Comprehensive Report on Investment Appraisal and Valuation Methods

VerifiedAdded on 2023/06/11

|12

|3804

|272

Report

AI Summary

This report provides a detailed analysis of investment appraisal techniques, including payback period, average rate of return (ARR), net present value (NPV), and internal rate of return (IRR), along with their respective advantages and disadvantages. It assesses the economic feasibility of a project involving the purchase of new storage machinery, commenting on the directors' decisions regarding equity repurchase and dividend payouts. Furthermore, the report computes various valuation methods such as the price-earnings ratio, discusses the challenges associated with these techniques, and offers recommendations for Kings Plc's board members. The analysis aims to provide a comprehensive understanding of financial management principles and their practical application in investment decisions and business valuation, highlighting the importance of accurate financial planning and risk assessment in achieving optimal returns on investment. Desklib offers additional resources for students seeking support in their studies.

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK...............................................................................................................................................3

1. Investment Appraisal Technique ............................................................................................3

(a). Calculate Various methods of investment appraisal techniques. Also state the economic

feasibility of the project..............................................................................................................3

(b). Comment on the directors decision and evalute effects of proposal on the company..........6

(c). Explain the advantages and disadvantages of investment appraisal techniques- ................6

3. Takeovers and mergers ..........................................................................................................8

(a). Compute various valuation methods....................................................................................8

(b) Critically converse above the challenges that bare associated with the valuation techniques

used above. Also recommend that what are the techniques that could be recommended to the

board member of Kings Plc. .....................................................................................................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................3

TASK...............................................................................................................................................3

1. Investment Appraisal Technique ............................................................................................3

(a). Calculate Various methods of investment appraisal techniques. Also state the economic

feasibility of the project..............................................................................................................3

(b). Comment on the directors decision and evalute effects of proposal on the company..........6

(c). Explain the advantages and disadvantages of investment appraisal techniques- ................6

3. Takeovers and mergers ..........................................................................................................8

(a). Compute various valuation methods....................................................................................8

(b) Critically converse above the challenges that bare associated with the valuation techniques

used above. Also recommend that what are the techniques that could be recommended to the

board member of Kings Plc. .....................................................................................................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

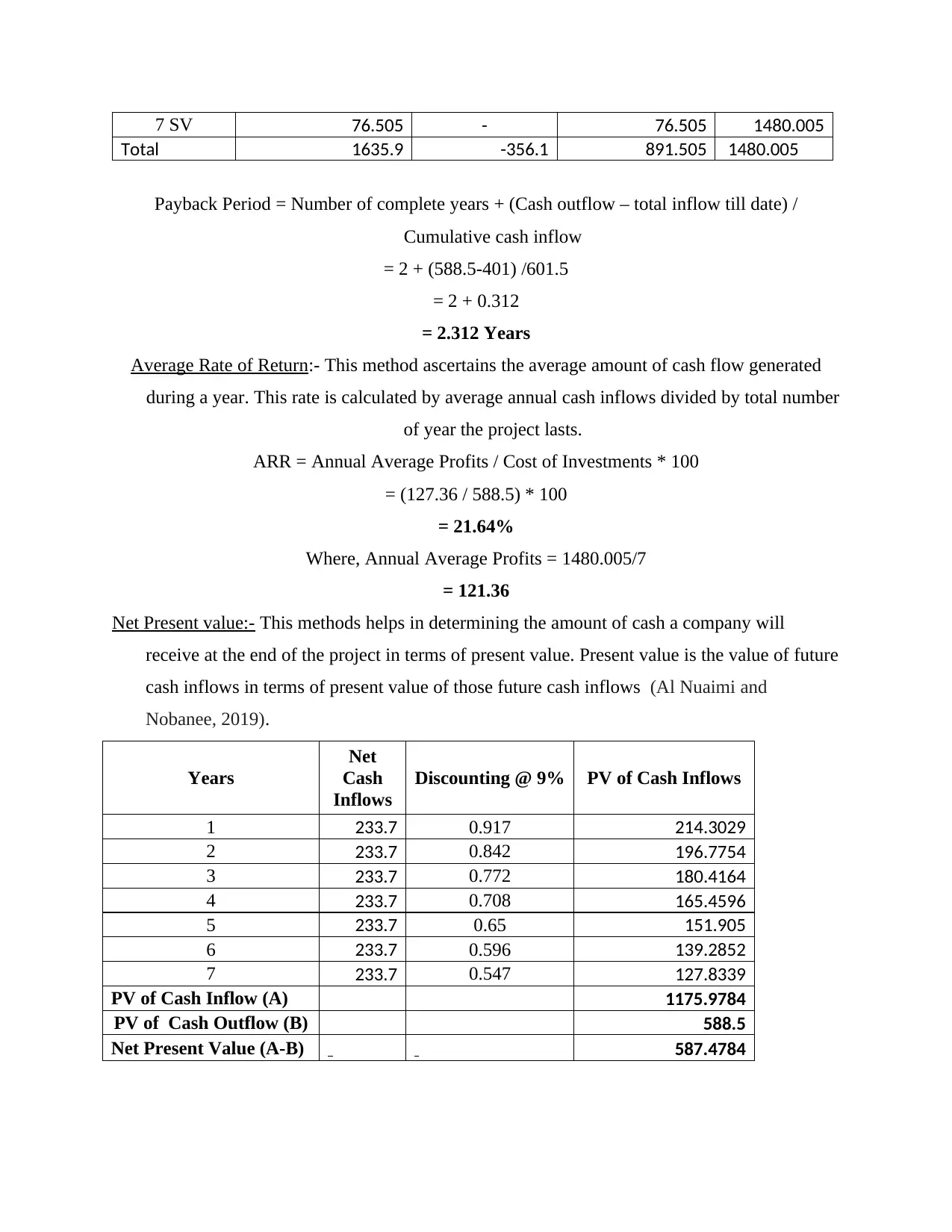

INTRODUCTION

Financial management is known for planning, controlling, organizing the financial

activities so that there is regular and adequate flow of funds to carry out smooth business

operations. Financial management is done by three segments, they are investment decisions,

financial decisions and dividend decisions (Yusoff, 2019). Capital Budgeting is the financial tool

to evaluate the investments and expenses so that the best returns on investment can be attained.

This technique is used by the business management in order to plan the investments on fixed

assets, with the help of this it can be determined whether the projects shall be accepted or not.

The following report consists of the techniques of capital budgeting and their calculations and

the impact of proposal on the business firm. With this, it also comprises the advantages and

disadvantages of investment appraisal techniques. Moreover, it also provides with the ratio

evaluation and the difficulties linked with the valuation methods.

TASK

1. Investment Appraisal Technique

(a). Calculate Various methods of investment appraisal techniques. Also state the economic

feasibility of the project.

Payback Period: This method ascertains time period in which an organisation recover its

initial outlay. It is the time taken to reach break even point. It does not lay any attention on the

overall inflows received during the life cycle of the project (Wicaksono, Laurens and Novianti,

2018).

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 -588.5 -588.5 0

1 233.7 33.2 200.5 200.5

2 233.7 33.2 200.5 401

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

Financial management is known for planning, controlling, organizing the financial

activities so that there is regular and adequate flow of funds to carry out smooth business

operations. Financial management is done by three segments, they are investment decisions,

financial decisions and dividend decisions (Yusoff, 2019). Capital Budgeting is the financial tool

to evaluate the investments and expenses so that the best returns on investment can be attained.

This technique is used by the business management in order to plan the investments on fixed

assets, with the help of this it can be determined whether the projects shall be accepted or not.

The following report consists of the techniques of capital budgeting and their calculations and

the impact of proposal on the business firm. With this, it also comprises the advantages and

disadvantages of investment appraisal techniques. Moreover, it also provides with the ratio

evaluation and the difficulties linked with the valuation methods.

TASK

1. Investment Appraisal Technique

(a). Calculate Various methods of investment appraisal techniques. Also state the economic

feasibility of the project.

Payback Period: This method ascertains time period in which an organisation recover its

initial outlay. It is the time taken to reach break even point. It does not lay any attention on the

overall inflows received during the life cycle of the project (Wicaksono, Laurens and Novianti,

2018).

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 -588.5 -588.5 0

1 233.7 33.2 200.5 200.5

2 233.7 33.2 200.5 401

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 SV 76.505 - 76.505 1480.005

Total 1635.9 -356.1 891.505 1480.005

Payback Period = Number of complete years + (Cash outflow – total inflow till date) /

Cumulative cash inflow

= 2 + (588.5-401) /601.5

= 2 + 0.312

= 2.312 Years

Average Rate of Return:- This method ascertains the average amount of cash flow generated

during a year. This rate is calculated by average annual cash inflows divided by total number

of year the project lasts.

ARR = Annual Average Profits / Cost of Investments * 100

= (127.36 / 588.5) * 100

= 21.64%

Where, Annual Average Profits = 1480.005/7

= 121.36

Net Present value:- This methods helps in determining the amount of cash a company will

receive at the end of the project in terms of present value. Present value is the value of future

cash inflows in terms of present value of those future cash inflows (Al Nuaimi and

Nobanee, 2019).

Years

Net

Cash

Inflows

Discounting @ 9% PV of Cash Inflows

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

PV of Cash Inflow (A) 1175.9784

PV of Cash Outflow (B) 588.5

Net Present Value (A-B) 587.4784

Total 1635.9 -356.1 891.505 1480.005

Payback Period = Number of complete years + (Cash outflow – total inflow till date) /

Cumulative cash inflow

= 2 + (588.5-401) /601.5

= 2 + 0.312

= 2.312 Years

Average Rate of Return:- This method ascertains the average amount of cash flow generated

during a year. This rate is calculated by average annual cash inflows divided by total number

of year the project lasts.

ARR = Annual Average Profits / Cost of Investments * 100

= (127.36 / 588.5) * 100

= 21.64%

Where, Annual Average Profits = 1480.005/7

= 121.36

Net Present value:- This methods helps in determining the amount of cash a company will

receive at the end of the project in terms of present value. Present value is the value of future

cash inflows in terms of present value of those future cash inflows (Al Nuaimi and

Nobanee, 2019).

Years

Net

Cash

Inflows

Discounting @ 9% PV of Cash Inflows

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

PV of Cash Inflow (A) 1175.9784

PV of Cash Outflow (B) 588.5

Net Present Value (A-B) 587.4784

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

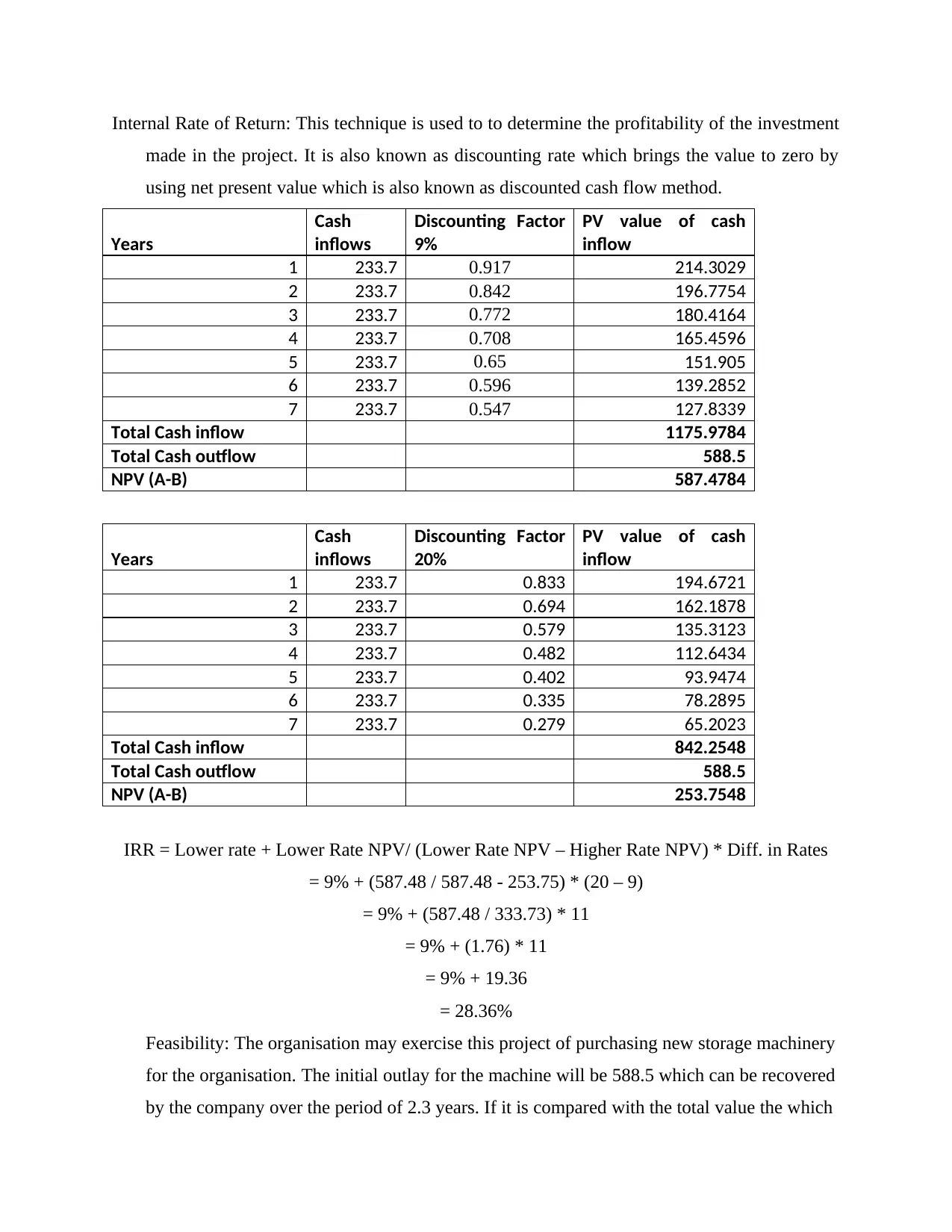

Internal Rate of Return: This technique is used to to determine the profitability of the investment

made in the project. It is also known as discounting rate which brings the value to zero by

using net present value which is also known as discounted cash flow method.

Years

Cash

inflows

Discounting Factor

9%

PV value of cash

inflow

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

Total Cash inflow 1175.9784

Total Cash outflow 588.5

NPV (A-B) 587.4784

Years

Cash

inflows

Discounting Factor

20%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

3 233.7 0.579 135.3123

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 9% + (587.48 / 587.48 - 253.75) * (20 – 9)

= 9% + (587.48 / 333.73) * 11

= 9% + (1.76) * 11

= 9% + 19.36

= 28.36%

Feasibility: The organisation may exercise this project of purchasing new storage machinery

for the organisation. The initial outlay for the machine will be 588.5 which can be recovered

by the company over the period of 2.3 years. If it is compared with the total value the which

made in the project. It is also known as discounting rate which brings the value to zero by

using net present value which is also known as discounted cash flow method.

Years

Cash

inflows

Discounting Factor

9%

PV value of cash

inflow

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

Total Cash inflow 1175.9784

Total Cash outflow 588.5

NPV (A-B) 587.4784

Years

Cash

inflows

Discounting Factor

20%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

3 233.7 0.579 135.3123

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 9% + (587.48 / 587.48 - 253.75) * (20 – 9)

= 9% + (587.48 / 333.73) * 11

= 9% + (1.76) * 11

= 9% + 19.36

= 28.36%

Feasibility: The organisation may exercise this project of purchasing new storage machinery

for the organisation. The initial outlay for the machine will be 588.5 which can be recovered

by the company over the period of 2.3 years. If it is compared with the total value the which

the organisation will be able to generate during the life cycle of the business will be 842.25.

The net amount in terms of today if the concern invest in the project then it will receive

253.75 at the end of the project. The NPV of the project is positive which states that the

business concern may buy this new machinery for the expanding their business operations.

This project shows a positive NPV which means that after the completion of the project the

firm will earn a fair amount of return from the project. The decision of making a new

purchase of machinery is relevant and company can proceed with this decision of making

purchase of new machinery (Yusufov and et.al., 2019).

(b). Comment on the directors decision and evalute effects of proposal on the company.

The decision of the finance director of choosing 50% of the inflow of the project is used in

repurchasing the equity capital and rest of the amount will be used to pay cash dividends to

the existing equity shareholders. The organisation realised by the organisation will be used

to increase promoters shareholding in the company which will help in reducing the existing

liabilities of the company. Buy back of equity shares is supported by some set of rules

prescribed in law.

Cash dividends are paid to the investors for the investment made by them in the organisation.

Investors do expect dividends in return of their investment made in the organisation.

Great ideas are supported by big business opportunities, it is the next new that the consumers can

get the new in the market that will solve their future problems of the business. The

business is evaluated by using the different methods of Investment appraisal techniques.

The organisation can opt for net present value which depicts the accurate value in terms of

today that the organisation will receive after specific period of time (Rodriguez, 2020) .

(c). Explain the advantages and disadvantages of investment appraisal techniques-

Payback period- It is the tool which is used to calculate the time taken to recover the cost of

investment. If the payback period is shorter then it means that the investments are attractive.

The advantages of payback period are as follows-

It is beneficial for those business enterprise which tend to make investments in small amount.

Payback period does not involve in the more tough evaluations i.e. they do not take other

complex factors into consideration. It is also simple in nature because it is very easy to

understand and calculate.

The net amount in terms of today if the concern invest in the project then it will receive

253.75 at the end of the project. The NPV of the project is positive which states that the

business concern may buy this new machinery for the expanding their business operations.

This project shows a positive NPV which means that after the completion of the project the

firm will earn a fair amount of return from the project. The decision of making a new

purchase of machinery is relevant and company can proceed with this decision of making

purchase of new machinery (Yusufov and et.al., 2019).

(b). Comment on the directors decision and evalute effects of proposal on the company.

The decision of the finance director of choosing 50% of the inflow of the project is used in

repurchasing the equity capital and rest of the amount will be used to pay cash dividends to

the existing equity shareholders. The organisation realised by the organisation will be used

to increase promoters shareholding in the company which will help in reducing the existing

liabilities of the company. Buy back of equity shares is supported by some set of rules

prescribed in law.

Cash dividends are paid to the investors for the investment made by them in the organisation.

Investors do expect dividends in return of their investment made in the organisation.

Great ideas are supported by big business opportunities, it is the next new that the consumers can

get the new in the market that will solve their future problems of the business. The

business is evaluated by using the different methods of Investment appraisal techniques.

The organisation can opt for net present value which depicts the accurate value in terms of

today that the organisation will receive after specific period of time (Rodriguez, 2020) .

(c). Explain the advantages and disadvantages of investment appraisal techniques-

Payback period- It is the tool which is used to calculate the time taken to recover the cost of

investment. If the payback period is shorter then it means that the investments are attractive.

The advantages of payback period are as follows-

It is beneficial for those business enterprise which tend to make investments in small amount.

Payback period does not involve in the more tough evaluations i.e. they do not take other

complex factors into consideration. It is also simple in nature because it is very easy to

understand and calculate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This method of investment appraisal technique focuses on how fast the money can be returned

from the investments that a company makes. This interpretation assists in calculating the

measure of the risk with respect to the project on which the company is going to make an

investment.

This metric favours the project that returns money to the firm in short time. Thus it can be said

that this technique of capital budgeting is focused on the liquidity (Chia-Cheng, Liu and

Hsu, 2019).

This method helps the company by protecting against the risk factors associated with long-term

investment.

Disadvantages of Payback Period-

The payback period is only concerned with that cash flow amount that is only covered with the

time till the initial investment is recouped. It does not consider the cash flows that occurs in

the upcoming years.

The firm cannot rely on this method as it does not cover the other scenarios like discount rates

and other factors.

It does not deliver guarantee that even if the payback period is short the business will earn profit.

Internal Rate of Return- This metric helps the company in assessing that which project is worth

for the investment purpose. This tool estimates the profitability associated with the particular

project. The IRR can be beneficial because-

As it is calculated by evaluating the interests rates at which the present value of future cash flows

equals the capital investment required. So, the subsequent cash flows are also considered.

It is simple means to assess the worthiness of various projects. It portrays that what investment

projects will give the highest capability cash flow.

The IRR technique does not require the hurdle rate which makes it easy for the company to

select the project that gives the return more than the cost of capital.

Drawbacks of IRR-

Another disadvantage of using this tool is that it does not report for the size of the project when

any investment is compared.

It ignores the the future cost that will be incurred during the life of the project. It also does not

account for the potential cost of the project. Various costs such as variable, fuel and

from the investments that a company makes. This interpretation assists in calculating the

measure of the risk with respect to the project on which the company is going to make an

investment.

This metric favours the project that returns money to the firm in short time. Thus it can be said

that this technique of capital budgeting is focused on the liquidity (Chia-Cheng, Liu and

Hsu, 2019).

This method helps the company by protecting against the risk factors associated with long-term

investment.

Disadvantages of Payback Period-

The payback period is only concerned with that cash flow amount that is only covered with the

time till the initial investment is recouped. It does not consider the cash flows that occurs in

the upcoming years.

The firm cannot rely on this method as it does not cover the other scenarios like discount rates

and other factors.

It does not deliver guarantee that even if the payback period is short the business will earn profit.

Internal Rate of Return- This metric helps the company in assessing that which project is worth

for the investment purpose. This tool estimates the profitability associated with the particular

project. The IRR can be beneficial because-

As it is calculated by evaluating the interests rates at which the present value of future cash flows

equals the capital investment required. So, the subsequent cash flows are also considered.

It is simple means to assess the worthiness of various projects. It portrays that what investment

projects will give the highest capability cash flow.

The IRR technique does not require the hurdle rate which makes it easy for the company to

select the project that gives the return more than the cost of capital.

Drawbacks of IRR-

Another disadvantage of using this tool is that it does not report for the size of the project when

any investment is compared.

It ignores the the future cost that will be incurred during the life of the project. It also does not

account for the potential cost of the project. Various costs such as variable, fuel and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maintenance cost incurred in the project. The opportunity cost of not reinvesting the amount

will shows a loss of income for the management (Gray, 2019).

Although it considers upcoming cash flows, but it makes an assumption that the future cash

flows can be invested again just as the equal rate as the IRR.

Net Present Value- It is an accounting measure which is the difference between the present value

of future cash inflows and present value of the future outflows over the period of time. The

benefits of the NPV can be as follows-

This helps the company by telling that the investment it is making would be beneficial for the

business or not.

It considers the cost of capital and the risk fundamentals in future projections.

Disadvantages Of net present value method are noted below-

It guesses the future cash flows which is the major problem as it can result in suboptimal

investments.

This method cannot be applied to those projects that have differentiated investment

amounts.

It is very difficult to apply this approach when the projects are compared and each of

them has variances in their life spans.

3. Takeovers and mergers

(a). Compute various valuation methods.

Price Earning Ratio- It is the measurement of the amount of money that an investor is

willing to pay for the each dollar of the firm's profit. It is also helpful in the determination of the

stock in terms of expensiveness and inexpensiveness. The price earning ratio can be determined

by dividing stock price with earnings per share. If this ratio is high then it signifies two things i.e.

either the price of stock is over valued or the company has rapid growth. But if the ratio is low

then it means the under valuation of stock price or the company is in the mature industry

(Ayodele, Oladokun and Kajimo-Shakantu, 2020). Investors make use of such ratio to make the

comparison between the value of stocks. This ratio has huge significance in the stock market and

also for the financial institutions like banking and insurance companies. It gives the accurate

information to evaluate the undervalued stocks on which the business enterprise can rely. In

other words it is the earning per share that the company net income would determine. It is the

income that will be earned by the organisation, it is the same as any investor will receive whom

will shows a loss of income for the management (Gray, 2019).

Although it considers upcoming cash flows, but it makes an assumption that the future cash

flows can be invested again just as the equal rate as the IRR.

Net Present Value- It is an accounting measure which is the difference between the present value

of future cash inflows and present value of the future outflows over the period of time. The

benefits of the NPV can be as follows-

This helps the company by telling that the investment it is making would be beneficial for the

business or not.

It considers the cost of capital and the risk fundamentals in future projections.

Disadvantages Of net present value method are noted below-

It guesses the future cash flows which is the major problem as it can result in suboptimal

investments.

This method cannot be applied to those projects that have differentiated investment

amounts.

It is very difficult to apply this approach when the projects are compared and each of

them has variances in their life spans.

3. Takeovers and mergers

(a). Compute various valuation methods.

Price Earning Ratio- It is the measurement of the amount of money that an investor is

willing to pay for the each dollar of the firm's profit. It is also helpful in the determination of the

stock in terms of expensiveness and inexpensiveness. The price earning ratio can be determined

by dividing stock price with earnings per share. If this ratio is high then it signifies two things i.e.

either the price of stock is over valued or the company has rapid growth. But if the ratio is low

then it means the under valuation of stock price or the company is in the mature industry

(Ayodele, Oladokun and Kajimo-Shakantu, 2020). Investors make use of such ratio to make the

comparison between the value of stocks. This ratio has huge significance in the stock market and

also for the financial institutions like banking and insurance companies. It gives the accurate

information to evaluate the undervalued stocks on which the business enterprise can rely. In

other words it is the earning per share that the company net income would determine. It is the

income that will be earned by the organisation, it is the same as any investor will receive whom

have purchased the share of the organisation. Increase in the price of stock increases the wealth

of the investors, which will also increase the wealth of the business concern.

Investors can use this ratio to ascertain the stock value in the market and it also helps in

determining the future value and growth of the stock in the recent time. The prices to be higher

of the stocks whose prices are regularly increased. The price of the stock is also determined in

the market by the demand and supply in the market. This ratio analysis tool aids in measuring the

future circumstances by comparing present performance with the past one. This does not cover

the debt structure while computing the financial reports (Sadly and et.al., 2018). Price earning

ratio is a great benchmarking tool for evaluation of stock as it helps in quick decision-making.

The formula for the above is = Market share price / Earnings per share

= 4.25 / 0.31

= 13.71

Value of the firm Dragon Plc which could be computed by using the P/E ratio of the Kings Plc is

below:

= Earnings per share of Dragon Plc * P/E of Kings plc

= (40.4 / 210) * 13.71

= 0.19 * 13.71

= 2.605

Discounted Cash flows- It is the valuation technique which is used to measure the value

of an investment on its expected future cash flows. It provides an assistance on valuing a

security, project, company, asset by using time value of money concept. It has its wide usage in

corporate financial management, patent valuation, investment finance and real state

development. This method can be applied by estimating all the future cash flows and discounted

rates using the cost of capital to get the present values. The positive discounted cash flow depicts

that the positive returns will be derived from the investment. Firms mainly use weighted average

method to value the stocks as it considers the values of past and previous values. It also considers

the rate of return earned by the shareholders (Dean and Hickman, 2018).

The cash flow is the addition of both the inflows and outflows is the NPV which is

covered as the value of cash flows. This tool uses particular figures that involves important

presupposition about the company, including cash flow projections, rate of growth, and other

factors that arrive at a value. It is more objective than the other measurement tools.

of the investors, which will also increase the wealth of the business concern.

Investors can use this ratio to ascertain the stock value in the market and it also helps in

determining the future value and growth of the stock in the recent time. The prices to be higher

of the stocks whose prices are regularly increased. The price of the stock is also determined in

the market by the demand and supply in the market. This ratio analysis tool aids in measuring the

future circumstances by comparing present performance with the past one. This does not cover

the debt structure while computing the financial reports (Sadly and et.al., 2018). Price earning

ratio is a great benchmarking tool for evaluation of stock as it helps in quick decision-making.

The formula for the above is = Market share price / Earnings per share

= 4.25 / 0.31

= 13.71

Value of the firm Dragon Plc which could be computed by using the P/E ratio of the Kings Plc is

below:

= Earnings per share of Dragon Plc * P/E of Kings plc

= (40.4 / 210) * 13.71

= 0.19 * 13.71

= 2.605

Discounted Cash flows- It is the valuation technique which is used to measure the value

of an investment on its expected future cash flows. It provides an assistance on valuing a

security, project, company, asset by using time value of money concept. It has its wide usage in

corporate financial management, patent valuation, investment finance and real state

development. This method can be applied by estimating all the future cash flows and discounted

rates using the cost of capital to get the present values. The positive discounted cash flow depicts

that the positive returns will be derived from the investment. Firms mainly use weighted average

method to value the stocks as it considers the values of past and previous values. It also considers

the rate of return earned by the shareholders (Dean and Hickman, 2018).

The cash flow is the addition of both the inflows and outflows is the NPV which is

covered as the value of cash flows. This tool uses particular figures that involves important

presupposition about the company, including cash flow projections, rate of growth, and other

factors that arrive at a value. It is more objective than the other measurement tools.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Annual After tax synergy / Cost of Capital

= 5.36 / 11% = 48.73

Dividend Valuation method- This method is used according to the size and type of the

organisation. It is one the method which is used to measure the value of the stock. This method

uses share growth and dividend received at the end of the year. It is basically used for the

valuation of blue chipped companies. It can be valued by using 2 methods which are mentioned

below,

1. Stock value = Dividend value per share / (Required rate of return – Dividend growth rate)

2. Rate of return = (Dividend payment / stock price) + Dividend growth rate

Po = D1 / (Ke – G)

= 12p / (6.13% - 2.5%)

= 12p / 3.6%

= 333.33 p or £ 3.33

Valuation of Dragon Plc

= Number of Equity Shares * the current market price per share

= 210 * 3.33

= £ 699.33.

Here,

Po - Current Market Price per share

Ke - Cost of Equity

D1 - Expected dividend per share

G - Growth rate

Working Notes:

Cost of Equity:

CAPM = Rf + B (Rm – Rf)

= 5.5 + 1.05 * (11% - 5.5%)

= 5.5 % = 1.05 * (5.5%)

= 5.55 + 0.58

= 6.13 %

= 5.36 / 11% = 48.73

Dividend Valuation method- This method is used according to the size and type of the

organisation. It is one the method which is used to measure the value of the stock. This method

uses share growth and dividend received at the end of the year. It is basically used for the

valuation of blue chipped companies. It can be valued by using 2 methods which are mentioned

below,

1. Stock value = Dividend value per share / (Required rate of return – Dividend growth rate)

2. Rate of return = (Dividend payment / stock price) + Dividend growth rate

Po = D1 / (Ke – G)

= 12p / (6.13% - 2.5%)

= 12p / 3.6%

= 333.33 p or £ 3.33

Valuation of Dragon Plc

= Number of Equity Shares * the current market price per share

= 210 * 3.33

= £ 699.33.

Here,

Po - Current Market Price per share

Ke - Cost of Equity

D1 - Expected dividend per share

G - Growth rate

Working Notes:

Cost of Equity:

CAPM = Rf + B (Rm – Rf)

= 5.5 + 1.05 * (11% - 5.5%)

= 5.5 % = 1.05 * (5.5%)

= 5.55 + 0.58

= 6.13 %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Calculation of Expected Dividend per share:

D1 = Dividend Paid (Do) + Growth Rate (G)

= 12p + 2.5

= 12.3 p

(b) Critically converse above the challenges that bare associated with the valuation techniques

used above. Also recommend that what are the techniques that could be recommended to

the board member of Kings Plc.

In the following case the organisation can opt for Discounted cash flow method. This method

present the fair value of the firm because it considers the time value of money. The assumption

in this method are more accurate as it considers discounted cash flow technique. The results

shown in this type of cash flow resembles the value which are more associated the actual values

of the organisation and is not based on the assumptions just like the other models (Oyewo, Vo

and Akinsanmi, 2021).

CONCLUSION

From the above report it can be concluded that organisation is working towards the

organisational goals which will improve the organisation's earnings and profitability. There are

various tools which can be used by the organisation to evaluate different proposal available to

the company. Some of the methods considers time value of money and other does not consider

time value of money. The project which provides highest return should be selected according to

the value derived by using the methods. Investment appraisal is an effective tool that the

organisation can access in checking the viability of the project. Value of share can be determined

by using different methods such as discounted cash flow, dividend valuation method and price

earning model. When any organisation wants to sell its share in the open market then it can use

different valuation methods that can ascertain the value of share.

REFERENCES

Books and Journals

Al Nuaimi, A. and Nobanee, H., 2019. Corporate sustainability reporting and corporate financial

growth. Available at SSRN 3472418.

D1 = Dividend Paid (Do) + Growth Rate (G)

= 12p + 2.5

= 12.3 p

(b) Critically converse above the challenges that bare associated with the valuation techniques

used above. Also recommend that what are the techniques that could be recommended to

the board member of Kings Plc.

In the following case the organisation can opt for Discounted cash flow method. This method

present the fair value of the firm because it considers the time value of money. The assumption

in this method are more accurate as it considers discounted cash flow technique. The results

shown in this type of cash flow resembles the value which are more associated the actual values

of the organisation and is not based on the assumptions just like the other models (Oyewo, Vo

and Akinsanmi, 2021).

CONCLUSION

From the above report it can be concluded that organisation is working towards the

organisational goals which will improve the organisation's earnings and profitability. There are

various tools which can be used by the organisation to evaluate different proposal available to

the company. Some of the methods considers time value of money and other does not consider

time value of money. The project which provides highest return should be selected according to

the value derived by using the methods. Investment appraisal is an effective tool that the

organisation can access in checking the viability of the project. Value of share can be determined

by using different methods such as discounted cash flow, dividend valuation method and price

earning model. When any organisation wants to sell its share in the open market then it can use

different valuation methods that can ascertain the value of share.

REFERENCES

Books and Journals

Al Nuaimi, A. and Nobanee, H., 2019. Corporate sustainability reporting and corporate financial

growth. Available at SSRN 3472418.

Ayodele, T.O., Oladokun, T.T. and Kajimo-Shakantu, K., 2020. Employability skills of real

estate graduates in Nigeria: a skill gap analysis. Journal of Facilities Management.

Baker, A.J., 2018. Business decision making. Routledge.

Chia-Cheng, C., Liu, Y. and Hsu, T.H., 2019. An analysis on investment performance of

machine learning: an empirical examination on Taiwan stock market. International

Journal of Economics and Financial Issues, 9(4), p.1.

Dean, M. and Hickman, R., 2018. Comparing cost-benefit analysis and multi actor multi criteria

analysis: The case of Blackpool and the South Fylde Line. In Decision-making for

sustainable transport and mobility. Edward Elgar Publishing.

Gray, R., 2019. Sustainability accounting and education: conflicts and possibilities.

In Incorporating sustainability in Management education (pp. 33-54). Palgrave

Macmillan, Cham.

Gunarathne, A.N. and Lee, K.H., 2019. Environmental and managerial information for cleaner

production strategies: An environmental management development perspective. Journal

of Cleaner Production, 237, p.117849.

Kyriacou, A.P., Muinelo-Gallo, L. and Roca-Sagalés, O., 2019. The efficiency of transport

infrastructure investment and the role of government quality: An empirical

analysis. Transport Policy, 74, pp.93-102.

Oyewo, B., Vo, X.V. and Akinsanmi, T., 2021. Strategy-related factors moderating the fit

between management accounting practice sophistication and organisational

effectiveness: the Global Management Accounting Principles (GMAP)

perspective. Spanish Journal of Finance and Accounting/Revista Española de

Financiación y Contabilidad, 50(2), pp.187-223.

Panova, Y. and Hilletofth, P., 2018. Managing supply chain risks and delays in construction

project. Industrial Management & Data Systems.

Rodriguez M, F., 2020, August. EOR Techniques Tailored to Venezuelan Conventional and

Unconventional Oils: Critical Review. In International Conference on Offshore

Mechanics and Arctic Engineering (Vol. 84430, p. V011T11A011). American Society

of Mechanical Engineers.

Sadly, M. and et.al., 2018, September. An Application of SMART Method in vendor selection of

Satellite Systems Case study of Indonesia Remote Sensing Satellite Systems

(InaRSSat). In 2018 IEEE International Conference on Aerospace Electronics and

Remote Sensing Technology (ICARES) (pp. 1-6). IEEE.

Wicaksono, A., Laurens, S. and Novianti, E., 2018, September. Impact analysis of computer

assisted audit techniques utilization on internal auditor performance. In 2018

International Conference on Information Management and Technology (ICIMTech) (pp.

267-271). IEEE.

Yusoff, Y., 2019. Linking green human resource management bundle to environmental

performance in malaysia’s hotel industry: The mediating role of organizational

citizenship behaviour towards environment. International Journal of Innovative

Technology and Exploring Engineering, 8(9), pp.1625-1630.

Yusufov, M. and et.al., 2019. Meta-analytic evaluation of stress reduction interventions for

undergraduate and graduate students. International Journal of Stress

Management, 26(2), p.132.

estate graduates in Nigeria: a skill gap analysis. Journal of Facilities Management.

Baker, A.J., 2018. Business decision making. Routledge.

Chia-Cheng, C., Liu, Y. and Hsu, T.H., 2019. An analysis on investment performance of

machine learning: an empirical examination on Taiwan stock market. International

Journal of Economics and Financial Issues, 9(4), p.1.

Dean, M. and Hickman, R., 2018. Comparing cost-benefit analysis and multi actor multi criteria

analysis: The case of Blackpool and the South Fylde Line. In Decision-making for

sustainable transport and mobility. Edward Elgar Publishing.

Gray, R., 2019. Sustainability accounting and education: conflicts and possibilities.

In Incorporating sustainability in Management education (pp. 33-54). Palgrave

Macmillan, Cham.

Gunarathne, A.N. and Lee, K.H., 2019. Environmental and managerial information for cleaner

production strategies: An environmental management development perspective. Journal

of Cleaner Production, 237, p.117849.

Kyriacou, A.P., Muinelo-Gallo, L. and Roca-Sagalés, O., 2019. The efficiency of transport

infrastructure investment and the role of government quality: An empirical

analysis. Transport Policy, 74, pp.93-102.

Oyewo, B., Vo, X.V. and Akinsanmi, T., 2021. Strategy-related factors moderating the fit

between management accounting practice sophistication and organisational

effectiveness: the Global Management Accounting Principles (GMAP)

perspective. Spanish Journal of Finance and Accounting/Revista Española de

Financiación y Contabilidad, 50(2), pp.187-223.

Panova, Y. and Hilletofth, P., 2018. Managing supply chain risks and delays in construction

project. Industrial Management & Data Systems.

Rodriguez M, F., 2020, August. EOR Techniques Tailored to Venezuelan Conventional and

Unconventional Oils: Critical Review. In International Conference on Offshore

Mechanics and Arctic Engineering (Vol. 84430, p. V011T11A011). American Society

of Mechanical Engineers.

Sadly, M. and et.al., 2018, September. An Application of SMART Method in vendor selection of

Satellite Systems Case study of Indonesia Remote Sensing Satellite Systems

(InaRSSat). In 2018 IEEE International Conference on Aerospace Electronics and

Remote Sensing Technology (ICARES) (pp. 1-6). IEEE.

Wicaksono, A., Laurens, S. and Novianti, E., 2018, September. Impact analysis of computer

assisted audit techniques utilization on internal auditor performance. In 2018

International Conference on Information Management and Technology (ICIMTech) (pp.

267-271). IEEE.

Yusoff, Y., 2019. Linking green human resource management bundle to environmental

performance in malaysia’s hotel industry: The mediating role of organizational

citizenship behaviour towards environment. International Journal of Innovative

Technology and Exploring Engineering, 8(9), pp.1625-1630.

Yusufov, M. and et.al., 2019. Meta-analytic evaluation of stress reduction interventions for

undergraduate and graduate students. International Journal of Stress

Management, 26(2), p.132.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.