Investment Management Report: Bond Pricing, Yields, and Risk Analysis

VerifiedAdded on 2021/02/22

|19

|4950

|78

Report

AI Summary

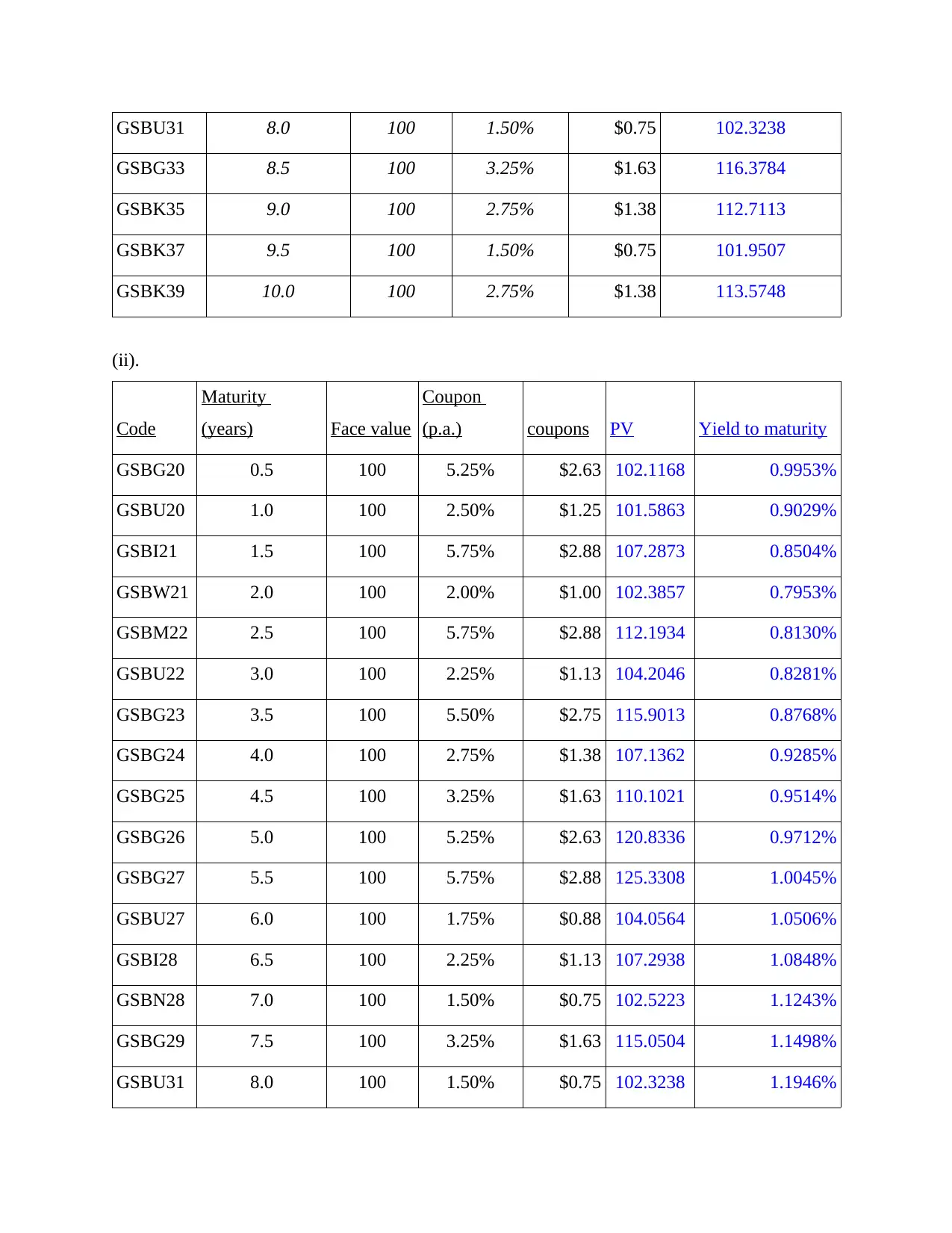

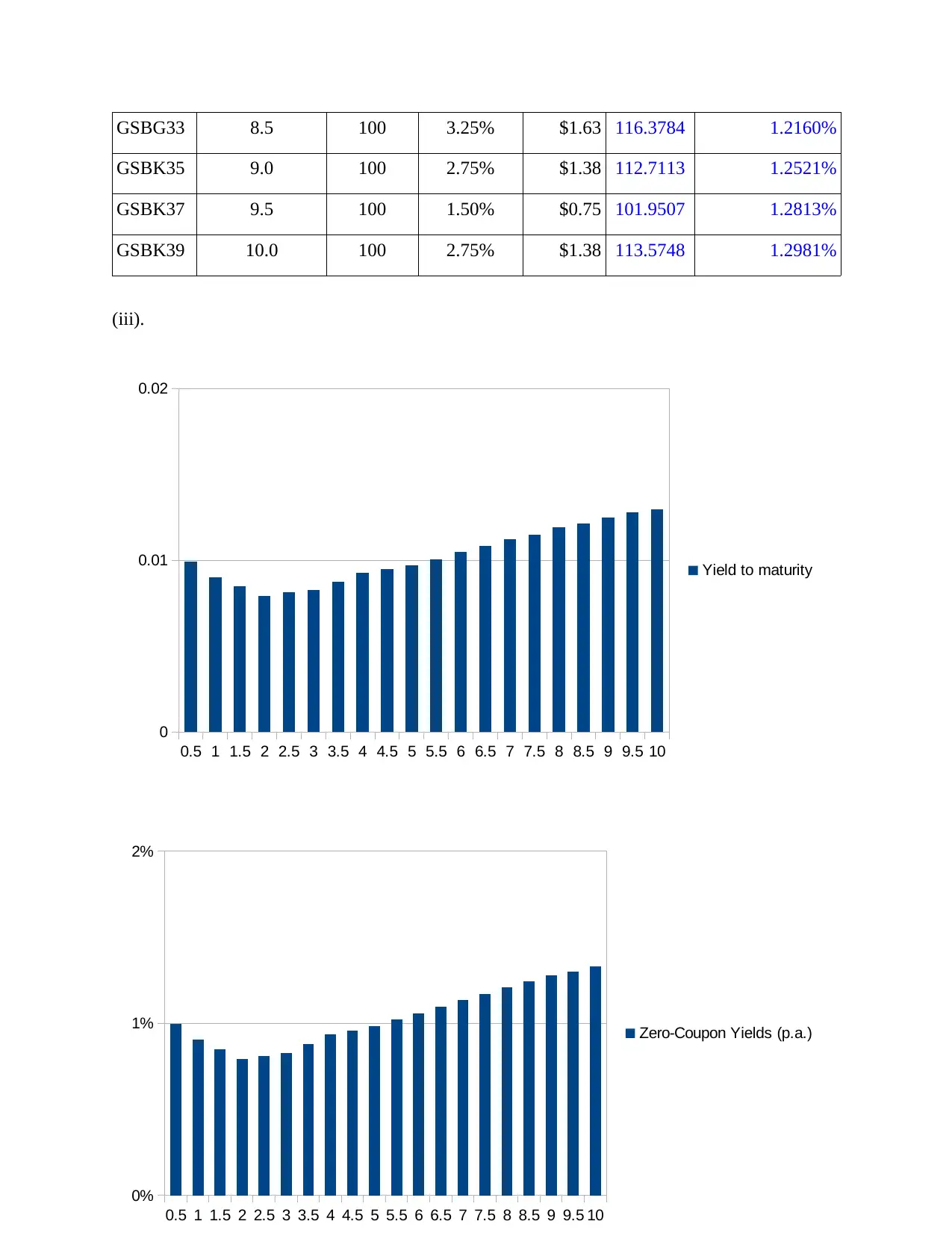

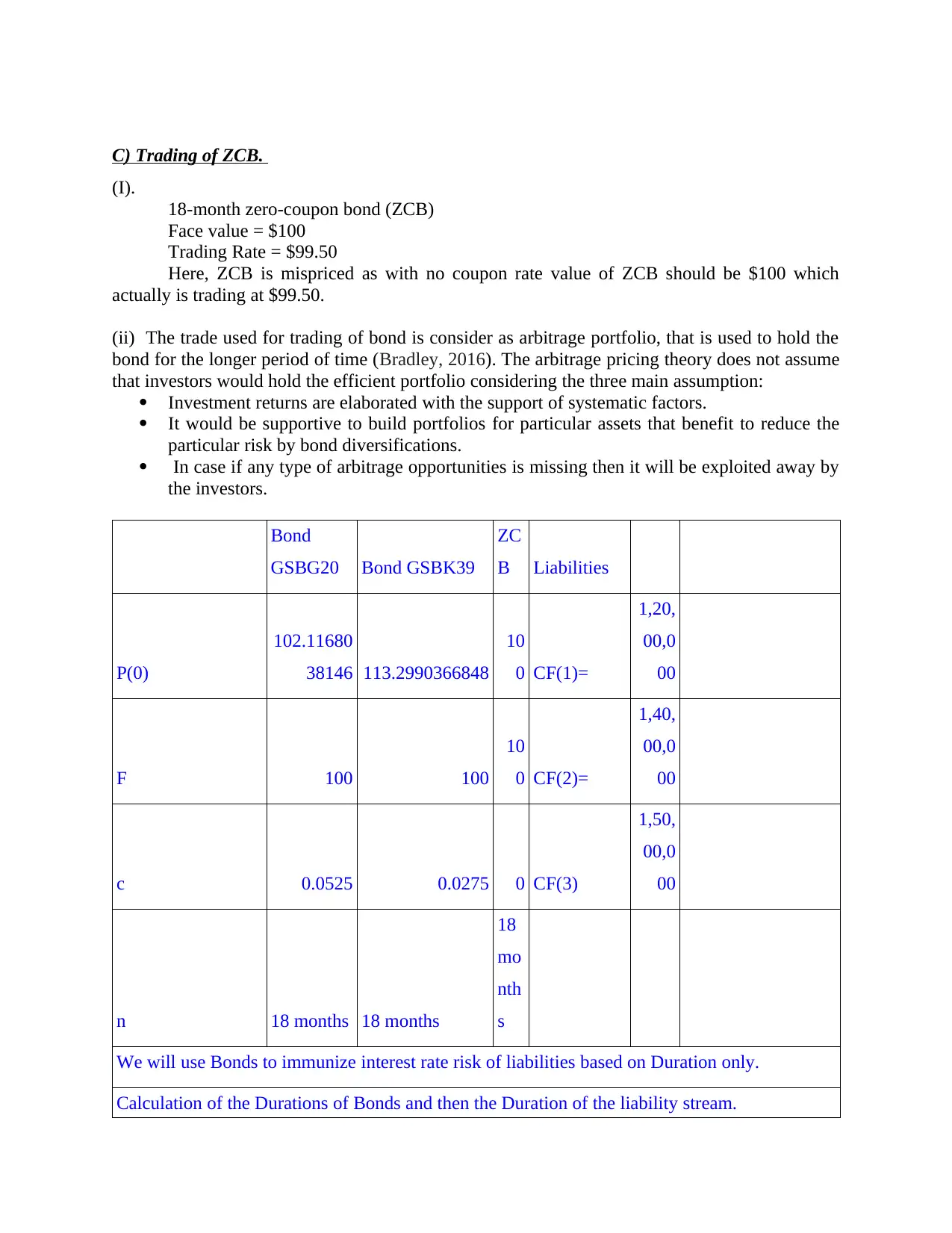

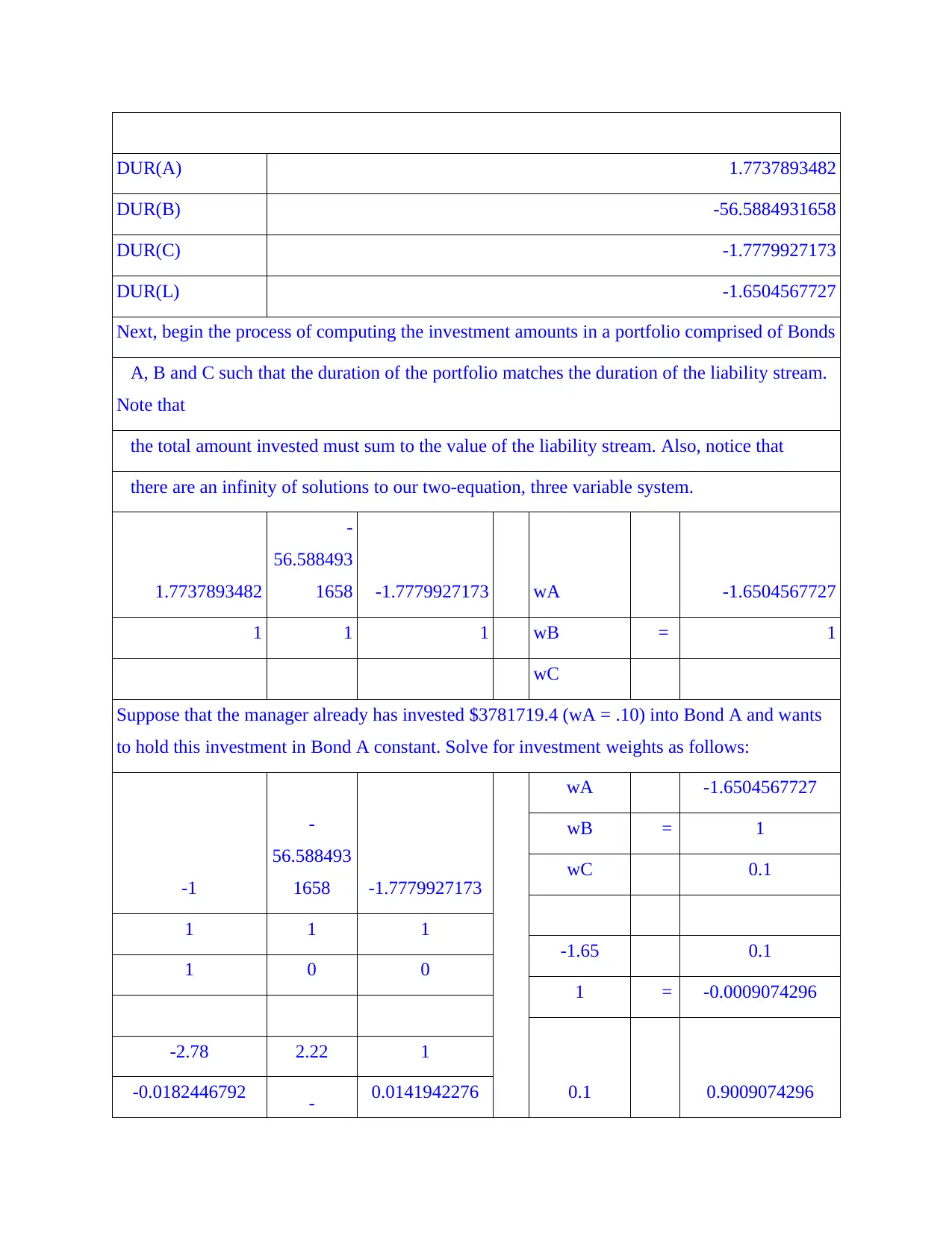

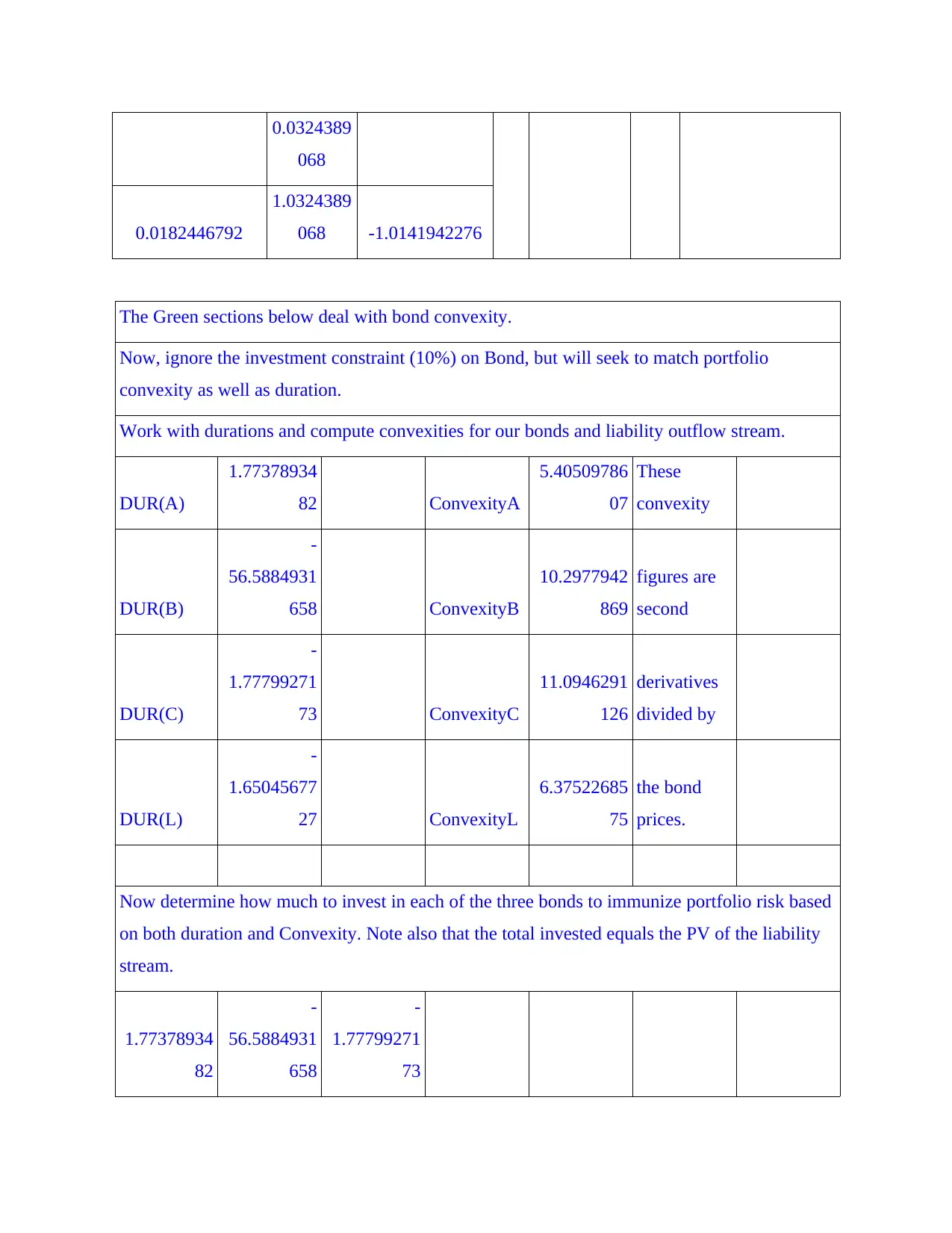

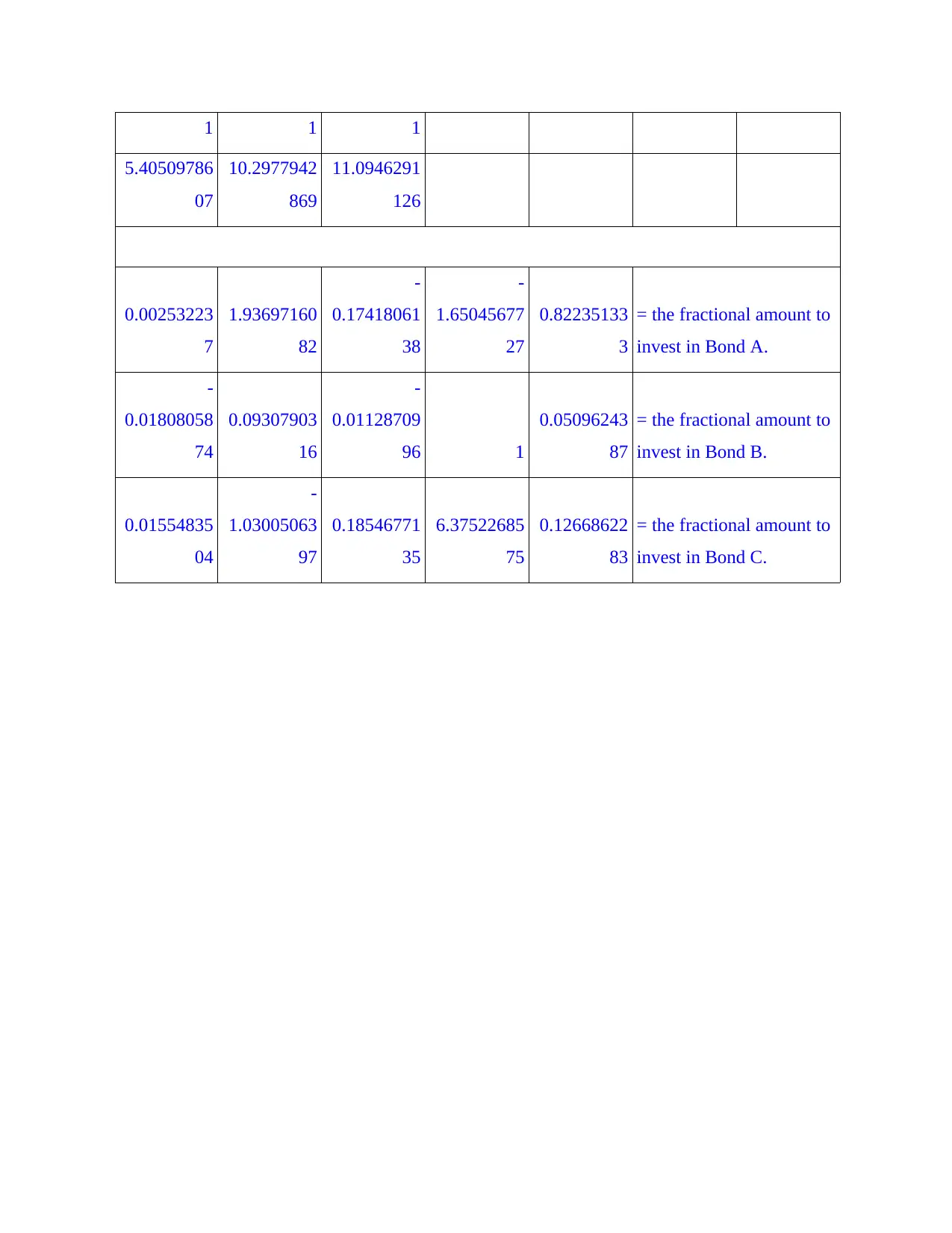

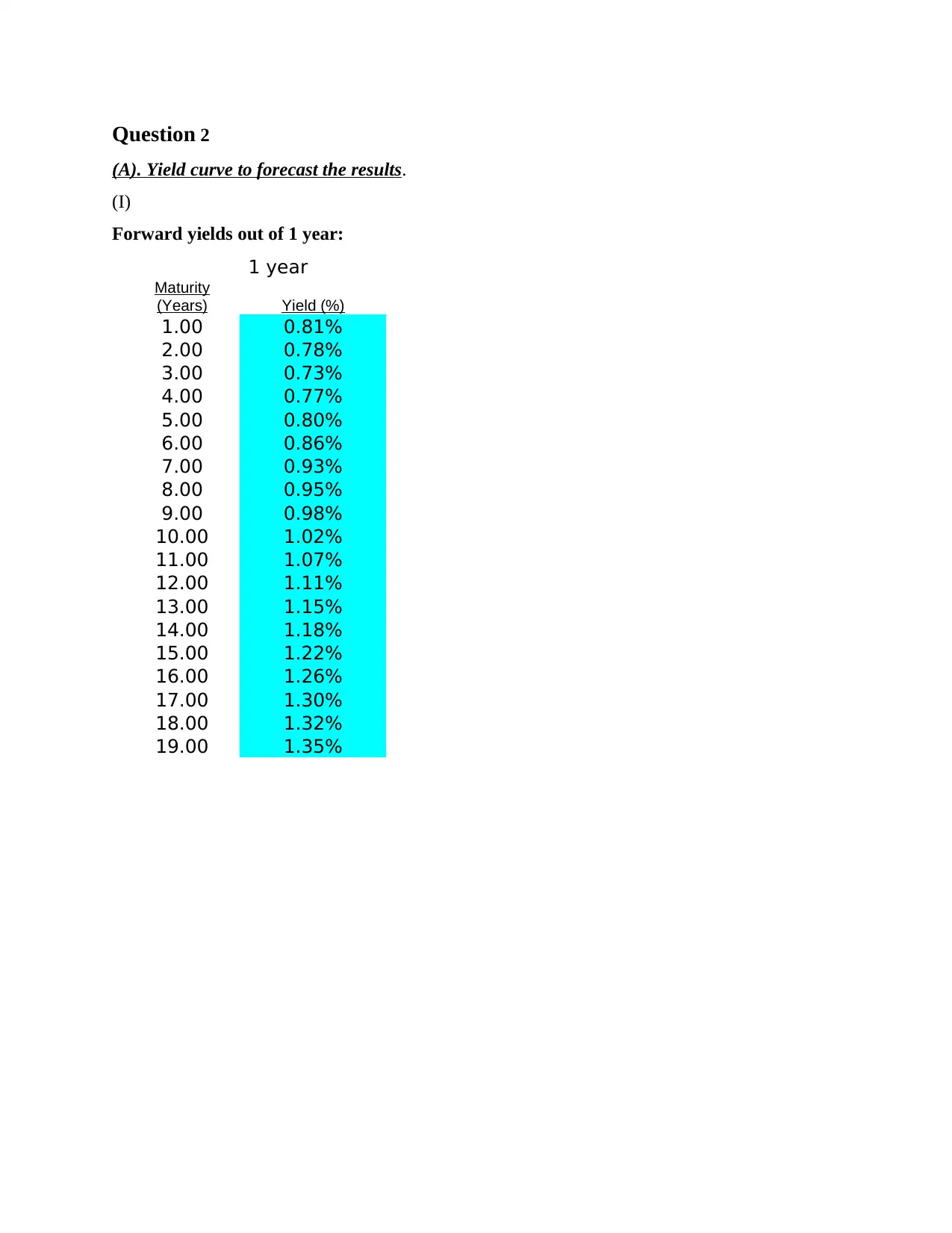

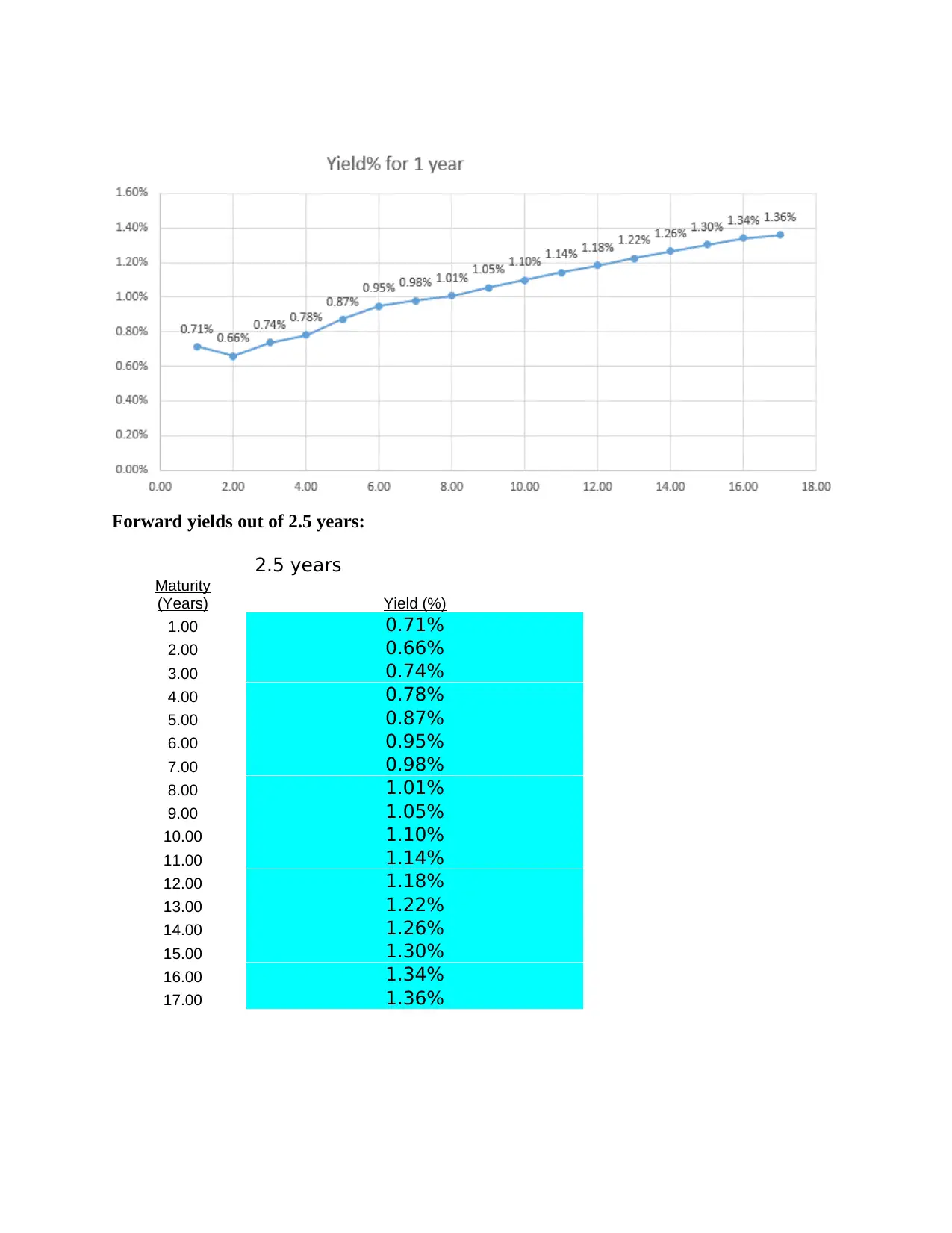

This report delves into the core concepts of investment management, focusing on bond pricing, yield curve analysis, and interest rate risk. It begins with an introduction to investment decisions and capital budgeting, emphasizing the significance of short-term asset investments. The report then analyzes the reasons behind the Reserve Bank of Australia's (RBA) cash rate decrease in June 2019, exploring its impact on the economy. It includes detailed calculations and tables for bond pricing, yield to maturity, and zero-coupon yields. The report also examines the trading of zero-coupon bonds and the application of arbitrage pricing theory. Furthermore, it explores the use of yield curves in forecasting, the theory of liquidity preference, and the impact of interest rate changes on investment strategies, offering insights for Roosters Bond Trust to manage risk effectively. The report concludes with an analysis of bond duration and convexity, providing a framework for immunizing portfolio risk.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.