Analysis of Investment Securities and Liquidity Management in Banking

VerifiedAdded on 2022/10/31

|14

|1744

|261

Report

AI Summary

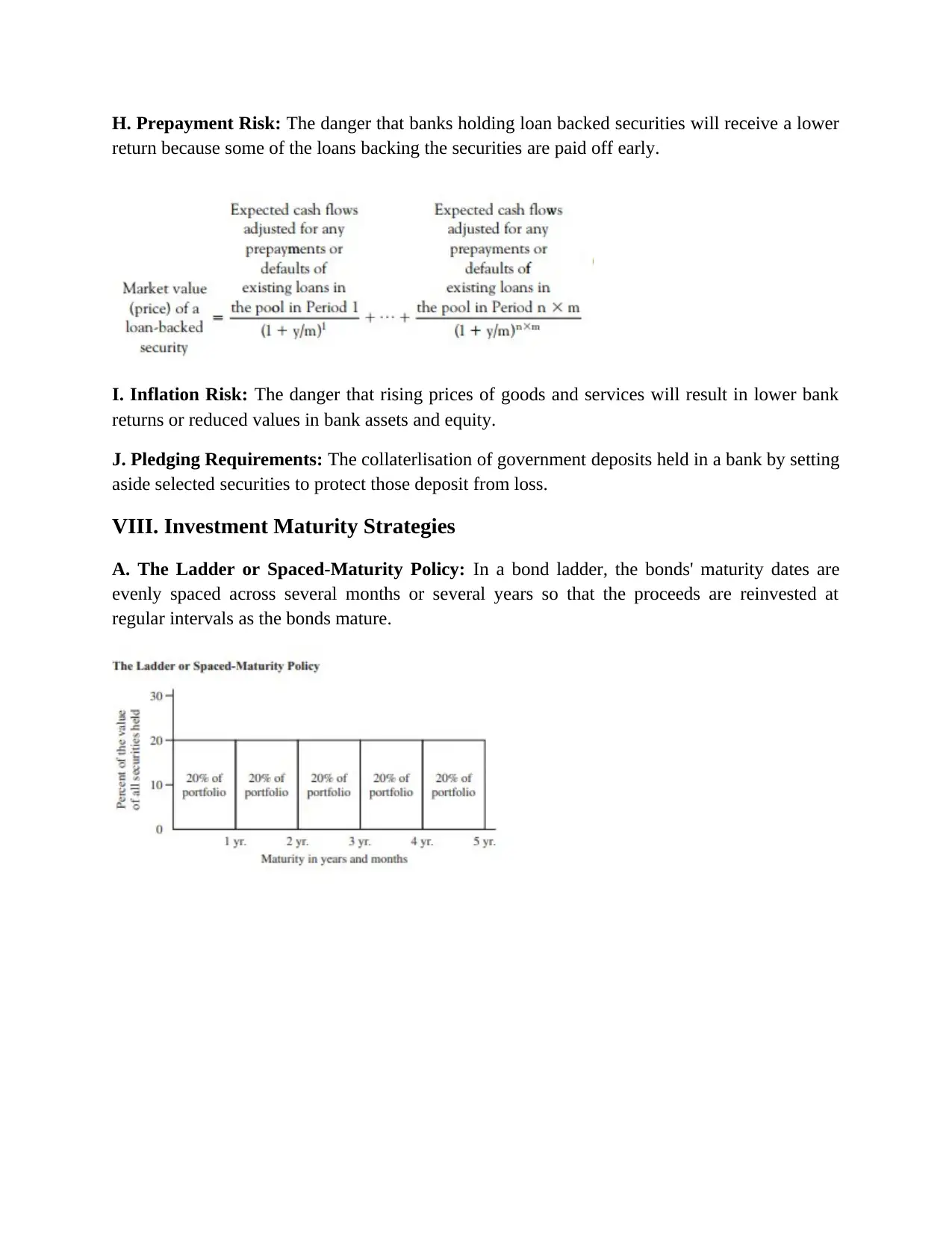

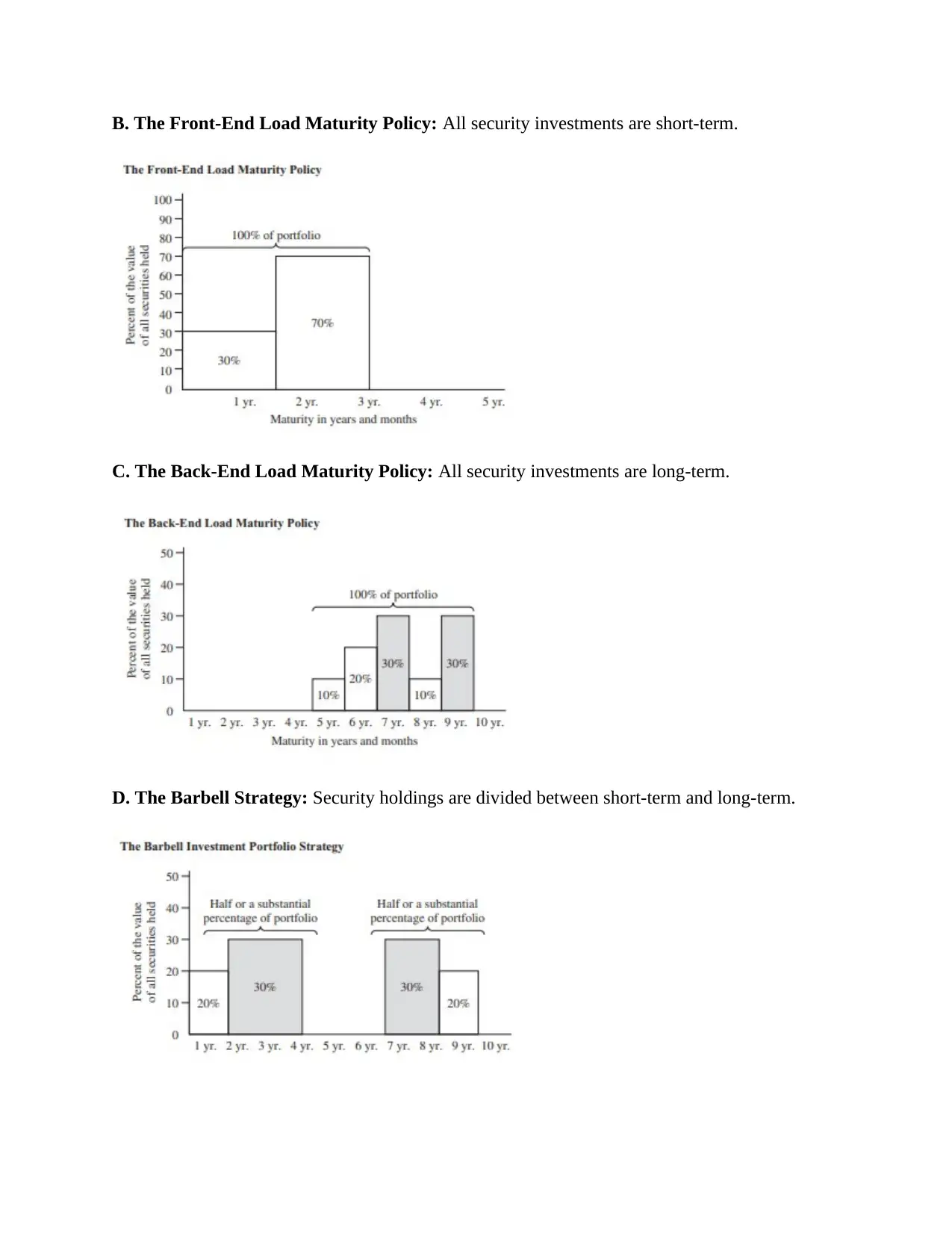

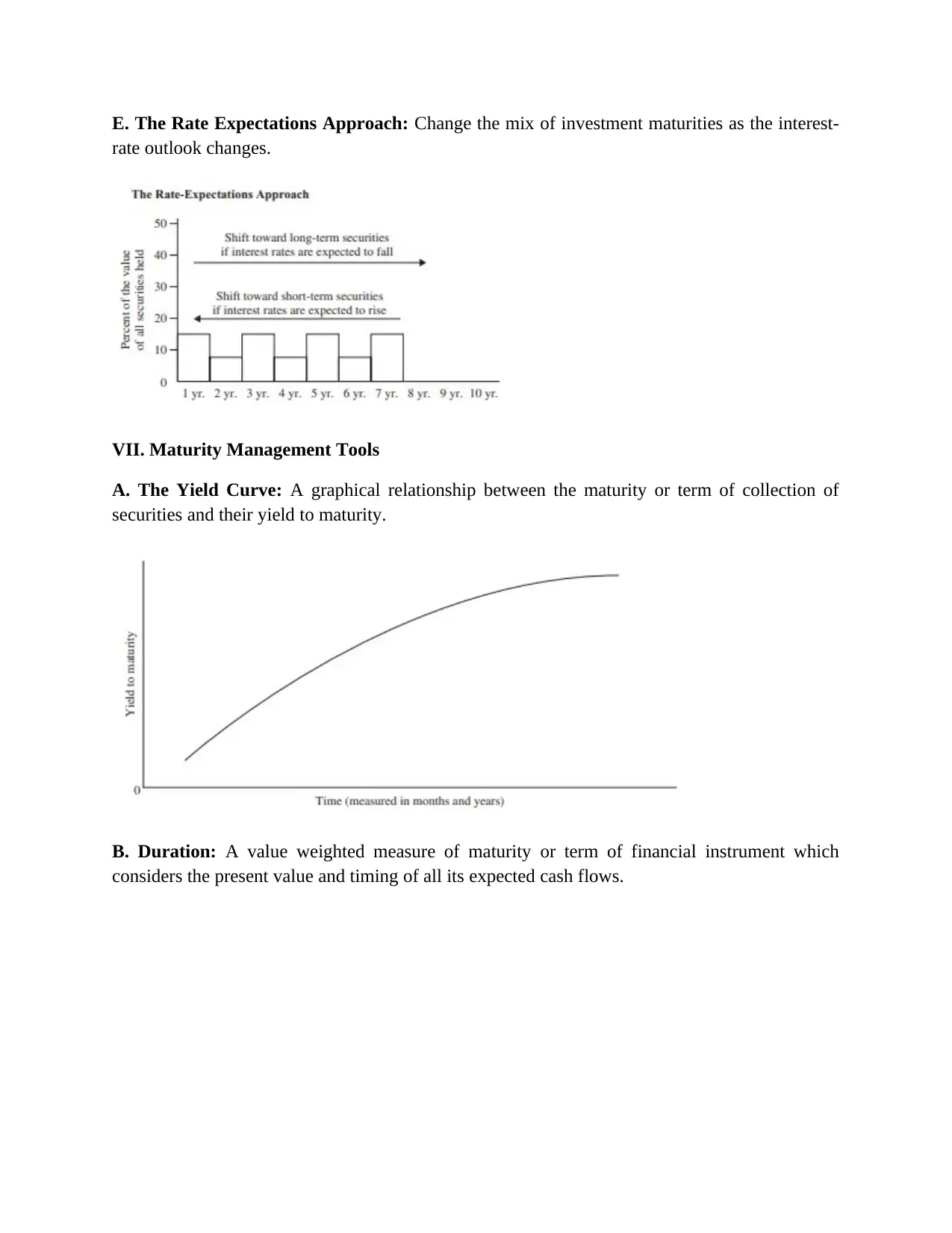

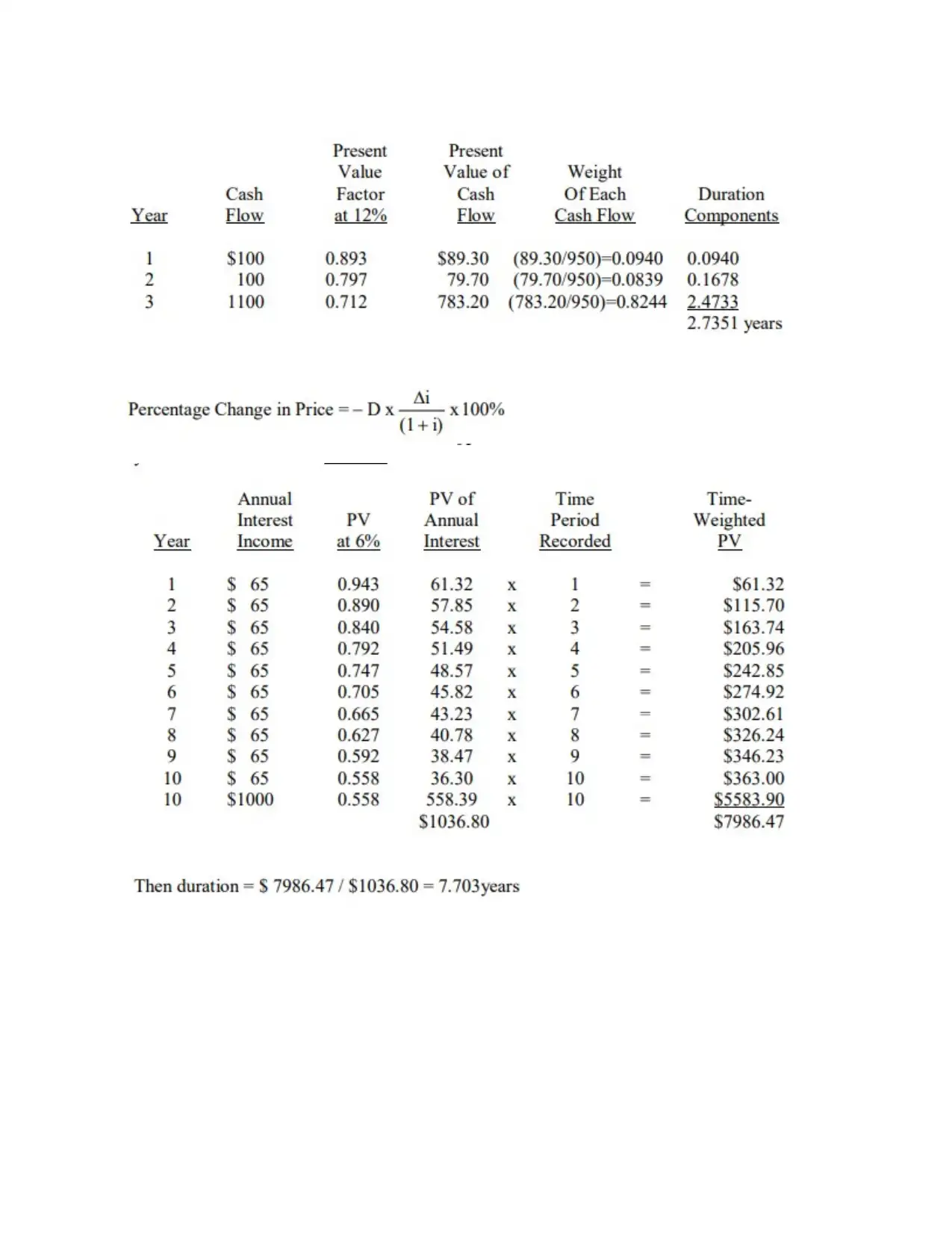

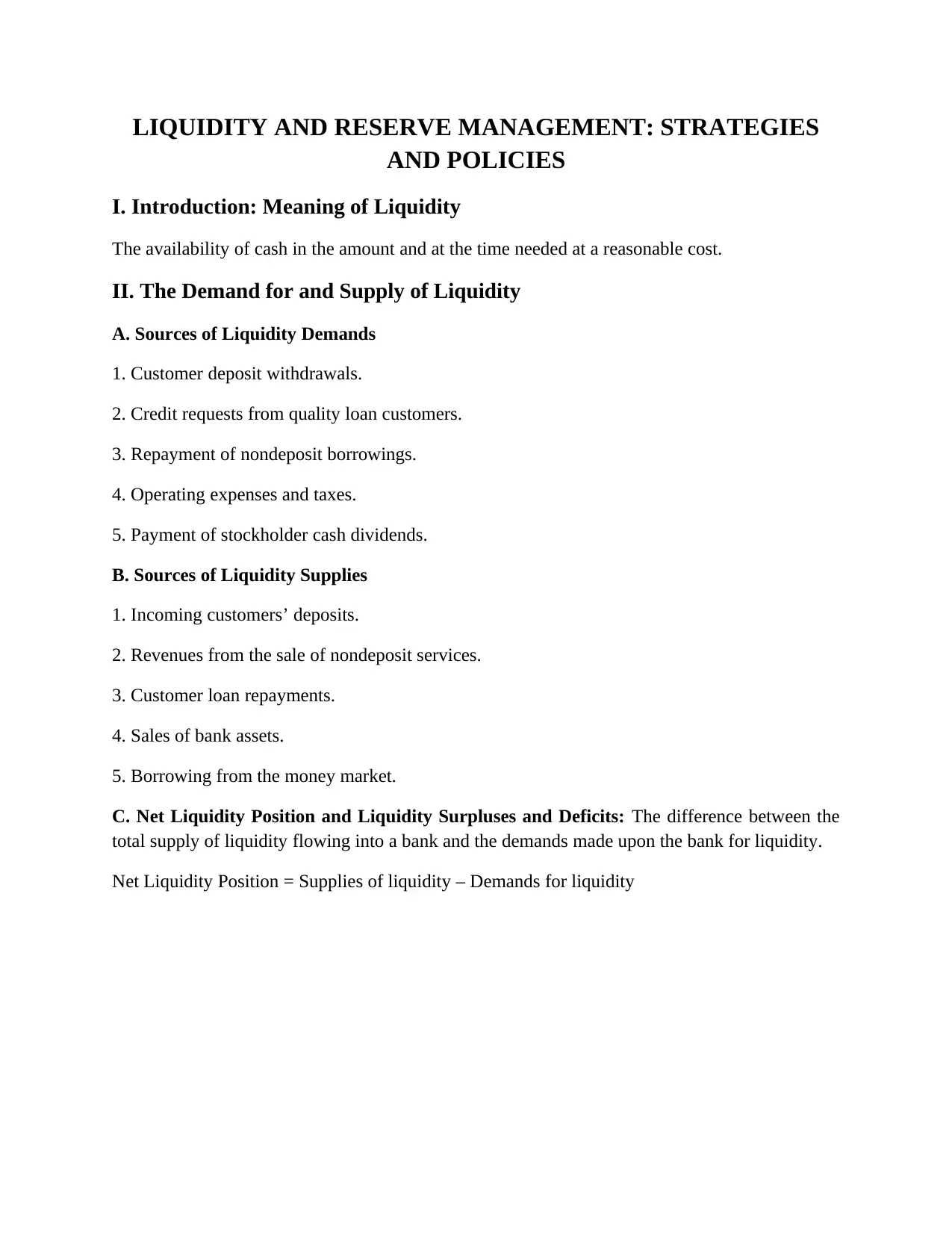

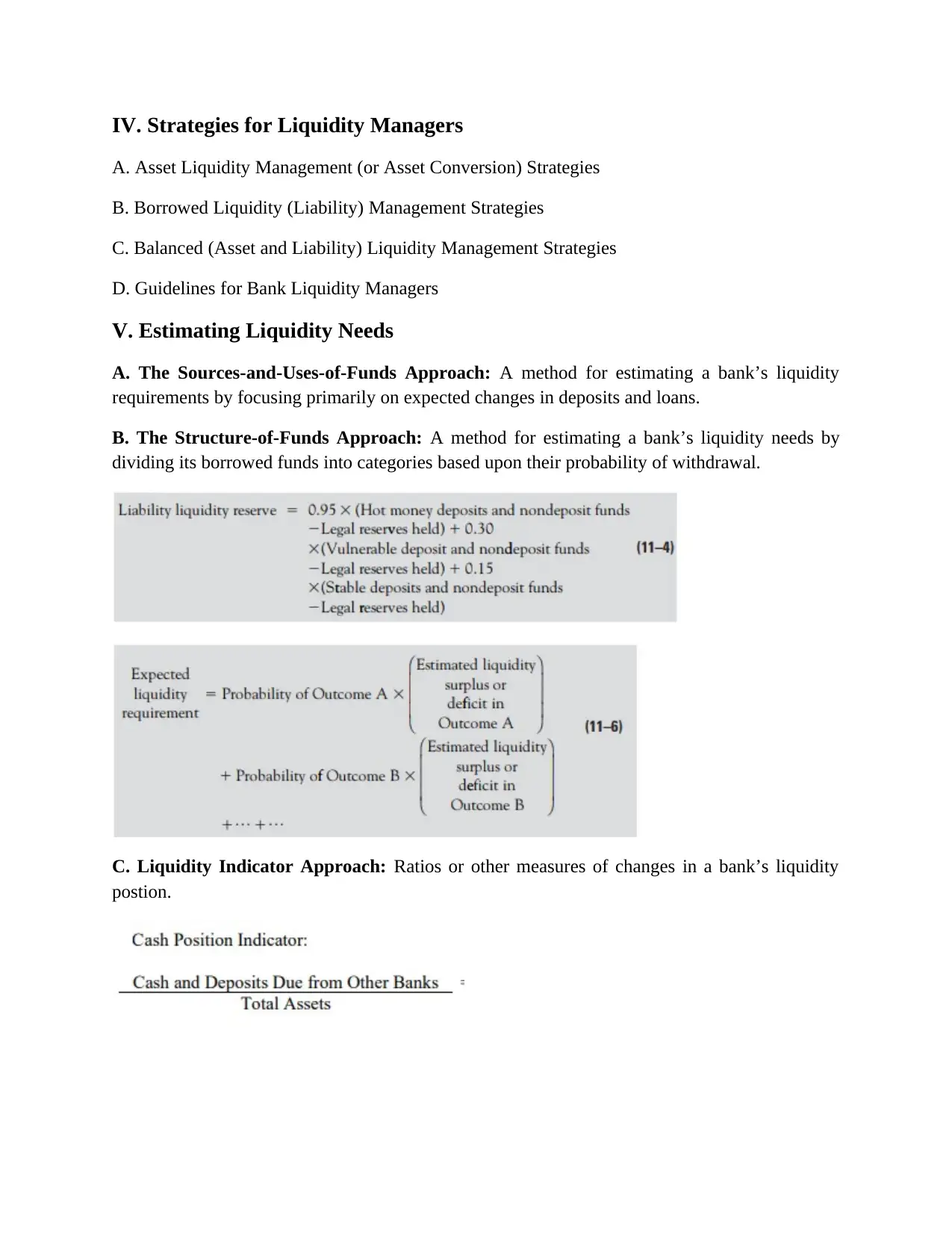

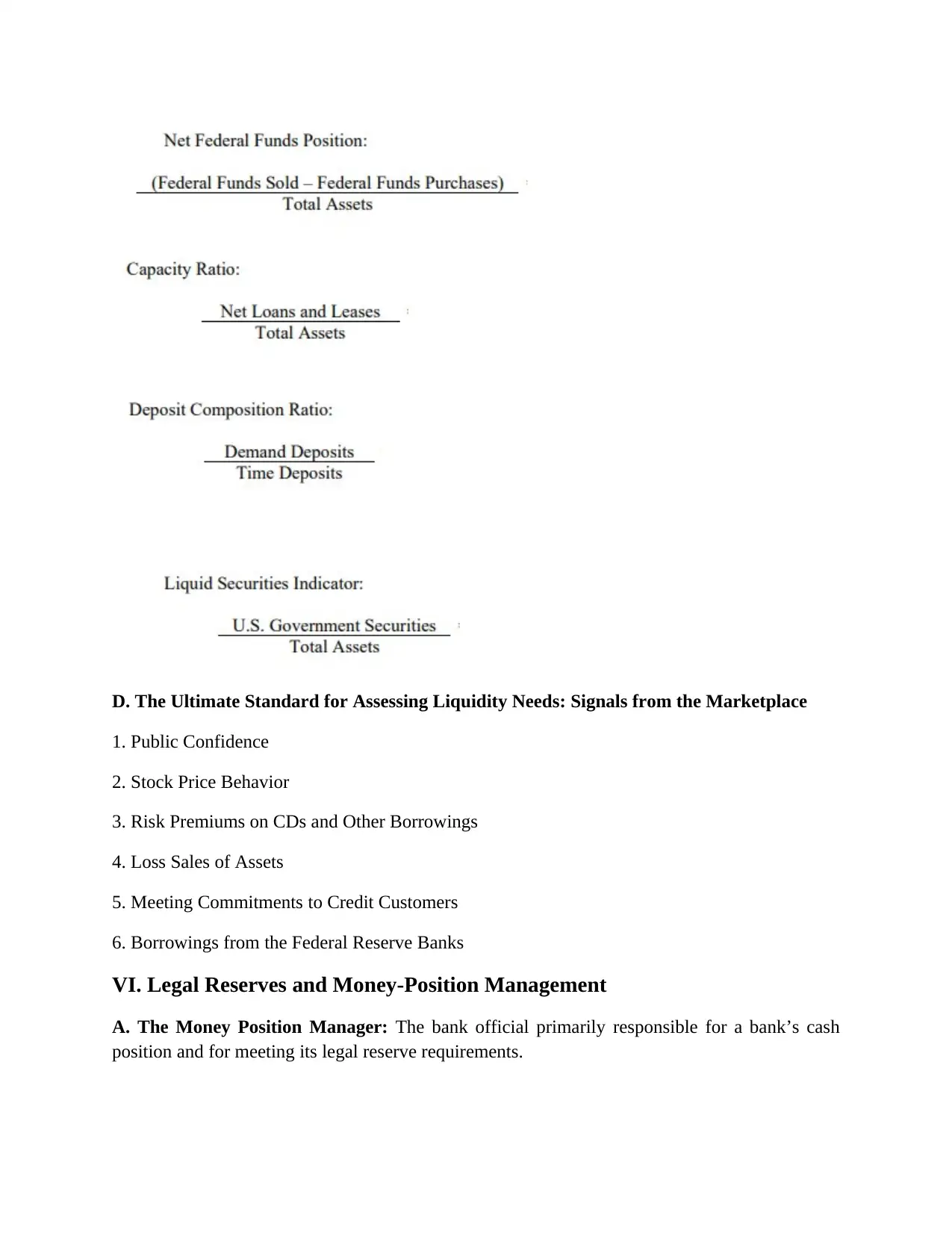

This report provides a comprehensive overview of the investment function within the banking and financial services sector. It delves into the roles investment securities play in bank portfolios, including stabilizing income, offsetting credit risk, providing diversification, ensuring liquidity, and reducing tax exposure. The report explores various investment instruments available to banks, categorizing them into money market and capital market instruments, and detailing popular instruments such as Treasury Bills, bonds, certificates of deposit, and corporate notes. Furthermore, it examines factors influencing the choice of investment securities, including expected rates of return, tax exposure, interest-rate risk, credit risk, business risk, liquidity risk, and other risks. It also discusses investment maturity strategies such as ladder, front-end load, back-end load, barbell, and rate expectations approaches, along with maturity management tools like the yield curve and duration. Finally, the report addresses liquidity and reserve management strategies, including asset, liability, and balanced approaches, and the significance of legal reserves and money-position management. The analysis includes the sources and uses of funds, factors influencing the money position, and the role of central bank reserve requirements.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.