Financial Accounting: Investment Appraisal and Funding for AYR Co.

VerifiedAdded on 2023/05/30

|27

|4329

|410

Report

AI Summary

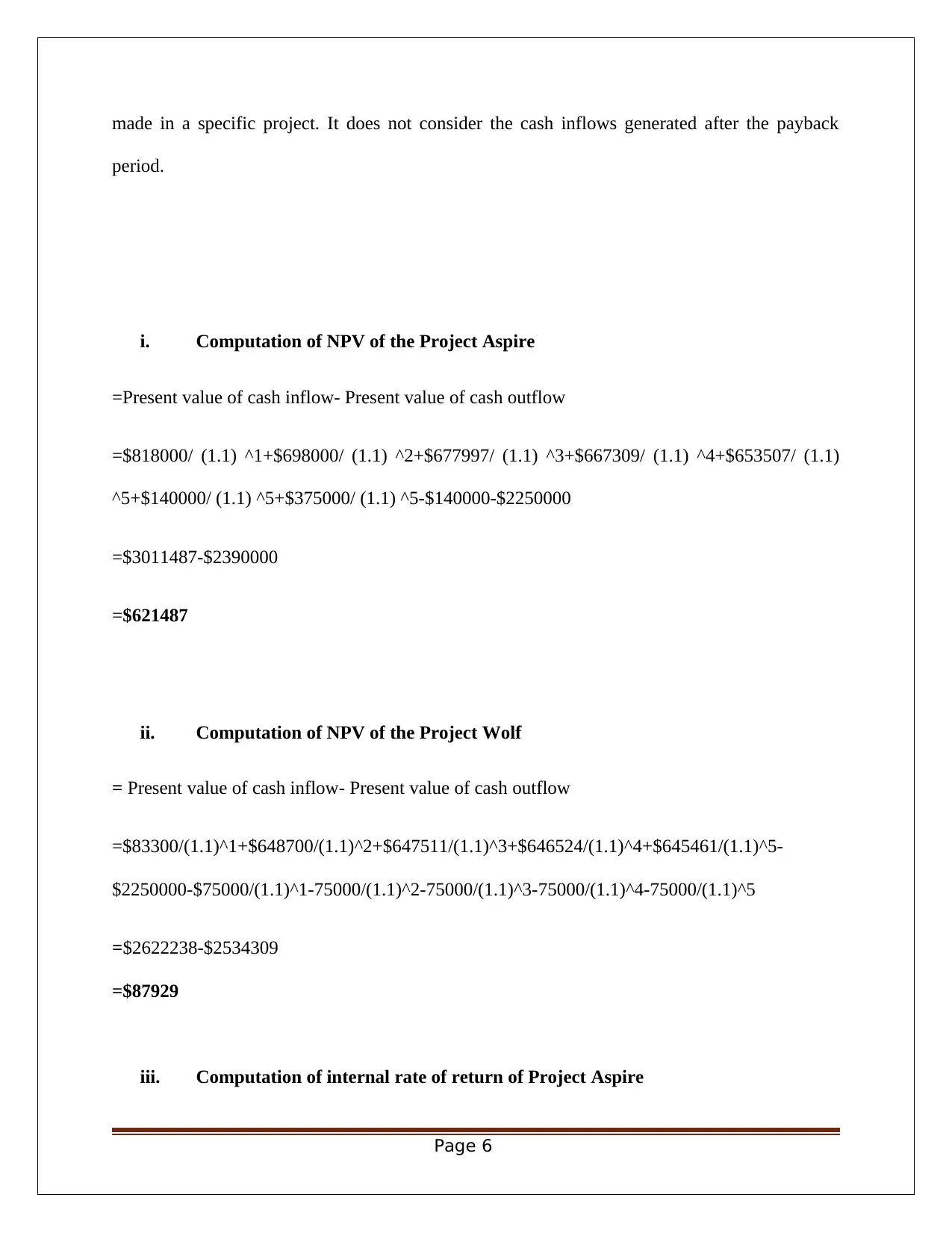

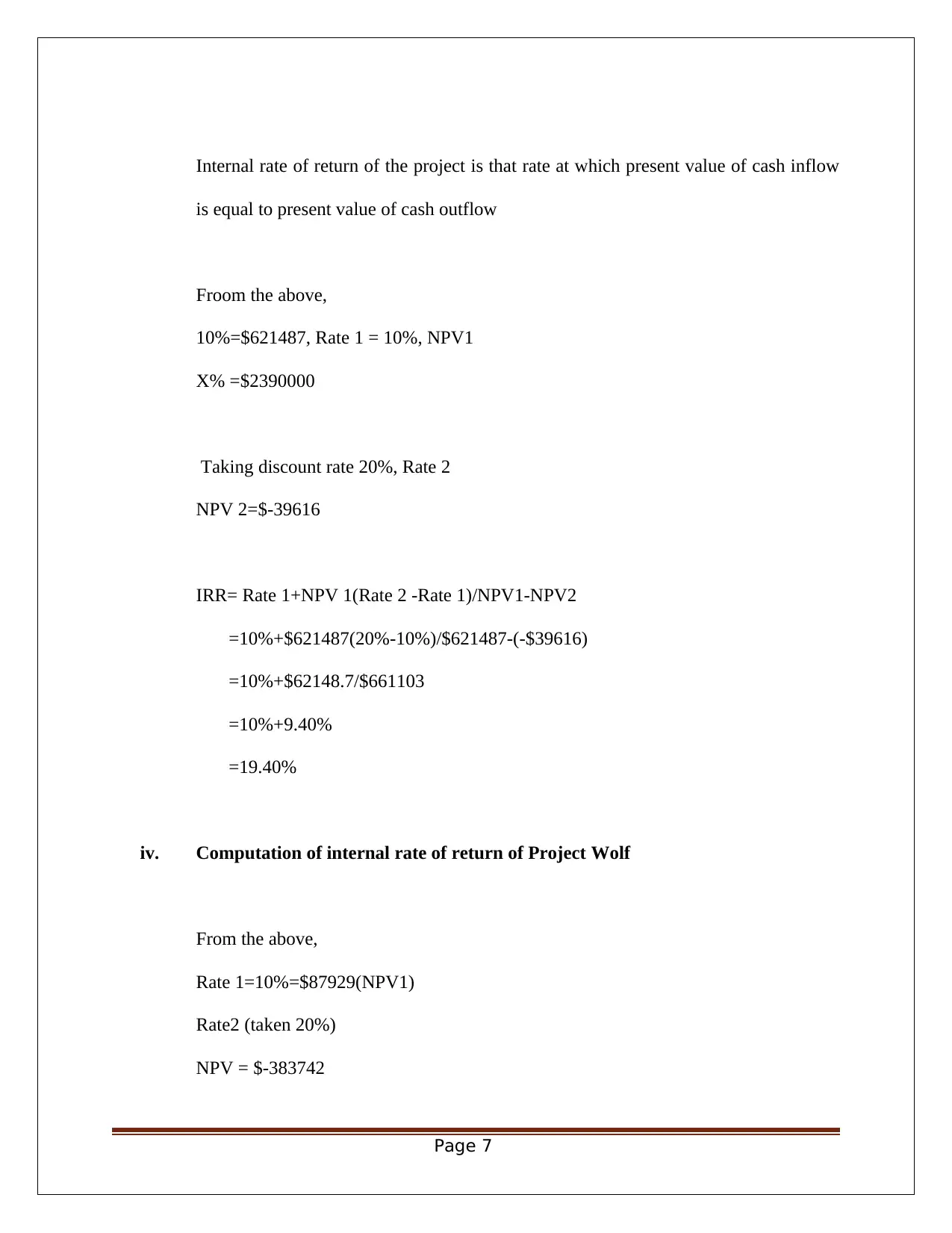

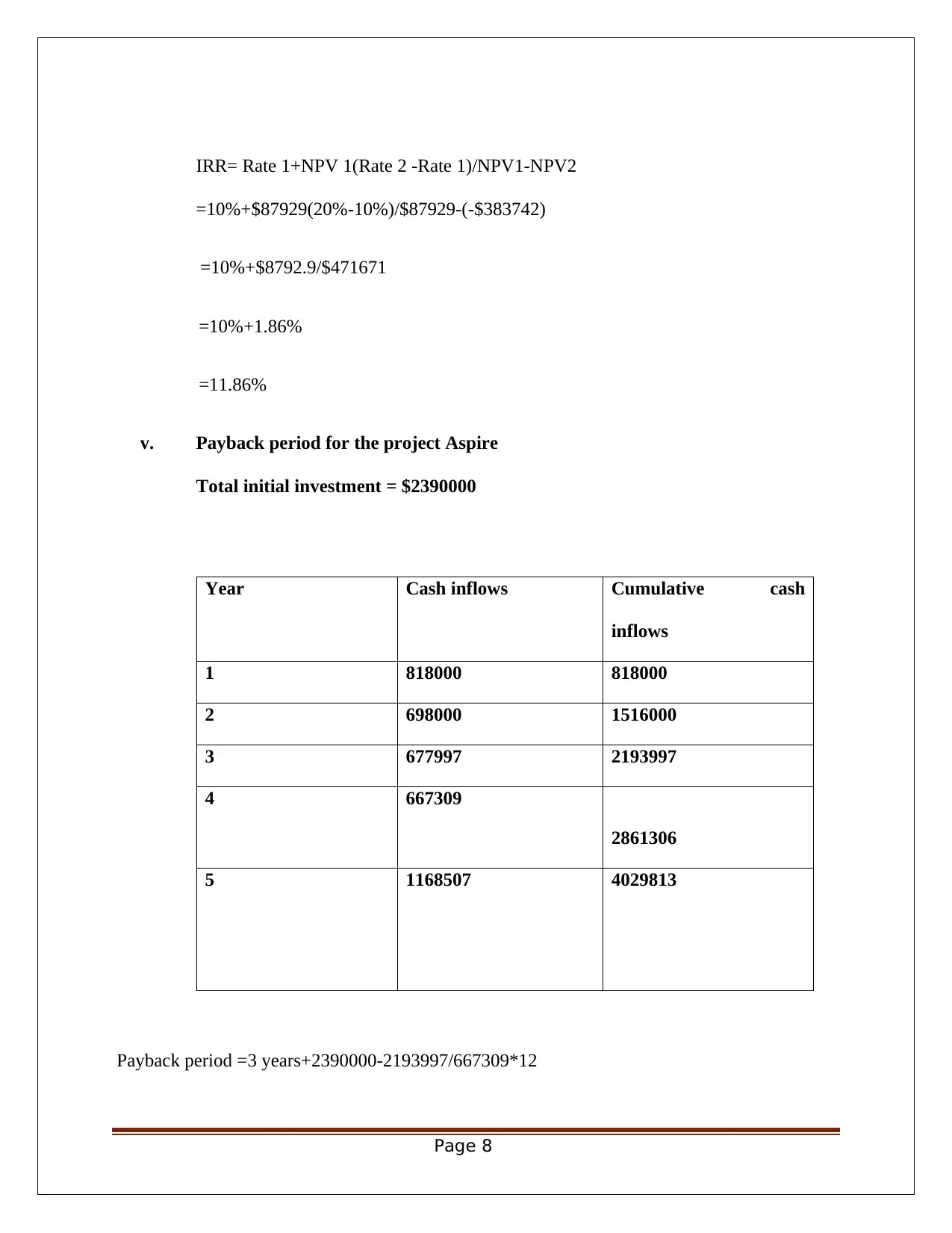

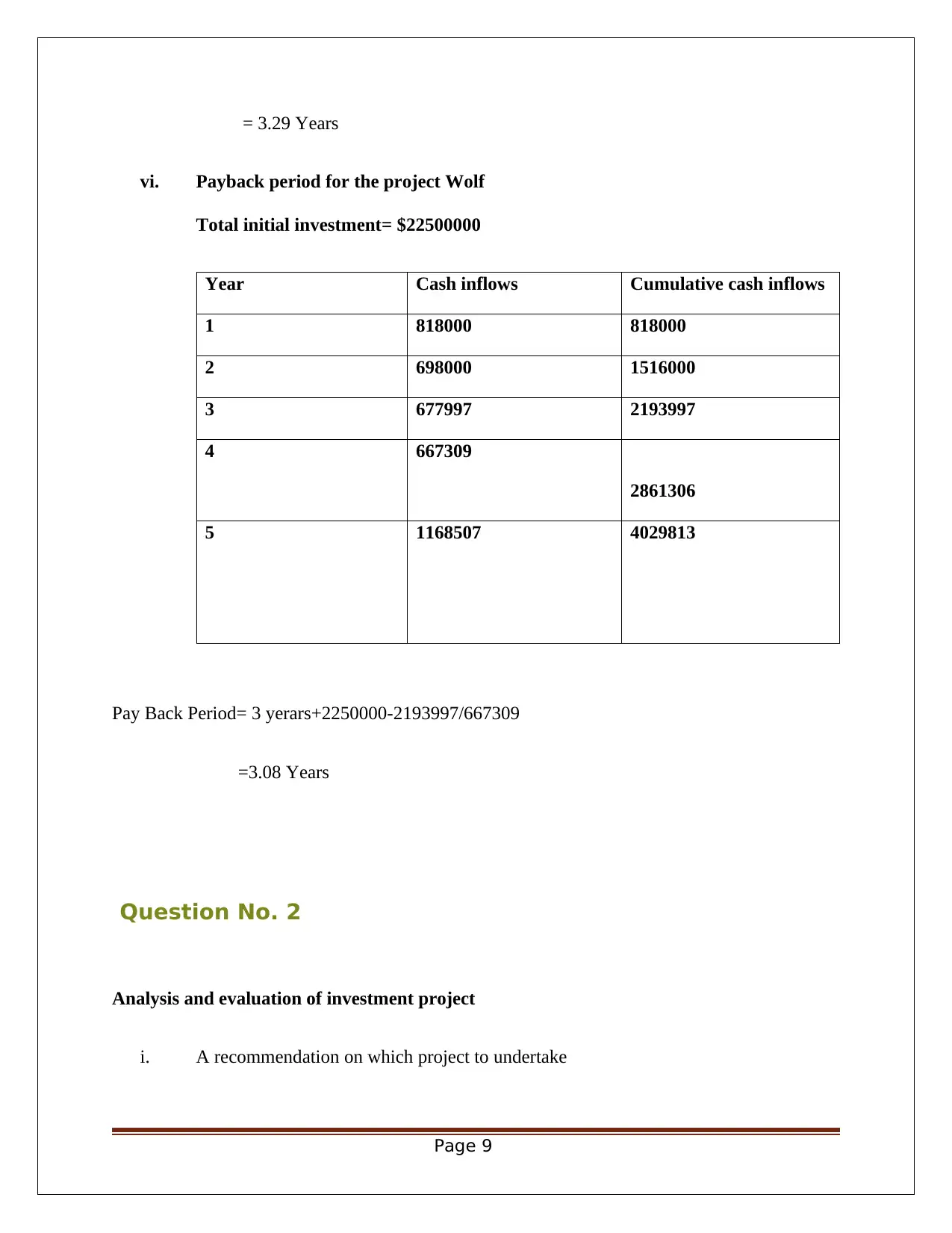

This report provides a comprehensive analysis of two investment projects, Project Aspire and Project Wolf, for AYR Co., utilizing capital budgeting techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period to justify project selection. The report recommends selecting a project and suggests additional factors for consideration beyond capital budgeting results. It also explores appropriate funding sources, including debt and equity, along with their respective costs and impact on the company's weighted average cost of capital. The analysis includes detailed calculations of NPV, IRR, and payback period for both projects, ultimately recommending Project Aspire based on its higher NPV and IRR. The report further discusses the strengths and weaknesses of each capital budgeting technique, emphasizing the superiority of NPV for decision-making. Additional factors such as consumer demand, uncertainty, and economic activity are highlighted for consideration before making a final investment decision. Finally, the report provides a detailed comparison of debt and equity financing, including their costs and implications for AYR Co.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.