Financial Management: Investment Appraisal Techniques Analysis

VerifiedAdded on 2022/11/28

|26

|3455

|125

Report

AI Summary

This report delves into the realm of financial management, meticulously examining various investment appraisal techniques. It begins by defining financial management and its critical role in strategic planning, resource allocation, and operational efficiency within a company. The core of the report centers on the calculation and evaluation of investment appraisal techniques, including the payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). Each technique is thoroughly computed, analyzed, and critically assessed to determine its viability and feasibility for investment decisions. Furthermore, the report provides a comparative analysis of the advantages and disadvantages of each method, offering insights into their practical application. The report also addresses the implications of specific financial decisions, such as the repurchase of equity and the payment of dividends, in the context of maximizing work efficiency and profitability. The findings highlight the importance of selecting the most appropriate financial strategies to enhance the financial health and performance of a business. The report concludes with a summary of the findings and their implications for effective financial management.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Question 2........................................................................................................................................3

A) Calculation of investment appraisal techniques.....................................................................3

B) Critical evaluation of the new proposal of the company........................................................7

Question 3......................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

Question 2........................................................................................................................................3

A) Calculation of investment appraisal techniques.....................................................................3

B) Critical evaluation of the new proposal of the company........................................................7

Question 3......................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Finance management can be described as the planning of strategy, arranging, and managing of

financial decisions and allocations. This is in reference to the notion that without money, no one

or company can work effectively or efficiently. The reason for this is that money is the most

important element that a company needs in order to make the best use of its resources and

manage its operations. Financial management is critical since it allows the company's

management to appropriately distribute finances within the business activities in order to

maximise output. This financial management will also help organisations provide financial

information to all of the company's owners. The computation of investment appraisal approaches

for analysing the feasibility and viability of the project will be outlined in this report. In addition

to this research of the organisation, the decision of a merger and acquisition have been

considered. The report also discusses several valuation methods of valuation, their benefits and

drawbacks, and offers suggestions for selecting the optimal value approach.

Question 2

Investment appraisal techniques

Investment appraisal techniques are the various methods relating to the viability of the

investment option (Ameliawati and Setiyani, 2018). This involves the different methods through

which the company can evaluate and analyse the viability and feasibility of the investment option

which will provide benefits to the company.

A) Calculation of investment appraisal techniques

Payback period

Computation of Payback period

Year Cash inflows Cumulative cash inflows

1 -100100 -100100

2 -100100 -200200

3 -100100 -300300

4 -100100 -400400

Finance management can be described as the planning of strategy, arranging, and managing of

financial decisions and allocations. This is in reference to the notion that without money, no one

or company can work effectively or efficiently. The reason for this is that money is the most

important element that a company needs in order to make the best use of its resources and

manage its operations. Financial management is critical since it allows the company's

management to appropriately distribute finances within the business activities in order to

maximise output. This financial management will also help organisations provide financial

information to all of the company's owners. The computation of investment appraisal approaches

for analysing the feasibility and viability of the project will be outlined in this report. In addition

to this research of the organisation, the decision of a merger and acquisition have been

considered. The report also discusses several valuation methods of valuation, their benefits and

drawbacks, and offers suggestions for selecting the optimal value approach.

Question 2

Investment appraisal techniques

Investment appraisal techniques are the various methods relating to the viability of the

investment option (Ameliawati and Setiyani, 2018). This involves the different methods through

which the company can evaluate and analyse the viability and feasibility of the investment option

which will provide benefits to the company.

A) Calculation of investment appraisal techniques

Payback period

Computation of Payback period

Year Cash inflows Cumulative cash inflows

1 -100100 -100100

2 -100100 -200200

3 -100100 -300300

4 -100100 -400400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 -100100 -500500

6 -100100 -600600

Initial investment 788300

Payback period Infinity

Payback period 4 year and half month/ 4.5 years

The cash inflow generated under this decision making is negative in nature. This is a false

decision making that can be taken by the business enterprises. This option allow the company to

offer more cash outflow than the cash inflow that do not support any positive inflow under the

business of company (Kehinde and Olugbenga, 2017). The whole situation is against the

business entity where the company do not favour the company to gain any positive inflow. As

per the expected figure the company will never be able to recover its original investment from

the whole decision making.

Accounting rate of return

Computation of Average rate of return

Year Cash inflows

1 -100100

2 -100100

3 -100100

4 -100100

5 -100100

6 -100100

Average profit or cash inflow -100100

Average initial investment 788300

average initial investment

[(initial investment + scrap value)

6 -100100 -600600

Initial investment 788300

Payback period Infinity

Payback period 4 year and half month/ 4.5 years

The cash inflow generated under this decision making is negative in nature. This is a false

decision making that can be taken by the business enterprises. This option allow the company to

offer more cash outflow than the cash inflow that do not support any positive inflow under the

business of company (Kehinde and Olugbenga, 2017). The whole situation is against the

business entity where the company do not favour the company to gain any positive inflow. As

per the expected figure the company will never be able to recover its original investment from

the whole decision making.

Accounting rate of return

Computation of Average rate of return

Year Cash inflows

1 -100100

2 -100100

3 -100100

4 -100100

5 -100100

6 -100100

Average profit or cash inflow -100100

Average initial investment 788300

average initial investment

[(initial investment + scrap value)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

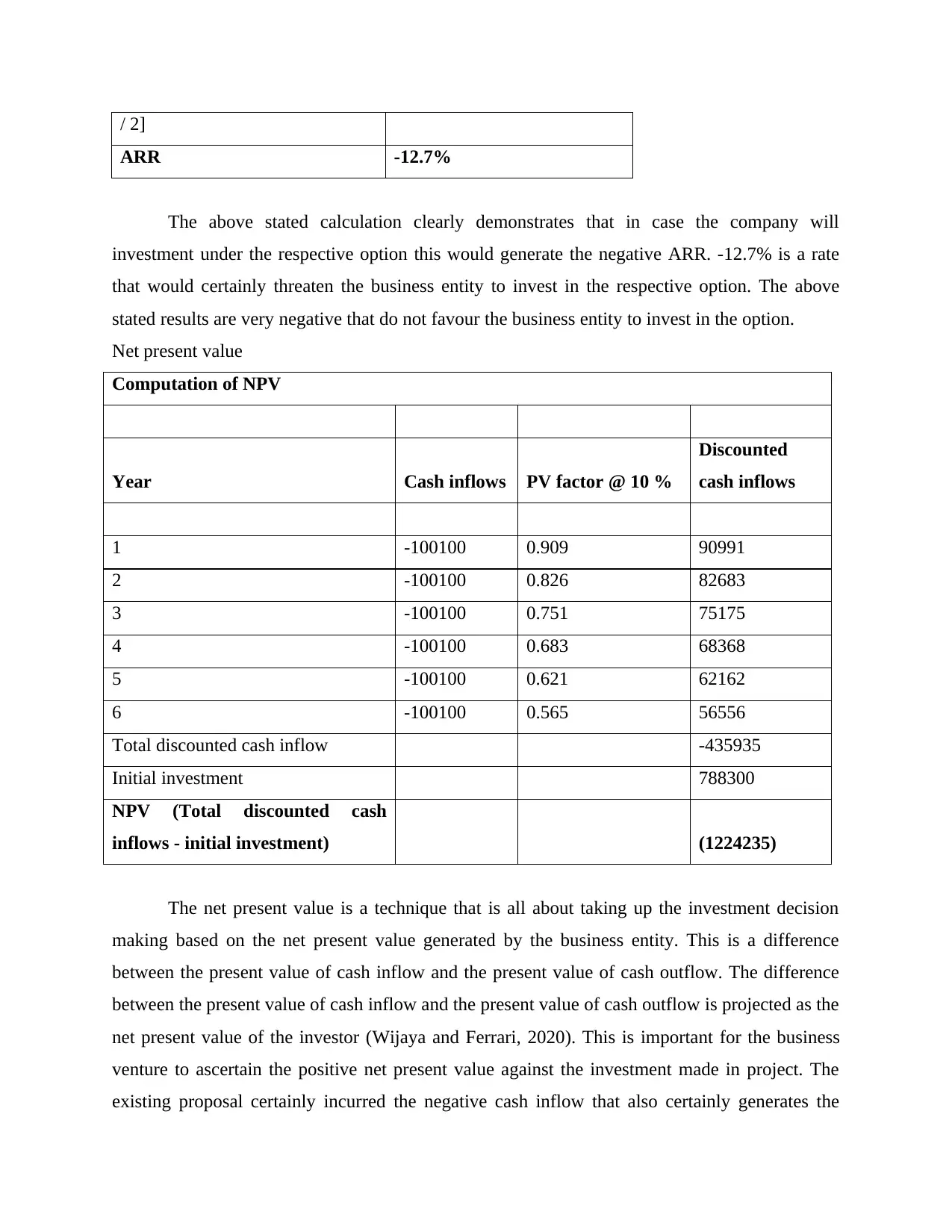

/ 2]

ARR -12.7%

The above stated calculation clearly demonstrates that in case the company will

investment under the respective option this would generate the negative ARR. -12.7% is a rate

that would certainly threaten the business entity to invest in the respective option. The above

stated results are very negative that do not favour the business entity to invest in the option.

Net present value

Computation of NPV

Year Cash inflows PV factor @ 10 %

Discounted

cash inflows

1 -100100 0.909 90991

2 -100100 0.826 82683

3 -100100 0.751 75175

4 -100100 0.683 68368

5 -100100 0.621 62162

6 -100100 0.565 56556

Total discounted cash inflow -435935

Initial investment 788300

NPV (Total discounted cash

inflows - initial investment) (1224235)

The net present value is a technique that is all about taking up the investment decision

making based on the net present value generated by the business entity. This is a difference

between the present value of cash inflow and the present value of cash outflow. The difference

between the present value of cash inflow and the present value of cash outflow is projected as the

net present value of the investor (Wijaya and Ferrari, 2020). This is important for the business

venture to ascertain the positive net present value against the investment made in project. The

existing proposal certainly incurred the negative cash inflow that also certainly generates the

ARR -12.7%

The above stated calculation clearly demonstrates that in case the company will

investment under the respective option this would generate the negative ARR. -12.7% is a rate

that would certainly threaten the business entity to invest in the respective option. The above

stated results are very negative that do not favour the business entity to invest in the option.

Net present value

Computation of NPV

Year Cash inflows PV factor @ 10 %

Discounted

cash inflows

1 -100100 0.909 90991

2 -100100 0.826 82683

3 -100100 0.751 75175

4 -100100 0.683 68368

5 -100100 0.621 62162

6 -100100 0.565 56556

Total discounted cash inflow -435935

Initial investment 788300

NPV (Total discounted cash

inflows - initial investment) (1224235)

The net present value is a technique that is all about taking up the investment decision

making based on the net present value generated by the business entity. This is a difference

between the present value of cash inflow and the present value of cash outflow. The difference

between the present value of cash inflow and the present value of cash outflow is projected as the

net present value of the investor (Wijaya and Ferrari, 2020). This is important for the business

venture to ascertain the positive net present value against the investment made in project. The

existing proposal certainly incurred the negative cash inflow that also certainly generates the

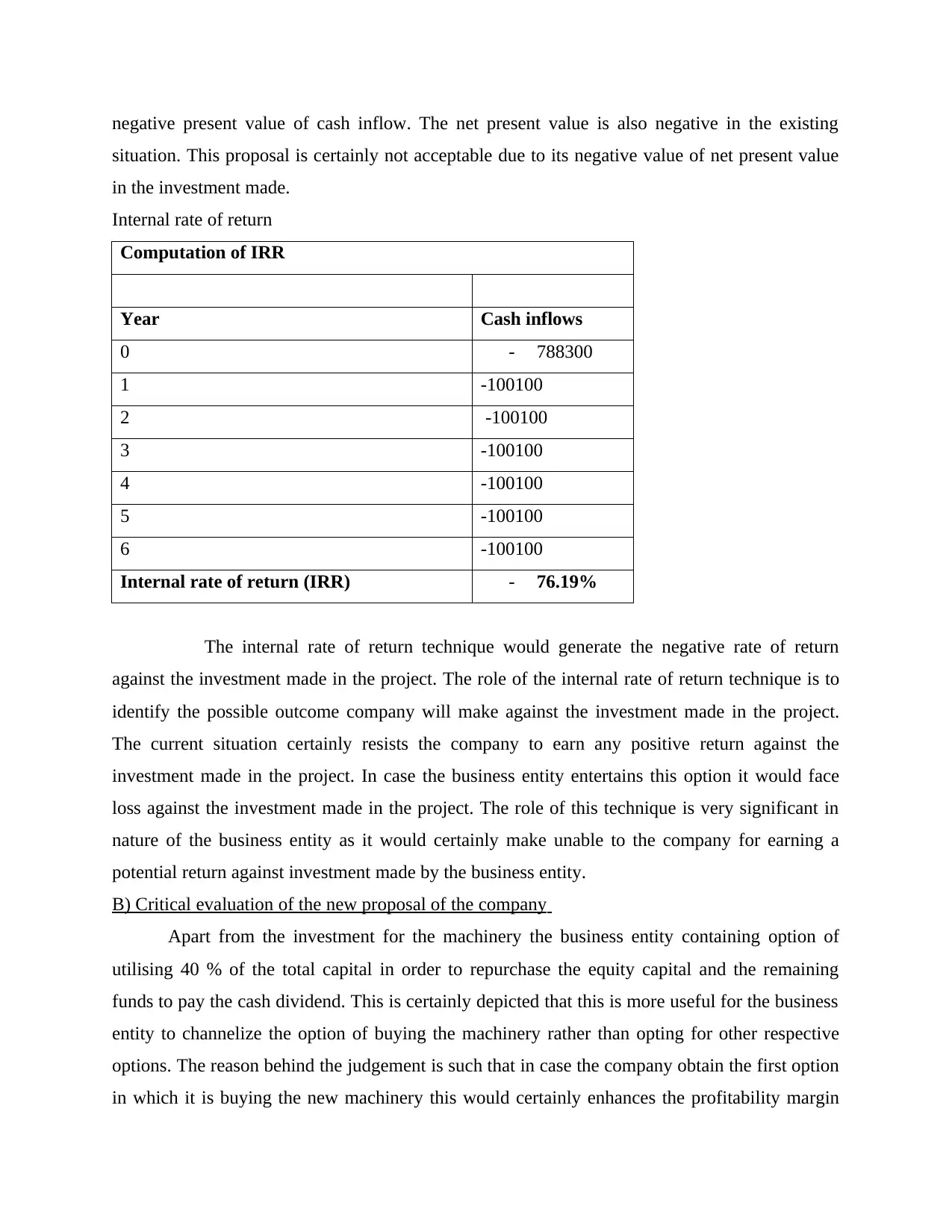

negative present value of cash inflow. The net present value is also negative in the existing

situation. This proposal is certainly not acceptable due to its negative value of net present value

in the investment made.

Internal rate of return

Computation of IRR

Year Cash inflows

0 - 788300

1 -100100

2 -100100

3 -100100

4 -100100

5 -100100

6 -100100

Internal rate of return (IRR) - 76.19%

The internal rate of return technique would generate the negative rate of return

against the investment made in the project. The role of the internal rate of return technique is to

identify the possible outcome company will make against the investment made in the project.

The current situation certainly resists the company to earn any positive return against the

investment made in the project. In case the business entity entertains this option it would face

loss against the investment made in the project. The role of this technique is very significant in

nature of the business entity as it would certainly make unable to the company for earning a

potential return against investment made by the business entity.

B) Critical evaluation of the new proposal of the company

Apart from the investment for the machinery the business entity containing option of

utilising 40 % of the total capital in order to repurchase the equity capital and the remaining

funds to pay the cash dividend. This is certainly depicted that this is more useful for the business

entity to channelize the option of buying the machinery rather than opting for other respective

options. The reason behind the judgement is such that in case the company obtain the first option

in which it is buying the new machinery this would certainly enhances the profitability margin

situation. This proposal is certainly not acceptable due to its negative value of net present value

in the investment made.

Internal rate of return

Computation of IRR

Year Cash inflows

0 - 788300

1 -100100

2 -100100

3 -100100

4 -100100

5 -100100

6 -100100

Internal rate of return (IRR) - 76.19%

The internal rate of return technique would generate the negative rate of return

against the investment made in the project. The role of the internal rate of return technique is to

identify the possible outcome company will make against the investment made in the project.

The current situation certainly resists the company to earn any positive return against the

investment made in the project. In case the business entity entertains this option it would face

loss against the investment made in the project. The role of this technique is very significant in

nature of the business entity as it would certainly make unable to the company for earning a

potential return against investment made by the business entity.

B) Critical evaluation of the new proposal of the company

Apart from the investment for the machinery the business entity containing option of

utilising 40 % of the total capital in order to repurchase the equity capital and the remaining

funds to pay the cash dividend. This is certainly depicted that this is more useful for the business

entity to channelize the option of buying the machinery rather than opting for other respective

options. The reason behind the judgement is such that in case the company obtain the first option

in which it is buying the new machinery this would certainly enhances the profitability margin

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

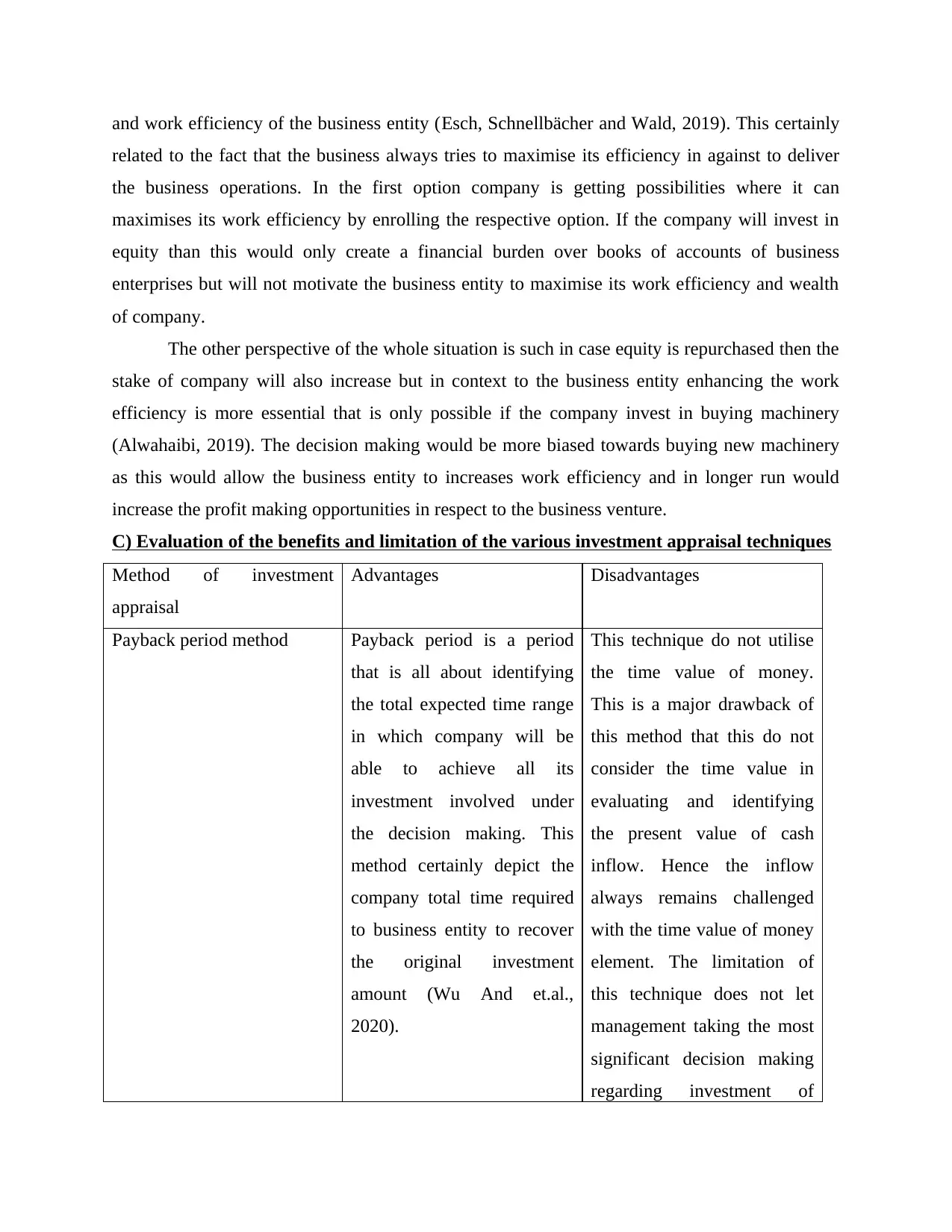

and work efficiency of the business entity (Esch, Schnellbächer and Wald, 2019). This certainly

related to the fact that the business always tries to maximise its efficiency in against to deliver

the business operations. In the first option company is getting possibilities where it can

maximises its work efficiency by enrolling the respective option. If the company will invest in

equity than this would only create a financial burden over books of accounts of business

enterprises but will not motivate the business entity to maximise its work efficiency and wealth

of company.

The other perspective of the whole situation is such in case equity is repurchased then the

stake of company will also increase but in context to the business entity enhancing the work

efficiency is more essential that is only possible if the company invest in buying machinery

(Alwahaibi, 2019). The decision making would be more biased towards buying new machinery

as this would allow the business entity to increases work efficiency and in longer run would

increase the profit making opportunities in respect to the business venture.

C) Evaluation of the benefits and limitation of the various investment appraisal techniques

Method of investment

appraisal

Advantages Disadvantages

Payback period method Payback period is a period

that is all about identifying

the total expected time range

in which company will be

able to achieve all its

investment involved under

the decision making. This

method certainly depict the

company total time required

to business entity to recover

the original investment

amount (Wu And et.al.,

2020).

This technique do not utilise

the time value of money.

This is a major drawback of

this method that this do not

consider the time value in

evaluating and identifying

the present value of cash

inflow. Hence the inflow

always remains challenged

with the time value of money

element. The limitation of

this technique does not let

management taking the most

significant decision making

regarding investment of

related to the fact that the business always tries to maximise its efficiency in against to deliver

the business operations. In the first option company is getting possibilities where it can

maximises its work efficiency by enrolling the respective option. If the company will invest in

equity than this would only create a financial burden over books of accounts of business

enterprises but will not motivate the business entity to maximise its work efficiency and wealth

of company.

The other perspective of the whole situation is such in case equity is repurchased then the

stake of company will also increase but in context to the business entity enhancing the work

efficiency is more essential that is only possible if the company invest in buying machinery

(Alwahaibi, 2019). The decision making would be more biased towards buying new machinery

as this would allow the business entity to increases work efficiency and in longer run would

increase the profit making opportunities in respect to the business venture.

C) Evaluation of the benefits and limitation of the various investment appraisal techniques

Method of investment

appraisal

Advantages Disadvantages

Payback period method Payback period is a period

that is all about identifying

the total expected time range

in which company will be

able to achieve all its

investment involved under

the decision making. This

method certainly depict the

company total time required

to business entity to recover

the original investment

amount (Wu And et.al.,

2020).

This technique do not utilise

the time value of money.

This is a major drawback of

this method that this do not

consider the time value in

evaluating and identifying

the present value of cash

inflow. Hence the inflow

always remains challenged

with the time value of money

element. The limitation of

this technique does not let

management taking the most

significant decision making

regarding investment of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company.

Accounting rate of return The advantage of using the

accounting rate of return

technique is that this method

of capital budgeting is

associated with accounting

information and other records

are not essential for taking up

the investment decision

making.

The technique is very easy

and competitive in nature as

compare to the other

investment appraisal

techniques.

This technique of investment

appraisal does not consider

the time value of money.

This is a massive drawback

of this method as this do not

involve the time value of

money when it comes to

analysing the investment

decision making (Dimitriou,

2018).

Time value competitive

ignores that do not allow the

company taking up the most

effective investment decision

making.

Another disadvantage or

limitation is that this strategy

does not consider into

account or neglect the flow

of cash from the investment

(Marchioni and Magni,

2018).

Furthermore, the ARR

approach of capital planning

does not take into account the

project's final worth.

Net present value The net present value

technique support the

company and investor to take

up such decisions that can

This method of investment

decision making has a

challenge of identifying the

discounted factors.

Accounting rate of return The advantage of using the

accounting rate of return

technique is that this method

of capital budgeting is

associated with accounting

information and other records

are not essential for taking up

the investment decision

making.

The technique is very easy

and competitive in nature as

compare to the other

investment appraisal

techniques.

This technique of investment

appraisal does not consider

the time value of money.

This is a massive drawback

of this method as this do not

involve the time value of

money when it comes to

analysing the investment

decision making (Dimitriou,

2018).

Time value competitive

ignores that do not allow the

company taking up the most

effective investment decision

making.

Another disadvantage or

limitation is that this strategy

does not consider into

account or neglect the flow

of cash from the investment

(Marchioni and Magni,

2018).

Furthermore, the ARR

approach of capital planning

does not take into account the

project's final worth.

Net present value The net present value

technique support the

company and investor to take

up such decisions that can

This method of investment

decision making has a

challenge of identifying the

discounted factors.

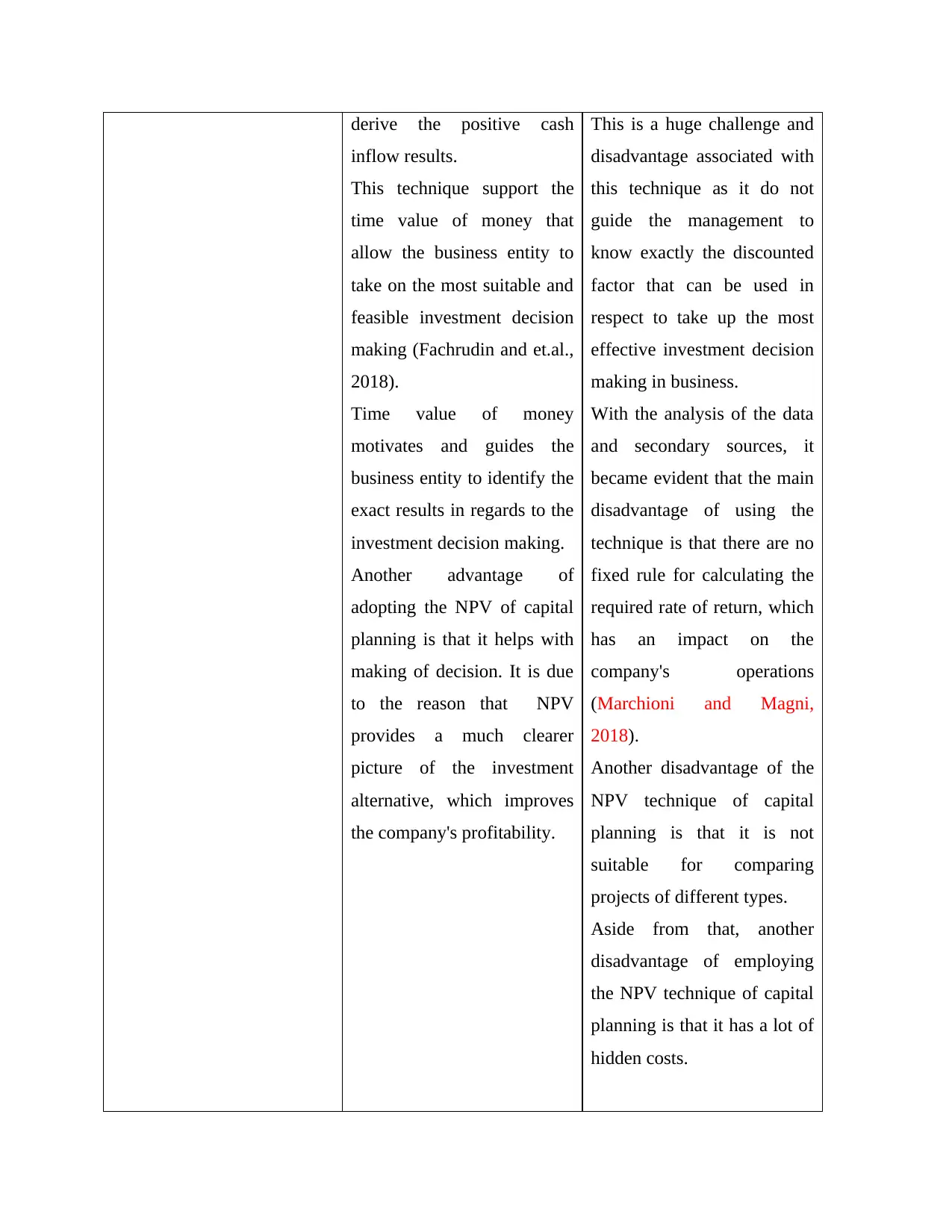

derive the positive cash

inflow results.

This technique support the

time value of money that

allow the business entity to

take on the most suitable and

feasible investment decision

making (Fachrudin and et.al.,

2018).

Time value of money

motivates and guides the

business entity to identify the

exact results in regards to the

investment decision making.

Another advantage of

adopting the NPV of capital

planning is that it helps with

making of decision. It is due

to the reason that NPV

provides a much clearer

picture of the investment

alternative, which improves

the company's profitability.

This is a huge challenge and

disadvantage associated with

this technique as it do not

guide the management to

know exactly the discounted

factor that can be used in

respect to take up the most

effective investment decision

making in business.

With the analysis of the data

and secondary sources, it

became evident that the main

disadvantage of using the

technique is that there are no

fixed rule for calculating the

required rate of return, which

has an impact on the

company's operations

(Marchioni and Magni,

2018).

Another disadvantage of the

NPV technique of capital

planning is that it is not

suitable for comparing

projects of different types.

Aside from that, another

disadvantage of employing

the NPV technique of capital

planning is that it has a lot of

hidden costs.

inflow results.

This technique support the

time value of money that

allow the business entity to

take on the most suitable and

feasible investment decision

making (Fachrudin and et.al.,

2018).

Time value of money

motivates and guides the

business entity to identify the

exact results in regards to the

investment decision making.

Another advantage of

adopting the NPV of capital

planning is that it helps with

making of decision. It is due

to the reason that NPV

provides a much clearer

picture of the investment

alternative, which improves

the company's profitability.

This is a huge challenge and

disadvantage associated with

this technique as it do not

guide the management to

know exactly the discounted

factor that can be used in

respect to take up the most

effective investment decision

making in business.

With the analysis of the data

and secondary sources, it

became evident that the main

disadvantage of using the

technique is that there are no

fixed rule for calculating the

required rate of return, which

has an impact on the

company's operations

(Marchioni and Magni,

2018).

Another disadvantage of the

NPV technique of capital

planning is that it is not

suitable for comparing

projects of different types.

Aside from that, another

disadvantage of employing

the NPV technique of capital

planning is that it has a lot of

hidden costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

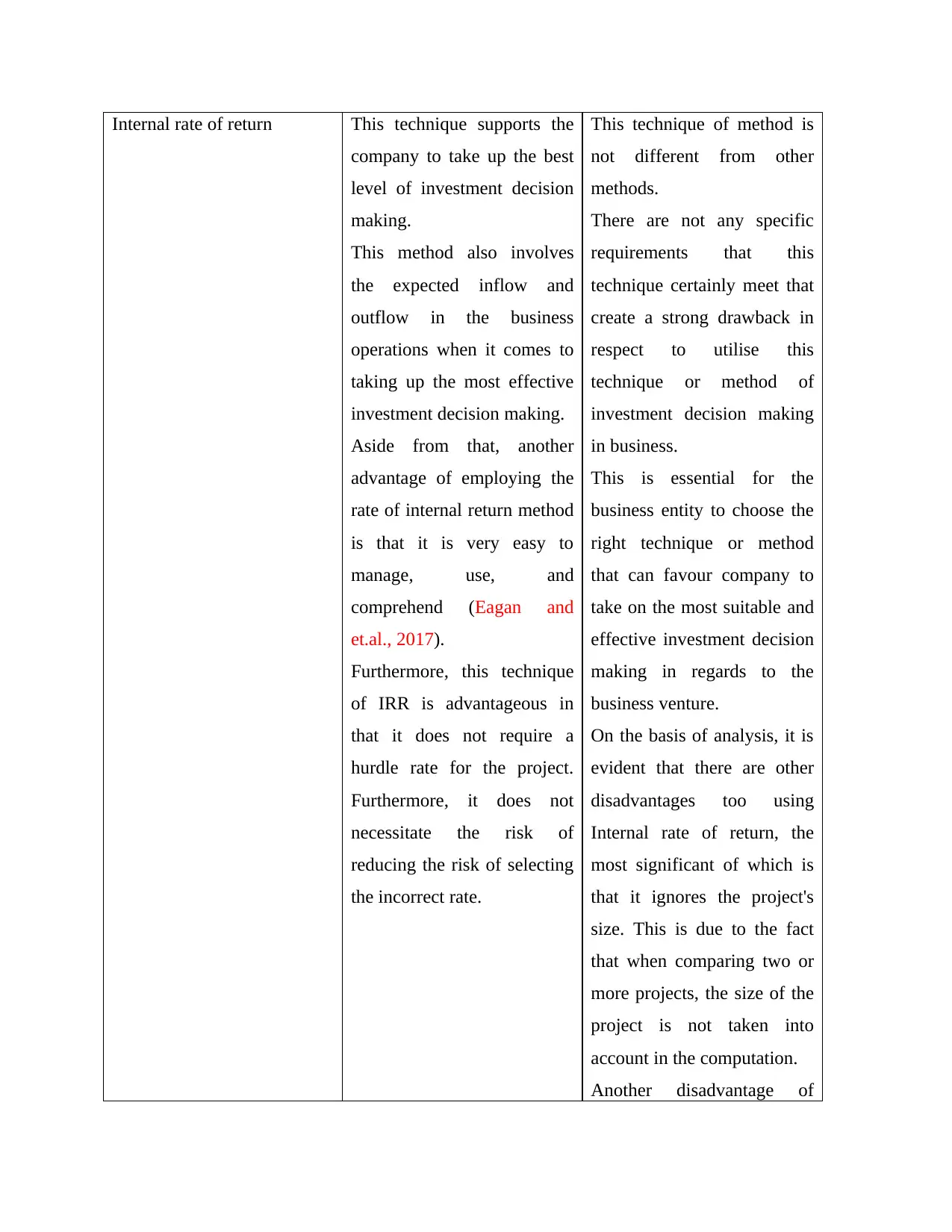

Internal rate of return This technique supports the

company to take up the best

level of investment decision

making.

This method also involves

the expected inflow and

outflow in the business

operations when it comes to

taking up the most effective

investment decision making.

Aside from that, another

advantage of employing the

rate of internal return method

is that it is very easy to

manage, use, and

comprehend (Eagan and

et.al., 2017).

Furthermore, this technique

of IRR is advantageous in

that it does not require a

hurdle rate for the project.

Furthermore, it does not

necessitate the risk of

reducing the risk of selecting

the incorrect rate.

This technique of method is

not different from other

methods.

There are not any specific

requirements that this

technique certainly meet that

create a strong drawback in

respect to utilise this

technique or method of

investment decision making

in business.

This is essential for the

business entity to choose the

right technique or method

that can favour company to

take on the most suitable and

effective investment decision

making in regards to the

business venture.

On the basis of analysis, it is

evident that there are other

disadvantages too using

Internal rate of return, the

most significant of which is

that it ignores the project's

size. This is due to the fact

that when comparing two or

more projects, the size of the

project is not taken into

account in the computation.

Another disadvantage of

company to take up the best

level of investment decision

making.

This method also involves

the expected inflow and

outflow in the business

operations when it comes to

taking up the most effective

investment decision making.

Aside from that, another

advantage of employing the

rate of internal return method

is that it is very easy to

manage, use, and

comprehend (Eagan and

et.al., 2017).

Furthermore, this technique

of IRR is advantageous in

that it does not require a

hurdle rate for the project.

Furthermore, it does not

necessitate the risk of

reducing the risk of selecting

the incorrect rate.

This technique of method is

not different from other

methods.

There are not any specific

requirements that this

technique certainly meet that

create a strong drawback in

respect to utilise this

technique or method of

investment decision making

in business.

This is essential for the

business entity to choose the

right technique or method

that can favour company to

take on the most suitable and

effective investment decision

making in regards to the

business venture.

On the basis of analysis, it is

evident that there are other

disadvantages too using

Internal rate of return, the

most significant of which is

that it ignores the project's

size. This is due to the fact

that when comparing two or

more projects, the size of the

project is not taken into

account in the computation.

Another disadvantage of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

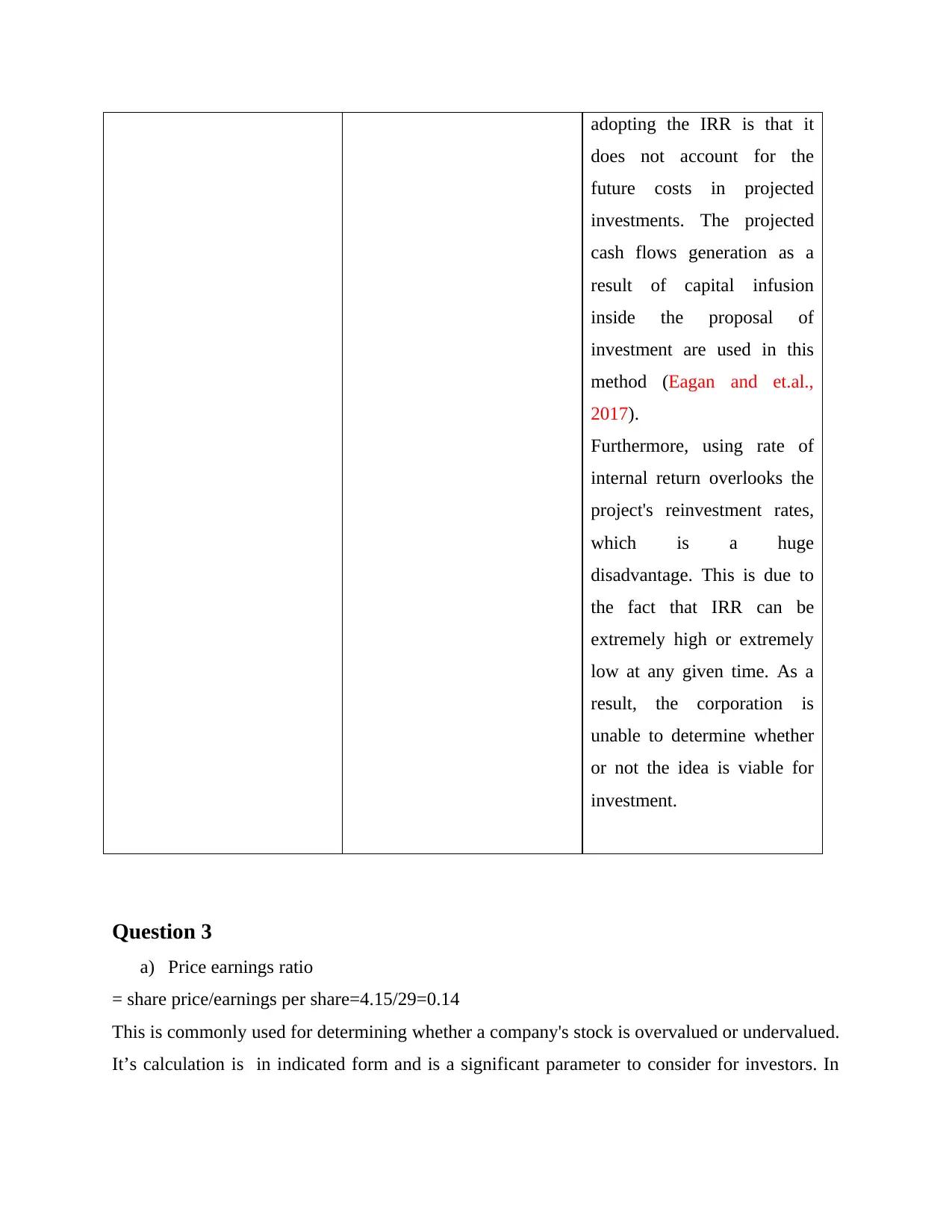

adopting the IRR is that it

does not account for the

future costs in projected

investments. The projected

cash flows generation as a

result of capital infusion

inside the proposal of

investment are used in this

method (Eagan and et.al.,

2017).

Furthermore, using rate of

internal return overlooks the

project's reinvestment rates,

which is a huge

disadvantage. This is due to

the fact that IRR can be

extremely high or extremely

low at any given time. As a

result, the corporation is

unable to determine whether

or not the idea is viable for

investment.

Question 3

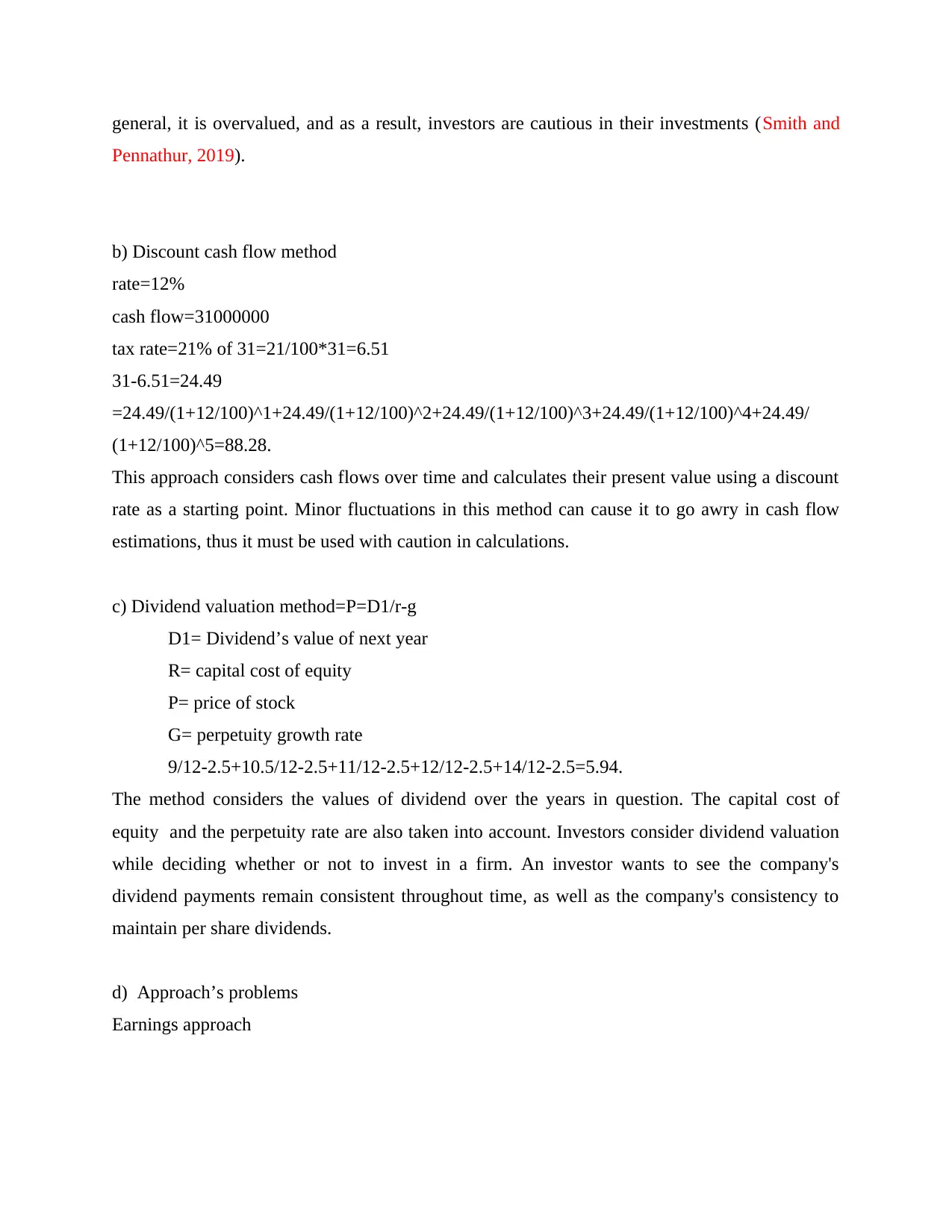

a) Price earnings ratio

= share price/earnings per share=4.15/29=0.14

This is commonly used for determining whether a company's stock is overvalued or undervalued.

It’s calculation is in indicated form and is a significant parameter to consider for investors. In

does not account for the

future costs in projected

investments. The projected

cash flows generation as a

result of capital infusion

inside the proposal of

investment are used in this

method (Eagan and et.al.,

2017).

Furthermore, using rate of

internal return overlooks the

project's reinvestment rates,

which is a huge

disadvantage. This is due to

the fact that IRR can be

extremely high or extremely

low at any given time. As a

result, the corporation is

unable to determine whether

or not the idea is viable for

investment.

Question 3

a) Price earnings ratio

= share price/earnings per share=4.15/29=0.14

This is commonly used for determining whether a company's stock is overvalued or undervalued.

It’s calculation is in indicated form and is a significant parameter to consider for investors. In

general, it is overvalued, and as a result, investors are cautious in their investments (Smith and

Pennathur, 2019).

b) Discount cash flow method

rate=12%

cash flow=31000000

tax rate=21% of 31=21/100*31=6.51

31-6.51=24.49

=24.49/(1+12/100)^1+24.49/(1+12/100)^2+24.49/(1+12/100)^3+24.49/(1+12/100)^4+24.49/

(1+12/100)^5=88.28.

This approach considers cash flows over time and calculates their present value using a discount

rate as a starting point. Minor fluctuations in this method can cause it to go awry in cash flow

estimations, thus it must be used with caution in calculations.

c) Dividend valuation method=P=D1/r-g

D1= Dividend’s value of next year

R= capital cost of equity

P= price of stock

G= perpetuity growth rate

9/12-2.5+10.5/12-2.5+11/12-2.5+12/12-2.5+14/12-2.5=5.94.

The method considers the values of dividend over the years in question. The capital cost of

equity and the perpetuity rate are also taken into account. Investors consider dividend valuation

while deciding whether or not to invest in a firm. An investor wants to see the company's

dividend payments remain consistent throughout time, as well as the company's consistency to

maintain per share dividends.

d) Approach’s problems

Earnings approach

Pennathur, 2019).

b) Discount cash flow method

rate=12%

cash flow=31000000

tax rate=21% of 31=21/100*31=6.51

31-6.51=24.49

=24.49/(1+12/100)^1+24.49/(1+12/100)^2+24.49/(1+12/100)^3+24.49/(1+12/100)^4+24.49/

(1+12/100)^5=88.28.

This approach considers cash flows over time and calculates their present value using a discount

rate as a starting point. Minor fluctuations in this method can cause it to go awry in cash flow

estimations, thus it must be used with caution in calculations.

c) Dividend valuation method=P=D1/r-g

D1= Dividend’s value of next year

R= capital cost of equity

P= price of stock

G= perpetuity growth rate

9/12-2.5+10.5/12-2.5+11/12-2.5+12/12-2.5+14/12-2.5=5.94.

The method considers the values of dividend over the years in question. The capital cost of

equity and the perpetuity rate are also taken into account. Investors consider dividend valuation

while deciding whether or not to invest in a firm. An investor wants to see the company's

dividend payments remain consistent throughout time, as well as the company's consistency to

maintain per share dividends.

d) Approach’s problems

Earnings approach

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.