S plc Financial Report: Investment Appraisal, Break-Even Analysis

VerifiedAdded on 2023/06/18

|15

|4214

|495

Report

AI Summary

This report provides a detailed analysis of S plc's financial strategies, focusing on capital investment appraisal techniques such as payback period, net present value (NPV), and internal rate of return (IRR). It assesses a new investment project by S plc, examining cash flow analysis, payback period, and NPV to determine project acceptability. The report also contrasts equity issues with long-term bank loans, evaluating the advantages and disadvantages of each. Furthermore, it calculates break-even sales revenue and margin of safety, analyzing the consequences of price changes and critically assessing the assumptions of cost-volume-profit analysis. Finally, the report compares different categories of suppliers, discusses the advantages of single versus multiple sourcing, and explores cross-sourcing with examples, providing a comprehensive overview of S plc's financial and procurement strategies.

Business Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

SECTION-A....................................................................................................................................3

Reason behind the importance of capital investment appraisal to S plc.....................................3

Cash flow analysis Statement of new investment by S plc.........................................................4

Calculate the pay back period and check whether the project is acceptable if S plc imposes a

three-year maximum payback period..........................................................................................4

Determine whether the project is acceptable or not according to its net -present value.............5

Determine the logic of net present value approach and its relation with cost of capital.............6

Calculate internal rate of return for investment proposal to know if the project should be

accepted or not............................................................................................................................6

Explain the reason behind considering net present value method superior to internal rate of

return...........................................................................................................................................7

SECTION-B.....................................................................................................................................7

Critically contrast Equity issue with long term bank loan..........................................................7

SECTION-C.....................................................................................................................................8

Calculate break-even sales revenue and the margin of safety.....................................................8

consequences of increase and decrease in price of 10%............................................................8

Critically analyse the assumption of cost volume profit analysis...............................................9

SECTION-D..................................................................................................................................10

Compare the three categories of suppliers................................................................................10

Compare the advantages of single sourcing and multiple sourcing of procurement................10

Discuss Cross-sourcing with example and its benefits to the buyer.........................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

SECTION-A....................................................................................................................................3

Reason behind the importance of capital investment appraisal to S plc.....................................3

Cash flow analysis Statement of new investment by S plc.........................................................4

Calculate the pay back period and check whether the project is acceptable if S plc imposes a

three-year maximum payback period..........................................................................................4

Determine whether the project is acceptable or not according to its net -present value.............5

Determine the logic of net present value approach and its relation with cost of capital.............6

Calculate internal rate of return for investment proposal to know if the project should be

accepted or not............................................................................................................................6

Explain the reason behind considering net present value method superior to internal rate of

return...........................................................................................................................................7

SECTION-B.....................................................................................................................................7

Critically contrast Equity issue with long term bank loan..........................................................7

SECTION-C.....................................................................................................................................8

Calculate break-even sales revenue and the margin of safety.....................................................8

consequences of increase and decrease in price of 10%............................................................8

Critically analyse the assumption of cost volume profit analysis...............................................9

SECTION-D..................................................................................................................................10

Compare the three categories of suppliers................................................................................10

Compare the advantages of single sourcing and multiple sourcing of procurement................10

Discuss Cross-sourcing with example and its benefits to the buyer.........................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial strategies of a business are concerned with acquisition and utilization of funds

and assets. They focuses on procuring resources for the firm, evaluation of costing techniques

and structure, ascertaining profit earning potential, managing accounts and many more. Their

main aim is to align the working of finance department in the direction of attaining business

objective by gaining strategic advantage (Banerjee, Tarazi and Akre., 2018). This report is based

on S plc and is divided into four sections. It discusses about the various financial strategies like

budgets, cash flow analysis, net present value approach, intern al rate of return and many more. It

further recognises the cheapest source of loan from bank along with comparing it with equity

shares. The report also determines the break even sales point and consequences of change in

price. At last, there is a description on various types of suppliers and sources of procurement.

SECTION-A

Reason behind the importance of capital investment appraisal to S plc.

It is technique of measuring the performance of a new project. It provides the answers of

questions that a particular investment will be proved beneficial to firm or not. There are various

techniques applied by S plc like payback period, accounting and internal rate of return, net

present value and many more. These are various reasons which proves that this process is very

important for S plc.

Involvement of company resources- Large amount of efforts and resources are applied

on a particular project. A single wrong decision by S plc can lead to huge loss of all these

things. So, it is always recommended to conduct this appraisal to identify the profitability

from that investment (Block, Hirt and Danielsen., 2018).

To tap possible alternatives- There are always some sort of options for all jobs. So, to

earn maximum profit, it required that S plc performs these techniques and examine the

benefits of all similar projects and find out the best alternative.

For avoiding uncertainty- The tools of capital investment appraisal recognises the

impact of inflation on prices and some other uncertain factors, through which true value

of project can be determined. Without applying this technique, management would not be

able to identify the costs and profits associated with it correctly and can result in taking

wrong procurement decision (Young and Legister., 2018).

Financial strategies of a business are concerned with acquisition and utilization of funds

and assets. They focuses on procuring resources for the firm, evaluation of costing techniques

and structure, ascertaining profit earning potential, managing accounts and many more. Their

main aim is to align the working of finance department in the direction of attaining business

objective by gaining strategic advantage (Banerjee, Tarazi and Akre., 2018). This report is based

on S plc and is divided into four sections. It discusses about the various financial strategies like

budgets, cash flow analysis, net present value approach, intern al rate of return and many more. It

further recognises the cheapest source of loan from bank along with comparing it with equity

shares. The report also determines the break even sales point and consequences of change in

price. At last, there is a description on various types of suppliers and sources of procurement.

SECTION-A

Reason behind the importance of capital investment appraisal to S plc.

It is technique of measuring the performance of a new project. It provides the answers of

questions that a particular investment will be proved beneficial to firm or not. There are various

techniques applied by S plc like payback period, accounting and internal rate of return, net

present value and many more. These are various reasons which proves that this process is very

important for S plc.

Involvement of company resources- Large amount of efforts and resources are applied

on a particular project. A single wrong decision by S plc can lead to huge loss of all these

things. So, it is always recommended to conduct this appraisal to identify the profitability

from that investment (Block, Hirt and Danielsen., 2018).

To tap possible alternatives- There are always some sort of options for all jobs. So, to

earn maximum profit, it required that S plc performs these techniques and examine the

benefits of all similar projects and find out the best alternative.

For avoiding uncertainty- The tools of capital investment appraisal recognises the

impact of inflation on prices and some other uncertain factors, through which true value

of project can be determined. Without applying this technique, management would not be

able to identify the costs and profits associated with it correctly and can result in taking

wrong procurement decision (Young and Legister., 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

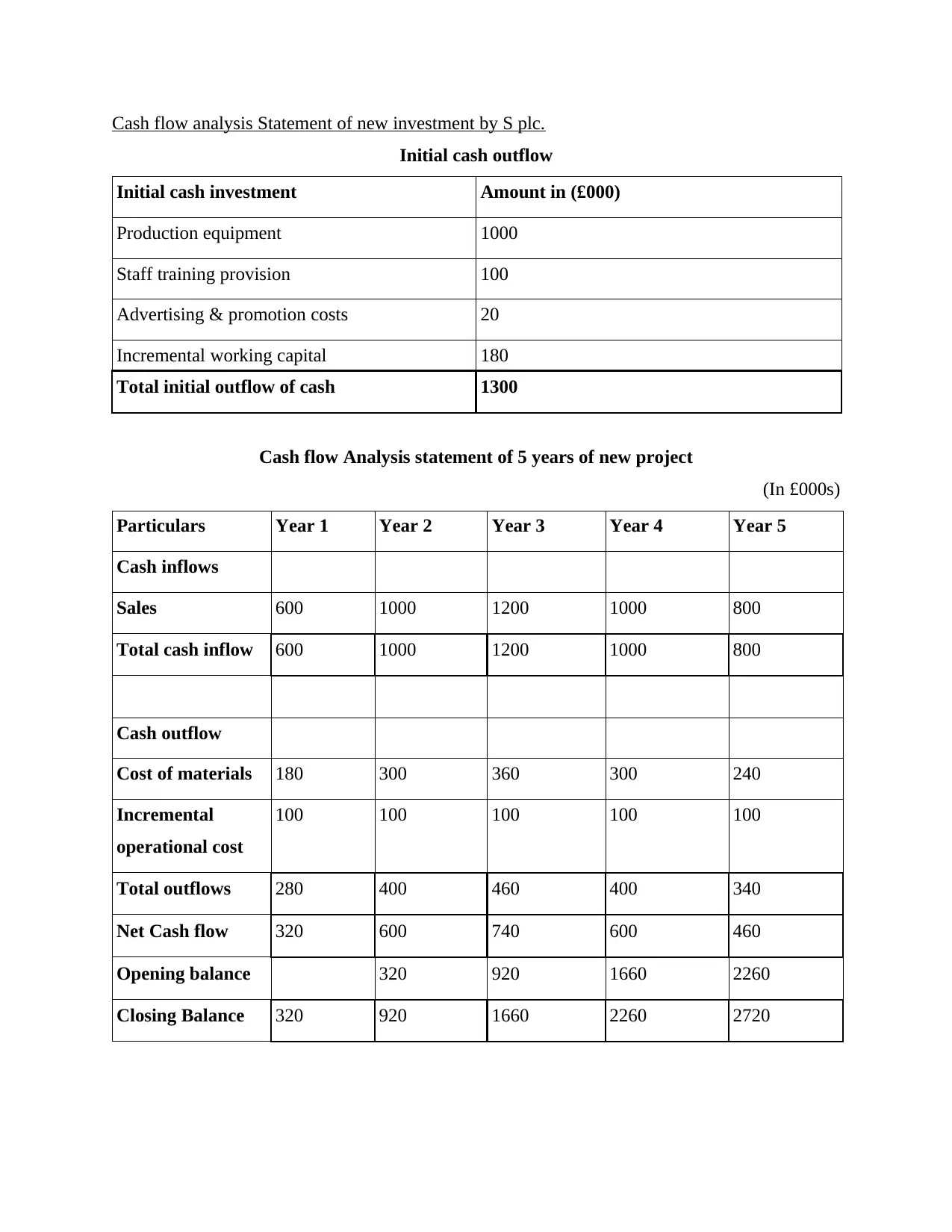

Cash flow analysis Statement of new investment by S plc.

Initial cash outflow

Initial cash investment Amount in (£000)

Production equipment 1000

Staff training provision 100

Advertising & promotion costs 20

Incremental working capital 180

Total initial outflow of cash 1300

Cash flow Analysis statement of 5 years of new project

(In £000s)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Cash inflows

Sales 600 1000 1200 1000 800

Total cash inflow 600 1000 1200 1000 800

Cash outflow

Cost of materials 180 300 360 300 240

Incremental

operational cost

100 100 100 100 100

Total outflows 280 400 460 400 340

Net Cash flow 320 600 740 600 460

Opening balance 320 920 1660 2260

Closing Balance 320 920 1660 2260 2720

Initial cash outflow

Initial cash investment Amount in (£000)

Production equipment 1000

Staff training provision 100

Advertising & promotion costs 20

Incremental working capital 180

Total initial outflow of cash 1300

Cash flow Analysis statement of 5 years of new project

(In £000s)

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Cash inflows

Sales 600 1000 1200 1000 800

Total cash inflow 600 1000 1200 1000 800

Cash outflow

Cost of materials 180 300 360 300 240

Incremental

operational cost

100 100 100 100 100

Total outflows 280 400 460 400 340

Net Cash flow 320 600 740 600 460

Opening balance 320 920 1660 2260

Closing Balance 320 920 1660 2260 2720

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

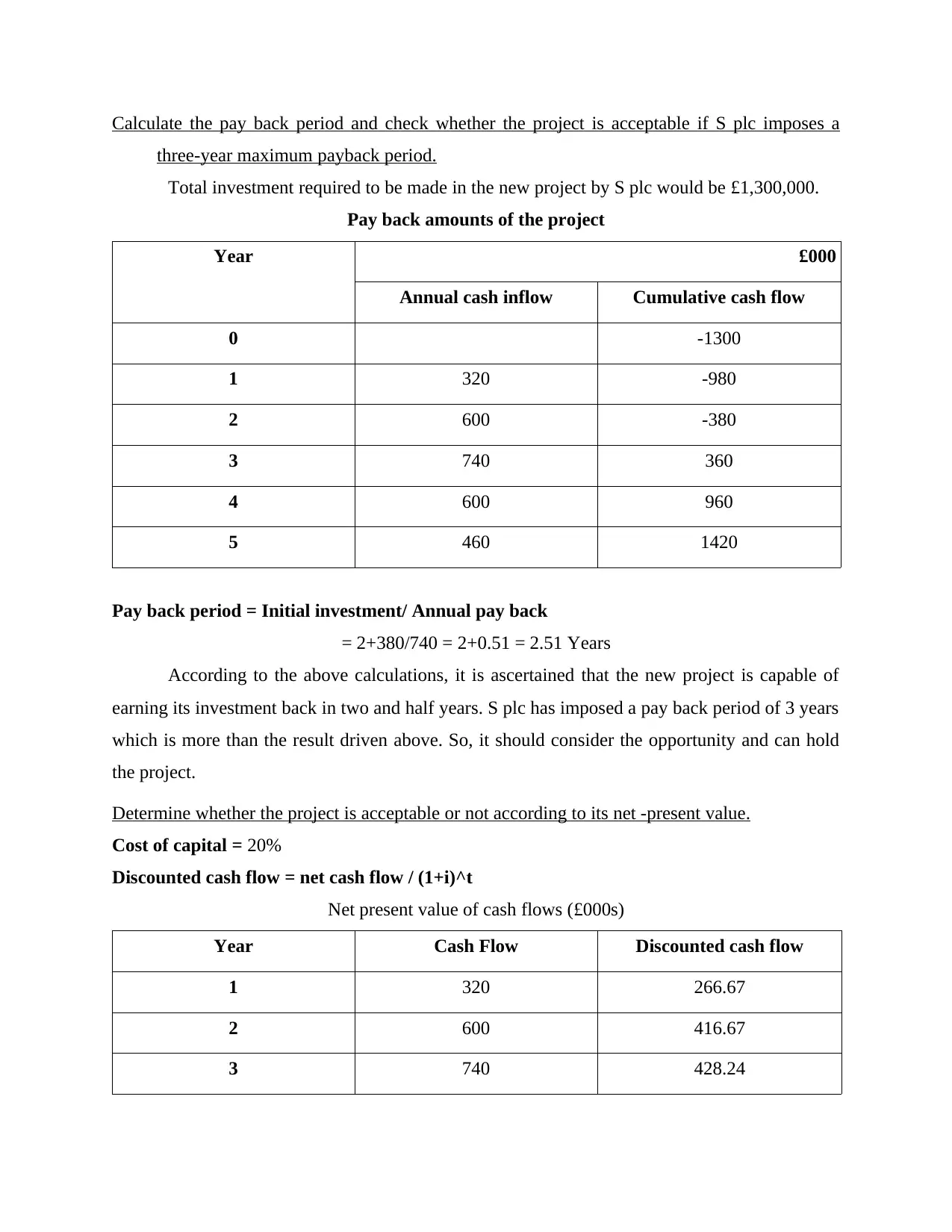

Calculate the pay back period and check whether the project is acceptable if S plc imposes a

three-year maximum payback period.

Total investment required to be made in the new project by S plc would be £1,300,000.

Pay back amounts of the project

Year £000

Annual cash inflow Cumulative cash flow

0 -1300

1 320 -980

2 600 -380

3 740 360

4 600 960

5 460 1420

Pay back period = Initial investment/ Annual pay back

= 2+380/740 = 2+0.51 = 2.51 Years

According to the above calculations, it is ascertained that the new project is capable of

earning its investment back in two and half years. S plc has imposed a pay back period of 3 years

which is more than the result driven above. So, it should consider the opportunity and can hold

the project.

Determine whether the project is acceptable or not according to its net -present value.

Cost of capital = 20%

Discounted cash flow = net cash flow / (1+i)^t

Net present value of cash flows (£000s)

Year Cash Flow Discounted cash flow

1 320 266.67

2 600 416.67

3 740 428.24

three-year maximum payback period.

Total investment required to be made in the new project by S plc would be £1,300,000.

Pay back amounts of the project

Year £000

Annual cash inflow Cumulative cash flow

0 -1300

1 320 -980

2 600 -380

3 740 360

4 600 960

5 460 1420

Pay back period = Initial investment/ Annual pay back

= 2+380/740 = 2+0.51 = 2.51 Years

According to the above calculations, it is ascertained that the new project is capable of

earning its investment back in two and half years. S plc has imposed a pay back period of 3 years

which is more than the result driven above. So, it should consider the opportunity and can hold

the project.

Determine whether the project is acceptable or not according to its net -present value.

Cost of capital = 20%

Discounted cash flow = net cash flow / (1+i)^t

Net present value of cash flows (£000s)

Year Cash Flow Discounted cash flow

1 320 266.67

2 600 416.67

3 740 428.24

4 600 289.44

5 460 184.86

Total 1585.87

Net present value of project = Present value of total cash inflows – Present value of cash

outflows

= 1585.87 – 1300

=285.87

The net present value of project is around £ 285,000. This means the firm can opt to

acquire the project as the result driven is positive and is far more than the value which would be

invested in the project.

Determine the logic of net present value approach and its relation with cost of capital.

Net present value means to ascertain the discounted value of all the cash inflows and

outflows over a period of time. It is used for analysing the feasibility of a project, on the basis of

which the decision of acceptance of rejection of investment is taken by firm. The value of cash

flow in future is always less than its present value because with time, the value of money

decreases. Thus the amount estimated to be received in future in always less than the cash

actually received. This tool helps in generating knowledge about the value which will be actually

received in future by applying discounting factor (Bulturbayevich and et.al., 2020). By applying

this tool, S plc can know the present value of all the projects it is holding or desires to invest.

Relation among net present value and cost of capital

Net present value of a project is directly related to the cost of capital associated with that

project. While calculating the amount, this tool makes use of interest rate which is paid by firms

for acquiring any type of debt. For companies, this rate is the cost of capital. Thus, there is a

great relation among these two terms, which can also be viewed in the formula below:

Net present value= net cash flow / (1+i)^t

Here, i denotes cost of capital.

5 460 184.86

Total 1585.87

Net present value of project = Present value of total cash inflows – Present value of cash

outflows

= 1585.87 – 1300

=285.87

The net present value of project is around £ 285,000. This means the firm can opt to

acquire the project as the result driven is positive and is far more than the value which would be

invested in the project.

Determine the logic of net present value approach and its relation with cost of capital.

Net present value means to ascertain the discounted value of all the cash inflows and

outflows over a period of time. It is used for analysing the feasibility of a project, on the basis of

which the decision of acceptance of rejection of investment is taken by firm. The value of cash

flow in future is always less than its present value because with time, the value of money

decreases. Thus the amount estimated to be received in future in always less than the cash

actually received. This tool helps in generating knowledge about the value which will be actually

received in future by applying discounting factor (Bulturbayevich and et.al., 2020). By applying

this tool, S plc can know the present value of all the projects it is holding or desires to invest.

Relation among net present value and cost of capital

Net present value of a project is directly related to the cost of capital associated with that

project. While calculating the amount, this tool makes use of interest rate which is paid by firms

for acquiring any type of debt. For companies, this rate is the cost of capital. Thus, there is a

great relation among these two terms, which can also be viewed in the formula below:

Net present value= net cash flow / (1+i)^t

Here, i denotes cost of capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculate internal rate of return for investment proposal to know if the project should be

accepted or not.

Whole calculating Internal rate of return, The net present value of project is considered to

be zero. The value is then ascertained with the help of hit and trial method.

Formula used for calculating IRR is :

Net present value= net cash flow / (1+i)^t

0 = -(1300[1+i]^0)+(320/[1+i]^1) + (600/[1+i]^2) + (740/[1+i]^3) + (600/[1+i]^4) +

(460/[1+i]^5)

By applying then percentage of around 27 % the value of NPV can be ascertained to be

zero. So, Internal rate of return for the project is 27 %. As per this result, it can be said that the

project can be accepted by the firm because IRR is much higher than the cost i9ncurreed by the

capital.

No, change in cost of capital would not have any effect on the internal rate of return as

there is no relation among the two when calculated differently. In actual, both the terms are

same.

Explain the reason behind considering net present value method superior to internal rate of

return.

Only IRR cannot handle multiple discount rates, but net present value holds this capacity.

Also , it cannot calculate the mixture of negative and positive cash flows. Thirdly, the value of

IRR in never known and works on hit and trial method (Cai and et.al., 2021).

SECTION-B

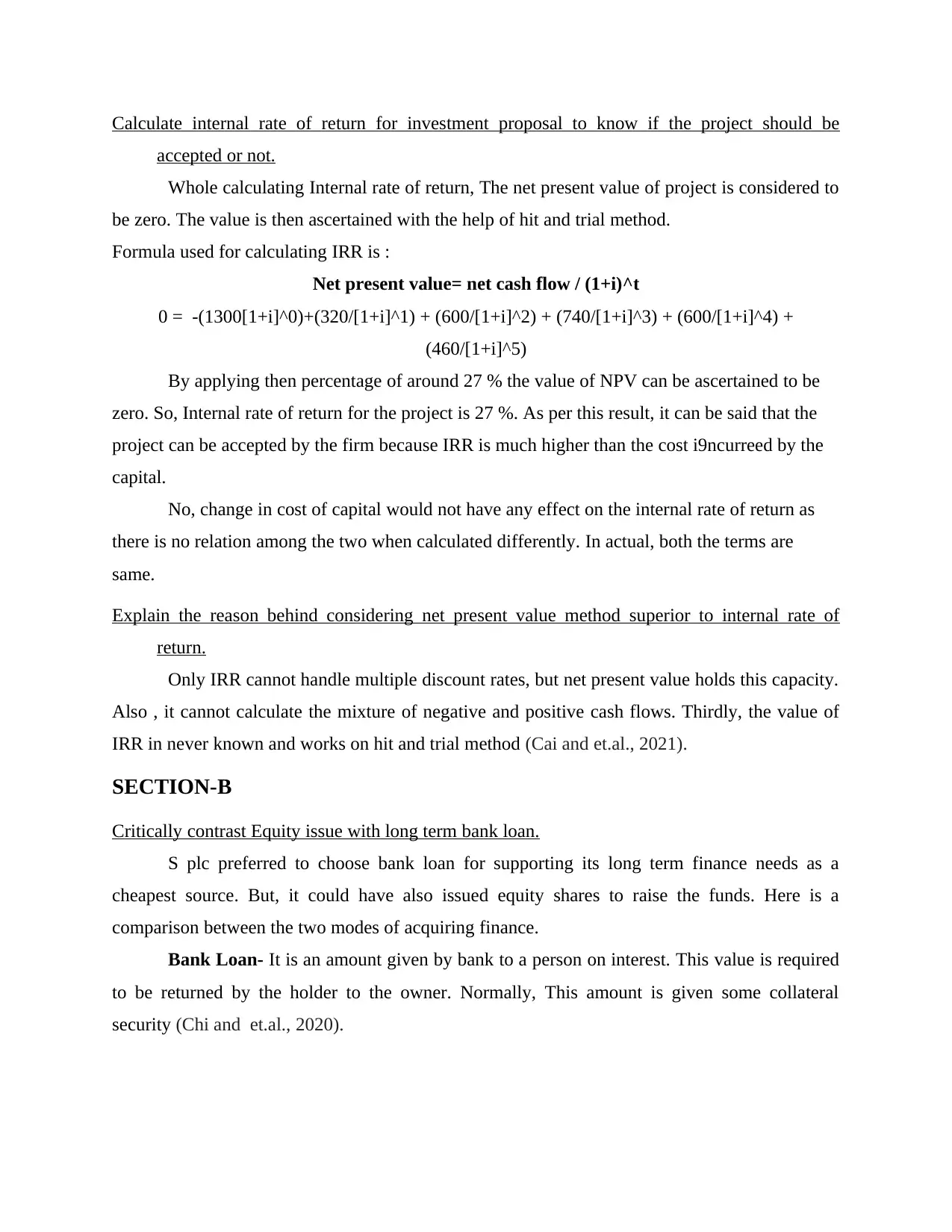

Critically contrast Equity issue with long term bank loan.

S plc preferred to choose bank loan for supporting its long term finance needs as a

cheapest source. But, it could have also issued equity shares to raise the funds. Here is a

comparison between the two modes of acquiring finance.

Bank Loan- It is an amount given by bank to a person on interest. This value is required

to be returned by the holder to the owner. Normally, This amount is given some collateral

security (Chi and et.al., 2020).

accepted or not.

Whole calculating Internal rate of return, The net present value of project is considered to

be zero. The value is then ascertained with the help of hit and trial method.

Formula used for calculating IRR is :

Net present value= net cash flow / (1+i)^t

0 = -(1300[1+i]^0)+(320/[1+i]^1) + (600/[1+i]^2) + (740/[1+i]^3) + (600/[1+i]^4) +

(460/[1+i]^5)

By applying then percentage of around 27 % the value of NPV can be ascertained to be

zero. So, Internal rate of return for the project is 27 %. As per this result, it can be said that the

project can be accepted by the firm because IRR is much higher than the cost i9ncurreed by the

capital.

No, change in cost of capital would not have any effect on the internal rate of return as

there is no relation among the two when calculated differently. In actual, both the terms are

same.

Explain the reason behind considering net present value method superior to internal rate of

return.

Only IRR cannot handle multiple discount rates, but net present value holds this capacity.

Also , it cannot calculate the mixture of negative and positive cash flows. Thirdly, the value of

IRR in never known and works on hit and trial method (Cai and et.al., 2021).

SECTION-B

Critically contrast Equity issue with long term bank loan.

S plc preferred to choose bank loan for supporting its long term finance needs as a

cheapest source. But, it could have also issued equity shares to raise the funds. Here is a

comparison between the two modes of acquiring finance.

Bank Loan- It is an amount given by bank to a person on interest. This value is required

to be returned by the holder to the owner. Normally, This amount is given some collateral

security (Chi and et.al., 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Equity Shares- These are issued by companies to the general public for fulfilling there

need of funds. The holder of these shares have right on the company and shares the profit and

losses faced by them.

Comparison between the bank loan and the equity shares

Basis Bank loan Equity shares

Risk Interest on borrowings is fixed and

thus, it is required to be paid even if

the company is facing losses.

Dividend is only paid at the the time of

profits and is not fixed, which means

firm can decide its amount on the basis

of their own requirement of cash.

Return The holder of loan is required to pay

the principle amount with interest, at

the time of completion of time period.

There is no compulsion of repayment of

amount, until liquidation.

Limitation on

use of funds

The creditor can put a limit on the use

of funds.

There is no stipulation on the usage of

money raised from shareholders.

Tax benefit Interest on this amount attracts tax

deduction by reducing it from profit

(EvmenchikBanerjee, Tarazi and

Akre., 2018).

The dividend paid on shares is not

acclaimed for taxation benefit as it is

not reduced from the taxable income.

Loss of

control

There is no risk of loss of control as the

creditors do not have any interest in the

functions of organisation.

Issuing more equity will result in more

control of outsiders on the firm and the

owners share in business will

automatically reduce.

SECTION-C

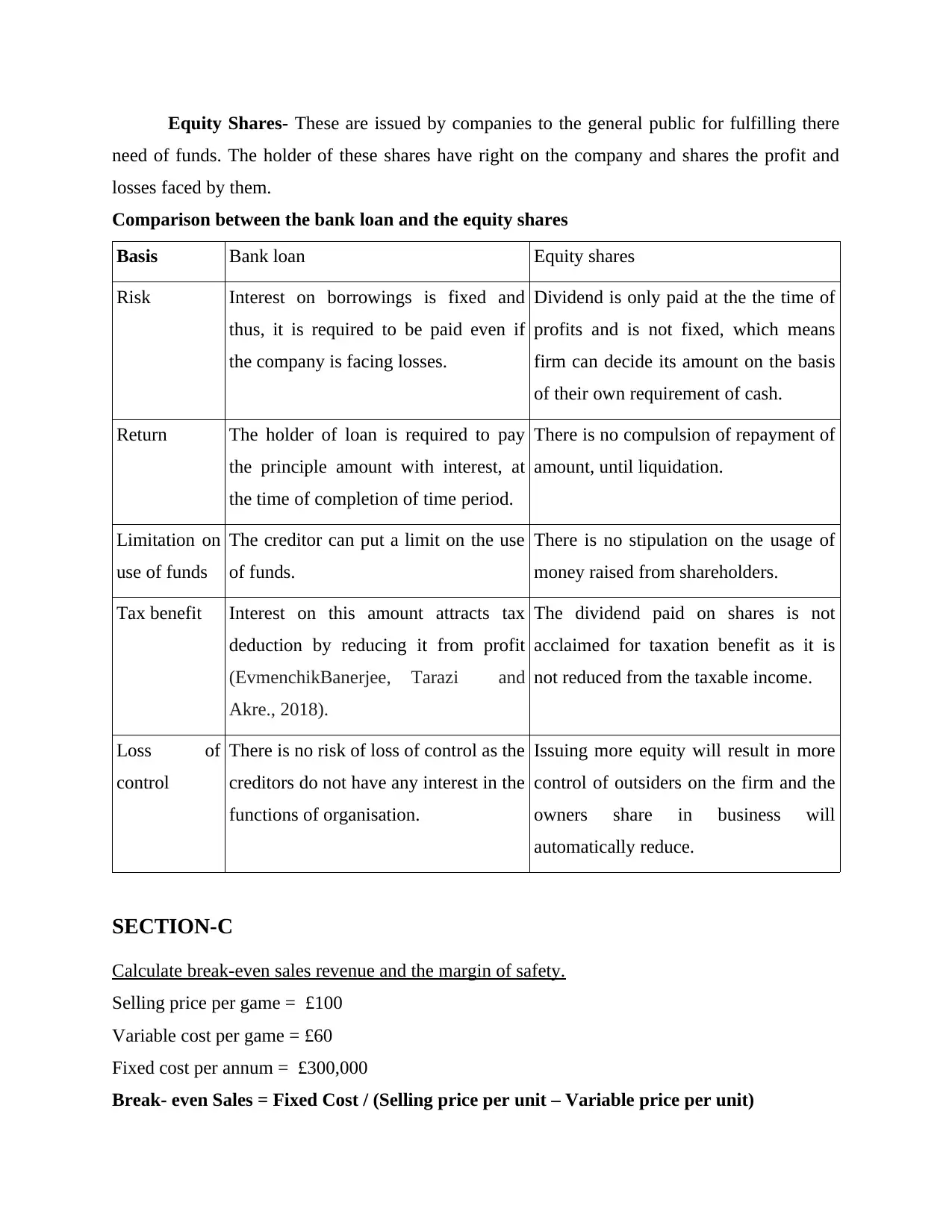

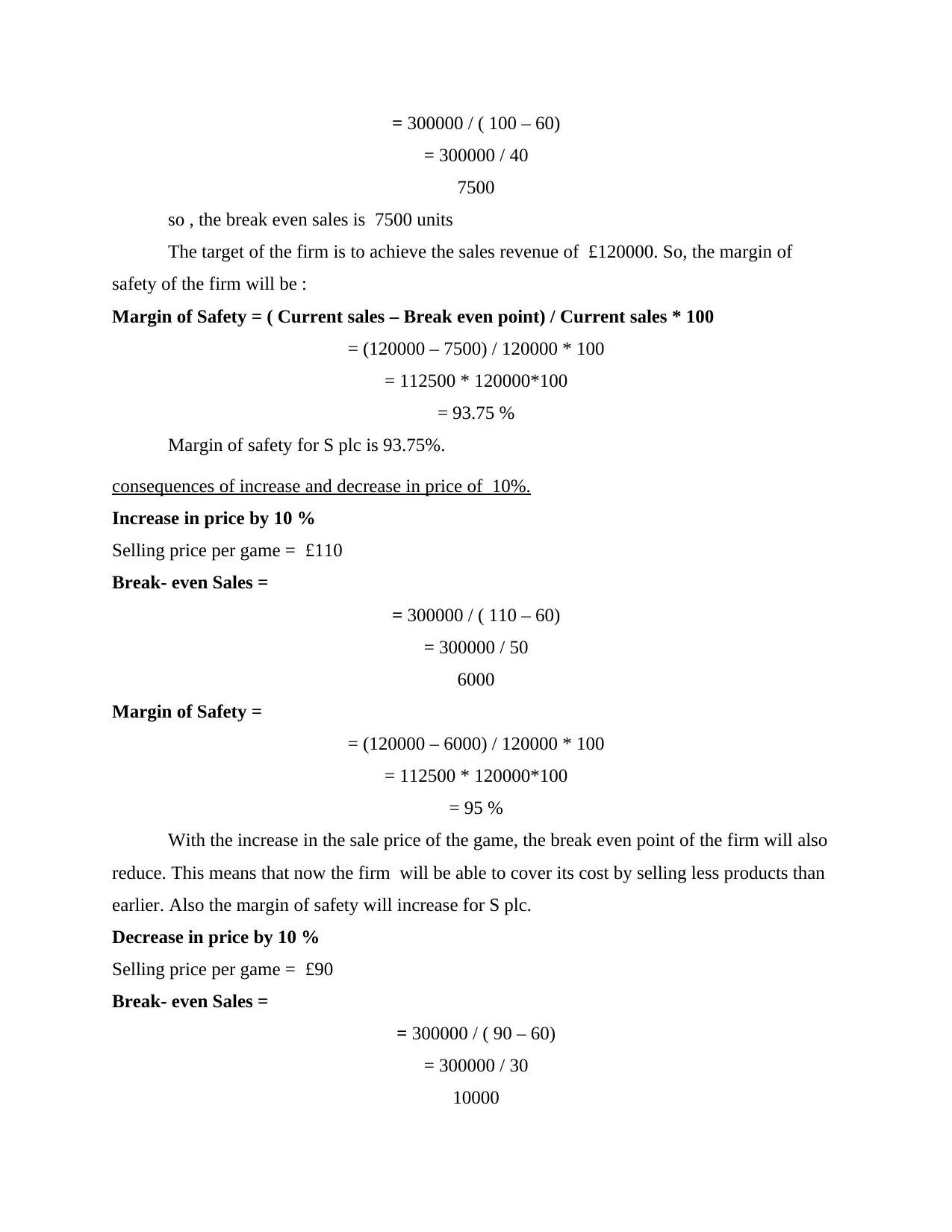

Calculate break-even sales revenue and the margin of safety.

Selling price per game = £100

Variable cost per game = £60

Fixed cost per annum = £300,000

Break- even Sales = Fixed Cost / (Selling price per unit – Variable price per unit)

need of funds. The holder of these shares have right on the company and shares the profit and

losses faced by them.

Comparison between the bank loan and the equity shares

Basis Bank loan Equity shares

Risk Interest on borrowings is fixed and

thus, it is required to be paid even if

the company is facing losses.

Dividend is only paid at the the time of

profits and is not fixed, which means

firm can decide its amount on the basis

of their own requirement of cash.

Return The holder of loan is required to pay

the principle amount with interest, at

the time of completion of time period.

There is no compulsion of repayment of

amount, until liquidation.

Limitation on

use of funds

The creditor can put a limit on the use

of funds.

There is no stipulation on the usage of

money raised from shareholders.

Tax benefit Interest on this amount attracts tax

deduction by reducing it from profit

(EvmenchikBanerjee, Tarazi and

Akre., 2018).

The dividend paid on shares is not

acclaimed for taxation benefit as it is

not reduced from the taxable income.

Loss of

control

There is no risk of loss of control as the

creditors do not have any interest in the

functions of organisation.

Issuing more equity will result in more

control of outsiders on the firm and the

owners share in business will

automatically reduce.

SECTION-C

Calculate break-even sales revenue and the margin of safety.

Selling price per game = £100

Variable cost per game = £60

Fixed cost per annum = £300,000

Break- even Sales = Fixed Cost / (Selling price per unit – Variable price per unit)

= 300000 / ( 100 – 60)

= 300000 / 40

7500

so , the break even sales is 7500 units

The target of the firm is to achieve the sales revenue of £120000. So, the margin of

safety of the firm will be :

Margin of Safety = ( Current sales – Break even point) / Current sales * 100

= (120000 – 7500) / 120000 * 100

= 112500 * 120000*100

= 93.75 %

Margin of safety for S plc is 93.75%.

consequences of increase and decrease in price of 10%.

Increase in price by 10 %

Selling price per game = £110

Break- even Sales =

= 300000 / ( 110 – 60)

= 300000 / 50

6000

Margin of Safety =

= (120000 – 6000) / 120000 * 100

= 112500 * 120000*100

= 95 %

With the increase in the sale price of the game, the break even point of the firm will also

reduce. This means that now the firm will be able to cover its cost by selling less products than

earlier. Also the margin of safety will increase for S plc.

Decrease in price by 10 %

Selling price per game = £90

Break- even Sales =

= 300000 / ( 90 – 60)

= 300000 / 30

10000

= 300000 / 40

7500

so , the break even sales is 7500 units

The target of the firm is to achieve the sales revenue of £120000. So, the margin of

safety of the firm will be :

Margin of Safety = ( Current sales – Break even point) / Current sales * 100

= (120000 – 7500) / 120000 * 100

= 112500 * 120000*100

= 93.75 %

Margin of safety for S plc is 93.75%.

consequences of increase and decrease in price of 10%.

Increase in price by 10 %

Selling price per game = £110

Break- even Sales =

= 300000 / ( 110 – 60)

= 300000 / 50

6000

Margin of Safety =

= (120000 – 6000) / 120000 * 100

= 112500 * 120000*100

= 95 %

With the increase in the sale price of the game, the break even point of the firm will also

reduce. This means that now the firm will be able to cover its cost by selling less products than

earlier. Also the margin of safety will increase for S plc.

Decrease in price by 10 %

Selling price per game = £90

Break- even Sales =

= 300000 / ( 90 – 60)

= 300000 / 30

10000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Margin of Safety =

= (120000 – 10000) / 120000 * 100

= 112500 * 120000*100

= 91.67 %

With the decrease in the price of product , the break even sales point of firm will reduce

which mean for covering the cast of manufacturing now, S plc would require to sell more

products which is up to 10000 units from 7500 units. Also the margin of safety will also reduce.

Critically analyse the assumption of cost volume profit analysis.

Cost volume profit analysis helps in determining the way in which changes in the cost

tends to affect the profit of the firm. Firms use this tool to determine the number of units it

requires to sell to gain minimum profits.

Critical analysis of the assumptions

Constant selling price- with the change in the volume of production, selling price in this

tool does not change which can negatively impact the analysis. As when number of units

increase, their costs tends to decrease and its impact on price is neglected (Labbe., 2017).

Division of cost sin fixed and variable- It created division among the cost incurred on

various products which means proper analysis on the basis of cost can be done.

SECTION-D

Compare the three categories of suppliers.

Suppliers are the persons, organisation or a firm which provides or sells goods or services

to its customers, normally the businesses. It acts as a middle man between the manufacturer and

the user of product by offering good quality material at effective rates. There are different types

of suppliers which have been distinguished below:

Strategic suppliers- These are the vendors on whom form trusts on, for good service and

supplies. They are long term partners of the firm and provides goods that are either tough

to arrange or a very important part for the success of product. The relationship with these

persons are usually tricky and requires special attention for ensuring regular supply of

raw material (Liu, Chiang and Tsai., 2020). But other then these, there are some other

preferred suppliers from whom all other requirements of material is fulfilled.

= (120000 – 10000) / 120000 * 100

= 112500 * 120000*100

= 91.67 %

With the decrease in the price of product , the break even sales point of firm will reduce

which mean for covering the cast of manufacturing now, S plc would require to sell more

products which is up to 10000 units from 7500 units. Also the margin of safety will also reduce.

Critically analyse the assumption of cost volume profit analysis.

Cost volume profit analysis helps in determining the way in which changes in the cost

tends to affect the profit of the firm. Firms use this tool to determine the number of units it

requires to sell to gain minimum profits.

Critical analysis of the assumptions

Constant selling price- with the change in the volume of production, selling price in this

tool does not change which can negatively impact the analysis. As when number of units

increase, their costs tends to decrease and its impact on price is neglected (Labbe., 2017).

Division of cost sin fixed and variable- It created division among the cost incurred on

various products which means proper analysis on the basis of cost can be done.

SECTION-D

Compare the three categories of suppliers.

Suppliers are the persons, organisation or a firm which provides or sells goods or services

to its customers, normally the businesses. It acts as a middle man between the manufacturer and

the user of product by offering good quality material at effective rates. There are different types

of suppliers which have been distinguished below:

Strategic suppliers- These are the vendors on whom form trusts on, for good service and

supplies. They are long term partners of the firm and provides goods that are either tough

to arrange or a very important part for the success of product. The relationship with these

persons are usually tricky and requires special attention for ensuring regular supply of

raw material (Liu, Chiang and Tsai., 2020). But other then these, there are some other

preferred suppliers from whom all other requirements of material is fulfilled.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Preferred suppliers- It is the person or the company which is pre-assessed by the firm

for arranging its supplies of goods and services. The process ensures that the party with

whom it will be dealing with help in the growth of business by providing goods in right

quantity, at correct time, and of high quality.

Transactional suppliers- It means to sign a contract of sale for providing specific types

of goods to the purchaser. There is a fixed time period in the the receiver of goods had to

make payment to the giver of product as per the agreement. These are usually made in the

cases of foreign suppliers as this case demands some sort of legal security regarding the

delivery of products (Mitik and et.al., 2017).

As discussed above all the above mentioned three suppliers are different form each other,

but the basic difference among them is the types of goods supplied by them. Where Strategic

ones deals in important products, preferred suppliers deals in remaining all kinds of products.

While transactional ones deals in the goods to be arranged from foreign parties.

Compare the advantages of single sourcing and multiple sourcing of procurement.

Single Sourcing means when a person or firm decides to purchase its raw material or

other inputs from a single vendor. It is the decision taken by the company by analysing the list of

number of vendors, out of which only one is shortlisted. Another usual process of this selection

is also based on bidding or quotation, from which, the business chooses the best one (Oleghe.,

2019).

Multiple sourcing means to arrange goods from the different number of vendors. In this

type, various vendors are contacted for fulfilling the need of raw materials.

Basis of advantages Single sourcing Multiple sourcing

Quality When a firm get its sources

from a same vendor, then there

are chances to get products of

same quality every time. This

is because, with time, the

vendor comes to know about

the exact requirement of the

buyer and tries to provide that

By adopting this technique, a

firm can have assess to various

qualities of same product,

according to which it can make

its goods as per its requirement

and quality it ants to choose

for a particular type of thing

(Sommer., 2018).

for arranging its supplies of goods and services. The process ensures that the party with

whom it will be dealing with help in the growth of business by providing goods in right

quantity, at correct time, and of high quality.

Transactional suppliers- It means to sign a contract of sale for providing specific types

of goods to the purchaser. There is a fixed time period in the the receiver of goods had to

make payment to the giver of product as per the agreement. These are usually made in the

cases of foreign suppliers as this case demands some sort of legal security regarding the

delivery of products (Mitik and et.al., 2017).

As discussed above all the above mentioned three suppliers are different form each other,

but the basic difference among them is the types of goods supplied by them. Where Strategic

ones deals in important products, preferred suppliers deals in remaining all kinds of products.

While transactional ones deals in the goods to be arranged from foreign parties.

Compare the advantages of single sourcing and multiple sourcing of procurement.

Single Sourcing means when a person or firm decides to purchase its raw material or

other inputs from a single vendor. It is the decision taken by the company by analysing the list of

number of vendors, out of which only one is shortlisted. Another usual process of this selection

is also based on bidding or quotation, from which, the business chooses the best one (Oleghe.,

2019).

Multiple sourcing means to arrange goods from the different number of vendors. In this

type, various vendors are contacted for fulfilling the need of raw materials.

Basis of advantages Single sourcing Multiple sourcing

Quality When a firm get its sources

from a same vendor, then there

are chances to get products of

same quality every time. This

is because, with time, the

vendor comes to know about

the exact requirement of the

buyer and tries to provide that

By adopting this technique, a

firm can have assess to various

qualities of same product,

according to which it can make

its goods as per its requirement

and quality it ants to choose

for a particular type of thing

(Sommer., 2018).

product with same quality.

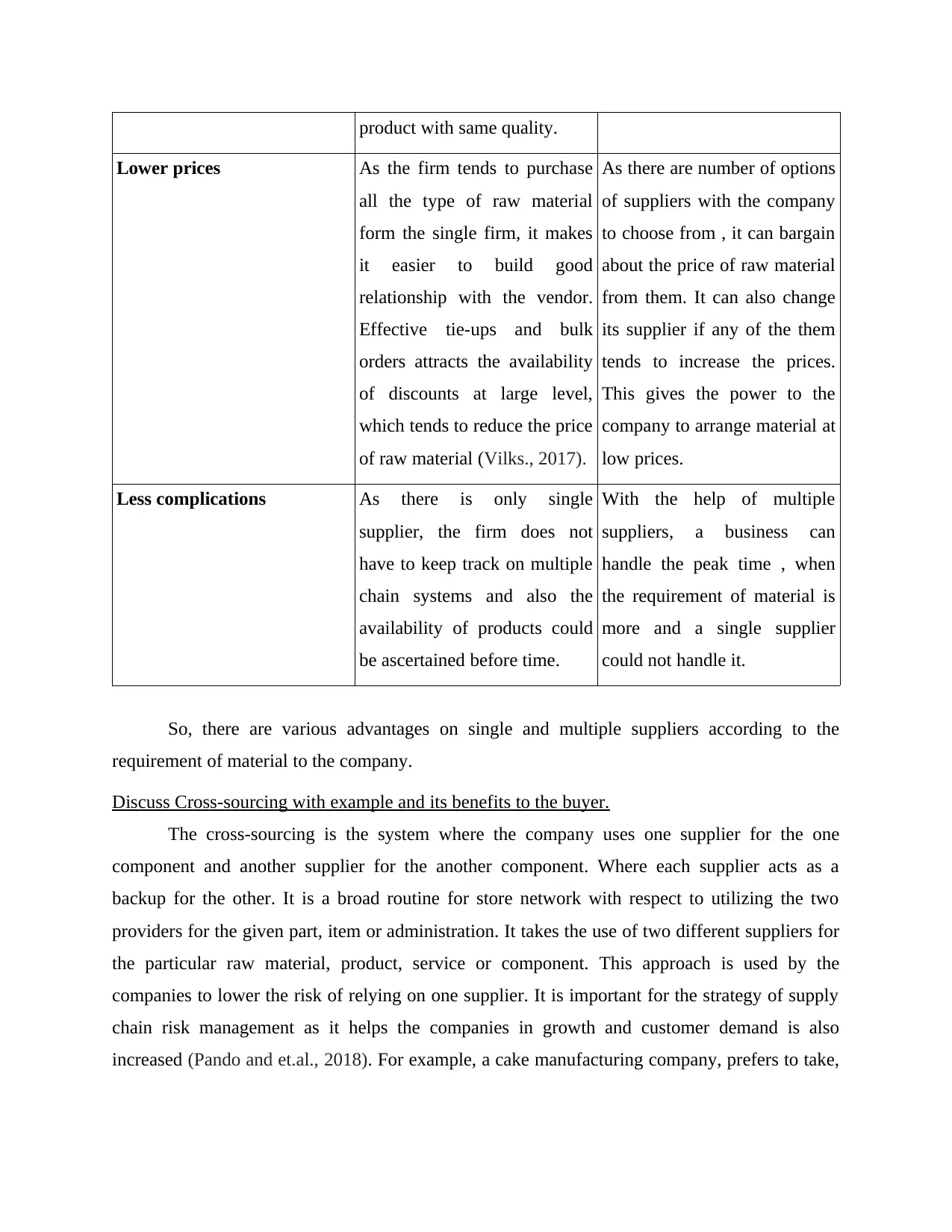

Lower prices As the firm tends to purchase

all the type of raw material

form the single firm, it makes

it easier to build good

relationship with the vendor.

Effective tie-ups and bulk

orders attracts the availability

of discounts at large level,

which tends to reduce the price

of raw material (Vilks., 2017).

As there are number of options

of suppliers with the company

to choose from , it can bargain

about the price of raw material

from them. It can also change

its supplier if any of the them

tends to increase the prices.

This gives the power to the

company to arrange material at

low prices.

Less complications As there is only single

supplier, the firm does not

have to keep track on multiple

chain systems and also the

availability of products could

be ascertained before time.

With the help of multiple

suppliers, a business can

handle the peak time , when

the requirement of material is

more and a single supplier

could not handle it.

So, there are various advantages on single and multiple suppliers according to the

requirement of material to the company.

Discuss Cross-sourcing with example and its benefits to the buyer.

The cross-sourcing is the system where the company uses one supplier for the one

component and another supplier for the another component. Where each supplier acts as a

backup for the other. It is a broad routine for store network with respect to utilizing the two

providers for the given part, item or administration. It takes the use of two different suppliers for

the particular raw material, product, service or component. This approach is used by the

companies to lower the risk of relying on one supplier. It is important for the strategy of supply

chain risk management as it helps the companies in growth and customer demand is also

increased (Pando and et.al., 2018). For example, a cake manufacturing company, prefers to take,

Lower prices As the firm tends to purchase

all the type of raw material

form the single firm, it makes

it easier to build good

relationship with the vendor.

Effective tie-ups and bulk

orders attracts the availability

of discounts at large level,

which tends to reduce the price

of raw material (Vilks., 2017).

As there are number of options

of suppliers with the company

to choose from , it can bargain

about the price of raw material

from them. It can also change

its supplier if any of the them

tends to increase the prices.

This gives the power to the

company to arrange material at

low prices.

Less complications As there is only single

supplier, the firm does not

have to keep track on multiple

chain systems and also the

availability of products could

be ascertained before time.

With the help of multiple

suppliers, a business can

handle the peak time , when

the requirement of material is

more and a single supplier

could not handle it.

So, there are various advantages on single and multiple suppliers according to the

requirement of material to the company.

Discuss Cross-sourcing with example and its benefits to the buyer.

The cross-sourcing is the system where the company uses one supplier for the one

component and another supplier for the another component. Where each supplier acts as a

backup for the other. It is a broad routine for store network with respect to utilizing the two

providers for the given part, item or administration. It takes the use of two different suppliers for

the particular raw material, product, service or component. This approach is used by the

companies to lower the risk of relying on one supplier. It is important for the strategy of supply

chain risk management as it helps the companies in growth and customer demand is also

increased (Pando and et.al., 2018). For example, a cake manufacturing company, prefers to take,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.