Corporate Finance: Investment Decision Analysis for Blue Mountain Ltd

VerifiedAdded on 2023/01/09

|8

|2294

|21

Report

AI Summary

This report provides a comprehensive analysis of an investment decision project evaluation for Blue Mountain Ltd, focusing on corporate finance principles. Part A of the report examines the investment decision to introduce a new product, including the calculation of Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index (PI), and Payback Period. The financial analysis utilizes Excel formulas to assess the project's viability. Part B delves into dividend policy and capital structure, discussing the principle of dividend irrelevance and its implications, as well as the impact of debt acquisition and capital expenditure on a company's financial health. The report concludes by highlighting the importance of considering both investment decisions and financial policies to maximize shareholder value, referencing key financial concepts and relevant academic literature. The analysis includes a discussion on the impact of dividend policy and capital structure decisions on the company's financial health and valuation.

Investment decision -

project evaluation

project evaluation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

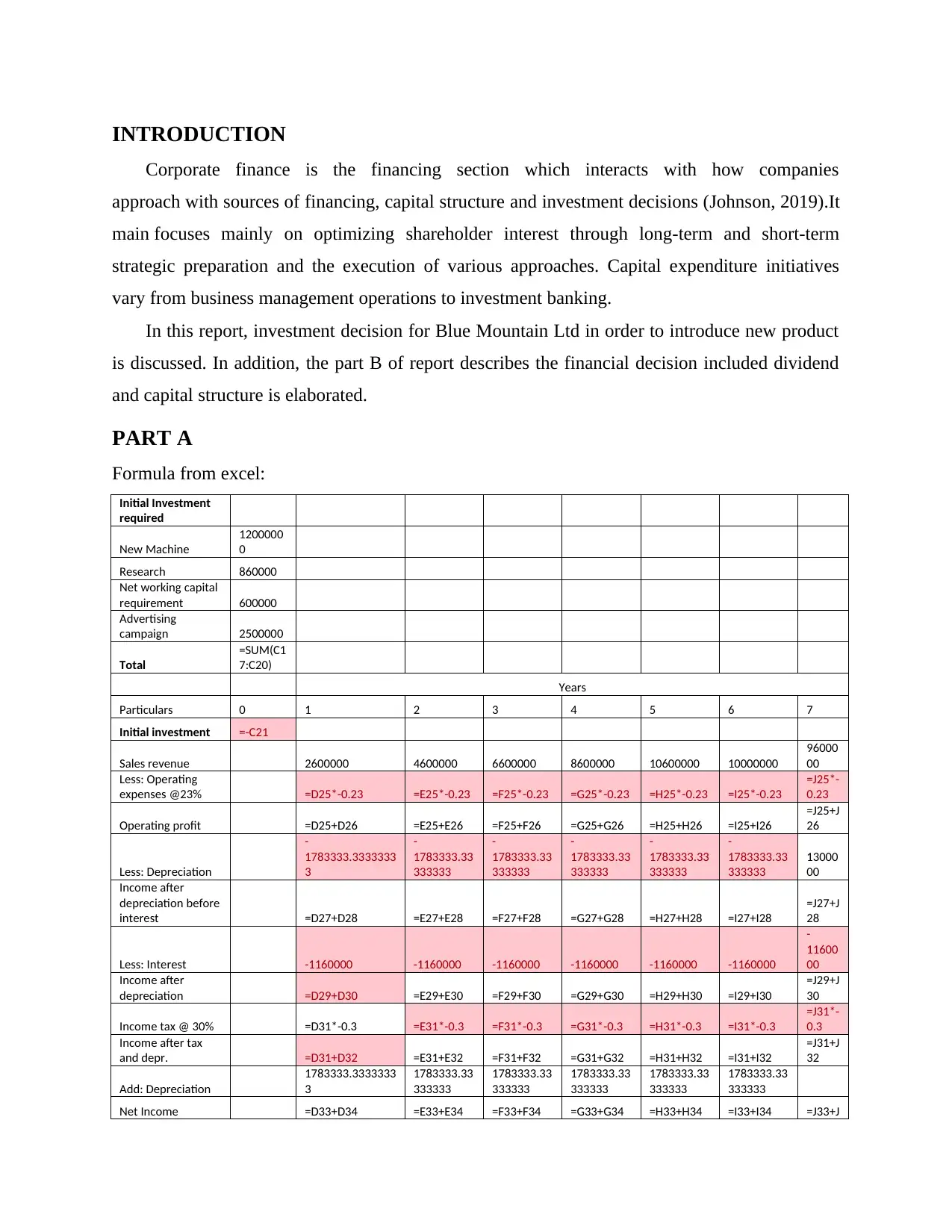

INTRODUCTION

Corporate finance is the financing section which interacts with how companies

approach with sources of financing, capital structure and investment decisions (Johnson, 2019).It

main focuses mainly on optimizing shareholder interest through long-term and short-term

strategic preparation and the execution of various approaches. Capital expenditure initiatives

vary from business management operations to investment banking.

In this report, investment decision for Blue Mountain Ltd in order to introduce new product

is discussed. In addition, the part B of report describes the financial decision included dividend

and capital structure is elaborated.

PART A

Formula from excel:

Initial Investment

required

New Machine

1200000

0

Research 860000

Net working capital

requirement 600000

Advertising

campaign 2500000

Total

=SUM(C1

7:C20)

Years

Particulars 0 1 2 3 4 5 6 7

Initial investment =-C21

Sales revenue 2600000 4600000 6600000 8600000 10600000 10000000

96000

00

Less: Operating

expenses @23% =D25*-0.23 =E25*-0.23 =F25*-0.23 =G25*-0.23 =H25*-0.23 =I25*-0.23

=J25*-

0.23

Operating profit =D25+D26 =E25+E26 =F25+F26 =G25+G26 =H25+H26 =I25+I26

=J25+J

26

Less: Depreciation

-

1783333.3333333

3

-

1783333.33

333333

-

1783333.33

333333

-

1783333.33

333333

-

1783333.33

333333

-

1783333.33

333333

13000

00

Income after

depreciation before

interest =D27+D28 =E27+E28 =F27+F28 =G27+G28 =H27+H28 =I27+I28

=J27+J

28

Less: Interest -1160000 -1160000 -1160000 -1160000 -1160000 -1160000

-

11600

00

Income after

depreciation =D29+D30 =E29+E30 =F29+F30 =G29+G30 =H29+H30 =I29+I30

=J29+J

30

Income tax @ 30% =D31*-0.3 =E31*-0.3 =F31*-0.3 =G31*-0.3 =H31*-0.3 =I31*-0.3

=J31*-

0.3

Income after tax

and depr. =D31+D32 =E31+E32 =F31+F32 =G31+G32 =H31+H32 =I31+I32

=J31+J

32

Add: Depreciation

1783333.3333333

3

1783333.33

333333

1783333.33

333333

1783333.33

333333

1783333.33

333333

1783333.33

333333

Net Income =D33+D34 =E33+E34 =F33+F34 =G33+G34 =H33+H34 =I33+I34 =J33+J

Corporate finance is the financing section which interacts with how companies

approach with sources of financing, capital structure and investment decisions (Johnson, 2019).It

main focuses mainly on optimizing shareholder interest through long-term and short-term

strategic preparation and the execution of various approaches. Capital expenditure initiatives

vary from business management operations to investment banking.

In this report, investment decision for Blue Mountain Ltd in order to introduce new product

is discussed. In addition, the part B of report describes the financial decision included dividend

and capital structure is elaborated.

PART A

Formula from excel:

Initial Investment

required

New Machine

1200000

0

Research 860000

Net working capital

requirement 600000

Advertising

campaign 2500000

Total

=SUM(C1

7:C20)

Years

Particulars 0 1 2 3 4 5 6 7

Initial investment =-C21

Sales revenue 2600000 4600000 6600000 8600000 10600000 10000000

96000

00

Less: Operating

expenses @23% =D25*-0.23 =E25*-0.23 =F25*-0.23 =G25*-0.23 =H25*-0.23 =I25*-0.23

=J25*-

0.23

Operating profit =D25+D26 =E25+E26 =F25+F26 =G25+G26 =H25+H26 =I25+I26

=J25+J

26

Less: Depreciation

-

1783333.3333333

3

-

1783333.33

333333

-

1783333.33

333333

-

1783333.33

333333

-

1783333.33

333333

-

1783333.33

333333

13000

00

Income after

depreciation before

interest =D27+D28 =E27+E28 =F27+F28 =G27+G28 =H27+H28 =I27+I28

=J27+J

28

Less: Interest -1160000 -1160000 -1160000 -1160000 -1160000 -1160000

-

11600

00

Income after

depreciation =D29+D30 =E29+E30 =F29+F30 =G29+G30 =H29+H30 =I29+I30

=J29+J

30

Income tax @ 30% =D31*-0.3 =E31*-0.3 =F31*-0.3 =G31*-0.3 =H31*-0.3 =I31*-0.3

=J31*-

0.3

Income after tax

and depr. =D31+D32 =E31+E32 =F31+F32 =G31+G32 =H31+H32 =I31+I32

=J31+J

32

Add: Depreciation

1783333.3333333

3

1783333.33

333333

1783333.33

333333

1783333.33

333333

1783333.33

333333

1783333.33

333333

Net Income =D33+D34 =E33+E34 =F33+F34 =G33+G34 =H33+H34 =I33+I34 =J33+J

34

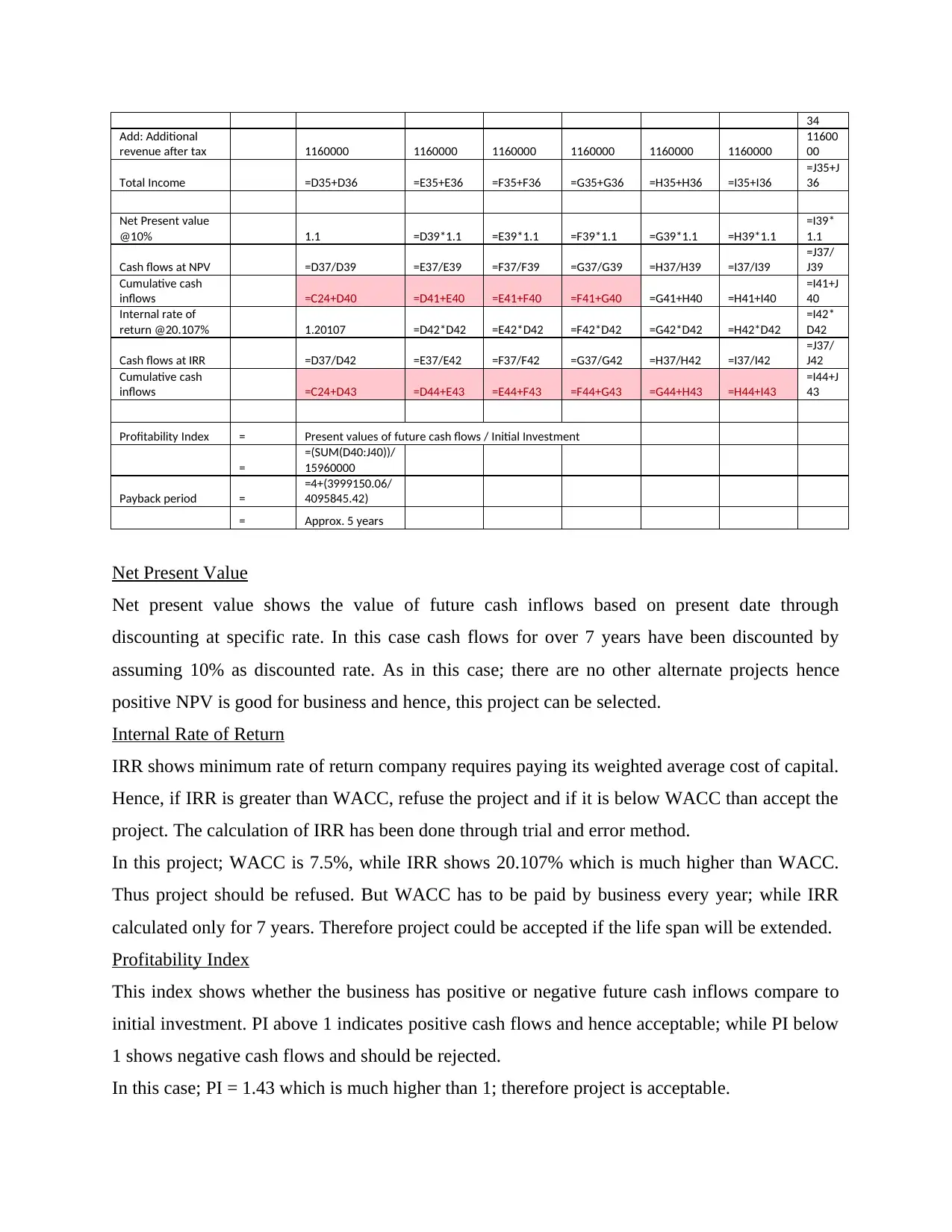

Add: Additional

revenue after tax 1160000 1160000 1160000 1160000 1160000 1160000

11600

00

Total Income =D35+D36 =E35+E36 =F35+F36 =G35+G36 =H35+H36 =I35+I36

=J35+J

36

Net Present value

@10% 1.1 =D39*1.1 =E39*1.1 =F39*1.1 =G39*1.1 =H39*1.1

=I39*

1.1

Cash flows at NPV =D37/D39 =E37/E39 =F37/F39 =G37/G39 =H37/H39 =I37/I39

=J37/

J39

Cumulative cash

inflows =C24+D40 =D41+E40 =E41+F40 =F41+G40 =G41+H40 =H41+I40

=I41+J

40

Internal rate of

return @20.107% 1.20107 =D42*D42 =E42*D42 =F42*D42 =G42*D42 =H42*D42

=I42*

D42

Cash flows at IRR =D37/D42 =E37/E42 =F37/F42 =G37/G42 =H37/H42 =I37/I42

=J37/

J42

Cumulative cash

inflows =C24+D43 =D44+E43 =E44+F43 =F44+G43 =G44+H43 =H44+I43

=I44+J

43

Profitability Index = Present values of future cash flows / Initial Investment

=

=(SUM(D40:J40))/

15960000

Payback period =

=4+(3999150.06/

4095845.42)

= Approx. 5 years

Net Present Value

Net present value shows the value of future cash inflows based on present date through

discounting at specific rate. In this case cash flows for over 7 years have been discounted by

assuming 10% as discounted rate. As in this case; there are no other alternate projects hence

positive NPV is good for business and hence, this project can be selected.

Internal Rate of Return

IRR shows minimum rate of return company requires paying its weighted average cost of capital.

Hence, if IRR is greater than WACC, refuse the project and if it is below WACC than accept the

project. The calculation of IRR has been done through trial and error method.

In this project; WACC is 7.5%, while IRR shows 20.107% which is much higher than WACC.

Thus project should be refused. But WACC has to be paid by business every year; while IRR

calculated only for 7 years. Therefore project could be accepted if the life span will be extended.

Profitability Index

This index shows whether the business has positive or negative future cash inflows compare to

initial investment. PI above 1 indicates positive cash flows and hence acceptable; while PI below

1 shows negative cash flows and should be rejected.

In this case; PI = 1.43 which is much higher than 1; therefore project is acceptable.

Add: Additional

revenue after tax 1160000 1160000 1160000 1160000 1160000 1160000

11600

00

Total Income =D35+D36 =E35+E36 =F35+F36 =G35+G36 =H35+H36 =I35+I36

=J35+J

36

Net Present value

@10% 1.1 =D39*1.1 =E39*1.1 =F39*1.1 =G39*1.1 =H39*1.1

=I39*

1.1

Cash flows at NPV =D37/D39 =E37/E39 =F37/F39 =G37/G39 =H37/H39 =I37/I39

=J37/

J39

Cumulative cash

inflows =C24+D40 =D41+E40 =E41+F40 =F41+G40 =G41+H40 =H41+I40

=I41+J

40

Internal rate of

return @20.107% 1.20107 =D42*D42 =E42*D42 =F42*D42 =G42*D42 =H42*D42

=I42*

D42

Cash flows at IRR =D37/D42 =E37/E42 =F37/F42 =G37/G42 =H37/H42 =I37/I42

=J37/

J42

Cumulative cash

inflows =C24+D43 =D44+E43 =E44+F43 =F44+G43 =G44+H43 =H44+I43

=I44+J

43

Profitability Index = Present values of future cash flows / Initial Investment

=

=(SUM(D40:J40))/

15960000

Payback period =

=4+(3999150.06/

4095845.42)

= Approx. 5 years

Net Present Value

Net present value shows the value of future cash inflows based on present date through

discounting at specific rate. In this case cash flows for over 7 years have been discounted by

assuming 10% as discounted rate. As in this case; there are no other alternate projects hence

positive NPV is good for business and hence, this project can be selected.

Internal Rate of Return

IRR shows minimum rate of return company requires paying its weighted average cost of capital.

Hence, if IRR is greater than WACC, refuse the project and if it is below WACC than accept the

project. The calculation of IRR has been done through trial and error method.

In this project; WACC is 7.5%, while IRR shows 20.107% which is much higher than WACC.

Thus project should be refused. But WACC has to be paid by business every year; while IRR

calculated only for 7 years. Therefore project could be accepted if the life span will be extended.

Profitability Index

This index shows whether the business has positive or negative future cash inflows compare to

initial investment. PI above 1 indicates positive cash flows and hence acceptable; while PI below

1 shows negative cash flows and should be rejected.

In this case; PI = 1.43 which is much higher than 1; therefore project is acceptable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Payback period

There’s no other project from which payback period could be matched; here discounted payback

period at the rate of 10% has been considered. The result shows initial investment can be covered

before 5th year and hence it is acceptable.

PART B

Dividend policy and capital structure:

The principle of dividend irrelevance maintains the assumption that dividends have little

impact on the market price of a firm. A dividend is usually a monetary pay out paid to the

owners from a company's earnings as a compensation for investment in the corporation. The

principle of capital structure irrelevance goes on to state that dividends will harm the potential of

a firm to remain profitable over the long run because the capital will be best spent reinvested in

the business to produce income (Lerner and Seru, 2017).It also implies that the announcement of

a corporation and the distribution of dividends will have little as well as minor impact on the

market price. Unless this principle is valid, then dividends will not contribute positively to the

market price of a business. The theory's assumption is that the potential of a corporation to make

a profit and expand its profits defines the market interest of a company which influences the

share price; not investment returns. Many who engage in the principle of capital structure

irrelevance claim that dividends give investors little additional value, and in some situations

suggest that cash flows will harm the company's financial position.

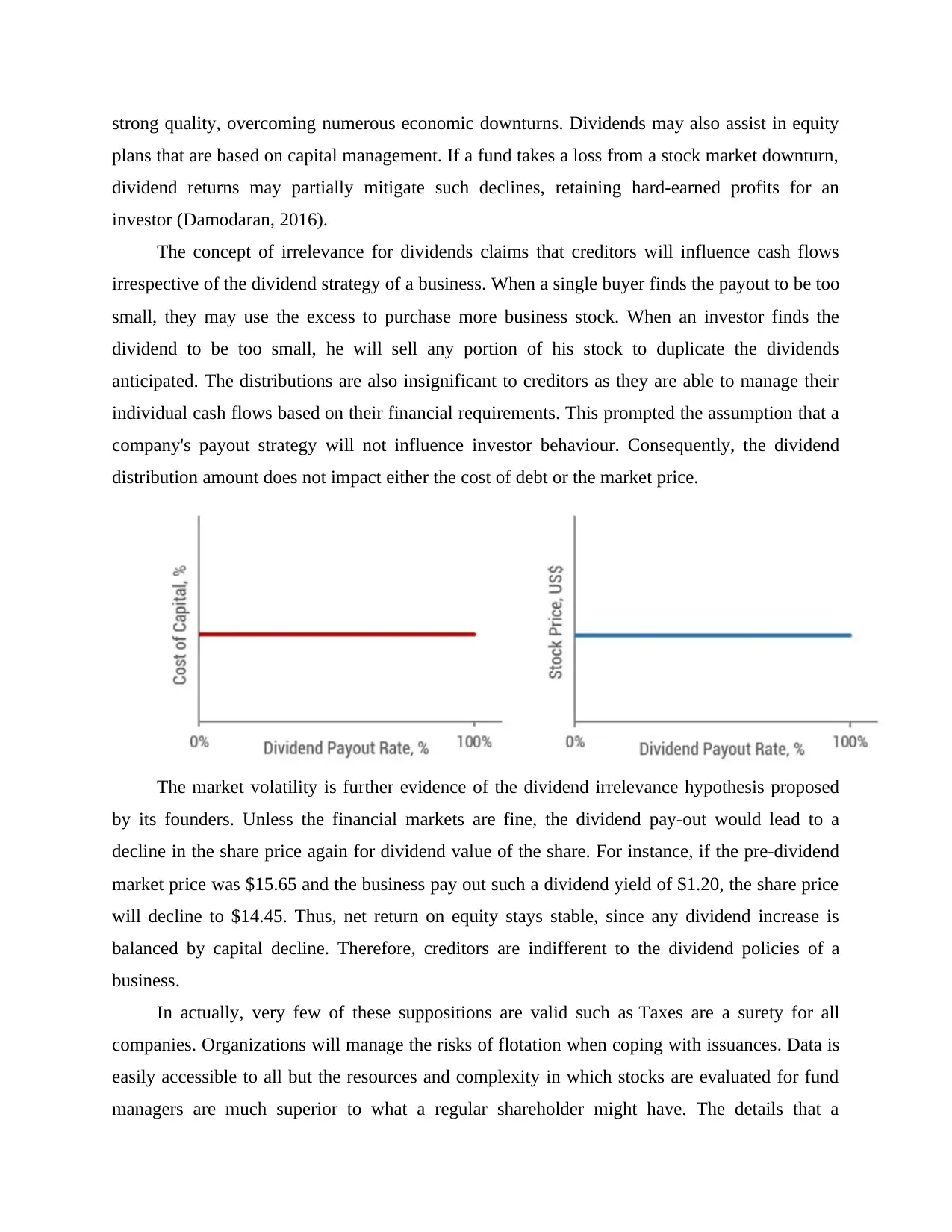

The hypothesis of dividend irrelevance claims that perhaps the economics works

successfully and that every dividend distribution would result in a decrease in the share price

even by sum of the dividend. For example, if the market price is $10, and the corporation paid a

profit of $1, the market would decline to $9 a share, a few days later. Keeping the shares for the

distribution then produces little advantage because the market price moves lower with the same

sum of the payment.Though this stock may fall after the dividends was already paid, such stocks

are retained by several dividend-seeking buyers for the steady dividends they give, generating an

enduring degree of demand. Therefore, a firm's stock price is influenced mostly by the dividend

strategy of the business. In a company bookkeeper or analyst conduct valuation experiments to

assess the inherent value of a portfolio. They also include considerations such as cash dividend

There’s no other project from which payback period could be matched; here discounted payback

period at the rate of 10% has been considered. The result shows initial investment can be covered

before 5th year and hence it is acceptable.

PART B

Dividend policy and capital structure:

The principle of dividend irrelevance maintains the assumption that dividends have little

impact on the market price of a firm. A dividend is usually a monetary pay out paid to the

owners from a company's earnings as a compensation for investment in the corporation. The

principle of capital structure irrelevance goes on to state that dividends will harm the potential of

a firm to remain profitable over the long run because the capital will be best spent reinvested in

the business to produce income (Lerner and Seru, 2017).It also implies that the announcement of

a corporation and the distribution of dividends will have little as well as minor impact on the

market price. Unless this principle is valid, then dividends will not contribute positively to the

market price of a business. The theory's assumption is that the potential of a corporation to make

a profit and expand its profits defines the market interest of a company which influences the

share price; not investment returns. Many who engage in the principle of capital structure

irrelevance claim that dividends give investors little additional value, and in some situations

suggest that cash flows will harm the company's financial position.

The hypothesis of dividend irrelevance claims that perhaps the economics works

successfully and that every dividend distribution would result in a decrease in the share price

even by sum of the dividend. For example, if the market price is $10, and the corporation paid a

profit of $1, the market would decline to $9 a share, a few days later. Keeping the shares for the

distribution then produces little advantage because the market price moves lower with the same

sum of the payment.Though this stock may fall after the dividends was already paid, such stocks

are retained by several dividend-seeking buyers for the steady dividends they give, generating an

enduring degree of demand. Therefore, a firm's stock price is influenced mostly by the dividend

strategy of the business. In a company bookkeeper or analyst conduct valuation experiments to

assess the inherent value of a portfolio. They also include considerations such as cash dividend

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as well as financial results and contextual metrics, including standards of personnel, economic

conditions and an appreciation of the role of the business in the market.

The principle of dividend irrelevance implies that the payment of dividends, that is never an

uncommon phenomenon, will damage corporations' economic well-being (Gullifer and Payne,

2015).

Debt acquisition

Dividends will harm a corporation if the business takes on loans to fund their dividend

pay-out money in the form of selling bonds to creditors or leveraging from a banking credit

facilities. Failure to control its leverage, weak management execution and external influences,

like sluggish economic development, may all contribute to the problems of a company.

Industries who do not offer dividends, though, have more capital at hand to allow investments,

grow in properties, and pay off the mortgage with the extra funds.

CAPEX spending

In case if a firm does not spend by capital spending (CAPEX) in its industry, there will be

a reduction in the value of the corporation as profits and undermine the profitability over time.

Capital spending is a major commitment that businesses undertake in maintaining long-term

financial wellbeing, which may involve purchasing houses, infrastructure, facilities, which

acquisitions. Investors purchasing dividend-paying securities seek to determine how a

management team is successfully juggling the dividend pay-outs and investing in their future

(Dang, Li and Yang, 2018).

Considering the principle of irrelevance dividends, a number of investors rely on dividends

while running their investments. For example an actual income policy, aims to define assets that

benefit out of regular returns (i.e. dividend and accrued interest). Although still fairly risk-averse,

existing sales approaches may be integrated through a continuum of risk along a variety of

decision processes.

Income focused plans are typically tailored to homeowners or risk-averse buyers. Such

income-seeking investors are buying securities of proven companies that have the track history

of regularly paying a dividend but are at lower risk of losing a dividend pay-out.Blue-chip

companies typically offer predictable dividends such as the International corporations who were

in business for many years, including Coca-Cola, Disney, PepsiCo, Walmart and McDonald's.

Such businesses are global players of their respective markets and have established brands with

conditions and an appreciation of the role of the business in the market.

The principle of dividend irrelevance implies that the payment of dividends, that is never an

uncommon phenomenon, will damage corporations' economic well-being (Gullifer and Payne,

2015).

Debt acquisition

Dividends will harm a corporation if the business takes on loans to fund their dividend

pay-out money in the form of selling bonds to creditors or leveraging from a banking credit

facilities. Failure to control its leverage, weak management execution and external influences,

like sluggish economic development, may all contribute to the problems of a company.

Industries who do not offer dividends, though, have more capital at hand to allow investments,

grow in properties, and pay off the mortgage with the extra funds.

CAPEX spending

In case if a firm does not spend by capital spending (CAPEX) in its industry, there will be

a reduction in the value of the corporation as profits and undermine the profitability over time.

Capital spending is a major commitment that businesses undertake in maintaining long-term

financial wellbeing, which may involve purchasing houses, infrastructure, facilities, which

acquisitions. Investors purchasing dividend-paying securities seek to determine how a

management team is successfully juggling the dividend pay-outs and investing in their future

(Dang, Li and Yang, 2018).

Considering the principle of irrelevance dividends, a number of investors rely on dividends

while running their investments. For example an actual income policy, aims to define assets that

benefit out of regular returns (i.e. dividend and accrued interest). Although still fairly risk-averse,

existing sales approaches may be integrated through a continuum of risk along a variety of

decision processes.

Income focused plans are typically tailored to homeowners or risk-averse buyers. Such

income-seeking investors are buying securities of proven companies that have the track history

of regularly paying a dividend but are at lower risk of losing a dividend pay-out.Blue-chip

companies typically offer predictable dividends such as the International corporations who were

in business for many years, including Coca-Cola, Disney, PepsiCo, Walmart and McDonald's.

Such businesses are global players of their respective markets and have established brands with

strong quality, overcoming numerous economic downturns. Dividends may also assist in equity

plans that are based on capital management. If a fund takes a loss from a stock market downturn,

dividend returns may partially mitigate such declines, retaining hard-earned profits for an

investor (Damodaran, 2016).

The concept of irrelevance for dividends claims that creditors will influence cash flows

irrespective of the dividend strategy of a business. When a single buyer finds the payout to be too

small, they may use the excess to purchase more business stock. When an investor finds the

dividend to be too small, he will sell any portion of his stock to duplicate the dividends

anticipated. The distributions are also insignificant to creditors as they are able to manage their

individual cash flows based on their financial requirements. This prompted the assumption that a

company's payout strategy will not influence investor behaviour. Consequently, the dividend

distribution amount does not impact either the cost of debt or the market price.

The market volatility is further evidence of the dividend irrelevance hypothesis proposed

by its founders. Unless the financial markets are fine, the dividend pay-out would lead to a

decline in the share price again for dividend value of the share. For instance, if the pre-dividend

market price was $15.65 and the business pay out such a dividend yield of $1.20, the share price

will decline to $14.45. Thus, net return on equity stays stable, since any dividend increase is

balanced by capital decline. Therefore, creditors are indifferent to the dividend policies of a

business.

In actually, very few of these suppositions are valid such as Taxes are a surety for all

companies. Organizations will manage the risks of flotation when coping with issuances. Data is

easily accessible to all but the resources and complexity in which stocks are evaluated for fund

managers are much superior to what a regular shareholder might have. The details that a

plans that are based on capital management. If a fund takes a loss from a stock market downturn,

dividend returns may partially mitigate such declines, retaining hard-earned profits for an

investor (Damodaran, 2016).

The concept of irrelevance for dividends claims that creditors will influence cash flows

irrespective of the dividend strategy of a business. When a single buyer finds the payout to be too

small, they may use the excess to purchase more business stock. When an investor finds the

dividend to be too small, he will sell any portion of his stock to duplicate the dividends

anticipated. The distributions are also insignificant to creditors as they are able to manage their

individual cash flows based on their financial requirements. This prompted the assumption that a

company's payout strategy will not influence investor behaviour. Consequently, the dividend

distribution amount does not impact either the cost of debt or the market price.

The market volatility is further evidence of the dividend irrelevance hypothesis proposed

by its founders. Unless the financial markets are fine, the dividend pay-out would lead to a

decline in the share price again for dividend value of the share. For instance, if the pre-dividend

market price was $15.65 and the business pay out such a dividend yield of $1.20, the share price

will decline to $14.45. Thus, net return on equity stays stable, since any dividend increase is

balanced by capital decline. Therefore, creditors are indifferent to the dividend policies of a

business.

In actually, very few of these suppositions are valid such as Taxes are a surety for all

companies. Organizations will manage the risks of flotation when coping with issuances. Data is

easily accessible to all but the resources and complexity in which stocks are evaluated for fund

managers are much superior to what a regular shareholder might have. The details that a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management of a business can have are always preferable to what an outside investor may have,

given the advanced resources they possess (Damodaran, 2016).

The determination mostly on form of funding to be included, the sum to also be collected

and the percentage to be generated in the total capitalization is referred to that as the judgment on

financial performance. Such actions are quite significant, since they affect the profits of the

shareholder.The financial structure of an organization often relies on its revenue, i.e. if the

business's valuation is supposed to stay constant, therefore the company will reach a large

leverage price. It is because the performance of the business in revenues means that the

organization is able to fulfil its commitments on a timely basis. Similarly, revenue increase also

means that the business is expected to collect debt capital to finance expenditure proposals.

CONCLUSION

In conclusion, it is observed that Modigliani and Miller believes it's just the willingness of

the business to raise profits and how dangerous the operation is that has an influence on the

organization's valuation. In addition, theirassumptions can technically be valid but in the real

environment they are not accurate. An ideal capital structure consists something that the total

capital expenditure is minimal and optimum profit per share.

given the advanced resources they possess (Damodaran, 2016).

The determination mostly on form of funding to be included, the sum to also be collected

and the percentage to be generated in the total capitalization is referred to that as the judgment on

financial performance. Such actions are quite significant, since they affect the profits of the

shareholder.The financial structure of an organization often relies on its revenue, i.e. if the

business's valuation is supposed to stay constant, therefore the company will reach a large

leverage price. It is because the performance of the business in revenues means that the

organization is able to fulfil its commitments on a timely basis. Similarly, revenue increase also

means that the business is expected to collect debt capital to finance expenditure proposals.

CONCLUSION

In conclusion, it is observed that Modigliani and Miller believes it's just the willingness of

the business to raise profits and how dangerous the operation is that has an influence on the

organization's valuation. In addition, theirassumptions can technically be valid but in the real

environment they are not accurate. An ideal capital structure consists something that the total

capital expenditure is minimal and optimum profit per share.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dang, C., Li, Z.F. and Yang, C., 2018.Measuring firm size in empirical corporate

finance. Journal of Banking & Finance, 86, pp.159-176.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy. Bloomsbury

Publishing.

Johnson, M., 2019. Corporate finance and the securities laws.Wolters Kluwer Law & Business.

Lerner, J. and Seru, A., 2017. The use and misuse of patent data: Issues for corporate finance

and beyond (No. w24053). National Bureau of Economic Research.

Books and Journals

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dang, C., Li, Z.F. and Yang, C., 2018.Measuring firm size in empirical corporate

finance. Journal of Banking & Finance, 86, pp.159-176.

Gullifer, L. and Payne, J., 2015. Corporate finance law: principles and policy. Bloomsbury

Publishing.

Johnson, M., 2019. Corporate finance and the securities laws.Wolters Kluwer Law & Business.

Lerner, J. and Seru, A., 2017. The use and misuse of patent data: Issues for corporate finance

and beyond (No. w24053). National Bureau of Economic Research.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.