Investment Appraisal Techniques: Risk Analysis, CAPM, and Allocation

VerifiedAdded on 2023/06/15

|11

|2025

|195

Report

AI Summary

This report provides a detailed analysis of investment appraisal techniques, including payback period, internal rate of return (IRR), net present value (NPV), and profitability index. It examines the merits and demerits of the IRR rule, determines the optimal allocation of an investment budget among different projects, and discusses the distinction between hard and soft capital rationing. Furthermore, the report calculates the systematic risk, non-systematic risk, and total risk of equity shares, assessing which company's returns are better explained by market returns and calculating the expected equilibrium risk-premium for each share. The analysis concludes that these techniques are crucial for making informed investment decisions.

Investment Appraisal

Techniques Risk and the

CAPM

Techniques Risk and the

CAPM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

(a) Calculation..........................................................................................................................................3

(b) Briefly discuss the merits and demerits of the internal rate of return rule........................................4

QUESTION 2.................................................................................................................................................5

Determine the optimal allocation of the investment budget among these projects...............................5

(b) Discuss the distinction between hard and soft capital rationing........................................................5

QUESTION 3.................................................................................................................................................6

(a) Calculate the systematic risk, the non-systematic risk and the total risk (𝜎𝑖 2 ) of the equity shares

of Vodafone Group and BT Group...........................................................................................................6

(b) Which company’s returns are better explained by the market’s returns?.........................................9

(c) Calculate the expected equilibrium risk-premium for each of the two shares. Comment on the

results......................................................................................................................................................9

CONCLUSION...............................................................................................................................................9

REFERENCES..............................................................................................................................................10

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

(a) Calculation..........................................................................................................................................3

(b) Briefly discuss the merits and demerits of the internal rate of return rule........................................4

QUESTION 2.................................................................................................................................................5

Determine the optimal allocation of the investment budget among these projects...............................5

(b) Discuss the distinction between hard and soft capital rationing........................................................5

QUESTION 3.................................................................................................................................................6

(a) Calculate the systematic risk, the non-systematic risk and the total risk (𝜎𝑖 2 ) of the equity shares

of Vodafone Group and BT Group...........................................................................................................6

(b) Which company’s returns are better explained by the market’s returns?.........................................9

(c) Calculate the expected equilibrium risk-premium for each of the two shares. Comment on the

results......................................................................................................................................................9

CONCLUSION...............................................................................................................................................9

REFERENCES..............................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Investment decisions are critical for all enterprises even though they affect both their

potential to succeed and their eventual business model. Investments typically involve large initial

financial expenditures, locking up substantial amounts of money. Payback period, internal rate of

return, net present value, profitability index, and net profit ratio are investment assessment

approaches. They are generally intended to assess the success of a new initiative. Whenever

embarking on any new Endeavour, the first thing to know is, "Is it sustainable or financially

viable?" These strategies provide excellent answers to this question. Every approach assesses the

topic from a distinct perspective and delivers a unique perspective. Let's take a quick look at

these strategies. This report based on the different investment appraisal techniques which is used

by various organisation with investment purpose.

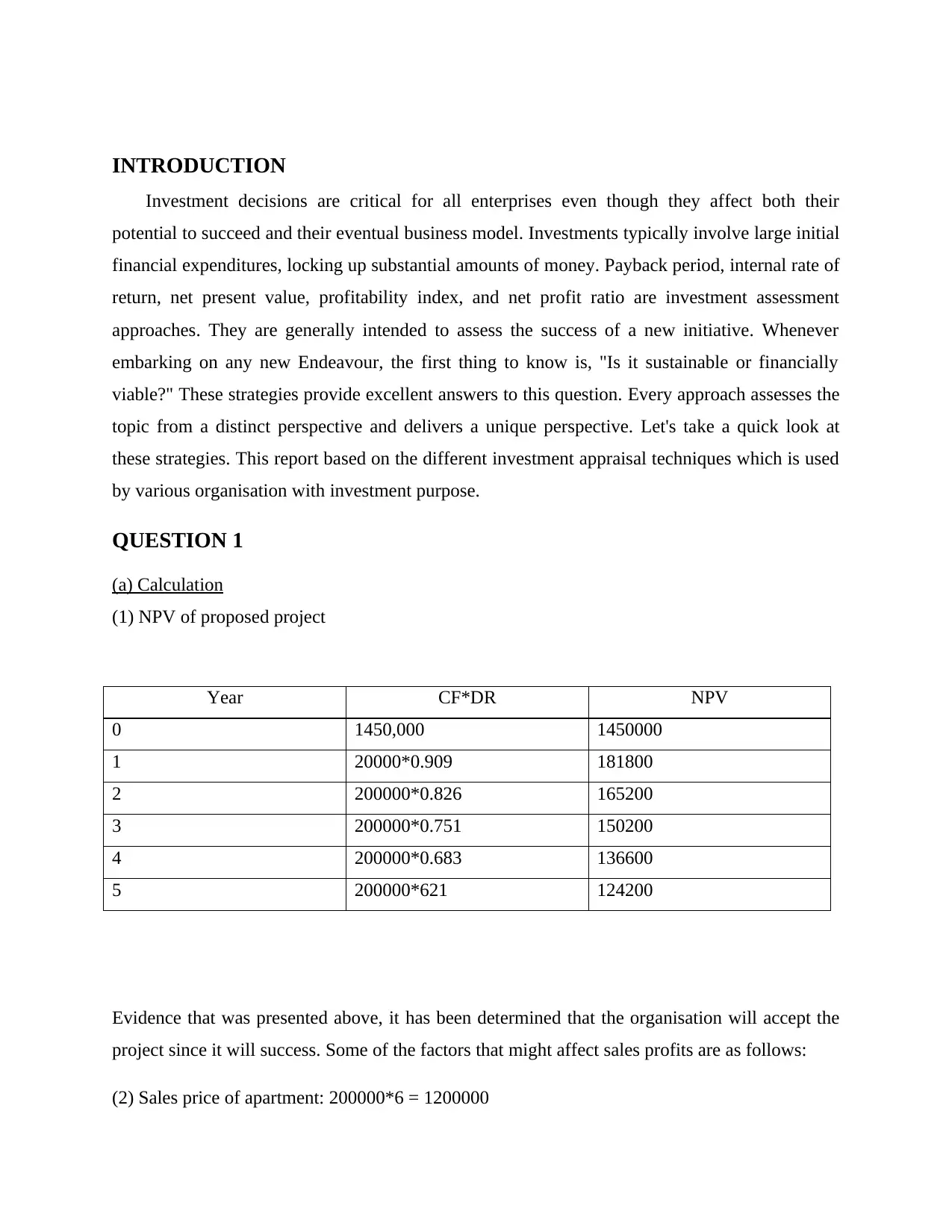

QUESTION 1

(a) Calculation

(1) NPV of proposed project

Year CF*DR NPV

0 1450,000 1450000

1 20000*0.909 181800

2 200000*0.826 165200

3 200000*0.751 150200

4 200000*0.683 136600

5 200000*621 124200

Evidence that was presented above, it has been determined that the organisation will accept the

project since it will success. Some of the factors that might affect sales profits are as follows:

(2) Sales price of apartment: 200000*6 = 1200000

Investment decisions are critical for all enterprises even though they affect both their

potential to succeed and their eventual business model. Investments typically involve large initial

financial expenditures, locking up substantial amounts of money. Payback period, internal rate of

return, net present value, profitability index, and net profit ratio are investment assessment

approaches. They are generally intended to assess the success of a new initiative. Whenever

embarking on any new Endeavour, the first thing to know is, "Is it sustainable or financially

viable?" These strategies provide excellent answers to this question. Every approach assesses the

topic from a distinct perspective and delivers a unique perspective. Let's take a quick look at

these strategies. This report based on the different investment appraisal techniques which is used

by various organisation with investment purpose.

QUESTION 1

(a) Calculation

(1) NPV of proposed project

Year CF*DR NPV

0 1450,000 1450000

1 20000*0.909 181800

2 200000*0.826 165200

3 200000*0.751 150200

4 200000*0.683 136600

5 200000*621 124200

Evidence that was presented above, it has been determined that the organisation will accept the

project since it will success. Some of the factors that might affect sales profits are as follows:

(2) Sales price of apartment: 200000*6 = 1200000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of financing: 1450000 *5% = 72500

(3) Explain results: All the calculation indicates cost that would be utilized to run and develop

the apartments. As a consequence, administration may assess how contemporary the current

obligations are for a specific period of time. If it costs considerably longer to recover trade

receivables than it does to collect accounts payable in a specific manner, the firm will be in

profitability. As a consequence, it is advised that company to keep concentrated on it at all

moments.

(b) Briefly discuss the merits and demerits of the internal rate of return rule

When implementing the internal rate of return to individual projects, it is essential to

comprehend its benefits and drawbacks. This very well approach of evaluating and selecting

capital projects necessitates a thorough examination and evaluation of the majority of initiatives.

This approach has several drawbacks for studying specific sorts of tasks, including such

conditionally incompatible developments, an unusual collection of cash flows, varied project

lifetimes, and so on.

Advantage:

Time value of money: The first and most crucial point is that while assessing a business, the

internal rate of return takes into consideration the time value of currency. This is a significant

decrease in the payback method, the indicator of profitability, and the Pay Back time. IRR may

be measured by determining the lending rate at which the PV of future revenues equals the

needed investment capital.

Simplicity: The most appealing aspect of this technique is that it is relatively straightforward to

comprehend once the IRR has been calculated. Accept the proposal whereas if IRR greater than

the cost of investment; alternatively, reject it. This is extremely difficult for individuals to

envision, which is why it is ideal until they run upon periodic exceptional issues, such as

different and incompatible initiatives, and so on.

Disadvantage:

The hurdle rate is a tough and subjective decision. There is no obligation in IRR to determine the

IRR hurdle rate or the necessary rate of return. It is not reliant on the hurdle rate, hence the

(3) Explain results: All the calculation indicates cost that would be utilized to run and develop

the apartments. As a consequence, administration may assess how contemporary the current

obligations are for a specific period of time. If it costs considerably longer to recover trade

receivables than it does to collect accounts payable in a specific manner, the firm will be in

profitability. As a consequence, it is advised that company to keep concentrated on it at all

moments.

(b) Briefly discuss the merits and demerits of the internal rate of return rule

When implementing the internal rate of return to individual projects, it is essential to

comprehend its benefits and drawbacks. This very well approach of evaluating and selecting

capital projects necessitates a thorough examination and evaluation of the majority of initiatives.

This approach has several drawbacks for studying specific sorts of tasks, including such

conditionally incompatible developments, an unusual collection of cash flows, varied project

lifetimes, and so on.

Advantage:

Time value of money: The first and most crucial point is that while assessing a business, the

internal rate of return takes into consideration the time value of currency. This is a significant

decrease in the payback method, the indicator of profitability, and the Pay Back time. IRR may

be measured by determining the lending rate at which the PV of future revenues equals the

needed investment capital.

Simplicity: The most appealing aspect of this technique is that it is relatively straightforward to

comprehend once the IRR has been calculated. Accept the proposal whereas if IRR greater than

the cost of investment; alternatively, reject it. This is extremely difficult for individuals to

envision, which is why it is ideal until they run upon periodic exceptional issues, such as

different and incompatible initiatives, and so on.

Disadvantage:

The hurdle rate is a tough and subjective decision. There is no obligation in IRR to determine the

IRR hurdle rate or the necessary rate of return. It is not reliant on the hurdle rate, hence the

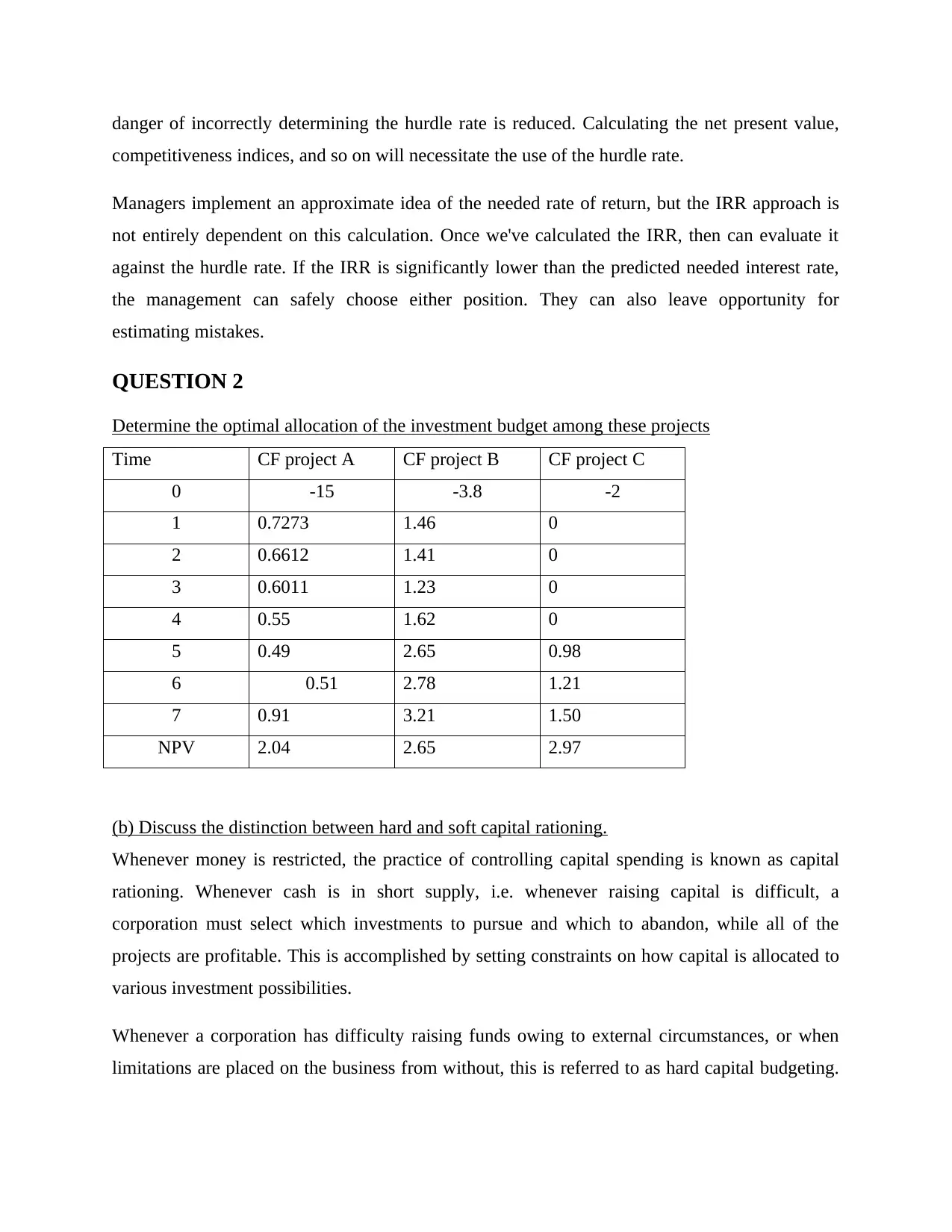

danger of incorrectly determining the hurdle rate is reduced. Calculating the net present value,

competitiveness indices, and so on will necessitate the use of the hurdle rate.

Managers implement an approximate idea of the needed rate of return, but the IRR approach is

not entirely dependent on this calculation. Once we've calculated the IRR, then can evaluate it

against the hurdle rate. If the IRR is significantly lower than the predicted needed interest rate,

the management can safely choose either position. They can also leave opportunity for

estimating mistakes.

QUESTION 2

Determine the optimal allocation of the investment budget among these projects

Time CF project A CF project B CF project C

0 -15 -3.8 -2

1 0.7273 1.46 0

2 0.6612 1.41 0

3 0.6011 1.23 0

4 0.55 1.62 0

5 0.49 2.65 0.98

6 0.51 2.78 1.21

7 0.91 3.21 1.50

NPV 2.04 2.65 2.97

(b) Discuss the distinction between hard and soft capital rationing.

Whenever money is restricted, the practice of controlling capital spending is known as capital

rationing. Whenever cash is in short supply, i.e. whenever raising capital is difficult, a

corporation must select which investments to pursue and which to abandon, while all of the

projects are profitable. This is accomplished by setting constraints on how capital is allocated to

various investment possibilities.

Whenever a corporation has difficulty raising funds owing to external circumstances, or when

limitations are placed on the business from without, this is referred to as hard capital budgeting.

competitiveness indices, and so on will necessitate the use of the hurdle rate.

Managers implement an approximate idea of the needed rate of return, but the IRR approach is

not entirely dependent on this calculation. Once we've calculated the IRR, then can evaluate it

against the hurdle rate. If the IRR is significantly lower than the predicted needed interest rate,

the management can safely choose either position. They can also leave opportunity for

estimating mistakes.

QUESTION 2

Determine the optimal allocation of the investment budget among these projects

Time CF project A CF project B CF project C

0 -15 -3.8 -2

1 0.7273 1.46 0

2 0.6612 1.41 0

3 0.6011 1.23 0

4 0.55 1.62 0

5 0.49 2.65 0.98

6 0.51 2.78 1.21

7 0.91 3.21 1.50

NPV 2.04 2.65 2.97

(b) Discuss the distinction between hard and soft capital rationing.

Whenever money is restricted, the practice of controlling capital spending is known as capital

rationing. Whenever cash is in short supply, i.e. whenever raising capital is difficult, a

corporation must select which investments to pursue and which to abandon, while all of the

projects are profitable. This is accomplished by setting constraints on how capital is allocated to

various investment possibilities.

Whenever a corporation has difficulty raising funds owing to external circumstances, or when

limitations are placed on the business from without, this is referred to as hard capital budgeting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

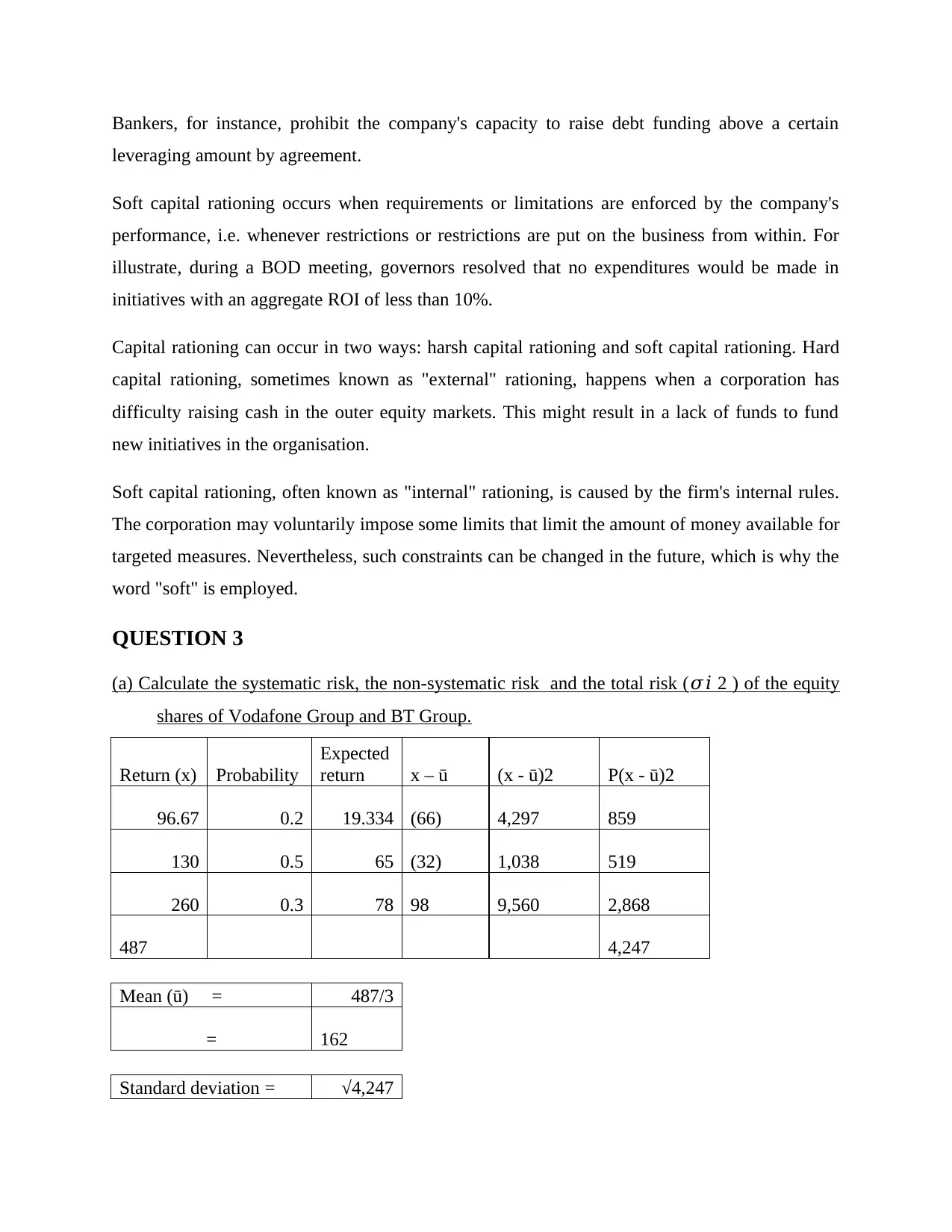

Bankers, for instance, prohibit the company's capacity to raise debt funding above a certain

leveraging amount by agreement.

Soft capital rationing occurs when requirements or limitations are enforced by the company's

performance, i.e. whenever restrictions or restrictions are put on the business from within. For

illustrate, during a BOD meeting, governors resolved that no expenditures would be made in

initiatives with an aggregate ROI of less than 10%.

Capital rationing can occur in two ways: harsh capital rationing and soft capital rationing. Hard

capital rationing, sometimes known as "external" rationing, happens when a corporation has

difficulty raising cash in the outer equity markets. This might result in a lack of funds to fund

new initiatives in the organisation.

Soft capital rationing, often known as "internal" rationing, is caused by the firm's internal rules.

The corporation may voluntarily impose some limits that limit the amount of money available for

targeted measures. Nevertheless, such constraints can be changed in the future, which is why the

word "soft" is employed.

QUESTION 3

(a) Calculate the systematic risk, the non-systematic risk and the total risk (𝜎𝑖 2 ) of the equity

shares of Vodafone Group and BT Group.

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

96.67 0.2 19.334 (66) 4,297 859

130 0.5 65 (32) 1,038 519

260 0.3 78 98 9,560 2,868

487 4,247

Mean (ū) = 487/3

= 162

Standard deviation = √4,247

leveraging amount by agreement.

Soft capital rationing occurs when requirements or limitations are enforced by the company's

performance, i.e. whenever restrictions or restrictions are put on the business from within. For

illustrate, during a BOD meeting, governors resolved that no expenditures would be made in

initiatives with an aggregate ROI of less than 10%.

Capital rationing can occur in two ways: harsh capital rationing and soft capital rationing. Hard

capital rationing, sometimes known as "external" rationing, happens when a corporation has

difficulty raising cash in the outer equity markets. This might result in a lack of funds to fund

new initiatives in the organisation.

Soft capital rationing, often known as "internal" rationing, is caused by the firm's internal rules.

The corporation may voluntarily impose some limits that limit the amount of money available for

targeted measures. Nevertheless, such constraints can be changed in the future, which is why the

word "soft" is employed.

QUESTION 3

(a) Calculate the systematic risk, the non-systematic risk and the total risk (𝜎𝑖 2 ) of the equity

shares of Vodafone Group and BT Group.

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

96.67 0.2 19.334 (66) 4,297 859

130 0.5 65 (32) 1,038 519

260 0.3 78 98 9,560 2,868

487 4,247

Mean (ū) = 487/3

= 162

Standard deviation = √4,247

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

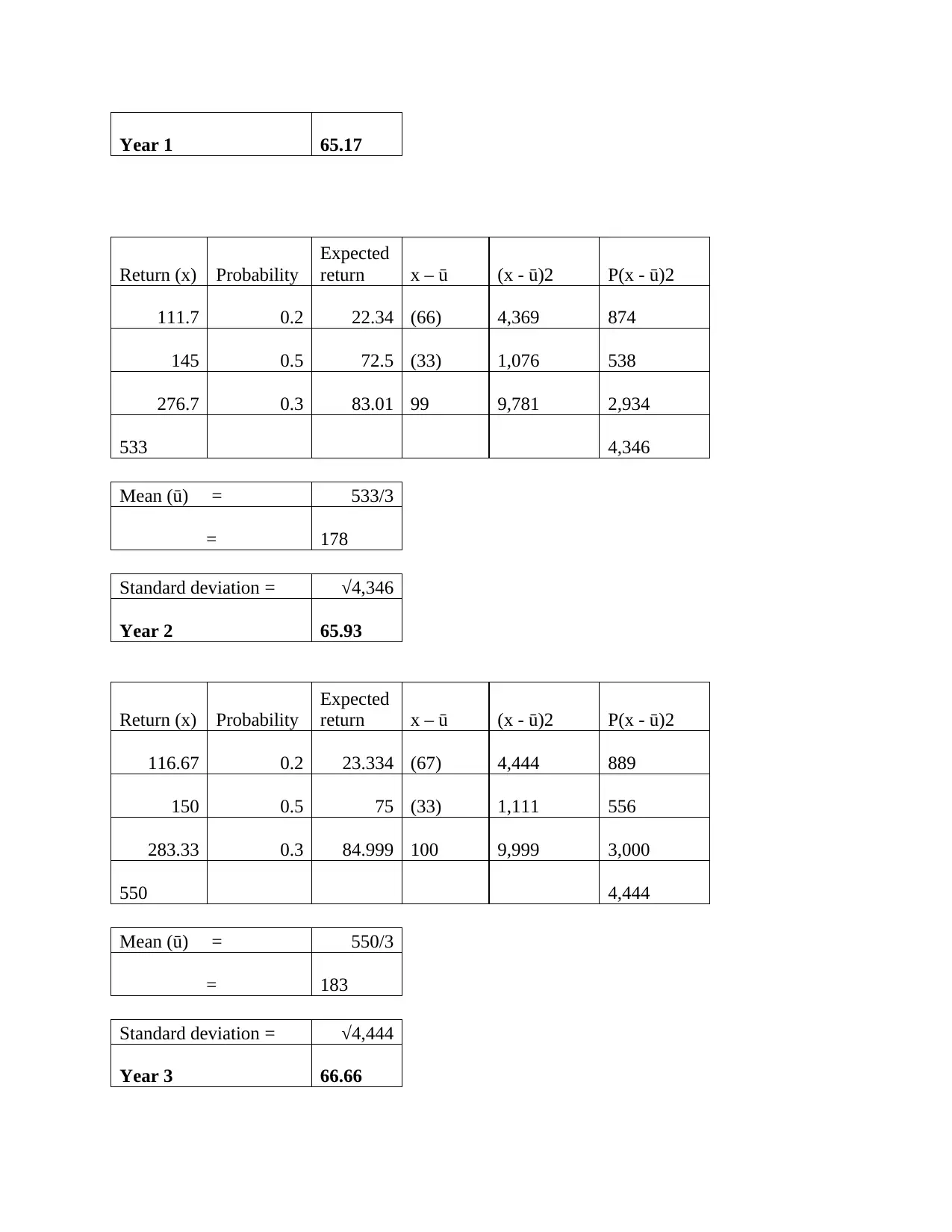

Year 1 65.17

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

111.7 0.2 22.34 (66) 4,369 874

145 0.5 72.5 (33) 1,076 538

276.7 0.3 83.01 99 9,781 2,934

533 4,346

Mean (ū) = 533/3

= 178

Standard deviation = √4,346

Year 2 65.93

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

116.67 0.2 23.334 (67) 4,444 889

150 0.5 75 (33) 1,111 556

283.33 0.3 84.999 100 9,999 3,000

550 4,444

Mean (ū) = 550/3

= 183

Standard deviation = √4,444

Year 3 66.66

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

111.7 0.2 22.34 (66) 4,369 874

145 0.5 72.5 (33) 1,076 538

276.7 0.3 83.01 99 9,781 2,934

533 4,346

Mean (ū) = 533/3

= 178

Standard deviation = √4,346

Year 2 65.93

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

116.67 0.2 23.334 (67) 4,444 889

150 0.5 75 (33) 1,111 556

283.33 0.3 84.999 100 9,999 3,000

550 4,444

Mean (ū) = 550/3

= 183

Standard deviation = √4,444

Year 3 66.66

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

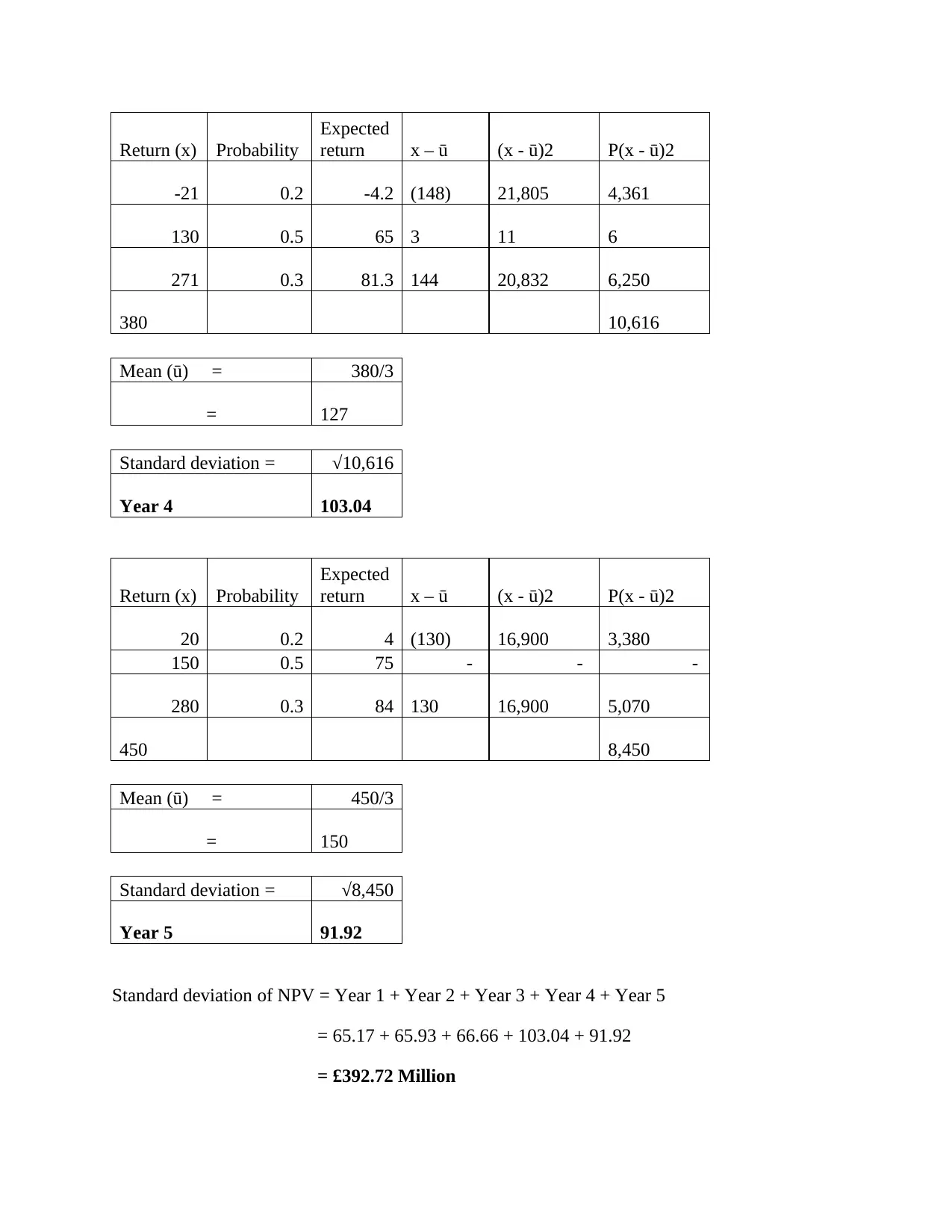

-21 0.2 -4.2 (148) 21,805 4,361

130 0.5 65 3 11 6

271 0.3 81.3 144 20,832 6,250

380 10,616

Mean (ū) = 380/3

= 127

Standard deviation = √10,616

Year 4 103.04

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

20 0.2 4 (130) 16,900 3,380

150 0.5 75 - - -

280 0.3 84 130 16,900 5,070

450 8,450

Mean (ū) = 450/3

= 150

Standard deviation = √8,450

Year 5 91.92

Standard deviation of NPV = Year 1 + Year 2 + Year 3 + Year 4 + Year 5

= 65.17 + 65.93 + 66.66 + 103.04 + 91.92

= £392.72 Million

Expected

return x – ū (x - ū)2 P(x - ū)2

-21 0.2 -4.2 (148) 21,805 4,361

130 0.5 65 3 11 6

271 0.3 81.3 144 20,832 6,250

380 10,616

Mean (ū) = 380/3

= 127

Standard deviation = √10,616

Year 4 103.04

Return (x) Probability

Expected

return x – ū (x - ū)2 P(x - ū)2

20 0.2 4 (130) 16,900 3,380

150 0.5 75 - - -

280 0.3 84 130 16,900 5,070

450 8,450

Mean (ū) = 450/3

= 150

Standard deviation = √8,450

Year 5 91.92

Standard deviation of NPV = Year 1 + Year 2 + Year 3 + Year 4 + Year 5

= 65.17 + 65.93 + 66.66 + 103.04 + 91.92

= £392.72 Million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) Which company’s returns are better explained by the market’s returns?

As per the analysis of both company shares it is saying that BT group plc has greater returns as

compare of Vodafone Plc. Company able to pay good dividend to their shareholders and take

advantage of competition in market.

(c) Calculate the expected equilibrium risk-premium for each of the two shares. Comment on the

results.

Mean of net present value = - £328m

Standard deviation = 392.72

Applying normal distribution:

Probability of avoiding liquidation that is (x > £100m):

P(x > £100m) = 1 - P(x < £100m)

= 1 – ( 100−(−328)

392.72 )

= 1 – 1.089

= - 0.09

Value of Z = 0.4641 or 46.41%

Hence, there is 46.41% chance that NPV will be higher than £100m.

CONCLUSION

As per the above report it has been calculated that these techniques are helping to take right

decision in regard investments.

As per the analysis of both company shares it is saying that BT group plc has greater returns as

compare of Vodafone Plc. Company able to pay good dividend to their shareholders and take

advantage of competition in market.

(c) Calculate the expected equilibrium risk-premium for each of the two shares. Comment on the

results.

Mean of net present value = - £328m

Standard deviation = 392.72

Applying normal distribution:

Probability of avoiding liquidation that is (x > £100m):

P(x > £100m) = 1 - P(x < £100m)

= 1 – ( 100−(−328)

392.72 )

= 1 – 1.089

= - 0.09

Value of Z = 0.4641 or 46.41%

Hence, there is 46.41% chance that NPV will be higher than £100m.

CONCLUSION

As per the above report it has been calculated that these techniques are helping to take right

decision in regard investments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Baker, C. R. and Persson, M. E., 2021. The Concept of Measurement in Financial Reporting.

In Historical Developments in the Accountancy Profession, Financial Reporting, and

Accounting Theory. Emerald Publishing Limited.

Mohamadi, M., 2020. Quality of Financial Reporting, Family Ownership, and Investment

Performance in Companies Listed in Tehran Stock Exchange. Journal of Accounting

Research. 10(3). pp.157-184.

Dameri, R. P., Garelli, R. and Resta, M., 2020. Neural networks in accounting: clustering firm

performance using financial reporting data. Journal of Information Systems. 34(2).

pp.149-166.

McVay, S. E. and Szerwo, B., 2021. Preparers and the Financial Reporting System. Accounting

and Business Research, forthcoming.

Yeboah, B. and Pais, C., 2021. International financial reporting standards adoption and

accounting quality: evidence from Ghanaian listed firms. Afro-Asian Journal of Finance

and Accounting. 11(4). pp.490-517.

Opare, S., Houqe, M. N. and Van Zijl, T., 2021. Meta‐analysis of the Impact of Adoption of

IFRS on Financial Reporting Comparability, Market Liquidity, and Cost of

Capital. Abacus. 57(3). pp.502-556.

Books and Journal

Baker, C. R. and Persson, M. E., 2021. The Concept of Measurement in Financial Reporting.

In Historical Developments in the Accountancy Profession, Financial Reporting, and

Accounting Theory. Emerald Publishing Limited.

Mohamadi, M., 2020. Quality of Financial Reporting, Family Ownership, and Investment

Performance in Companies Listed in Tehran Stock Exchange. Journal of Accounting

Research. 10(3). pp.157-184.

Dameri, R. P., Garelli, R. and Resta, M., 2020. Neural networks in accounting: clustering firm

performance using financial reporting data. Journal of Information Systems. 34(2).

pp.149-166.

McVay, S. E. and Szerwo, B., 2021. Preparers and the Financial Reporting System. Accounting

and Business Research, forthcoming.

Yeboah, B. and Pais, C., 2021. International financial reporting standards adoption and

accounting quality: evidence from Ghanaian listed firms. Afro-Asian Journal of Finance

and Accounting. 11(4). pp.490-517.

Opare, S., Houqe, M. N. and Van Zijl, T., 2021. Meta‐analysis of the Impact of Adoption of

IFRS on Financial Reporting Comparability, Market Liquidity, and Cost of

Capital. Abacus. 57(3). pp.502-556.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.