Investment Decision: NPV, IRR, MIRR, Payback Analysis for Alternatives

VerifiedAdded on 2023/06/15

|9

|1109

|470

Report

AI Summary

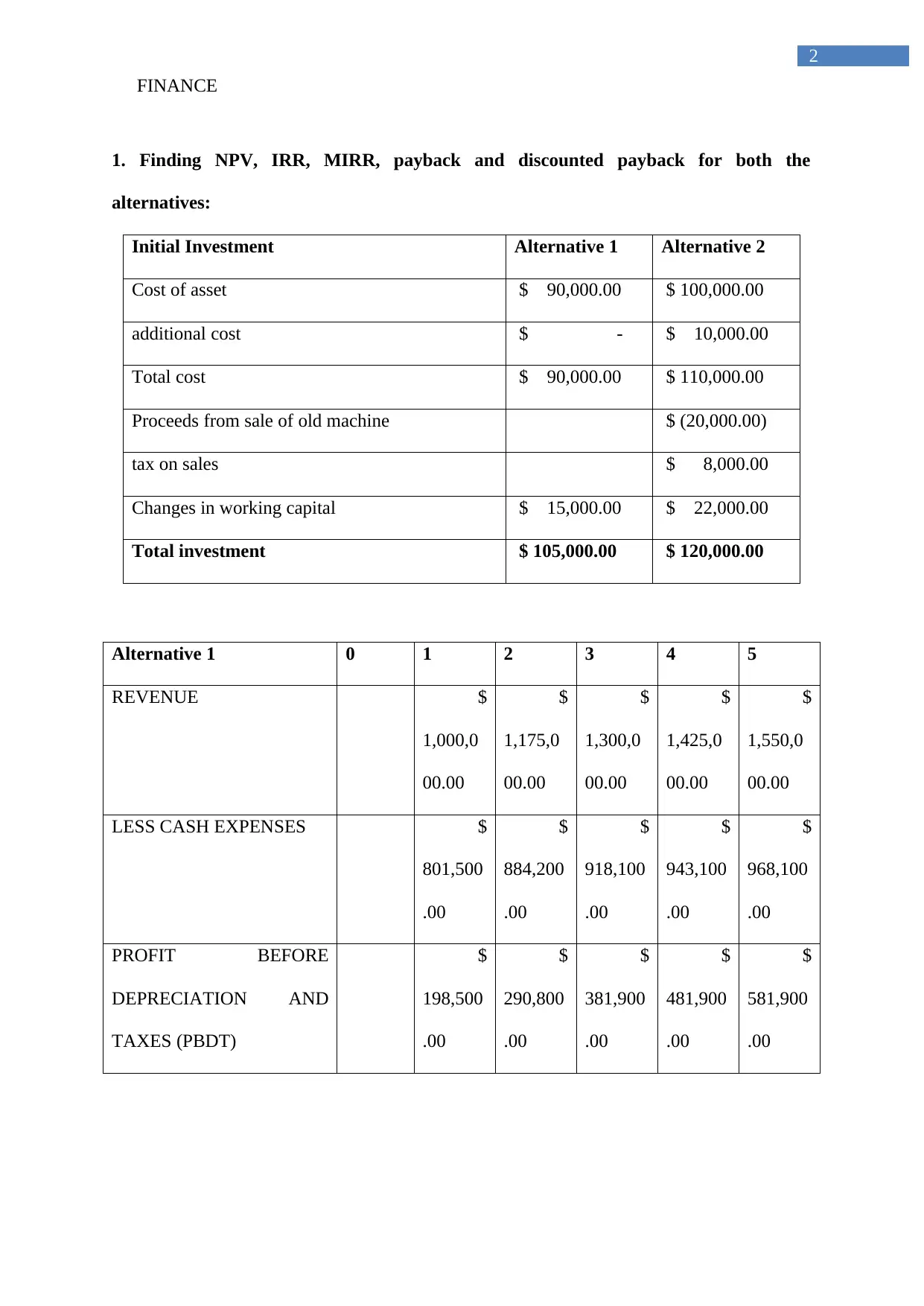

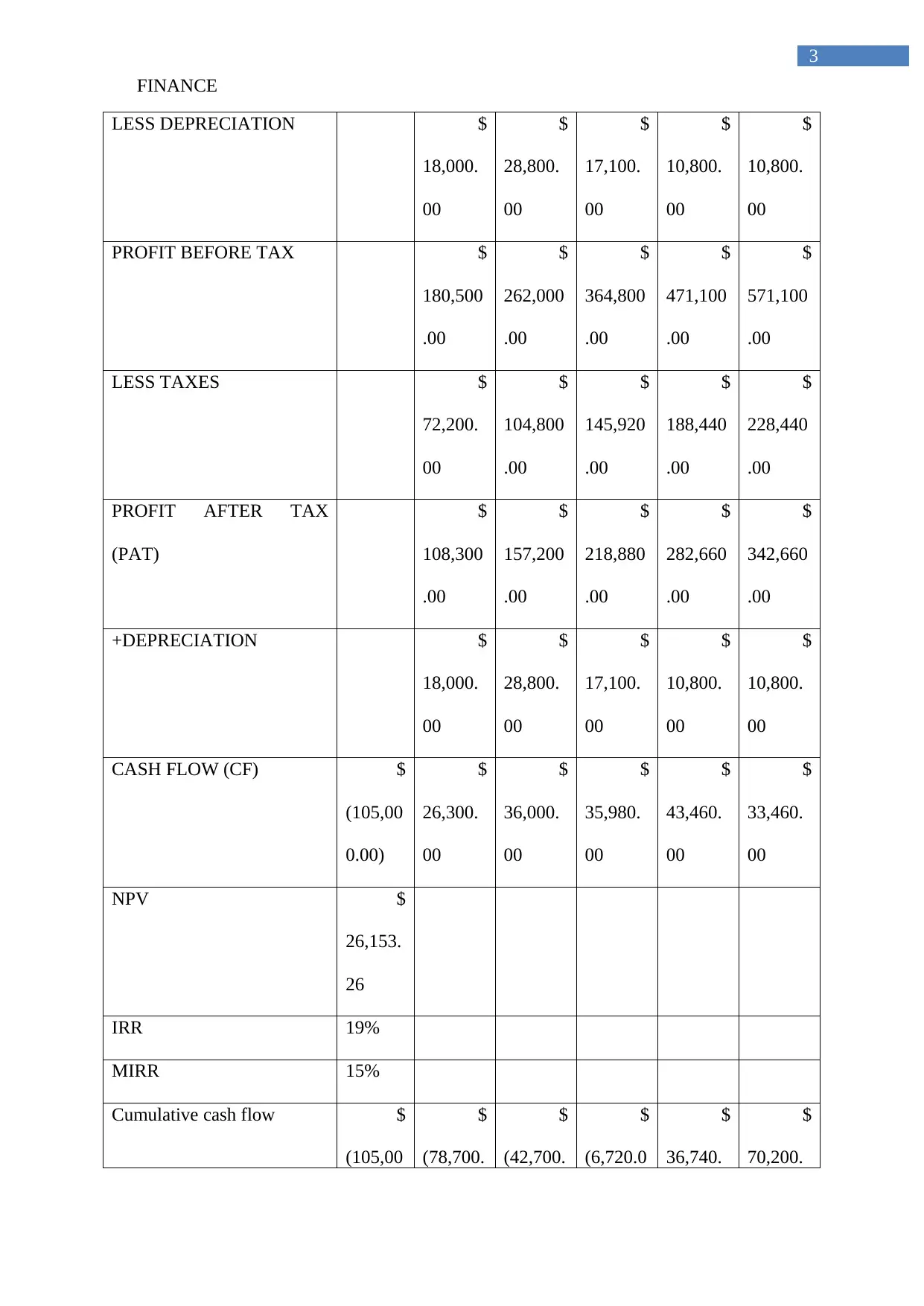

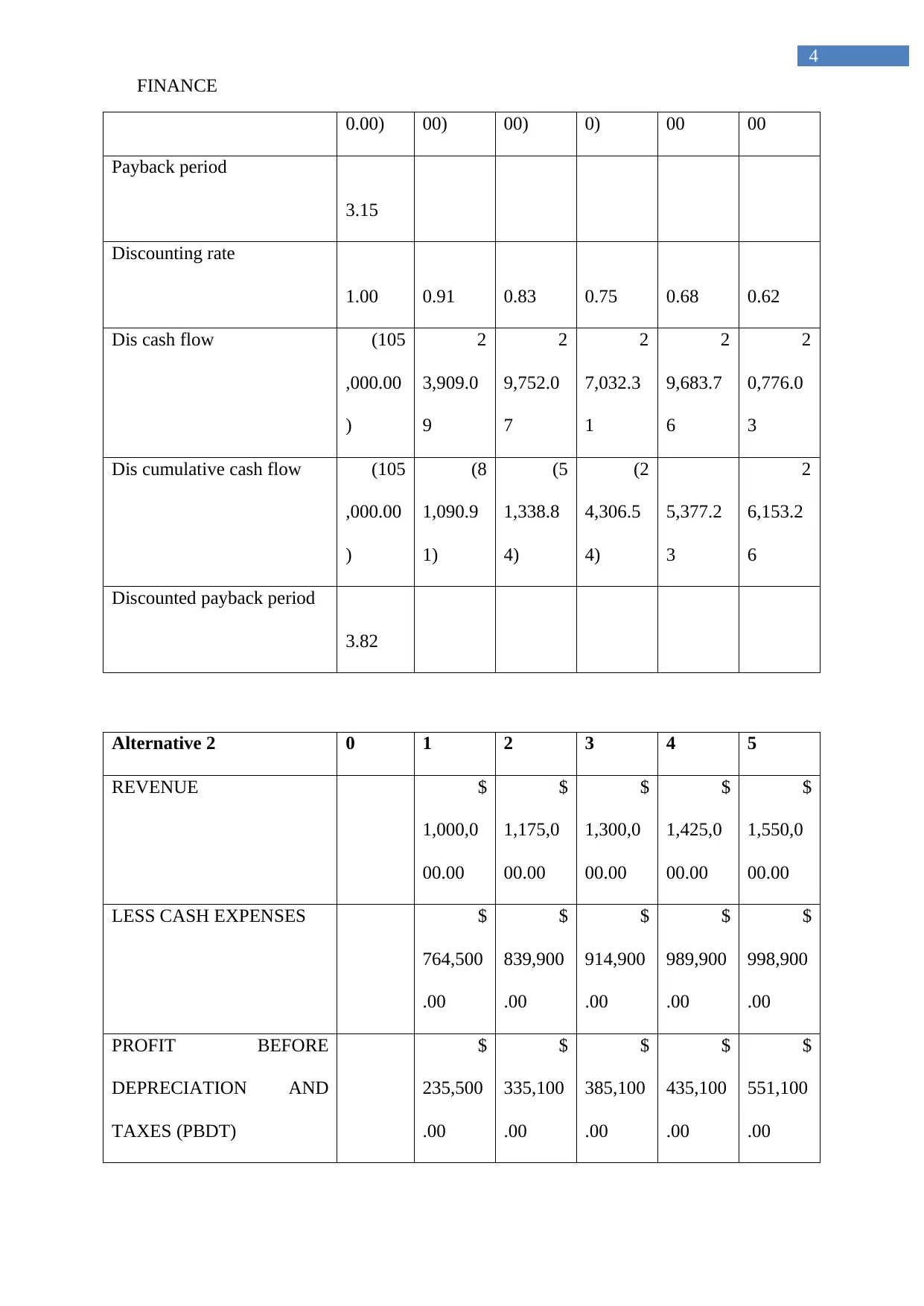

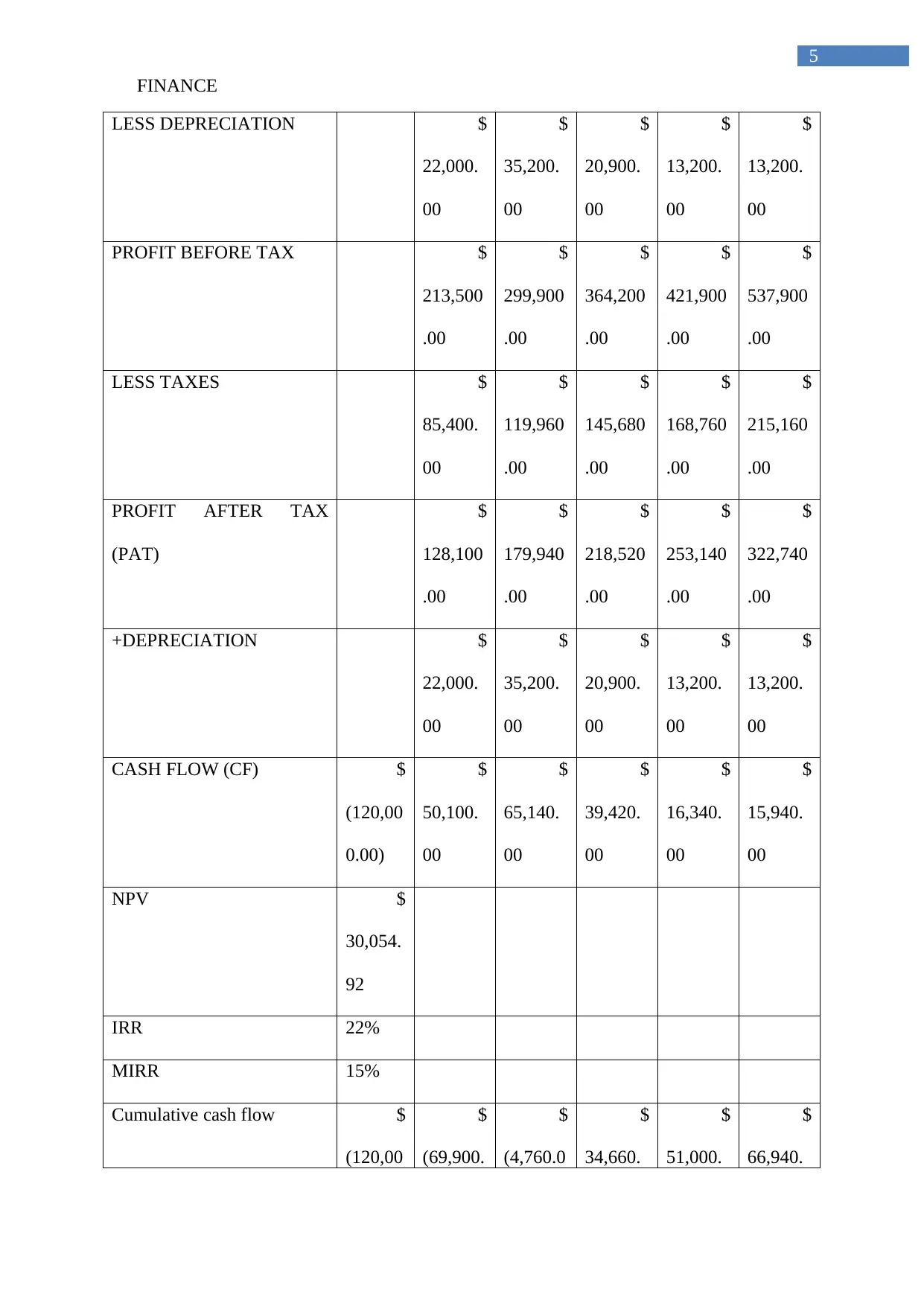

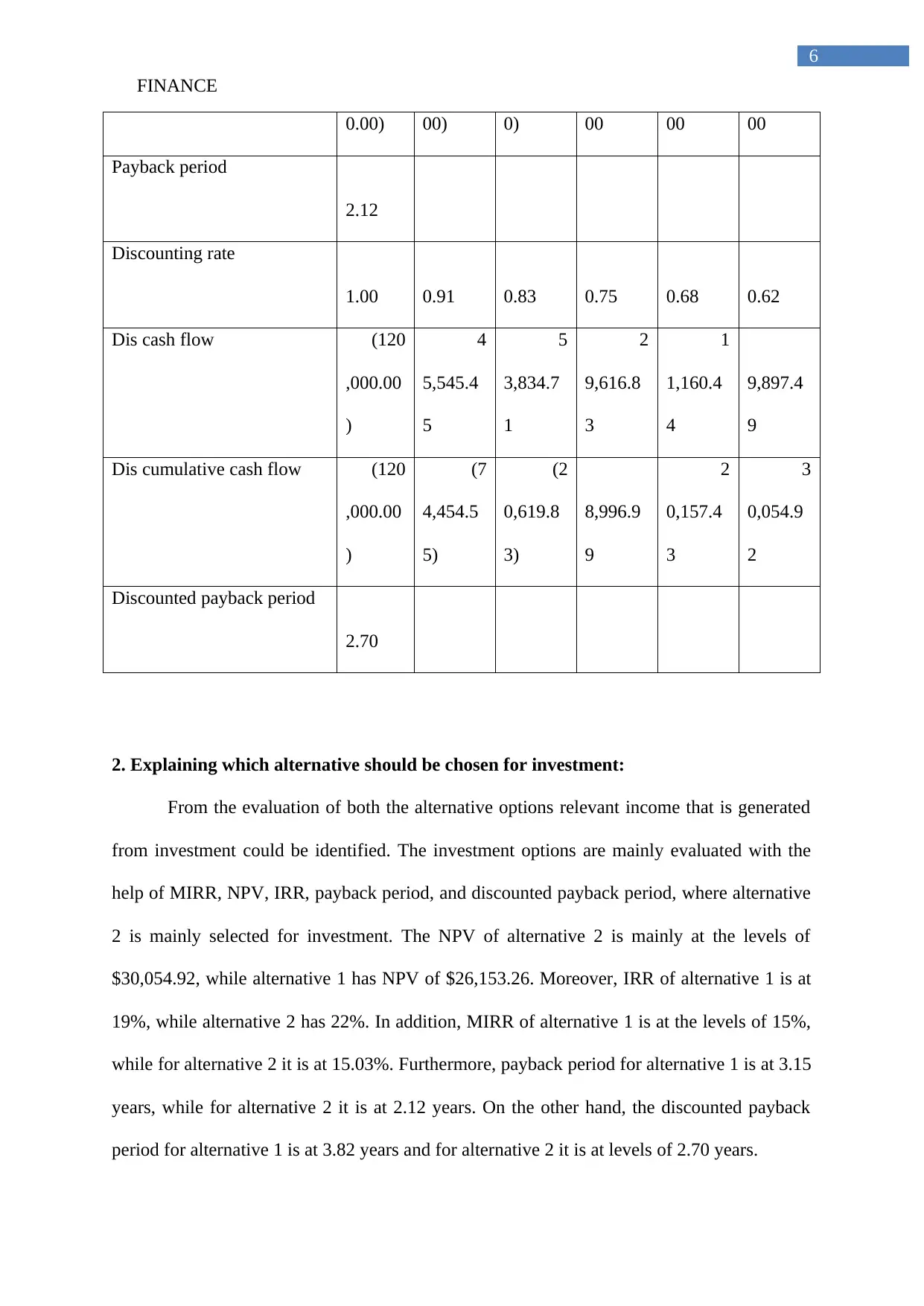

This report provides a detailed financial analysis of two investment alternatives, focusing on calculating and interpreting key metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), Modified Internal Rate of Return (MIRR), payback period, and discounted payback period. The analysis involves projecting revenues, expenses, depreciation, and taxes for each alternative over a five-year period to determine cash flows. The report concludes that Alternative 2 is the more favorable investment option due to its higher NPV ($30,054.92 vs. $26,153.26), higher IRR (22% vs. 19%), and shorter payback periods (2.12 years vs. 3.15 years, and 2.70 years vs 3.82 years for discounted payback). The report recommends that Clark Upholstery Company adopt Alternative 2 to maximize returns and increase revenue, aligning with investment appraisal techniques that support higher profitability.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.