Investment Appraisal and IRR Analysis for Machine Selection

VerifiedAdded on 2023/06/13

|8

|1657

|300

Report

AI Summary

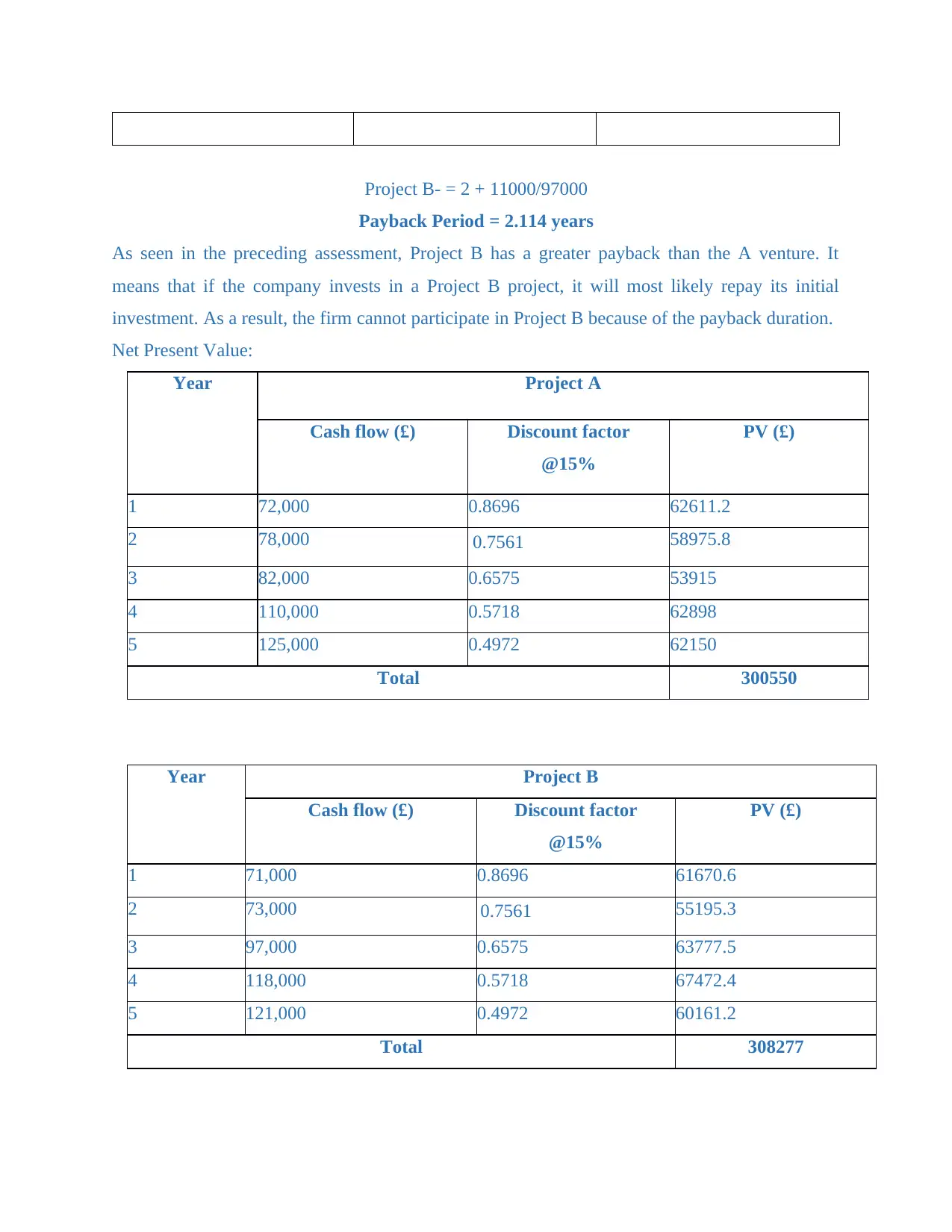

This report provides a detailed examination of investment appraisal metrics, including Net Present Value (NPV), Internal Rate of Return (IRR), Accounting Rate of Return (ARR), and payback period, to evaluate and recommend the optimal machine selection between options A20 and B25. The analysis considers the Director of Finance's claim regarding the IRR and offers explanations based on NPV and shareholder perspectives. Calculations for NPV and payback period are presented, demonstrating that while Project A has a shorter payback period, Project B exhibits a higher NPV, making it the more advantageous investment. The report concludes that investment appraisal methodologies are crucial for assessing project efficacy and guiding investment decisions, ultimately recommending option B25 based on its superior NPV and ARR.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.