Finance TMA 02: Investment Appraisal and Valuation of Tata Steel

VerifiedAdded on 2022/09/16

|10

|2870

|22

Homework Assignment

AI Summary

This assignment solution for Finance TMA 02 focuses on the financial analysis of Tata Steel Limited. It begins by discussing the importance of using cash flows over profits in investment appraisal, differentiating between relevant and irrelevant cash flows, and explaining the impact of inflation. The solution then presents a discounted cash flow (DCF) analysis to determine the company's fair value per share, including calculations for WACC, enterprise value, and terminal value. Furthermore, the assignment explores the concept of enterprise value and the adjusted book value approach for valuation, along with the application of market multiple ratios like EV/EBITDA. The document provides detailed calculations and explanations, making it a comprehensive resource for understanding financial analysis and valuation techniques within the context of a real-world company.

FINANCE

TMA 02

Tata Steel Limited

TMA 02

Tata Steel Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer 1

Part a

The investment appraisal process is a crucial process as the capital budgeting decisions are

not only concerning a huge amount but are also irreversible decisions. Hence, it is important

that such decisions are based on efficient calculations. One of most crucial elements of such

decision is to compute the estimated cash flows of the project proposals.

It is significant to note that while both the cash flows and the profits are crucial for a

business, most of the investment appraisal techniques use cash flows instead of the profits.

Cash flow includes the inflows and outflows of funds from a business. The significance of the

cash flows is for the conduct of the daily operations including the payment of the taxes,

paying employees, purchasing inventory, and other operating costs. The significance of the

use of the cash flows for the investment appraisal is that once the profits after tax have been

computed, the operating costs for which the actual cash payments have not been made, are

added back to the profits to arrive at the relevant cash flows (Bierman and Smidt, 2012). In

contrast to this, the profits refer to the surplus left in the business after the deduction of all the

expenses, whether the payment is made in cash or not. The profits of the business are arrived

after the application of various accounting standards and conventions and thus are complex to

compute. The reasons the cash flows are preferred is that the most of the techniques are based

on the time value of money where the initial investments are compared with the discounted

cash flows and not profits. The profits cannot be discounted. While the profits represent a low

conservative number, the cash flows are representative of the best estimates (Goyat and Nain,

2016). For the purpose of the capital budgeting exercise, the best estimates are more relevant.

Part b

Only the relevant cash flows are to be considered for the purpose of the capital budgeting

process. The relevant cash flows are the ones that would occur in the future and would impact

the incremental cost or revenues. Thus, the cash flows beyond the said definition are termed

as the irrelevant cash flows. For instance, the sunk costs are the renowned irrelevant cash

flows (Pogue, 2010). The sunk costs refer to those costs which have already been incurred in

the past irrespective of the selection or the rejection of the proposal. Thus, these costs are

important in terms of the historical data, the same are not useful for the future decision

making processes. The yet another irrelevant cash flow is in the form of the depreciation as

Part a

The investment appraisal process is a crucial process as the capital budgeting decisions are

not only concerning a huge amount but are also irreversible decisions. Hence, it is important

that such decisions are based on efficient calculations. One of most crucial elements of such

decision is to compute the estimated cash flows of the project proposals.

It is significant to note that while both the cash flows and the profits are crucial for a

business, most of the investment appraisal techniques use cash flows instead of the profits.

Cash flow includes the inflows and outflows of funds from a business. The significance of the

cash flows is for the conduct of the daily operations including the payment of the taxes,

paying employees, purchasing inventory, and other operating costs. The significance of the

use of the cash flows for the investment appraisal is that once the profits after tax have been

computed, the operating costs for which the actual cash payments have not been made, are

added back to the profits to arrive at the relevant cash flows (Bierman and Smidt, 2012). In

contrast to this, the profits refer to the surplus left in the business after the deduction of all the

expenses, whether the payment is made in cash or not. The profits of the business are arrived

after the application of various accounting standards and conventions and thus are complex to

compute. The reasons the cash flows are preferred is that the most of the techniques are based

on the time value of money where the initial investments are compared with the discounted

cash flows and not profits. The profits cannot be discounted. While the profits represent a low

conservative number, the cash flows are representative of the best estimates (Goyat and Nain,

2016). For the purpose of the capital budgeting exercise, the best estimates are more relevant.

Part b

Only the relevant cash flows are to be considered for the purpose of the capital budgeting

process. The relevant cash flows are the ones that would occur in the future and would impact

the incremental cost or revenues. Thus, the cash flows beyond the said definition are termed

as the irrelevant cash flows. For instance, the sunk costs are the renowned irrelevant cash

flows (Pogue, 2010). The sunk costs refer to those costs which have already been incurred in

the past irrespective of the selection or the rejection of the proposal. Thus, these costs are

important in terms of the historical data, the same are not useful for the future decision

making processes. The yet another irrelevant cash flow is in the form of the depreciation as

the said expense is not incurred in the cash. The examples or the relevant cash flows is in the

form of the opportunity costs. The opportunity cost refers to the cost of rejecting an activity

while choosing to accept the others (Ross et. al, 2014). Thus, in simple words these are the

lost revenues while the existing resources are moved from their current use. The yet another

relevant cash flows are in the form of the incremental cash flows. The costs only pertaining to

the decision must be considered and not the once that are already committed and would be

incurred whether or not the decision to accept is made. Thus, as elaborated above, the

relevant cash flows lead to the correct estimation of the net cash flows of a project proposal.

Part c

Inflation is a prevailing trend of increasing prices in the economy from one year to the other.

Inflation is one of the most important concepts in the project proposal evaluation and the

revenues and costs are subjected to the inflation to arrive at the nominal costs or the profits as

estimated to occur from a proposal in the future periods. It is significant to consider the effect

of the inflation in the determination of the cash flows because in a business environment

where the economies have an increasing inflation trends, with the passage of time the future

cash flows will have a decreased purchasing power in terms of current value (Rὂhrich, 2014).

Thus, in order to ascertain the relevant cash flows with maintenance of the purchasing power

of future cash inflows, it is crucial to inflate the cash receipts. In order to give the right effect

of the inflation to the cash flows, it is important to understand the difference between the

general and the specific inflation rates. The general inflation rate is as applicable to the whole

economy and determined through a public measure index, the specific inflation rate is

applicable to the specific project variables differently. This means that the variables such as

variable costs and fixed costs, selling price are subjected to the different rates of inflation.

The managers must apply the relative inflation rates to different variables to arrive at the

nominal cash flows or cash flows in the current price terms that are inflated into future

values.

Part d

The technique to be used in the evaluation of the better choice from the in house production

facility and the outsourcing of the production is the “Incremental Cash Flow analysis.” It is

also referred to as the marginal analysis, relevant cost approach, or the differential analysis.

The incremental analysis denotes the decision-making tool wherein the determination of the

true cost difference between varied choices is conducted. The key principle involved in such

form of the opportunity costs. The opportunity cost refers to the cost of rejecting an activity

while choosing to accept the others (Ross et. al, 2014). Thus, in simple words these are the

lost revenues while the existing resources are moved from their current use. The yet another

relevant cash flows are in the form of the incremental cash flows. The costs only pertaining to

the decision must be considered and not the once that are already committed and would be

incurred whether or not the decision to accept is made. Thus, as elaborated above, the

relevant cash flows lead to the correct estimation of the net cash flows of a project proposal.

Part c

Inflation is a prevailing trend of increasing prices in the economy from one year to the other.

Inflation is one of the most important concepts in the project proposal evaluation and the

revenues and costs are subjected to the inflation to arrive at the nominal costs or the profits as

estimated to occur from a proposal in the future periods. It is significant to consider the effect

of the inflation in the determination of the cash flows because in a business environment

where the economies have an increasing inflation trends, with the passage of time the future

cash flows will have a decreased purchasing power in terms of current value (Rὂhrich, 2014).

Thus, in order to ascertain the relevant cash flows with maintenance of the purchasing power

of future cash inflows, it is crucial to inflate the cash receipts. In order to give the right effect

of the inflation to the cash flows, it is important to understand the difference between the

general and the specific inflation rates. The general inflation rate is as applicable to the whole

economy and determined through a public measure index, the specific inflation rate is

applicable to the specific project variables differently. This means that the variables such as

variable costs and fixed costs, selling price are subjected to the different rates of inflation.

The managers must apply the relative inflation rates to different variables to arrive at the

nominal cash flows or cash flows in the current price terms that are inflated into future

values.

Part d

The technique to be used in the evaluation of the better choice from the in house production

facility and the outsourcing of the production is the “Incremental Cash Flow analysis.” It is

also referred to as the marginal analysis, relevant cost approach, or the differential analysis.

The incremental analysis denotes the decision-making tool wherein the determination of the

true cost difference between varied choices is conducted. The key principle involved in such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analysis is that the sunk cost or past cost are ignored. It is to be noted that such technique

involves the consideration of both the qualitative as well as the quantitative factors. The

quantitative factors to be involved are the change in the purchase cost per unit, production

cost per unit, incremental fixed costs if any, changes in the production capacity available to

the business and others (Scott, 2012). The qualitative factors involved in the evaluation are

the impact of the decision on suppliers in the form of partnership or discounts, control over

quality of the component, reliability of suppliers, and changes in the customers’ expectations

apart from the others. Thus, both the factors are evaluated in relation to the in house and the

outsourcing proposals, and accordingly the decisions are reached.

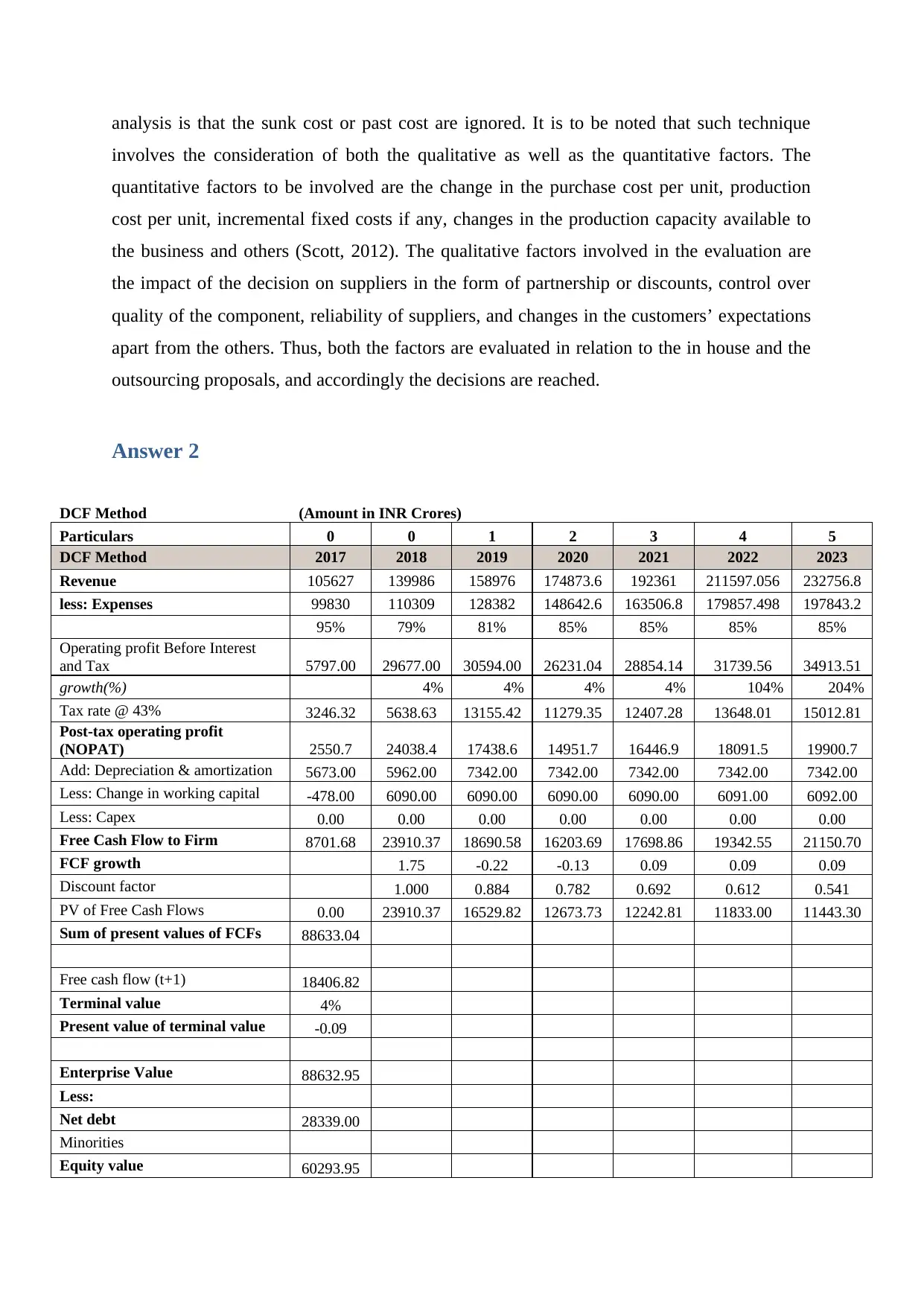

Answer 2

DCF Method (Amount in INR Crores)

Particulars 0 0 1 2 3 4 5

DCF Method 2017 2018 2019 2020 2021 2022 2023

Revenue 105627 139986 158976 174873.6 192361 211597.056 232756.8

less: Expenses 99830 110309 128382 148642.6 163506.8 179857.498 197843.2

95% 79% 81% 85% 85% 85% 85%

Operating profit Before Interest

and Tax 5797.00 29677.00 30594.00 26231.04 28854.14 31739.56 34913.51

growth(%) 4% 4% 4% 4% 104% 204%

Tax rate @ 43% 3246.32 5638.63 13155.42 11279.35 12407.28 13648.01 15012.81

Post-tax operating profit

(NOPAT) 2550.7 24038.4 17438.6 14951.7 16446.9 18091.5 19900.7

Add: Depreciation & amortization 5673.00 5962.00 7342.00 7342.00 7342.00 7342.00 7342.00

Less: Change in working capital -478.00 6090.00 6090.00 6090.00 6090.00 6091.00 6092.00

Less: Capex 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Free Cash Flow to Firm 8701.68 23910.37 18690.58 16203.69 17698.86 19342.55 21150.70

FCF growth 1.75 -0.22 -0.13 0.09 0.09 0.09

Discount factor 1.000 0.884 0.782 0.692 0.612 0.541

PV of Free Cash Flows 0.00 23910.37 16529.82 12673.73 12242.81 11833.00 11443.30

Sum of present values of FCFs 88633.04

Free cash flow (t+1) 18406.82

Terminal value 4%

Present value of terminal value -0.09

Enterprise Value 88632.95

Less:

Net debt 28339.00

Minorities

Equity value 60293.95

involves the consideration of both the qualitative as well as the quantitative factors. The

quantitative factors to be involved are the change in the purchase cost per unit, production

cost per unit, incremental fixed costs if any, changes in the production capacity available to

the business and others (Scott, 2012). The qualitative factors involved in the evaluation are

the impact of the decision on suppliers in the form of partnership or discounts, control over

quality of the component, reliability of suppliers, and changes in the customers’ expectations

apart from the others. Thus, both the factors are evaluated in relation to the in house and the

outsourcing proposals, and accordingly the decisions are reached.

Answer 2

DCF Method (Amount in INR Crores)

Particulars 0 0 1 2 3 4 5

DCF Method 2017 2018 2019 2020 2021 2022 2023

Revenue 105627 139986 158976 174873.6 192361 211597.056 232756.8

less: Expenses 99830 110309 128382 148642.6 163506.8 179857.498 197843.2

95% 79% 81% 85% 85% 85% 85%

Operating profit Before Interest

and Tax 5797.00 29677.00 30594.00 26231.04 28854.14 31739.56 34913.51

growth(%) 4% 4% 4% 4% 104% 204%

Tax rate @ 43% 3246.32 5638.63 13155.42 11279.35 12407.28 13648.01 15012.81

Post-tax operating profit

(NOPAT) 2550.7 24038.4 17438.6 14951.7 16446.9 18091.5 19900.7

Add: Depreciation & amortization 5673.00 5962.00 7342.00 7342.00 7342.00 7342.00 7342.00

Less: Change in working capital -478.00 6090.00 6090.00 6090.00 6090.00 6091.00 6092.00

Less: Capex 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Free Cash Flow to Firm 8701.68 23910.37 18690.58 16203.69 17698.86 19342.55 21150.70

FCF growth 1.75 -0.22 -0.13 0.09 0.09 0.09

Discount factor 1.000 0.884 0.782 0.692 0.612 0.541

PV of Free Cash Flows 0.00 23910.37 16529.82 12673.73 12242.81 11833.00 11443.30

Sum of present values of FCFs 88633.04

Free cash flow (t+1) 18406.82

Terminal value 4%

Present value of terminal value -0.09

Enterprise Value 88632.95

Less:

Net debt 28339.00

Minorities

Equity value 60293.95

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

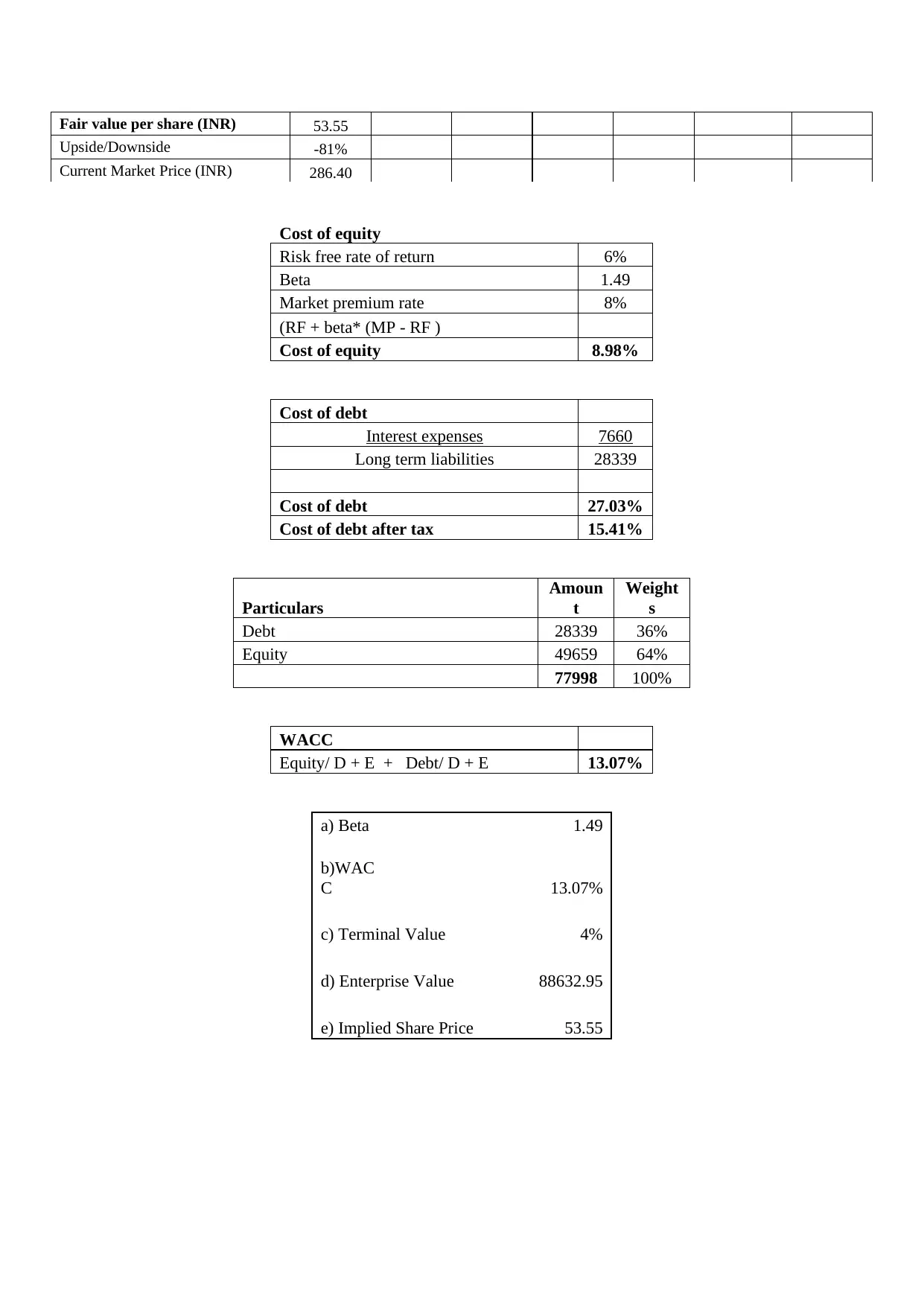

Fair value per share (INR) 53.55

Upside/Downside -81%

Current Market Price (INR) 286.40

Cost of equity

Risk free rate of return 6%

Beta 1.49

Market premium rate 8%

(RF + beta* (MP - RF )

Cost of equity 8.98%

Cost of debt

Interest expenses 7660

Long term liabilities 28339

Cost of debt 27.03%

Cost of debt after tax 15.41%

Particulars

Amoun

t

Weight

s

Debt 28339 36%

Equity 49659 64%

77998 100%

WACC

Equity/ D + E + Debt/ D + E 13.07%

a) Beta 1.49

b)WAC

C 13.07%

c) Terminal Value 4%

d) Enterprise Value 88632.95

e) Implied Share Price 53.55

Upside/Downside -81%

Current Market Price (INR) 286.40

Cost of equity

Risk free rate of return 6%

Beta 1.49

Market premium rate 8%

(RF + beta* (MP - RF )

Cost of equity 8.98%

Cost of debt

Interest expenses 7660

Long term liabilities 28339

Cost of debt 27.03%

Cost of debt after tax 15.41%

Particulars

Amoun

t

Weight

s

Debt 28339 36%

Equity 49659 64%

77998 100%

WACC

Equity/ D + E + Debt/ D + E 13.07%

a) Beta 1.49

b)WAC

C 13.07%

c) Terminal Value 4%

d) Enterprise Value 88632.95

e) Implied Share Price 53.55

Answer 3

Part a

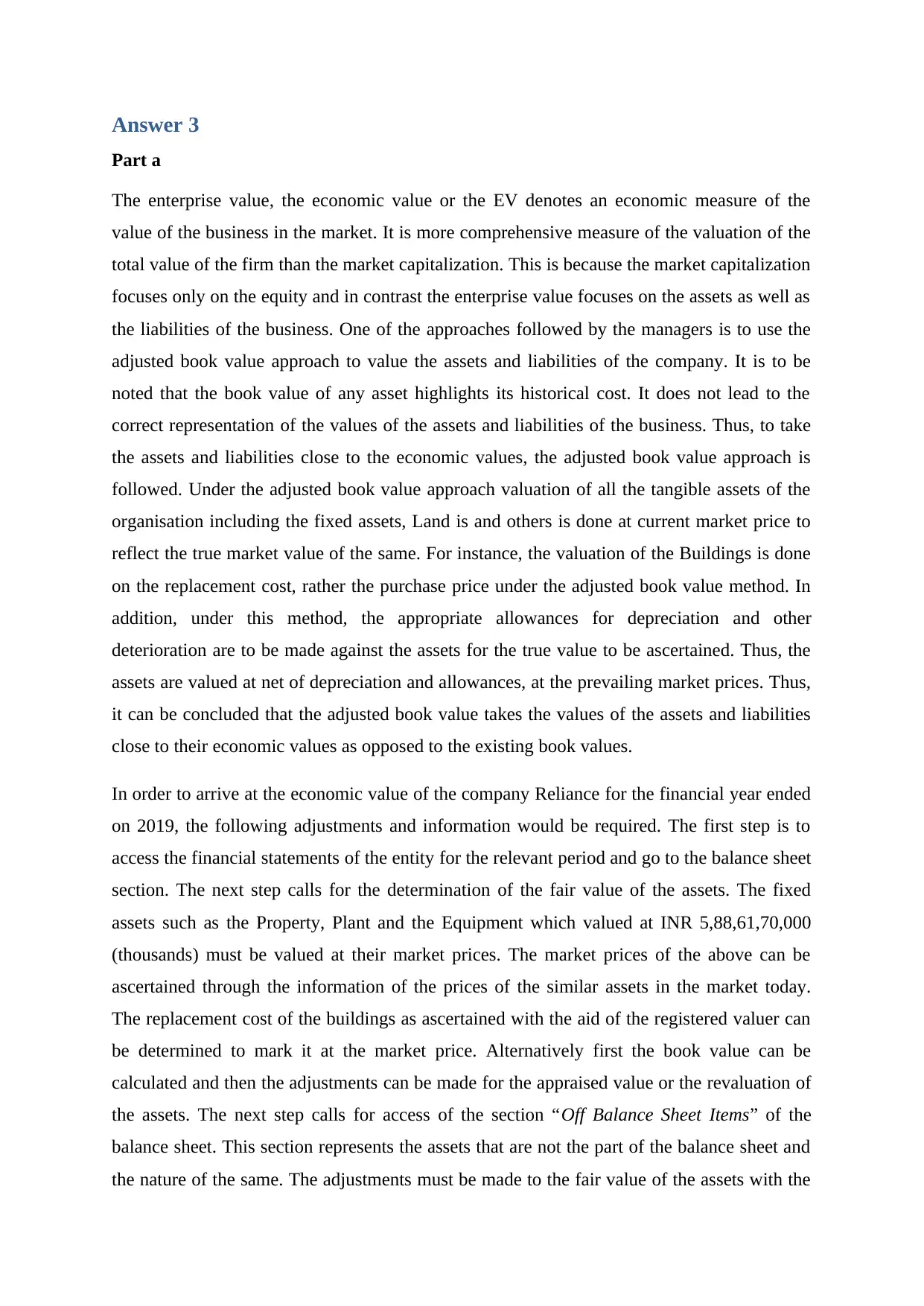

The enterprise value, the economic value or the EV denotes an economic measure of the

value of the business in the market. It is more comprehensive measure of the valuation of the

total value of the firm than the market capitalization. This is because the market capitalization

focuses only on the equity and in contrast the enterprise value focuses on the assets as well as

the liabilities of the business. One of the approaches followed by the managers is to use the

adjusted book value approach to value the assets and liabilities of the company. It is to be

noted that the book value of any asset highlights its historical cost. It does not lead to the

correct representation of the values of the assets and liabilities of the business. Thus, to take

the assets and liabilities close to the economic values, the adjusted book value approach is

followed. Under the adjusted book value approach valuation of all the tangible assets of the

organisation including the fixed assets, Land is and others is done at current market price to

reflect the true market value of the same. For instance, the valuation of the Buildings is done

on the replacement cost, rather the purchase price under the adjusted book value method. In

addition, under this method, the appropriate allowances for depreciation and other

deterioration are to be made against the assets for the true value to be ascertained. Thus, the

assets are valued at net of depreciation and allowances, at the prevailing market prices. Thus,

it can be concluded that the adjusted book value takes the values of the assets and liabilities

close to their economic values as opposed to the existing book values.

In order to arrive at the economic value of the company Reliance for the financial year ended

on 2019, the following adjustments and information would be required. The first step is to

access the financial statements of the entity for the relevant period and go to the balance sheet

section. The next step calls for the determination of the fair value of the assets. The fixed

assets such as the Property, Plant and the Equipment which valued at INR 5,88,61,70,000

(thousands) must be valued at their market prices. The market prices of the above can be

ascertained through the information of the prices of the similar assets in the market today.

The replacement cost of the buildings as ascertained with the aid of the registered valuer can

be determined to mark it at the market price. Alternatively first the book value can be

calculated and then the adjustments can be made for the appraised value or the revaluation of

the assets. The next step calls for access of the section “Off Balance Sheet Items” of the

balance sheet. This section represents the assets that are not the part of the balance sheet and

the nature of the same. The adjustments must be made to the fair value of the assets with the

Part a

The enterprise value, the economic value or the EV denotes an economic measure of the

value of the business in the market. It is more comprehensive measure of the valuation of the

total value of the firm than the market capitalization. This is because the market capitalization

focuses only on the equity and in contrast the enterprise value focuses on the assets as well as

the liabilities of the business. One of the approaches followed by the managers is to use the

adjusted book value approach to value the assets and liabilities of the company. It is to be

noted that the book value of any asset highlights its historical cost. It does not lead to the

correct representation of the values of the assets and liabilities of the business. Thus, to take

the assets and liabilities close to the economic values, the adjusted book value approach is

followed. Under the adjusted book value approach valuation of all the tangible assets of the

organisation including the fixed assets, Land is and others is done at current market price to

reflect the true market value of the same. For instance, the valuation of the Buildings is done

on the replacement cost, rather the purchase price under the adjusted book value method. In

addition, under this method, the appropriate allowances for depreciation and other

deterioration are to be made against the assets for the true value to be ascertained. Thus, the

assets are valued at net of depreciation and allowances, at the prevailing market prices. Thus,

it can be concluded that the adjusted book value takes the values of the assets and liabilities

close to their economic values as opposed to the existing book values.

In order to arrive at the economic value of the company Reliance for the financial year ended

on 2019, the following adjustments and information would be required. The first step is to

access the financial statements of the entity for the relevant period and go to the balance sheet

section. The next step calls for the determination of the fair value of the assets. The fixed

assets such as the Property, Plant and the Equipment which valued at INR 5,88,61,70,000

(thousands) must be valued at their market prices. The market prices of the above can be

ascertained through the information of the prices of the similar assets in the market today.

The replacement cost of the buildings as ascertained with the aid of the registered valuer can

be determined to mark it at the market price. Alternatively first the book value can be

calculated and then the adjustments can be made for the appraised value or the revaluation of

the assets. The next step calls for access of the section “Off Balance Sheet Items” of the

balance sheet. This section represents the assets that are not the part of the balance sheet and

the nature of the same. The adjustments must be made to the fair value of the assets with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Off Balance Sheet Items to arrive at the adjusted book values which are close to the economic

value.

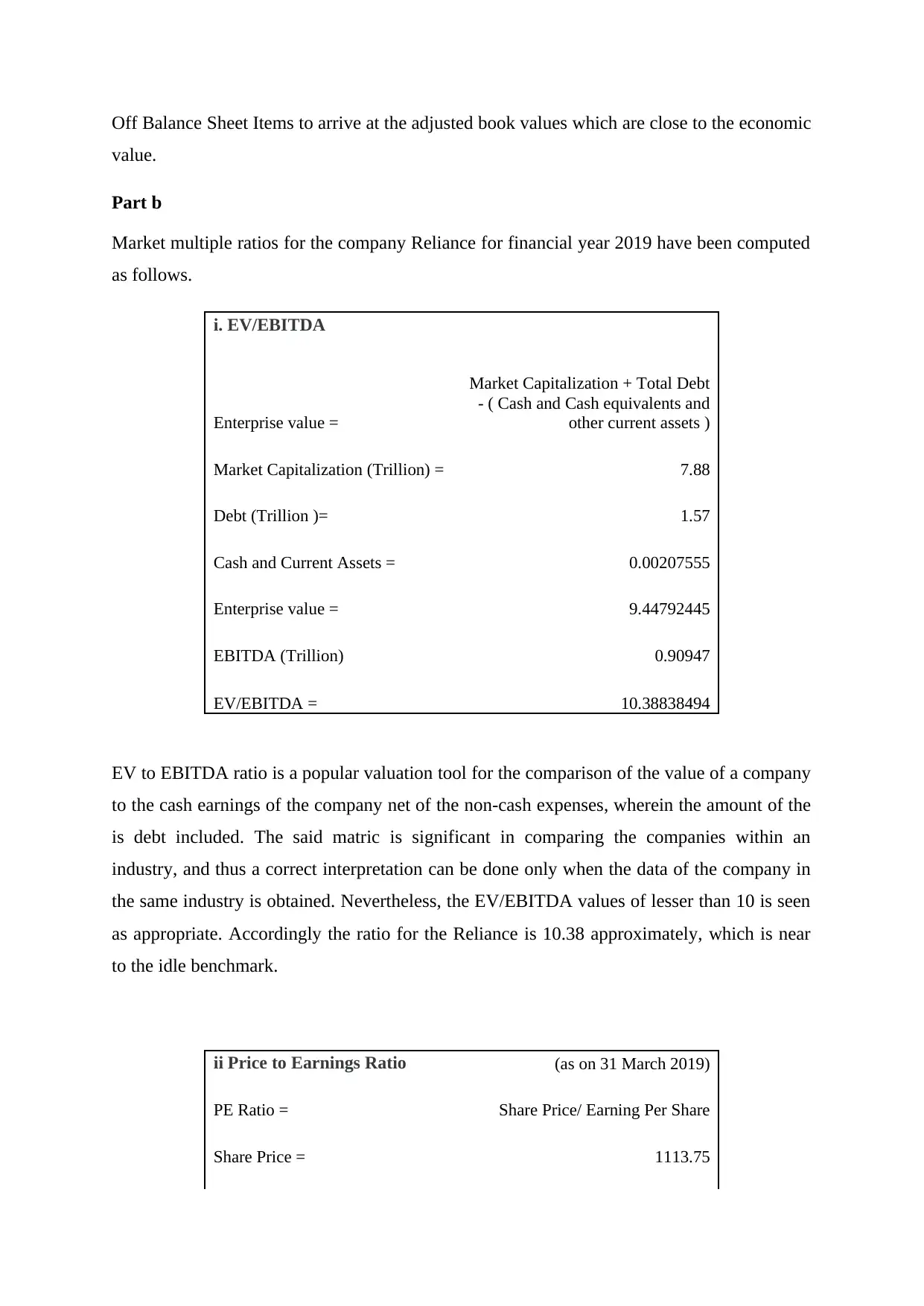

Part b

Market multiple ratios for the company Reliance for financial year 2019 have been computed

as follows.

i. EV/EBITDA

Enterprise value =

Market Capitalization + Total Debt

- ( Cash and Cash equivalents and

other current assets )

Market Capitalization (Trillion) = 7.88

Debt (Trillion )= 1.57

Cash and Current Assets = 0.00207555

Enterprise value = 9.44792445

EBITDA (Trillion) 0.90947

EV/EBITDA = 10.38838494

EV to EBITDA ratio is a popular valuation tool for the comparison of the value of a company

to the cash earnings of the company net of the non-cash expenses, wherein the amount of the

is debt included. The said matric is significant in comparing the companies within an

industry, and thus a correct interpretation can be done only when the data of the company in

the same industry is obtained. Nevertheless, the EV/EBITDA values of lesser than 10 is seen

as appropriate. Accordingly the ratio for the Reliance is 10.38 approximately, which is near

to the idle benchmark.

ii Price to Earnings Ratio (as on 31 March 2019)

PE Ratio = Share Price/ Earning Per Share

Share Price = 1113.75

value.

Part b

Market multiple ratios for the company Reliance for financial year 2019 have been computed

as follows.

i. EV/EBITDA

Enterprise value =

Market Capitalization + Total Debt

- ( Cash and Cash equivalents and

other current assets )

Market Capitalization (Trillion) = 7.88

Debt (Trillion )= 1.57

Cash and Current Assets = 0.00207555

Enterprise value = 9.44792445

EBITDA (Trillion) 0.90947

EV/EBITDA = 10.38838494

EV to EBITDA ratio is a popular valuation tool for the comparison of the value of a company

to the cash earnings of the company net of the non-cash expenses, wherein the amount of the

is debt included. The said matric is significant in comparing the companies within an

industry, and thus a correct interpretation can be done only when the data of the company in

the same industry is obtained. Nevertheless, the EV/EBITDA values of lesser than 10 is seen

as appropriate. Accordingly the ratio for the Reliance is 10.38 approximately, which is near

to the idle benchmark.

ii Price to Earnings Ratio (as on 31 March 2019)

PE Ratio = Share Price/ Earning Per Share

Share Price = 1113.75

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EPS = 66.82

PE Ratio = 16.6679138

The Price Multiple or the Price to Earnings Ratio is yet another key ratio of the interests of

the investors. It is used for the determination of the relative value of the shares of an

organisation in when the comparison is made between the choices of the two or more stocks.

Further, it is also used for the comparison of a company in relation to its historical data and

thus gives a view of the prevalent market conditions. In the case of the company Reliance, it

has been ascertained that the PE Ratio has been computed out to be 16.67. Such a high P/E

ratio maybe indicative of two things. Firstly, it could indicate that the shares of the company

Reliance is over-valued. Also it could mean that the investors of the company are expecting

high growth rate in the upcoming periods.

The Price to Cash Flow ratio is a tool of stock valuation wherein the value of a stock is

assessed in relation to the operating cash flow. Thus, the ratio can be calculated either on the

per share basis or using the total amounts. For the computation of this ratio, the operating

cash flow is used where the non-cash expenses are added back to the net income such as

depreciation and amortization charges. Thus, it is ascertained from the ratio as to how much

cash is generated as against the stock price. Thus, as per the ratio above computed for

Reliance, the per share cash generation is of INR 17229.

iii Price to Cash Flow Ratio

Price to Cash Flow Ratio =

Market Capitalization / Operating

Cash Flow

(Amount in Trillion)

Operating Cash flow = 0.00045736

Market Capitalization = 7.88

Price to Cash Flow Ratio = 17229.31607

PE Ratio = 16.6679138

The Price Multiple or the Price to Earnings Ratio is yet another key ratio of the interests of

the investors. It is used for the determination of the relative value of the shares of an

organisation in when the comparison is made between the choices of the two or more stocks.

Further, it is also used for the comparison of a company in relation to its historical data and

thus gives a view of the prevalent market conditions. In the case of the company Reliance, it

has been ascertained that the PE Ratio has been computed out to be 16.67. Such a high P/E

ratio maybe indicative of two things. Firstly, it could indicate that the shares of the company

Reliance is over-valued. Also it could mean that the investors of the company are expecting

high growth rate in the upcoming periods.

The Price to Cash Flow ratio is a tool of stock valuation wherein the value of a stock is

assessed in relation to the operating cash flow. Thus, the ratio can be calculated either on the

per share basis or using the total amounts. For the computation of this ratio, the operating

cash flow is used where the non-cash expenses are added back to the net income such as

depreciation and amortization charges. Thus, it is ascertained from the ratio as to how much

cash is generated as against the stock price. Thus, as per the ratio above computed for

Reliance, the per share cash generation is of INR 17229.

iii Price to Cash Flow Ratio

Price to Cash Flow Ratio =

Market Capitalization / Operating

Cash Flow

(Amount in Trillion)

Operating Cash flow = 0.00045736

Market Capitalization = 7.88

Price to Cash Flow Ratio = 17229.31607

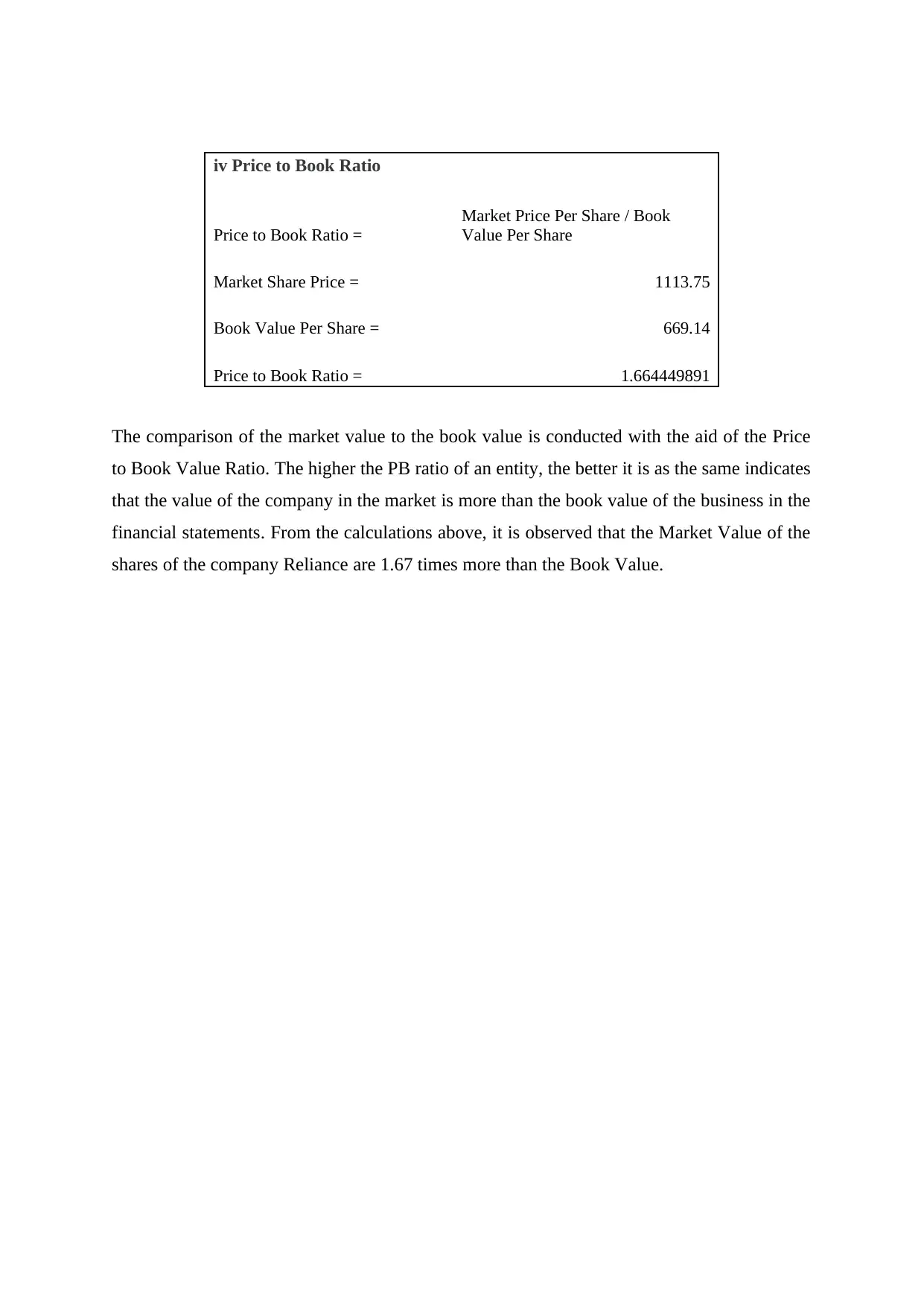

iv Price to Book Ratio

Price to Book Ratio =

Market Price Per Share / Book

Value Per Share

Market Share Price = 1113.75

Book Value Per Share = 669.14

Price to Book Ratio = 1.664449891

The comparison of the market value to the book value is conducted with the aid of the Price

to Book Value Ratio. The higher the PB ratio of an entity, the better it is as the same indicates

that the value of the company in the market is more than the book value of the business in the

financial statements. From the calculations above, it is observed that the Market Value of the

shares of the company Reliance are 1.67 times more than the Book Value.

Price to Book Ratio =

Market Price Per Share / Book

Value Per Share

Market Share Price = 1113.75

Book Value Per Share = 669.14

Price to Book Ratio = 1.664449891

The comparison of the market value to the book value is conducted with the aid of the Price

to Book Value Ratio. The higher the PB ratio of an entity, the better it is as the same indicates

that the value of the company in the market is more than the book value of the business in the

financial statements. From the calculations above, it is observed that the Market Value of the

shares of the company Reliance are 1.67 times more than the Book Value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Bierman Jr, H., and Smidt, S. (2012) The capital budgeting decision: economic analysis of

investment projects. 9th ed. Oxon: Routledge.

Goyat, S., and Nain, A. (2016) Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Pogue, M. (2010) Corporate Investment Decisions: Principles and Practice. New York:

Business Expert Press, p. 53.

Ross, S. A., Westerfield, R. W., Jaffe, J., and Kakani, R. K. (2014) Corporate Finance. 8th ed.

New Delhi: Tata McGraw Hill Education Pvt Ltd.

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a Case

Study. Boston: Walter de Gruyter GmbH & Co.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press, p. 342.

Bierman Jr, H., and Smidt, S. (2012) The capital budgeting decision: economic analysis of

investment projects. 9th ed. Oxon: Routledge.

Goyat, S., and Nain, A. (2016) Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Pogue, M. (2010) Corporate Investment Decisions: Principles and Practice. New York:

Business Expert Press, p. 53.

Ross, S. A., Westerfield, R. W., Jaffe, J., and Kakani, R. K. (2014) Corporate Finance. 8th ed.

New Delhi: Tata McGraw Hill Education Pvt Ltd.

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a Case

Study. Boston: Walter de Gruyter GmbH & Co.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press, p. 342.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.