Financial Management Report: Investment Appraisal and Valuation

VerifiedAdded on 2022/12/14

|16

|4153

|296

Report

AI Summary

This report delves into financial management, exploring various investment appraisal techniques and company valuation methods. It begins with a detailed calculation and analysis of investment appraisal techniques, including payback period, accounting rate of return, net present value, and internal rate of return, providing formulas and calculations. The report then critically evaluates the impact of a director's proposal on the company, considering potential benefits and challenges. Furthermore, it examines the advantages and disadvantages of each investment appraisal technique. The report also covers company valuation using price-earnings ratio, discounted cash flow, and dividend valuation methods, along with a discussion of the problems associated with valuation methods and recommendations. The conclusion summarizes the key findings and insights from the analysis.

APC 308 Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 2........................................................................................................................................3

(a) Investment appraisal technique..............................................................................................3

(b) Critical evaluation of the effect of Directors proposal on the company................................6

(c) Advantage and disadvantage of investment appraisal technique...........................................7

Question 3........................................................................................................................................9

(a) Valuation of company using Price/earnings ratio..................................................................9

(b) Valuation of company using Discounted cash flow method................................................10

(c) Valuation of company using dividend valuation method.....................................................10

(d) Problems with valuation method and recommended method..............................................11

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 2........................................................................................................................................3

(a) Investment appraisal technique..............................................................................................3

(b) Critical evaluation of the effect of Directors proposal on the company................................6

(c) Advantage and disadvantage of investment appraisal technique...........................................7

Question 3........................................................................................................................................9

(a) Valuation of company using Price/earnings ratio..................................................................9

(b) Valuation of company using Discounted cash flow method................................................10

(c) Valuation of company using dividend valuation method.....................................................10

(d) Problems with valuation method and recommended method..............................................11

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION

Financial management is the most crucial for the company and need proper attention of the

line managers because it affects the overall operational and financial performance of the

company (Sugeng and Suryani, 2018). The report will address the different investment appraisal

technique advantage and disadvantage after calculation of investment proposal.

MAIN BODY

Question 2

(a) Investment appraisal technique

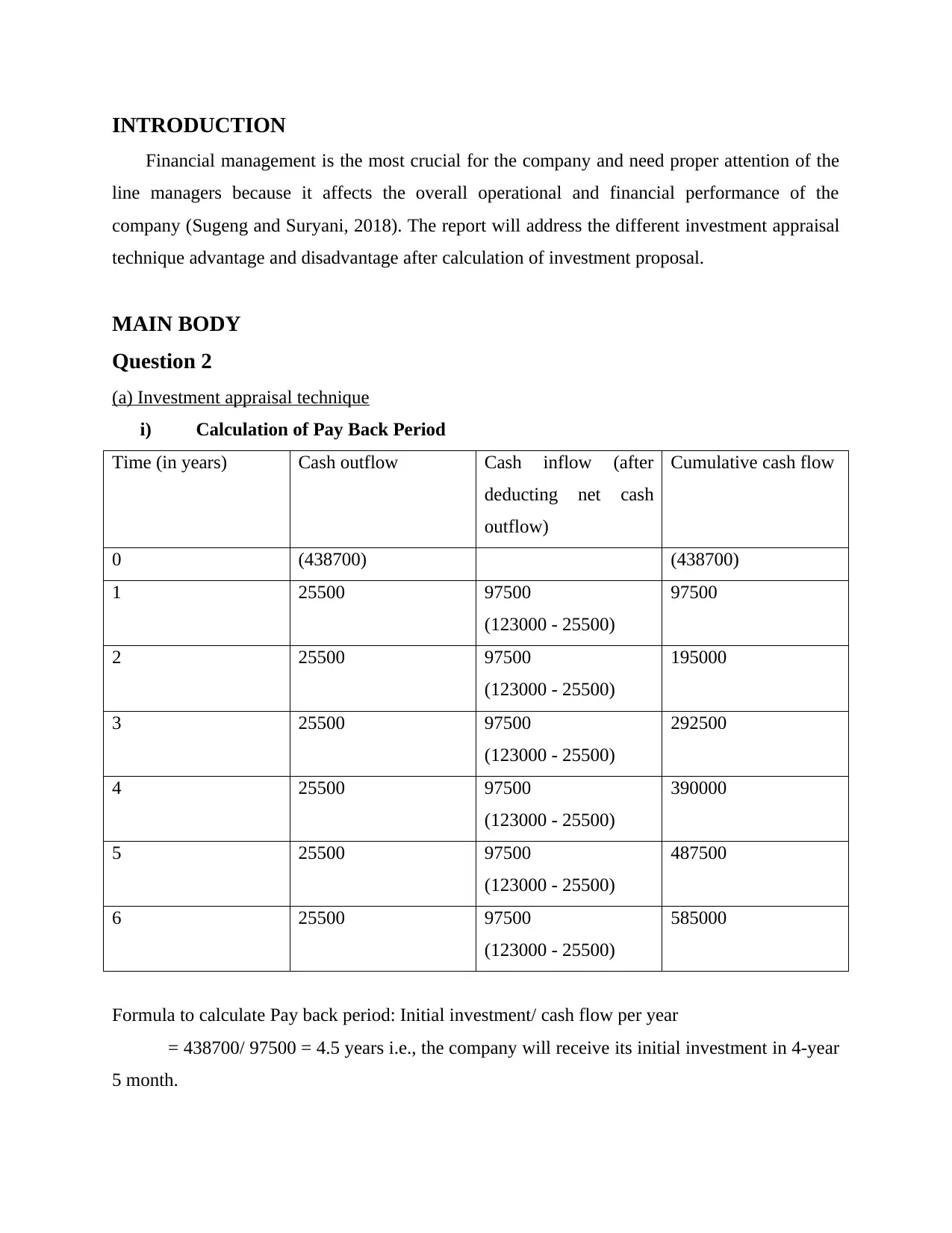

i) Calculation of Pay Back Period

Time (in years) Cash outflow Cash inflow (after

deducting net cash

outflow)

Cumulative cash flow

0 (438700) (438700)

1 25500 97500

(123000 - 25500)

97500

2 25500 97500

(123000 - 25500)

195000

3 25500 97500

(123000 - 25500)

292500

4 25500 97500

(123000 - 25500)

390000

5 25500 97500

(123000 - 25500)

487500

6 25500 97500

(123000 - 25500)

585000

Formula to calculate Pay back period: Initial investment/ cash flow per year

= 438700/ 97500 = 4.5 years i.e., the company will receive its initial investment in 4-year

5 month.

Financial management is the most crucial for the company and need proper attention of the

line managers because it affects the overall operational and financial performance of the

company (Sugeng and Suryani, 2018). The report will address the different investment appraisal

technique advantage and disadvantage after calculation of investment proposal.

MAIN BODY

Question 2

(a) Investment appraisal technique

i) Calculation of Pay Back Period

Time (in years) Cash outflow Cash inflow (after

deducting net cash

outflow)

Cumulative cash flow

0 (438700) (438700)

1 25500 97500

(123000 - 25500)

97500

2 25500 97500

(123000 - 25500)

195000

3 25500 97500

(123000 - 25500)

292500

4 25500 97500

(123000 - 25500)

390000

5 25500 97500

(123000 - 25500)

487500

6 25500 97500

(123000 - 25500)

585000

Formula to calculate Pay back period: Initial investment/ cash flow per year

= 438700/ 97500 = 4.5 years i.e., the company will receive its initial investment in 4-year

5 month.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

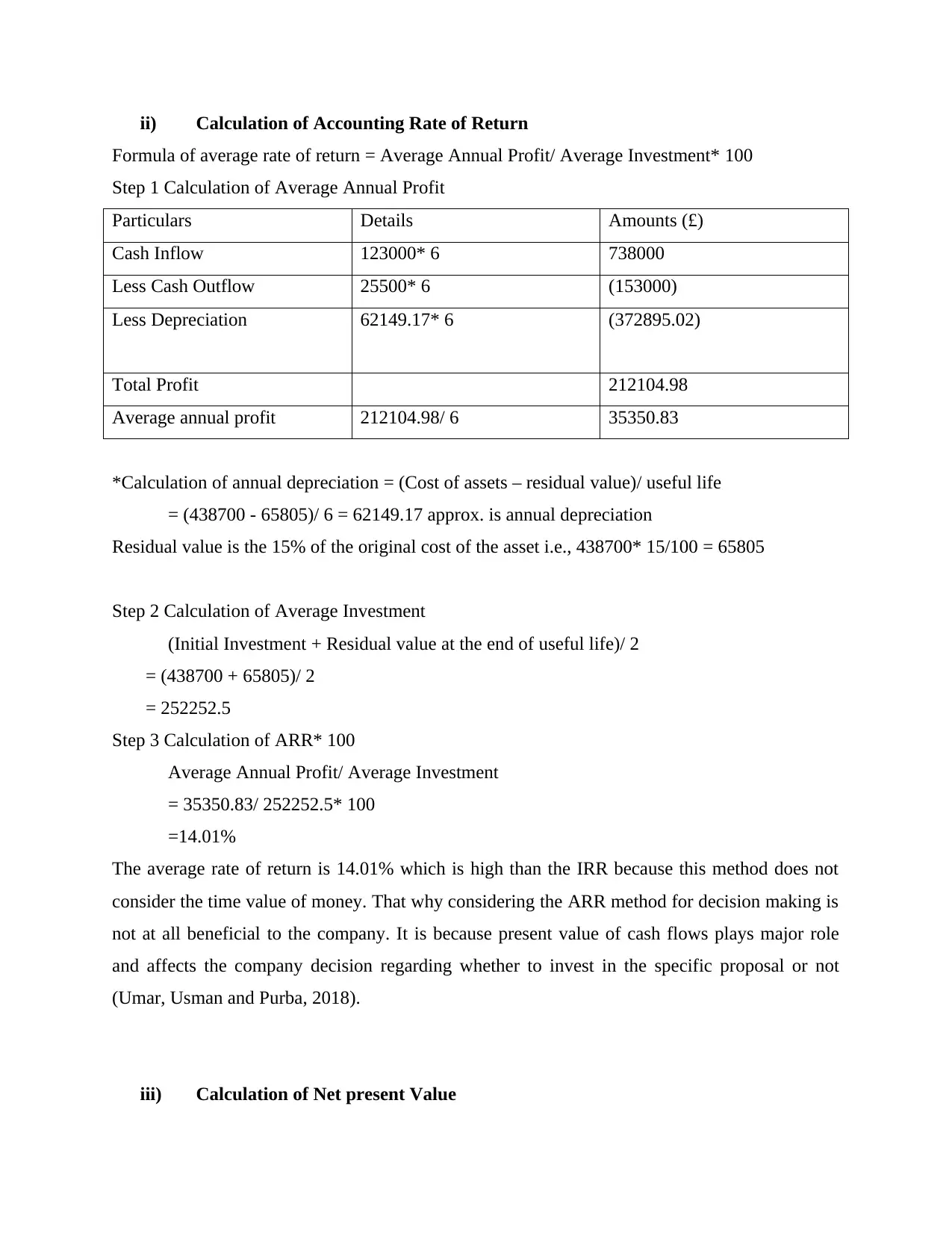

ii) Calculation of Accounting Rate of Return

Formula of average rate of return = Average Annual Profit/ Average Investment* 100

Step 1 Calculation of Average Annual Profit

Particulars Details Amounts (£)

Cash Inflow 123000* 6 738000

Less Cash Outflow 25500* 6 (153000)

Less Depreciation 62149.17* 6 (372895.02)

Total Profit 212104.98

Average annual profit 212104.98/ 6 35350.83

*Calculation of annual depreciation = (Cost of assets – residual value)/ useful life

= (438700 - 65805)/ 6 = 62149.17 approx. is annual depreciation

Residual value is the 15% of the original cost of the asset i.e., 438700* 15/100 = 65805

Step 2 Calculation of Average Investment

(Initial Investment + Residual value at the end of useful life)/ 2

= (438700 + 65805)/ 2

= 252252.5

Step 3 Calculation of ARR* 100

Average Annual Profit/ Average Investment

= 35350.83/ 252252.5* 100

=14.01%

The average rate of return is 14.01% which is high than the IRR because this method does not

consider the time value of money. That why considering the ARR method for decision making is

not at all beneficial to the company. It is because present value of cash flows plays major role

and affects the company decision regarding whether to invest in the specific proposal or not

(Umar, Usman and Purba, 2018).

iii) Calculation of Net present Value

Formula of average rate of return = Average Annual Profit/ Average Investment* 100

Step 1 Calculation of Average Annual Profit

Particulars Details Amounts (£)

Cash Inflow 123000* 6 738000

Less Cash Outflow 25500* 6 (153000)

Less Depreciation 62149.17* 6 (372895.02)

Total Profit 212104.98

Average annual profit 212104.98/ 6 35350.83

*Calculation of annual depreciation = (Cost of assets – residual value)/ useful life

= (438700 - 65805)/ 6 = 62149.17 approx. is annual depreciation

Residual value is the 15% of the original cost of the asset i.e., 438700* 15/100 = 65805

Step 2 Calculation of Average Investment

(Initial Investment + Residual value at the end of useful life)/ 2

= (438700 + 65805)/ 2

= 252252.5

Step 3 Calculation of ARR* 100

Average Annual Profit/ Average Investment

= 35350.83/ 252252.5* 100

=14.01%

The average rate of return is 14.01% which is high than the IRR because this method does not

consider the time value of money. That why considering the ARR method for decision making is

not at all beneficial to the company. It is because present value of cash flows plays major role

and affects the company decision regarding whether to invest in the specific proposal or not

(Umar, Usman and Purba, 2018).

iii) Calculation of Net present Value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

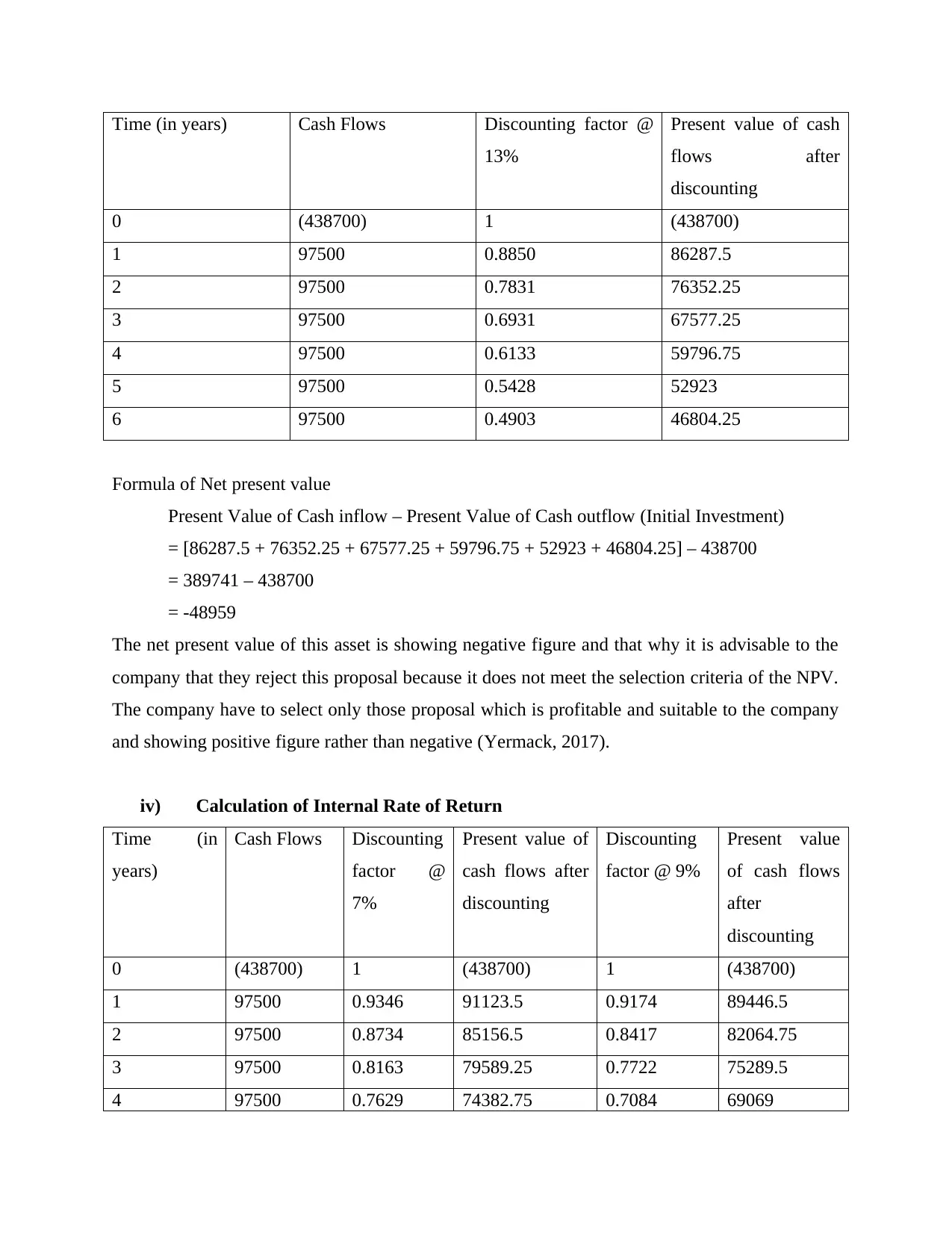

Time (in years) Cash Flows Discounting factor @

13%

Present value of cash

flows after

discounting

0 (438700) 1 (438700)

1 97500 0.8850 86287.5

2 97500 0.7831 76352.25

3 97500 0.6931 67577.25

4 97500 0.6133 59796.75

5 97500 0.5428 52923

6 97500 0.4903 46804.25

Formula of Net present value

Present Value of Cash inflow – Present Value of Cash outflow (Initial Investment)

= [86287.5 + 76352.25 + 67577.25 + 59796.75 + 52923 + 46804.25] – 438700

= 389741 – 438700

= -48959

The net present value of this asset is showing negative figure and that why it is advisable to the

company that they reject this proposal because it does not meet the selection criteria of the NPV.

The company have to select only those proposal which is profitable and suitable to the company

and showing positive figure rather than negative (Yermack, 2017).

iv) Calculation of Internal Rate of Return

Time (in

years)

Cash Flows Discounting

factor @

7%

Present value of

cash flows after

discounting

Discounting

factor @ 9%

Present value

of cash flows

after

discounting

0 (438700) 1 (438700) 1 (438700)

1 97500 0.9346 91123.5 0.9174 89446.5

2 97500 0.8734 85156.5 0.8417 82064.75

3 97500 0.8163 79589.25 0.7722 75289.5

4 97500 0.7629 74382.75 0.7084 69069

13%

Present value of cash

flows after

discounting

0 (438700) 1 (438700)

1 97500 0.8850 86287.5

2 97500 0.7831 76352.25

3 97500 0.6931 67577.25

4 97500 0.6133 59796.75

5 97500 0.5428 52923

6 97500 0.4903 46804.25

Formula of Net present value

Present Value of Cash inflow – Present Value of Cash outflow (Initial Investment)

= [86287.5 + 76352.25 + 67577.25 + 59796.75 + 52923 + 46804.25] – 438700

= 389741 – 438700

= -48959

The net present value of this asset is showing negative figure and that why it is advisable to the

company that they reject this proposal because it does not meet the selection criteria of the NPV.

The company have to select only those proposal which is profitable and suitable to the company

and showing positive figure rather than negative (Yermack, 2017).

iv) Calculation of Internal Rate of Return

Time (in

years)

Cash Flows Discounting

factor @

7%

Present value of

cash flows after

discounting

Discounting

factor @ 9%

Present value

of cash flows

after

discounting

0 (438700) 1 (438700) 1 (438700)

1 97500 0.9346 91123.5 0.9174 89446.5

2 97500 0.8734 85156.5 0.8417 82064.75

3 97500 0.8163 79589.25 0.7722 75289.5

4 97500 0.7629 74382.75 0.7084 69069

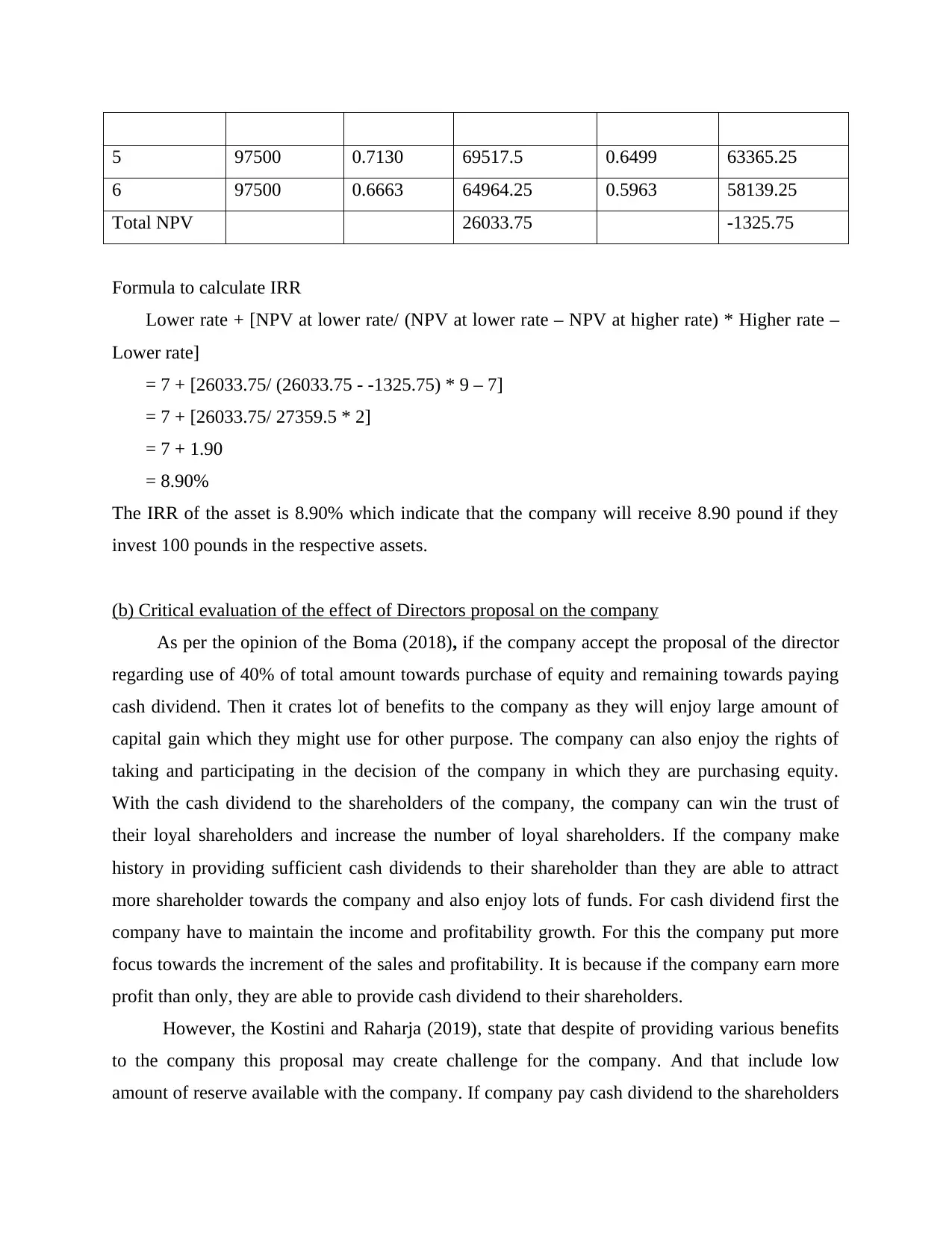

5 97500 0.7130 69517.5 0.6499 63365.25

6 97500 0.6663 64964.25 0.5963 58139.25

Total NPV 26033.75 -1325.75

Formula to calculate IRR

Lower rate + [NPV at lower rate/ (NPV at lower rate – NPV at higher rate) * Higher rate –

Lower rate]

= 7 + [26033.75/ (26033.75 - -1325.75) * 9 – 7]

= 7 + [26033.75/ 27359.5 * 2]

= 7 + 1.90

= 8.90%

The IRR of the asset is 8.90% which indicate that the company will receive 8.90 pound if they

invest 100 pounds in the respective assets.

(b) Critical evaluation of the effect of Directors proposal on the company

As per the opinion of the Boma (2018), if the company accept the proposal of the director

regarding use of 40% of total amount towards purchase of equity and remaining towards paying

cash dividend. Then it crates lot of benefits to the company as they will enjoy large amount of

capital gain which they might use for other purpose. The company can also enjoy the rights of

taking and participating in the decision of the company in which they are purchasing equity.

With the cash dividend to the shareholders of the company, the company can win the trust of

their loyal shareholders and increase the number of loyal shareholders. If the company make

history in providing sufficient cash dividends to their shareholder than they are able to attract

more shareholder towards the company and also enjoy lots of funds. For cash dividend first the

company have to maintain the income and profitability growth. For this the company put more

focus towards the increment of the sales and profitability. It is because if the company earn more

profit than only, they are able to provide cash dividend to their shareholders.

However, the Kostini and Raharja (2019), state that despite of providing various benefits

to the company this proposal may create challenge for the company. And that include low

amount of reserve available with the company. If company pay cash dividend to the shareholders

6 97500 0.6663 64964.25 0.5963 58139.25

Total NPV 26033.75 -1325.75

Formula to calculate IRR

Lower rate + [NPV at lower rate/ (NPV at lower rate – NPV at higher rate) * Higher rate –

Lower rate]

= 7 + [26033.75/ (26033.75 - -1325.75) * 9 – 7]

= 7 + [26033.75/ 27359.5 * 2]

= 7 + 1.90

= 8.90%

The IRR of the asset is 8.90% which indicate that the company will receive 8.90 pound if they

invest 100 pounds in the respective assets.

(b) Critical evaluation of the effect of Directors proposal on the company

As per the opinion of the Boma (2018), if the company accept the proposal of the director

regarding use of 40% of total amount towards purchase of equity and remaining towards paying

cash dividend. Then it crates lot of benefits to the company as they will enjoy large amount of

capital gain which they might use for other purpose. The company can also enjoy the rights of

taking and participating in the decision of the company in which they are purchasing equity.

With the cash dividend to the shareholders of the company, the company can win the trust of

their loyal shareholders and increase the number of loyal shareholders. If the company make

history in providing sufficient cash dividends to their shareholder than they are able to attract

more shareholder towards the company and also enjoy lots of funds. For cash dividend first the

company have to maintain the income and profitability growth. For this the company put more

focus towards the increment of the sales and profitability. It is because if the company earn more

profit than only, they are able to provide cash dividend to their shareholders.

However, the Kostini and Raharja (2019), state that despite of providing various benefits

to the company this proposal may create challenge for the company. And that include low

amount of reserve available with the company. If company pay cash dividend to the shareholders

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that at the time of need it might possible that the company do not have sufficient cash with

themselves. Because of buying equity in the other company is quite risky for them as there is no

collateral security is attaching with this when compared to debts. Because of fluctuation in the

market price, it also become difficult for the company to grab profits from the market.

(c) Advantage and disadvantage of investment appraisal technique

This is a financial ratio used to analyse and identify the percentage of return the company will

receive after investing fund in a specific assets or investment plan. The advantage and

disadvantage of the following investment appraisal are as follow:

Advantage of Payback period:

As Takahashi (2020), stated that the one of the advantages of the payback period is that

it is simple to use and understand that in what time the company will receive its initial

cash outlay because it reflects result in time period rather percentage or ratio.

This also helps the manager of the company in taking quickly decision because this

technique involve limited resources to consider.

It is preferable to the company if they want to know the liquidity of the business as it

states that the project with shorter time period is best for the company.

Whenever there is uncertainty regarding the impact of rapid technological change, the

company can reduce the chances of obsolescence loss by selecting PB period technique.

Disadvantage of Payback period:

However, the Voinea (2017), stated that the most important factor that largely affects the

decision of the investment is time value of money and this is the disadvantage of PB

period that they do not consider time value of money.

It does not consider all cash flows in the decision-making process because it only covers

the cash flows until the company receive its initial investment.

Because of that the company may lose that projects that provide higher returns after the

payback periods. That why it is not recommendable to the company that want to invest

huge amount of fund.

This method is so simple that it does not able to show any realistic figure and also the

projects reflect irregular cash flows which became confusing for decision-making.

themselves. Because of buying equity in the other company is quite risky for them as there is no

collateral security is attaching with this when compared to debts. Because of fluctuation in the

market price, it also become difficult for the company to grab profits from the market.

(c) Advantage and disadvantage of investment appraisal technique

This is a financial ratio used to analyse and identify the percentage of return the company will

receive after investing fund in a specific assets or investment plan. The advantage and

disadvantage of the following investment appraisal are as follow:

Advantage of Payback period:

As Takahashi (2020), stated that the one of the advantages of the payback period is that

it is simple to use and understand that in what time the company will receive its initial

cash outlay because it reflects result in time period rather percentage or ratio.

This also helps the manager of the company in taking quickly decision because this

technique involve limited resources to consider.

It is preferable to the company if they want to know the liquidity of the business as it

states that the project with shorter time period is best for the company.

Whenever there is uncertainty regarding the impact of rapid technological change, the

company can reduce the chances of obsolescence loss by selecting PB period technique.

Disadvantage of Payback period:

However, the Voinea (2017), stated that the most important factor that largely affects the

decision of the investment is time value of money and this is the disadvantage of PB

period that they do not consider time value of money.

It does not consider all cash flows in the decision-making process because it only covers

the cash flows until the company receive its initial investment.

Because of that the company may lose that projects that provide higher returns after the

payback periods. That why it is not recommendable to the company that want to invest

huge amount of fund.

This method is so simple that it does not able to show any realistic figure and also the

projects reflect irregular cash flows which became confusing for decision-making.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage of Average rate of return:

As per the opinion of the Schuster and et.al. (2020), as like PB period, this technique of

investment appraisal is easy and simple to calculate and understand. It is because it

considers the total profit from investment after deducting depreciation as depreciation is

a non-cash item.

It is important for the company to consider this because it recognizes the fact of net

earnings i.e., earnings after tax and depreciation.

With this the company can clearly view the real picture of profit of all investments plans

as well as it also satisfies the needs and interest of the owners that wants higher rate of

returns.

This is the only method that consider accounting concept for calculating rate of return.

Disadvantage of Average rate of return:

However, the Balliauw and et.al. (2019), in this contrast state that the primary and most

crucial weakness of this method is that it ignores the time factor in selecting the best

alternatives out of the all alternatives.

In case, if company want to invest in a particular project than they cannot consider this

method because for ARR the project with 10% return in 10 year is better than project

with 8% profit in 5 years.

This do not consider cash inflows which are way better than the profit factors and useful

and beneficial for decision making purpose.

Advantage of Net present Value:

As per the views of the Wang and et.al. (2018), the most important and significant

advantage of using this technique for decision purpose is that it consider the time value of

money to calculate higher returns.

In this, the future cash inflows are first converted into the present cash inflows by

considering the discounting factors. And if the difference between the present value of

cash inflow and initial investment is positive than only the company are allowable to

invest in that specific project.

It not only helps the company in evaluating the projects that are of same size but also

help in identifying the whether the particular project is profitable and suitable to the

company or not.

As per the opinion of the Schuster and et.al. (2020), as like PB period, this technique of

investment appraisal is easy and simple to calculate and understand. It is because it

considers the total profit from investment after deducting depreciation as depreciation is

a non-cash item.

It is important for the company to consider this because it recognizes the fact of net

earnings i.e., earnings after tax and depreciation.

With this the company can clearly view the real picture of profit of all investments plans

as well as it also satisfies the needs and interest of the owners that wants higher rate of

returns.

This is the only method that consider accounting concept for calculating rate of return.

Disadvantage of Average rate of return:

However, the Balliauw and et.al. (2019), in this contrast state that the primary and most

crucial weakness of this method is that it ignores the time factor in selecting the best

alternatives out of the all alternatives.

In case, if company want to invest in a particular project than they cannot consider this

method because for ARR the project with 10% return in 10 year is better than project

with 8% profit in 5 years.

This do not consider cash inflows which are way better than the profit factors and useful

and beneficial for decision making purpose.

Advantage of Net present Value:

As per the views of the Wang and et.al. (2018), the most important and significant

advantage of using this technique for decision purpose is that it consider the time value of

money to calculate higher returns.

In this, the future cash inflows are first converted into the present cash inflows by

considering the discounting factors. And if the difference between the present value of

cash inflow and initial investment is positive than only the company are allowable to

invest in that specific project.

It not only helps the company in evaluating the projects that are of same size but also

help in identifying the whether the particular project is profitable and suitable to the

company or not.

Disadvantage of Net present value:

However, the Huang (2020), states that the entire calculation of the rate of return is

depend upon the discounted factors and there is not at all any set guidelines is available

for calculation of required rate of return.

As it offers the facility of comparing the projects that are of same size but in case of the

investment plans of different size net present value method is of no use.

It does not consider any hidden and sunk cost for the purpose of calculating the rate of

return of the projects.

Advantage of Internal rate of return:

As Jitmaneeroj (2017), states that IRR provides the quick snapshot of which projects is

beneficial for them because it is simple, easily understandable and also consider time

factor (discounting factor).

The IRR method does not provide the hurdle rate to the company because it is subjective

and provide rough estimate of the required rate of return of projects.

It equally weights each and every cash flow by using the time value of money.

Disadvantage of Internal rate of return:

However, the Yang (2020), in the contradiction defines that this technique of investment

appraisal does not consider the future cost that the company might bear in future.

And the impact of which is that the company bear huge losses because of not considering

the impact of such uncertain cost on the profitability of the investment plan.

This method while calculating the rate of return make an assumption that if the company

reinvest the same cash flows in future will enjoy the same benefits that they are enjoying

now.

Question 3

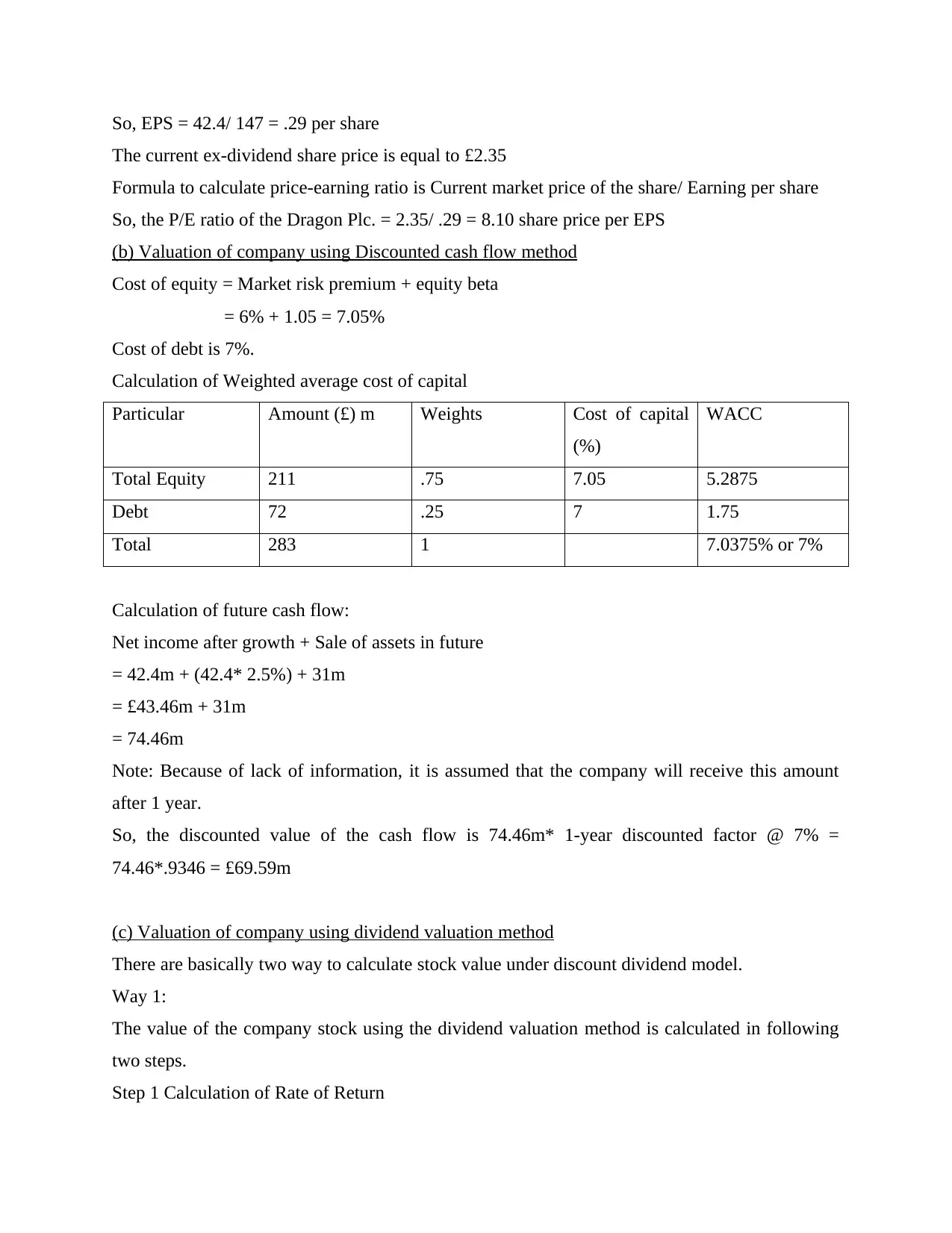

(a) Valuation of company using Price/earnings ratio

Price-earning ratio is the valuation methods with the help of which the research can analyse the

value of the company according its ability to pay its shareholders from the earnings of the

company.

Here in the give case, the total number of ordinary shares is £147m and earning’s available for

equity shareholders (Distributable earnings) is £42.4m

Formula of Earning Per Share = Distributable earnings/ total number of ordinary shares

However, the Huang (2020), states that the entire calculation of the rate of return is

depend upon the discounted factors and there is not at all any set guidelines is available

for calculation of required rate of return.

As it offers the facility of comparing the projects that are of same size but in case of the

investment plans of different size net present value method is of no use.

It does not consider any hidden and sunk cost for the purpose of calculating the rate of

return of the projects.

Advantage of Internal rate of return:

As Jitmaneeroj (2017), states that IRR provides the quick snapshot of which projects is

beneficial for them because it is simple, easily understandable and also consider time

factor (discounting factor).

The IRR method does not provide the hurdle rate to the company because it is subjective

and provide rough estimate of the required rate of return of projects.

It equally weights each and every cash flow by using the time value of money.

Disadvantage of Internal rate of return:

However, the Yang (2020), in the contradiction defines that this technique of investment

appraisal does not consider the future cost that the company might bear in future.

And the impact of which is that the company bear huge losses because of not considering

the impact of such uncertain cost on the profitability of the investment plan.

This method while calculating the rate of return make an assumption that if the company

reinvest the same cash flows in future will enjoy the same benefits that they are enjoying

now.

Question 3

(a) Valuation of company using Price/earnings ratio

Price-earning ratio is the valuation methods with the help of which the research can analyse the

value of the company according its ability to pay its shareholders from the earnings of the

company.

Here in the give case, the total number of ordinary shares is £147m and earning’s available for

equity shareholders (Distributable earnings) is £42.4m

Formula of Earning Per Share = Distributable earnings/ total number of ordinary shares

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

So, EPS = 42.4/ 147 = .29 per share

The current ex-dividend share price is equal to £2.35

Formula to calculate price-earning ratio is Current market price of the share/ Earning per share

So, the P/E ratio of the Dragon Plc. = 2.35/ .29 = 8.10 share price per EPS

(b) Valuation of company using Discounted cash flow method

Cost of equity = Market risk premium + equity beta

= 6% + 1.05 = 7.05%

Cost of debt is 7%.

Calculation of Weighted average cost of capital

Particular Amount (£) m Weights Cost of capital

(%)

WACC

Total Equity 211 .75 7.05 5.2875

Debt 72 .25 7 1.75

Total 283 1 7.0375% or 7%

Calculation of future cash flow:

Net income after growth + Sale of assets in future

= 42.4m + (42.4* 2.5%) + 31m

= £43.46m + 31m

= 74.46m

Note: Because of lack of information, it is assumed that the company will receive this amount

after 1 year.

So, the discounted value of the cash flow is 74.46m* 1-year discounted factor @ 7% =

74.46*.9346 = £69.59m

(c) Valuation of company using dividend valuation method

There are basically two way to calculate stock value under discount dividend model.

Way 1:

The value of the company stock using the dividend valuation method is calculated in following

two steps.

Step 1 Calculation of Rate of Return

The current ex-dividend share price is equal to £2.35

Formula to calculate price-earning ratio is Current market price of the share/ Earning per share

So, the P/E ratio of the Dragon Plc. = 2.35/ .29 = 8.10 share price per EPS

(b) Valuation of company using Discounted cash flow method

Cost of equity = Market risk premium + equity beta

= 6% + 1.05 = 7.05%

Cost of debt is 7%.

Calculation of Weighted average cost of capital

Particular Amount (£) m Weights Cost of capital

(%)

WACC

Total Equity 211 .75 7.05 5.2875

Debt 72 .25 7 1.75

Total 283 1 7.0375% or 7%

Calculation of future cash flow:

Net income after growth + Sale of assets in future

= 42.4m + (42.4* 2.5%) + 31m

= £43.46m + 31m

= 74.46m

Note: Because of lack of information, it is assumed that the company will receive this amount

after 1 year.

So, the discounted value of the cash flow is 74.46m* 1-year discounted factor @ 7% =

74.46*.9346 = £69.59m

(c) Valuation of company using dividend valuation method

There are basically two way to calculate stock value under discount dividend model.

Way 1:

The value of the company stock using the dividend valuation method is calculated in following

two steps.

Step 1 Calculation of Rate of Return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Formula = (Dividend Payment/ Stock Price) + Dividend growth rate

= (.1435/2.35) + 2.5%

= .0611 + .025

= .0861 or 8.61%

Here, in this question latest dividend payment is equal to .1435 and the current stock price is

£2.35. And the growth rate of earning is 2.5%. Because of the lack of information, it is assumed

that the company’s dividend growth rate is equal to earnings growth rate and that is 2.5%.

Step 2 Calculation of Shareholder value

Stock Value = Dividend per share/ (Required rate of return – Dividend growth rate)

= .1435/ (.0861 - .025)

= .1435/ .0611

= £2.35

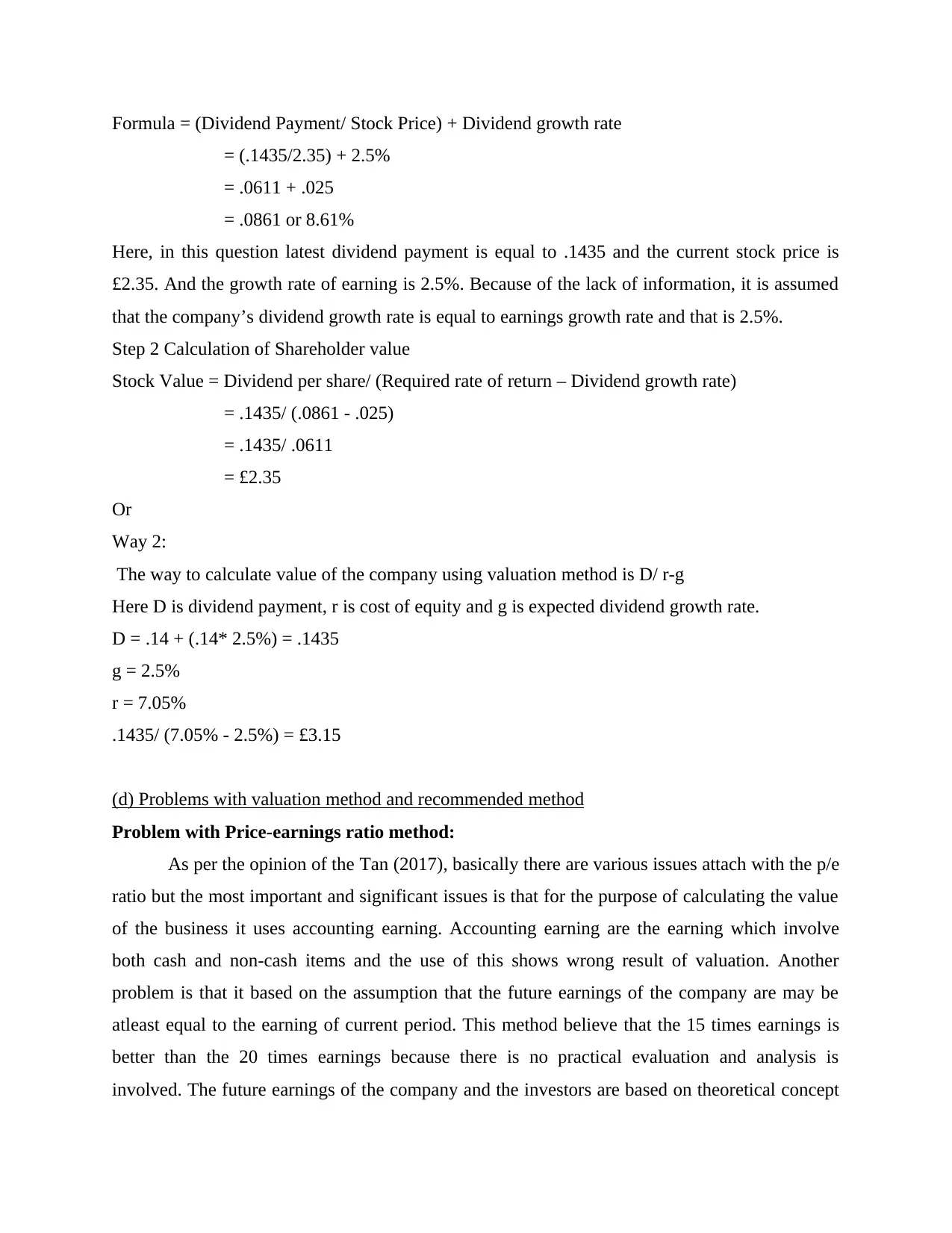

Or

Way 2:

The way to calculate value of the company using valuation method is D/ r-g

Here D is dividend payment, r is cost of equity and g is expected dividend growth rate.

D = .14 + (.14* 2.5%) = .1435

g = 2.5%

r = 7.05%

.1435/ (7.05% - 2.5%) = £3.15

(d) Problems with valuation method and recommended method

Problem with Price-earnings ratio method:

As per the opinion of the Tan (2017), basically there are various issues attach with the p/e

ratio but the most important and significant issues is that for the purpose of calculating the value

of the business it uses accounting earning. Accounting earning are the earning which involve

both cash and non-cash items and the use of this shows wrong result of valuation. Another

problem is that it based on the assumption that the future earnings of the company are may be

atleast equal to the earning of current period. This method believe that the 15 times earnings is

better than the 20 times earnings because there is no practical evaluation and analysis is

involved. The future earnings of the company and the investors are based on theoretical concept

= (.1435/2.35) + 2.5%

= .0611 + .025

= .0861 or 8.61%

Here, in this question latest dividend payment is equal to .1435 and the current stock price is

£2.35. And the growth rate of earning is 2.5%. Because of the lack of information, it is assumed

that the company’s dividend growth rate is equal to earnings growth rate and that is 2.5%.

Step 2 Calculation of Shareholder value

Stock Value = Dividend per share/ (Required rate of return – Dividend growth rate)

= .1435/ (.0861 - .025)

= .1435/ .0611

= £2.35

Or

Way 2:

The way to calculate value of the company using valuation method is D/ r-g

Here D is dividend payment, r is cost of equity and g is expected dividend growth rate.

D = .14 + (.14* 2.5%) = .1435

g = 2.5%

r = 7.05%

.1435/ (7.05% - 2.5%) = £3.15

(d) Problems with valuation method and recommended method

Problem with Price-earnings ratio method:

As per the opinion of the Tan (2017), basically there are various issues attach with the p/e

ratio but the most important and significant issues is that for the purpose of calculating the value

of the business it uses accounting earning. Accounting earning are the earning which involve

both cash and non-cash items and the use of this shows wrong result of valuation. Another

problem is that it based on the assumption that the future earnings of the company are may be

atleast equal to the earning of current period. This method believe that the 15 times earnings is

better than the 20 times earnings because there is no practical evaluation and analysis is

involved. The future earnings of the company and the investors are based on theoretical concept

in this method. The investors can use this method for valuing the stocks of the company but only

adopting this method is not beneficial for the investors. In order to know the best and accurate

value of the company’s stocks than the investors have to use p/e method with some other

valuation method.

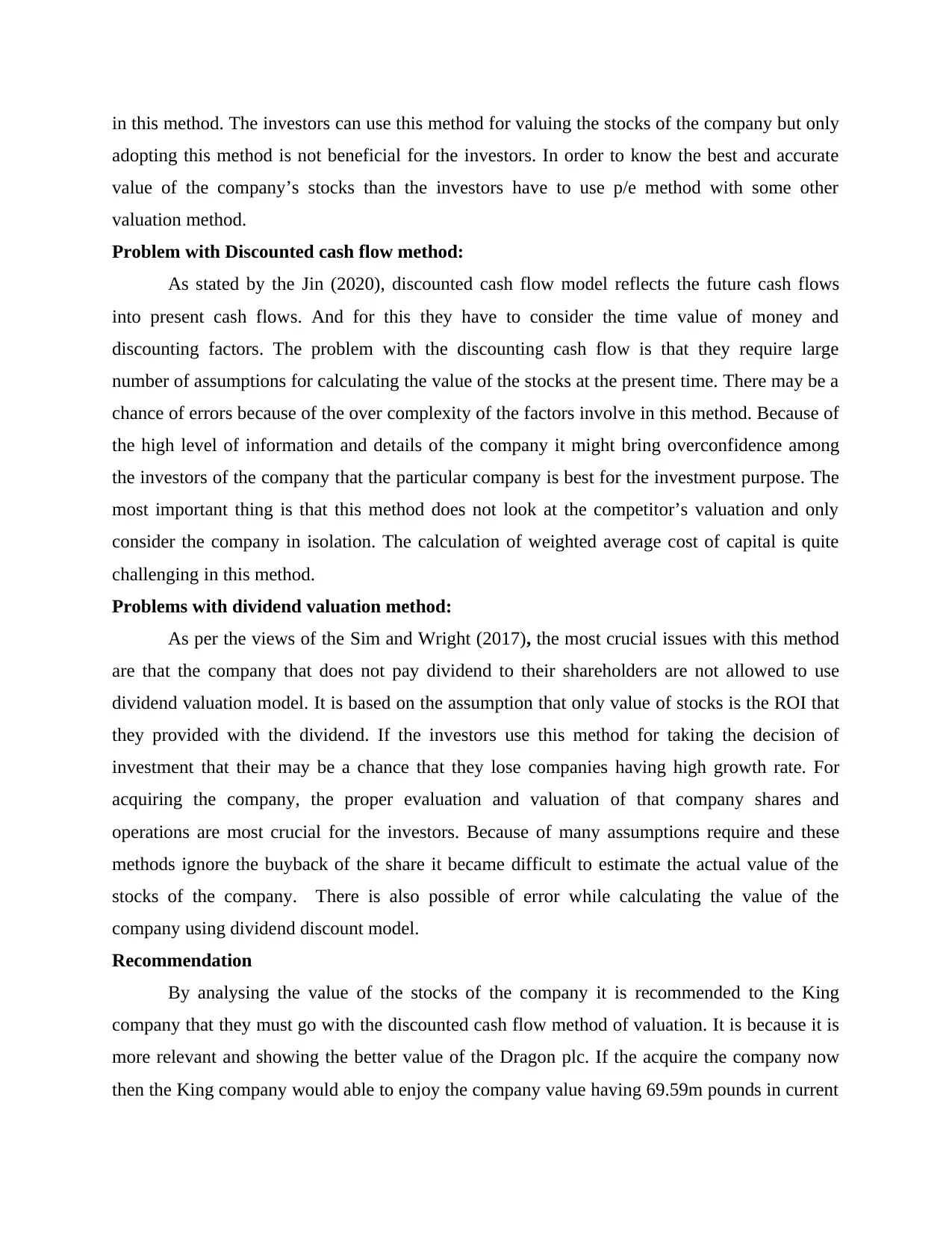

Problem with Discounted cash flow method:

As stated by the Jin (2020), discounted cash flow model reflects the future cash flows

into present cash flows. And for this they have to consider the time value of money and

discounting factors. The problem with the discounting cash flow is that they require large

number of assumptions for calculating the value of the stocks at the present time. There may be a

chance of errors because of the over complexity of the factors involve in this method. Because of

the high level of information and details of the company it might bring overconfidence among

the investors of the company that the particular company is best for the investment purpose. The

most important thing is that this method does not look at the competitor’s valuation and only

consider the company in isolation. The calculation of weighted average cost of capital is quite

challenging in this method.

Problems with dividend valuation method:

As per the views of the Sim and Wright (2017), the most crucial issues with this method

are that the company that does not pay dividend to their shareholders are not allowed to use

dividend valuation model. It is based on the assumption that only value of stocks is the ROI that

they provided with the dividend. If the investors use this method for taking the decision of

investment that their may be a chance that they lose companies having high growth rate. For

acquiring the company, the proper evaluation and valuation of that company shares and

operations are most crucial for the investors. Because of many assumptions require and these

methods ignore the buyback of the share it became difficult to estimate the actual value of the

stocks of the company. There is also possible of error while calculating the value of the

company using dividend discount model.

Recommendation

By analysing the value of the stocks of the company it is recommended to the King

company that they must go with the discounted cash flow method of valuation. It is because it is

more relevant and showing the better value of the Dragon plc. If the acquire the company now

then the King company would able to enjoy the company value having 69.59m pounds in current

adopting this method is not beneficial for the investors. In order to know the best and accurate

value of the company’s stocks than the investors have to use p/e method with some other

valuation method.

Problem with Discounted cash flow method:

As stated by the Jin (2020), discounted cash flow model reflects the future cash flows

into present cash flows. And for this they have to consider the time value of money and

discounting factors. The problem with the discounting cash flow is that they require large

number of assumptions for calculating the value of the stocks at the present time. There may be a

chance of errors because of the over complexity of the factors involve in this method. Because of

the high level of information and details of the company it might bring overconfidence among

the investors of the company that the particular company is best for the investment purpose. The

most important thing is that this method does not look at the competitor’s valuation and only

consider the company in isolation. The calculation of weighted average cost of capital is quite

challenging in this method.

Problems with dividend valuation method:

As per the views of the Sim and Wright (2017), the most crucial issues with this method

are that the company that does not pay dividend to their shareholders are not allowed to use

dividend valuation model. It is based on the assumption that only value of stocks is the ROI that

they provided with the dividend. If the investors use this method for taking the decision of

investment that their may be a chance that they lose companies having high growth rate. For

acquiring the company, the proper evaluation and valuation of that company shares and

operations are most crucial for the investors. Because of many assumptions require and these

methods ignore the buyback of the share it became difficult to estimate the actual value of the

stocks of the company. There is also possible of error while calculating the value of the

company using dividend discount model.

Recommendation

By analysing the value of the stocks of the company it is recommended to the King

company that they must go with the discounted cash flow method of valuation. It is because it is

more relevant and showing the better value of the Dragon plc. If the acquire the company now

then the King company would able to enjoy the company value having 69.59m pounds in current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.