Financial Behaviour: Investment Policy Statement Report Analysis

VerifiedAdded on 2023/02/01

|8

|1879

|32

Report

AI Summary

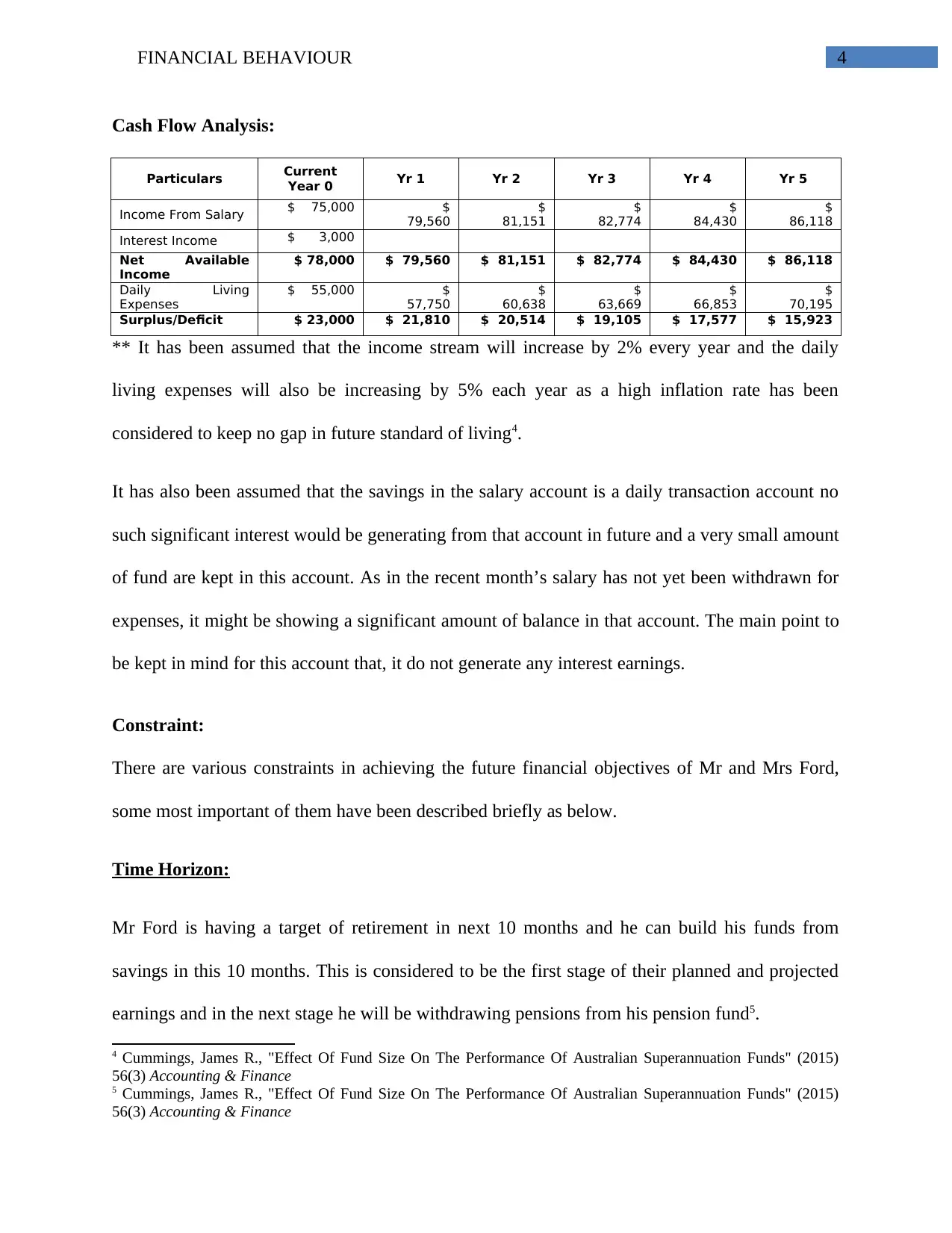

This report presents an Investment Policy Statement (IPS) prepared for Mr. and Mrs. Ford, focusing on their financial goals and investment strategies. The IPS begins with a background of the Fords, who are approaching retirement and have specific income and expense profiles. Their objectives include securing an annual return to maintain their lifestyle, funding their son's wedding, and setting aside funds for holidays and emergencies. The report assesses their risk tolerance, recommending a moderate approach with a mix of growth and risk-free investments. A detailed cash flow analysis projects their income and expenses over five years, considering inflation. Constraints such as time horizon, liquidity, and taxes are also addressed, along with asset allocation strategies. The recommended approach involves a 30% growth fund investment strategy. The report concludes by emphasizing the importance of reviewing the information and ensuring it aligns with the Fords' financial expectations, offering a comprehensive framework for their retirement planning and investment management.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.