Investment Proposal for New Product Line: Financial Evaluation

VerifiedAdded on 2019/10/12

|14

|3378

|203

Report

AI Summary

This report presents an investment proposal for a new product line, employing the net present value (NPV) discounting technique and the payback period method for financial evaluation. The proposal outlines a six-year plan, detailing cash flows, including purchases, wages, advertising, and income. The analysis calculates the NPV, which is positive at 73,202, and a payback period of approximately three years, suggesting the project's financial viability. The report highlights the importance of investment proposals in attracting investors and providing financial insights. It also discusses the advantages of NPV in considering the time value of money and the limitations of the payback period, such as not accounting for the time value of money and other critical factors. The application of these methods in project selection and their criticisms are also addressed, providing a comprehensive financial perspective on the investment decision-making process. The report concludes that the project is acceptable based on the positive financial outcomes.

Investment Proposal

Student Name:

Course work:

University:

Student Name:

Course work:

University:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................3

Importance of Investment proposal.................................................................................................3

Discounting cash flow technique.....................................................................................................4

Traditional cash flow technique.......................................................................................................5

Proposed Investment proposal.........................................................................................................5

Application for the determination of cash flow...............................................................................6

Criticism of the methods..................................................................................................................7

Logical aspect of Decision making..................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................10

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................3

Importance of Investment proposal.................................................................................................3

Discounting cash flow technique.....................................................................................................4

Traditional cash flow technique.......................................................................................................5

Proposed Investment proposal.........................................................................................................5

Application for the determination of cash flow...............................................................................6

Criticism of the methods..................................................................................................................7

Logical aspect of Decision making..................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................10

Executive Summary

The investment proposal is a very important document of the company because it creates the first

impression on the investors which helps them to proceed towards the next investment process.

The investment proposal includes two sections, namely, descriptive information and financial

information. The net present value discounting technique and pay-back period traditional

technique is used by the company for preparing the investment proposal for six years. The net

present value technique is used for taking the decision regarding the investment in the project.

The pay-back period is used to determine the duration require to recover the initial cash flow of

investment in the project. The net present cash flow does not consider the opportunity cost which

is very necessary to choose the project. The pay-back period does not consider the time value of

money, risk, and other important factors to evaluate the project. The net present value of the

company is positive and the pay-back period is positive which shows the new product investment

proposal must be accepted.

The investment proposal is a very important document of the company because it creates the first

impression on the investors which helps them to proceed towards the next investment process.

The investment proposal includes two sections, namely, descriptive information and financial

information. The net present value discounting technique and pay-back period traditional

technique is used by the company for preparing the investment proposal for six years. The net

present value technique is used for taking the decision regarding the investment in the project.

The pay-back period is used to determine the duration require to recover the initial cash flow of

investment in the project. The net present cash flow does not consider the opportunity cost which

is very necessary to choose the project. The pay-back period does not consider the time value of

money, risk, and other important factors to evaluate the project. The net present value of the

company is positive and the pay-back period is positive which shows the new product investment

proposal must be accepted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

In this present paper, we will discuss the measures to improve the shareholder's wealth of

international listed company within the textbook publishing industry. In this paper, investment

proposal for six years has been made for the product line using Net present value discounted

technique and payback period traditional technique.

Investment proposal is defined as the document which is prepared by the sponsor for a new

investment project in an existing firm. The aim of investment proposal is to motivate the

potential investors to enter into the mutual benefit business relationship by entering into the

investment proposal. The information in the proposal helps the investors to understand the value

of the firm and enables them to understand the reward associated with investment in the project.

The proposal is prepared as a generic document which is intended to reach the wide range of

investors. The main aim of investment proposal is to attract the investors to invest in the

particular project by showing them the benefits of investment. The net present value discounting

technique and pay-back period traditional technique is used by the company for preparing the

investment proposal for the new product line of the company.

Importance of Investment proposal

The investment proposal is a very important to document for the company. It is used by the

company attract the investors for investing in the project. The information included in the

proposal helps to provide the screenshot of company’s financial position. It also shows the

benefits of entering into the proposal. The scope of the project is to provide key sections which

provide the relevant information to the investors. The proposal starts with the nature of the

investment opportunity which includes history and background of the company’s investments.

The proposal addresses the structure of the investment with the duration and returns on

investment (Bierman et al., 2012). The originator of the proposal needs to consider the relevant

information which is required by the investor's such returns of investment, the growth of

investment, and others. The investment proposal allows the investors to concentrate the

investment decision which is a very crucial decision for an investor because it includes the

commitment of huge amount of funds. The information includes competition analysis, market

In this present paper, we will discuss the measures to improve the shareholder's wealth of

international listed company within the textbook publishing industry. In this paper, investment

proposal for six years has been made for the product line using Net present value discounted

technique and payback period traditional technique.

Investment proposal is defined as the document which is prepared by the sponsor for a new

investment project in an existing firm. The aim of investment proposal is to motivate the

potential investors to enter into the mutual benefit business relationship by entering into the

investment proposal. The information in the proposal helps the investors to understand the value

of the firm and enables them to understand the reward associated with investment in the project.

The proposal is prepared as a generic document which is intended to reach the wide range of

investors. The main aim of investment proposal is to attract the investors to invest in the

particular project by showing them the benefits of investment. The net present value discounting

technique and pay-back period traditional technique is used by the company for preparing the

investment proposal for the new product line of the company.

Importance of Investment proposal

The investment proposal is a very important to document for the company. It is used by the

company attract the investors for investing in the project. The information included in the

proposal helps to provide the screenshot of company’s financial position. It also shows the

benefits of entering into the proposal. The scope of the project is to provide key sections which

provide the relevant information to the investors. The proposal starts with the nature of the

investment opportunity which includes history and background of the company’s investments.

The proposal addresses the structure of the investment with the duration and returns on

investment (Bierman et al., 2012). The originator of the proposal needs to consider the relevant

information which is required by the investor's such returns of investment, the growth of

investment, and others. The investment proposal allows the investors to concentrate the

investment decision which is a very crucial decision for an investor because it includes the

commitment of huge amount of funds. The information includes competition analysis, market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

strategy, traction and others. The investment proposal is very necessary because it is used to raise

the funds for the investment in the particular project. The funds include equity, debts, and trade

funds. The collateral needs to support the application for the funding of the project. The proposal

must grab the attention of the investors and it must create the first impression on the investors so

that they can precede the funding application to the next application. The small section of the

proposal makes the next phase of the investment process. The proposal consists of two sections,

namely, descriptive section and financial information section. The descriptive section includes

the history of the company, details of the product and services, management team, details of the

investor sector, advantages of investment in the project and others. The financial information

section includes historical and current trading position of the company. The broad headings of

investment proposal include executive summary, history of the company, details of the product

and services, details of the target market, profiles of the company’s directors, founders and

others, SWOT analysis, relevant information for investors, regulations, and exit strategy

(Pompian et al., 2012).

Discounting cash flow technique

The discounting cash flow technique provides the most objective basis for evaluating and

choosing the investment project. It enables one to isolate the difference in the period of time of

cash flows for various projects by discounting the cash flows to the present values. The

discounting technique takes into account the magnitude and duration of the expected cash flows

in each period of the life of the project. The net present value is the discounting technique which

is used by the company for taking the decision to accept or reject the project. It is calculated by

deducting the present cash inflow from the present cash outflow of the project (Leyman et al.,

2016. The cash flow is discounted at the desired rate of return which is equal to the cost of

capital. The equation of net present value is as follows:

the funds for the investment in the particular project. The funds include equity, debts, and trade

funds. The collateral needs to support the application for the funding of the project. The proposal

must grab the attention of the investors and it must create the first impression on the investors so

that they can precede the funding application to the next application. The small section of the

proposal makes the next phase of the investment process. The proposal consists of two sections,

namely, descriptive section and financial information section. The descriptive section includes

the history of the company, details of the product and services, management team, details of the

investor sector, advantages of investment in the project and others. The financial information

section includes historical and current trading position of the company. The broad headings of

investment proposal include executive summary, history of the company, details of the product

and services, details of the target market, profiles of the company’s directors, founders and

others, SWOT analysis, relevant information for investors, regulations, and exit strategy

(Pompian et al., 2012).

Discounting cash flow technique

The discounting cash flow technique provides the most objective basis for evaluating and

choosing the investment project. It enables one to isolate the difference in the period of time of

cash flows for various projects by discounting the cash flows to the present values. The

discounting technique takes into account the magnitude and duration of the expected cash flows

in each period of the life of the project. The net present value is the discounting technique which

is used by the company for taking the decision to accept or reject the project. It is calculated by

deducting the present cash inflow from the present cash outflow of the project (Leyman et al.,

2016. The cash flow is discounted at the desired rate of return which is equal to the cost of

capital. The equation of net present value is as follows:

In the above equation A1, A2, till An are the cash flows of the project, K is the cost of capital of

the firm. The advantage of Net present value includes the recognition of the time value of

money; it includes the cash flows of the whole life of the project, and its objective is to maximize

the wealth of the shareholders. It is the measurement of the profitability of the project. It

determines the cost and benefits of each of the period of investment. The net present value is the

sum of the discounted future cash flows. It is the very important tool for determining the profit or

loss related to the investment in the project. The positive Net present value reflects the

profitability in investing in the project, and the negative net present value reflects the loss in

investment in the project. It is the standard method for using the time value of money to appraise

the long-term projects of the company. It is used in the economics, finance, and accounting

areas. The discounting mainly refers to take the future amount and find its value (Lind et al.,

2013). The future value is differing from the present value because of the time value of money.

The financial management recognizes the time value of money because of some factors, which

includes inflation, uncertainty, and opportunity cost. The assumptions of the net present value

analysis include that the investment horizon of the investment projects must be equally

considered by the investors, the appropriate rate to discount the expected cash flow is 10%, and

the shareholders cannot receive more than 10% return if the level of risk is equally treated.

Traditional cash flows technique

The traditional cash flow technique includes Payback period which is used to determine the time

require to recover the initial investment in the project. It helps to determine the break-even point

of the project. The payback period helps to find how long it takes to "pay for itself." The payback

period is easy to calculate, and it acts asa analysis tools to measure the recovering period of the

project. It is the stand-alone tool which is used to compare an investment to "doing nothing" of

the project. Following is the equation of payback period:

the firm. The advantage of Net present value includes the recognition of the time value of

money; it includes the cash flows of the whole life of the project, and its objective is to maximize

the wealth of the shareholders. It is the measurement of the profitability of the project. It

determines the cost and benefits of each of the period of investment. The net present value is the

sum of the discounted future cash flows. It is the very important tool for determining the profit or

loss related to the investment in the project. The positive Net present value reflects the

profitability in investing in the project, and the negative net present value reflects the loss in

investment in the project. It is the standard method for using the time value of money to appraise

the long-term projects of the company. It is used in the economics, finance, and accounting

areas. The discounting mainly refers to take the future amount and find its value (Lind et al.,

2013). The future value is differing from the present value because of the time value of money.

The financial management recognizes the time value of money because of some factors, which

includes inflation, uncertainty, and opportunity cost. The assumptions of the net present value

analysis include that the investment horizon of the investment projects must be equally

considered by the investors, the appropriate rate to discount the expected cash flow is 10%, and

the shareholders cannot receive more than 10% return if the level of risk is equally treated.

Traditional cash flows technique

The traditional cash flow technique includes Payback period which is used to determine the time

require to recover the initial investment in the project. It helps to determine the break-even point

of the project. The payback period helps to find how long it takes to "pay for itself." The payback

period is easy to calculate, and it acts asa analysis tools to measure the recovering period of the

project. It is the stand-alone tool which is used to compare an investment to "doing nothing" of

the project. Following is the equation of payback period:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Ny represents the number of years after the initial investment; n is the value of the

cumulative cash flow, P is the first value of the positive cash flow. The formula is used to

calculate the payback period and in the first year. The cumulative cash flow drops negative value

in the starting and then reached to the positive value. Initially, the sum of all the cash outflows is

calculated then cumulative positive cash outflow is calculated. The modified payback is

calculated by deducting the cumulative positive cash flow from total cash outflow. It is one of

the most popular traditional techniques of cash flow which is used for evaluating investment

proposal. It is used to determine the number of years requires recovering the initial outlay of the

company. The advantages of using payback period technique are that the riskiness of the project

can be the tackle. It provides the insight liquidity of the project (Bansal et al., 2015).

Proposed Investment proposal

The proposed investment proposal is made for the six years by using the net present value

discounting technique and pay-back period traditional technique. The following table shows the

investment proposal for the new product line in the company.

cumulative cash flow, P is the first value of the positive cash flow. The formula is used to

calculate the payback period and in the first year. The cumulative cash flow drops negative value

in the starting and then reached to the positive value. Initially, the sum of all the cash outflows is

calculated then cumulative positive cash outflow is calculated. The modified payback is

calculated by deducting the cumulative positive cash flow from total cash outflow. It is one of

the most popular traditional techniques of cash flow which is used for evaluating investment

proposal. It is used to determine the number of years requires recovering the initial outlay of the

company. The advantages of using payback period technique are that the riskiness of the project

can be the tackle. It provides the insight liquidity of the project (Bansal et al., 2015).

Proposed Investment proposal

The proposed investment proposal is made for the six years by using the net present value

discounting technique and pay-back period traditional technique. The following table shows the

investment proposal for the new product line in the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

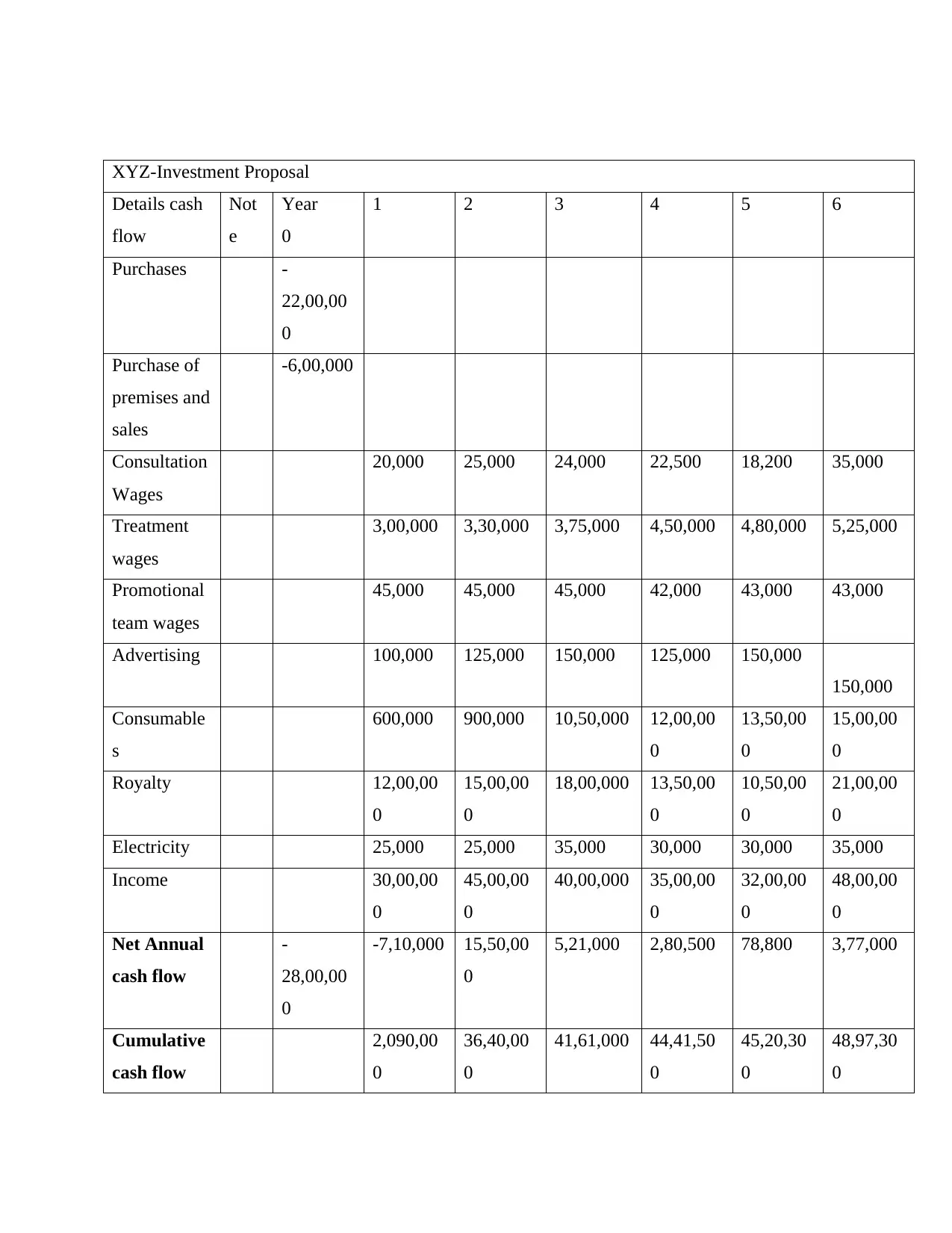

XYZ-Investment Proposal

Details cash

flow

Not

e

Year

0

1 2 3 4 5 6

Purchases -

22,00,00

0

Purchase of

premises and

sales

-6,00,000

Consultation

Wages

20,000 25,000 24,000 22,500 18,200 35,000

Treatment

wages

3,00,000 3,30,000 3,75,000 4,50,000 4,80,000 5,25,000

Promotional

team wages

45,000 45,000 45,000 42,000 43,000 43,000

Advertising 100,000 125,000 150,000 125,000 150,000

150,000

Consumable

s

600,000 900,000 10,50,000 12,00,00

0

13,50,00

0

15,00,00

0

Royalty 12,00,00

0

15,00,00

0

18,00,000 13,50,00

0

10,50,00

0

21,00,00

0

Electricity 25,000 25,000 35,000 30,000 30,000 35,000

Income 30,00,00

0

45,00,00

0

40,00,000 35,00,00

0

32,00,00

0

48,00,00

0

Net Annual

cash flow

-

28,00,00

0

-7,10,000 15,50,00

0

5,21,000 2,80,500 78,800 3,77,000

Cumulative

cash flow

2,090,00

0

36,40,00

0

41,61,000 44,41,50

0

45,20,30

0

48,97,30

0

Details cash

flow

Not

e

Year

0

1 2 3 4 5 6

Purchases -

22,00,00

0

Purchase of

premises and

sales

-6,00,000

Consultation

Wages

20,000 25,000 24,000 22,500 18,200 35,000

Treatment

wages

3,00,000 3,30,000 3,75,000 4,50,000 4,80,000 5,25,000

Promotional

team wages

45,000 45,000 45,000 42,000 43,000 43,000

Advertising 100,000 125,000 150,000 125,000 150,000

150,000

Consumable

s

600,000 900,000 10,50,000 12,00,00

0

13,50,00

0

15,00,00

0

Royalty 12,00,00

0

15,00,00

0

18,00,000 13,50,00

0

10,50,00

0

21,00,00

0

Electricity 25,000 25,000 35,000 30,000 30,000 35,000

Income 30,00,00

0

45,00,00

0

40,00,000 35,00,00

0

32,00,00

0

48,00,00

0

Net Annual

cash flow

-

28,00,00

0

-7,10,000 15,50,00

0

5,21,000 2,80,500 78,800 3,77,000

Cumulative

cash flow

2,090,00

0

36,40,00

0

41,61,000 44,41,50

0

45,20,30

0

48,97,30

0

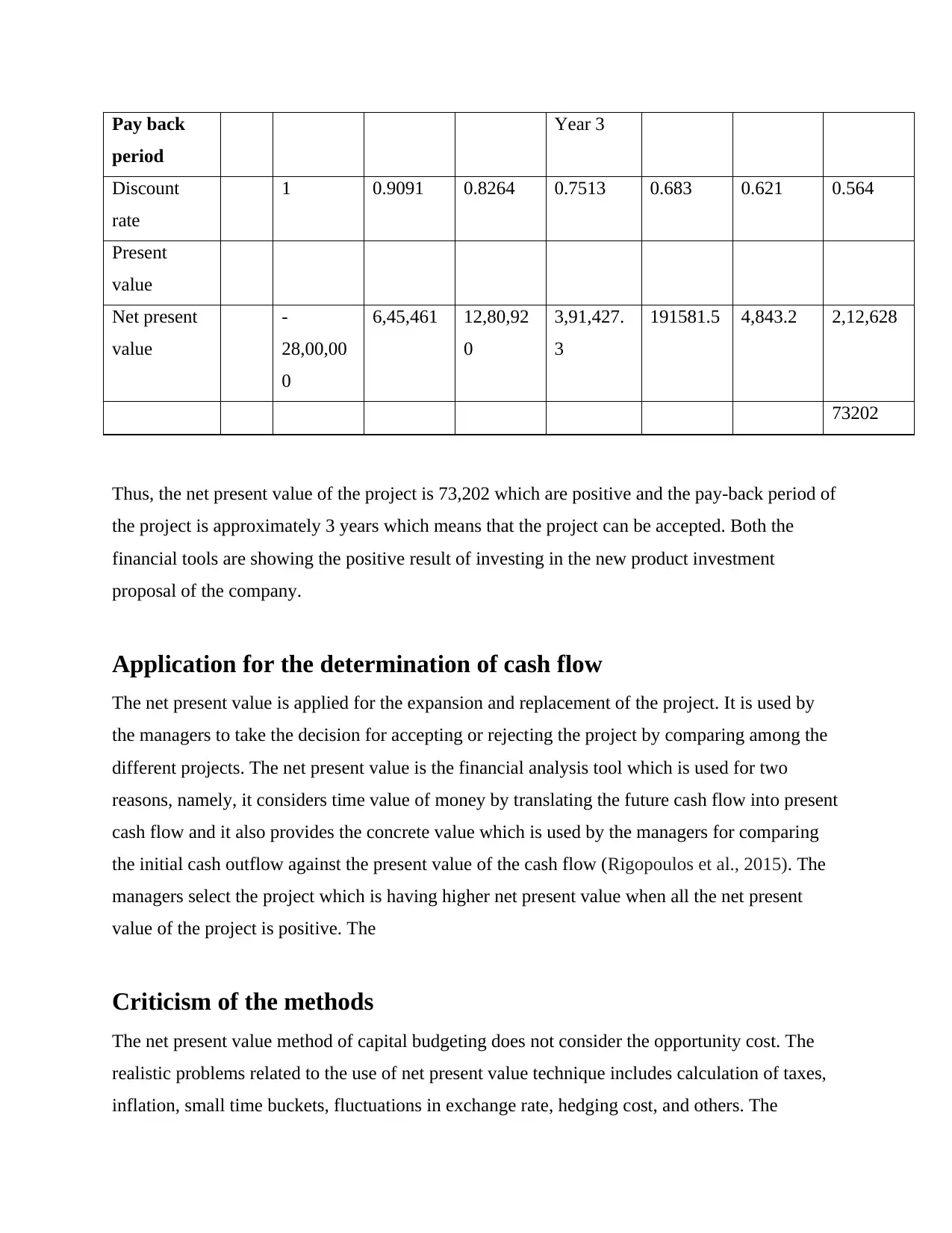

Pay back

period

Year 3

Discount

rate

1 0.9091 0.8264 0.7513 0.683 0.621 0.564

Present

value

Net present

value

-

28,00,00

0

6,45,461 12,80,92

0

3,91,427.

3

191581.5 4,843.2 2,12,628

73202

Thus, the net present value of the project is 73,202 which are positive and the pay-back period of

the project is approximately 3 years which means that the project can be accepted. Both the

financial tools are showing the positive result of investing in the new product investment

proposal of the company.

Application for the determination of cash flow

The net present value is applied for the expansion and replacement of the project. It is used by

the managers to take the decision for accepting or rejecting the project by comparing among the

different projects. The net present value is the financial analysis tool which is used for two

reasons, namely, it considers time value of money by translating the future cash flow into present

cash flow and it also provides the concrete value which is used by the managers for comparing

the initial cash outflow against the present value of the cash flow (Rigopoulos et al., 2015). The

managers select the project which is having higher net present value when all the net present

value of the project is positive. The

Criticism of the methods

The net present value method of capital budgeting does not consider the opportunity cost. The

realistic problems related to the use of net present value technique includes calculation of taxes,

inflation, small time buckets, fluctuations in exchange rate, hedging cost, and others. The

period

Year 3

Discount

rate

1 0.9091 0.8264 0.7513 0.683 0.621 0.564

Present

value

Net present

value

-

28,00,00

0

6,45,461 12,80,92

0

3,91,427.

3

191581.5 4,843.2 2,12,628

73202

Thus, the net present value of the project is 73,202 which are positive and the pay-back period of

the project is approximately 3 years which means that the project can be accepted. Both the

financial tools are showing the positive result of investing in the new product investment

proposal of the company.

Application for the determination of cash flow

The net present value is applied for the expansion and replacement of the project. It is used by

the managers to take the decision for accepting or rejecting the project by comparing among the

different projects. The net present value is the financial analysis tool which is used for two

reasons, namely, it considers time value of money by translating the future cash flow into present

cash flow and it also provides the concrete value which is used by the managers for comparing

the initial cash outflow against the present value of the cash flow (Rigopoulos et al., 2015). The

managers select the project which is having higher net present value when all the net present

value of the project is positive. The

Criticism of the methods

The net present value method of capital budgeting does not consider the opportunity cost. The

realistic problems related to the use of net present value technique includes calculation of taxes,

inflation, small time buckets, fluctuations in exchange rate, hedging cost, and others. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

payback period method has serious limitations because it does not take into account the time

value of money, financing, risk and other important factors which need to be considered. It does

not consider any comparison of the projects. It is also not considered the cash inflow of the

project, the profitability of the project and it also fails to define the cash inflows of the project

(Pasqual et al., 2013).

Logical aspect of Decision making

The net present value indicates the value added by the project in the company. The positive Rt of

the project shows the positive cash inflow of the company and if it is negatives then the status of

discounted cash outflow within the time t. The projects having positive NPV could be accepted.

According to the financial theories, the company should compare the two mutually exclusive

projects, and the one with higher net present value should be selected (Kogan et al., 2014). The

present value indicates that the earnings of the projects are more than the anticipated cost of the

project. The concept of net present value is based on the rule of net present value. According to

the rule of net present value if the net present value is more than one then the project can be

accepted, if the net present value of the project is less than one then the project must be rejected

and if the net present value of the project is zero it means there is neither a loss nor a profit so the

company can accept the project or reject the project. The logical aspect of payback period

includes that if the initial outlay cost of the project is covered in the shorter period then the

company can accept the project, but if the project takes a long time to cover the initial outlay cost

then the company may not accept the project. The very crucial decision investment of funds is a

very crucial decision for the investors because it requires the commitment of huge funds. The net

present value discounting techniques acts as analytical tools which help in taking the decision

regarding the acceptance of the project (Clemen et al., 2013).

Conclusion

The investment proposal plays an important role in raise the capital for the investment projects of

the company. The proposal includes the information which is relevant for the investors and

consumers. The aim of the proposal is to attract the investors by showing the benefits of

value of money, financing, risk and other important factors which need to be considered. It does

not consider any comparison of the projects. It is also not considered the cash inflow of the

project, the profitability of the project and it also fails to define the cash inflows of the project

(Pasqual et al., 2013).

Logical aspect of Decision making

The net present value indicates the value added by the project in the company. The positive Rt of

the project shows the positive cash inflow of the company and if it is negatives then the status of

discounted cash outflow within the time t. The projects having positive NPV could be accepted.

According to the financial theories, the company should compare the two mutually exclusive

projects, and the one with higher net present value should be selected (Kogan et al., 2014). The

present value indicates that the earnings of the projects are more than the anticipated cost of the

project. The concept of net present value is based on the rule of net present value. According to

the rule of net present value if the net present value is more than one then the project can be

accepted, if the net present value of the project is less than one then the project must be rejected

and if the net present value of the project is zero it means there is neither a loss nor a profit so the

company can accept the project or reject the project. The logical aspect of payback period

includes that if the initial outlay cost of the project is covered in the shorter period then the

company can accept the project, but if the project takes a long time to cover the initial outlay cost

then the company may not accept the project. The very crucial decision investment of funds is a

very crucial decision for the investors because it requires the commitment of huge funds. The net

present value discounting techniques acts as analytical tools which help in taking the decision

regarding the acceptance of the project (Clemen et al., 2013).

Conclusion

The investment proposal plays an important role in raise the capital for the investment projects of

the company. The proposal includes the information which is relevant for the investors and

consumers. The aim of the proposal is to attract the investors by showing the benefits of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investment in the particular project. The investment project includes two sections, namely,

descriptive information and financial information. The descriptive information includes history

and the background information about the company. The financial information includes the rate

of return, growth of investment, and other financial aspects of the investment in the project. It

allows the investors to concrete the investment decision which is the very crucial decision

because it involves the commitment of huge funds. The objective of discounting cash flow

technique is to evaluate and assess the project. The net present value technique is used evaluating

the project and preparation of investment proposal for the six years. The net present value is

applicable in economics, finance and accounts. It is used by the managers for taking the decision

regarding the acceptance or rejection of the project. The net present value rule explains the

criteria for accepting and rejecting the project. It the net present value is positive then the project

can be accepted, if the net present value is negative, then the project must be rejected, and if the

net present value is zero, then it is to the investor that he may accept or reject the project. The

traditional technique pay-back period is used for preparing the investment proposal for the six

years. The investment proposal is made for the new product line in the company. The net present

value does not include the opportunity cost which is very necessary for the selecting the project

for the company. The pay-back period does not include the profitability of the company, time

value of money, risk and other important factors which are very necessary for evaluating the

project. The logical aspect of using net present value method is according to the rule of net

present value which is used by the managers for taking a decision regarding the selection of the

project. According to the financial analysis, the net present value of the project is positive which

means then the project can be accepted and the pay-back period of the company is three years

which manes the initial cash outlay of the company will be covered in the first three years of the

investment. It shows that the project must be accepted.

descriptive information and financial information. The descriptive information includes history

and the background information about the company. The financial information includes the rate

of return, growth of investment, and other financial aspects of the investment in the project. It

allows the investors to concrete the investment decision which is the very crucial decision

because it involves the commitment of huge funds. The objective of discounting cash flow

technique is to evaluate and assess the project. The net present value technique is used evaluating

the project and preparation of investment proposal for the six years. The net present value is

applicable in economics, finance and accounts. It is used by the managers for taking the decision

regarding the acceptance or rejection of the project. The net present value rule explains the

criteria for accepting and rejecting the project. It the net present value is positive then the project

can be accepted, if the net present value is negative, then the project must be rejected, and if the

net present value is zero, then it is to the investor that he may accept or reject the project. The

traditional technique pay-back period is used for preparing the investment proposal for the six

years. The investment proposal is made for the new product line in the company. The net present

value does not include the opportunity cost which is very necessary for the selecting the project

for the company. The pay-back period does not include the profitability of the company, time

value of money, risk and other important factors which are very necessary for evaluating the

project. The logical aspect of using net present value method is according to the rule of net

present value which is used by the managers for taking a decision regarding the selection of the

project. According to the financial analysis, the net present value of the project is positive which

means then the project can be accepted and the pay-back period of the company is three years

which manes the initial cash outlay of the company will be covered in the first three years of the

investment. It shows that the project must be accepted.

References

Lyman, P. and Vanhoucke, M., 2016. Capital-and resource-constrained project scheduling with

net present value optimization. European Journal of Operational Research.

Lind, R.C., Arrow, K.J., Corey, G.R., Dasgupta, P., Sen, A.K., Stauffer, T., Stiglitz, J.E. and

Stockfisch, J.A., 2013. Discounting for time and risk in energy policy (Vol. 3). Routledge.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Kogan, A. (2014). The Criticism of Net Present Value and Equivalent Annual Cost. Journal of

Advanced Research in Law and Economics, 5(1 (9)), 15.

Rigopoulos, G., 2015. A review on Real Options utilization in Capital Budgeting

practice. International Journal of Information, Business and Management, 7(2), p.1.

Clemen, R.T. and Reilly, T., 2013. Making hard decisions with DecisionTools. Cengage

Learning.

Bansal, P. and Sharma, G., 2015, January. Making Social Issues Count: How Businesses Make

Responsible Strategic Decisions. In Academy of Management Proceedings (Vol. 2015, No. 1, p.

16173). Academy of Management.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Technical note: equivalence of different

profitability criteria with the net present value. International Journal of Production

Economics, 142(1), pp.205-210.

Pompian, M., 2012. Behavioral finance and investor types. Private Wealth Management Feature

Articles, 2012(1), pp.1-3.

Lyman, P. and Vanhoucke, M., 2016. Capital-and resource-constrained project scheduling with

net present value optimization. European Journal of Operational Research.

Lind, R.C., Arrow, K.J., Corey, G.R., Dasgupta, P., Sen, A.K., Stauffer, T., Stiglitz, J.E. and

Stockfisch, J.A., 2013. Discounting for time and risk in energy policy (Vol. 3). Routledge.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Kogan, A. (2014). The Criticism of Net Present Value and Equivalent Annual Cost. Journal of

Advanced Research in Law and Economics, 5(1 (9)), 15.

Rigopoulos, G., 2015. A review on Real Options utilization in Capital Budgeting

practice. International Journal of Information, Business and Management, 7(2), p.1.

Clemen, R.T. and Reilly, T., 2013. Making hard decisions with DecisionTools. Cengage

Learning.

Bansal, P. and Sharma, G., 2015, January. Making Social Issues Count: How Businesses Make

Responsible Strategic Decisions. In Academy of Management Proceedings (Vol. 2015, No. 1, p.

16173). Academy of Management.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Technical note: equivalence of different

profitability criteria with the net present value. International Journal of Production

Economics, 142(1), pp.205-210.

Pompian, M., 2012. Behavioral finance and investor types. Private Wealth Management Feature

Articles, 2012(1), pp.1-3.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.