25503 Investment Analysis Assignment - Part I Summer 2018 - University

VerifiedAdded on 2023/04/20

|11

|1855

|217

Project

AI Summary

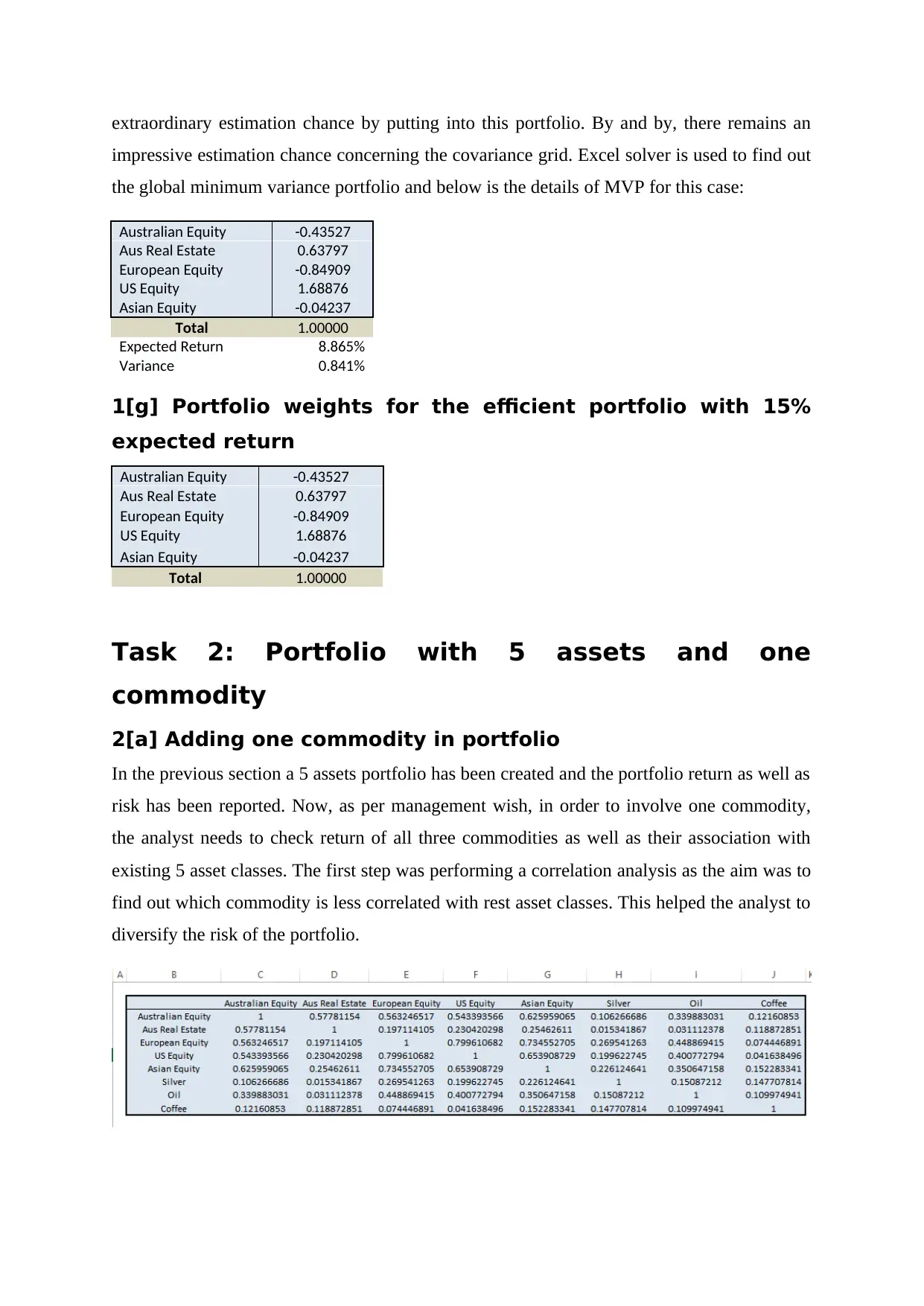

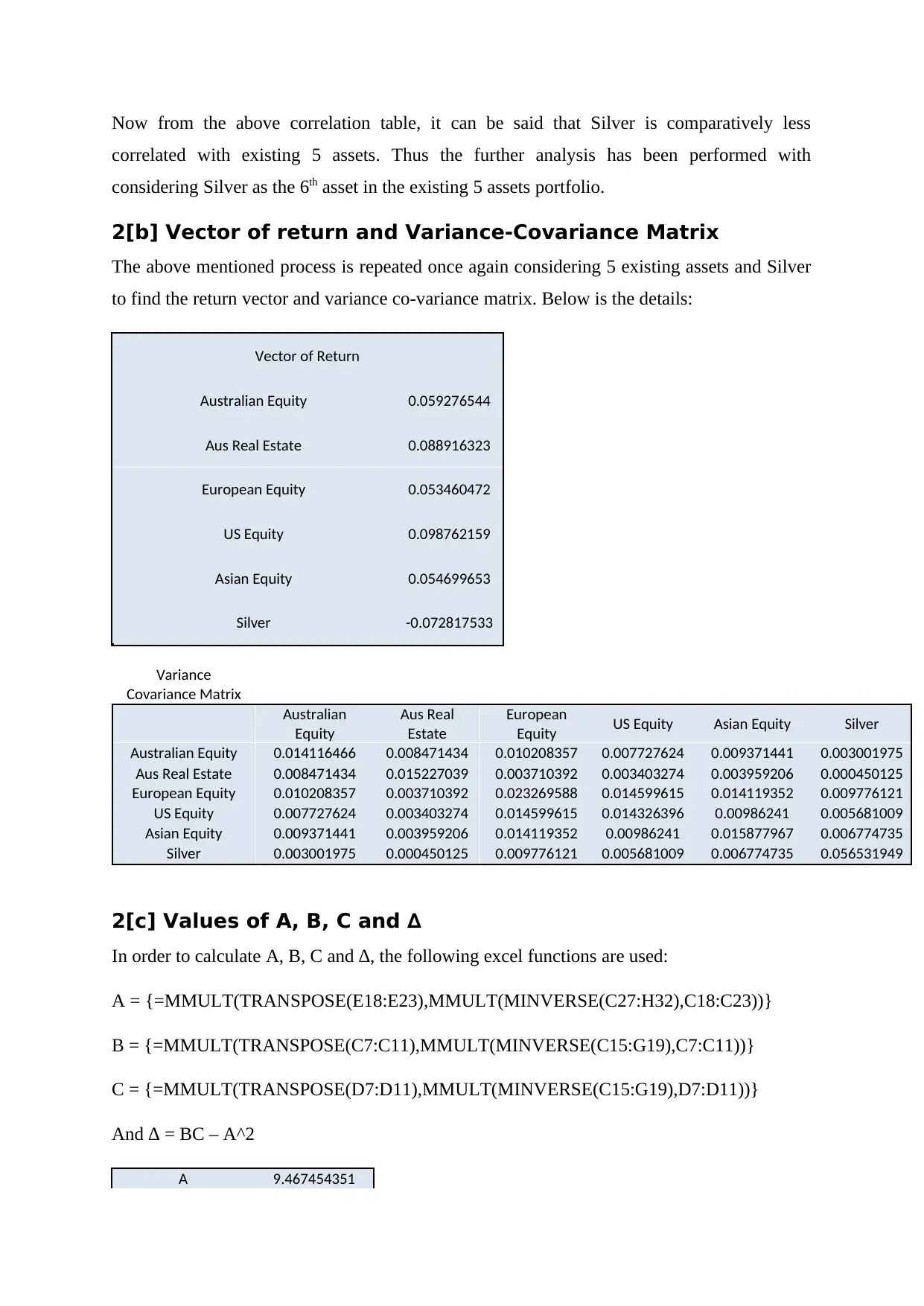

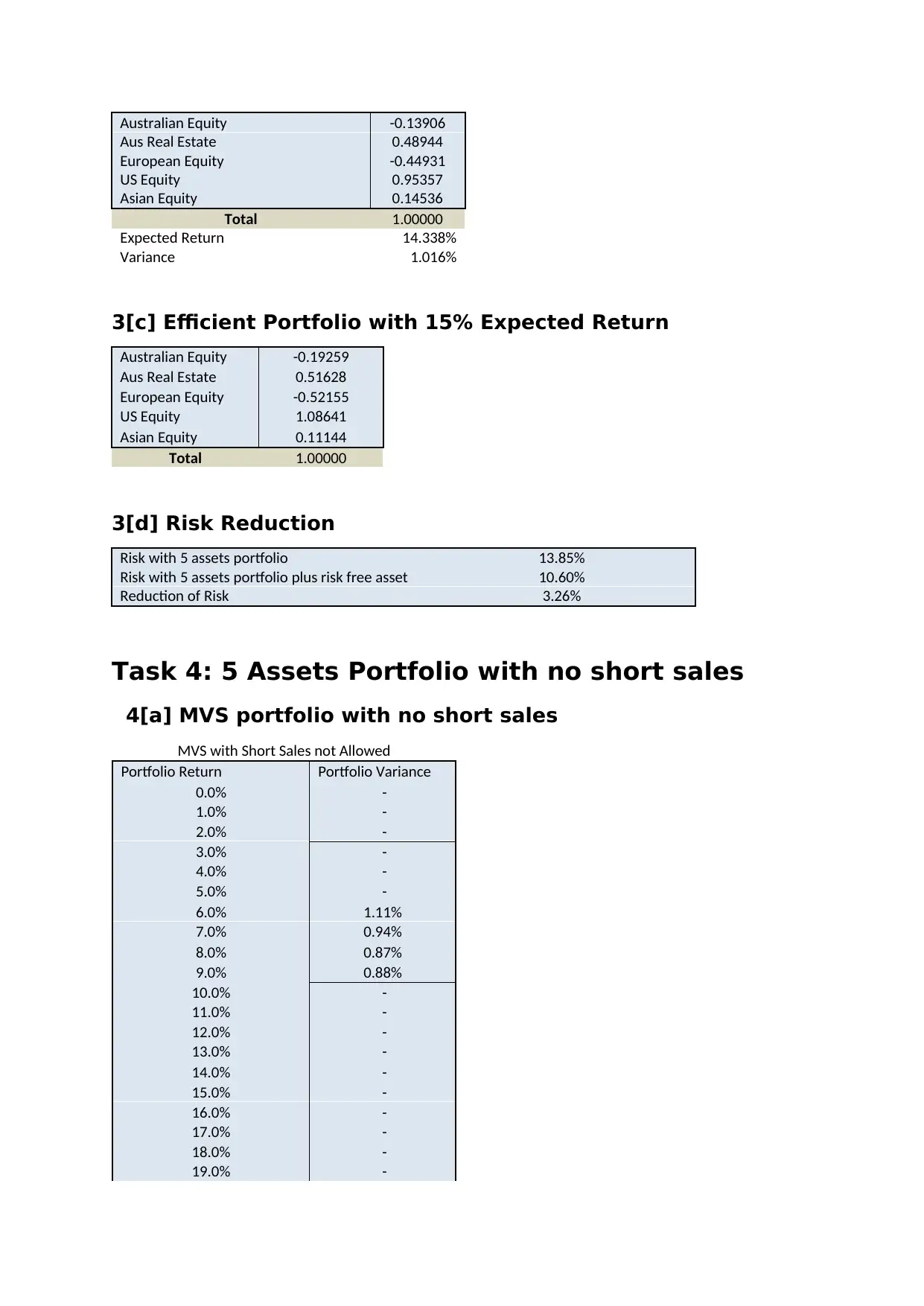

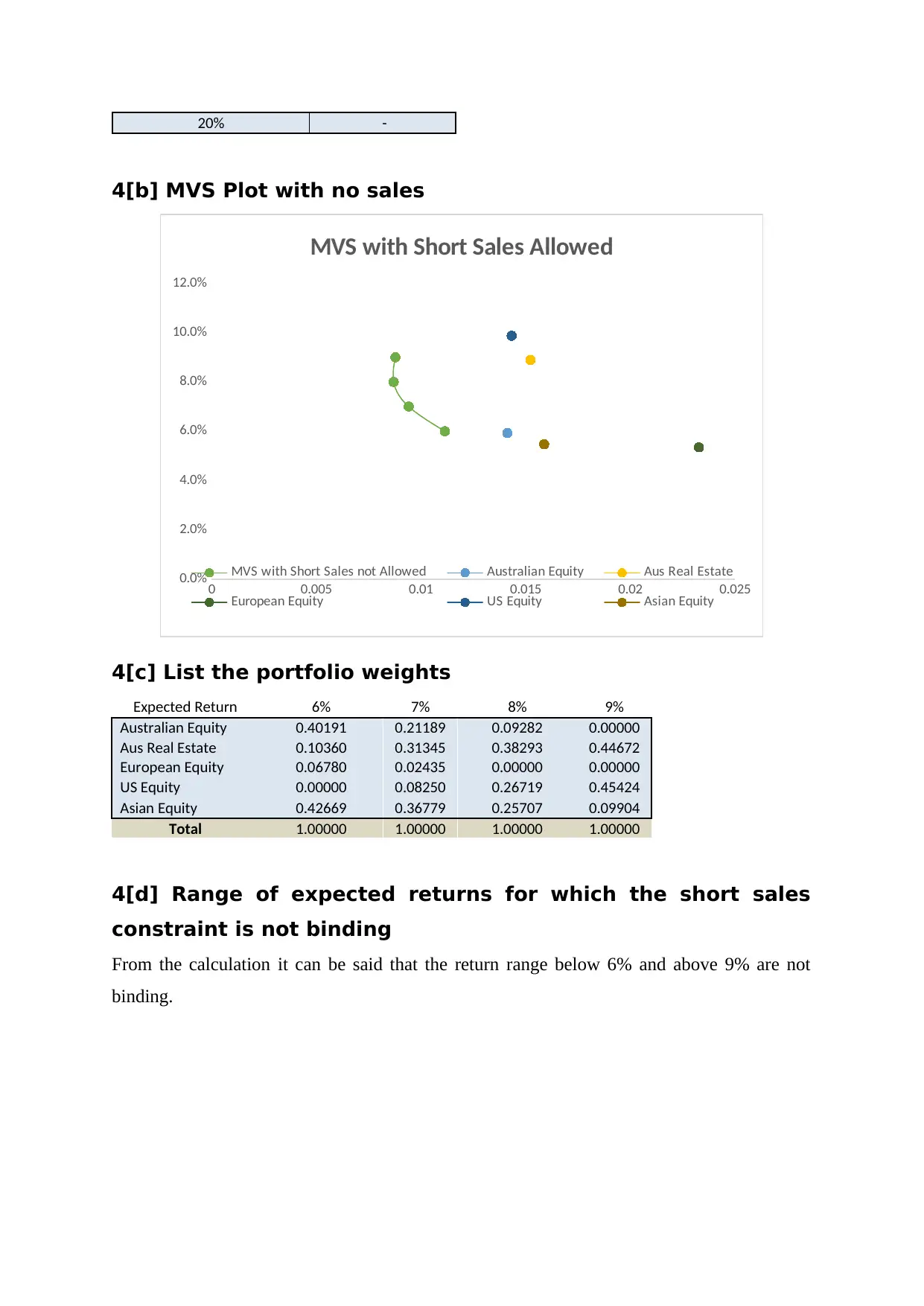

This assignment presents a detailed investment analysis, focusing on portfolio construction and risk management. It begins with a five-asset portfolio, exploring weekly returns, mean-variance analysis, efficient and inefficient assets, and the calculation of key parameters like A, B, C, and delta. The analysis includes MVS plots with and without short sales, determination of the global minimum variance portfolio, and efficient portfolio weights for a 15% expected return. The second part of the assignment expands the portfolio to include a commodity (Silver), repeating the analysis and assessing the impact on risk and return. The final sections incorporate a risk-free rate, construct a tangency portfolio, and analyze portfolio performance with and without short-selling constraints. The assignment demonstrates the application of financial modeling techniques to optimize investment strategies and manage portfolio risk.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.