Investment Decisions: NPV, IRR, Bond Valuation & Risk Assessment

VerifiedAdded on 2023/06/17

|17

|3055

|388

Homework Assignment

AI Summary

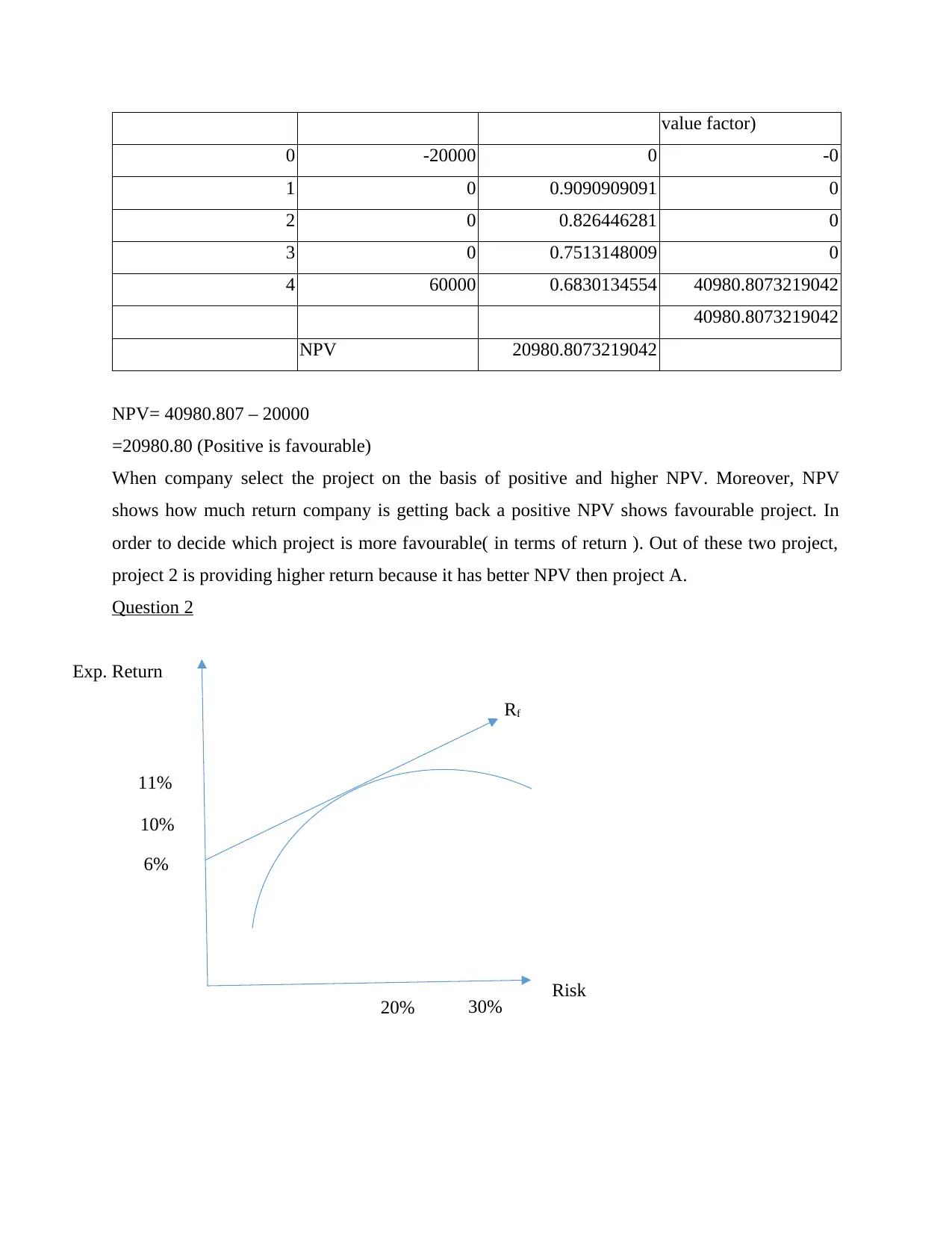

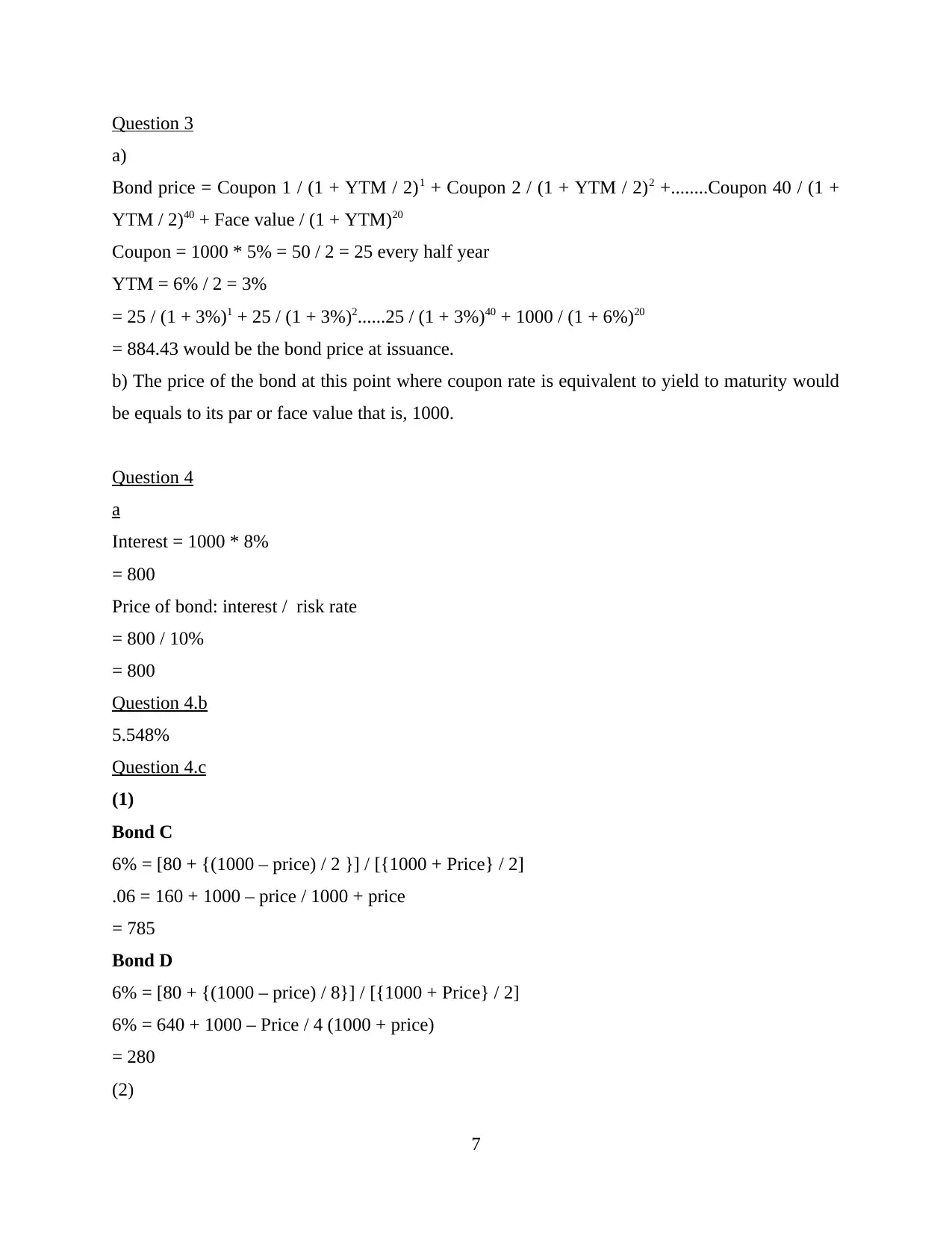

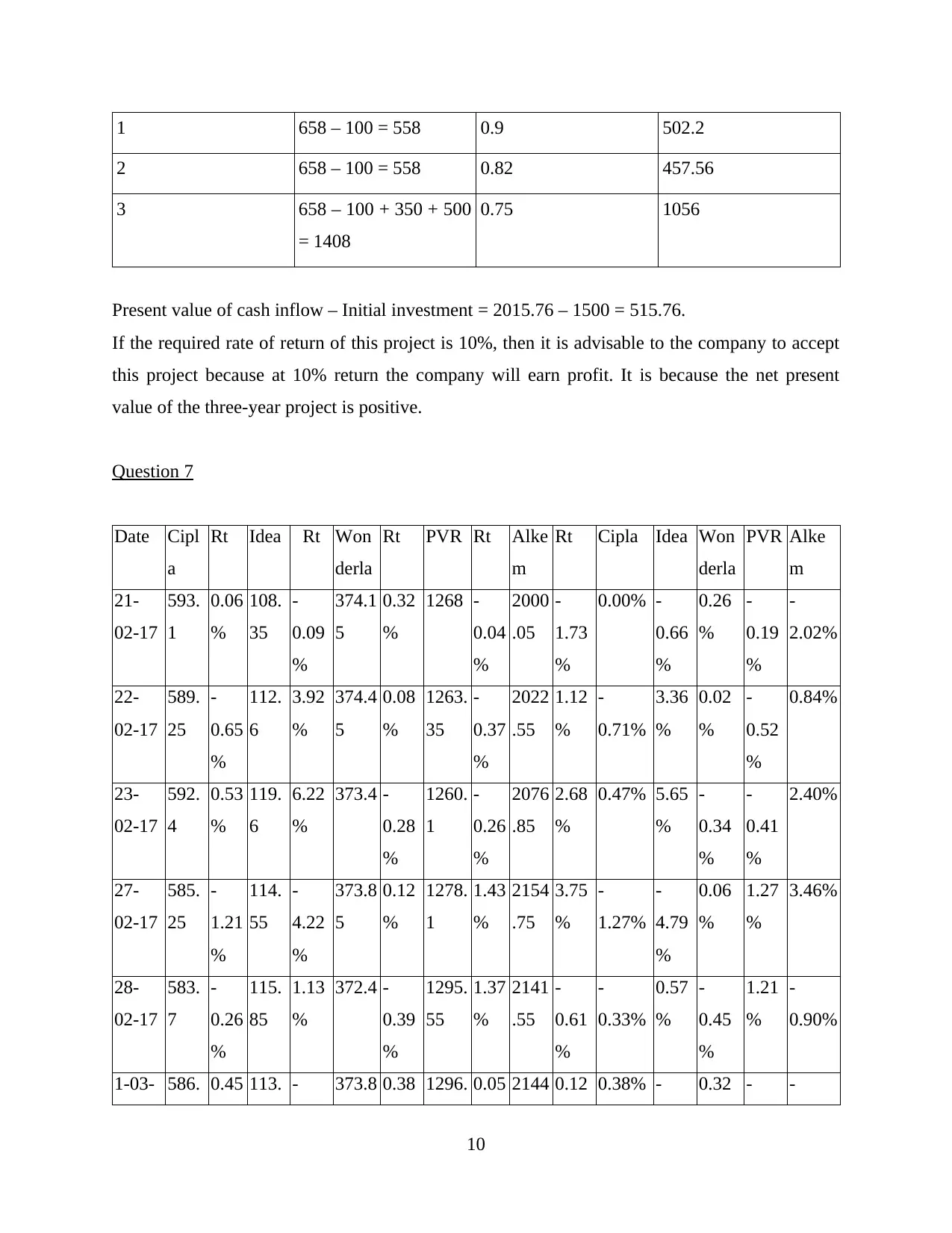

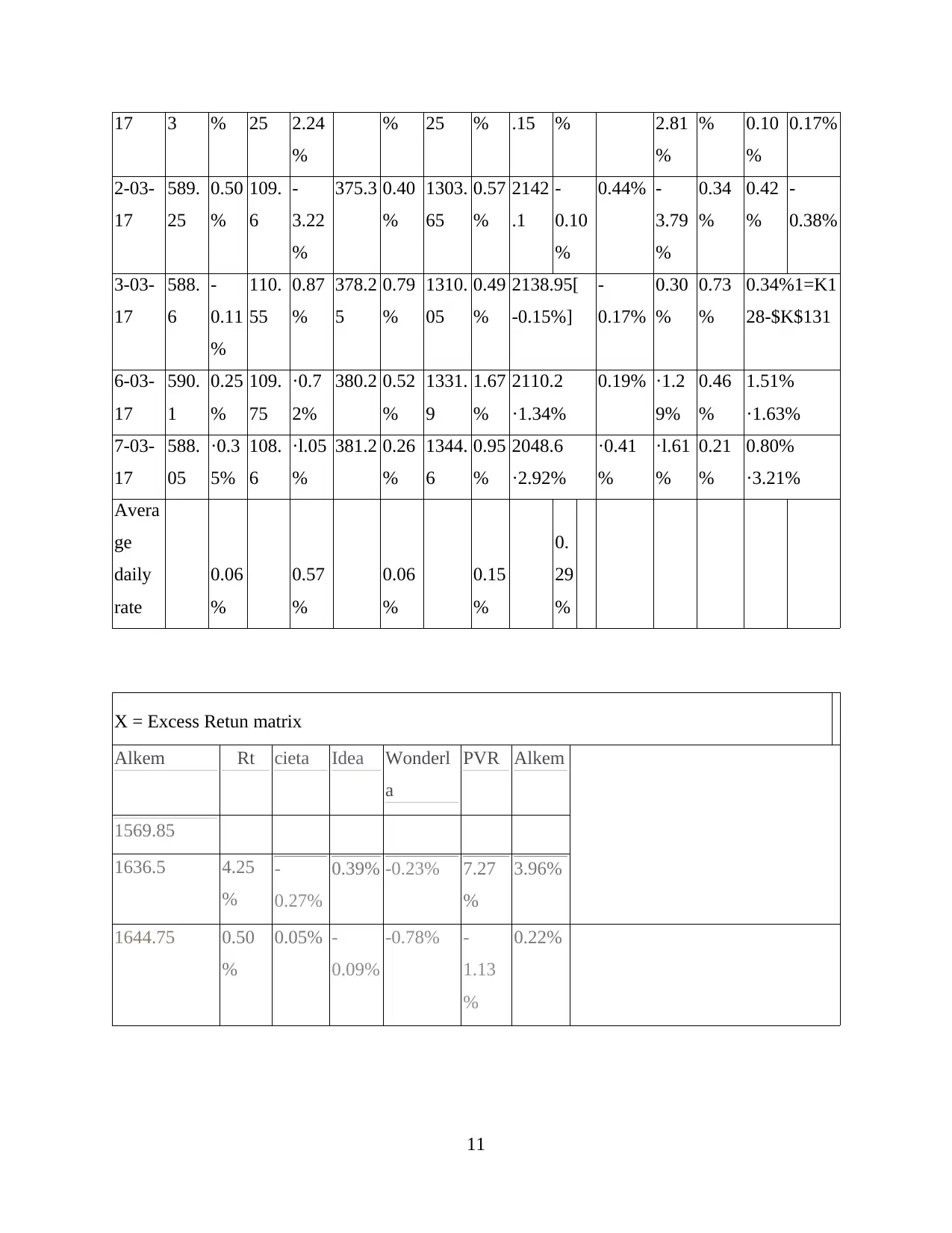

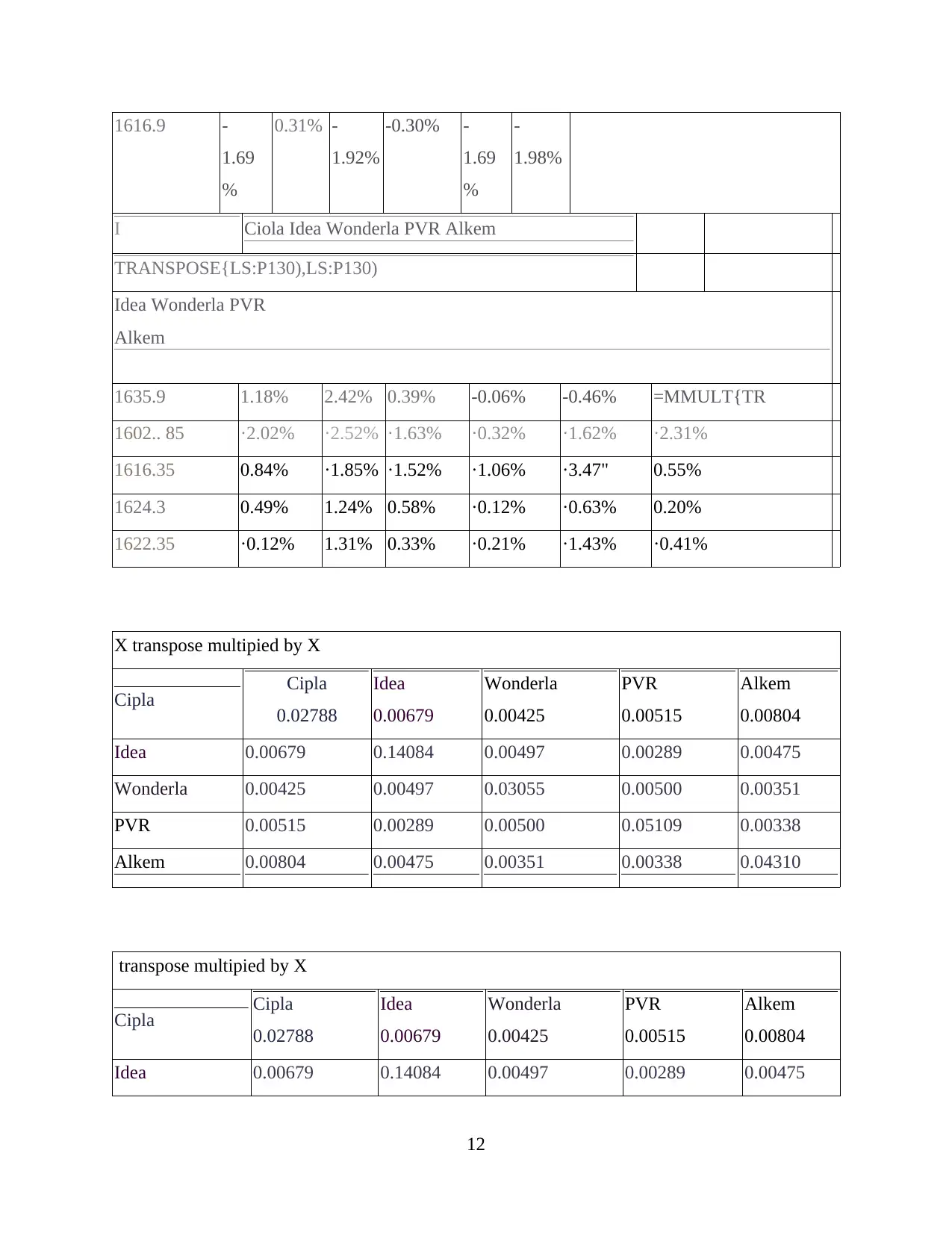

This assignment solution covers key principles of finance, including the calculation of Internal Rate of Return (IRR) and Net Present Value (NPV) for project evaluation. It demonstrates how to calculate IRR by finding the discount rate at which NPV is zero and provides detailed NPV calculations for two projects at a 10% discount rate, determining project favorability based on higher NPV. The assignment also addresses bond valuation, including calculating bond prices at issuance and when coupon rates equal yield to maturity, alongside the impact of yield to maturity on bond value and risk assessment. Further topics include calculating the salvage value of fixed assets, operating cash flow, cash flow from assets, and NPV for a three-year project, alongside analysis of stock returns and calculation of the Weighted Average Cost of Capital (WACC) to determine the viability of a project based on its net cash inflow and present value. Desklib offers this document, contributed by a student, along with other solved assignments and study resources.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.