Report on Investment Appraisal Techniques & Capital Structure

VerifiedAdded on 2023/06/11

|20

|3671

|158

Report

AI Summary

This report provides a detailed analysis of Faith Plc's capital structure and investment appraisal techniques. It covers the cost of equity, WACC calculation using both book and market values, and interprets the results. The report also examines the relationship between IRR and WACC. Furthermore, it evaluates investment appraisal techniques such as payback period, accounting rate of return (ARR), and net present value (NPV) for Pizza Mat (PM) Limited, including organizational effects and benefits/disadvantages in the sector. The analysis includes calculations and interpretations of financial data to assess the investment efficiency and financial significance of the companies.

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1- Cost of Capital and Capital Structure......................................................................1

a. Cost of equity...........................................................................................................................1

WACC with Book value and Market Value................................................................................3

b. Assessment of Overall WACC Cost of Capital.......................................................................4

c. Interpretations..........................................................................................................................7

d. There is a link between the company's IRR and WACC classification...................................8

Question 2- Investment Appraisal Techniques............................................................................8

Accounting Rate of Return..........................................................................................................9

b. Organizational Effects of Investment Appraisal Techniques................................................11

c. Benefits and Disadvantages of Capital Assessment Technique in the Sector.......................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1- Cost of Capital and Capital Structure......................................................................1

a. Cost of equity...........................................................................................................................1

WACC with Book value and Market Value................................................................................3

b. Assessment of Overall WACC Cost of Capital.......................................................................4

c. Interpretations..........................................................................................................................7

d. There is a link between the company's IRR and WACC classification...................................8

Question 2- Investment Appraisal Techniques............................................................................8

Accounting Rate of Return..........................................................................................................9

b. Organizational Effects of Investment Appraisal Techniques................................................11

c. Benefits and Disadvantages of Capital Assessment Technique in the Sector.......................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management is the branch of business that focuses on costs, earnings, funds, and

debts (Alawattage and Wickramasinghe, 2018). Financial management is a management function

wherein the director is in charge of conceptualization, implementation, coordination, regulation,

and evaluation. In ability to execute a business company efficiently, the management must have

a thorough knowledge of fiscal management. Financial authorities have involved incorporating

management strategies into the company's investment tools as well as playing a key role in

budgeting control.

MAIN BODY

Question 1- Cost of Capital and Capital Structure

a. Cost of equity

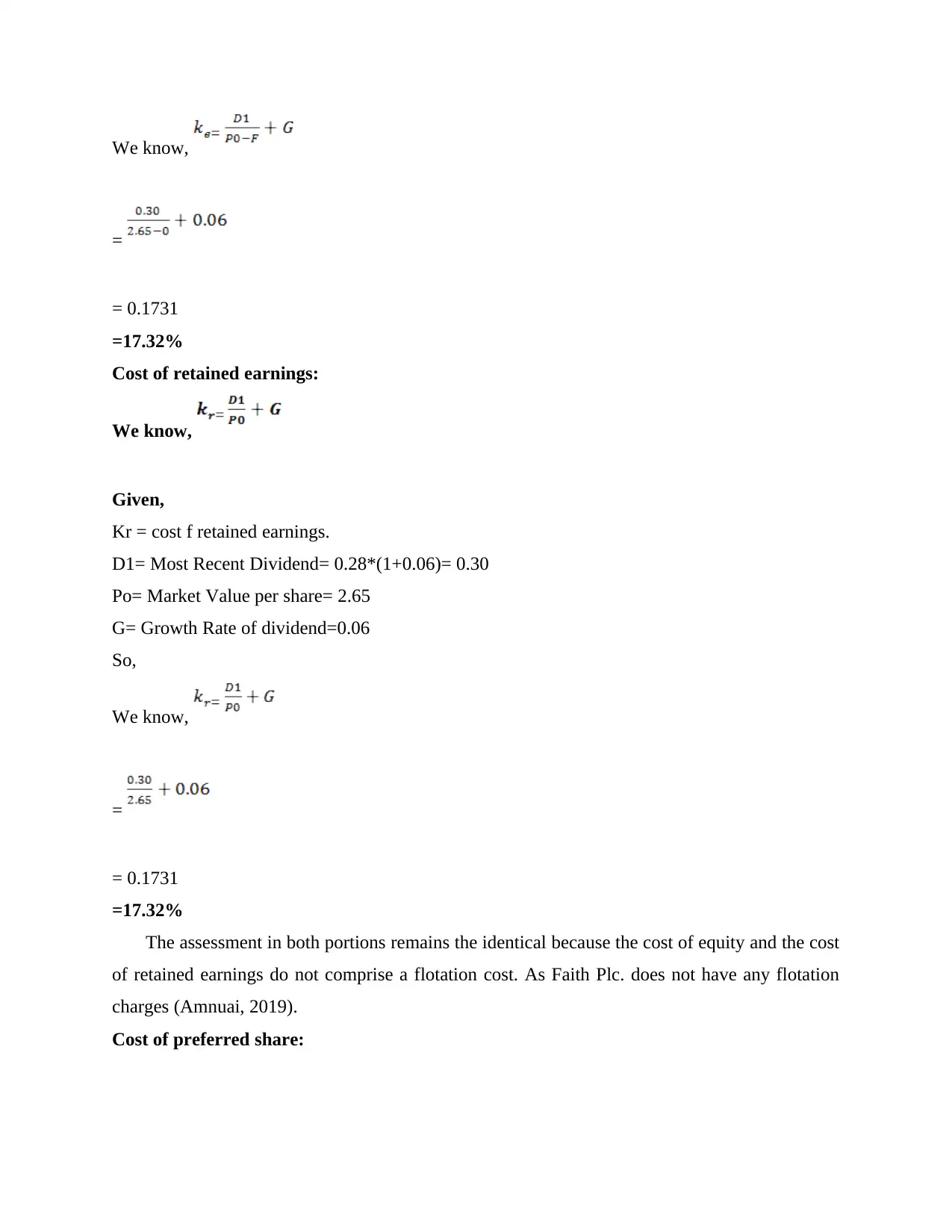

Cost of equity:

We know,

Given, = Cost of Equity

D1= Most Recent Dividend= 0.28*(1+0.06)= 0.30

Po= Market Value per share= 2.65

F= flotation cost = 0

G= Growth Rate of dividend

0.21 =0.28

0r,

Or, g= 0.0587 or 6%

So,

Financial management is the branch of business that focuses on costs, earnings, funds, and

debts (Alawattage and Wickramasinghe, 2018). Financial management is a management function

wherein the director is in charge of conceptualization, implementation, coordination, regulation,

and evaluation. In ability to execute a business company efficiently, the management must have

a thorough knowledge of fiscal management. Financial authorities have involved incorporating

management strategies into the company's investment tools as well as playing a key role in

budgeting control.

MAIN BODY

Question 1- Cost of Capital and Capital Structure

a. Cost of equity

Cost of equity:

We know,

Given, = Cost of Equity

D1= Most Recent Dividend= 0.28*(1+0.06)= 0.30

Po= Market Value per share= 2.65

F= flotation cost = 0

G= Growth Rate of dividend

0.21 =0.28

0r,

Or, g= 0.0587 or 6%

So,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

We know,

=

= 0.1731

=17.32%

Cost of retained earnings:

We know,

Given,

Kr = cost f retained earnings.

D1= Most Recent Dividend= 0.28*(1+0.06)= 0.30

Po= Market Value per share= 2.65

G= Growth Rate of dividend=0.06

So,

We know,

=

= 0.1731

=17.32%

The assessment in both portions remains the identical because the cost of equity and the cost

of retained earnings do not comprise a flotation cost. As Faith Plc. does not have any flotation

charges (Amnuai, 2019).

Cost of preferred share:

=

= 0.1731

=17.32%

Cost of retained earnings:

We know,

Given,

Kr = cost f retained earnings.

D1= Most Recent Dividend= 0.28*(1+0.06)= 0.30

Po= Market Value per share= 2.65

G= Growth Rate of dividend=0.06

So,

We know,

=

= 0.1731

=17.32%

The assessment in both portions remains the identical because the cost of equity and the cost

of retained earnings do not comprise a flotation cost. As Faith Plc. does not have any flotation

charges (Amnuai, 2019).

Cost of preferred share:

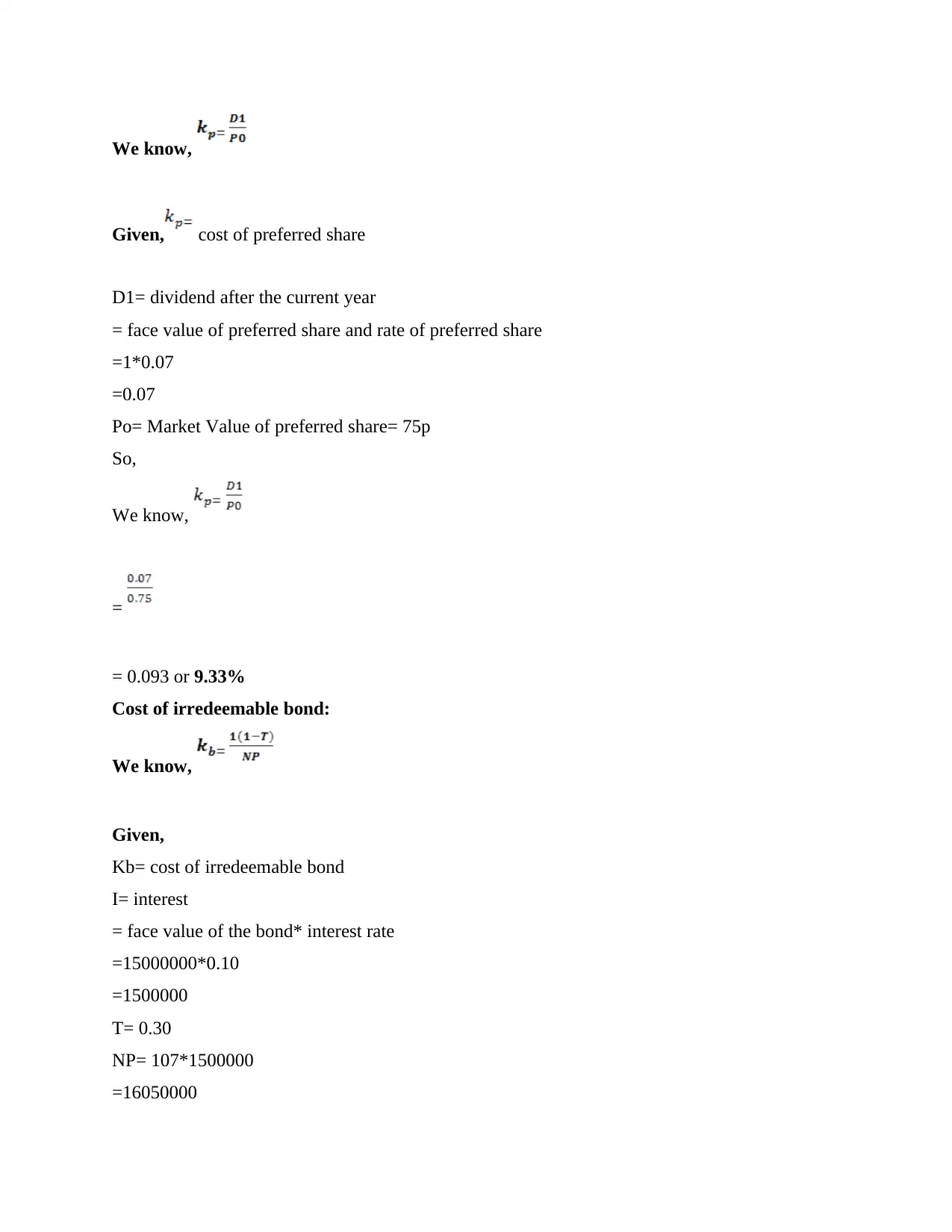

We know,

Given, cost of preferred share

D1= dividend after the current year

= face value of preferred share and rate of preferred share

=1*0.07

=0.07

Po= Market Value of preferred share= 75p

So,

We know,

=

= 0.093 or 9.33%

Cost of irredeemable bond:

We know,

Given,

Kb= cost of irredeemable bond

I= interest

= face value of the bond* interest rate

=15000000*0.10

=1500000

T= 0.30

NP= 107*1500000

=16050000

Given, cost of preferred share

D1= dividend after the current year

= face value of preferred share and rate of preferred share

=1*0.07

=0.07

Po= Market Value of preferred share= 75p

So,

We know,

=

= 0.093 or 9.33%

Cost of irredeemable bond:

We know,

Given,

Kb= cost of irredeemable bond

I= interest

= face value of the bond* interest rate

=15000000*0.10

=1500000

T= 0.30

NP= 107*1500000

=16050000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

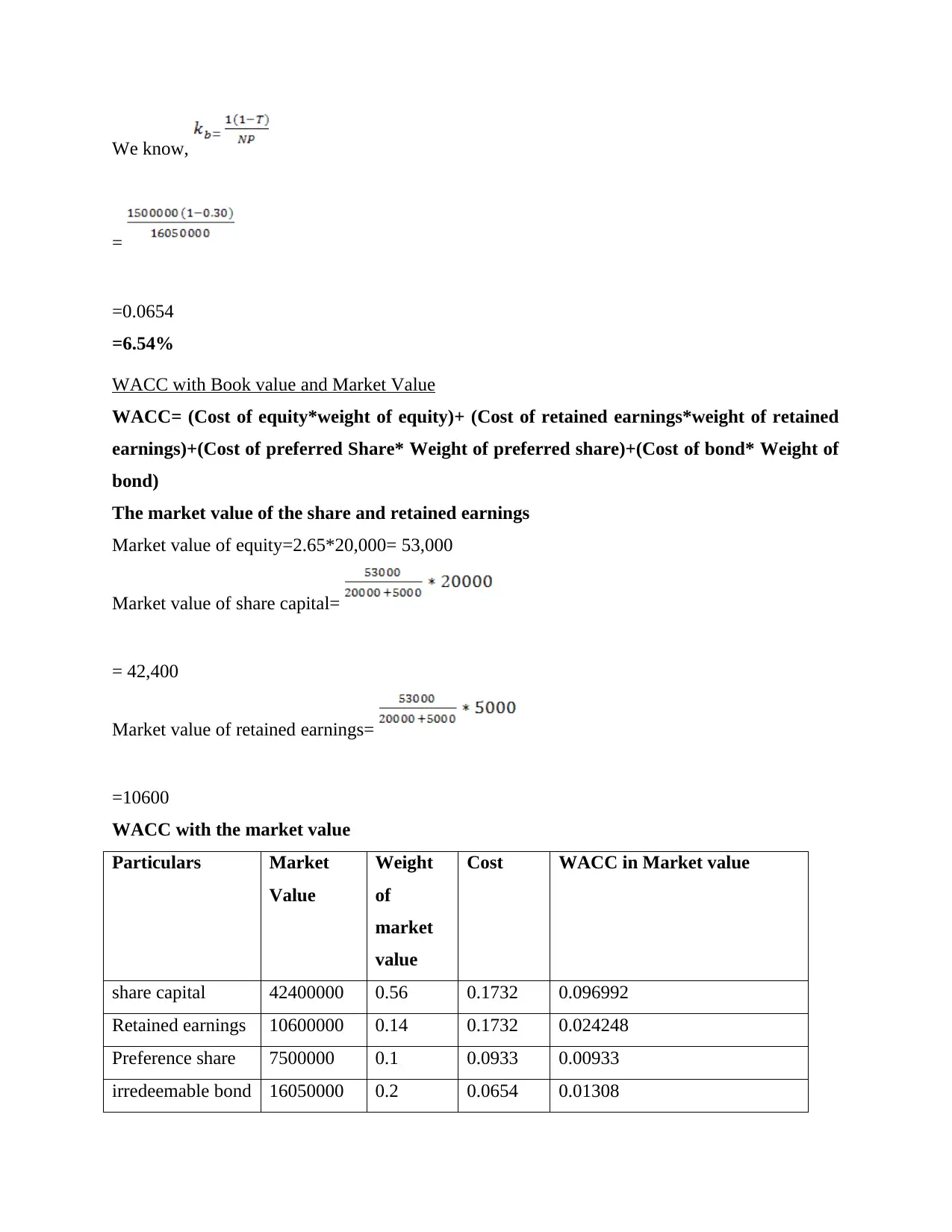

We know,

=

=0.0654

=6.54%

WACC with Book value and Market Value

WACC= (Cost of equity*weight of equity)+ (Cost of retained earnings*weight of retained

earnings)+(Cost of preferred Share* Weight of preferred share)+(Cost of bond* Weight of

bond)

The market value of the share and retained earnings

Market value of equity=2.65*20,000= 53,000

Market value of share capital=

= 42,400

Market value of retained earnings=

=10600

WACC with the market value

Particulars Market

Value

Weight

of

market

value

Cost WACC in Market value

share capital 42400000 0.56 0.1732 0.096992

Retained earnings 10600000 0.14 0.1732 0.024248

Preference share 7500000 0.1 0.0933 0.00933

irredeemable bond 16050000 0.2 0.0654 0.01308

=

=0.0654

=6.54%

WACC with Book value and Market Value

WACC= (Cost of equity*weight of equity)+ (Cost of retained earnings*weight of retained

earnings)+(Cost of preferred Share* Weight of preferred share)+(Cost of bond* Weight of

bond)

The market value of the share and retained earnings

Market value of equity=2.65*20,000= 53,000

Market value of share capital=

= 42,400

Market value of retained earnings=

=10600

WACC with the market value

Particulars Market

Value

Weight

of

market

value

Cost WACC in Market value

share capital 42400000 0.56 0.1732 0.096992

Retained earnings 10600000 0.14 0.1732 0.024248

Preference share 7500000 0.1 0.0933 0.00933

irredeemable bond 16050000 0.2 0.0654 0.01308

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

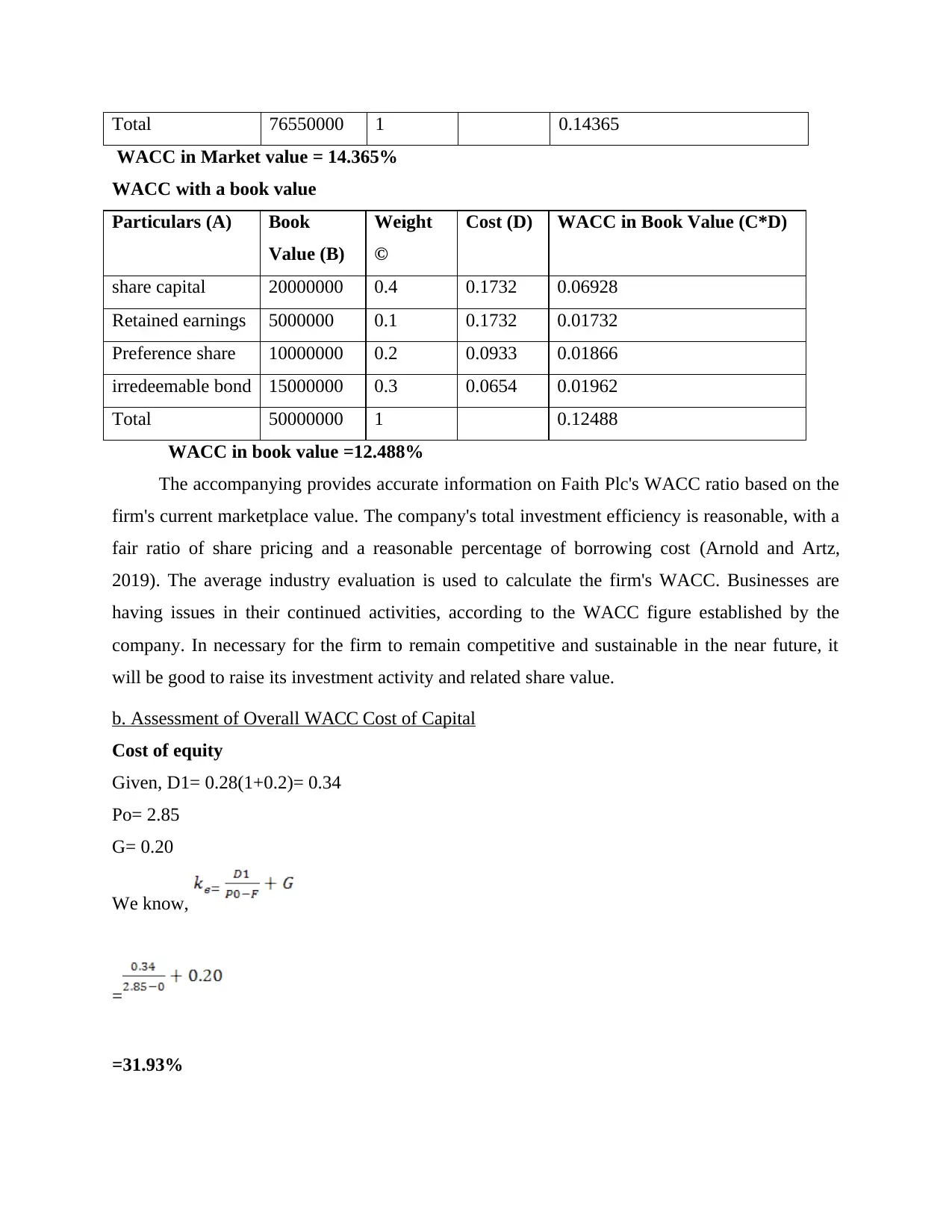

Total 76550000 1 0.14365

WACC in Market value = 14.365%

WACC with a book value

Particulars (A) Book

Value (B)

Weight

©

Cost (D) WACC in Book Value (C*D)

share capital 20000000 0.4 0.1732 0.06928

Retained earnings 5000000 0.1 0.1732 0.01732

Preference share 10000000 0.2 0.0933 0.01866

irredeemable bond 15000000 0.3 0.0654 0.01962

Total 50000000 1 0.12488

WACC in book value =12.488%

The accompanying provides accurate information on Faith Plc's WACC ratio based on the

firm's current marketplace value. The company's total investment efficiency is reasonable, with a

fair ratio of share pricing and a reasonable percentage of borrowing cost (Arnold and Artz,

2019). The average industry evaluation is used to calculate the firm's WACC. Businesses are

having issues in their continued activities, according to the WACC figure established by the

company. In necessary for the firm to remain competitive and sustainable in the near future, it

will be good to raise its investment activity and related share value.

b. Assessment of Overall WACC Cost of Capital

Cost of equity

Given, D1= 0.28(1+0.2)= 0.34

Po= 2.85

G= 0.20

We know,

=

=31.93%

WACC in Market value = 14.365%

WACC with a book value

Particulars (A) Book

Value (B)

Weight

©

Cost (D) WACC in Book Value (C*D)

share capital 20000000 0.4 0.1732 0.06928

Retained earnings 5000000 0.1 0.1732 0.01732

Preference share 10000000 0.2 0.0933 0.01866

irredeemable bond 15000000 0.3 0.0654 0.01962

Total 50000000 1 0.12488

WACC in book value =12.488%

The accompanying provides accurate information on Faith Plc's WACC ratio based on the

firm's current marketplace value. The company's total investment efficiency is reasonable, with a

fair ratio of share pricing and a reasonable percentage of borrowing cost (Arnold and Artz,

2019). The average industry evaluation is used to calculate the firm's WACC. Businesses are

having issues in their continued activities, according to the WACC figure established by the

company. In necessary for the firm to remain competitive and sustainable in the near future, it

will be good to raise its investment activity and related share value.

b. Assessment of Overall WACC Cost of Capital

Cost of equity

Given, D1= 0.28(1+0.2)= 0.34

Po= 2.85

G= 0.20

We know,

=

=31.93%

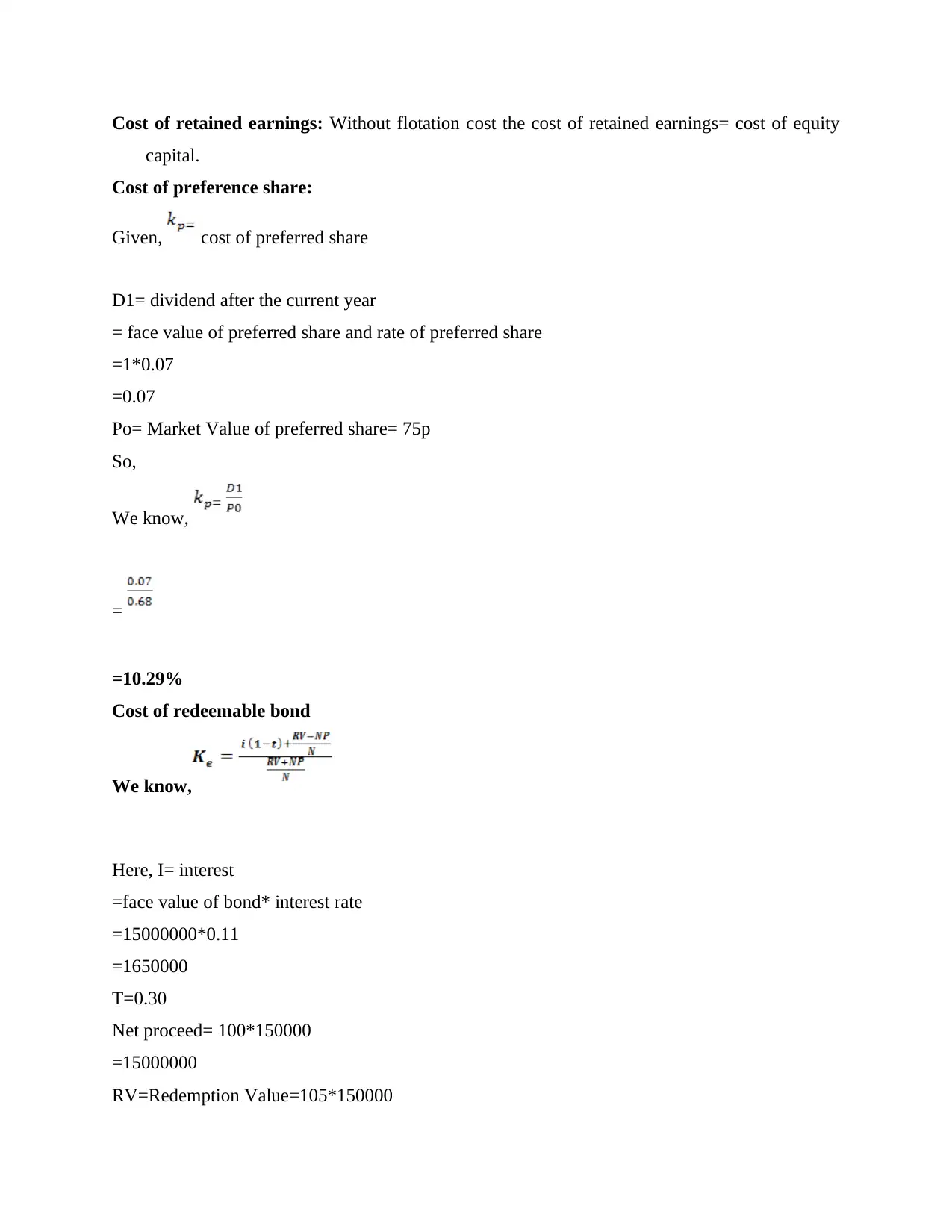

Cost of retained earnings: Without flotation cost the cost of retained earnings= cost of equity

capital.

Cost of preference share:

Given, cost of preferred share

D1= dividend after the current year

= face value of preferred share and rate of preferred share

=1*0.07

=0.07

Po= Market Value of preferred share= 75p

So,

We know,

=

=10.29%

Cost of redeemable bond

We know,

Here, I= interest

=face value of bond* interest rate

=15000000*0.11

=1650000

T=0.30

Net proceed= 100*150000

=15000000

RV=Redemption Value=105*150000

capital.

Cost of preference share:

Given, cost of preferred share

D1= dividend after the current year

= face value of preferred share and rate of preferred share

=1*0.07

=0.07

Po= Market Value of preferred share= 75p

So,

We know,

=

=10.29%

Cost of redeemable bond

We know,

Here, I= interest

=face value of bond* interest rate

=15000000*0.11

=1650000

T=0.30

Net proceed= 100*150000

=15000000

RV=Redemption Value=105*150000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

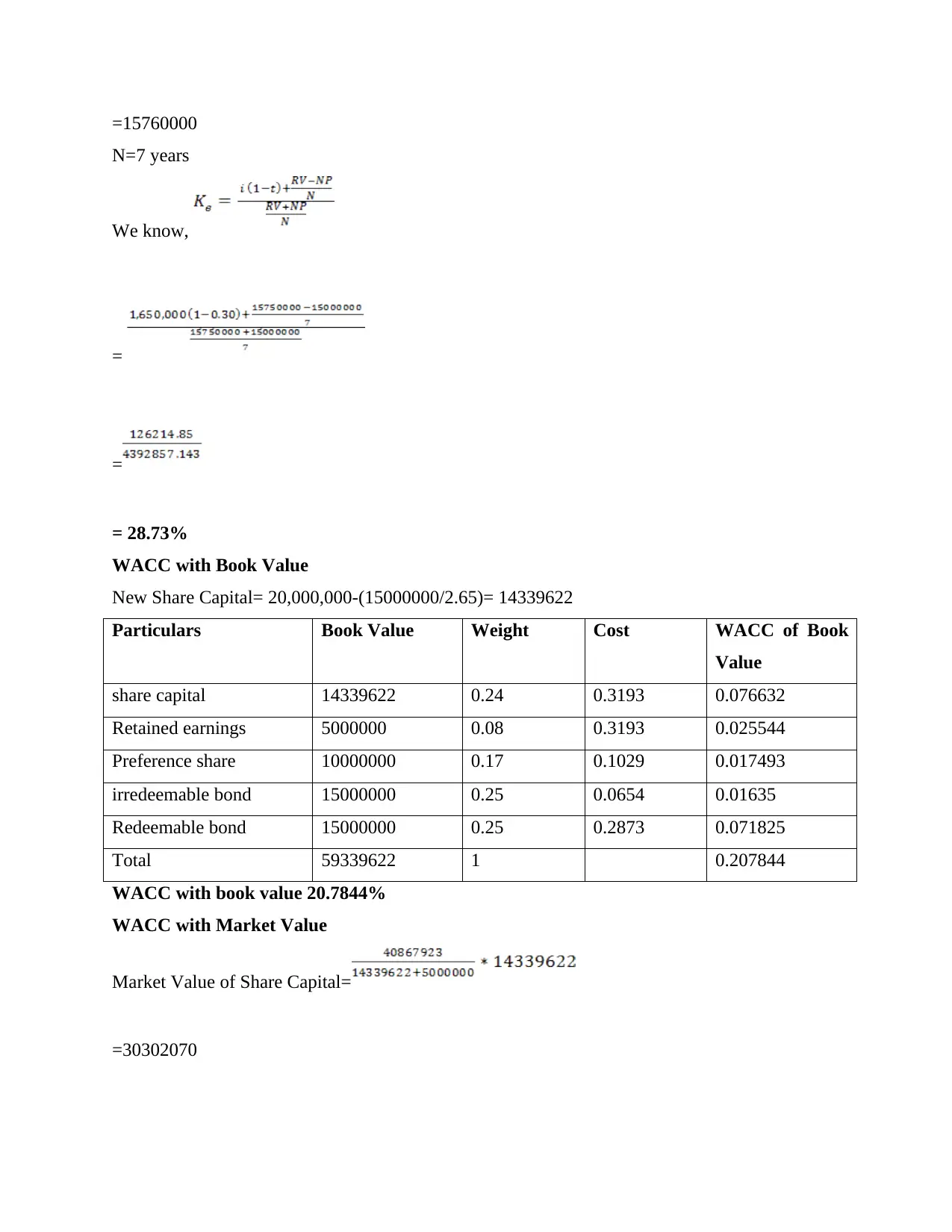

=15760000

N=7 years

We know,

=

=

= 28.73%

WACC with Book Value

New Share Capital= 20,000,000-(15000000/2.65)= 14339622

Particulars Book Value Weight Cost WACC of Book

Value

share capital 14339622 0.24 0.3193 0.076632

Retained earnings 5000000 0.08 0.3193 0.025544

Preference share 10000000 0.17 0.1029 0.017493

irredeemable bond 15000000 0.25 0.0654 0.01635

Redeemable bond 15000000 0.25 0.2873 0.071825

Total 59339622 1 0.207844

WACC with book value 20.7844%

WACC with Market Value

Market Value of Share Capital=

=30302070

N=7 years

We know,

=

=

= 28.73%

WACC with Book Value

New Share Capital= 20,000,000-(15000000/2.65)= 14339622

Particulars Book Value Weight Cost WACC of Book

Value

share capital 14339622 0.24 0.3193 0.076632

Retained earnings 5000000 0.08 0.3193 0.025544

Preference share 10000000 0.17 0.1029 0.017493

irredeemable bond 15000000 0.25 0.0654 0.01635

Redeemable bond 15000000 0.25 0.2873 0.071825

Total 59339622 1 0.207844

WACC with book value 20.7844%

WACC with Market Value

Market Value of Share Capital=

=30302070

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

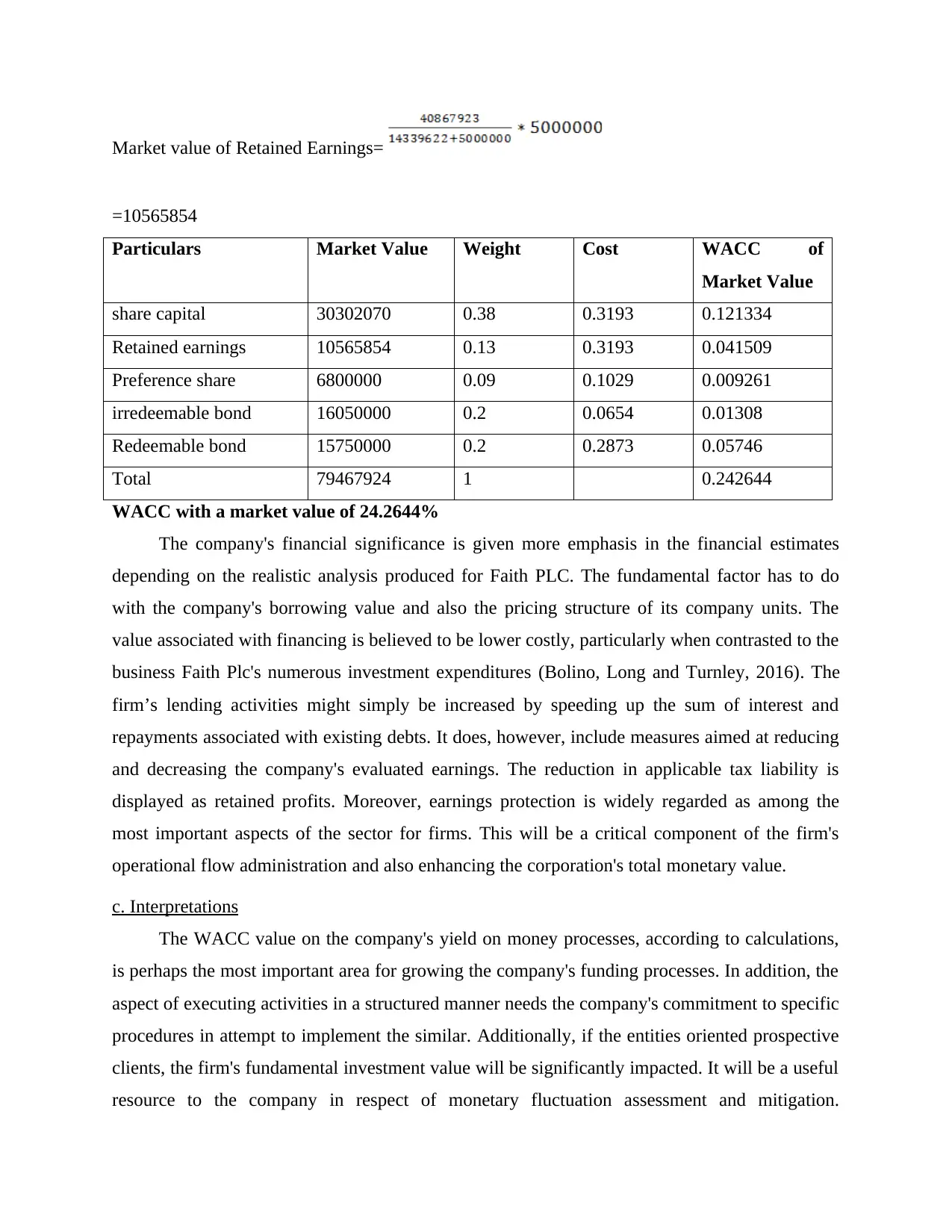

Market value of Retained Earnings=

=10565854

Particulars Market Value Weight Cost WACC of

Market Value

share capital 30302070 0.38 0.3193 0.121334

Retained earnings 10565854 0.13 0.3193 0.041509

Preference share 6800000 0.09 0.1029 0.009261

irredeemable bond 16050000 0.2 0.0654 0.01308

Redeemable bond 15750000 0.2 0.2873 0.05746

Total 79467924 1 0.242644

WACC with a market value of 24.2644%

The company's financial significance is given more emphasis in the financial estimates

depending on the realistic analysis produced for Faith PLC. The fundamental factor has to do

with the company's borrowing value and also the pricing structure of its company units. The

value associated with financing is believed to be lower costly, particularly when contrasted to the

business Faith Plc's numerous investment expenditures (Bolino, Long and Turnley, 2016). The

firm’s lending activities might simply be increased by speeding up the sum of interest and

repayments associated with existing debts. It does, however, include measures aimed at reducing

and decreasing the company's evaluated earnings. The reduction in applicable tax liability is

displayed as retained profits. Moreover, earnings protection is widely regarded as among the

most important aspects of the sector for firms. This will be a critical component of the firm's

operational flow administration and also enhancing the corporation's total monetary value.

c. Interpretations

The WACC value on the company's yield on money processes, according to calculations,

is perhaps the most important area for growing the company's funding processes. In addition, the

aspect of executing activities in a structured manner needs the company's commitment to specific

procedures in attempt to implement the similar. Additionally, if the entities oriented prospective

clients, the firm's fundamental investment value will be significantly impacted. It will be a useful

resource to the company in respect of monetary fluctuation assessment and mitigation.

=10565854

Particulars Market Value Weight Cost WACC of

Market Value

share capital 30302070 0.38 0.3193 0.121334

Retained earnings 10565854 0.13 0.3193 0.041509

Preference share 6800000 0.09 0.1029 0.009261

irredeemable bond 16050000 0.2 0.0654 0.01308

Redeemable bond 15750000 0.2 0.2873 0.05746

Total 79467924 1 0.242644

WACC with a market value of 24.2644%

The company's financial significance is given more emphasis in the financial estimates

depending on the realistic analysis produced for Faith PLC. The fundamental factor has to do

with the company's borrowing value and also the pricing structure of its company units. The

value associated with financing is believed to be lower costly, particularly when contrasted to the

business Faith Plc's numerous investment expenditures (Bolino, Long and Turnley, 2016). The

firm’s lending activities might simply be increased by speeding up the sum of interest and

repayments associated with existing debts. It does, however, include measures aimed at reducing

and decreasing the company's evaluated earnings. The reduction in applicable tax liability is

displayed as retained profits. Moreover, earnings protection is widely regarded as among the

most important aspects of the sector for firms. This will be a critical component of the firm's

operational flow administration and also enhancing the corporation's total monetary value.

c. Interpretations

The WACC value on the company's yield on money processes, according to calculations,

is perhaps the most important area for growing the company's funding processes. In addition, the

aspect of executing activities in a structured manner needs the company's commitment to specific

procedures in attempt to implement the similar. Additionally, if the entities oriented prospective

clients, the firm's fundamental investment value will be significantly impacted. It will be a useful

resource to the company in respect of monetary fluctuation assessment and mitigation.

Conventional theory is perhaps the most suitable notion to include in the company's WACC

pricing evaluation technique (Brierley, 2017). The investment activities of Faith Plc, including

its leverage proportion, must be managed in an organised way. This must help to achieve better

and more consistent maintenance of the WACC threshold. When the organization's gearing

proportion rises, on either hand, the WACC value of the company is controlled and protected.

The WACC statistic gets substantially more accurate and trustworthy as the borrowing prices

tied to the firm's investment expenditure climb. A decrease in the effective borrowing rates, on

either side, would assist the organisation in regards of building a more equitable technique of

forecasting for the current and future.

d. There is a link between the company's IRR and WACC classification

In the case of capital management or numerous financial situations of the business, both

the methods, WACC and IRR, are utilised simultaneously, although for different goals.

Moreover, regardless of the notion that they will be used in the identical manner, the concepts of

IRR and WACC differ. It's most well acknowledged as a matrix that shows statistics to calculate

the overall present value of cash inflow sequencing. Likewise, Faith Plc, the present corporation,

uses the approach in reality to determine and analyse network upgrades. The company may

expect more monetary productivity if it set greater corporate goals. Additionally, WACC is a

proportional way of calculating the yearly taxes expenditure of a company's capital assets. It

allows the company to evaluate its payout in particular to determine the value of its corporate

stock structure (Donnez and Dolmans, 2016). While a company starts a venture, it must calculate

WACC to assess the variability of the company, whereas IRR is utilised to evaluate the

spending. The corporation substantially encourages the concept as well as the method of

financial forecasting in order to make a decision on corporate financial exchanges. As a

consequence, such techniques help the company increase its range by selecting promising and

beneficial regions. From a management standpoint, firms used to link the process for making

investment decisions with average financing costs. The link implies that the present value of the

business is more than the value of cash spending, enabling the NPV to be computed, and the

value of NPV is 0.

Question 2- Investment Appraisal Techniques

Given,

Initial Investment= £588,300

pricing evaluation technique (Brierley, 2017). The investment activities of Faith Plc, including

its leverage proportion, must be managed in an organised way. This must help to achieve better

and more consistent maintenance of the WACC threshold. When the organization's gearing

proportion rises, on either hand, the WACC value of the company is controlled and protected.

The WACC statistic gets substantially more accurate and trustworthy as the borrowing prices

tied to the firm's investment expenditure climb. A decrease in the effective borrowing rates, on

either side, would assist the organisation in regards of building a more equitable technique of

forecasting for the current and future.

d. There is a link between the company's IRR and WACC classification

In the case of capital management or numerous financial situations of the business, both

the methods, WACC and IRR, are utilised simultaneously, although for different goals.

Moreover, regardless of the notion that they will be used in the identical manner, the concepts of

IRR and WACC differ. It's most well acknowledged as a matrix that shows statistics to calculate

the overall present value of cash inflow sequencing. Likewise, Faith Plc, the present corporation,

uses the approach in reality to determine and analyse network upgrades. The company may

expect more monetary productivity if it set greater corporate goals. Additionally, WACC is a

proportional way of calculating the yearly taxes expenditure of a company's capital assets. It

allows the company to evaluate its payout in particular to determine the value of its corporate

stock structure (Donnez and Dolmans, 2016). While a company starts a venture, it must calculate

WACC to assess the variability of the company, whereas IRR is utilised to evaluate the

spending. The corporation substantially encourages the concept as well as the method of

financial forecasting in order to make a decision on corporate financial exchanges. As a

consequence, such techniques help the company increase its range by selecting promising and

beneficial regions. From a management standpoint, firms used to link the process for making

investment decisions with average financing costs. The link implies that the present value of the

business is more than the value of cash spending, enabling the NPV to be computed, and the

value of NPV is 0.

Question 2- Investment Appraisal Techniques

Given,

Initial Investment= £588,300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.