Investment Management: Senior Citizen Recreation Club Fund IPS

VerifiedAdded on 2022/11/13

|11

|3416

|205

Report

AI Summary

This report presents an Investment Policy Statement (IPS) created for the Senior Citizens’ Recreation Club (SCRC) Fund. The IPS outlines the fund's objectives, which include capital protection and consistent returns, with a time horizon exceeding ten years. It details risk tolerance, return requirements, and unique investment constraints, such as excluding environmentally harmful or unethical companies. The report covers asset allocation strategies, targeting specific percentages for equity, fixed income, and alternative investments, along with the selection of securities within these classes. It also addresses legal and tax considerations, liquidity needs, and provides a comparison of portfolio performance metrics. The fund employs a balanced, long-term investment approach to achieve its financial goals, ensuring diversification and mitigating market risks, with a portion of the fund held in cash for short-term emergencies.

Running Head: INVESTMENT MANAGEMENT

Investment Management

Name of the Student

Name of the University

Investment Management

Name of the Student

Name of the University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT MANAGEMENT

2

Table of Contents

Introduction.....................................................................................................................................3

Objectives of the Investments..........................................................................................................3

Time Horizon.....................................................................................................................................3

Risk Tolerance....................................................................................................................................3

Return requirements.........................................................................................................................3

Unique needs and circumstances......................................................................................................4

Legal and regulatory consideration...................................................................................................4

Tax considerations.............................................................................................................................4

Liquidity requirements......................................................................................................................4

Strategy of Asset Allocation..............................................................................................................4

Strategy for selecting security..........................................................................................................6

Comparing the Portfolio Performance..............................................................................................8

References......................................................................................................................................11

2

Table of Contents

Introduction.....................................................................................................................................3

Objectives of the Investments..........................................................................................................3

Time Horizon.....................................................................................................................................3

Risk Tolerance....................................................................................................................................3

Return requirements.........................................................................................................................3

Unique needs and circumstances......................................................................................................4

Legal and regulatory consideration...................................................................................................4

Tax considerations.............................................................................................................................4

Liquidity requirements......................................................................................................................4

Strategy of Asset Allocation..............................................................................................................4

Strategy for selecting security..........................................................................................................6

Comparing the Portfolio Performance..............................................................................................8

References......................................................................................................................................11

INVESTMENT MANAGEMENT

3

Introduction

The assessment includes the creation of the IPS or the investment policy statement for

the exploit return of the Fund (Senior Citizen Recreation Club Fund). These funds are related

to the SCRC (Senior Citizens’ Recreation club). The IPS creation of the fund will help the

club maintain comprehensive strategies that will direct all the financial assessment of the

club. The fund will offer a better and consistent financial sustainability, thus maintaining any

troubles will decrease the financial procedure of the club.

Objectives of the Investments

There are two main objectives of the funds and the main objective focuses on the

reliability of the return generation on a regular basis alongside looking for the protection of

the capital that is invested in the long-term. This is the most important objective, as this will

be accounted for any unforeseen event that causes any kind of financial trouble in the future

for Senior Citizens’ Recreation Club. The next or the secondary objective is to decrease the

unpredictability of the many burdens that will occur in the future (Akole et al. 2016).

Therefore, it is important to focus on the diversification.

Time Horizon

When the club fund is aware of the possibilities for the degradation of the capital then

the time horizon is specific about it in regards to an excess of 10 years. This is all processed

in order to retain a strong capital approval rate. The degradation of the capital happened over

a time horizon by engaging in balanced long-term investment as set by the investment policy

statements.

Risk Tolerance

In order to gain a good return production attached with capital approval, there needs

to be some instability that is unpredicted but also does not trouble the objective that is set for

the distribution of the fund. Along with the objective of the mentioned funds, the consistency

has to be made to overflow the funds and time horizon of 10 years should be reduced.

Return requirements

Along with the level of risk tolerance, it is expected to find the return requirements

falling in line with the allocation of the asset’s fund policy. Because of this, the peg has been

allocated with an entire return fund of eight percent higher that is after opposing any increase

impacts on the market.

3

Introduction

The assessment includes the creation of the IPS or the investment policy statement for

the exploit return of the Fund (Senior Citizen Recreation Club Fund). These funds are related

to the SCRC (Senior Citizens’ Recreation club). The IPS creation of the fund will help the

club maintain comprehensive strategies that will direct all the financial assessment of the

club. The fund will offer a better and consistent financial sustainability, thus maintaining any

troubles will decrease the financial procedure of the club.

Objectives of the Investments

There are two main objectives of the funds and the main objective focuses on the

reliability of the return generation on a regular basis alongside looking for the protection of

the capital that is invested in the long-term. This is the most important objective, as this will

be accounted for any unforeseen event that causes any kind of financial trouble in the future

for Senior Citizens’ Recreation Club. The next or the secondary objective is to decrease the

unpredictability of the many burdens that will occur in the future (Akole et al. 2016).

Therefore, it is important to focus on the diversification.

Time Horizon

When the club fund is aware of the possibilities for the degradation of the capital then

the time horizon is specific about it in regards to an excess of 10 years. This is all processed

in order to retain a strong capital approval rate. The degradation of the capital happened over

a time horizon by engaging in balanced long-term investment as set by the investment policy

statements.

Risk Tolerance

In order to gain a good return production attached with capital approval, there needs

to be some instability that is unpredicted but also does not trouble the objective that is set for

the distribution of the fund. Along with the objective of the mentioned funds, the consistency

has to be made to overflow the funds and time horizon of 10 years should be reduced.

Return requirements

Along with the level of risk tolerance, it is expected to find the return requirements

falling in line with the allocation of the asset’s fund policy. Because of this, the peg has been

allocated with an entire return fund of eight percent higher that is after opposing any increase

impacts on the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT MANAGEMENT

4

Unique needs and circumstances

The Senior Citizen Recreation Club Fund evidently stated that the limits valuing the

investments are not available in the following areas:

Investment is available for a company whose activities poses a threat to the

environment.

Investing in an energy-based company is not allowed.

Investments are not allowed for the companies that manufacture tobacco or alcohol or

any unethical products along with that the companies that are not appropriate in the

areas seeming moral, social.

The investments are not allowed for the companies that are benefiting from

disreputable medicinal research.

Legal and regulatory consideration

The funds of the clubs are clearly stated in the consumer protection act of 2009 and

the native version of the WSR (Wall Street Reform) synchronizes it. The act also includes the

safeguarding the significance of the investors for any kind of losses that are not mentioned. It

is protected by the method of variation from fund objectives or allocated targeted funds.

Tax considerations

All the funds of the Senior Citizen Recreation Club Fund are registered under Section

501(c). And any kind of taxes that are implicated while selling or buying of the investments

mentioned in the IPS is immune and therefore will not be taken into consideration.

Liquidity requirements

There are many other sources for financing the Senior Citizen Recreation Club and

fund is just one of them. For the everyday operation of the club, the fund is very important as

it operates as a support method for financing the club. A steady quantity of sum has to be

cash has to be reserved in a bank account of a trustworthy commercial bank or invested in

cash. There has to be a limit for withdrawal of any kind of money and not more than $40000

should be allowed in a day. This is all to make sure from any periodic withdrawals that may

be necessary for any kind of emergency.

Strategy of Asset Allocation

There are many pieces of research regarding asset allocation and initial research

highlights the fact that in order to steady the instability of the fund the asset allocation is far

4

Unique needs and circumstances

The Senior Citizen Recreation Club Fund evidently stated that the limits valuing the

investments are not available in the following areas:

Investment is available for a company whose activities poses a threat to the

environment.

Investing in an energy-based company is not allowed.

Investments are not allowed for the companies that manufacture tobacco or alcohol or

any unethical products along with that the companies that are not appropriate in the

areas seeming moral, social.

The investments are not allowed for the companies that are benefiting from

disreputable medicinal research.

Legal and regulatory consideration

The funds of the clubs are clearly stated in the consumer protection act of 2009 and

the native version of the WSR (Wall Street Reform) synchronizes it. The act also includes the

safeguarding the significance of the investors for any kind of losses that are not mentioned. It

is protected by the method of variation from fund objectives or allocated targeted funds.

Tax considerations

All the funds of the Senior Citizen Recreation Club Fund are registered under Section

501(c). And any kind of taxes that are implicated while selling or buying of the investments

mentioned in the IPS is immune and therefore will not be taken into consideration.

Liquidity requirements

There are many other sources for financing the Senior Citizen Recreation Club and

fund is just one of them. For the everyday operation of the club, the fund is very important as

it operates as a support method for financing the club. A steady quantity of sum has to be

cash has to be reserved in a bank account of a trustworthy commercial bank or invested in

cash. There has to be a limit for withdrawal of any kind of money and not more than $40000

should be allowed in a day. This is all to make sure from any periodic withdrawals that may

be necessary for any kind of emergency.

Strategy of Asset Allocation

There are many pieces of research regarding asset allocation and initial research

highlights the fact that in order to steady the instability of the fund the asset allocation is far

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT MANAGEMENT

5

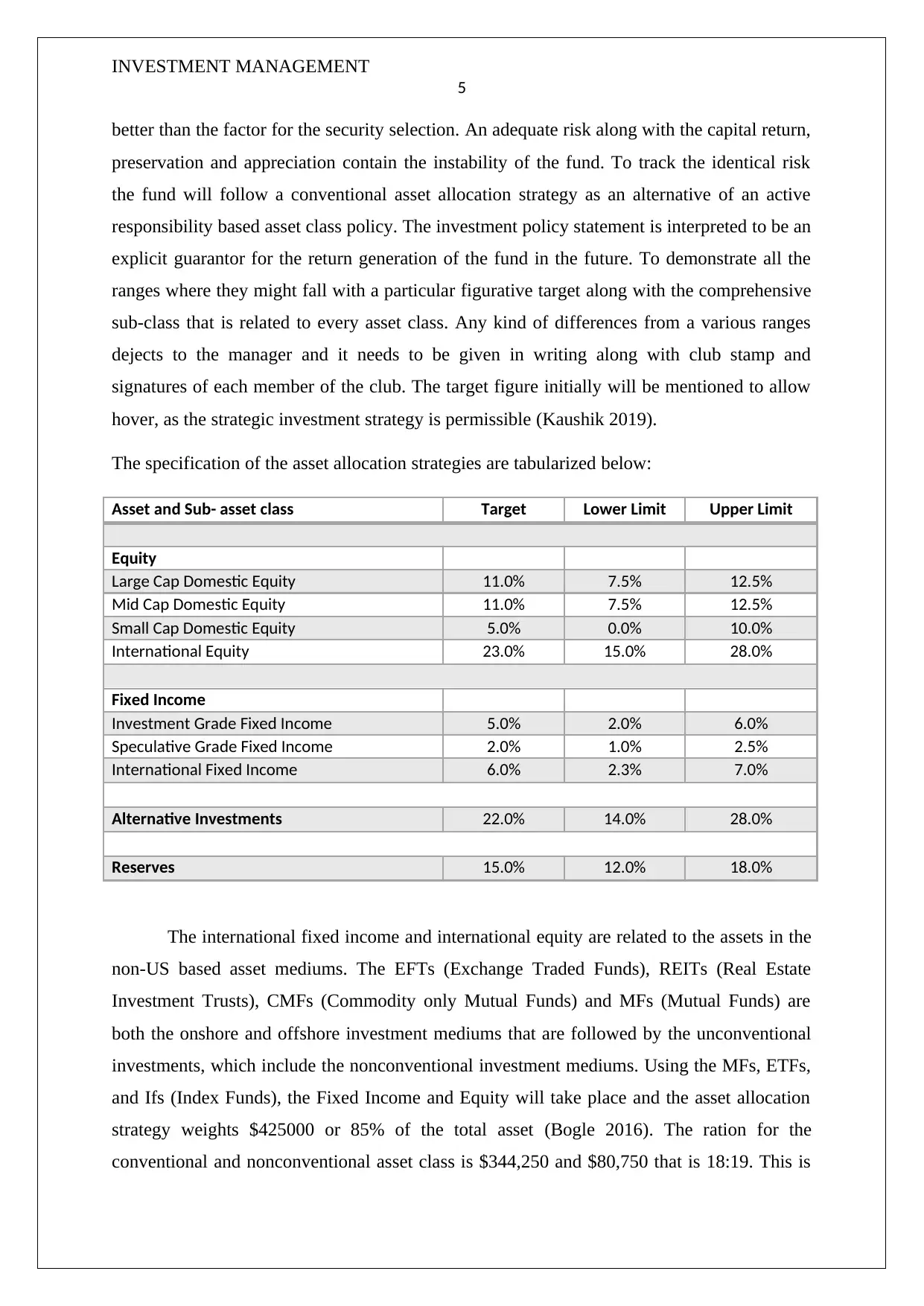

better than the factor for the security selection. An adequate risk along with the capital return,

preservation and appreciation contain the instability of the fund. To track the identical risk

the fund will follow a conventional asset allocation strategy as an alternative of an active

responsibility based asset class policy. The investment policy statement is interpreted to be an

explicit guarantor for the return generation of the fund in the future. To demonstrate all the

ranges where they might fall with a particular figurative target along with the comprehensive

sub-class that is related to every asset class. Any kind of differences from a various ranges

dejects to the manager and it needs to be given in writing along with club stamp and

signatures of each member of the club. The target figure initially will be mentioned to allow

hover, as the strategic investment strategy is permissible (Kaushik 2019).

The specification of the asset allocation strategies are tabularized below:

Asset and Sub- asset class Target Lower Limit Upper Limit

Equity

Large Cap Domestic Equity 11.0% 7.5% 12.5%

Mid Cap Domestic Equity 11.0% 7.5% 12.5%

Small Cap Domestic Equity 5.0% 0.0% 10.0%

International Equity 23.0% 15.0% 28.0%

Fixed Income

Investment Grade Fixed Income 5.0% 2.0% 6.0%

Speculative Grade Fixed Income 2.0% 1.0% 2.5%

International Fixed Income 6.0% 2.3% 7.0%

Alternative Investments 22.0% 14.0% 28.0%

Reserves 15.0% 12.0% 18.0%

The international fixed income and international equity are related to the assets in the

non-US based asset mediums. The EFTs (Exchange Traded Funds), REITs (Real Estate

Investment Trusts), CMFs (Commodity only Mutual Funds) and MFs (Mutual Funds) are

both the onshore and offshore investment mediums that are followed by the unconventional

investments, which include the nonconventional investment mediums. Using the MFs, ETFs,

and Ifs (Index Funds), the Fixed Income and Equity will take place and the asset allocation

strategy weights $425000 or 85% of the total asset (Bogle 2016). The ration for the

conventional and nonconventional asset class is $344,250 and $80,750 that is 18:19. This is

5

better than the factor for the security selection. An adequate risk along with the capital return,

preservation and appreciation contain the instability of the fund. To track the identical risk

the fund will follow a conventional asset allocation strategy as an alternative of an active

responsibility based asset class policy. The investment policy statement is interpreted to be an

explicit guarantor for the return generation of the fund in the future. To demonstrate all the

ranges where they might fall with a particular figurative target along with the comprehensive

sub-class that is related to every asset class. Any kind of differences from a various ranges

dejects to the manager and it needs to be given in writing along with club stamp and

signatures of each member of the club. The target figure initially will be mentioned to allow

hover, as the strategic investment strategy is permissible (Kaushik 2019).

The specification of the asset allocation strategies are tabularized below:

Asset and Sub- asset class Target Lower Limit Upper Limit

Equity

Large Cap Domestic Equity 11.0% 7.5% 12.5%

Mid Cap Domestic Equity 11.0% 7.5% 12.5%

Small Cap Domestic Equity 5.0% 0.0% 10.0%

International Equity 23.0% 15.0% 28.0%

Fixed Income

Investment Grade Fixed Income 5.0% 2.0% 6.0%

Speculative Grade Fixed Income 2.0% 1.0% 2.5%

International Fixed Income 6.0% 2.3% 7.0%

Alternative Investments 22.0% 14.0% 28.0%

Reserves 15.0% 12.0% 18.0%

The international fixed income and international equity are related to the assets in the

non-US based asset mediums. The EFTs (Exchange Traded Funds), REITs (Real Estate

Investment Trusts), CMFs (Commodity only Mutual Funds) and MFs (Mutual Funds) are

both the onshore and offshore investment mediums that are followed by the unconventional

investments, which include the nonconventional investment mediums. Using the MFs, ETFs,

and Ifs (Index Funds), the Fixed Income and Equity will take place and the asset allocation

strategy weights $425000 or 85% of the total asset (Bogle 2016). The ration for the

conventional and nonconventional asset class is $344,250 and $80,750 that is 18:19. This is

INVESTMENT MANAGEMENT

6

to make sure of the diversification and to not fall for the unconsidered traps of market

collapse and early fall in the standard security modules. To make certain of the liquidity the

unconventional investments of $110000 that weigh 22% of the allocated asset are not

approached by the direct investments. In order to avoid an investment suck-up the direct

investments in merchandise or in real estate are used. This results in a lack of improvement in

the capital invested which than later gets into the non-diversification that is related to the

investment class. The pooled investment mediums are uses for all these types of investments

to bring the benefit of diversification by engaging in the direct investments of the above-

mentioned possibility and having a worthy capital foundation (Hamilton and Wu 2015).

Finally, a detachment $75000 or 15% of the primary investment quantity is set apart

as cash to mitigate the short-term emergencies in the functioning procedure of the club any

time throughout the entire cycle of investment. To save the importance of the fund the cash

needs to be deposited in the savings bank account of any commercial banks especially in the

BOA (Bank of America) which offers a 0.03 % interest rate. The interest rate may seem very

small but the advantages of the bank compensate the latency cost in terms of FDIC protection

(Box et al. 2018).

Strategy for selecting security

An ultimate standard for the asset class factors explicitly related to the Fixed income

and Equity will be defined after giving general asset class and sub-class selection. The

standard in inquiry for the Fixed Income will be the US comprehensive Bond Index that is

Barclay’s Capital. The standard in inquiry for the Equity will be both the S&P 500 Index

(Standard & Poor’s 500), and the Russell 3000 Index. The security selection for both the

fixed income and equity will search for an answer to outperform these standards. The

outperformance for the fixed income will be according to the gross return without allowing

the deduction fees and the outperformance for the Equity will be according to the net return

after allowing the deduction fees. The comprehensible investment will be made in funds and

will be invested in organizations that are not decreasing under the limitations clause as

mentioned previously (Gara 2019).

By checking the growth rate and evaluating the growth of the company, an investment

of 11% or $55000 is made focusing on long-term appreciation of the capital as Large Cap

Domestic Equity in the “T.Rowe Price Instl Large Cap Core Gr FD”. The company gives a

6

to make sure of the diversification and to not fall for the unconsidered traps of market

collapse and early fall in the standard security modules. To make certain of the liquidity the

unconventional investments of $110000 that weigh 22% of the allocated asset are not

approached by the direct investments. In order to avoid an investment suck-up the direct

investments in merchandise or in real estate are used. This results in a lack of improvement in

the capital invested which than later gets into the non-diversification that is related to the

investment class. The pooled investment mediums are uses for all these types of investments

to bring the benefit of diversification by engaging in the direct investments of the above-

mentioned possibility and having a worthy capital foundation (Hamilton and Wu 2015).

Finally, a detachment $75000 or 15% of the primary investment quantity is set apart

as cash to mitigate the short-term emergencies in the functioning procedure of the club any

time throughout the entire cycle of investment. To save the importance of the fund the cash

needs to be deposited in the savings bank account of any commercial banks especially in the

BOA (Bank of America) which offers a 0.03 % interest rate. The interest rate may seem very

small but the advantages of the bank compensate the latency cost in terms of FDIC protection

(Box et al. 2018).

Strategy for selecting security

An ultimate standard for the asset class factors explicitly related to the Fixed income

and Equity will be defined after giving general asset class and sub-class selection. The

standard in inquiry for the Fixed Income will be the US comprehensive Bond Index that is

Barclay’s Capital. The standard in inquiry for the Equity will be both the S&P 500 Index

(Standard & Poor’s 500), and the Russell 3000 Index. The security selection for both the

fixed income and equity will search for an answer to outperform these standards. The

outperformance for the fixed income will be according to the gross return without allowing

the deduction fees and the outperformance for the Equity will be according to the net return

after allowing the deduction fees. The comprehensible investment will be made in funds and

will be invested in organizations that are not decreasing under the limitations clause as

mentioned previously (Gara 2019).

By checking the growth rate and evaluating the growth of the company, an investment

of 11% or $55000 is made focusing on long-term appreciation of the capital as Large Cap

Domestic Equity in the “T.Rowe Price Instl Large Cap Core Gr FD”. The company gives a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT MANAGEMENT

7

return average of 9.76% a year whipping the standards by 1.77%. This type of fund is

balanced to develop on an incessant scale without any type of slow-downs signals.

Focusing on the extended capital appreciation an investment of 11% or $55000 will

be made into the “DF Dent Midcap Growth Fund” for the Mid Cap Domestic Equity. The

80% of the funds are advanced in the favoured stocks, widespread stocks, and some

companies listed in the US. The finance supports company comes with a heavy presentation

when it comes to whipping the standards by the return of 18.2% a year, which is compared to

the 7.99% registered by standards.

Some investments are made into the “Virtus KAR Small-Cap Core Fund” as a Small

Cap Domestic Equity, so it is only 5% or $25000 of the fund. However, it helps in capital

appreciation but it also keeps the extra revenues as its minor concern although investing in

US-based companies. The fund beats the average standards by 425 BP (basic points) as a year

return of 12.24% (Cao et al. 2017).

The next is the international equity, as it is leading the capital appreciation the focus is

on the research-based diversification. Therefore, an investment of 23% or $115000 is made

into the “MFS International Diversification Fund”. A negative return for a year is highlighted

to the tune of 0.11% and was still enhanced comparing to the standards of negative return of

2.16% to the tune of 380 Basis Points. The recent presentation of the fund came out as a

return generation of 7.77% highlighting higher development.

There is an investment of 5% or $25000 is to be made into the “iShares iBoxx

Investment Grade Corporate Bond ETF” as Investment Grade Fixed Income. The company

sports more than 1000 quality bond investment with an advanced bias tune of 27% for all the

banking sector companies. The fund produced in a year capitulates as 3.6% evaluated with

the inadequate 0.01% yield produced by the standards (Dannhauser 2017).

The investments made into the company “Federated HighIncome Bond Fund”

regardless of being rated as exploratory, display a well-built cash flow policy following the

management. The investment is of 2% or $10000 of the fund as Speculative Grade Fixed

Income. 474 Basic Points bet the standards registering a year yield of 4.75%.

There was an investment of 6% or $30000 as International Fixed Income in the

“SPDR® Blmbg Barclays Intl Trs Bd ETF” company. This was for searching and mapping

the standards by offering an equivalent gross yield basis for a year without deducting the fee.

7

return average of 9.76% a year whipping the standards by 1.77%. This type of fund is

balanced to develop on an incessant scale without any type of slow-downs signals.

Focusing on the extended capital appreciation an investment of 11% or $55000 will

be made into the “DF Dent Midcap Growth Fund” for the Mid Cap Domestic Equity. The

80% of the funds are advanced in the favoured stocks, widespread stocks, and some

companies listed in the US. The finance supports company comes with a heavy presentation

when it comes to whipping the standards by the return of 18.2% a year, which is compared to

the 7.99% registered by standards.

Some investments are made into the “Virtus KAR Small-Cap Core Fund” as a Small

Cap Domestic Equity, so it is only 5% or $25000 of the fund. However, it helps in capital

appreciation but it also keeps the extra revenues as its minor concern although investing in

US-based companies. The fund beats the average standards by 425 BP (basic points) as a year

return of 12.24% (Cao et al. 2017).

The next is the international equity, as it is leading the capital appreciation the focus is

on the research-based diversification. Therefore, an investment of 23% or $115000 is made

into the “MFS International Diversification Fund”. A negative return for a year is highlighted

to the tune of 0.11% and was still enhanced comparing to the standards of negative return of

2.16% to the tune of 380 Basis Points. The recent presentation of the fund came out as a

return generation of 7.77% highlighting higher development.

There is an investment of 5% or $25000 is to be made into the “iShares iBoxx

Investment Grade Corporate Bond ETF” as Investment Grade Fixed Income. The company

sports more than 1000 quality bond investment with an advanced bias tune of 27% for all the

banking sector companies. The fund produced in a year capitulates as 3.6% evaluated with

the inadequate 0.01% yield produced by the standards (Dannhauser 2017).

The investments made into the company “Federated HighIncome Bond Fund”

regardless of being rated as exploratory, display a well-built cash flow policy following the

management. The investment is of 2% or $10000 of the fund as Speculative Grade Fixed

Income. 474 Basic Points bet the standards registering a year yield of 4.75%.

There was an investment of 6% or $30000 as International Fixed Income in the

“SPDR® Blmbg Barclays Intl Trs Bd ETF” company. This was for searching and mapping

the standards by offering an equivalent gross yield basis for a year without deducting the fee.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT MANAGEMENT

8

This has registered as the highest standard beating the margin by 666 Basic Points and tuning

as 6.67%.

Lastly, there was an investment made in the “Vanguard Real Estate Index Fund” for

$110,000, which would be proportionate to the tune of $71,500 or 65%. These investments

are made in the real estate for both industrial and commercial, big residential, and other

companies in the US. There were 12.04% of returns in a year (Gara 2019). There was an

investment in the “United States Oil Fund” as well; all the remaining $38500 or 35% of the

funds were invested. The returns from the remaining investment were generated as 18.63% a

year. The unconventional investment fund generates 14.35% of return a year. Finally, this

results in a high return asset generation and offers an adequate diversification. In general, the

collection of all the returns would produce a return of 11.72%. This gives an increase of

3.72% returns over the predetermined 8% in the investment policy statements (Dzhabarov et

al. 2018).

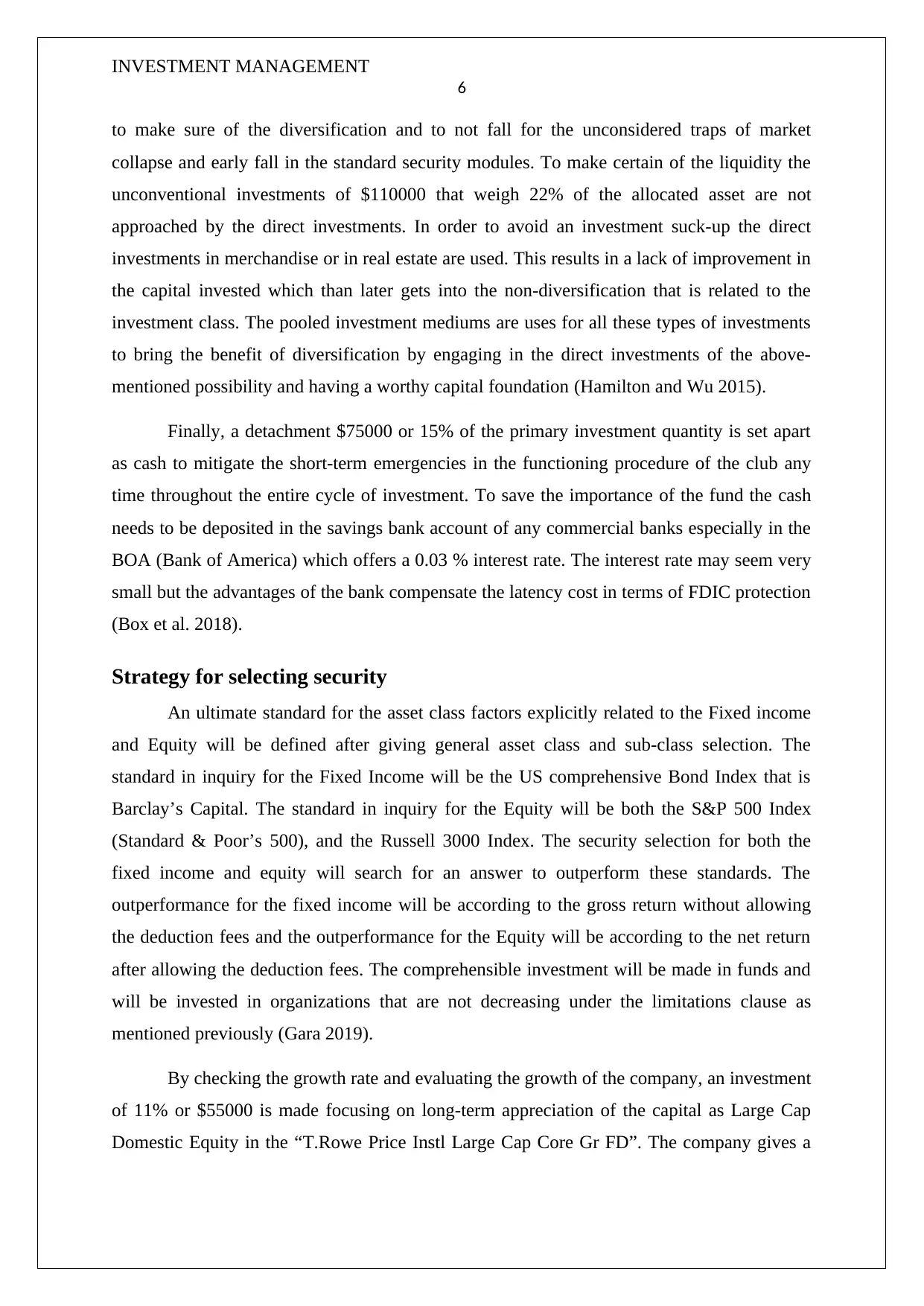

Comparing the Portfolio Performance

The portfolio created from 1st Feb 2019 to 31st July 2019, gives the detailed weekly-

returns for over 6 months data. The portfolio is based on the value cost returns and is very

small and taking into account that there are no spending that have been accepted. The below

graph will show the same (Geczy and Samonov 2016).

8

This has registered as the highest standard beating the margin by 666 Basic Points and tuning

as 6.67%.

Lastly, there was an investment made in the “Vanguard Real Estate Index Fund” for

$110,000, which would be proportionate to the tune of $71,500 or 65%. These investments

are made in the real estate for both industrial and commercial, big residential, and other

companies in the US. There were 12.04% of returns in a year (Gara 2019). There was an

investment in the “United States Oil Fund” as well; all the remaining $38500 or 35% of the

funds were invested. The returns from the remaining investment were generated as 18.63% a

year. The unconventional investment fund generates 14.35% of return a year. Finally, this

results in a high return asset generation and offers an adequate diversification. In general, the

collection of all the returns would produce a return of 11.72%. This gives an increase of

3.72% returns over the predetermined 8% in the investment policy statements (Dzhabarov et

al. 2018).

Comparing the Portfolio Performance

The portfolio created from 1st Feb 2019 to 31st July 2019, gives the detailed weekly-

returns for over 6 months data. The portfolio is based on the value cost returns and is very

small and taking into account that there are no spending that have been accepted. The below

graph will show the same (Geczy and Samonov 2016).

INVESTMENT MANAGEMENT

9

The starting from the 1st of Feb the return of 1.21% has gone up to 1.28% as it is

highlighted in the portfolio. There were many unpredictable investments that were made and

considering that, it seems to be better. The unpredictability of the investments ranges to an

inadequate 0.80% thus the reliability of the portfolio is being questioned even though

assuming a high unpredictability of our investment policy statements. When the real year

ends the return payoffs will portrait advanced as stock price changes have been the main

factor (Geller 2016).

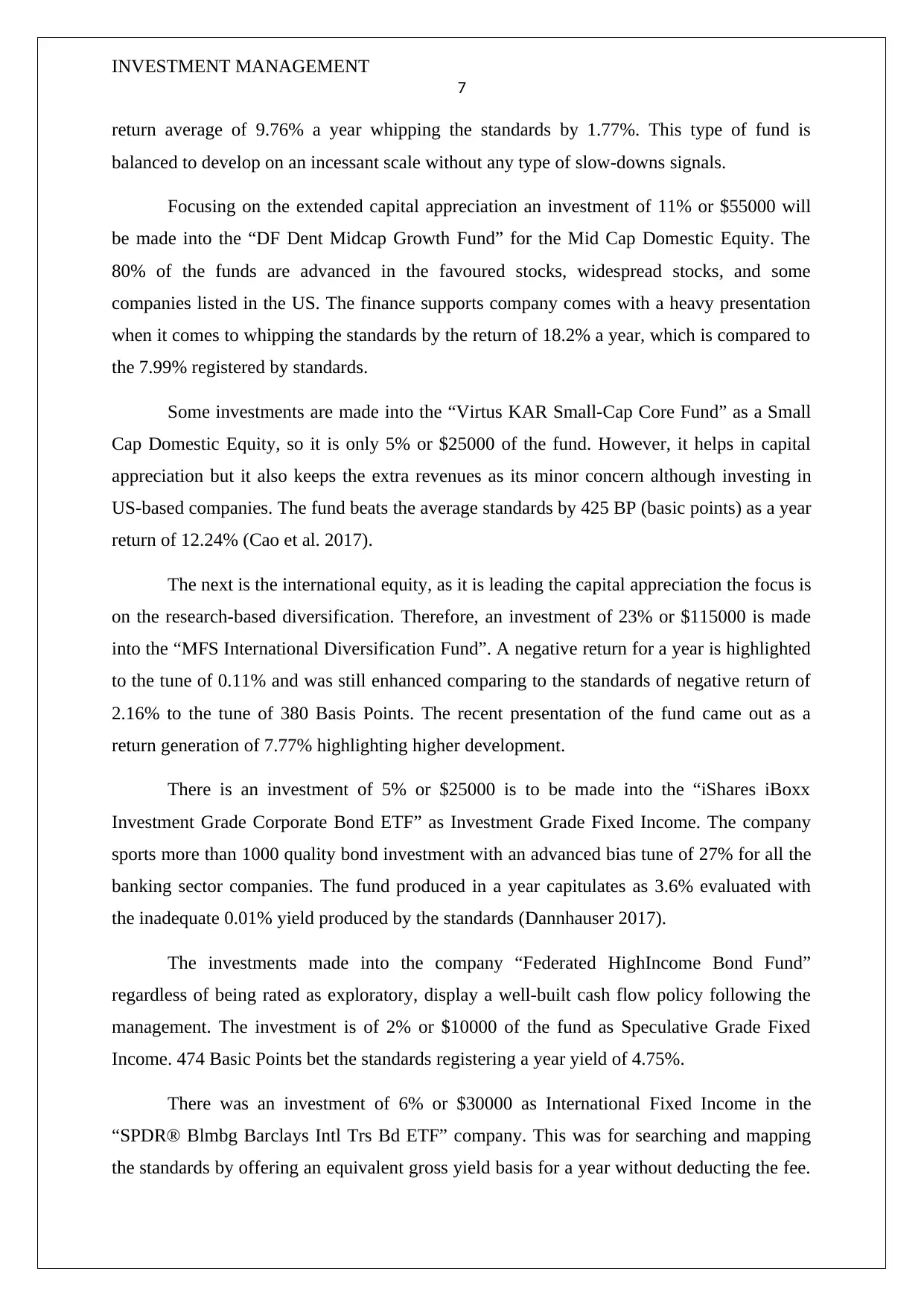

We have measured the six-month CAGR (Compounded Annual Growth Rate) in

order to offer a clear performance picture of the portfolio. Below table is the evaluation per

component as highlighted.

6 month Returns (1st February - 31st July)

Particulars Weights in the Portfolio Returns

Large Cap Domestic Equity 11% 0.73%

Mid Cap Domestic Equity 11% 3.89%

Small Cap Domestic Equity 5% 9.36%

International Equity 23% 2.54%

Investment Grade Fixed Income 5% 4.61%

Speculative Grade Fixed Income 2% 0.79%

International Fixed Income 6% 0.11%

Alternative Investment – Real Estate 14.3% 3.03%

Alternative Investment – Oil 7.70% 3.55%

Reserves 15% 0.03%

The above table brings a return of 2.52% over a six-month time in a portfolio on a

cash value basis. This highlights the information of the portfolio that it is reliable with asset

approval and with the capital appreciation without including the accounts of the frequent

income. There was a little increase $12,620 in a limited time exclusive of income influx as

the capital appreciations have enhanced from $500,000 to $ 512,622.3.

The portfolio is compared with a year of interest rate from the Bank of America as

cash maximize account for the abovementioned investment amount that will be 0.40% p.a.

The standard cash maximizes account rate outlines for all banking sectors came up to 0.65%

p.a. The figures are mentioned as per annum however; the returns are for weekly over a six-

month period as mentioned above that us 1.28%. The monthly basis returns are 2.252% and it

is only bookkeeping cost returns. The return of the cash maximizer account comes out as

0.054% per month that builds up to 0.324% over a six-month (Fender and Lewrick 2015).

9

The starting from the 1st of Feb the return of 1.21% has gone up to 1.28% as it is

highlighted in the portfolio. There were many unpredictable investments that were made and

considering that, it seems to be better. The unpredictability of the investments ranges to an

inadequate 0.80% thus the reliability of the portfolio is being questioned even though

assuming a high unpredictability of our investment policy statements. When the real year

ends the return payoffs will portrait advanced as stock price changes have been the main

factor (Geller 2016).

We have measured the six-month CAGR (Compounded Annual Growth Rate) in

order to offer a clear performance picture of the portfolio. Below table is the evaluation per

component as highlighted.

6 month Returns (1st February - 31st July)

Particulars Weights in the Portfolio Returns

Large Cap Domestic Equity 11% 0.73%

Mid Cap Domestic Equity 11% 3.89%

Small Cap Domestic Equity 5% 9.36%

International Equity 23% 2.54%

Investment Grade Fixed Income 5% 4.61%

Speculative Grade Fixed Income 2% 0.79%

International Fixed Income 6% 0.11%

Alternative Investment – Real Estate 14.3% 3.03%

Alternative Investment – Oil 7.70% 3.55%

Reserves 15% 0.03%

The above table brings a return of 2.52% over a six-month time in a portfolio on a

cash value basis. This highlights the information of the portfolio that it is reliable with asset

approval and with the capital appreciation without including the accounts of the frequent

income. There was a little increase $12,620 in a limited time exclusive of income influx as

the capital appreciations have enhanced from $500,000 to $ 512,622.3.

The portfolio is compared with a year of interest rate from the Bank of America as

cash maximize account for the abovementioned investment amount that will be 0.40% p.a.

The standard cash maximizes account rate outlines for all banking sectors came up to 0.65%

p.a. The figures are mentioned as per annum however; the returns are for weekly over a six-

month period as mentioned above that us 1.28%. The monthly basis returns are 2.252% and it

is only bookkeeping cost returns. The return of the cash maximizer account comes out as

0.054% per month that builds up to 0.324% over a six-month (Fender and Lewrick 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT MANAGEMENT

10

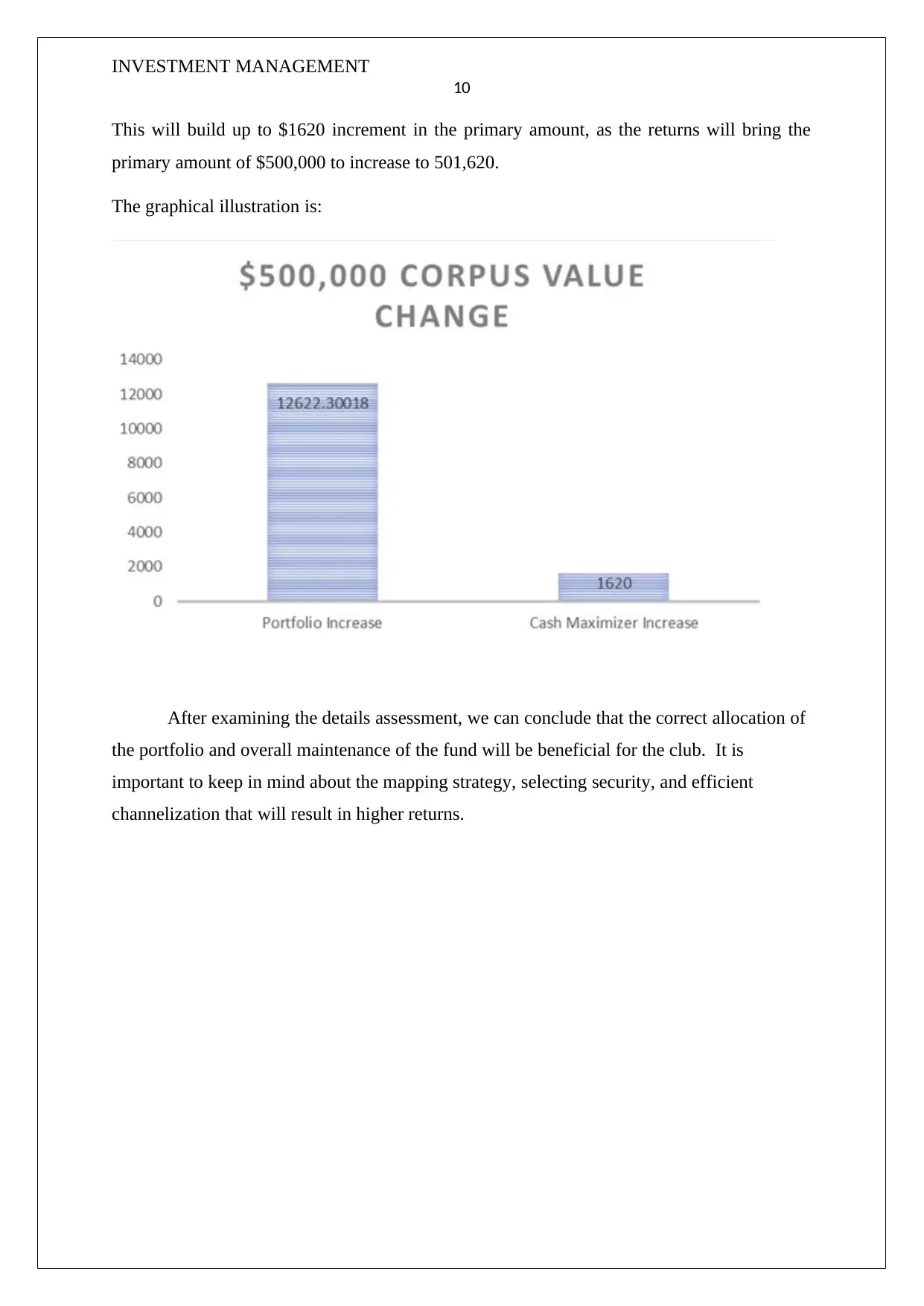

This will build up to $1620 increment in the primary amount, as the returns will bring the

primary amount of $500,000 to increase to 501,620.

The graphical illustration is:

After examining the details assessment, we can conclude that the correct allocation of

the portfolio and overall maintenance of the fund will be beneficial for the club. It is

important to keep in mind about the mapping strategy, selecting security, and efficient

channelization that will result in higher returns.

10

This will build up to $1620 increment in the primary amount, as the returns will bring the

primary amount of $500,000 to increase to 501,620.

The graphical illustration is:

After examining the details assessment, we can conclude that the correct allocation of

the portfolio and overall maintenance of the fund will be beneficial for the club. It is

important to keep in mind about the mapping strategy, selecting security, and efficient

channelization that will result in higher returns.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT MANAGEMENT

11

References

Akole, N.V., Chakravarthi, J.R. and Hebbar, P.M., FMR LLC, 2016. Real-Time Spend

Management with Savings Goals. U.S. Patent Application 15/018,820.

Bogle, J.C., 2016. The index mutual fund: 40 years of growth, change, and

challenge. Financial Analysts Journal, 72(1), pp.9-13.

Box, T., Davis, R.L. and Fuller, K.P., 2018. ETF Competition and Market Quality. Financial

Management.

Cao, C., Iliev, P. and Velthuis, R., 2017. Style drift: Evidence from small-cap mutual

funds. Journal of Banking & Finance, 78, pp.42-57.

Dannhauser, C.D., 2017. The impact of innovation: Evidence from corporate bond exchange-

traded funds (ETFs). Journal of Financial Economics, 125(3), pp.537-560.

Deng, Y., Devos, E., Rahman, S. and Tsang, D., 2016. The role of debt covenants in the

investment grade bond market–the REIT experiment. The Journal of Real Estate Finance and

Economics, 52(4), pp.428-448.

Dzhabarov, C., Ziegler, A. and Ziemba, W.T., 2018. Sell in May and go away: the evidence

in the international equity index futures markets. Quantitative Finance, 18(2), pp.171-181.

Fender, I. and Lewrick, U., 2015. Shifting tides–market liquidity and market-making in fixed

income instruments. BIS Quarterly Review, March.

Gara, A., 2019. Fortified Returns. FORBES, 202(1), pp.86-87.

Geczy, C.C. and Samonov, M., 2016. Two centuries of price-return momentum. Financial

Analysts Journal, 72(5), pp.32-56.

Geller, S.M., 2016. Investment Policy Statements: Legal and Practical Considerations. The

CPA Journal, 86(1), p.70.

Hamilton, J.D. and Wu, J.C., 2015. Effects of index‐fund investing on commodity futures

prices. International economic review, 56(1), pp.187-205.

Kaushik, A., 2019. Performance Evaluation of Mid-Cap Retail Equity Mutual

Funds. International Journal of Finance & Banking Studies (2147-4486), 8(2), pp.09-17.

11

References

Akole, N.V., Chakravarthi, J.R. and Hebbar, P.M., FMR LLC, 2016. Real-Time Spend

Management with Savings Goals. U.S. Patent Application 15/018,820.

Bogle, J.C., 2016. The index mutual fund: 40 years of growth, change, and

challenge. Financial Analysts Journal, 72(1), pp.9-13.

Box, T., Davis, R.L. and Fuller, K.P., 2018. ETF Competition and Market Quality. Financial

Management.

Cao, C., Iliev, P. and Velthuis, R., 2017. Style drift: Evidence from small-cap mutual

funds. Journal of Banking & Finance, 78, pp.42-57.

Dannhauser, C.D., 2017. The impact of innovation: Evidence from corporate bond exchange-

traded funds (ETFs). Journal of Financial Economics, 125(3), pp.537-560.

Deng, Y., Devos, E., Rahman, S. and Tsang, D., 2016. The role of debt covenants in the

investment grade bond market–the REIT experiment. The Journal of Real Estate Finance and

Economics, 52(4), pp.428-448.

Dzhabarov, C., Ziegler, A. and Ziemba, W.T., 2018. Sell in May and go away: the evidence

in the international equity index futures markets. Quantitative Finance, 18(2), pp.171-181.

Fender, I. and Lewrick, U., 2015. Shifting tides–market liquidity and market-making in fixed

income instruments. BIS Quarterly Review, March.

Gara, A., 2019. Fortified Returns. FORBES, 202(1), pp.86-87.

Geczy, C.C. and Samonov, M., 2016. Two centuries of price-return momentum. Financial

Analysts Journal, 72(5), pp.32-56.

Geller, S.M., 2016. Investment Policy Statements: Legal and Practical Considerations. The

CPA Journal, 86(1), p.70.

Hamilton, J.D. and Wu, J.C., 2015. Effects of index‐fund investing on commodity futures

prices. International economic review, 56(1), pp.187-205.

Kaushik, A., 2019. Performance Evaluation of Mid-Cap Retail Equity Mutual

Funds. International Journal of Finance & Banking Studies (2147-4486), 8(2), pp.09-17.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.