Capital Structure, Cost of Capital, and Project Evaluation-Finance

VerifiedAdded on 2023/06/08

|12

|2931

|254

Homework Assignment

AI Summary

This assignment provides a detailed solution to a financial management problem involving HighSky Company, focusing on optimizing capital structure and making informed investment decisions. It covers key concepts such as Weighted Average Cost of Capital (WACC), dividend growth model, and internal rate of return (IRR) to evaluate project profitability. The assignment includes computations for cost of equity, break-even points for different capital sources, and analysis of the impact of capital structure changes on earnings per share (EPS). Various methods for computing growth rates and their effect on the cost of equity are also examined. The analysis helps in determining which projects should be accepted based on their IRR relative to the company's WACC, and compares different capital structures to recommend the most suitable one considering profitability, cash flows, and shareholder consent. The document also contains additional questions about indifference points between equity and debt financing, showcasing comprehensive financial analysis techniques. Desklib offers this and similar solved assignments to aid students in their studies.

FINANCIAL MANAGEMENT ASSIGNMENT

Question 1

Answer 1

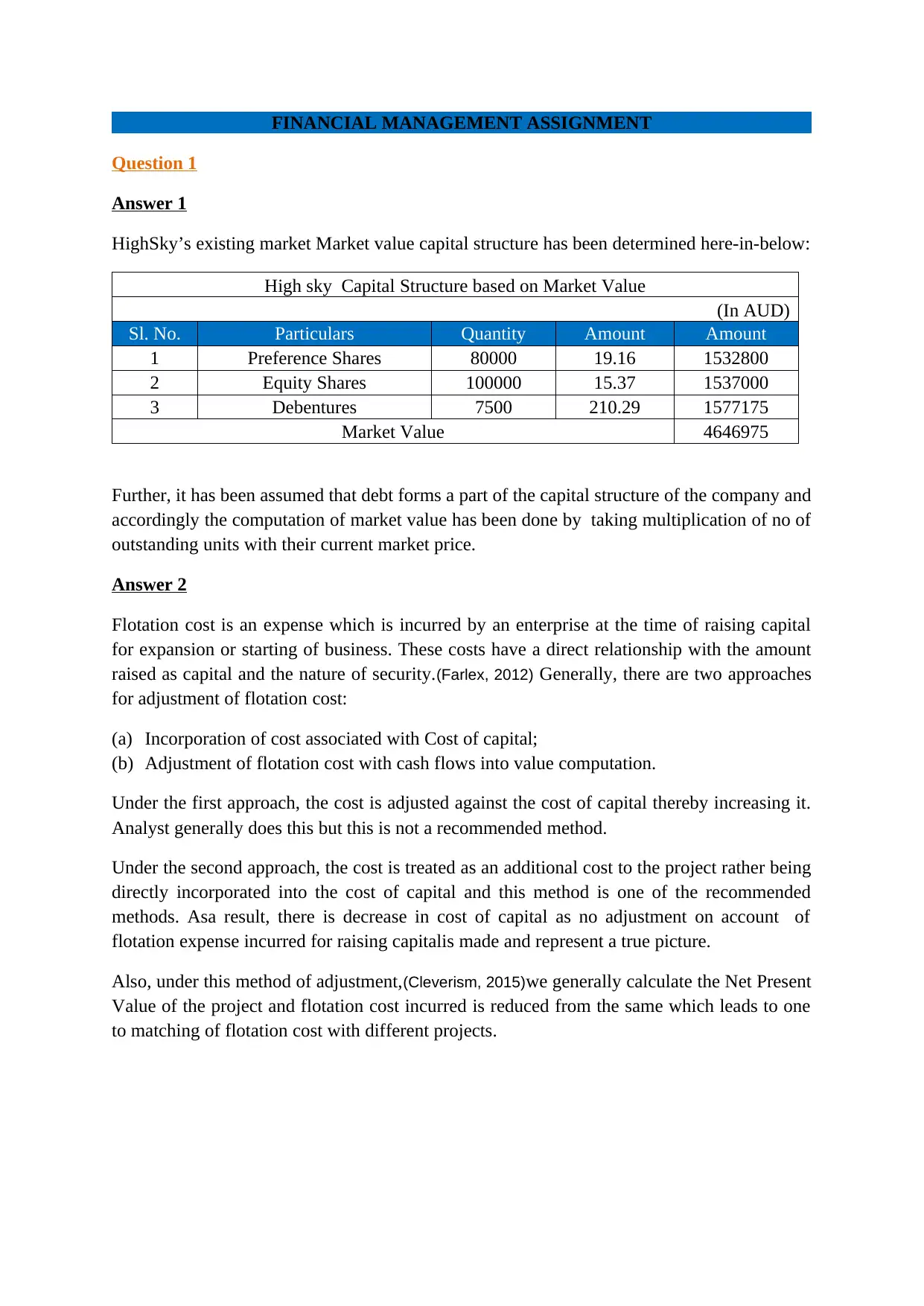

HighSky’s existing market Market value capital structure has been determined here-in-below:

High sky Capital Structure based on Market Value

(In AUD)

Sl. No. Particulars Quantity Amount Amount

1 Preference Shares 80000 19.16 1532800

2 Equity Shares 100000 15.37 1537000

3 Debentures 7500 210.29 1577175

Market Value 4646975

Further, it has been assumed that debt forms a part of the capital structure of the company and

accordingly the computation of market value has been done by taking multiplication of no of

outstanding units with their current market price.

Answer 2

Flotation cost is an expense which is incurred by an enterprise at the time of raising capital

for expansion or starting of business. These costs have a direct relationship with the amount

raised as capital and the nature of security.(Farlex, 2012) Generally, there are two approaches

for adjustment of flotation cost:

(a) Incorporation of cost associated with Cost of capital;

(b) Adjustment of flotation cost with cash flows into value computation.

Under the first approach, the cost is adjusted against the cost of capital thereby increasing it.

Analyst generally does this but this is not a recommended method.

Under the second approach, the cost is treated as an additional cost to the project rather being

directly incorporated into the cost of capital and this method is one of the recommended

methods. Asa result, there is decrease in cost of capital as no adjustment on account of

flotation expense incurred for raising capitalis made and represent a true picture.

Also, under this method of adjustment,(Cleverism, 2015)we generally calculate the Net Present

Value of the project and flotation cost incurred is reduced from the same which leads to one

to matching of flotation cost with different projects.

Question 1

Answer 1

HighSky’s existing market Market value capital structure has been determined here-in-below:

High sky Capital Structure based on Market Value

(In AUD)

Sl. No. Particulars Quantity Amount Amount

1 Preference Shares 80000 19.16 1532800

2 Equity Shares 100000 15.37 1537000

3 Debentures 7500 210.29 1577175

Market Value 4646975

Further, it has been assumed that debt forms a part of the capital structure of the company and

accordingly the computation of market value has been done by taking multiplication of no of

outstanding units with their current market price.

Answer 2

Flotation cost is an expense which is incurred by an enterprise at the time of raising capital

for expansion or starting of business. These costs have a direct relationship with the amount

raised as capital and the nature of security.(Farlex, 2012) Generally, there are two approaches

for adjustment of flotation cost:

(a) Incorporation of cost associated with Cost of capital;

(b) Adjustment of flotation cost with cash flows into value computation.

Under the first approach, the cost is adjusted against the cost of capital thereby increasing it.

Analyst generally does this but this is not a recommended method.

Under the second approach, the cost is treated as an additional cost to the project rather being

directly incorporated into the cost of capital and this method is one of the recommended

methods. Asa result, there is decrease in cost of capital as no adjustment on account of

flotation expense incurred for raising capitalis made and represent a true picture.

Also, under this method of adjustment,(Cleverism, 2015)we generally calculate the Net Present

Value of the project and flotation cost incurred is reduced from the same which leads to one

to matching of flotation cost with different projects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

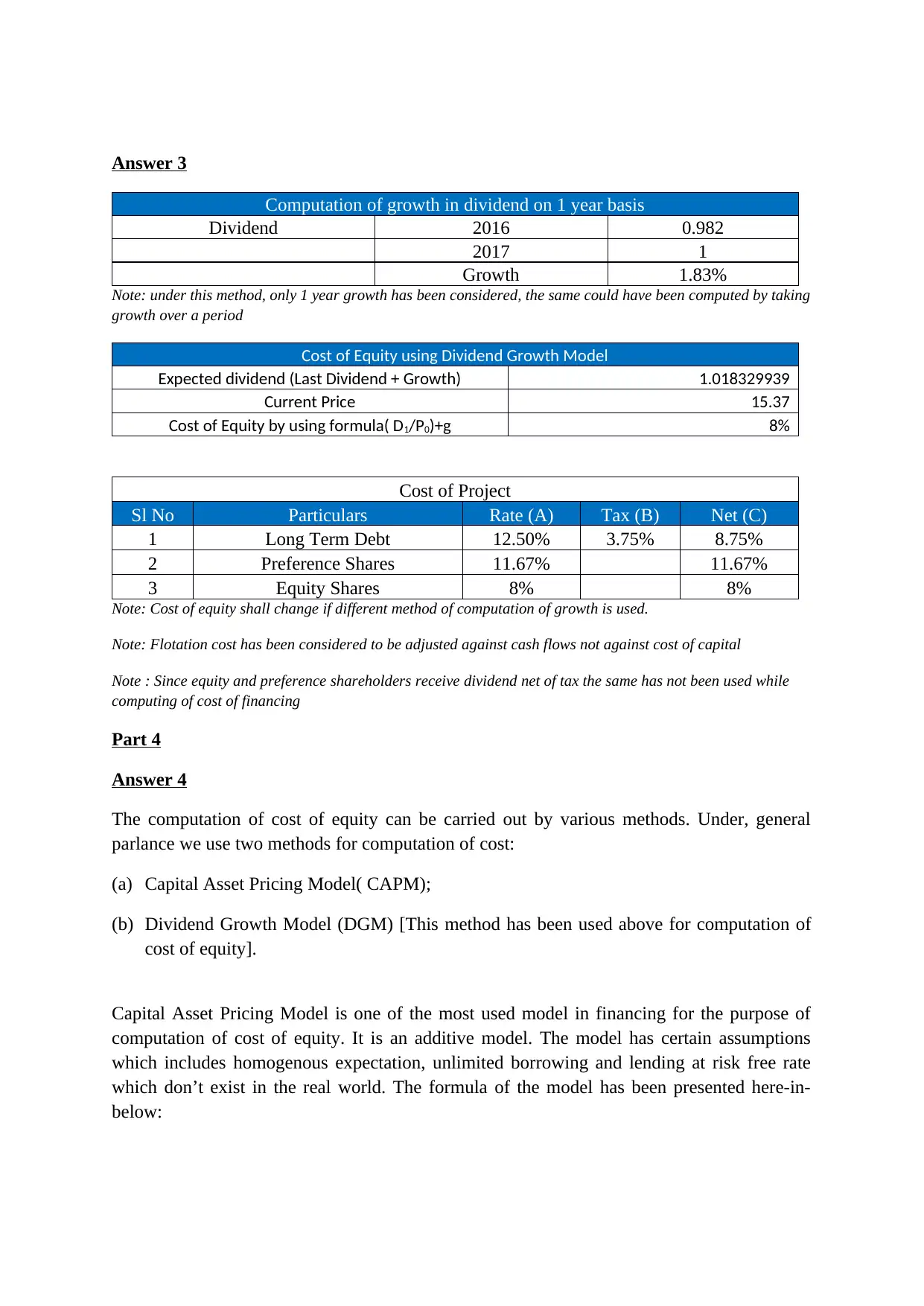

Answer 3

Computation of growth in dividend on 1 year basis

Dividend 2016 0.982

2017 1

Growth 1.83%

Note: under this method, only 1 year growth has been considered, the same could have been computed by taking

growth over a period

Cost of Equity using Dividend Growth Model

Expected dividend (Last Dividend + Growth) 1.018329939

Current Price 15.37

Cost of Equity by using formula( D1/P0)+g 8%

Cost of Project

Sl No Particulars Rate (A) Tax (B) Net (C)

1 Long Term Debt 12.50% 3.75% 8.75%

2 Preference Shares 11.67% 11.67%

3 Equity Shares 8% 8%

Note: Cost of equity shall change if different method of computation of growth is used.

Note: Flotation cost has been considered to be adjusted against cash flows not against cost of capital

Note : Since equity and preference shareholders receive dividend net of tax the same has not been used while

computing of cost of financing

Part 4

Answer 4

The computation of cost of equity can be carried out by various methods. Under, general

parlance we use two methods for computation of cost:

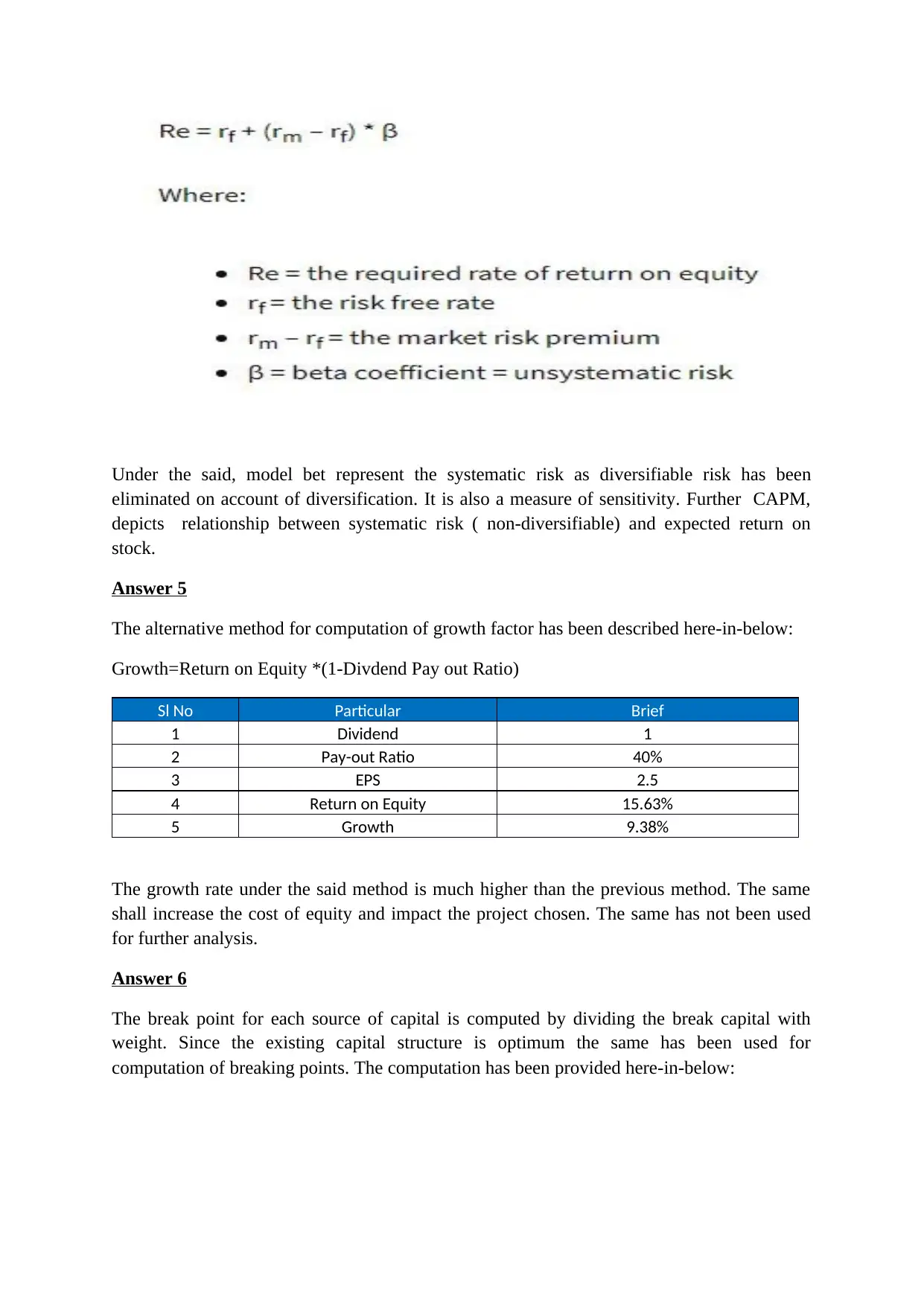

(a) Capital Asset Pricing Model( CAPM);

(b) Dividend Growth Model (DGM) [This method has been used above for computation of

cost of equity].

Capital Asset Pricing Model is one of the most used model in financing for the purpose of

computation of cost of equity. It is an additive model. The model has certain assumptions

which includes homogenous expectation, unlimited borrowing and lending at risk free rate

which don’t exist in the real world. The formula of the model has been presented here-in-

below:

Computation of growth in dividend on 1 year basis

Dividend 2016 0.982

2017 1

Growth 1.83%

Note: under this method, only 1 year growth has been considered, the same could have been computed by taking

growth over a period

Cost of Equity using Dividend Growth Model

Expected dividend (Last Dividend + Growth) 1.018329939

Current Price 15.37

Cost of Equity by using formula( D1/P0)+g 8%

Cost of Project

Sl No Particulars Rate (A) Tax (B) Net (C)

1 Long Term Debt 12.50% 3.75% 8.75%

2 Preference Shares 11.67% 11.67%

3 Equity Shares 8% 8%

Note: Cost of equity shall change if different method of computation of growth is used.

Note: Flotation cost has been considered to be adjusted against cash flows not against cost of capital

Note : Since equity and preference shareholders receive dividend net of tax the same has not been used while

computing of cost of financing

Part 4

Answer 4

The computation of cost of equity can be carried out by various methods. Under, general

parlance we use two methods for computation of cost:

(a) Capital Asset Pricing Model( CAPM);

(b) Dividend Growth Model (DGM) [This method has been used above for computation of

cost of equity].

Capital Asset Pricing Model is one of the most used model in financing for the purpose of

computation of cost of equity. It is an additive model. The model has certain assumptions

which includes homogenous expectation, unlimited borrowing and lending at risk free rate

which don’t exist in the real world. The formula of the model has been presented here-in-

below:

Under the said, model bet represent the systematic risk as diversifiable risk has been

eliminated on account of diversification. It is also a measure of sensitivity. Further CAPM,

depicts relationship between systematic risk ( non-diversifiable) and expected return on

stock.

Answer 5

The alternative method for computation of growth factor has been described here-in-below:

Growth=Return on Equity *(1-Divdend Pay out Ratio)

Sl No Particular Brief

1 Dividend 1

2 Pay-out Ratio 40%

3 EPS 2.5

4 Return on Equity 15.63%

5 Growth 9.38%

The growth rate under the said method is much higher than the previous method. The same

shall increase the cost of equity and impact the project chosen. The same has not been used

for further analysis.

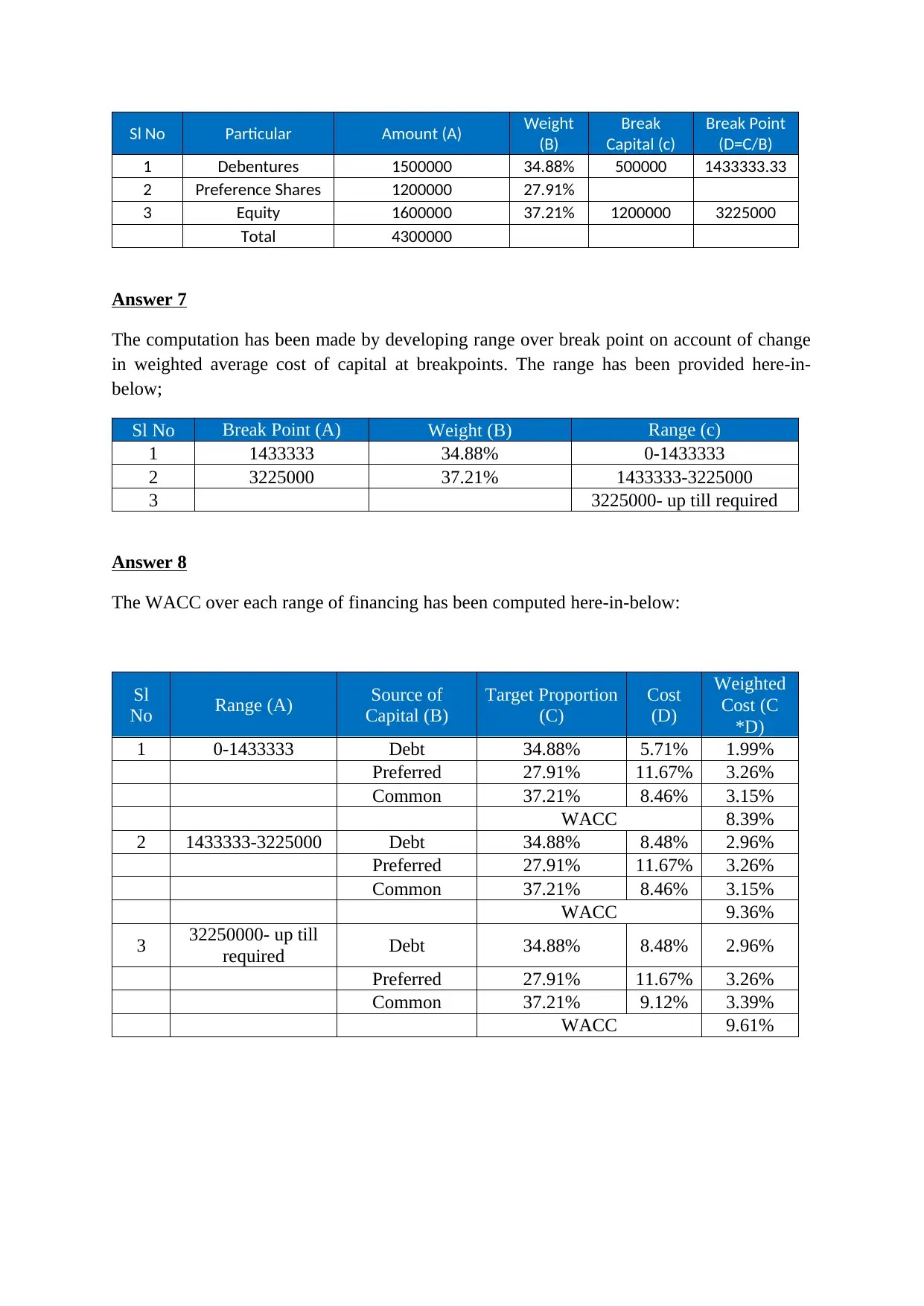

Answer 6

The break point for each source of capital is computed by dividing the break capital with

weight. Since the existing capital structure is optimum the same has been used for

computation of breaking points. The computation has been provided here-in-below:

eliminated on account of diversification. It is also a measure of sensitivity. Further CAPM,

depicts relationship between systematic risk ( non-diversifiable) and expected return on

stock.

Answer 5

The alternative method for computation of growth factor has been described here-in-below:

Growth=Return on Equity *(1-Divdend Pay out Ratio)

Sl No Particular Brief

1 Dividend 1

2 Pay-out Ratio 40%

3 EPS 2.5

4 Return on Equity 15.63%

5 Growth 9.38%

The growth rate under the said method is much higher than the previous method. The same

shall increase the cost of equity and impact the project chosen. The same has not been used

for further analysis.

Answer 6

The break point for each source of capital is computed by dividing the break capital with

weight. Since the existing capital structure is optimum the same has been used for

computation of breaking points. The computation has been provided here-in-below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sl No Particular Amount (A) Weight

(B)

Break

Capital (c)

Break Point

(D=C/B)

1 Debentures 1500000 34.88% 500000 1433333.33

2 Preference Shares 1200000 27.91%

3 Equity 1600000 37.21% 1200000 3225000

Total 4300000

Answer 7

The computation has been made by developing range over break point on account of change

in weighted average cost of capital at breakpoints. The range has been provided here-in-

below;

Sl No Break Point (A) Weight (B) Range (c)

1 1433333 34.88% 0-1433333

2 3225000 37.21% 1433333-3225000

3 3225000- up till required

Answer 8

The WACC over each range of financing has been computed here-in-below:

Sl

No Range (A) Source of

Capital (B)

Target Proportion

(C)

Cost

(D)

Weighted

Cost (C

*D)

1 0-1433333 Debt 34.88% 5.71% 1.99%

Preferred 27.91% 11.67% 3.26%

Common 37.21% 8.46% 3.15%

WACC 8.39%

2 1433333-3225000 Debt 34.88% 8.48% 2.96%

Preferred 27.91% 11.67% 3.26%

Common 37.21% 8.46% 3.15%

WACC 9.36%

3 32250000- up till

required Debt 34.88% 8.48% 2.96%

Preferred 27.91% 11.67% 3.26%

Common 37.21% 9.12% 3.39%

WACC 9.61%

(B)

Break

Capital (c)

Break Point

(D=C/B)

1 Debentures 1500000 34.88% 500000 1433333.33

2 Preference Shares 1200000 27.91%

3 Equity 1600000 37.21% 1200000 3225000

Total 4300000

Answer 7

The computation has been made by developing range over break point on account of change

in weighted average cost of capital at breakpoints. The range has been provided here-in-

below;

Sl No Break Point (A) Weight (B) Range (c)

1 1433333 34.88% 0-1433333

2 3225000 37.21% 1433333-3225000

3 3225000- up till required

Answer 8

The WACC over each range of financing has been computed here-in-below:

Sl

No Range (A) Source of

Capital (B)

Target Proportion

(C)

Cost

(D)

Weighted

Cost (C

*D)

1 0-1433333 Debt 34.88% 5.71% 1.99%

Preferred 27.91% 11.67% 3.26%

Common 37.21% 8.46% 3.15%

WACC 8.39%

2 1433333-3225000 Debt 34.88% 8.48% 2.96%

Preferred 27.91% 11.67% 3.26%

Common 37.21% 8.46% 3.15%

WACC 9.36%

3 32250000- up till

required Debt 34.88% 8.48% 2.96%

Preferred 27.91% 11.67% 3.26%

Common 37.21% 9.12% 3.39%

WACC 9.61%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

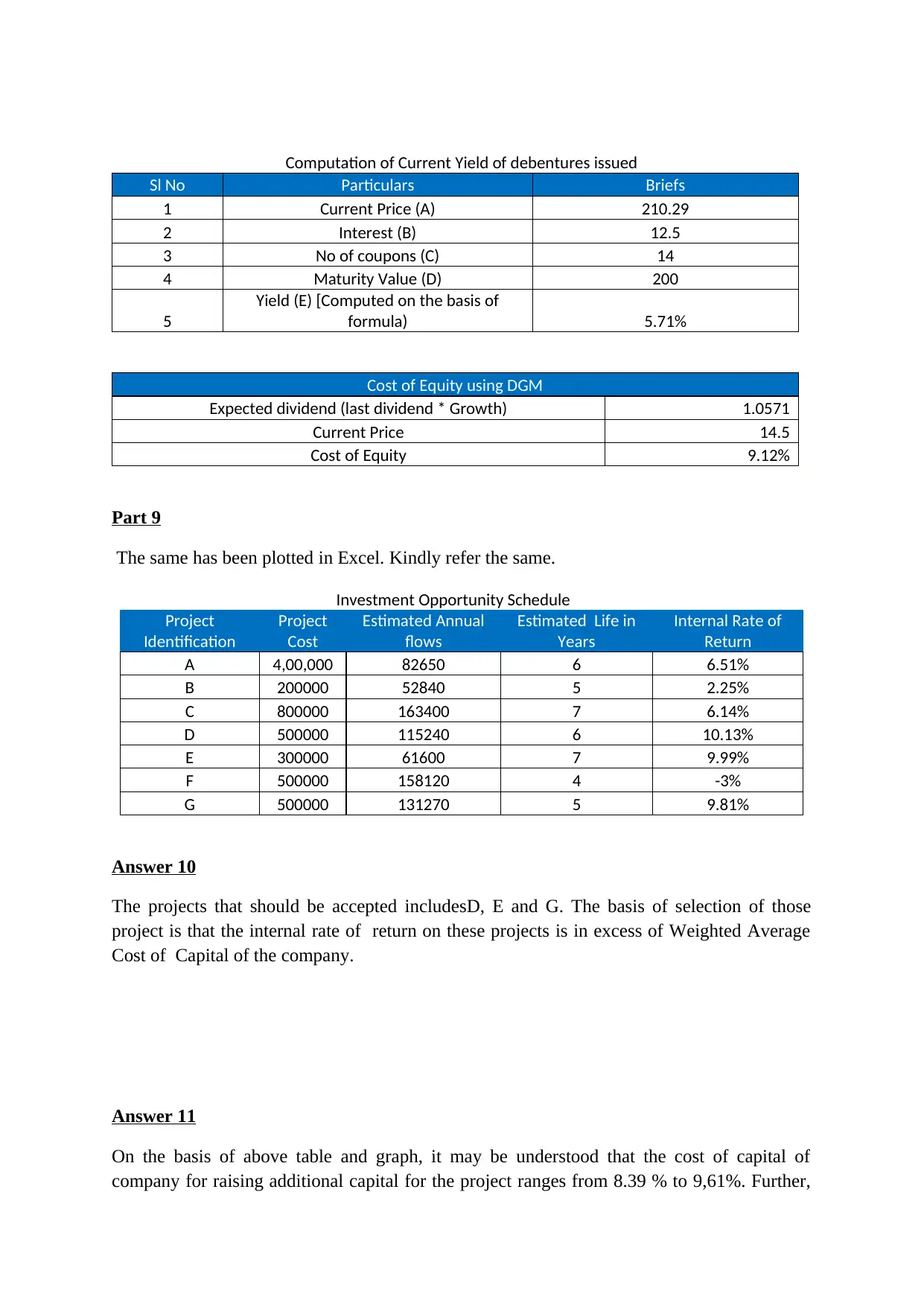

Computation of Current Yield of debentures issued

Sl No Particulars Briefs

1 Current Price (A) 210.29

2 Interest (B) 12.5

3 No of coupons (C) 14

4 Maturity Value (D) 200

5

Yield (E) [Computed on the basis of

formula) 5.71%

Cost of Equity using DGM

Expected dividend (last dividend * Growth) 1.0571

Current Price 14.5

Cost of Equity 9.12%

Part 9

The same has been plotted in Excel. Kindly refer the same.

Investment Opportunity Schedule

Project

Identification

Project

Cost

Estimated Annual

flows

Estimated Life in

Years

Internal Rate of

Return

A 4,00,000 82650 6 6.51%

B 200000 52840 5 2.25%

C 800000 163400 7 6.14%

D 500000 115240 6 10.13%

E 300000 61600 7 9.99%

F 500000 158120 4 -3%

G 500000 131270 5 9.81%

Answer 10

The projects that should be accepted includesD, E and G. The basis of selection of those

project is that the internal rate of return on these projects is in excess of Weighted Average

Cost of Capital of the company.

Answer 11

On the basis of above table and graph, it may be understood that the cost of capital of

company for raising additional capital for the project ranges from 8.39 % to 9,61%. Further,

Sl No Particulars Briefs

1 Current Price (A) 210.29

2 Interest (B) 12.5

3 No of coupons (C) 14

4 Maturity Value (D) 200

5

Yield (E) [Computed on the basis of

formula) 5.71%

Cost of Equity using DGM

Expected dividend (last dividend * Growth) 1.0571

Current Price 14.5

Cost of Equity 9.12%

Part 9

The same has been plotted in Excel. Kindly refer the same.

Investment Opportunity Schedule

Project

Identification

Project

Cost

Estimated Annual

flows

Estimated Life in

Years

Internal Rate of

Return

A 4,00,000 82650 6 6.51%

B 200000 52840 5 2.25%

C 800000 163400 7 6.14%

D 500000 115240 6 10.13%

E 300000 61600 7 9.99%

F 500000 158120 4 -3%

G 500000 131270 5 9.81%

Answer 10

The projects that should be accepted includesD, E and G. The basis of selection of those

project is that the internal rate of return on these projects is in excess of Weighted Average

Cost of Capital of the company.

Answer 11

On the basis of above table and graph, it may be understood that the cost of capital of

company for raising additional capital for the project ranges from 8.39 % to 9,61%. Further,

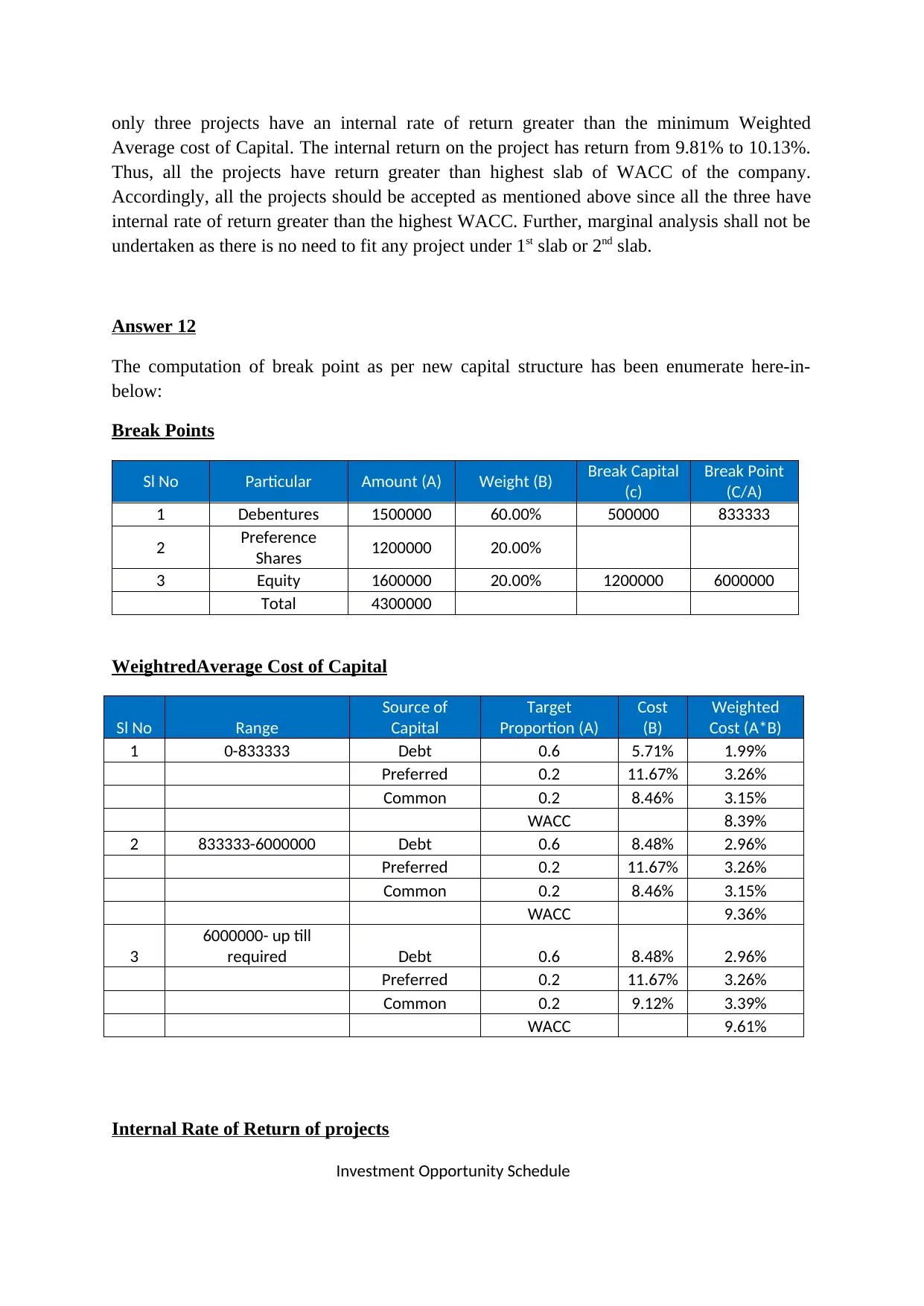

only three projects have an internal rate of return greater than the minimum Weighted

Average cost of Capital. The internal return on the project has return from 9.81% to 10.13%.

Thus, all the projects have return greater than highest slab of WACC of the company.

Accordingly, all the projects should be accepted as mentioned above since all the three have

internal rate of return greater than the highest WACC. Further, marginal analysis shall not be

undertaken as there is no need to fit any project under 1st slab or 2nd slab.

Answer 12

The computation of break point as per new capital structure has been enumerate here-in-

below:

Break Points

Sl No Particular Amount (A) Weight (B) Break Capital

(c)

Break Point

(C/A)

1 Debentures 1500000 60.00% 500000 833333

2 Preference

Shares 1200000 20.00%

3 Equity 1600000 20.00% 1200000 6000000

Total 4300000

WeightredAverage Cost of Capital

Sl No Range

Source of

Capital

Target

Proportion (A)

Cost

(B)

Weighted

Cost (A*B)

1 0-833333 Debt 0.6 5.71% 1.99%

Preferred 0.2 11.67% 3.26%

Common 0.2 8.46% 3.15%

WACC 8.39%

2 833333-6000000 Debt 0.6 8.48% 2.96%

Preferred 0.2 11.67% 3.26%

Common 0.2 8.46% 3.15%

WACC 9.36%

3

6000000- up till

required Debt 0.6 8.48% 2.96%

Preferred 0.2 11.67% 3.26%

Common 0.2 9.12% 3.39%

WACC 9.61%

Internal Rate of Return of projects

Investment Opportunity Schedule

Average cost of Capital. The internal return on the project has return from 9.81% to 10.13%.

Thus, all the projects have return greater than highest slab of WACC of the company.

Accordingly, all the projects should be accepted as mentioned above since all the three have

internal rate of return greater than the highest WACC. Further, marginal analysis shall not be

undertaken as there is no need to fit any project under 1st slab or 2nd slab.

Answer 12

The computation of break point as per new capital structure has been enumerate here-in-

below:

Break Points

Sl No Particular Amount (A) Weight (B) Break Capital

(c)

Break Point

(C/A)

1 Debentures 1500000 60.00% 500000 833333

2 Preference

Shares 1200000 20.00%

3 Equity 1600000 20.00% 1200000 6000000

Total 4300000

WeightredAverage Cost of Capital

Sl No Range

Source of

Capital

Target

Proportion (A)

Cost

(B)

Weighted

Cost (A*B)

1 0-833333 Debt 0.6 5.71% 1.99%

Preferred 0.2 11.67% 3.26%

Common 0.2 8.46% 3.15%

WACC 8.39%

2 833333-6000000 Debt 0.6 8.48% 2.96%

Preferred 0.2 11.67% 3.26%

Common 0.2 8.46% 3.15%

WACC 9.36%

3

6000000- up till

required Debt 0.6 8.48% 2.96%

Preferred 0.2 11.67% 3.26%

Common 0.2 9.12% 3.39%

WACC 9.61%

Internal Rate of Return of projects

Investment Opportunity Schedule

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

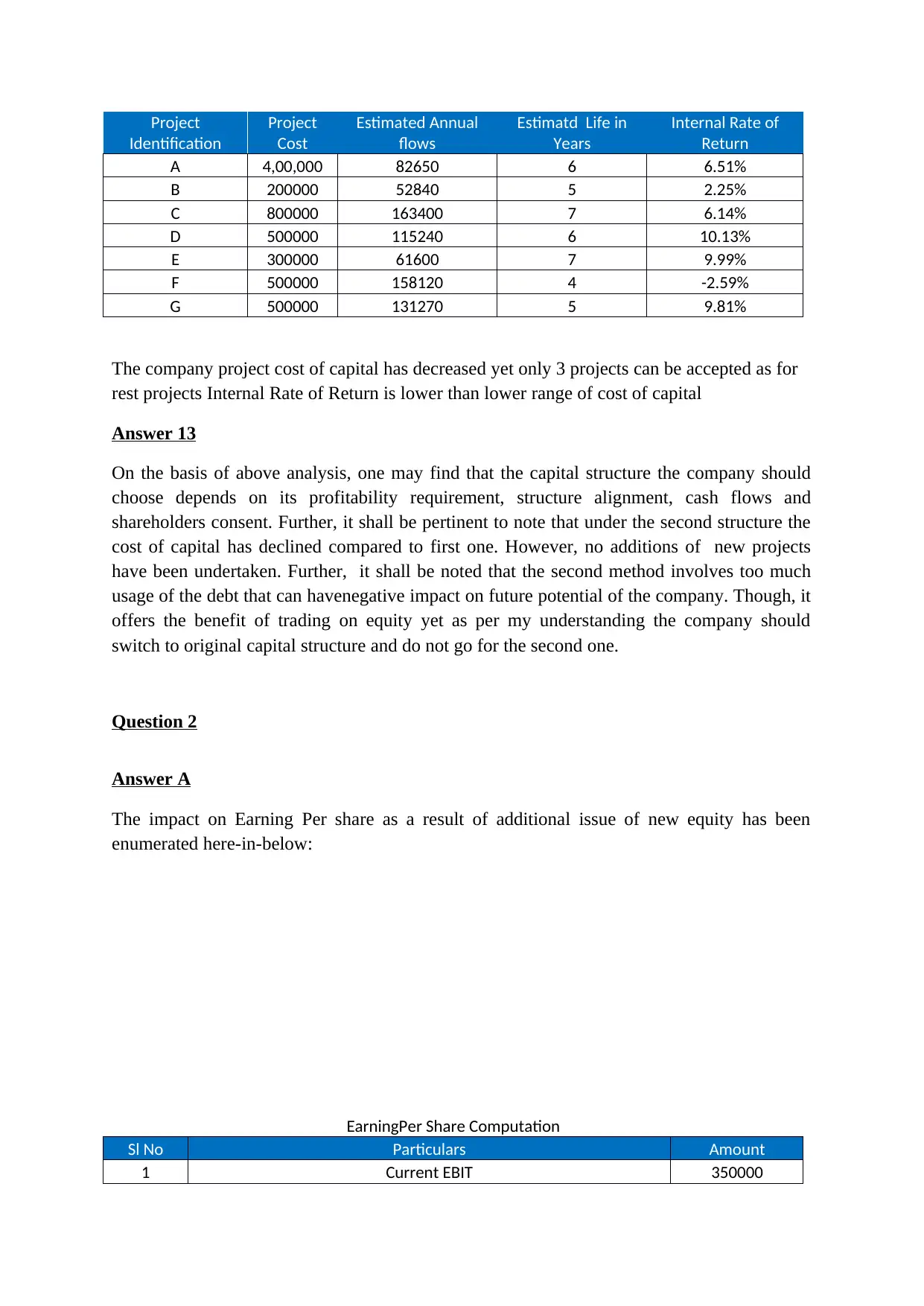

Project

Identification

Project

Cost

Estimated Annual

flows

Estimatd Life in

Years

Internal Rate of

Return

A 4,00,000 82650 6 6.51%

B 200000 52840 5 2.25%

C 800000 163400 7 6.14%

D 500000 115240 6 10.13%

E 300000 61600 7 9.99%

F 500000 158120 4 -2.59%

G 500000 131270 5 9.81%

The company project cost of capital has decreased yet only 3 projects can be accepted as for

rest projects Internal Rate of Return is lower than lower range of cost of capital

Answer 13

On the basis of above analysis, one may find that the capital structure the company should

choose depends on its profitability requirement, structure alignment, cash flows and

shareholders consent. Further, it shall be pertinent to note that under the second structure the

cost of capital has declined compared to first one. However, no additions of new projects

have been undertaken. Further, it shall be noted that the second method involves too much

usage of the debt that can havenegative impact on future potential of the company. Though, it

offers the benefit of trading on equity yet as per my understanding the company should

switch to original capital structure and do not go for the second one.

Question 2

Answer A

The impact on Earning Per share as a result of additional issue of new equity has been

enumerated here-in-below:

EarningPer Share Computation

Sl No Particulars Amount

1 Current EBIT 350000

Identification

Project

Cost

Estimated Annual

flows

Estimatd Life in

Years

Internal Rate of

Return

A 4,00,000 82650 6 6.51%

B 200000 52840 5 2.25%

C 800000 163400 7 6.14%

D 500000 115240 6 10.13%

E 300000 61600 7 9.99%

F 500000 158120 4 -2.59%

G 500000 131270 5 9.81%

The company project cost of capital has decreased yet only 3 projects can be accepted as for

rest projects Internal Rate of Return is lower than lower range of cost of capital

Answer 13

On the basis of above analysis, one may find that the capital structure the company should

choose depends on its profitability requirement, structure alignment, cash flows and

shareholders consent. Further, it shall be pertinent to note that under the second structure the

cost of capital has declined compared to first one. However, no additions of new projects

have been undertaken. Further, it shall be noted that the second method involves too much

usage of the debt that can havenegative impact on future potential of the company. Though, it

offers the benefit of trading on equity yet as per my understanding the company should

switch to original capital structure and do not go for the second one.

Question 2

Answer A

The impact on Earning Per share as a result of additional issue of new equity has been

enumerated here-in-below:

EarningPer Share Computation

Sl No Particulars Amount

1 Current EBIT 350000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

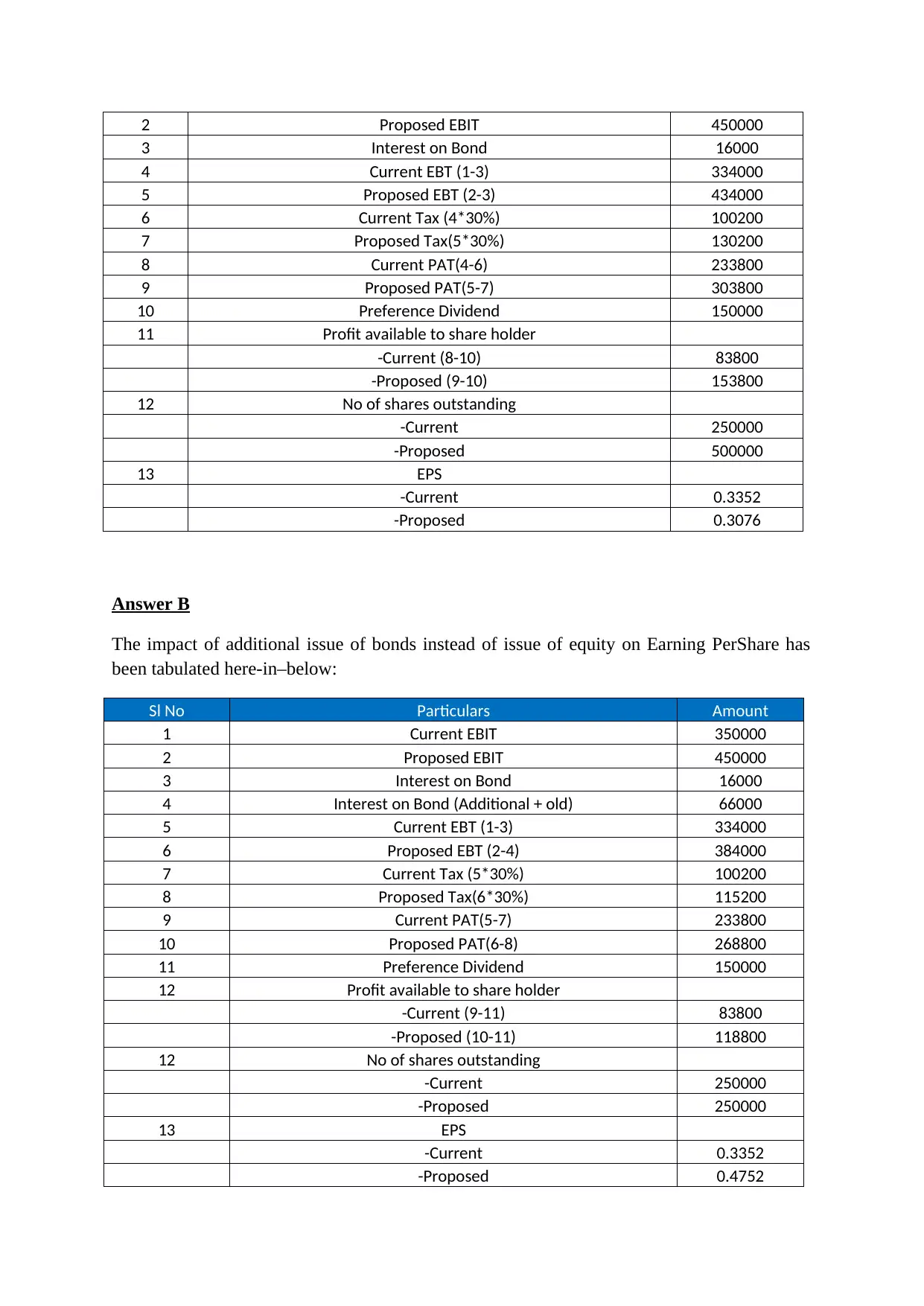

2 Proposed EBIT 450000

3 Interest on Bond 16000

4 Current EBT (1-3) 334000

5 Proposed EBT (2-3) 434000

6 Current Tax (4*30%) 100200

7 Proposed Tax(5*30%) 130200

8 Current PAT(4-6) 233800

9 Proposed PAT(5-7) 303800

10 Preference Dividend 150000

11 Profit available to share holder

-Current (8-10) 83800

-Proposed (9-10) 153800

12 No of shares outstanding

-Current 250000

-Proposed 500000

13 EPS

-Current 0.3352

-Proposed 0.3076

Answer B

The impact of additional issue of bonds instead of issue of equity on Earning PerShare has

been tabulated here-in–below:

Sl No Particulars Amount

1 Current EBIT 350000

2 Proposed EBIT 450000

3 Interest on Bond 16000

4 Interest on Bond (Additional + old) 66000

5 Current EBT (1-3) 334000

6 Proposed EBT (2-4) 384000

7 Current Tax (5*30%) 100200

8 Proposed Tax(6*30%) 115200

9 Current PAT(5-7) 233800

10 Proposed PAT(6-8) 268800

11 Preference Dividend 150000

12 Profit available to share holder

-Current (9-11) 83800

-Proposed (10-11) 118800

12 No of shares outstanding

-Current 250000

-Proposed 250000

13 EPS

-Current 0.3352

-Proposed 0.4752

3 Interest on Bond 16000

4 Current EBT (1-3) 334000

5 Proposed EBT (2-3) 434000

6 Current Tax (4*30%) 100200

7 Proposed Tax(5*30%) 130200

8 Current PAT(4-6) 233800

9 Proposed PAT(5-7) 303800

10 Preference Dividend 150000

11 Profit available to share holder

-Current (8-10) 83800

-Proposed (9-10) 153800

12 No of shares outstanding

-Current 250000

-Proposed 500000

13 EPS

-Current 0.3352

-Proposed 0.3076

Answer B

The impact of additional issue of bonds instead of issue of equity on Earning PerShare has

been tabulated here-in–below:

Sl No Particulars Amount

1 Current EBIT 350000

2 Proposed EBIT 450000

3 Interest on Bond 16000

4 Interest on Bond (Additional + old) 66000

5 Current EBT (1-3) 334000

6 Proposed EBT (2-4) 384000

7 Current Tax (5*30%) 100200

8 Proposed Tax(6*30%) 115200

9 Current PAT(5-7) 233800

10 Proposed PAT(6-8) 268800

11 Preference Dividend 150000

12 Profit available to share holder

-Current (9-11) 83800

-Proposed (10-11) 118800

12 No of shares outstanding

-Current 250000

-Proposed 250000

13 EPS

-Current 0.3352

-Proposed 0.4752

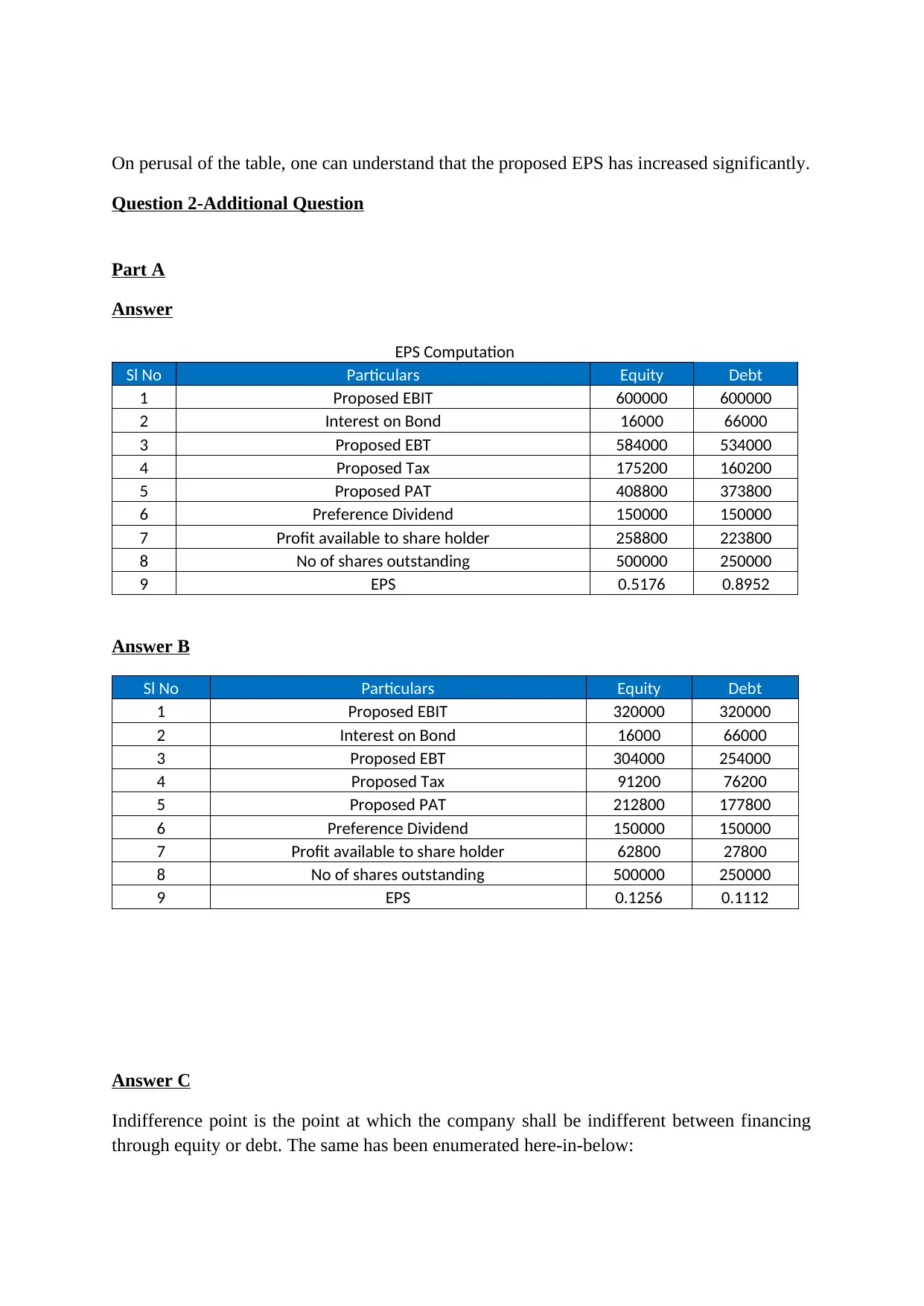

On perusal of the table, one can understand that the proposed EPS has increased significantly.

Question 2-Additional Question

Part A

Answer

EPS Computation

Sl No Particulars Equity Debt

1 Proposed EBIT 600000 600000

2 Interest on Bond 16000 66000

3 Proposed EBT 584000 534000

4 Proposed Tax 175200 160200

5 Proposed PAT 408800 373800

6 Preference Dividend 150000 150000

7 Profit available to share holder 258800 223800

8 No of shares outstanding 500000 250000

9 EPS 0.5176 0.8952

Answer B

Sl No Particulars Equity Debt

1 Proposed EBIT 320000 320000

2 Interest on Bond 16000 66000

3 Proposed EBT 304000 254000

4 Proposed Tax 91200 76200

5 Proposed PAT 212800 177800

6 Preference Dividend 150000 150000

7 Profit available to share holder 62800 27800

8 No of shares outstanding 500000 250000

9 EPS 0.1256 0.1112

Answer C

Indifference point is the point at which the company shall be indifferent between financing

through equity or debt. The same has been enumerated here-in-below:

Question 2-Additional Question

Part A

Answer

EPS Computation

Sl No Particulars Equity Debt

1 Proposed EBIT 600000 600000

2 Interest on Bond 16000 66000

3 Proposed EBT 584000 534000

4 Proposed Tax 175200 160200

5 Proposed PAT 408800 373800

6 Preference Dividend 150000 150000

7 Profit available to share holder 258800 223800

8 No of shares outstanding 500000 250000

9 EPS 0.5176 0.8952

Answer B

Sl No Particulars Equity Debt

1 Proposed EBIT 320000 320000

2 Interest on Bond 16000 66000

3 Proposed EBT 304000 254000

4 Proposed Tax 91200 76200

5 Proposed PAT 212800 177800

6 Preference Dividend 150000 150000

7 Profit available to share holder 62800 27800

8 No of shares outstanding 500000 250000

9 EPS 0.1256 0.1112

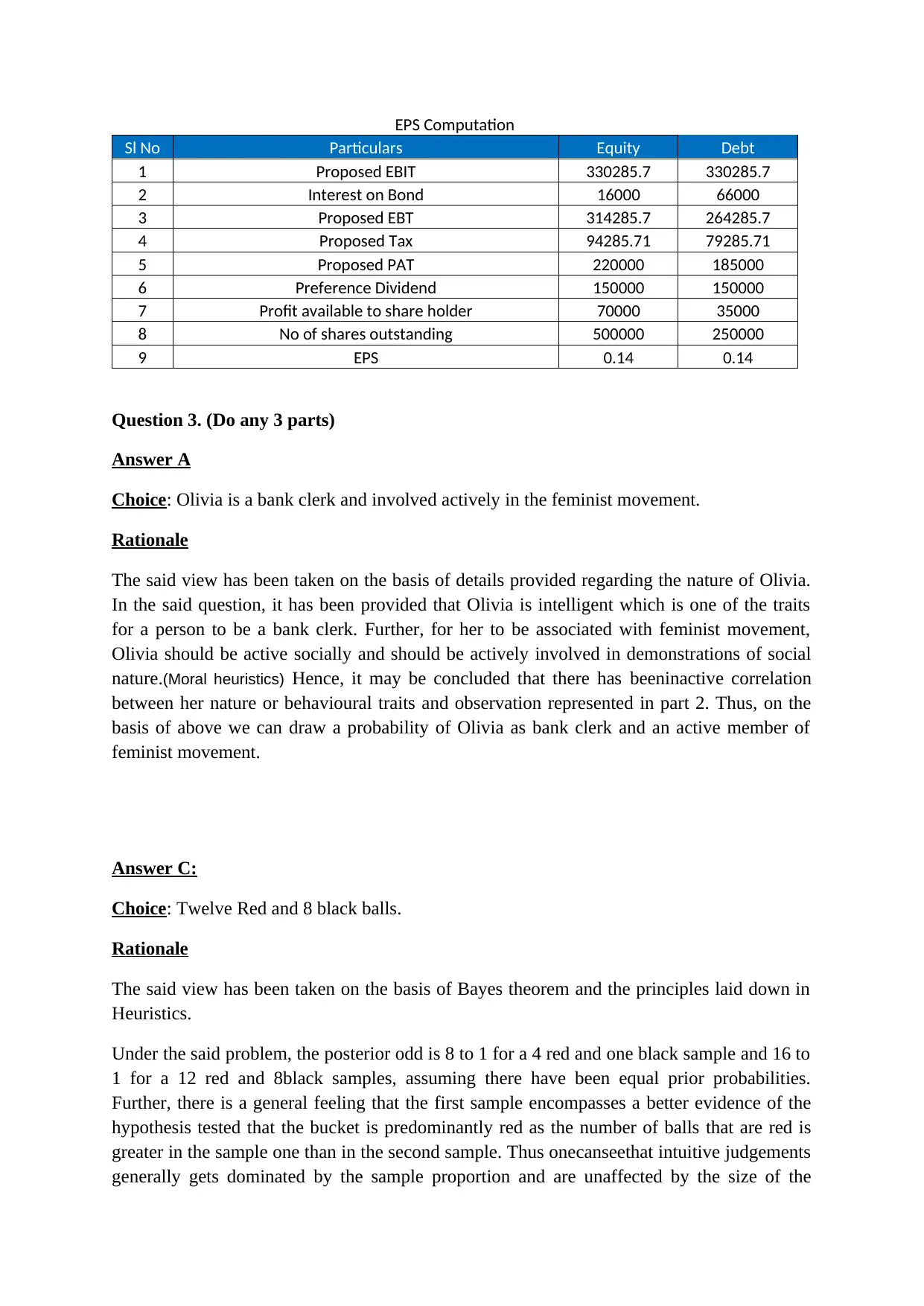

Answer C

Indifference point is the point at which the company shall be indifferent between financing

through equity or debt. The same has been enumerated here-in-below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EPS Computation

Sl No Particulars Equity Debt

1 Proposed EBIT 330285.7 330285.7

2 Interest on Bond 16000 66000

3 Proposed EBT 314285.7 264285.7

4 Proposed Tax 94285.71 79285.71

5 Proposed PAT 220000 185000

6 Preference Dividend 150000 150000

7 Profit available to share holder 70000 35000

8 No of shares outstanding 500000 250000

9 EPS 0.14 0.14

Question 3. (Do any 3 parts)

Answer A

Choice: Olivia is a bank clerk and involved actively in the feminist movement.

Rationale

The said view has been taken on the basis of details provided regarding the nature of Olivia.

In the said question, it has been provided that Olivia is intelligent which is one of the traits

for a person to be a bank clerk. Further, for her to be associated with feminist movement,

Olivia should be active socially and should be actively involved in demonstrations of social

nature.(Moral heuristics) Hence, it may be concluded that there has beeninactive correlation

between her nature or behavioural traits and observation represented in part 2. Thus, on the

basis of above we can draw a probability of Olivia as bank clerk and an active member of

feminist movement.

Answer C:

Choice: Twelve Red and 8 black balls.

Rationale

The said view has been taken on the basis of Bayes theorem and the principles laid down in

Heuristics.

Under the said problem, the posterior odd is 8 to 1 for a 4 red and one black sample and 16 to

1 for a 12 red and 8black samples, assuming there have been equal prior probabilities.

Further, there is a general feeling that the first sample encompasses a better evidence of the

hypothesis tested that the bucket is predominantly red as the number of balls that are red is

greater in the sample one than in the second sample. Thus onecanseethat intuitive judgements

generally gets dominated by the sample proportion and are unaffected by the size of the

Sl No Particulars Equity Debt

1 Proposed EBIT 330285.7 330285.7

2 Interest on Bond 16000 66000

3 Proposed EBT 314285.7 264285.7

4 Proposed Tax 94285.71 79285.71

5 Proposed PAT 220000 185000

6 Preference Dividend 150000 150000

7 Profit available to share holder 70000 35000

8 No of shares outstanding 500000 250000

9 EPS 0.14 0.14

Question 3. (Do any 3 parts)

Answer A

Choice: Olivia is a bank clerk and involved actively in the feminist movement.

Rationale

The said view has been taken on the basis of details provided regarding the nature of Olivia.

In the said question, it has been provided that Olivia is intelligent which is one of the traits

for a person to be a bank clerk. Further, for her to be associated with feminist movement,

Olivia should be active socially and should be actively involved in demonstrations of social

nature.(Moral heuristics) Hence, it may be concluded that there has beeninactive correlation

between her nature or behavioural traits and observation represented in part 2. Thus, on the

basis of above we can draw a probability of Olivia as bank clerk and an active member of

feminist movement.

Answer C:

Choice: Twelve Red and 8 black balls.

Rationale

The said view has been taken on the basis of Bayes theorem and the principles laid down in

Heuristics.

Under the said problem, the posterior odd is 8 to 1 for a 4 red and one black sample and 16 to

1 for a 12 red and 8black samples, assuming there have been equal prior probabilities.

Further, there is a general feeling that the first sample encompasses a better evidence of the

hypothesis tested that the bucket is predominantly red as the number of balls that are red is

greater in the sample one than in the second sample. Thus onecanseethat intuitive judgements

generally gets dominated by the sample proportion and are unaffected by the size of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sample which plays a crucial role in determination of posterior odds (Kahneman and Tversky,

1972). Further, intuitive estimates of posterior odds are far less extreme than the correct

values. The above problem is generally referred to as conservatism and draw two are more

likely.(Moral heuristics) Thus, the odds are in favour of second sample.

Part D

Answer d:

Choice: The choice shall depend on the group he is if he is in the first group he might be a

lawyer s there is greater proportion of lawyer in the first group. If he is in the second group he

might be a engineer as there is greater proportion of engineer in the second group. Thus, the

choice shall depend on the group he is.(Lawlor) Further, the second details that has been

provided is of no use and does not provide any detail of his traits as of engineer or lawyer as

both can be successful, able etc.

Rationale

If Ben has been part of the first group then the probability of him being an lawyer is 70 %

while that of an engineer is 30% Thus, under the first group he is most likely a lawyer.

Similarly, if Ben is part of group two, the probability of him being an engineer is 70% and

that of lawyer is 30%.Thus, under the second group he is most likely a engineer. Further, by

applying Bayes theorem ratio of odds (0.7/0.3)^2 are 5.44 for each description. The above

question is a sheer example of insensitivity of prior probability of outcome.

References:

1972). Further, intuitive estimates of posterior odds are far less extreme than the correct

values. The above problem is generally referred to as conservatism and draw two are more

likely.(Moral heuristics) Thus, the odds are in favour of second sample.

Part D

Answer d:

Choice: The choice shall depend on the group he is if he is in the first group he might be a

lawyer s there is greater proportion of lawyer in the first group. If he is in the second group he

might be a engineer as there is greater proportion of engineer in the second group. Thus, the

choice shall depend on the group he is.(Lawlor) Further, the second details that has been

provided is of no use and does not provide any detail of his traits as of engineer or lawyer as

both can be successful, able etc.

Rationale

If Ben has been part of the first group then the probability of him being an lawyer is 70 %

while that of an engineer is 30% Thus, under the first group he is most likely a lawyer.

Similarly, if Ben is part of group two, the probability of him being an engineer is 70% and

that of lawyer is 30%.Thus, under the second group he is most likely a engineer. Further, by

applying Bayes theorem ratio of odds (0.7/0.3)^2 are 5.44 for each description. The above

question is a sheer example of insensitivity of prior probability of outcome.

References:

Cleverism. (2015, November 29). Cost of Capital for Your Business . Retrieved September 9, 2018,

from financetrain.com: https://www.cleverism.com/calculate-cost-capital-business/

Farlex. (2012). Flotation Costs. Retrieved September 9, 2018, from financial-

dictionary.thefreedictionary.com:

https://financial-dictionary.thefreedictionary.com/flotation+cost

Lawlor, R. (n.d.). Engineering in Society. Retrieved September 9, 2018, from www.raeng.org.uk :

https://www.raeng.org.uk/publications/reports/engineering-in-society

Moral heuristics. (n.d.). Retrieved September 9, 2018, from 2005:

https://pdfs.semanticscholar.org/ee9d/d3028f999ac560dde661a6c8ab1a50e9eafa.pdf

from financetrain.com: https://www.cleverism.com/calculate-cost-capital-business/

Farlex. (2012). Flotation Costs. Retrieved September 9, 2018, from financial-

dictionary.thefreedictionary.com:

https://financial-dictionary.thefreedictionary.com/flotation+cost

Lawlor, R. (n.d.). Engineering in Society. Retrieved September 9, 2018, from www.raeng.org.uk :

https://www.raeng.org.uk/publications/reports/engineering-in-society

Moral heuristics. (n.d.). Retrieved September 9, 2018, from 2005:

https://pdfs.semanticscholar.org/ee9d/d3028f999ac560dde661a6c8ab1a50e9eafa.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.