Corporate Accounting: Investment, Liquidation & Consolidation Analysis

VerifiedAdded on 2023/06/08

|15

|2781

|98

Report

AI Summary

This assignment solution delves into various aspects of corporate accounting, providing detailed explanations and journal entries for investment in joint ventures, allocation to beneficiaries in liquidation scenarios, and consolidation analysis. It includes calculations for the value of investment, share in profit, goodwill, and the proportion of unsecured options in liquidation. The document also presents consolidated journal entries, addressing share capital, retained earnings, and non-controlling interests. Furthermore, it offers a business report analyzing the requirements for consolidating financial statements according to AASB 10, considering factors such as control, power, and influence over investee entities like Struggle Ltd., VBCL, and MSCL. This comprehensive resource helps in understanding complex accounting procedures and standards.

Corporate Accounting

Corporate Accounting

1 | P a g e

Corporate Accounting

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

Contents

Solution1: Accounting for Investment in Joint Ventures.......................................................................3

Solution 2: Allocation to beneficiaries in case of Liquidation................................................................8

Solution 3: Journal Entries in Consolidation........................................................................................10

Solution 4: Consolidation Analysis.......................................................................................................12

References:..........................................................................................................................................14

2 | P a g e

Contents

Solution1: Accounting for Investment in Joint Ventures.......................................................................3

Solution 2: Allocation to beneficiaries in case of Liquidation................................................................8

Solution 3: Journal Entries in Consolidation........................................................................................10

Solution 4: Consolidation Analysis.......................................................................................................12

References:..........................................................................................................................................14

2 | P a g e

Corporate Accounting

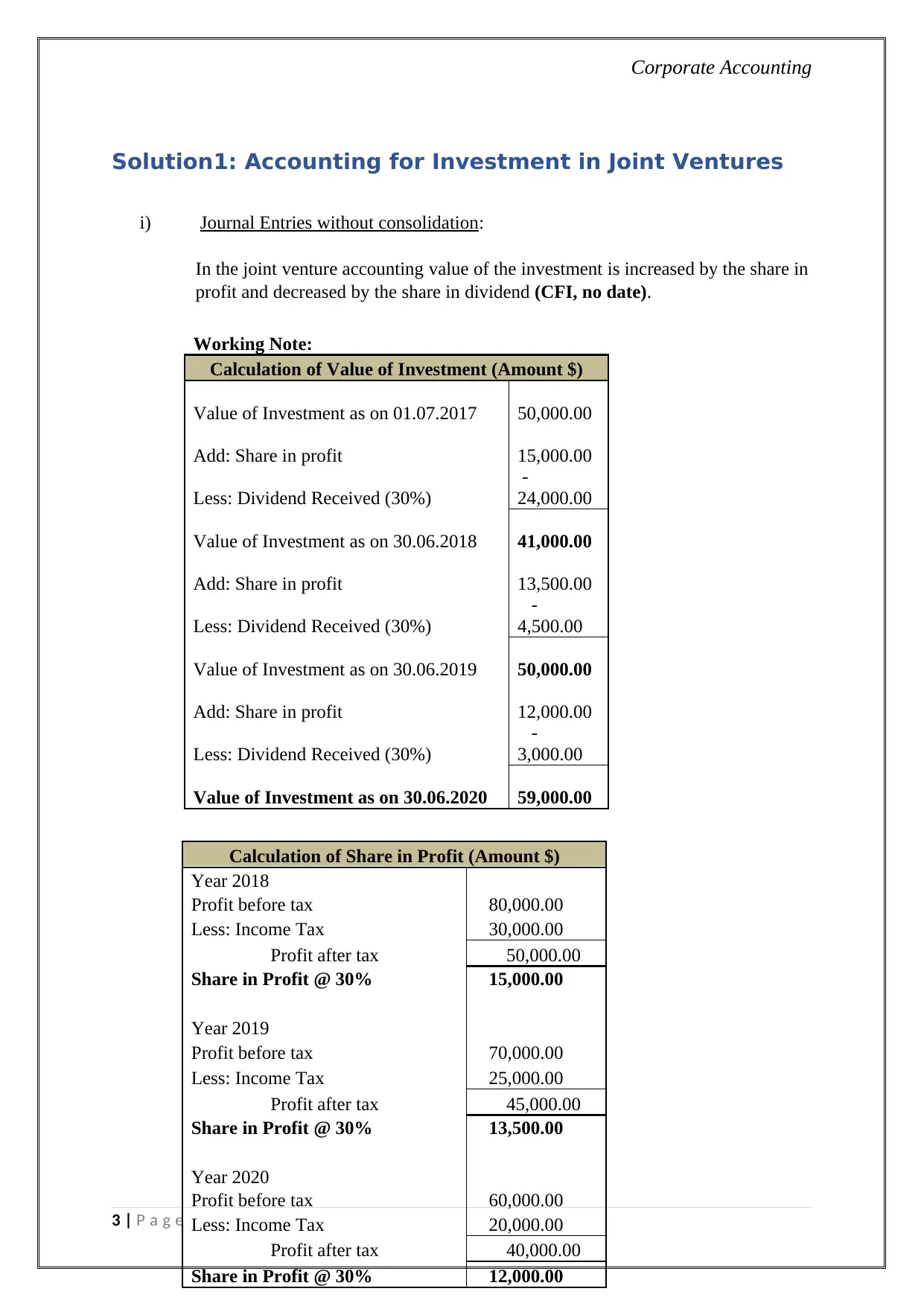

Solution1: Accounting for Investment in Joint Ventures

i) Journal Entries without consolidation:

In the joint venture accounting value of the investment is increased by the share in

profit and decreased by the share in dividend (CFI, no date).

3 | P a g e

Working Note:

Calculation of Value of Investment (Amount $)

Value of Investment as on 01.07.2017 50,000.00

Add: Share in profit 15,000.00

Less: Dividend Received (30%)

-

24,000.00

Value of Investment as on 30.06.2018 41,000.00

Add: Share in profit 13,500.00

Less: Dividend Received (30%)

-

4,500.00

Value of Investment as on 30.06.2019 50,000.00

Add: Share in profit 12,000.00

Less: Dividend Received (30%)

-

3,000.00

Value of Investment as on 30.06.2020 59,000.00

Calculation of Share in Profit (Amount $)

Year 2018

Profit before tax 80,000.00

Less: Income Tax 30,000.00

Profit after tax 50,000.00

Share in Profit @ 30% 15,000.00

Year 2019

Profit before tax 70,000.00

Less: Income Tax 25,000.00

Profit after tax 45,000.00

Share in Profit @ 30% 13,500.00

Year 2020

Profit before tax 60,000.00

Less: Income Tax 20,000.00

Profit after tax 40,000.00

Share in Profit @ 30% 12,000.00

Solution1: Accounting for Investment in Joint Ventures

i) Journal Entries without consolidation:

In the joint venture accounting value of the investment is increased by the share in

profit and decreased by the share in dividend (CFI, no date).

3 | P a g e

Working Note:

Calculation of Value of Investment (Amount $)

Value of Investment as on 01.07.2017 50,000.00

Add: Share in profit 15,000.00

Less: Dividend Received (30%)

-

24,000.00

Value of Investment as on 30.06.2018 41,000.00

Add: Share in profit 13,500.00

Less: Dividend Received (30%)

-

4,500.00

Value of Investment as on 30.06.2019 50,000.00

Add: Share in profit 12,000.00

Less: Dividend Received (30%)

-

3,000.00

Value of Investment as on 30.06.2020 59,000.00

Calculation of Share in Profit (Amount $)

Year 2018

Profit before tax 80,000.00

Less: Income Tax 30,000.00

Profit after tax 50,000.00

Share in Profit @ 30% 15,000.00

Year 2019

Profit before tax 70,000.00

Less: Income Tax 25,000.00

Profit after tax 45,000.00

Share in Profit @ 30% 13,500.00

Year 2020

Profit before tax 60,000.00

Less: Income Tax 20,000.00

Profit after tax 40,000.00

Share in Profit @ 30% 12,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

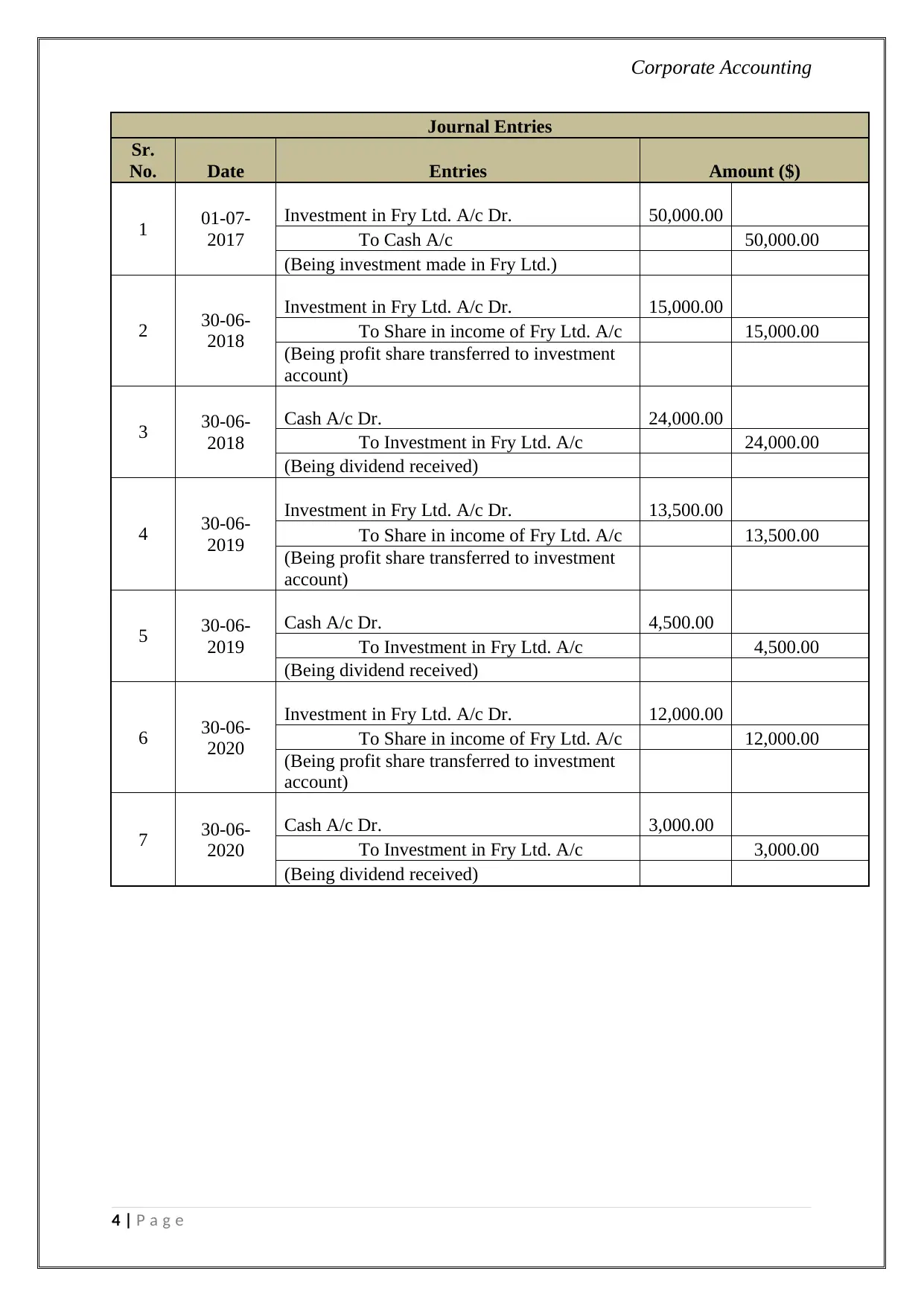

Journal Entries

Sr.

No. Date Entries Amount ($)

1 01-07-

2017

Investment in Fry Ltd. A/c Dr. 50,000.00

To Cash A/c 50,000.00

(Being investment made in Fry Ltd.)

2 30-06-

2018

Investment in Fry Ltd. A/c Dr. 15,000.00

To Share in income of Fry Ltd. A/c 15,000.00

(Being profit share transferred to investment

account)

3 30-06-

2018

Cash A/c Dr. 24,000.00

To Investment in Fry Ltd. A/c 24,000.00

(Being dividend received)

4 30-06-

2019

Investment in Fry Ltd. A/c Dr. 13,500.00

To Share in income of Fry Ltd. A/c 13,500.00

(Being profit share transferred to investment

account)

5 30-06-

2019

Cash A/c Dr. 4,500.00

To Investment in Fry Ltd. A/c 4,500.00

(Being dividend received)

6 30-06-

2020

Investment in Fry Ltd. A/c Dr. 12,000.00

To Share in income of Fry Ltd. A/c 12,000.00

(Being profit share transferred to investment

account)

7 30-06-

2020

Cash A/c Dr. 3,000.00

To Investment in Fry Ltd. A/c 3,000.00

(Being dividend received)

4 | P a g e

Journal Entries

Sr.

No. Date Entries Amount ($)

1 01-07-

2017

Investment in Fry Ltd. A/c Dr. 50,000.00

To Cash A/c 50,000.00

(Being investment made in Fry Ltd.)

2 30-06-

2018

Investment in Fry Ltd. A/c Dr. 15,000.00

To Share in income of Fry Ltd. A/c 15,000.00

(Being profit share transferred to investment

account)

3 30-06-

2018

Cash A/c Dr. 24,000.00

To Investment in Fry Ltd. A/c 24,000.00

(Being dividend received)

4 30-06-

2019

Investment in Fry Ltd. A/c Dr. 13,500.00

To Share in income of Fry Ltd. A/c 13,500.00

(Being profit share transferred to investment

account)

5 30-06-

2019

Cash A/c Dr. 4,500.00

To Investment in Fry Ltd. A/c 4,500.00

(Being dividend received)

6 30-06-

2020

Investment in Fry Ltd. A/c Dr. 12,000.00

To Share in income of Fry Ltd. A/c 12,000.00

(Being profit share transferred to investment

account)

7 30-06-

2020

Cash A/c Dr. 3,000.00

To Investment in Fry Ltd. A/c 3,000.00

(Being dividend received)

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

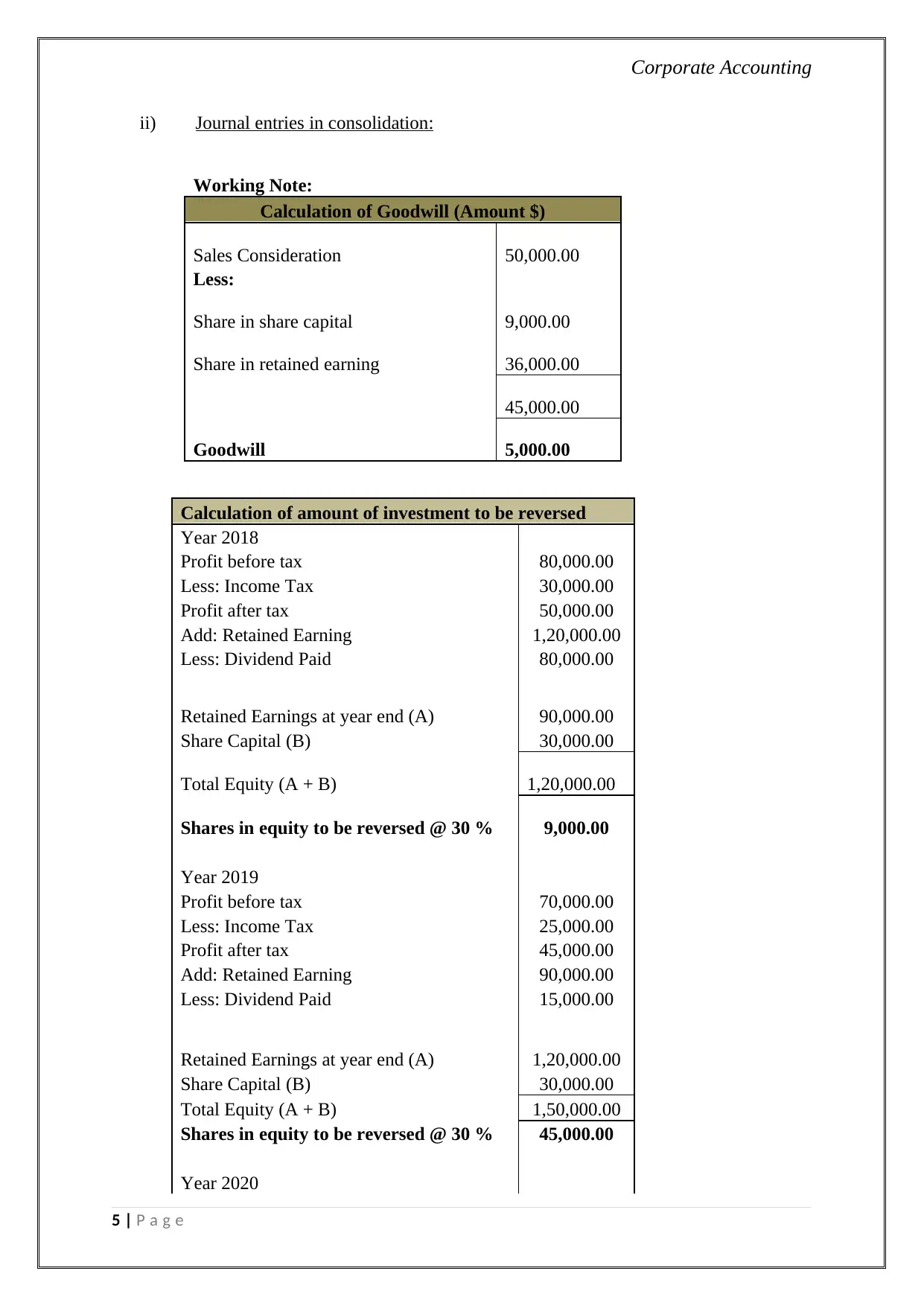

ii) Journal entries in consolidation:

Working Note:

Calculation of Goodwill (Amount $)

Sales Consideration 50,000.00

Less:

Share in share capital 9,000.00

Share in retained earning 36,000.00

45,000.00

Goodwill 5,000.00

Calculation of amount of investment to be reversed

Year 2018

Profit before tax 80,000.00

Less: Income Tax 30,000.00

Profit after tax 50,000.00

Add: Retained Earning 1,20,000.00

Less: Dividend Paid 80,000.00

Retained Earnings at year end (A) 90,000.00

Share Capital (B) 30,000.00

Total Equity (A + B) 1,20,000.00

Shares in equity to be reversed @ 30 % 9,000.00

Year 2019

Profit before tax 70,000.00

Less: Income Tax 25,000.00

Profit after tax 45,000.00

Add: Retained Earning 90,000.00

Less: Dividend Paid 15,000.00

Retained Earnings at year end (A) 1,20,000.00

Share Capital (B) 30,000.00

Total Equity (A + B) 1,50,000.00

Shares in equity to be reversed @ 30 % 45,000.00

Year 2020

5 | P a g e

ii) Journal entries in consolidation:

Working Note:

Calculation of Goodwill (Amount $)

Sales Consideration 50,000.00

Less:

Share in share capital 9,000.00

Share in retained earning 36,000.00

45,000.00

Goodwill 5,000.00

Calculation of amount of investment to be reversed

Year 2018

Profit before tax 80,000.00

Less: Income Tax 30,000.00

Profit after tax 50,000.00

Add: Retained Earning 1,20,000.00

Less: Dividend Paid 80,000.00

Retained Earnings at year end (A) 90,000.00

Share Capital (B) 30,000.00

Total Equity (A + B) 1,20,000.00

Shares in equity to be reversed @ 30 % 9,000.00

Year 2019

Profit before tax 70,000.00

Less: Income Tax 25,000.00

Profit after tax 45,000.00

Add: Retained Earning 90,000.00

Less: Dividend Paid 15,000.00

Retained Earnings at year end (A) 1,20,000.00

Share Capital (B) 30,000.00

Total Equity (A + B) 1,50,000.00

Shares in equity to be reversed @ 30 % 45,000.00

Year 2020

5 | P a g e

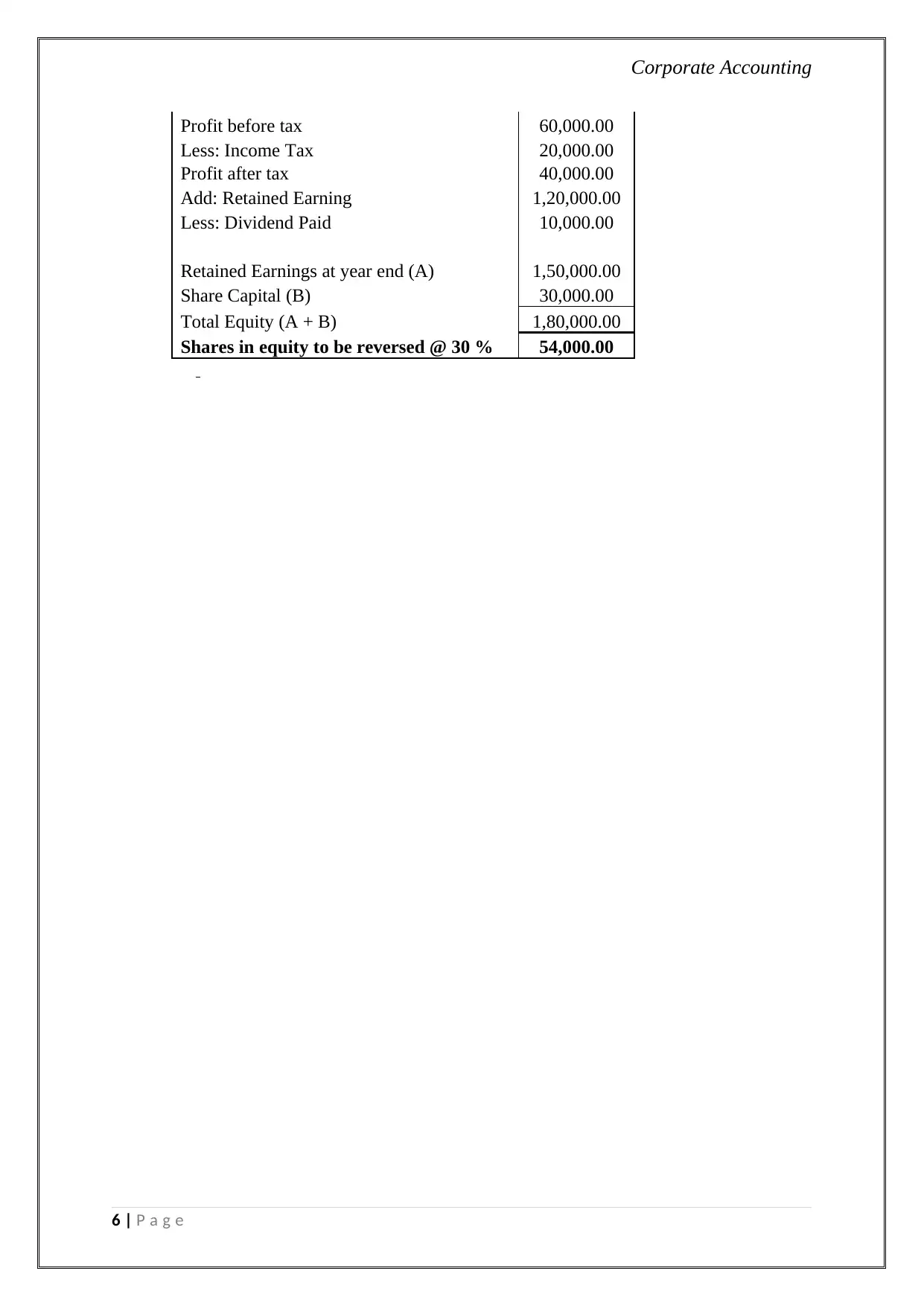

Corporate Accounting

Profit before tax 60,000.00

Less: Income Tax 20,000.00

Profit after tax 40,000.00

Add: Retained Earning 1,20,000.00

Less: Dividend Paid 10,000.00

Retained Earnings at year end (A) 1,50,000.00

Share Capital (B) 30,000.00

Total Equity (A + B) 1,80,000.00

Shares in equity to be reversed @ 30 % 54,000.00

6 | P a g e

Profit before tax 60,000.00

Less: Income Tax 20,000.00

Profit after tax 40,000.00

Add: Retained Earning 1,20,000.00

Less: Dividend Paid 10,000.00

Retained Earnings at year end (A) 1,50,000.00

Share Capital (B) 30,000.00

Total Equity (A + B) 1,80,000.00

Shares in equity to be reversed @ 30 % 54,000.00

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

Journal Entries

Sr.

No. Date Entries Amount ($)

1 01-07-

2017

Shares in equity of Fry Ltd. A/c Dr. 45,000.00

Goodwill A/c Dr. 5,000.00

To Cash A/c 50,000.00

(Being investment in Fly Ltd. recognized)

2 30-06-

2018

Dividend Income A/c Dr. 24,000.00

To Dividend Expense A/c 24,000.00

(Being dividend of Small Ltd. reversed)

3 30-06-

2018

Share Capital A/c Dr. 9,000.00

Retained Earnings A/c Dr. 27,000.00

To Share in equity of Fry Ltd. A/c 36,000.00

(Being investment in Fly Ltd. reversed)

4 30-06-

2018

Share Capital of Fry Ltd. A/c Dr. 21,000.00

Retained Earnings of Fry Ltd. A/c Dr. 63,000.00

To Minority Interest A/c 84,000.00

(Being share capital transferred to minority

interest)

5 30-06-

2019

Dividend Income A/c Dr. 4,500.00

To Dividend Expense A/c 4,500.00

(Being dividend of Small Ltd. reversed)

6 30-06-

2019

Share Capital A/c Dr. 9,000.00

Retained Earnings A/c Dr. 36,000.00

To Share in equity of Fry Ltd. A/c 45,000.00

(Being investment in Fly Ltd. reversed)

7 30-06-

2019

Share Capital of Fry Ltd. A/c Dr. 21,000.00

Retained Earnings of Fry Ltd. A/c Dr. 84,000.00

To Minority Interest A/c 1,05,000.00

(Being share capital transferred to minority

interest)

8 30-06- Dividend Income A/c Dr.

7 | P a g e

Journal Entries

Sr.

No. Date Entries Amount ($)

1 01-07-

2017

Shares in equity of Fry Ltd. A/c Dr. 45,000.00

Goodwill A/c Dr. 5,000.00

To Cash A/c 50,000.00

(Being investment in Fly Ltd. recognized)

2 30-06-

2018

Dividend Income A/c Dr. 24,000.00

To Dividend Expense A/c 24,000.00

(Being dividend of Small Ltd. reversed)

3 30-06-

2018

Share Capital A/c Dr. 9,000.00

Retained Earnings A/c Dr. 27,000.00

To Share in equity of Fry Ltd. A/c 36,000.00

(Being investment in Fly Ltd. reversed)

4 30-06-

2018

Share Capital of Fry Ltd. A/c Dr. 21,000.00

Retained Earnings of Fry Ltd. A/c Dr. 63,000.00

To Minority Interest A/c 84,000.00

(Being share capital transferred to minority

interest)

5 30-06-

2019

Dividend Income A/c Dr. 4,500.00

To Dividend Expense A/c 4,500.00

(Being dividend of Small Ltd. reversed)

6 30-06-

2019

Share Capital A/c Dr. 9,000.00

Retained Earnings A/c Dr. 36,000.00

To Share in equity of Fry Ltd. A/c 45,000.00

(Being investment in Fly Ltd. reversed)

7 30-06-

2019

Share Capital of Fry Ltd. A/c Dr. 21,000.00

Retained Earnings of Fry Ltd. A/c Dr. 84,000.00

To Minority Interest A/c 1,05,000.00

(Being share capital transferred to minority

interest)

8 30-06- Dividend Income A/c Dr.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

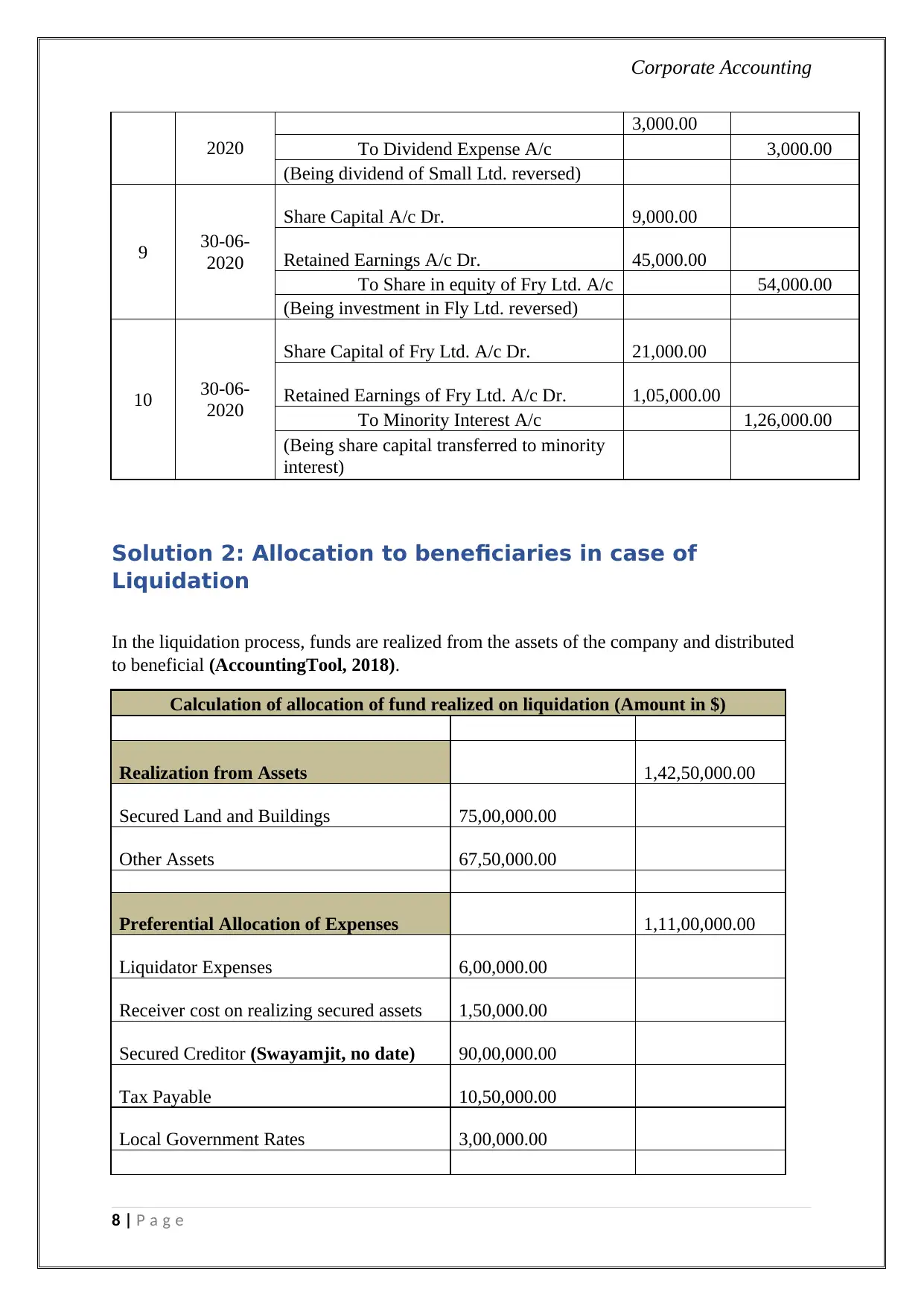

2020

3,000.00

To Dividend Expense A/c 3,000.00

(Being dividend of Small Ltd. reversed)

9 30-06-

2020

Share Capital A/c Dr. 9,000.00

Retained Earnings A/c Dr. 45,000.00

To Share in equity of Fry Ltd. A/c 54,000.00

(Being investment in Fly Ltd. reversed)

10 30-06-

2020

Share Capital of Fry Ltd. A/c Dr. 21,000.00

Retained Earnings of Fry Ltd. A/c Dr. 1,05,000.00

To Minority Interest A/c 1,26,000.00

(Being share capital transferred to minority

interest)

Solution 2: Allocation to beneficiaries in case of

Liquidation

In the liquidation process, funds are realized from the assets of the company and distributed

to beneficial (AccountingTool, 2018).

Calculation of allocation of fund realized on liquidation (Amount in $)

Realization from Assets 1,42,50,000.00

Secured Land and Buildings 75,00,000.00

Other Assets 67,50,000.00

Preferential Allocation of Expenses 1,11,00,000.00

Liquidator Expenses 6,00,000.00

Receiver cost on realizing secured assets 1,50,000.00

Secured Creditor (Swayamjit, no date) 90,00,000.00

Tax Payable 10,50,000.00

Local Government Rates 3,00,000.00

8 | P a g e

2020

3,000.00

To Dividend Expense A/c 3,000.00

(Being dividend of Small Ltd. reversed)

9 30-06-

2020

Share Capital A/c Dr. 9,000.00

Retained Earnings A/c Dr. 45,000.00

To Share in equity of Fry Ltd. A/c 54,000.00

(Being investment in Fly Ltd. reversed)

10 30-06-

2020

Share Capital of Fry Ltd. A/c Dr. 21,000.00

Retained Earnings of Fry Ltd. A/c Dr. 1,05,000.00

To Minority Interest A/c 1,26,000.00

(Being share capital transferred to minority

interest)

Solution 2: Allocation to beneficiaries in case of

Liquidation

In the liquidation process, funds are realized from the assets of the company and distributed

to beneficial (AccountingTool, 2018).

Calculation of allocation of fund realized on liquidation (Amount in $)

Realization from Assets 1,42,50,000.00

Secured Land and Buildings 75,00,000.00

Other Assets 67,50,000.00

Preferential Allocation of Expenses 1,11,00,000.00

Liquidator Expenses 6,00,000.00

Receiver cost on realizing secured assets 1,50,000.00

Secured Creditor (Swayamjit, no date) 90,00,000.00

Tax Payable 10,50,000.00

Local Government Rates 3,00,000.00

8 | P a g e

Corporate Accounting

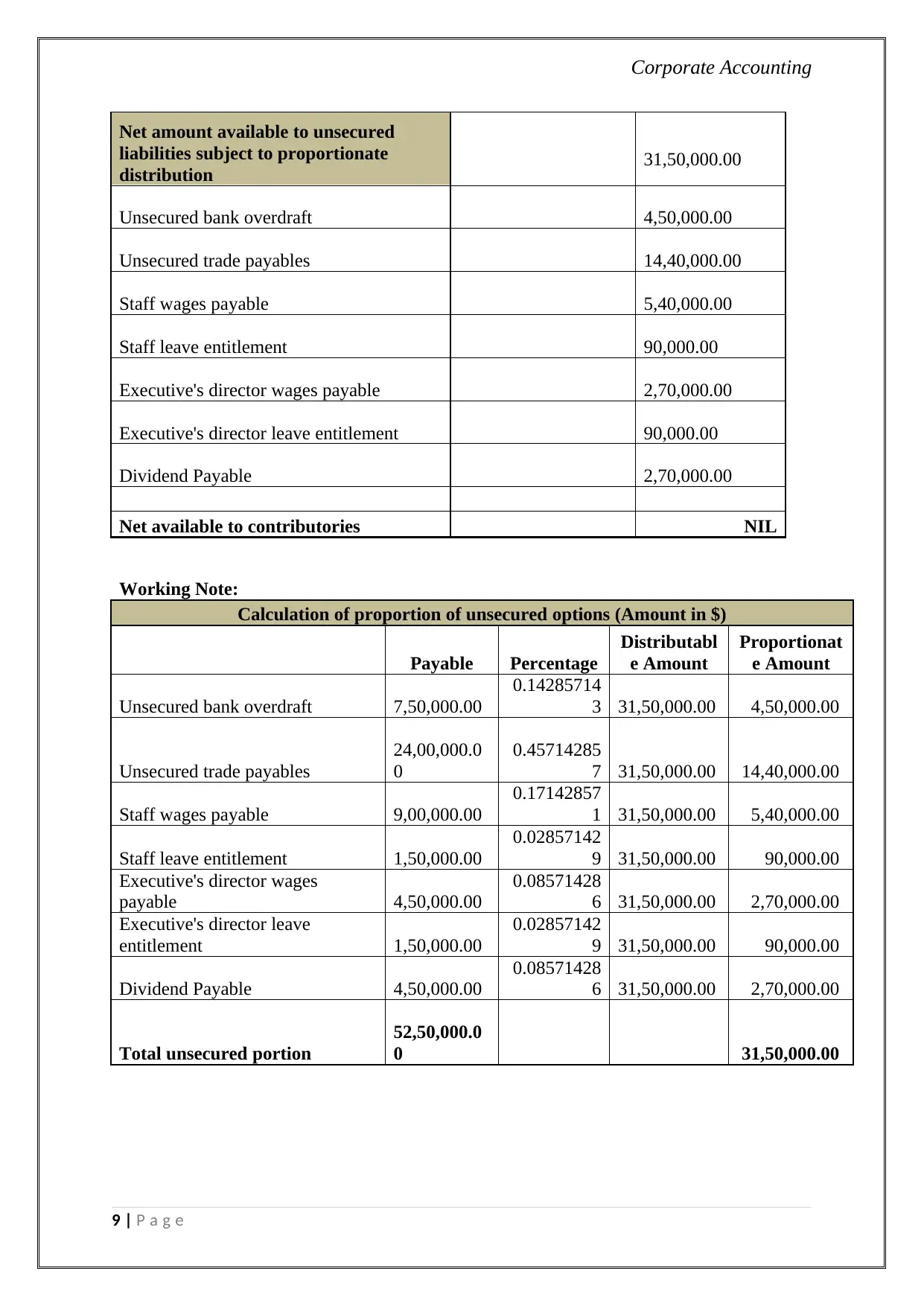

Net amount available to unsecured

liabilities subject to proportionate

distribution 31,50,000.00

Unsecured bank overdraft 4,50,000.00

Unsecured trade payables 14,40,000.00

Staff wages payable 5,40,000.00

Staff leave entitlement 90,000.00

Executive's director wages payable 2,70,000.00

Executive's director leave entitlement 90,000.00

Dividend Payable 2,70,000.00

Net available to contributories NIL

Working Note:

Calculation of proportion of unsecured options (Amount in $)

Payable Percentage

Distributabl

e Amount

Proportionat

e Amount

Unsecured bank overdraft 7,50,000.00

0.14285714

3 31,50,000.00 4,50,000.00

Unsecured trade payables

24,00,000.0

0

0.45714285

7 31,50,000.00 14,40,000.00

Staff wages payable 9,00,000.00

0.17142857

1 31,50,000.00 5,40,000.00

Staff leave entitlement 1,50,000.00

0.02857142

9 31,50,000.00 90,000.00

Executive's director wages

payable 4,50,000.00

0.08571428

6 31,50,000.00 2,70,000.00

Executive's director leave

entitlement 1,50,000.00

0.02857142

9 31,50,000.00 90,000.00

Dividend Payable 4,50,000.00

0.08571428

6 31,50,000.00 2,70,000.00

Total unsecured portion

52,50,000.0

0 31,50,000.00

9 | P a g e

Net amount available to unsecured

liabilities subject to proportionate

distribution 31,50,000.00

Unsecured bank overdraft 4,50,000.00

Unsecured trade payables 14,40,000.00

Staff wages payable 5,40,000.00

Staff leave entitlement 90,000.00

Executive's director wages payable 2,70,000.00

Executive's director leave entitlement 90,000.00

Dividend Payable 2,70,000.00

Net available to contributories NIL

Working Note:

Calculation of proportion of unsecured options (Amount in $)

Payable Percentage

Distributabl

e Amount

Proportionat

e Amount

Unsecured bank overdraft 7,50,000.00

0.14285714

3 31,50,000.00 4,50,000.00

Unsecured trade payables

24,00,000.0

0

0.45714285

7 31,50,000.00 14,40,000.00

Staff wages payable 9,00,000.00

0.17142857

1 31,50,000.00 5,40,000.00

Staff leave entitlement 1,50,000.00

0.02857142

9 31,50,000.00 90,000.00

Executive's director wages

payable 4,50,000.00

0.08571428

6 31,50,000.00 2,70,000.00

Executive's director leave

entitlement 1,50,000.00

0.02857142

9 31,50,000.00 90,000.00

Dividend Payable 4,50,000.00

0.08571428

6 31,50,000.00 2,70,000.00

Total unsecured portion

52,50,000.0

0 31,50,000.00

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

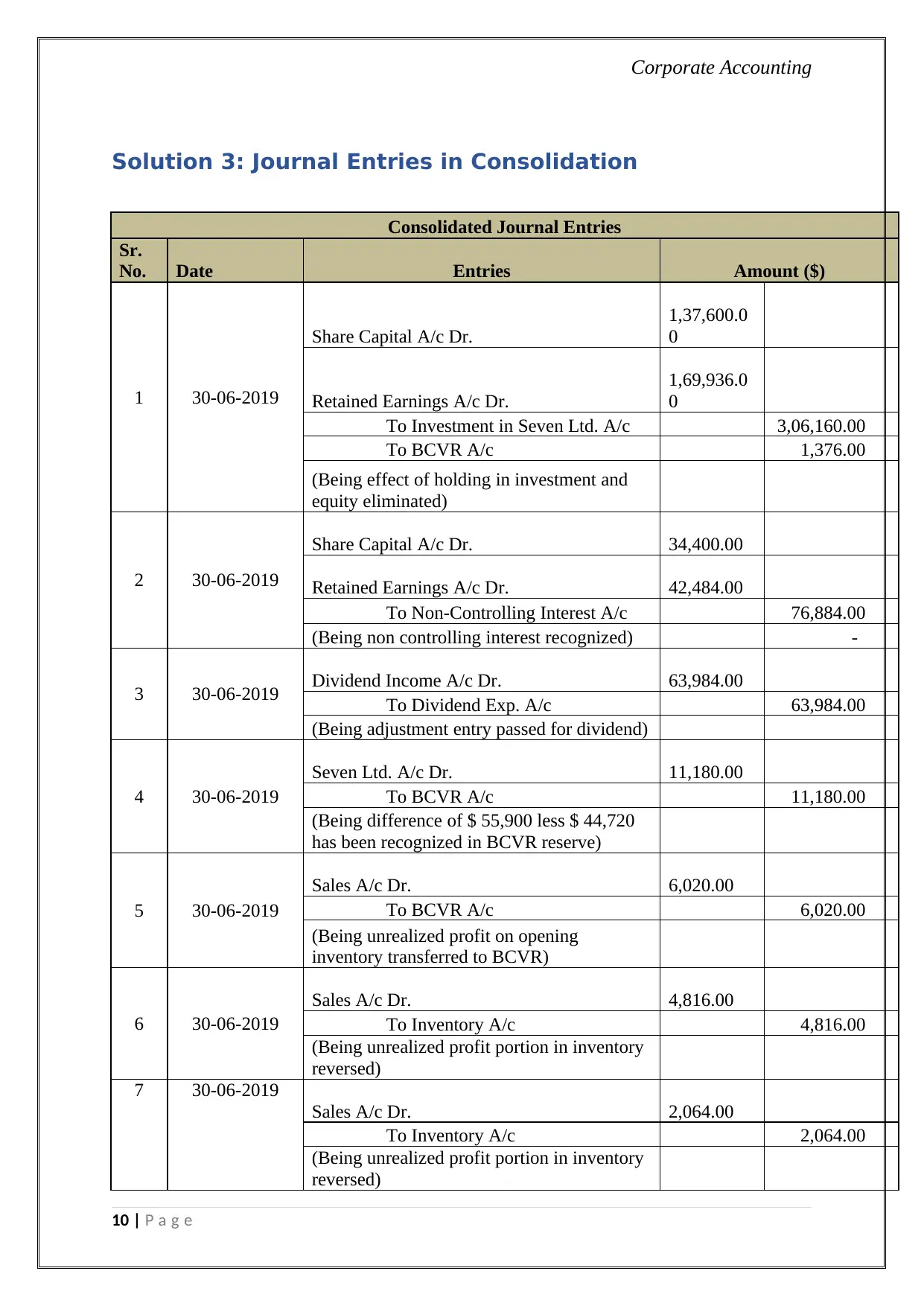

Solution 3: Journal Entries in Consolidation

Consolidated Journal Entries

Sr.

No. Date Entries Amount ($)

1 30-06-2019

Share Capital A/c Dr.

1,37,600.0

0

Retained Earnings A/c Dr.

1,69,936.0

0

To Investment in Seven Ltd. A/c 3,06,160.00

To BCVR A/c 1,376.00

(Being effect of holding in investment and

equity eliminated)

2 30-06-2019

Share Capital A/c Dr. 34,400.00

Retained Earnings A/c Dr. 42,484.00

To Non-Controlling Interest A/c 76,884.00

(Being non controlling interest recognized) -

3 30-06-2019 Dividend Income A/c Dr. 63,984.00

To Dividend Exp. A/c 63,984.00

(Being adjustment entry passed for dividend)

4 30-06-2019

Seven Ltd. A/c Dr. 11,180.00

To BCVR A/c 11,180.00

(Being difference of $ 55,900 less $ 44,720

has been recognized in BCVR reserve)

5 30-06-2019

Sales A/c Dr. 6,020.00

To BCVR A/c 6,020.00

(Being unrealized profit on opening

inventory transferred to BCVR)

6 30-06-2019

Sales A/c Dr. 4,816.00

To Inventory A/c 4,816.00

(Being unrealized profit portion in inventory

reversed)

7 30-06-2019

Sales A/c Dr. 2,064.00

To Inventory A/c 2,064.00

(Being unrealized profit portion in inventory

reversed)

10 | P a g e

Solution 3: Journal Entries in Consolidation

Consolidated Journal Entries

Sr.

No. Date Entries Amount ($)

1 30-06-2019

Share Capital A/c Dr.

1,37,600.0

0

Retained Earnings A/c Dr.

1,69,936.0

0

To Investment in Seven Ltd. A/c 3,06,160.00

To BCVR A/c 1,376.00

(Being effect of holding in investment and

equity eliminated)

2 30-06-2019

Share Capital A/c Dr. 34,400.00

Retained Earnings A/c Dr. 42,484.00

To Non-Controlling Interest A/c 76,884.00

(Being non controlling interest recognized) -

3 30-06-2019 Dividend Income A/c Dr. 63,984.00

To Dividend Exp. A/c 63,984.00

(Being adjustment entry passed for dividend)

4 30-06-2019

Seven Ltd. A/c Dr. 11,180.00

To BCVR A/c 11,180.00

(Being difference of $ 55,900 less $ 44,720

has been recognized in BCVR reserve)

5 30-06-2019

Sales A/c Dr. 6,020.00

To BCVR A/c 6,020.00

(Being unrealized profit on opening

inventory transferred to BCVR)

6 30-06-2019

Sales A/c Dr. 4,816.00

To Inventory A/c 4,816.00

(Being unrealized profit portion in inventory

reversed)

7 30-06-2019

Sales A/c Dr. 2,064.00

To Inventory A/c 2,064.00

(Being unrealized profit portion in inventory

reversed)

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

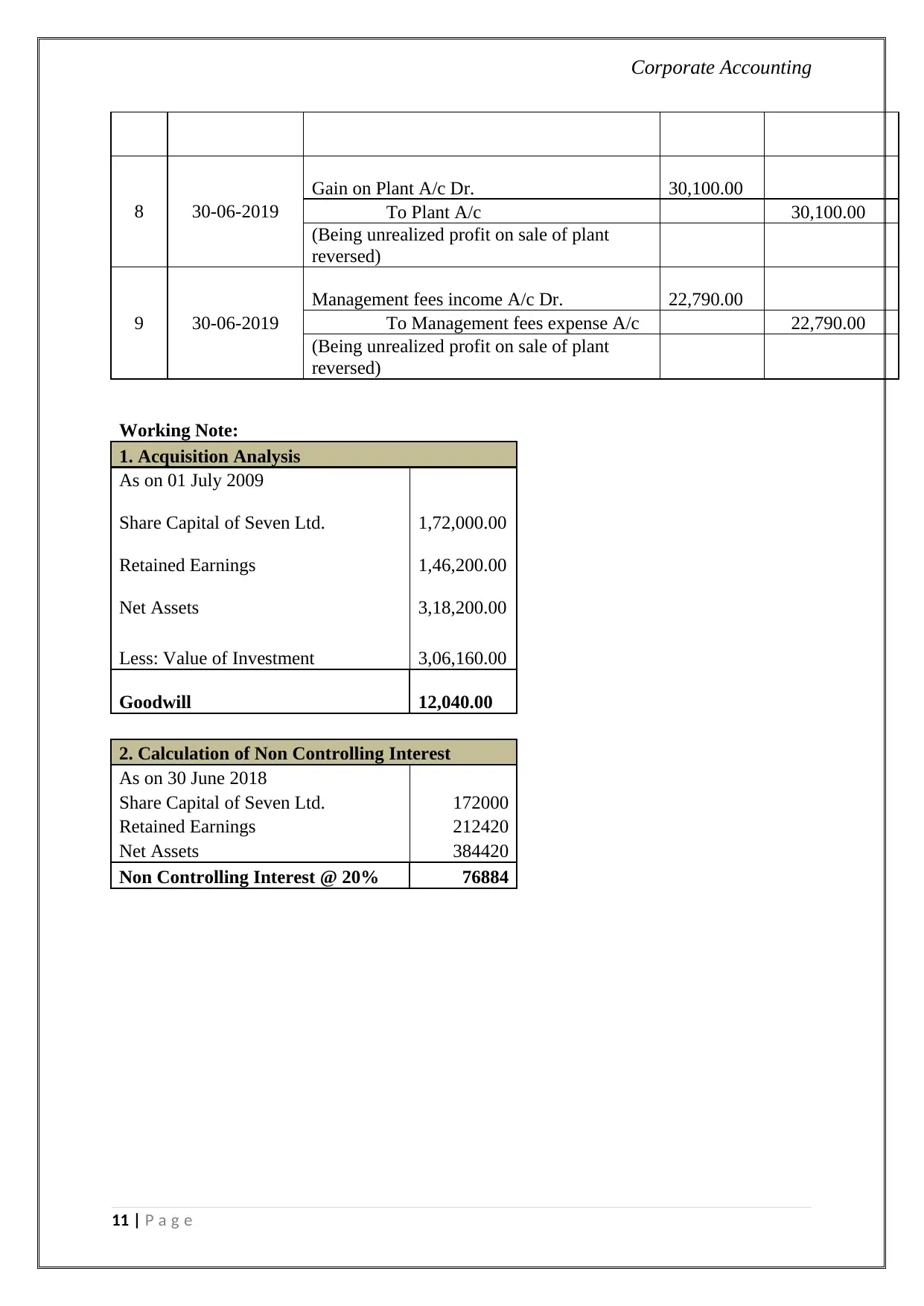

8 30-06-2019

Gain on Plant A/c Dr. 30,100.00

To Plant A/c 30,100.00

(Being unrealized profit on sale of plant

reversed)

9 30-06-2019

Management fees income A/c Dr. 22,790.00

To Management fees expense A/c 22,790.00

(Being unrealized profit on sale of plant

reversed)

Working Note:

1. Acquisition Analysis

As on 01 July 2009

Share Capital of Seven Ltd. 1,72,000.00

Retained Earnings 1,46,200.00

Net Assets 3,18,200.00

Less: Value of Investment 3,06,160.00

Goodwill 12,040.00

2. Calculation of Non Controlling Interest

As on 30 June 2018

Share Capital of Seven Ltd. 172000

Retained Earnings 212420

Net Assets 384420

Non Controlling Interest @ 20% 76884

11 | P a g e

8 30-06-2019

Gain on Plant A/c Dr. 30,100.00

To Plant A/c 30,100.00

(Being unrealized profit on sale of plant

reversed)

9 30-06-2019

Management fees income A/c Dr. 22,790.00

To Management fees expense A/c 22,790.00

(Being unrealized profit on sale of plant

reversed)

Working Note:

1. Acquisition Analysis

As on 01 July 2009

Share Capital of Seven Ltd. 1,72,000.00

Retained Earnings 1,46,200.00

Net Assets 3,18,200.00

Less: Value of Investment 3,06,160.00

Goodwill 12,040.00

2. Calculation of Non Controlling Interest

As on 30 June 2018

Share Capital of Seven Ltd. 172000

Retained Earnings 212420

Net Assets 384420

Non Controlling Interest @ 20% 76884

11 | P a g e

Corporate Accounting

Solution 4: Consolidation Analysis

Business Report

Report To : Bill Handy

Designation : Finance Director

Company : Northern Australia Global Investment Ltd (NAGIL)

Subject : Requirement of consolidation of financial statements

Background:

The company has made the investment in number of other entities. It has also

provided the loan to some entities. Consolidation becomes important in this

position as required by AASB 10. We are providing the consolidation analysis

case to case which is as follows:

i) According to AASB 10 “Consolidated Financial Statement”, an entity

should consolidate its financial statement with its subsidiaries, associates,

joint ventures on which the entity can exercise control (Knapp, 2013).

AASB 10 defines the term controls as if the investor is able to exercise his

right in respect of variable returns for the investee & also able to affect the

return through the utilization of power with respect to investee. AASB 10

also defines the term power which means that the investor has the ability

to affect the operational activities of the company (AASB, no date).

In the instant case, the company NAGIL holds the 70 percent stake in the

Struggle Ltd. AASB 10 does not prescribe the specific limit for the

consolidation of the financial statements between two entities. NAGIL

does not hold any position in the board of directors and also it does not

involve in the regular activities (PWC, no date). But, it has substantial

holding in the Struggle Ltd., which means that it any decision in the

Struggle Ltd. may be affected by the NAGIL. As such, NAGIL has

appropriate control in the Struggle Ltd., which may affect the NAGIL’s

return on investment. As such, Para 10 to 18 of AASB has been justified

by the NAGIL.

It may be concluded that NAGIL may prepare the consolidated financial

statement with the company Struggle Ltd.

ii) AASB 10 describes that control through the equity portion is not enough

for the determination of consolidation requirement between two entities.

According to the standard there are no hard and fast rules for the

consolidation requirement (Deloitte, no date). The consolidation is

already based on facts and circumstances of the particular case.

12 | P a g e

Solution 4: Consolidation Analysis

Business Report

Report To : Bill Handy

Designation : Finance Director

Company : Northern Australia Global Investment Ltd (NAGIL)

Subject : Requirement of consolidation of financial statements

Background:

The company has made the investment in number of other entities. It has also

provided the loan to some entities. Consolidation becomes important in this

position as required by AASB 10. We are providing the consolidation analysis

case to case which is as follows:

i) According to AASB 10 “Consolidated Financial Statement”, an entity

should consolidate its financial statement with its subsidiaries, associates,

joint ventures on which the entity can exercise control (Knapp, 2013).

AASB 10 defines the term controls as if the investor is able to exercise his

right in respect of variable returns for the investee & also able to affect the

return through the utilization of power with respect to investee. AASB 10

also defines the term power which means that the investor has the ability

to affect the operational activities of the company (AASB, no date).

In the instant case, the company NAGIL holds the 70 percent stake in the

Struggle Ltd. AASB 10 does not prescribe the specific limit for the

consolidation of the financial statements between two entities. NAGIL

does not hold any position in the board of directors and also it does not

involve in the regular activities (PWC, no date). But, it has substantial

holding in the Struggle Ltd., which means that it any decision in the

Struggle Ltd. may be affected by the NAGIL. As such, NAGIL has

appropriate control in the Struggle Ltd., which may affect the NAGIL’s

return on investment. As such, Para 10 to 18 of AASB has been justified

by the NAGIL.

It may be concluded that NAGIL may prepare the consolidated financial

statement with the company Struggle Ltd.

ii) AASB 10 describes that control through the equity portion is not enough

for the determination of consolidation requirement between two entities.

According to the standard there are no hard and fast rules for the

consolidation requirement (Deloitte, no date). The consolidation is

already based on facts and circumstances of the particular case.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.