Financial Report: Investment Appraisal for Supanova Vacuum Cleaner

VerifiedAdded on 2023/06/13

|12

|2979

|117

Report

AI Summary

This report provides a comprehensive investment appraisal of Aspiradora Limited's potential project: manufacturing the Supanova vacuum cleaner. It estimates annual incremental cash flows, compares the Supanova project against expanding the existing Darkstar product line using Net Present Value (NPV) and other appraisal techniques, and addresses challenges in mutually exclusive project selection. The analysis favors the Supanova project due to its positive NPV, suggesting it will generate greater value for shareholders. The report concludes with a recommendation to continue the existing product line at a lower scale and invest in the new Supanova product, while acknowledging the importance of accurate cost of capital predictions and the benefits of economies of scale through expansion.

REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

(A) Estimation of Annual Incremental Cash Flows for The Manufacture of Supanova Vacuum

Cleaner....................................................................................................................................3

(B) Comparative Evaluation of the Two Projects Using Appropriate Appraisal Techniques:5

C) Problems arising using investment appraisal techniques when the projects are mutually

exclusive and discussion on assertion that expansion will generate value to shareholders:. .8

(D) Recommendation to Aspiradora regarding the course of action they have to implement:9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

(A) Estimation of Annual Incremental Cash Flows for The Manufacture of Supanova Vacuum

Cleaner....................................................................................................................................3

(B) Comparative Evaluation of the Two Projects Using Appropriate Appraisal Techniques:5

C) Problems arising using investment appraisal techniques when the projects are mutually

exclusive and discussion on assertion that expansion will generate value to shareholders:. .8

(D) Recommendation to Aspiradora regarding the course of action they have to implement:9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Investment appraisal techniques are financial instruments used in the organisation in order to

evaluate the feasibility of the desired project or not. There are numerous investment proposal

techniques such as Net present value method, profitability index, internal rate of return method,

average rate of return and so on (Spencer and et.al., 2019, July). The best method to evaluate the

desirability of the project is NPV method as it considers time value of money and is suitable

when we have to select one proposal amongst the two. In this report there are two alternative

options evaluating by the Aspiradora limited that is whether to introduce a new luxury product in

order to increase the sales in high end market that is bag less and cordless vacuum cleaner called

as Supanova or to go for expansion using the existing product that is Dark star by spending

certain amount of capital investment in market development as suggested by the marketing

managers of Aspiradora. At the end of this report certain recommendation is also provided to the

organisation with respect to selection and reason for the same. It is also recommended that

existing product that is Dark Star must be continue and lower amount of investment to be made

in new product so that its benefits cab be analysed.

TASK

(A) Estimation of Annual Incremental Cash Flows for The Manufacture of Supanova Vacuum

Cleaner.

The following statement has been prepared on the basis on information available. In

preparation of the statement the following assumption has been taken place:

The Selling price of Supanova has been constant throughout the period of 5 years

Capital allowance received from the government has been considered as inflow since it is

a rebate on actuation of plant and machinery and must be settled against it.

The working capital invested over the period of 5 years has been fully recovered at the

end of 5th year fully and all the accounts receivable and payable are settled accordingly.

There is negative cash balance in the form of inflow in year 1 because cost of plant and

machinery has been considered as cash outflow at the beginning.

Tax payable on capital gain will be settled at the end of fifth year assuming that it is paid

at the end of project life.

Investment appraisal techniques are financial instruments used in the organisation in order to

evaluate the feasibility of the desired project or not. There are numerous investment proposal

techniques such as Net present value method, profitability index, internal rate of return method,

average rate of return and so on (Spencer and et.al., 2019, July). The best method to evaluate the

desirability of the project is NPV method as it considers time value of money and is suitable

when we have to select one proposal amongst the two. In this report there are two alternative

options evaluating by the Aspiradora limited that is whether to introduce a new luxury product in

order to increase the sales in high end market that is bag less and cordless vacuum cleaner called

as Supanova or to go for expansion using the existing product that is Dark star by spending

certain amount of capital investment in market development as suggested by the marketing

managers of Aspiradora. At the end of this report certain recommendation is also provided to the

organisation with respect to selection and reason for the same. It is also recommended that

existing product that is Dark Star must be continue and lower amount of investment to be made

in new product so that its benefits cab be analysed.

TASK

(A) Estimation of Annual Incremental Cash Flows for The Manufacture of Supanova Vacuum

Cleaner.

The following statement has been prepared on the basis on information available. In

preparation of the statement the following assumption has been taken place:

The Selling price of Supanova has been constant throughout the period of 5 years

Capital allowance received from the government has been considered as inflow since it is

a rebate on actuation of plant and machinery and must be settled against it.

The working capital invested over the period of 5 years has been fully recovered at the

end of 5th year fully and all the accounts receivable and payable are settled accordingly.

There is negative cash balance in the form of inflow in year 1 because cost of plant and

machinery has been considered as cash outflow at the beginning.

Tax payable on capital gain will be settled at the end of fifth year assuming that it is paid

at the end of project life.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In calculating the incremental cash flows discounting has not been carried out as question

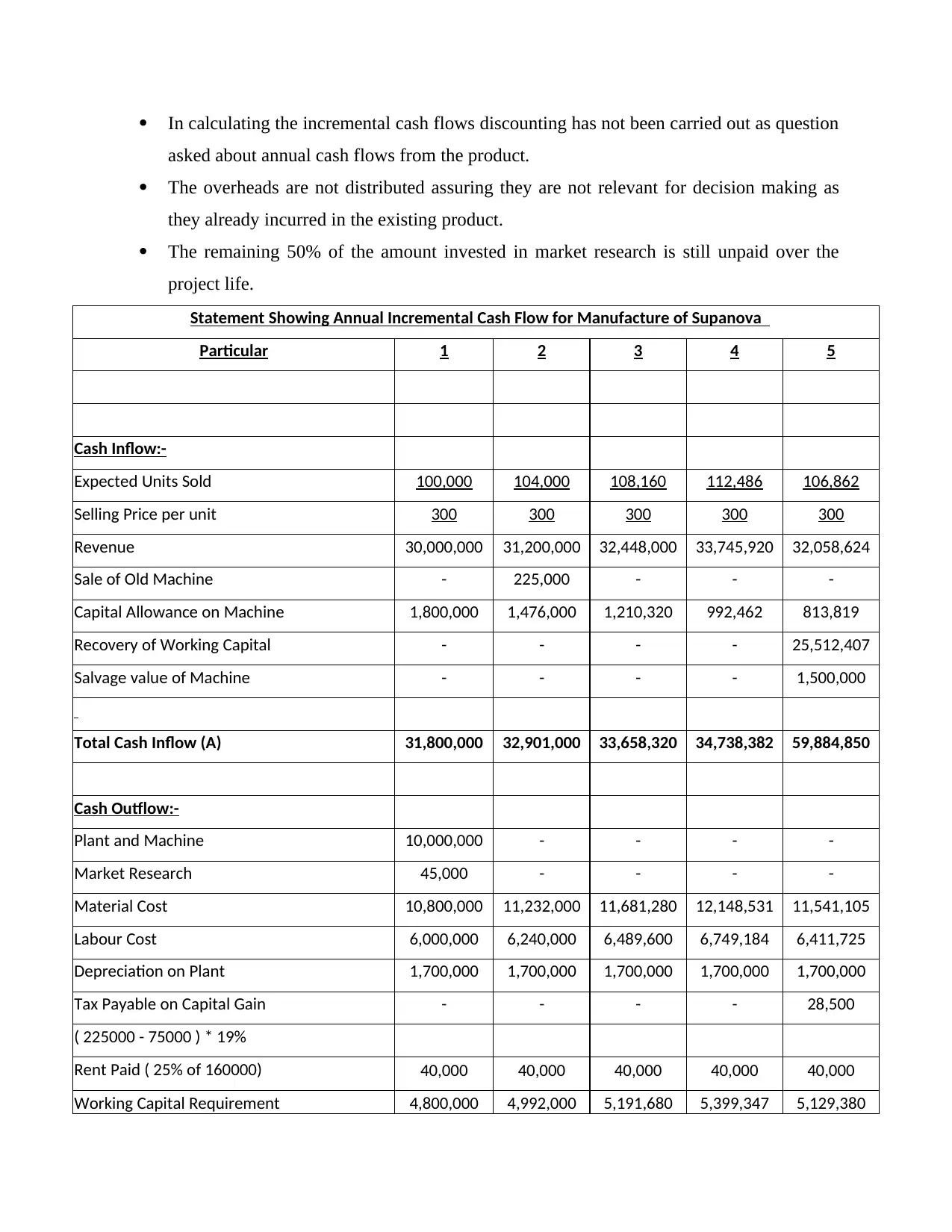

asked about annual cash flows from the product.

The overheads are not distributed assuring they are not relevant for decision making as

they already incurred in the existing product.

The remaining 50% of the amount invested in market research is still unpaid over the

project life.

Statement Showing Annual Incremental Cash Flow for Manufacture of Supanova

Particular 1 2 3 4 5

Cash Inflow:-

Expected Units Sold 100,000 104,000 108,160 112,486 106,862

Selling Price per unit 300 300 300 300 300

Revenue 30,000,000 31,200,000 32,448,000 33,745,920 32,058,624

Sale of Old Machine - 225,000 - - -

Capital Allowance on Machine 1,800,000 1,476,000 1,210,320 992,462 813,819

Recovery of Working Capital - - - - 25,512,407

Salvage value of Machine - - - - 1,500,000

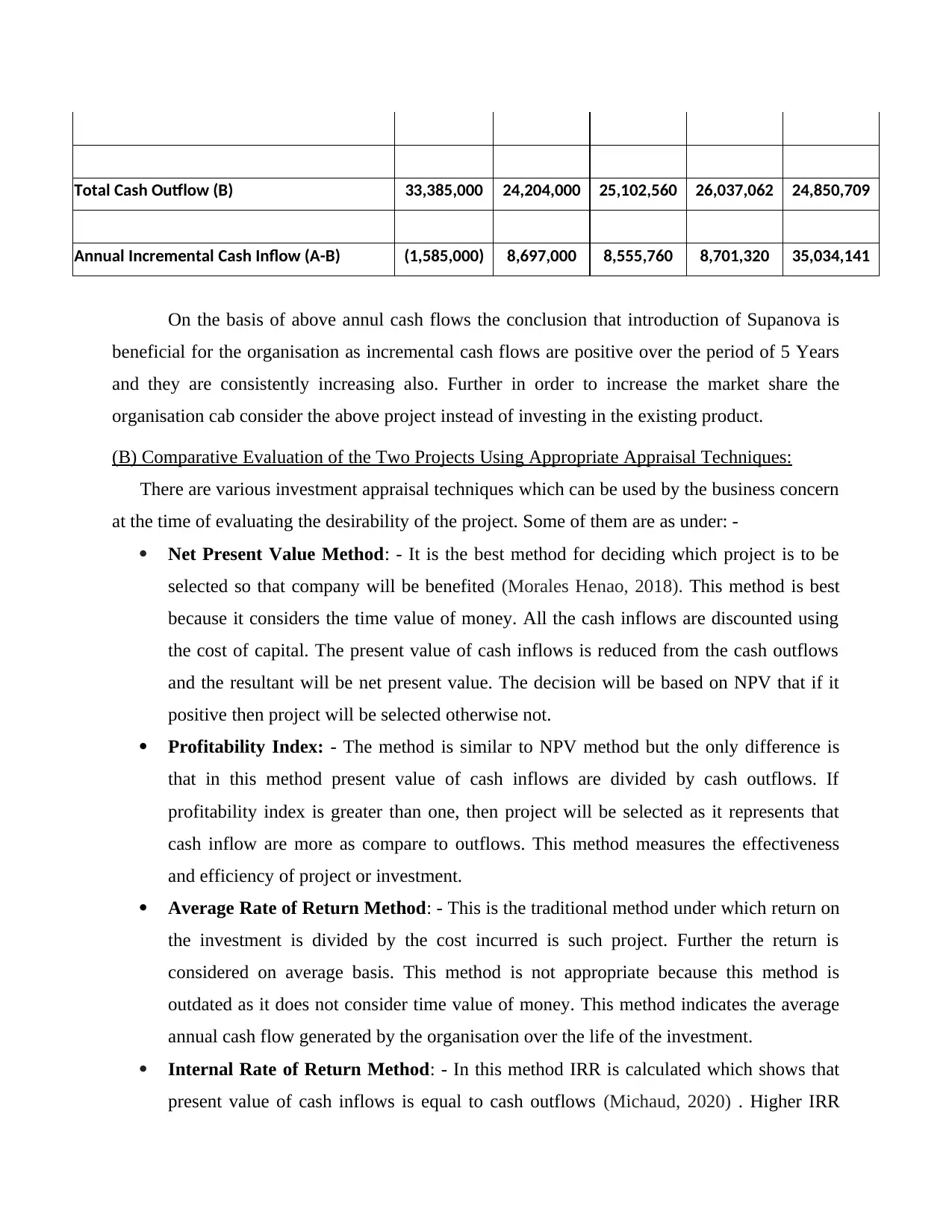

Total Cash Inflow (A) 31,800,000 32,901,000 33,658,320 34,738,382 59,884,850

Cash Outflow:-

Plant and Machine 10,000,000 - - - -

Market Research 45,000 - - - -

Material Cost 10,800,000 11,232,000 11,681,280 12,148,531 11,541,105

Labour Cost 6,000,000 6,240,000 6,489,600 6,749,184 6,411,725

Depreciation on Plant 1,700,000 1,700,000 1,700,000 1,700,000 1,700,000

Tax Payable on Capital Gain - - - - 28,500

( 225000 - 75000 ) * 19%

Rent Paid ( 25% of 160000) 40,000 40,000 40,000 40,000 40,000

Working Capital Requirement 4,800,000 4,992,000 5,191,680 5,399,347 5,129,380

asked about annual cash flows from the product.

The overheads are not distributed assuring they are not relevant for decision making as

they already incurred in the existing product.

The remaining 50% of the amount invested in market research is still unpaid over the

project life.

Statement Showing Annual Incremental Cash Flow for Manufacture of Supanova

Particular 1 2 3 4 5

Cash Inflow:-

Expected Units Sold 100,000 104,000 108,160 112,486 106,862

Selling Price per unit 300 300 300 300 300

Revenue 30,000,000 31,200,000 32,448,000 33,745,920 32,058,624

Sale of Old Machine - 225,000 - - -

Capital Allowance on Machine 1,800,000 1,476,000 1,210,320 992,462 813,819

Recovery of Working Capital - - - - 25,512,407

Salvage value of Machine - - - - 1,500,000

Total Cash Inflow (A) 31,800,000 32,901,000 33,658,320 34,738,382 59,884,850

Cash Outflow:-

Plant and Machine 10,000,000 - - - -

Market Research 45,000 - - - -

Material Cost 10,800,000 11,232,000 11,681,280 12,148,531 11,541,105

Labour Cost 6,000,000 6,240,000 6,489,600 6,749,184 6,411,725

Depreciation on Plant 1,700,000 1,700,000 1,700,000 1,700,000 1,700,000

Tax Payable on Capital Gain - - - - 28,500

( 225000 - 75000 ) * 19%

Rent Paid ( 25% of 160000) 40,000 40,000 40,000 40,000 40,000

Working Capital Requirement 4,800,000 4,992,000 5,191,680 5,399,347 5,129,380

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Cash Outflow (B) 33,385,000 24,204,000 25,102,560 26,037,062 24,850,709

Annual Incremental Cash Inflow (A-B) (1,585,000) 8,697,000 8,555,760 8,701,320 35,034,141

On the basis of above annul cash flows the conclusion that introduction of Supanova is

beneficial for the organisation as incremental cash flows are positive over the period of 5 Years

and they are consistently increasing also. Further in order to increase the market share the

organisation cab consider the above project instead of investing in the existing product.

(B) Comparative Evaluation of the Two Projects Using Appropriate Appraisal Techniques:

There are various investment appraisal techniques which can be used by the business concern

at the time of evaluating the desirability of the project. Some of them are as under: -

Net Present Value Method: - It is the best method for deciding which project is to be

selected so that company will be benefited (Morales Henao, 2018). This method is best

because it considers the time value of money. All the cash inflows are discounted using

the cost of capital. The present value of cash inflows is reduced from the cash outflows

and the resultant will be net present value. The decision will be based on NPV that if it

positive then project will be selected otherwise not.

Profitability Index: - The method is similar to NPV method but the only difference is

that in this method present value of cash inflows are divided by cash outflows. If

profitability index is greater than one, then project will be selected as it represents that

cash inflow are more as compare to outflows. This method measures the effectiveness

and efficiency of project or investment.

Average Rate of Return Method: - This is the traditional method under which return on

the investment is divided by the cost incurred is such project. Further the return is

considered on average basis. This method is not appropriate because this method is

outdated as it does not consider time value of money. This method indicates the average

annual cash flow generated by the organisation over the life of the investment.

Internal Rate of Return Method: - In this method IRR is calculated which shows that

present value of cash inflows is equal to cash outflows (Michaud, 2020) . Higher IRR

Annual Incremental Cash Inflow (A-B) (1,585,000) 8,697,000 8,555,760 8,701,320 35,034,141

On the basis of above annul cash flows the conclusion that introduction of Supanova is

beneficial for the organisation as incremental cash flows are positive over the period of 5 Years

and they are consistently increasing also. Further in order to increase the market share the

organisation cab consider the above project instead of investing in the existing product.

(B) Comparative Evaluation of the Two Projects Using Appropriate Appraisal Techniques:

There are various investment appraisal techniques which can be used by the business concern

at the time of evaluating the desirability of the project. Some of them are as under: -

Net Present Value Method: - It is the best method for deciding which project is to be

selected so that company will be benefited (Morales Henao, 2018). This method is best

because it considers the time value of money. All the cash inflows are discounted using

the cost of capital. The present value of cash inflows is reduced from the cash outflows

and the resultant will be net present value. The decision will be based on NPV that if it

positive then project will be selected otherwise not.

Profitability Index: - The method is similar to NPV method but the only difference is

that in this method present value of cash inflows are divided by cash outflows. If

profitability index is greater than one, then project will be selected as it represents that

cash inflow are more as compare to outflows. This method measures the effectiveness

and efficiency of project or investment.

Average Rate of Return Method: - This is the traditional method under which return on

the investment is divided by the cost incurred is such project. Further the return is

considered on average basis. This method is not appropriate because this method is

outdated as it does not consider time value of money. This method indicates the average

annual cash flow generated by the organisation over the life of the investment.

Internal Rate of Return Method: - In this method IRR is calculated which shows that

present value of cash inflows is equal to cash outflows (Michaud, 2020) . Higher IRR

denotes that project is financially feasible as it justifies that inflows are more as compare

to cash outflows. IRR is the discount rate that make the net present value nil as to make

cash outflows and inflows equals at the desired rate.

Payback Period: - This method simply indicates that how much time is required by the

project to recover the investment made in it at the beginning of the year. Those project

will be selected whole payback is lower as it showcases that the organisation will recover

its cost at the rapid rate and enjoys the benefit afterword’s.

When we carried out the comparative analysis of the projects under consideration that is

whether to introduced Supanova or to continue with Darkstar model then above techniques needs

to implemented. As NPV is best among all the method therefore feasibility is calculated as

under: -

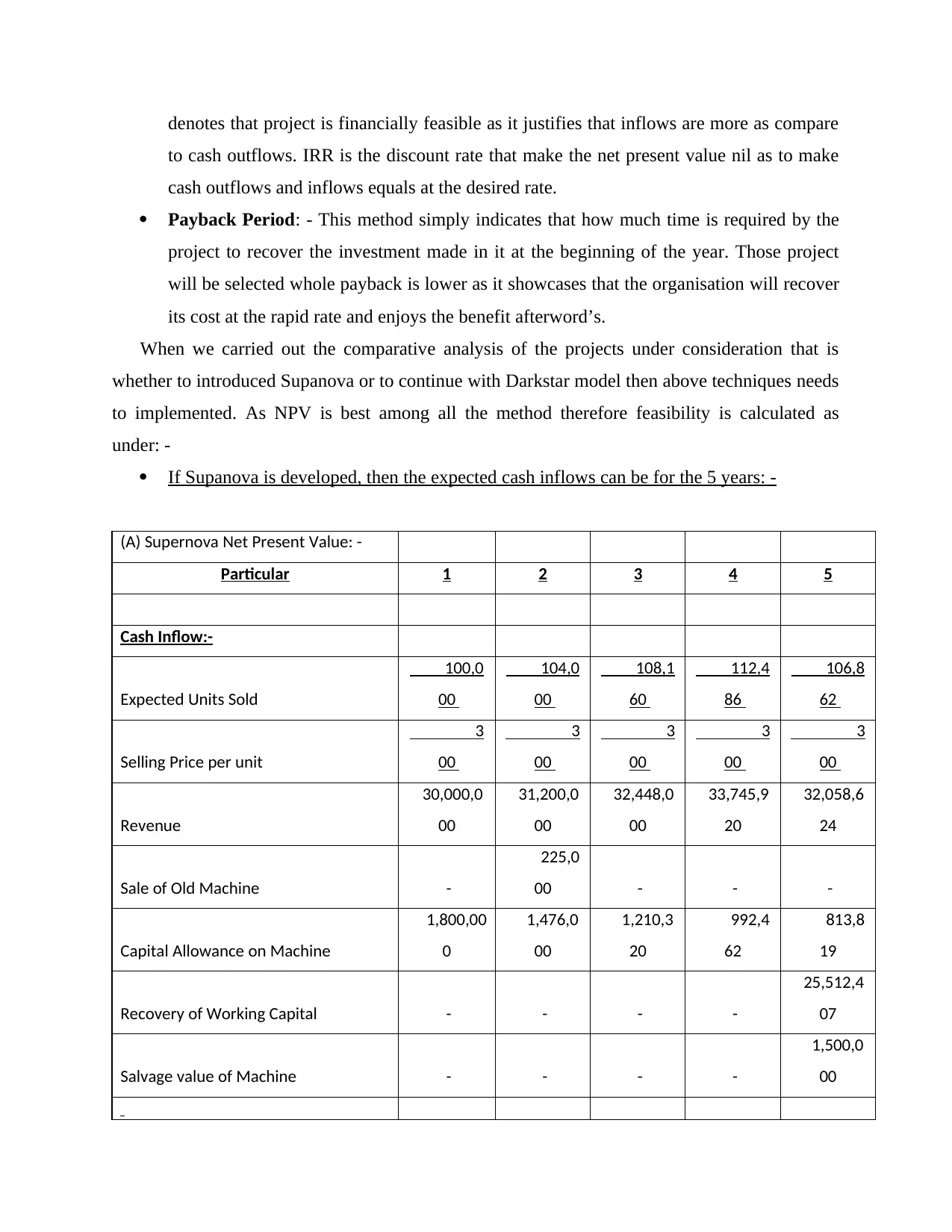

If Supanova is developed, then the expected cash inflows can be for the 5 years: -

(A) Supernova Net Present Value: -

Particular 1 2 3 4 5

Cash Inflow:-

Expected Units Sold

100,0

00

104,0

00

108,1

60

112,4

86

106,8

62

Selling Price per unit

3

00

3

00

3

00

3

00

3

00

Revenue

30,000,0

00

31,200,0

00

32,448,0

00

33,745,9

20

32,058,6

24

Sale of Old Machine -

225,0

00 - - -

Capital Allowance on Machine

1,800,00

0

1,476,0

00

1,210,3

20

992,4

62

813,8

19

Recovery of Working Capital - - - -

25,512,4

07

Salvage value of Machine - - - -

1,500,0

00

to cash outflows. IRR is the discount rate that make the net present value nil as to make

cash outflows and inflows equals at the desired rate.

Payback Period: - This method simply indicates that how much time is required by the

project to recover the investment made in it at the beginning of the year. Those project

will be selected whole payback is lower as it showcases that the organisation will recover

its cost at the rapid rate and enjoys the benefit afterword’s.

When we carried out the comparative analysis of the projects under consideration that is

whether to introduced Supanova or to continue with Darkstar model then above techniques needs

to implemented. As NPV is best among all the method therefore feasibility is calculated as

under: -

If Supanova is developed, then the expected cash inflows can be for the 5 years: -

(A) Supernova Net Present Value: -

Particular 1 2 3 4 5

Cash Inflow:-

Expected Units Sold

100,0

00

104,0

00

108,1

60

112,4

86

106,8

62

Selling Price per unit

3

00

3

00

3

00

3

00

3

00

Revenue

30,000,0

00

31,200,0

00

32,448,0

00

33,745,9

20

32,058,6

24

Sale of Old Machine -

225,0

00 - - -

Capital Allowance on Machine

1,800,00

0

1,476,0

00

1,210,3

20

992,4

62

813,8

19

Recovery of Working Capital - - - -

25,512,4

07

Salvage value of Machine - - - -

1,500,0

00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Cash Inflow (A)

31,800,0

00

32,901,0

00

33,658,3

20

34,738,3

82

59,884,8

50

Cash Outflow:-

Plant and Machine

10,000,0

00 - - - -

Market Research

45,0

00 - - - -

Material Cost

10,800,0

00

11,232,0

00

11,681,2

80

12,148,5

31

11,541,1

05

Labor Cost

6,000,00

0

6,240,0

00

6,489,6

00

6,749,1

84

6,411,7

25

Depreciation on Plant

1,700,00

0

1,700,0

00

1,700,0

00

1,700,0

00

1,700,0

00

Tax Payable on Capital Gain - - - -

28,5

00

( 225000 - 75000 ) * 19%

Rent Paid( 25% of 160000)

40,0

00

40,0

00

40,0

00

40,0

00

40,0

00

Working Capital Requirement

4,800,00

0

4,992,0

00

5,191,6

80

5,399,3

47

5,129,3

80

Total Cash Outflow (B) 33,385,000 24,204,000 25,102,560 26,037,062 24,850,709

Annual Incremental Cash Inflow (A-B) (1,585,000) 8,697,000 8,555,760 8,701,320 35,034,141

Discounting @ 13% 0.885 0.783 0.693 0.613 0.543

Present Value of Cash Inflow

31,800,0

00

32,901,0

00

33,658,3

20

34,738,3

82

59,884,8

50

Cash Outflow:-

Plant and Machine

10,000,0

00 - - - -

Market Research

45,0

00 - - - -

Material Cost

10,800,0

00

11,232,0

00

11,681,2

80

12,148,5

31

11,541,1

05

Labor Cost

6,000,00

0

6,240,0

00

6,489,6

00

6,749,1

84

6,411,7

25

Depreciation on Plant

1,700,00

0

1,700,0

00

1,700,0

00

1,700,0

00

1,700,0

00

Tax Payable on Capital Gain - - - -

28,5

00

( 225000 - 75000 ) * 19%

Rent Paid( 25% of 160000)

40,0

00

40,0

00

40,0

00

40,0

00

40,0

00

Working Capital Requirement

4,800,00

0

4,992,0

00

5,191,6

80

5,399,3

47

5,129,3

80

Total Cash Outflow (B) 33,385,000 24,204,000 25,102,560 26,037,062 24,850,709

Annual Incremental Cash Inflow (A-B) (1,585,000) 8,697,000 8,555,760 8,701,320 35,034,141

Discounting @ 13% 0.885 0.783 0.693 0.613 0.543

Present Value of Cash Inflow

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

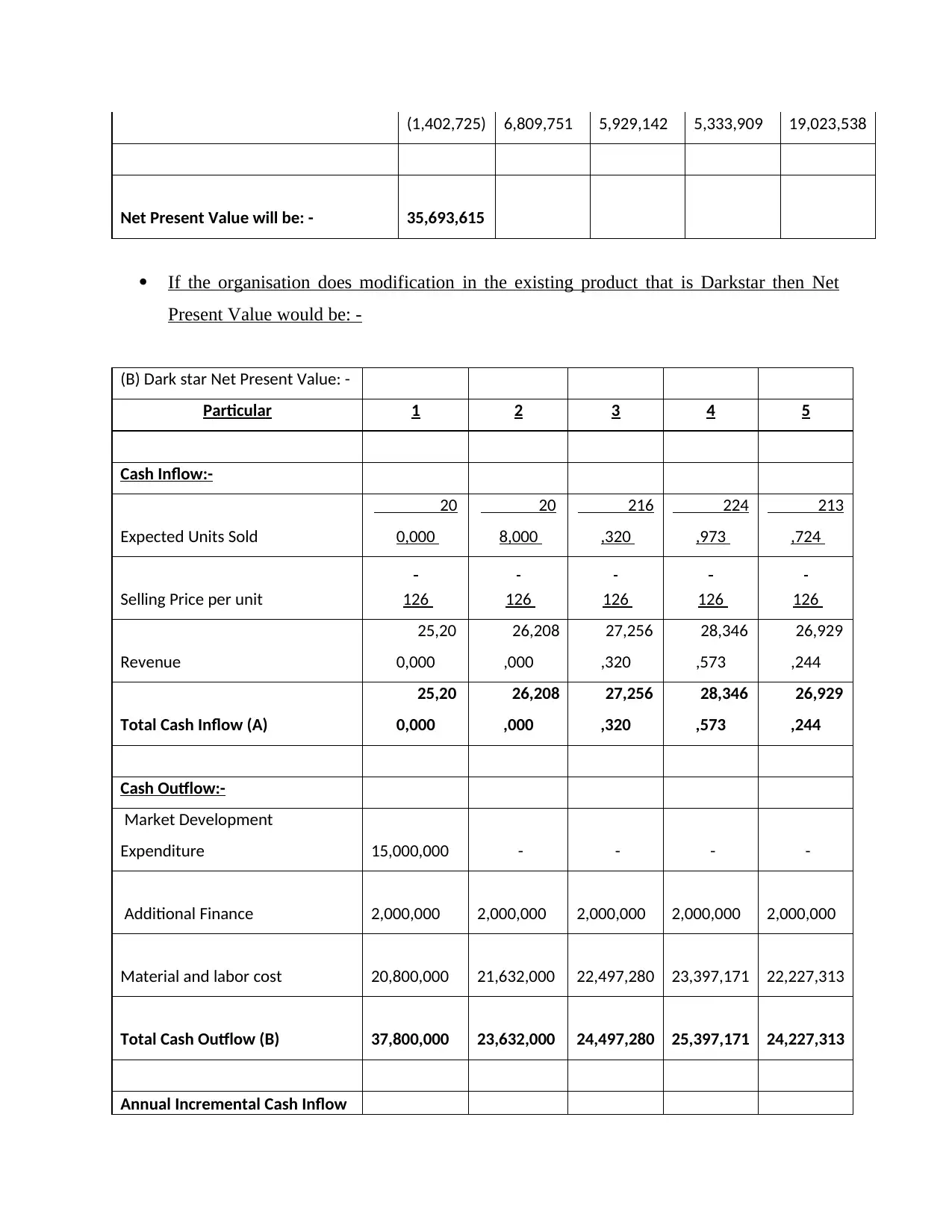

(1,402,725) 6,809,751 5,929,142 5,333,909 19,023,538

Net Present Value will be: - 35,693,615

If the organisation does modification in the existing product that is Darkstar then Net

Present Value would be: -

(B) Dark star Net Present Value: -

Particular 1 2 3 4 5

Cash Inflow:-

Expected Units Sold

20

0,000

20

8,000

216

,320

224

,973

213

,724

Selling Price per unit 126 126 126 126 126

Revenue

25,20

0,000

26,208

,000

27,256

,320

28,346

,573

26,929

,244

Total Cash Inflow (A)

25,20

0,000

26,208

,000

27,256

,320

28,346

,573

26,929

,244

Cash Outflow:-

Market Development

Expenditure 15,000,000 - - - -

Additional Finance 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000

Material and labor cost 20,800,000 21,632,000 22,497,280 23,397,171 22,227,313

Total Cash Outflow (B) 37,800,000 23,632,000 24,497,280 25,397,171 24,227,313

Annual Incremental Cash Inflow

Net Present Value will be: - 35,693,615

If the organisation does modification in the existing product that is Darkstar then Net

Present Value would be: -

(B) Dark star Net Present Value: -

Particular 1 2 3 4 5

Cash Inflow:-

Expected Units Sold

20

0,000

20

8,000

216

,320

224

,973

213

,724

Selling Price per unit 126 126 126 126 126

Revenue

25,20

0,000

26,208

,000

27,256

,320

28,346

,573

26,929

,244

Total Cash Inflow (A)

25,20

0,000

26,208

,000

27,256

,320

28,346

,573

26,929

,244

Cash Outflow:-

Market Development

Expenditure 15,000,000 - - - -

Additional Finance 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000

Material and labor cost 20,800,000 21,632,000 22,497,280 23,397,171 22,227,313

Total Cash Outflow (B) 37,800,000 23,632,000 24,497,280 25,397,171 24,227,313

Annual Incremental Cash Inflow

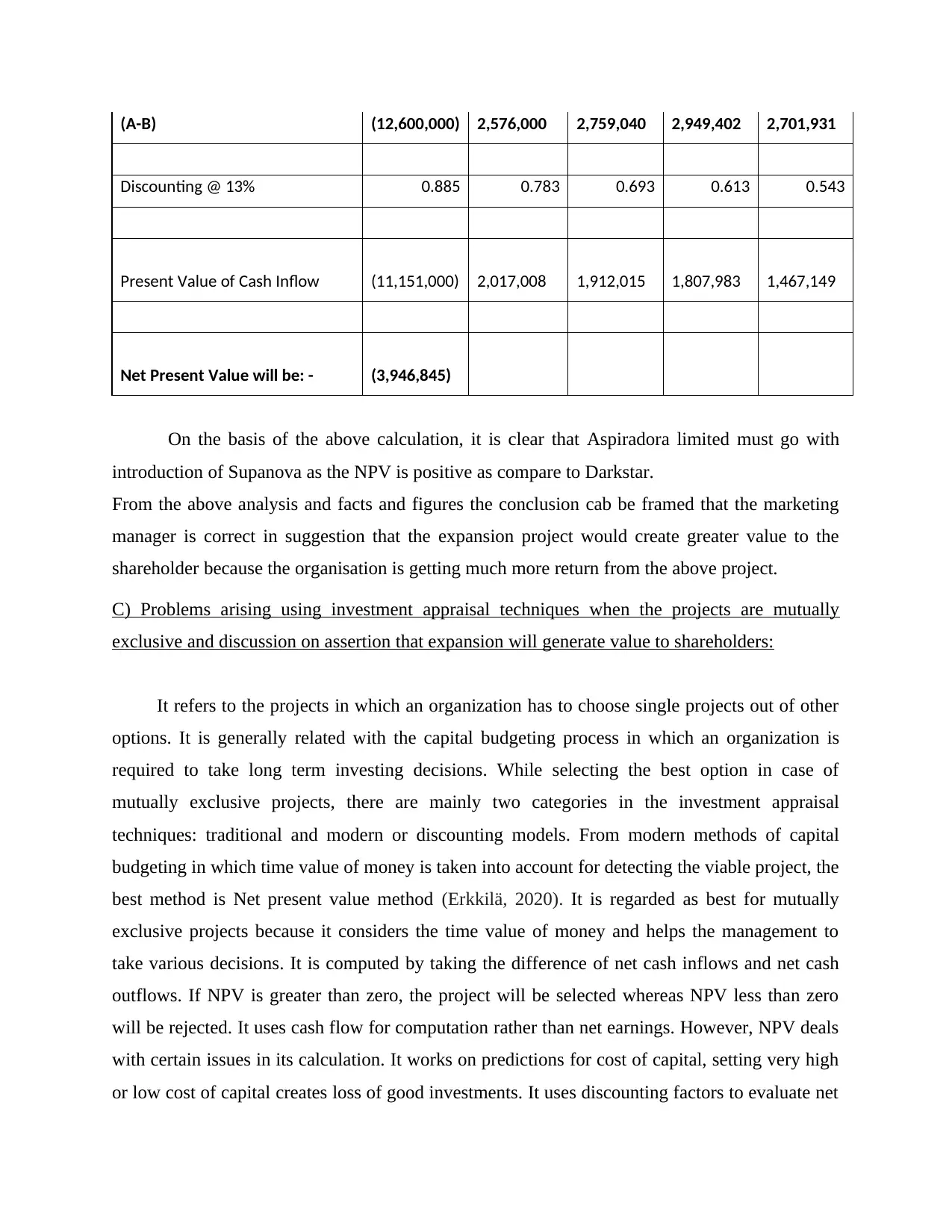

(A-B) (12,600,000) 2,576,000 2,759,040 2,949,402 2,701,931

Discounting @ 13% 0.885 0.783 0.693 0.613 0.543

Present Value of Cash Inflow (11,151,000) 2,017,008 1,912,015 1,807,983 1,467,149

Net Present Value will be: - (3,946,845)

On the basis of the above calculation, it is clear that Aspiradora limited must go with

introduction of Supanova as the NPV is positive as compare to Darkstar.

From the above analysis and facts and figures the conclusion cab be framed that the marketing

manager is correct in suggestion that the expansion project would create greater value to the

shareholder because the organisation is getting much more return from the above project.

C) Problems arising using investment appraisal techniques when the projects are mutually

exclusive and discussion on assertion that expansion will generate value to shareholders:

It refers to the projects in which an organization has to choose single projects out of other

options. It is generally related with the capital budgeting process in which an organization is

required to take long term investing decisions. While selecting the best option in case of

mutually exclusive projects, there are mainly two categories in the investment appraisal

techniques: traditional and modern or discounting models. From modern methods of capital

budgeting in which time value of money is taken into account for detecting the viable project, the

best method is Net present value method (Erkkilä, 2020). It is regarded as best for mutually

exclusive projects because it considers the time value of money and helps the management to

take various decisions. It is computed by taking the difference of net cash inflows and net cash

outflows. If NPV is greater than zero, the project will be selected whereas NPV less than zero

will be rejected. It uses cash flow for computation rather than net earnings. However, NPV deals

with certain issues in its calculation. It works on predictions for cost of capital, setting very high

or low cost of capital creates loss of good investments. It uses discounting factors to evaluate net

Discounting @ 13% 0.885 0.783 0.693 0.613 0.543

Present Value of Cash Inflow (11,151,000) 2,017,008 1,912,015 1,807,983 1,467,149

Net Present Value will be: - (3,946,845)

On the basis of the above calculation, it is clear that Aspiradora limited must go with

introduction of Supanova as the NPV is positive as compare to Darkstar.

From the above analysis and facts and figures the conclusion cab be framed that the marketing

manager is correct in suggestion that the expansion project would create greater value to the

shareholder because the organisation is getting much more return from the above project.

C) Problems arising using investment appraisal techniques when the projects are mutually

exclusive and discussion on assertion that expansion will generate value to shareholders:

It refers to the projects in which an organization has to choose single projects out of other

options. It is generally related with the capital budgeting process in which an organization is

required to take long term investing decisions. While selecting the best option in case of

mutually exclusive projects, there are mainly two categories in the investment appraisal

techniques: traditional and modern or discounting models. From modern methods of capital

budgeting in which time value of money is taken into account for detecting the viable project, the

best method is Net present value method (Erkkilä, 2020). It is regarded as best for mutually

exclusive projects because it considers the time value of money and helps the management to

take various decisions. It is computed by taking the difference of net cash inflows and net cash

outflows. If NPV is greater than zero, the project will be selected whereas NPV less than zero

will be rejected. It uses cash flow for computation rather than net earnings. However, NPV deals

with certain issues in its calculation. It works on predictions for cost of capital, setting very high

or low cost of capital creates loss of good investments. It uses discounting factors to evaluate net

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

present value which makes this tool complex. In case of expansion, the economies of scale can

be achieved and organization will offer more incentives and dividend to its employees. The use

of expansion strategies helps to capture good market shares and increases the earning per share

of the enterprise.

(D) Recommendation to Aspiradora regarding the course of action they have to implement:

It is recommended to the organisation that instead of discontinuing their existing product

they must continue it lower scale of production so that they can get the benefit of economies of

scale. Further since both the products are vacuum cleaner therefore their manufacturing facilities

cab be mixed up together so that cost of the entity has been reduced. It is given in the question

that Supanova is more expensive as the organisation needs to install new machinery for the same.

Another alternate is available that entity can overtakes similar venture so that synergy benefit

they can get. Further if they discontinue their existing products then they lose their existing

customer as Darkstar is their hit product. They can use customised and advantage technology in

order to upgrade the same that will reduce the burden on expenses over them. Further the major

factor that the organisation is ignoring is that these are the projected results of Supanova. Their

might be the possibility that go beyond or against the expectation and as a result of which the

entity will nowhere as they discontinue the current line. When the organisation are dealing with

mutually exclusive project not doubt the cost will reduce to dismantle one project however it also

includes risk on the organisation that if the new product on which the business concern is relying

fails than it is difficult for them to survive in the competition.

be achieved and organization will offer more incentives and dividend to its employees. The use

of expansion strategies helps to capture good market shares and increases the earning per share

of the enterprise.

(D) Recommendation to Aspiradora regarding the course of action they have to implement:

It is recommended to the organisation that instead of discontinuing their existing product

they must continue it lower scale of production so that they can get the benefit of economies of

scale. Further since both the products are vacuum cleaner therefore their manufacturing facilities

cab be mixed up together so that cost of the entity has been reduced. It is given in the question

that Supanova is more expensive as the organisation needs to install new machinery for the same.

Another alternate is available that entity can overtakes similar venture so that synergy benefit

they can get. Further if they discontinue their existing products then they lose their existing

customer as Darkstar is their hit product. They can use customised and advantage technology in

order to upgrade the same that will reduce the burden on expenses over them. Further the major

factor that the organisation is ignoring is that these are the projected results of Supanova. Their

might be the possibility that go beyond or against the expectation and as a result of which the

entity will nowhere as they discontinue the current line. When the organisation are dealing with

mutually exclusive project not doubt the cost will reduce to dismantle one project however it also

includes risk on the organisation that if the new product on which the business concern is relying

fails than it is difficult for them to survive in the competition.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above projects the conclusion can be drawn that decision making with respect to

selection of products requires inverse research considering the structure of the entity and further

estimated cost and expenditure the organisation incurs or earn in implementing that desired

project or product. Further when the organisation is evaluating about selecting mutually

exclusive projects then decision should be taken on implemented appraisal techniques such as

Net present value, profitability index, internal rate of return and so on. In this report Aspiradora

limited wants to analyse regarding the feasibility of Supanove their new bag less and cordless

vacuum cleaner as compare to their existing product which is Darkstar. Since the sale of Darkstar

is decreasing therefore the company is planning to implement the new product. However, this

product is mutually exclusive therefore decision will take in the above mentioned report on the

basis of using appraisal technique. At the end of this report certain recommendation is also

provided to the organisation with respect to selection and reason for the same. It is also

recommended that existing product that is Dark Star must be continue and lower amount of

investment to be made in new product so that its benefits cab be analysed.

From the above projects the conclusion can be drawn that decision making with respect to

selection of products requires inverse research considering the structure of the entity and further

estimated cost and expenditure the organisation incurs or earn in implementing that desired

project or product. Further when the organisation is evaluating about selecting mutually

exclusive projects then decision should be taken on implemented appraisal techniques such as

Net present value, profitability index, internal rate of return and so on. In this report Aspiradora

limited wants to analyse regarding the feasibility of Supanove their new bag less and cordless

vacuum cleaner as compare to their existing product which is Darkstar. Since the sale of Darkstar

is decreasing therefore the company is planning to implement the new product. However, this

product is mutually exclusive therefore decision will take in the above mentioned report on the

basis of using appraisal technique. At the end of this report certain recommendation is also

provided to the organisation with respect to selection and reason for the same. It is also

recommended that existing product that is Dark Star must be continue and lower amount of

investment to be made in new product so that its benefits cab be analysed.

REFERENCES

Books and Journals

Amran and et.al., 2018. Financial Literacy among Malaysian Households in Managing

Income. Indian Journal of Public Health Research & Development, 9(11).

Basile, I. and Neunuebel, C., 2019. Blended finance in fragile contexts: opportunities and risks.

De Swaan, J.C., 2020. Seeking Virtue in Finance: Contributing to Society in a Conflicted

Industry. Cambridge University Press.

Erkkilä, S., 2020. Managing voluntary employee turnover with HR analytics.

Foltys, J. and Strojek-Filus, M., 2019. Selected Problems of Managing Intangible Assets in a

Modern Enterprise in the Aspect of Accounting. Zeszyty Naukowe Wyższej Szkoły

Humanitas. Zarządzanie. (4). pp.147-170.

Gomez-Conde and et.al., 2021. The Effect of Management Control Systems in Managing the

Unknown: Does the Market Appreciate the Breadth of Vision? Available at SSRN

3675688.

Kelkar, A.S. and Ramachandran, N., 2020, November. Impact of Uncertainty on Financial

Performance: An Analytical Review with Reference to Accounting, Corporate Finance

and Auditing. In International Conference on Business and Technology (pp. 1474-1486).

Springer, Cham.

Michaud, S., 2020. Bright Ideas: Hoag HTM Takes the Lead on Managing Equipment Life

Cycles. Biomedical Instrumentation & Technology. 54(3). pp.212-215.

Morales Henao, A., 2018. Calculating for Managing: The Emergence of the Idea of Risk

Management. Apuntes Contables, (21).

Pawlak, R., 2019. Practical aspects of applying the selected model of managing knowledge

derived from project experience. E-mentor. 81(4). p.47.

Spencer and et.al., 2019, July. Routine Regulation as a Source for Managing Conflict within

Alliances: An Integrative Framework. In Academy of Management Proceedings (Vol.

2019, No. 1, p. 15160). Briarcliff Manor, NY 10510: Academy of Management.

Webb, T., 2018. Managing match officials. Routledge Handbook of Football Business and

Management.

Books and Journals

Amran and et.al., 2018. Financial Literacy among Malaysian Households in Managing

Income. Indian Journal of Public Health Research & Development, 9(11).

Basile, I. and Neunuebel, C., 2019. Blended finance in fragile contexts: opportunities and risks.

De Swaan, J.C., 2020. Seeking Virtue in Finance: Contributing to Society in a Conflicted

Industry. Cambridge University Press.

Erkkilä, S., 2020. Managing voluntary employee turnover with HR analytics.

Foltys, J. and Strojek-Filus, M., 2019. Selected Problems of Managing Intangible Assets in a

Modern Enterprise in the Aspect of Accounting. Zeszyty Naukowe Wyższej Szkoły

Humanitas. Zarządzanie. (4). pp.147-170.

Gomez-Conde and et.al., 2021. The Effect of Management Control Systems in Managing the

Unknown: Does the Market Appreciate the Breadth of Vision? Available at SSRN

3675688.

Kelkar, A.S. and Ramachandran, N., 2020, November. Impact of Uncertainty on Financial

Performance: An Analytical Review with Reference to Accounting, Corporate Finance

and Auditing. In International Conference on Business and Technology (pp. 1474-1486).

Springer, Cham.

Michaud, S., 2020. Bright Ideas: Hoag HTM Takes the Lead on Managing Equipment Life

Cycles. Biomedical Instrumentation & Technology. 54(3). pp.212-215.

Morales Henao, A., 2018. Calculating for Managing: The Emergence of the Idea of Risk

Management. Apuntes Contables, (21).

Pawlak, R., 2019. Practical aspects of applying the selected model of managing knowledge

derived from project experience. E-mentor. 81(4). p.47.

Spencer and et.al., 2019, July. Routine Regulation as a Source for Managing Conflict within

Alliances: An Integrative Framework. In Academy of Management Proceedings (Vol.

2019, No. 1, p. 15160). Briarcliff Manor, NY 10510: Academy of Management.

Webb, T., 2018. Managing match officials. Routledge Handbook of Football Business and

Management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.