Comprehensive Accounting and Finance Report: Investment Appraisal

VerifiedAdded on 2020/10/05

|15

|4043

|231

Report

AI Summary

This report provides a detailed analysis of accounting and finance principles, encompassing financial statements, break-even analysis, and investment appraisal techniques. Part A focuses on preparing an income statement and balance sheet for Gravepals Plc for 2017. Part B delves into break-even analysis, margin of safety, and Clarkenpark Ltd's strategy, including identifying and explaining assumptions within the break-even model. Part C explores investment appraisal techniques such as payback period, accounting rate of return, and net present value, offering recommendations on purchasing a new machine. The report includes calculations, explanations, and analyses of key merits and demerits for each technique, along with a discussion of budgeting as a strategic planning tool. The conclusion summarizes the key findings and recommendations, supported by a comprehensive list of references.

INTRODUCTION TO

ACCOUNTING AND FINANCE

ACCOUNTING AND FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

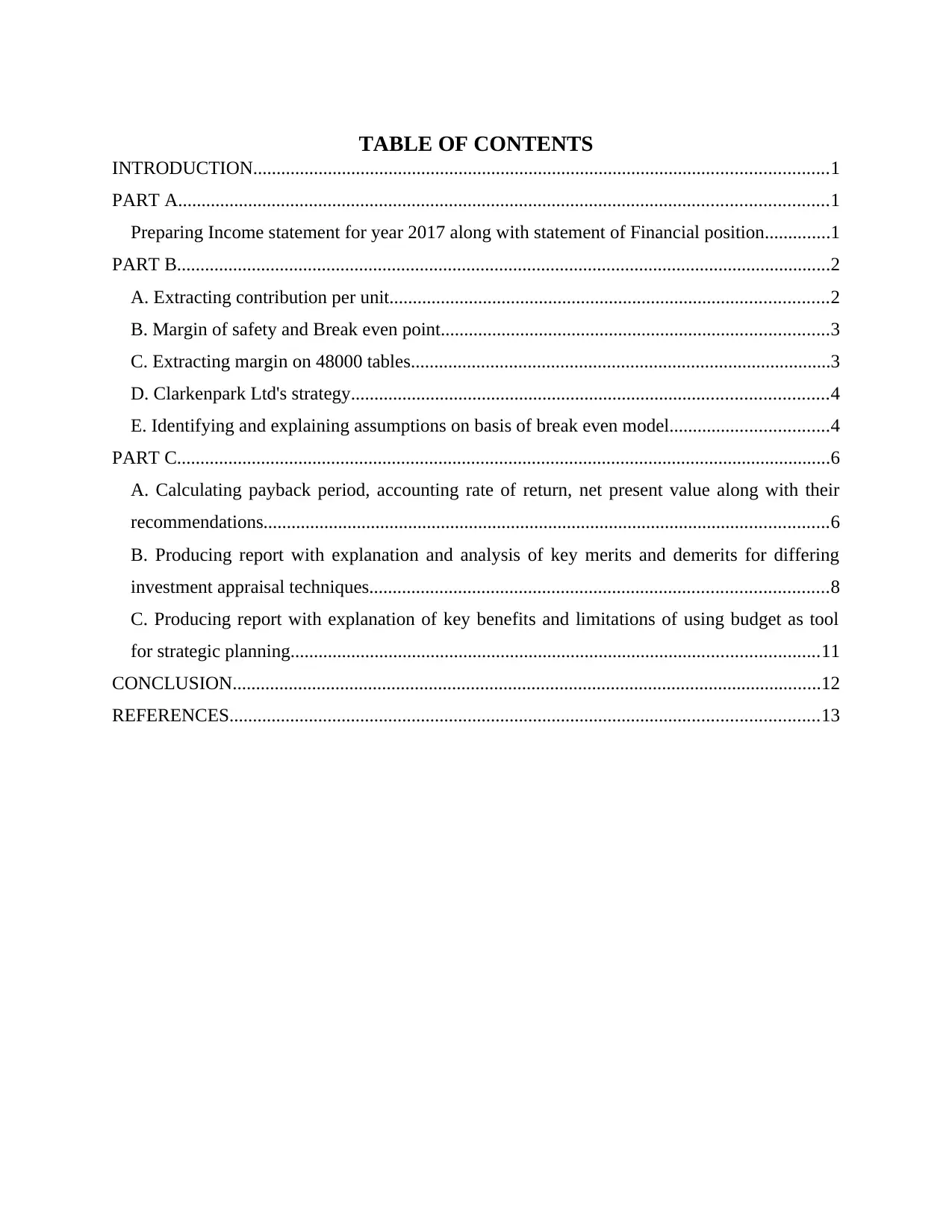

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Preparing Income statement for year 2017 along with statement of Financial position..............1

PART B............................................................................................................................................2

A. Extracting contribution per unit..............................................................................................2

B. Margin of safety and Break even point...................................................................................3

C. Extracting margin on 48000 tables..........................................................................................3

D. Clarkenpark Ltd's strategy......................................................................................................4

E. Identifying and explaining assumptions on basis of break even model..................................4

PART C............................................................................................................................................6

A. Calculating payback period, accounting rate of return, net present value along with their

recommendations.........................................................................................................................6

B. Producing report with explanation and analysis of key merits and demerits for differing

investment appraisal techniques..................................................................................................8

C. Producing report with explanation of key benefits and limitations of using budget as tool

for strategic planning.................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Preparing Income statement for year 2017 along with statement of Financial position..............1

PART B............................................................................................................................................2

A. Extracting contribution per unit..............................................................................................2

B. Margin of safety and Break even point...................................................................................3

C. Extracting margin on 48000 tables..........................................................................................3

D. Clarkenpark Ltd's strategy......................................................................................................4

E. Identifying and explaining assumptions on basis of break even model..................................4

PART C............................................................................................................................................6

A. Calculating payback period, accounting rate of return, net present value along with their

recommendations.........................................................................................................................6

B. Producing report with explanation and analysis of key merits and demerits for differing

investment appraisal techniques..................................................................................................8

C. Producing report with explanation of key benefits and limitations of using budget as tool

for strategic planning.................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Accounting is considered as comprehensive and systematic tracing of numerous financial

transactions related to business. It is also referred as process of classifying, summarizing and

analysing reports to transactions for over sighting agencies, tax collection entities and regulators.

In the similar aspect, finance is business term on basis of creation, investments, study of money

along with other financial instruments. The present report will give brief discussion about

appropriate understanding of fundamental concepts, techniques and models with application of

financial accounting along with management accounting. Further, it will reflect role of finance at

global and local level with reference to financial statements, Break even and margin of safety

analysis. In this similar aspect, there will be introduction of various investment appraisal

techniques with recommendation and analysis to purchase new machine or not.

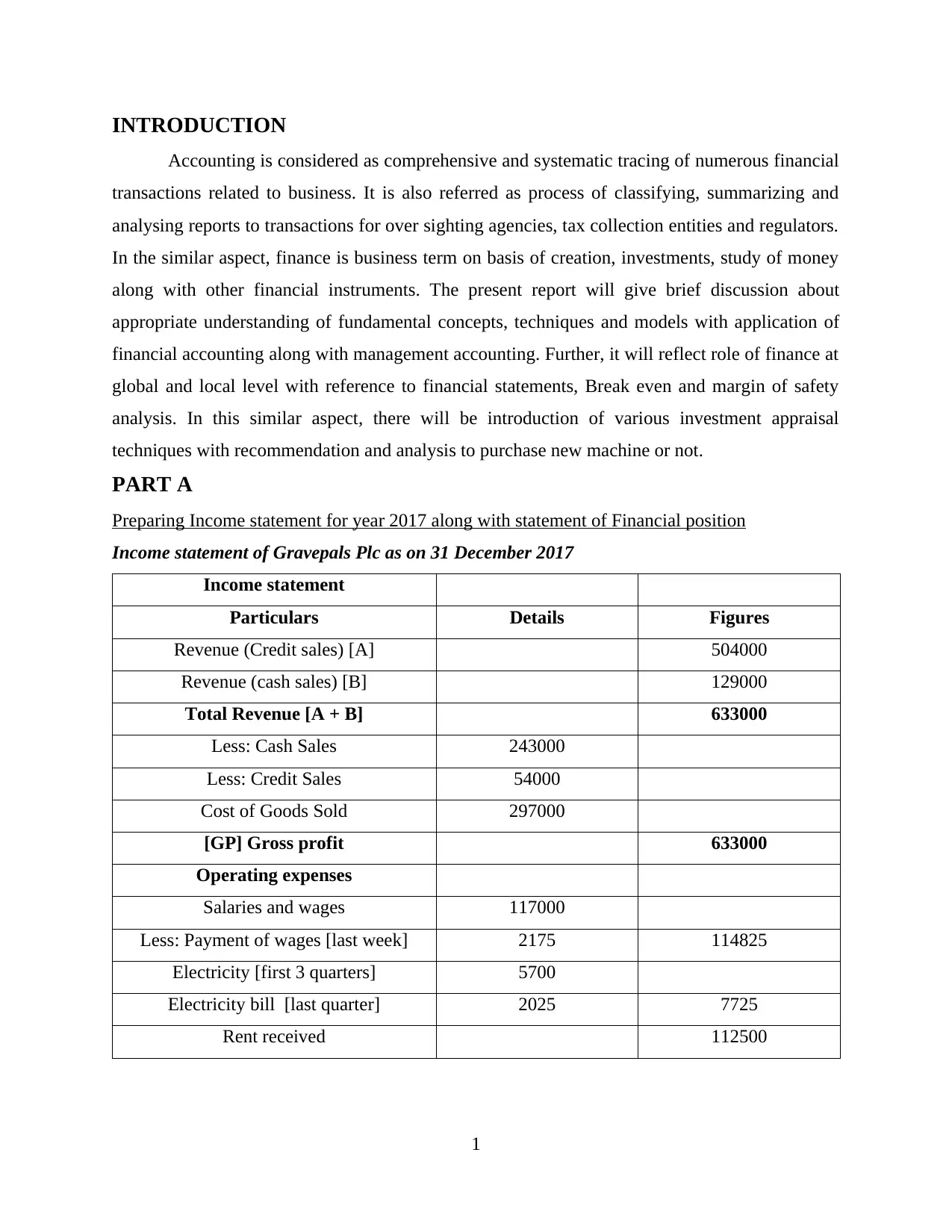

PART A

Preparing Income statement for year 2017 along with statement of Financial position

Income statement of Gravepals Plc as on 31 December 2017

Income statement

Particulars Details Figures

Revenue (Credit sales) [A] 504000

Revenue (cash sales) [B] 129000

Total Revenue [A + B] 633000

Less: Cash Sales 243000

Less: Credit Sales 54000

Cost of Goods Sold 297000

[GP] Gross profit 633000

Operating expenses

Salaries and wages 117000

Less: Payment of wages [last week] 2175 114825

Electricity [first 3 quarters] 5700

Electricity bill [last quarter] 2025 7725

Rent received 112500

1

Accounting is considered as comprehensive and systematic tracing of numerous financial

transactions related to business. It is also referred as process of classifying, summarizing and

analysing reports to transactions for over sighting agencies, tax collection entities and regulators.

In the similar aspect, finance is business term on basis of creation, investments, study of money

along with other financial instruments. The present report will give brief discussion about

appropriate understanding of fundamental concepts, techniques and models with application of

financial accounting along with management accounting. Further, it will reflect role of finance at

global and local level with reference to financial statements, Break even and margin of safety

analysis. In this similar aspect, there will be introduction of various investment appraisal

techniques with recommendation and analysis to purchase new machine or not.

PART A

Preparing Income statement for year 2017 along with statement of Financial position

Income statement of Gravepals Plc as on 31 December 2017

Income statement

Particulars Details Figures

Revenue (Credit sales) [A] 504000

Revenue (cash sales) [B] 129000

Total Revenue [A + B] 633000

Less: Cash Sales 243000

Less: Credit Sales 54000

Cost of Goods Sold 297000

[GP] Gross profit 633000

Operating expenses

Salaries and wages 117000

Less: Payment of wages [last week] 2175 114825

Electricity [first 3 quarters] 5700

Electricity bill [last quarter] 2025 7725

Rent received 112500

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Payment of tax on business premises [1

January] 2400

Payment of tax on business premises [1

April] 4500 6900

Delivery van depreciation 16320

Bad debts 1500

Sum of operating expenses 259770

Net profit 373230

Balance sheet of Gravepals Plc as on 31 December 2017

Particulars Details Amount

Current assets

Accounts receivables 438000

Less: Bad debts 1500 436500

Total stock 525000

Sum of current assets 961500

Fixed assets

Delivery van Cost 60000

Add: costs of operating 33600

Less: Sales 12000

Total van cost 81600

Residual life 5

Depreciation expense 16320

Valuation of van 65280 65280

Sum of fixed assets 65280

Total assets 1026780

Liabilities

Current liabilities

Accounts payables 393000

Total current liabilities 393000

2

January] 2400

Payment of tax on business premises [1

April] 4500 6900

Delivery van depreciation 16320

Bad debts 1500

Sum of operating expenses 259770

Net profit 373230

Balance sheet of Gravepals Plc as on 31 December 2017

Particulars Details Amount

Current assets

Accounts receivables 438000

Less: Bad debts 1500 436500

Total stock 525000

Sum of current assets 961500

Fixed assets

Delivery van Cost 60000

Add: costs of operating 33600

Less: Sales 12000

Total van cost 81600

Residual life 5

Depreciation expense 16320

Valuation of van 65280 65280

Sum of fixed assets 65280

Total assets 1026780

Liabilities

Current liabilities

Accounts payables 393000

Total current liabilities 393000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

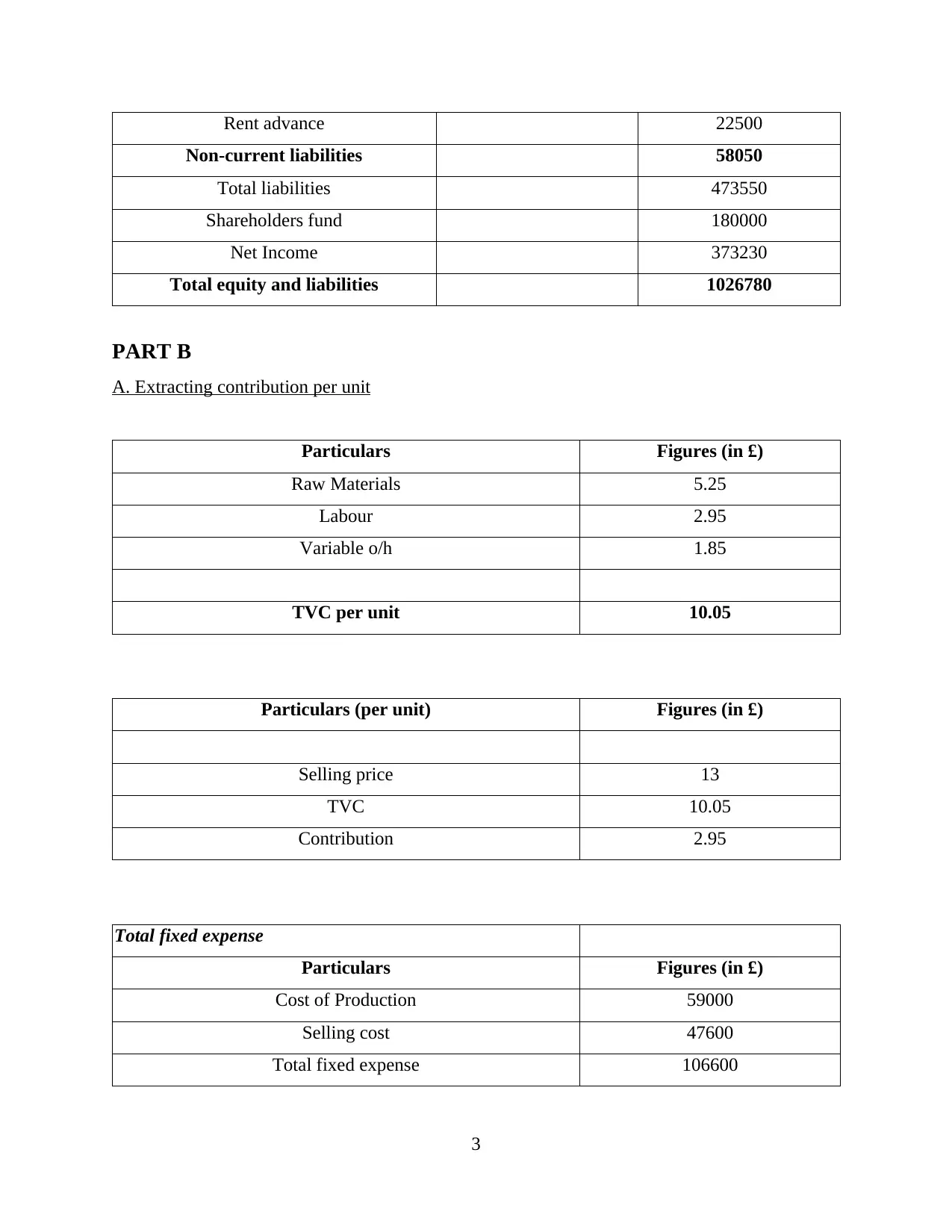

Rent advance 22500

Non-current liabilities 58050

Total liabilities 473550

Shareholders fund 180000

Net Income 373230

Total equity and liabilities 1026780

PART B

A. Extracting contribution per unit

Particulars Figures (in £)

Raw Materials 5.25

Labour 2.95

Variable o/h 1.85

TVC per unit 10.05

Particulars (per unit) Figures (in £)

Selling price 13

TVC 10.05

Contribution 2.95

Total fixed expense

Particulars Figures (in £)

Cost of Production 59000

Selling cost 47600

Total fixed expense 106600

3

Non-current liabilities 58050

Total liabilities 473550

Shareholders fund 180000

Net Income 373230

Total equity and liabilities 1026780

PART B

A. Extracting contribution per unit

Particulars Figures (in £)

Raw Materials 5.25

Labour 2.95

Variable o/h 1.85

TVC per unit 10.05

Particulars (per unit) Figures (in £)

Selling price 13

TVC 10.05

Contribution 2.95

Total fixed expense

Particulars Figures (in £)

Cost of Production 59000

Selling cost 47600

Total fixed expense 106600

3

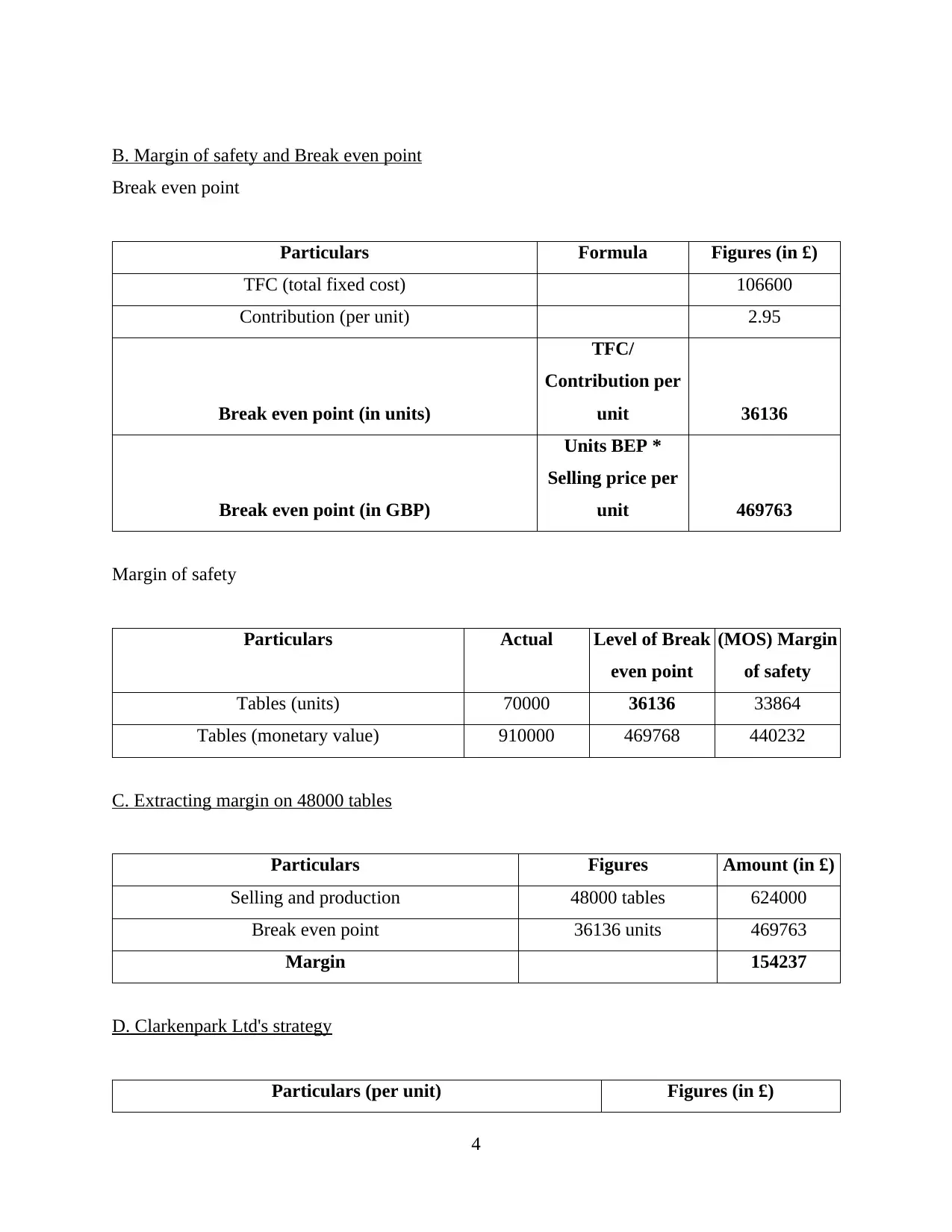

B. Margin of safety and Break even point

Break even point

Particulars Formula Figures (in £)

TFC (total fixed cost) 106600

Contribution (per unit) 2.95

Break even point (in units)

TFC/

Contribution per

unit 36136

Break even point (in GBP)

Units BEP *

Selling price per

unit 469763

Margin of safety

Particulars Actual Level of Break

even point

(MOS) Margin

of safety

Tables (units) 70000 36136 33864

Tables (monetary value) 910000 469768 440232

C. Extracting margin on 48000 tables

Particulars Figures Amount (in £)

Selling and production 48000 tables 624000

Break even point 36136 units 469763

Margin 154237

D. Clarkenpark Ltd's strategy

Particulars (per unit) Figures (in £)

4

Break even point

Particulars Formula Figures (in £)

TFC (total fixed cost) 106600

Contribution (per unit) 2.95

Break even point (in units)

TFC/

Contribution per

unit 36136

Break even point (in GBP)

Units BEP *

Selling price per

unit 469763

Margin of safety

Particulars Actual Level of Break

even point

(MOS) Margin

of safety

Tables (units) 70000 36136 33864

Tables (monetary value) 910000 469768 440232

C. Extracting margin on 48000 tables

Particulars Figures Amount (in £)

Selling and production 48000 tables 624000

Break even point 36136 units 469763

Margin 154237

D. Clarkenpark Ltd's strategy

Particulars (per unit) Figures (in £)

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

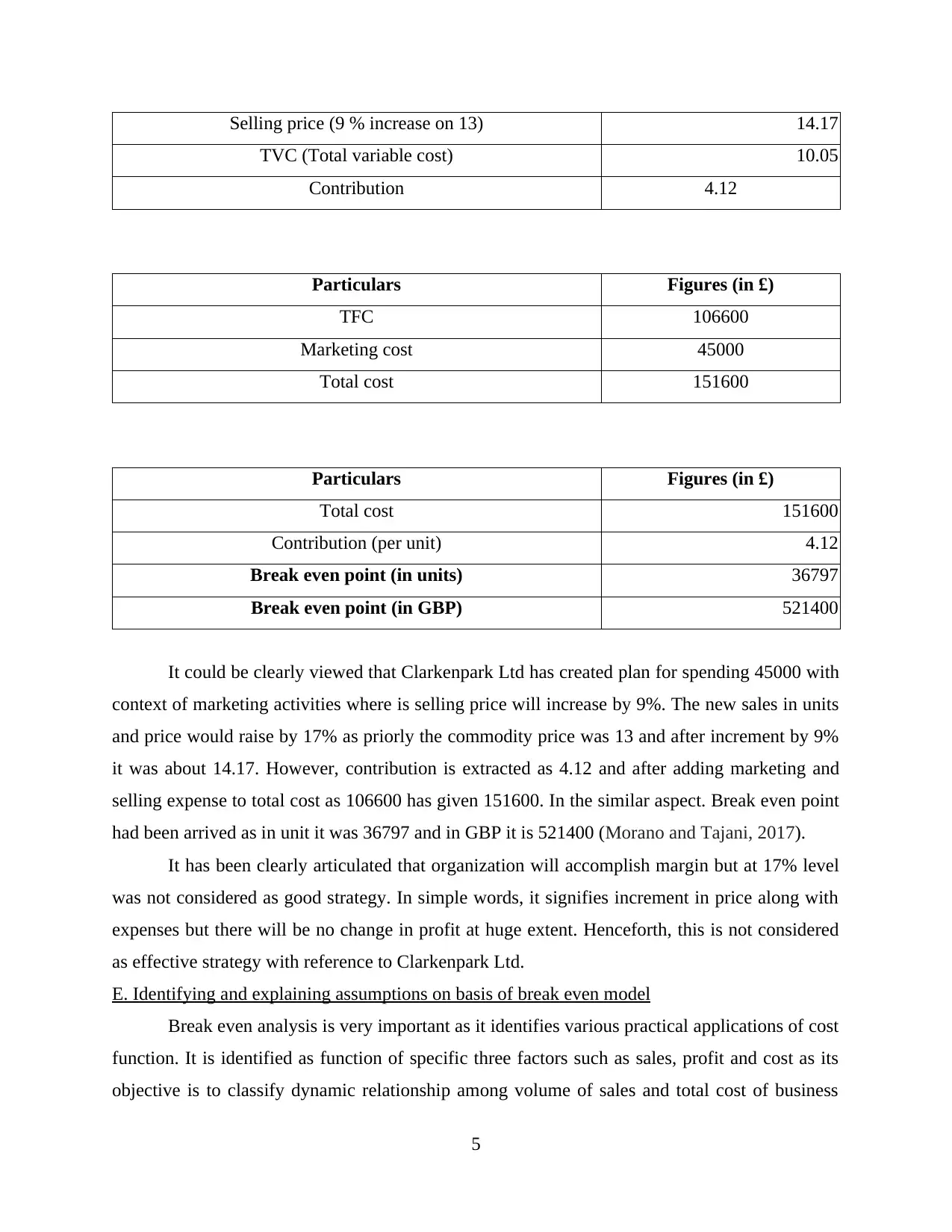

Selling price (9 % increase on 13) 14.17

TVC (Total variable cost) 10.05

Contribution 4.12

Particulars Figures (in £)

TFC 106600

Marketing cost 45000

Total cost 151600

Particulars Figures (in £)

Total cost 151600

Contribution (per unit) 4.12

Break even point (in units) 36797

Break even point (in GBP) 521400

It could be clearly viewed that Clarkenpark Ltd has created plan for spending 45000 with

context of marketing activities where is selling price will increase by 9%. The new sales in units

and price would raise by 17% as priorly the commodity price was 13 and after increment by 9%

it was about 14.17. However, contribution is extracted as 4.12 and after adding marketing and

selling expense to total cost as 106600 has given 151600. In the similar aspect. Break even point

had been arrived as in unit it was 36797 and in GBP it is 521400 (Morano and Tajani, 2017).

It has been clearly articulated that organization will accomplish margin but at 17% level

was not considered as good strategy. In simple words, it signifies increment in price along with

expenses but there will be no change in profit at huge extent. Henceforth, this is not considered

as effective strategy with reference to Clarkenpark Ltd.

E. Identifying and explaining assumptions on basis of break even model

Break even analysis is very important as it identifies various practical applications of cost

function. It is identified as function of specific three factors such as sales, profit and cost as its

objective is to classify dynamic relationship among volume of sales and total cost of business

5

TVC (Total variable cost) 10.05

Contribution 4.12

Particulars Figures (in £)

TFC 106600

Marketing cost 45000

Total cost 151600

Particulars Figures (in £)

Total cost 151600

Contribution (per unit) 4.12

Break even point (in units) 36797

Break even point (in GBP) 521400

It could be clearly viewed that Clarkenpark Ltd has created plan for spending 45000 with

context of marketing activities where is selling price will increase by 9%. The new sales in units

and price would raise by 17% as priorly the commodity price was 13 and after increment by 9%

it was about 14.17. However, contribution is extracted as 4.12 and after adding marketing and

selling expense to total cost as 106600 has given 151600. In the similar aspect. Break even point

had been arrived as in unit it was 36797 and in GBP it is 521400 (Morano and Tajani, 2017).

It has been clearly articulated that organization will accomplish margin but at 17% level

was not considered as good strategy. In simple words, it signifies increment in price along with

expenses but there will be no change in profit at huge extent. Henceforth, this is not considered

as effective strategy with reference to Clarkenpark Ltd.

E. Identifying and explaining assumptions on basis of break even model

Break even analysis is very important as it identifies various practical applications of cost

function. It is identified as function of specific three factors such as sales, profit and cost as its

objective is to classify dynamic relationship among volume of sales and total cost of business

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

entity. It helps in understanding operating condition which exists when business entity breaks

even, in simple words when sales is equal to all incurred expenses for attaining sales level. This

model is based on numerous assumptions which are stated below:

There is appropriate classification of total cost in variable and fixed cost as it avoids semi

variable cost.

The product's price is considered as constant or stable.

There is presence of linearity among cost and revenue functions.

Generally, volume of production and sales are equal.

The variable cost will be attaining increment with constant rate.

The technology is constant with absence of improvement in labour efficiency.

There is no change in factor price.

The fixed cost is constant with consideration of particular volume.

The alterations in input price is ruled out.

With context of multi product firm there is stability in product mix.

Analysing about model which could be utilised with specific range of business

Break even analysis is used for identifying about volume of sales for business when it is

making profit on basis of variable and fixed cost along with selling price. It is used in

conjunction with forecast of sales along with appropriate development of pricing strategy as part

of business or marketing plan. In nutshell, its uses for business had been identified for business

perspective are stated below:

It is used for identifying the number of units with business requirements for dell in order

for ignoring loss. It is used with reference to budgeting process as it exactly identifies

units for selling with context to break-even.

It also motivates employees majorly sales staff as it clearly reflects profit at different

points of sales (Cortes, Amano and Yamasaki, 2017).

The most important aspect for application of break even analysis for improving growth as

it allows various users for input actual units sold with context of revenue, fixed and variable

costs sold on per units. The sales volume is fixed for recovering specified return on capital

employed as it provides recommendations for shifting sales mix. It provides creating inter-firm

profitability comparison. Further, it reveals about profit earning capacity and strength of specific

concern with absence of effort and difficulty.

6

even, in simple words when sales is equal to all incurred expenses for attaining sales level. This

model is based on numerous assumptions which are stated below:

There is appropriate classification of total cost in variable and fixed cost as it avoids semi

variable cost.

The product's price is considered as constant or stable.

There is presence of linearity among cost and revenue functions.

Generally, volume of production and sales are equal.

The variable cost will be attaining increment with constant rate.

The technology is constant with absence of improvement in labour efficiency.

There is no change in factor price.

The fixed cost is constant with consideration of particular volume.

The alterations in input price is ruled out.

With context of multi product firm there is stability in product mix.

Analysing about model which could be utilised with specific range of business

Break even analysis is used for identifying about volume of sales for business when it is

making profit on basis of variable and fixed cost along with selling price. It is used in

conjunction with forecast of sales along with appropriate development of pricing strategy as part

of business or marketing plan. In nutshell, its uses for business had been identified for business

perspective are stated below:

It is used for identifying the number of units with business requirements for dell in order

for ignoring loss. It is used with reference to budgeting process as it exactly identifies

units for selling with context to break-even.

It also motivates employees majorly sales staff as it clearly reflects profit at different

points of sales (Cortes, Amano and Yamasaki, 2017).

The most important aspect for application of break even analysis for improving growth as

it allows various users for input actual units sold with context of revenue, fixed and variable

costs sold on per units. The sales volume is fixed for recovering specified return on capital

employed as it provides recommendations for shifting sales mix. It provides creating inter-firm

profitability comparison. Further, it reveals about profit earning capacity and strength of specific

concern with absence of effort and difficulty.

6

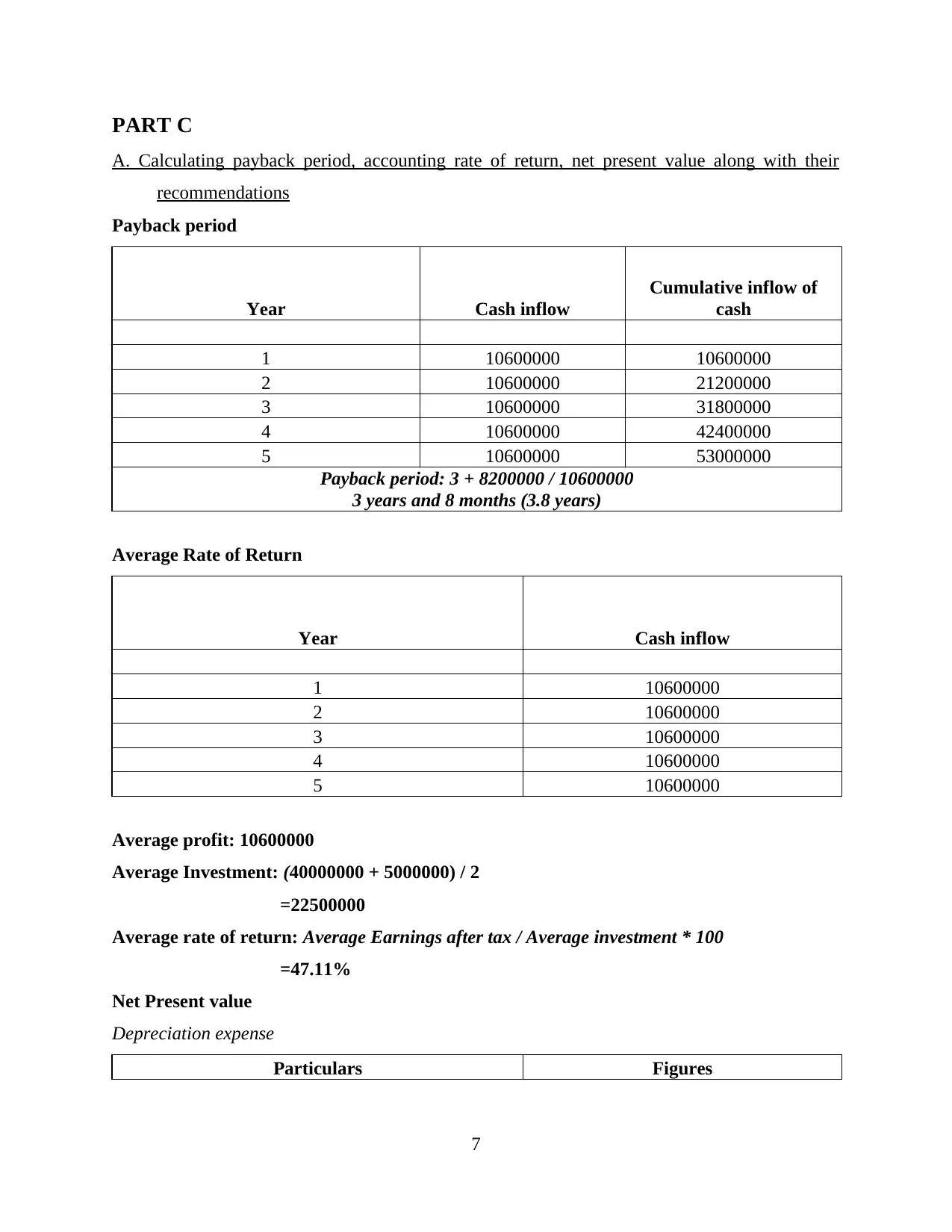

PART C

A. Calculating payback period, accounting rate of return, net present value along with their

recommendations

Payback period

Year Cash inflow

Cumulative inflow of

cash

1 10600000 10600000

2 10600000 21200000

3 10600000 31800000

4 10600000 42400000

5 10600000 53000000

Payback period: 3 + 8200000 / 10600000

3 years and 8 months (3.8 years)

Average Rate of Return

Year Cash inflow

1 10600000

2 10600000

3 10600000

4 10600000

5 10600000

Average profit: 10600000

Average Investment: (40000000 + 5000000) / 2

=22500000

Average rate of return: Average Earnings after tax / Average investment * 100

=47.11%

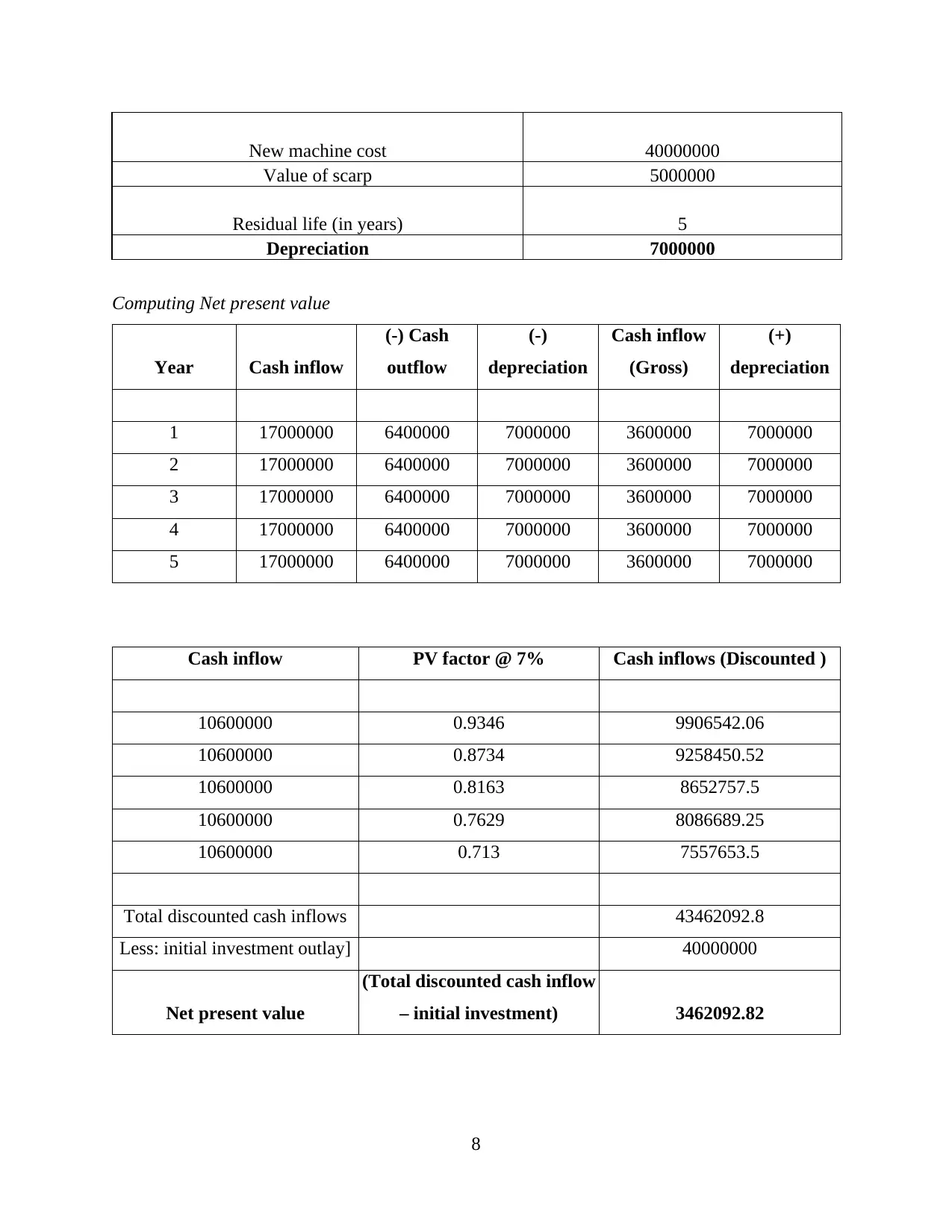

Net Present value

Depreciation expense

Particulars Figures

7

A. Calculating payback period, accounting rate of return, net present value along with their

recommendations

Payback period

Year Cash inflow

Cumulative inflow of

cash

1 10600000 10600000

2 10600000 21200000

3 10600000 31800000

4 10600000 42400000

5 10600000 53000000

Payback period: 3 + 8200000 / 10600000

3 years and 8 months (3.8 years)

Average Rate of Return

Year Cash inflow

1 10600000

2 10600000

3 10600000

4 10600000

5 10600000

Average profit: 10600000

Average Investment: (40000000 + 5000000) / 2

=22500000

Average rate of return: Average Earnings after tax / Average investment * 100

=47.11%

Net Present value

Depreciation expense

Particulars Figures

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

New machine cost 40000000

Value of scarp 5000000

Residual life (in years) 5

Depreciation 7000000

Computing Net present value

Year Cash inflow

(-) Cash

outflow

(-)

depreciation

Cash inflow

(Gross)

(+)

depreciation

1 17000000 6400000 7000000 3600000 7000000

2 17000000 6400000 7000000 3600000 7000000

3 17000000 6400000 7000000 3600000 7000000

4 17000000 6400000 7000000 3600000 7000000

5 17000000 6400000 7000000 3600000 7000000

Cash inflow PV factor @ 7% Cash inflows (Discounted )

10600000 0.9346 9906542.06

10600000 0.8734 9258450.52

10600000 0.8163 8652757.5

10600000 0.7629 8086689.25

10600000 0.713 7557653.5

Total discounted cash inflows 43462092.8

Less: initial investment outlay] 40000000

Net present value

(Total discounted cash inflow

– initial investment) 3462092.82

8

Value of scarp 5000000

Residual life (in years) 5

Depreciation 7000000

Computing Net present value

Year Cash inflow

(-) Cash

outflow

(-)

depreciation

Cash inflow

(Gross)

(+)

depreciation

1 17000000 6400000 7000000 3600000 7000000

2 17000000 6400000 7000000 3600000 7000000

3 17000000 6400000 7000000 3600000 7000000

4 17000000 6400000 7000000 3600000 7000000

5 17000000 6400000 7000000 3600000 7000000

Cash inflow PV factor @ 7% Cash inflows (Discounted )

10600000 0.9346 9906542.06

10600000 0.8734 9258450.52

10600000 0.8163 8652757.5

10600000 0.7629 8086689.25

10600000 0.713 7557653.5

Total discounted cash inflows 43462092.8

Less: initial investment outlay] 40000000

Net present value

(Total discounted cash inflow

– initial investment) 3462092.82

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Recommendation: The decision about purchasing machine has been taken by considering

investment appraisal techniques such as payback period, Average rate of return and net present

value.

Payback period: It is replicated as covering its initial cost as in this project of 5 years, its

initial investment of 40000000 will be recovered in 3 years and 8 months with 7% cost of capital.

In simple words, it could be elaborated that this project is beneficial and give profit after this

duration as there is measurement of length of required time (Jonker, Junginger and Faaij, 2014).

Average rate of return: It is an accounting concept which has consideration of time

factor as returns are produced via net profit of proposed capital investment. It is reflected in

percentage form as in above project, its average investment of 22500000 along with average net

income as 10600000 along with appropriate return as 47.11%.

Net Present value: There is analysis of profitability of this project with context of

determining net present value. There is extraction of depreciation of residual life of 5 years as its

scrap value is 5000000 so its depreciation as 7000000. In this aspect, its cash inflow as 17000000

by excluding cash outflow of 6400000 and depreciation which will give gross cash flow. Again

there will be addition of depreciation will be accomplished as cash inflow with its cost of capital

as 7% will lead to discounted cash inflows. After performing this procedure, the sum of

discounted cash inflow will be considered as sum then it will exclude initial investment then its

final outcome as net present value. The above machine's net present value is extracted as

3462092.82 which is profitable to Dane Jones Ltd.

Hence, this analysis of investment appraisal techniques, it has been evaluated that this

machine could be brought to business as each outcome is favourable and beneficial to Dane

Jones Ltd.

B. Producing report with explanation and analysis of key merits and demerits for differing

investment appraisal techniques

Investment appraisal techniques is referred as planning process which is used for

identifying long term investments of company like new machines and products, replacing

machinery, research development projects and worth with cash funding via optimal capital

structure of business entity. The decision about investment is associated with tactical and

strategic business decisions with requirement of attaining objectives for long term perspective.

9

investment appraisal techniques such as payback period, Average rate of return and net present

value.

Payback period: It is replicated as covering its initial cost as in this project of 5 years, its

initial investment of 40000000 will be recovered in 3 years and 8 months with 7% cost of capital.

In simple words, it could be elaborated that this project is beneficial and give profit after this

duration as there is measurement of length of required time (Jonker, Junginger and Faaij, 2014).

Average rate of return: It is an accounting concept which has consideration of time

factor as returns are produced via net profit of proposed capital investment. It is reflected in

percentage form as in above project, its average investment of 22500000 along with average net

income as 10600000 along with appropriate return as 47.11%.

Net Present value: There is analysis of profitability of this project with context of

determining net present value. There is extraction of depreciation of residual life of 5 years as its

scrap value is 5000000 so its depreciation as 7000000. In this aspect, its cash inflow as 17000000

by excluding cash outflow of 6400000 and depreciation which will give gross cash flow. Again

there will be addition of depreciation will be accomplished as cash inflow with its cost of capital

as 7% will lead to discounted cash inflows. After performing this procedure, the sum of

discounted cash inflow will be considered as sum then it will exclude initial investment then its

final outcome as net present value. The above machine's net present value is extracted as

3462092.82 which is profitable to Dane Jones Ltd.

Hence, this analysis of investment appraisal techniques, it has been evaluated that this

machine could be brought to business as each outcome is favourable and beneficial to Dane

Jones Ltd.

B. Producing report with explanation and analysis of key merits and demerits for differing

investment appraisal techniques

Investment appraisal techniques is referred as planning process which is used for

identifying long term investments of company like new machines and products, replacing

machinery, research development projects and worth with cash funding via optimal capital

structure of business entity. The decision about investment is associated with tactical and

strategic business decisions with requirement of attaining objectives for long term perspective.

9

There are various techniques for investment appraisal techniques which are beneficial to business

but it has demerits as well which are stated below:

Payback Period: It is referred as time length with requirement of recovering investment

cost. It is provided with specific investment of project which is significant as proper determinant

for undertaking project or position where long payback period are not directly desirable for

position of investment. In simple words, it is time when initial cash outflow is recovered with

cash inflow which is produced through investment (Vesty and et.al., 2018). It is considered as

simplest technique of investment appraisal. Its merits and demerits are explained below:

Merits

It is very easy to calculate and understandable as well.

There is need of less time, cost and labour as compared to different capital budgeting

methods.

It avoids and reduce loss via obsolescence with preference to short payback period as

compared to long.

It is highly suitable for business entity with short amount of cash in hand along with weak

liquidity position of cash is very weak.

It provides huge importance for speedy investment recovery with context of capital assets

(Hyk, 2018).

Demerits

This method does not consider time value of money.

It might mislead decisions of capital budgeting as it fails for measuring capital

expenditure's productivity due to absence for reattempting measure for investment

returns.

It avoids liquidity and short term solvency with specific business concern.

The economic life and capital wastage has been avoided through restricting particular

consideration of gross earnings of project.

The cost of capital has been overlooked which is specific factor for sound capital

budgeting decision as it does not consider cash inflow arising after payback period.

Accounting Rate of return: It is financial ratio which is used for capital budgeting as it

measures amount of profit and expected on particular investment. It divides average profit

through initial investment for extracting return or ration which is expected. Generally, it is used

10

but it has demerits as well which are stated below:

Payback Period: It is referred as time length with requirement of recovering investment

cost. It is provided with specific investment of project which is significant as proper determinant

for undertaking project or position where long payback period are not directly desirable for

position of investment. In simple words, it is time when initial cash outflow is recovered with

cash inflow which is produced through investment (Vesty and et.al., 2018). It is considered as

simplest technique of investment appraisal. Its merits and demerits are explained below:

Merits

It is very easy to calculate and understandable as well.

There is need of less time, cost and labour as compared to different capital budgeting

methods.

It avoids and reduce loss via obsolescence with preference to short payback period as

compared to long.

It is highly suitable for business entity with short amount of cash in hand along with weak

liquidity position of cash is very weak.

It provides huge importance for speedy investment recovery with context of capital assets

(Hyk, 2018).

Demerits

This method does not consider time value of money.

It might mislead decisions of capital budgeting as it fails for measuring capital

expenditure's productivity due to absence for reattempting measure for investment

returns.

It avoids liquidity and short term solvency with specific business concern.

The economic life and capital wastage has been avoided through restricting particular

consideration of gross earnings of project.

The cost of capital has been overlooked which is specific factor for sound capital

budgeting decision as it does not consider cash inflow arising after payback period.

Accounting Rate of return: It is financial ratio which is used for capital budgeting as it

measures amount of profit and expected on particular investment. It divides average profit

through initial investment for extracting return or ration which is expected. Generally, it is used

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.