in terms of saving the

organization intrinsic value and wellness of

the stakeholders (Kerzner and Kerzner,

2017).

Merits:

lead into the opportunity loss of the unused

fund of an organization which causes the

comparable decrease in the value of the firm

within the market (Chen and et al., 2018).

However, the opportunity loss of the unused

fund of an organization is equal to the

required return rate of an organization

IRR greater than r Project acceptance

The Net Present Value of Project is greater

than to the 0

Project acceptance will lead to the better

market value and also the better shareholder

value

The increase in magnitude value of the

organization is equal to the NPV of the

projects

IRR greater than r Project rejected

The Net Present Value of Project is less than

to the 0

The project rejection will in favour of the

organization in terms of saving the

organization intrinsic value and wellness of

the stakeholders (Kerzner and Kerzner,

2017).

Merits:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The time value of the money it considers and the total cash flow is generated over the project

life of any project

The NPV is consistent with the business objectives and maximizes the wealth of shareholders

Demerits:

It needs to be done under lengthy and complicated calculation

The calculation will results in the multiple IRRs when there is no conventional cash flow

determined (Gulam, 2018).

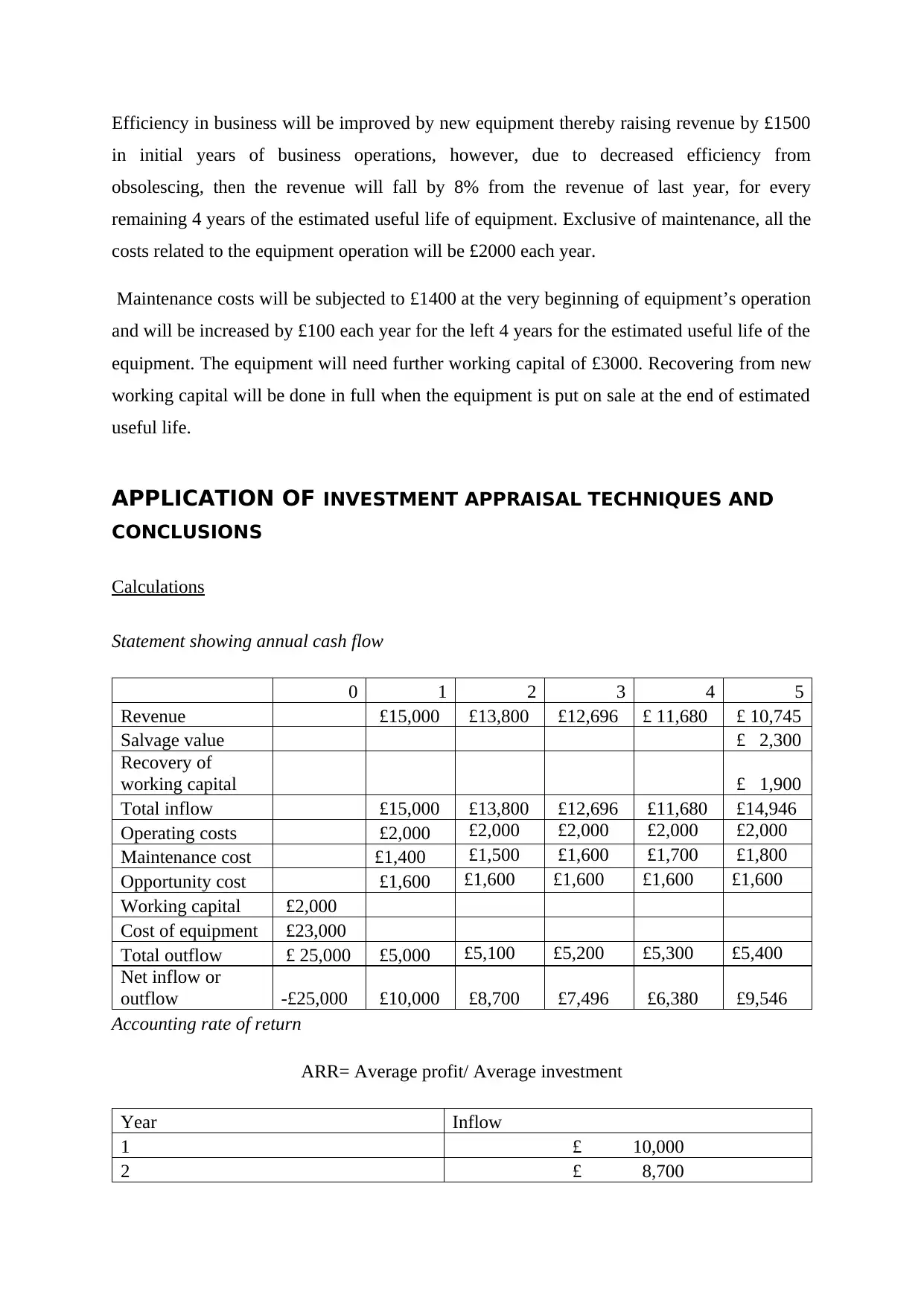

INVESTMENT SCENARIO

Option 1

£

Manufacturing limited

Installation of equipment will do in the building which is owned by Manufacturing Ltd but is

not utilized currently, in case the project is not continued, then the building will be put on a

rental basis for £1600 per year.

Further, a feasibility study has been conducted for the purchase of new die casting machine.

The preparation cost meant for feasibility study will be £5000.

It is indicated by management that the highest agreeable Payback Period for Manufacturing

Ltd will be 5 years. Further, they also indicated that each cash outflow at the starting stage of

project, inclusive of any increment in the working capital and another outflow of funds must

be recovered from the free cash flow of projects in the time period of maximum 5 years, for

getting the project acceptable in accordance with the Payback Period method. Cost of capital

is 10%.

The cost of equipment will be £23000 and is likely to have an estimated useful life of 5 years,

and straight –line based depreciation will be done to a nil book value. Further, the equipment

is likely to have a recovered value of £2300 with the end of 5 years.

life of any project

The NPV is consistent with the business objectives and maximizes the wealth of shareholders

Demerits:

It needs to be done under lengthy and complicated calculation

The calculation will results in the multiple IRRs when there is no conventional cash flow

determined (Gulam, 2018).

INVESTMENT SCENARIO

Option 1

£

Manufacturing limited

Installation of equipment will do in the building which is owned by Manufacturing Ltd but is

not utilized currently, in case the project is not continued, then the building will be put on a

rental basis for £1600 per year.

Further, a feasibility study has been conducted for the purchase of new die casting machine.

The preparation cost meant for feasibility study will be £5000.

It is indicated by management that the highest agreeable Payback Period for Manufacturing

Ltd will be 5 years. Further, they also indicated that each cash outflow at the starting stage of

project, inclusive of any increment in the working capital and another outflow of funds must

be recovered from the free cash flow of projects in the time period of maximum 5 years, for

getting the project acceptable in accordance with the Payback Period method. Cost of capital

is 10%.

The cost of equipment will be £23000 and is likely to have an estimated useful life of 5 years,

and straight –line based depreciation will be done to a nil book value. Further, the equipment

is likely to have a recovered value of £2300 with the end of 5 years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Efficiency in business will be improved by new equipment thereby raising revenue by £1500

in initial years of business operations, however, due to decreased efficiency from

obsolescing, then the revenue will fall by 8% from the revenue of last year, for every

remaining 4 years of the estimated useful life of equipment. Exclusive of maintenance, all the

costs related to the equipment operation will be £2000 each year.

Maintenance costs will be subjected to £1400 at the very beginning of equipment’s operation

and will be increased by £100 each year for the left 4 years for the estimated useful life of the

equipment. The equipment will need further working capital of £3000. Recovering from new

working capital will be done in full when the equipment is put on sale at the end of estimated

useful life.

APPLICATION OF INVESTMENT APPRAISAL TECHNIQUES AND

CONCLUSIONS

Calculations

Statement showing annual cash flow

0 1 2 3 4 5

Revenue £15,000 £13,800 £12,696 £ 11,680 £ 10,745

Salvage value £ 2,300

Recovery of

working capital £ 1,900

Total inflow £15,000 £13,800 £12,696 £11,680 £14,946

Operating costs £2,000 £2,000 £2,000 £2,000 £2,000

Maintenance cost £1,400 £1,500 £1,600 £1,700 £1,800

Opportunity cost £1,600 £1,600 £1,600 £1,600 £1,600

Working capital £2,000

Cost of equipment £23,000

Total outflow £ 25,000 £5,000 £5,100 £5,200 £5,300 £5,400

Net inflow or

outflow -£25,000 £10,000 £8,700 £7,496 £6,380 £9,546

Accounting rate of return

ARR= Average profit/ Average investment

Year Inflow

1 £ 10,000

2 £ 8,700

in initial years of business operations, however, due to decreased efficiency from

obsolescing, then the revenue will fall by 8% from the revenue of last year, for every

remaining 4 years of the estimated useful life of equipment. Exclusive of maintenance, all the

costs related to the equipment operation will be £2000 each year.

Maintenance costs will be subjected to £1400 at the very beginning of equipment’s operation

and will be increased by £100 each year for the left 4 years for the estimated useful life of the

equipment. The equipment will need further working capital of £3000. Recovering from new

working capital will be done in full when the equipment is put on sale at the end of estimated

useful life.

APPLICATION OF INVESTMENT APPRAISAL TECHNIQUES AND

CONCLUSIONS

Calculations

Statement showing annual cash flow

0 1 2 3 4 5

Revenue £15,000 £13,800 £12,696 £ 11,680 £ 10,745

Salvage value £ 2,300

Recovery of

working capital £ 1,900

Total inflow £15,000 £13,800 £12,696 £11,680 £14,946

Operating costs £2,000 £2,000 £2,000 £2,000 £2,000

Maintenance cost £1,400 £1,500 £1,600 £1,700 £1,800

Opportunity cost £1,600 £1,600 £1,600 £1,600 £1,600

Working capital £2,000

Cost of equipment £23,000

Total outflow £ 25,000 £5,000 £5,100 £5,200 £5,300 £5,400

Net inflow or

outflow -£25,000 £10,000 £8,700 £7,496 £6,380 £9,546

Accounting rate of return

ARR= Average profit/ Average investment

Year Inflow

1 £ 10,000

2 £ 8,700

3 £ 7,496

4 £ 6,380

5 £ 9,546

Average of Net inflow £ 8,424.44

Initial investment £ 25,000.00

ARR 34%

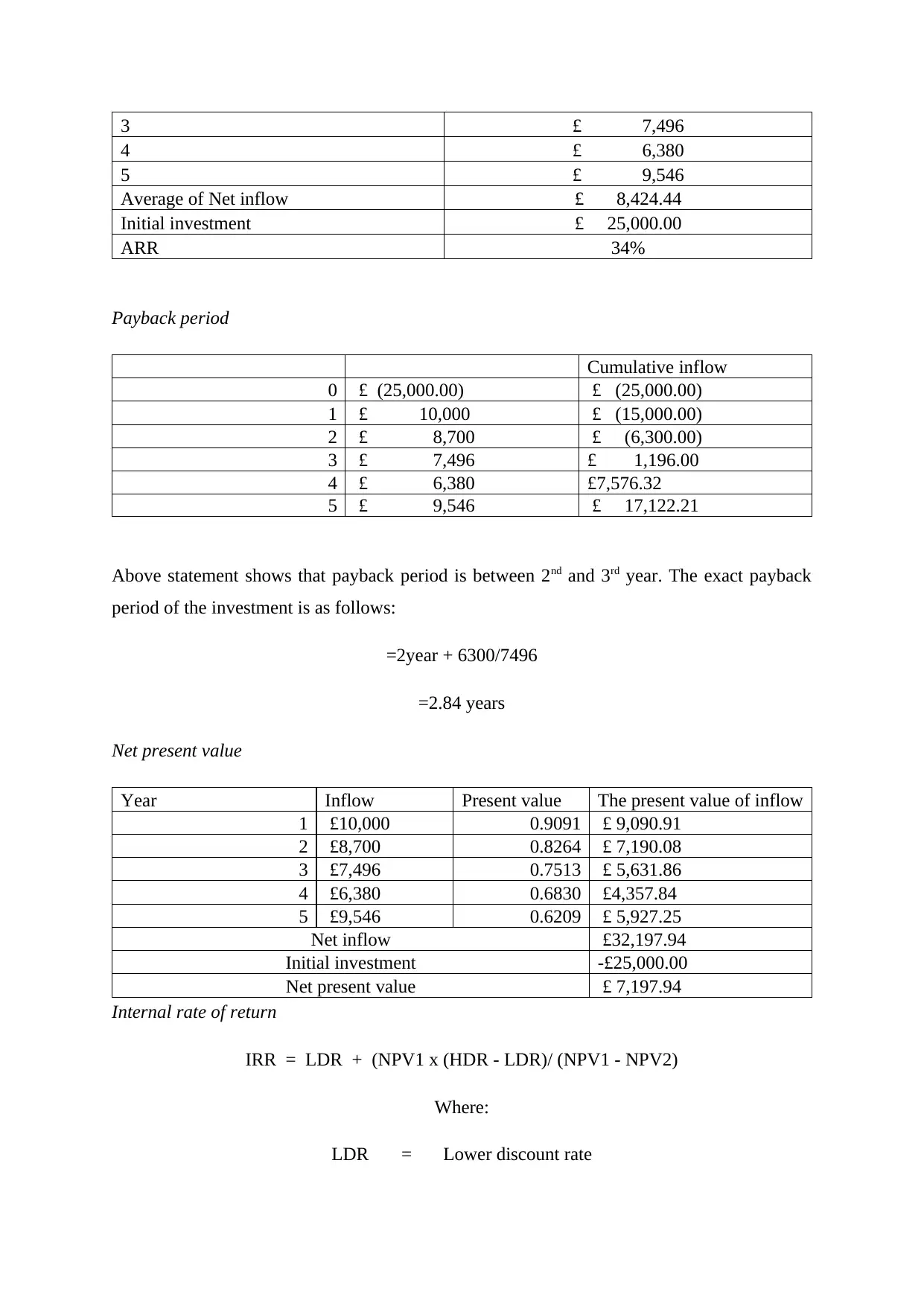

Payback period

Cumulative inflow

0 £ (25,000.00) £ (25,000.00)

1 £ 10,000 £ (15,000.00)

2 £ 8,700 £ (6,300.00)

3 £ 7,496 £ 1,196.00

4 £ 6,380 £7,576.32

5 £ 9,546 £ 17,122.21

Above statement shows that payback period is between 2nd and 3rd year. The exact payback

period of the investment is as follows:

=2year + 6300/7496

=2.84 years

Net present value

Year Inflow Present value The present value of inflow

1 £10,000 0.9091 £ 9,090.91

2 £8,700 0.8264 £ 7,190.08

3 £7,496 0.7513 £ 5,631.86

4 £6,380 0.6830 £4,357.84

5 £9,546 0.6209 £ 5,927.25

Net inflow £32,197.94

Initial investment -£25,000.00

Net present value £ 7,197.94

Internal rate of return

IRR = LDR + (NPV1 x (HDR - LDR)/ (NPV1 - NPV2)

Where:

LDR = Lower discount rate

4 £ 6,380

5 £ 9,546

Average of Net inflow £ 8,424.44

Initial investment £ 25,000.00

ARR 34%

Payback period

Cumulative inflow

0 £ (25,000.00) £ (25,000.00)

1 £ 10,000 £ (15,000.00)

2 £ 8,700 £ (6,300.00)

3 £ 7,496 £ 1,196.00

4 £ 6,380 £7,576.32

5 £ 9,546 £ 17,122.21

Above statement shows that payback period is between 2nd and 3rd year. The exact payback

period of the investment is as follows:

=2year + 6300/7496

=2.84 years

Net present value

Year Inflow Present value The present value of inflow

1 £10,000 0.9091 £ 9,090.91

2 £8,700 0.8264 £ 7,190.08

3 £7,496 0.7513 £ 5,631.86

4 £6,380 0.6830 £4,357.84

5 £9,546 0.6209 £ 5,927.25

Net inflow £32,197.94

Initial investment -£25,000.00

Net present value £ 7,197.94

Internal rate of return

IRR = LDR + (NPV1 x (HDR - LDR)/ (NPV1 - NPV2)

Where:

LDR = Lower discount rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.