Investment Management Report: Risk, Return, and Portfolio Optimization

VerifiedAdded on 2023/01/06

|16

|2637

|29

Report

AI Summary

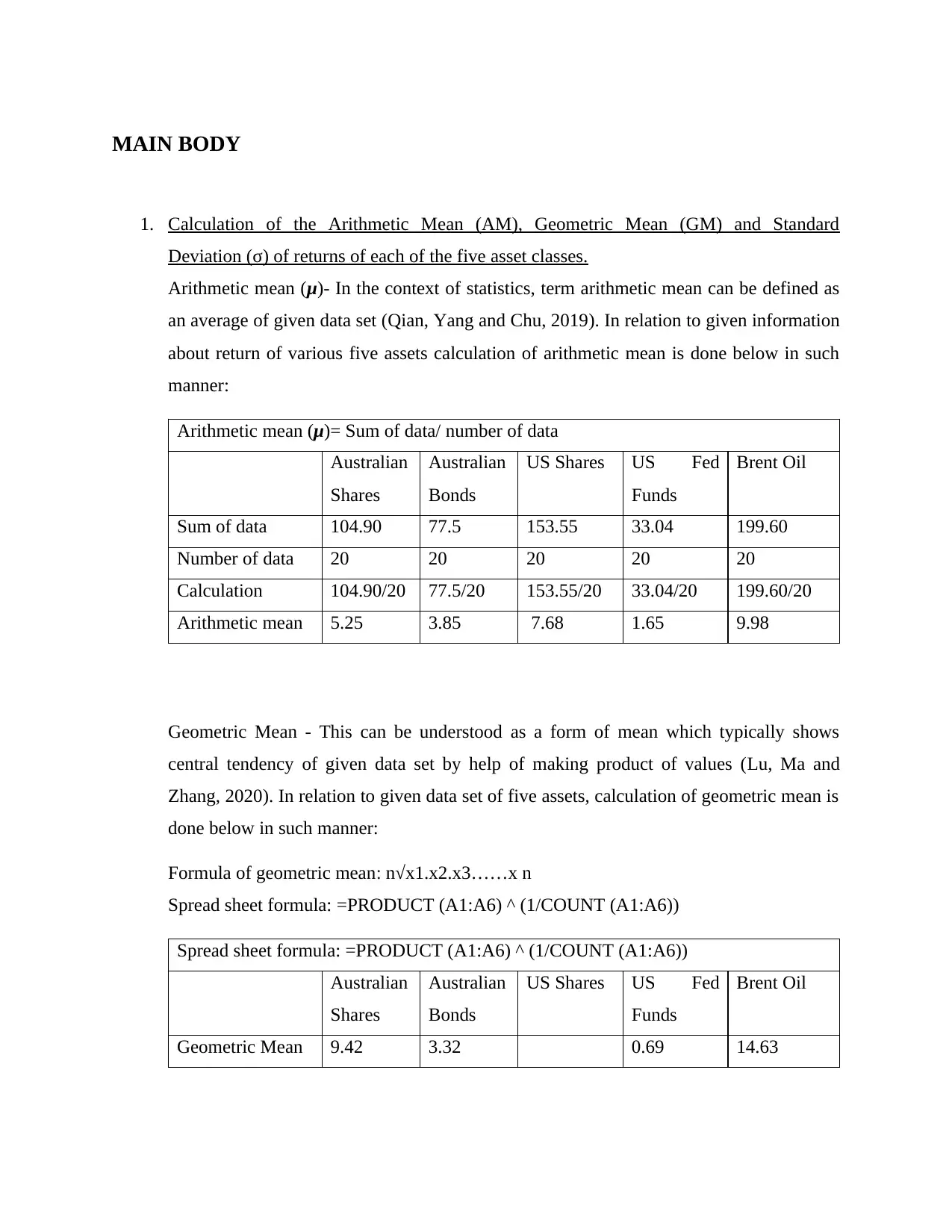

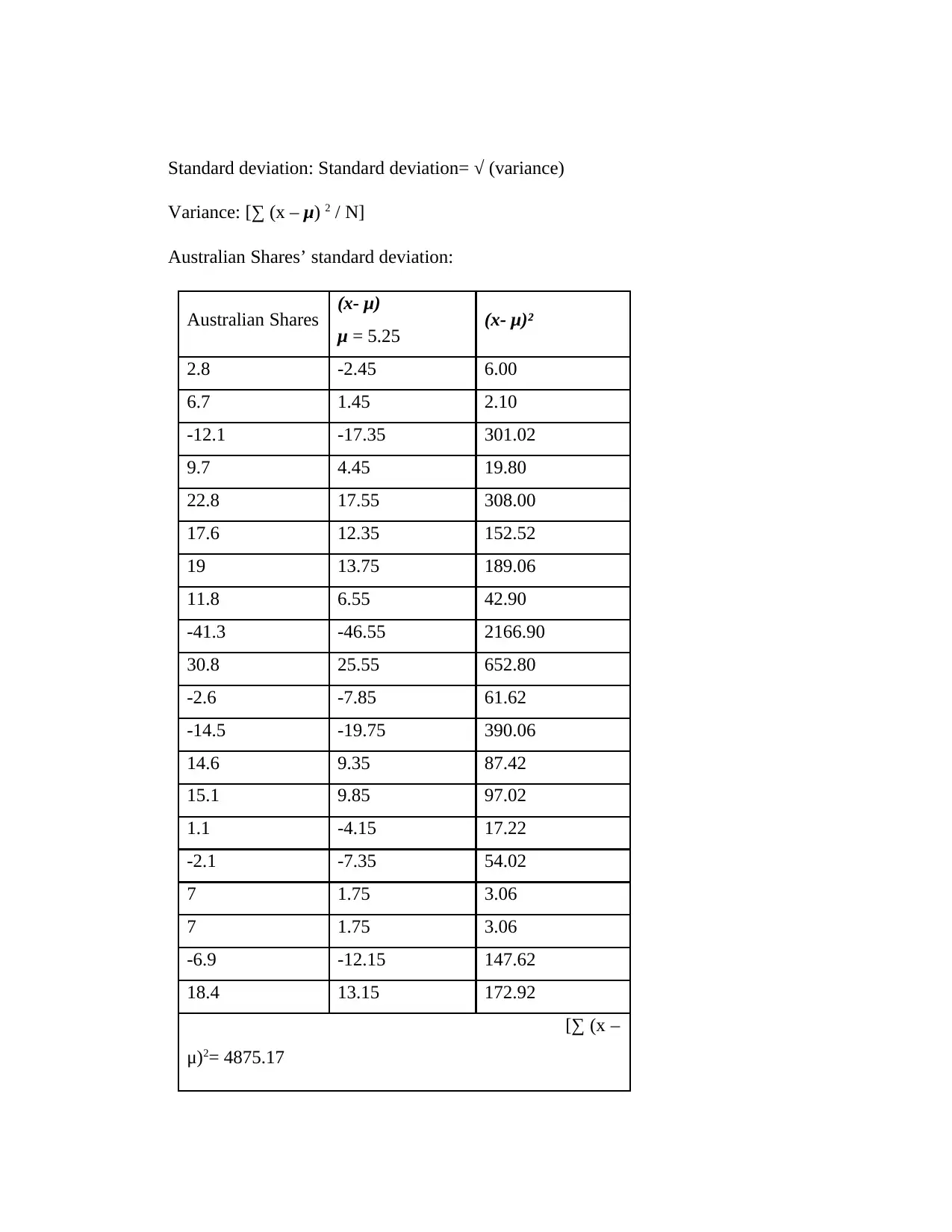

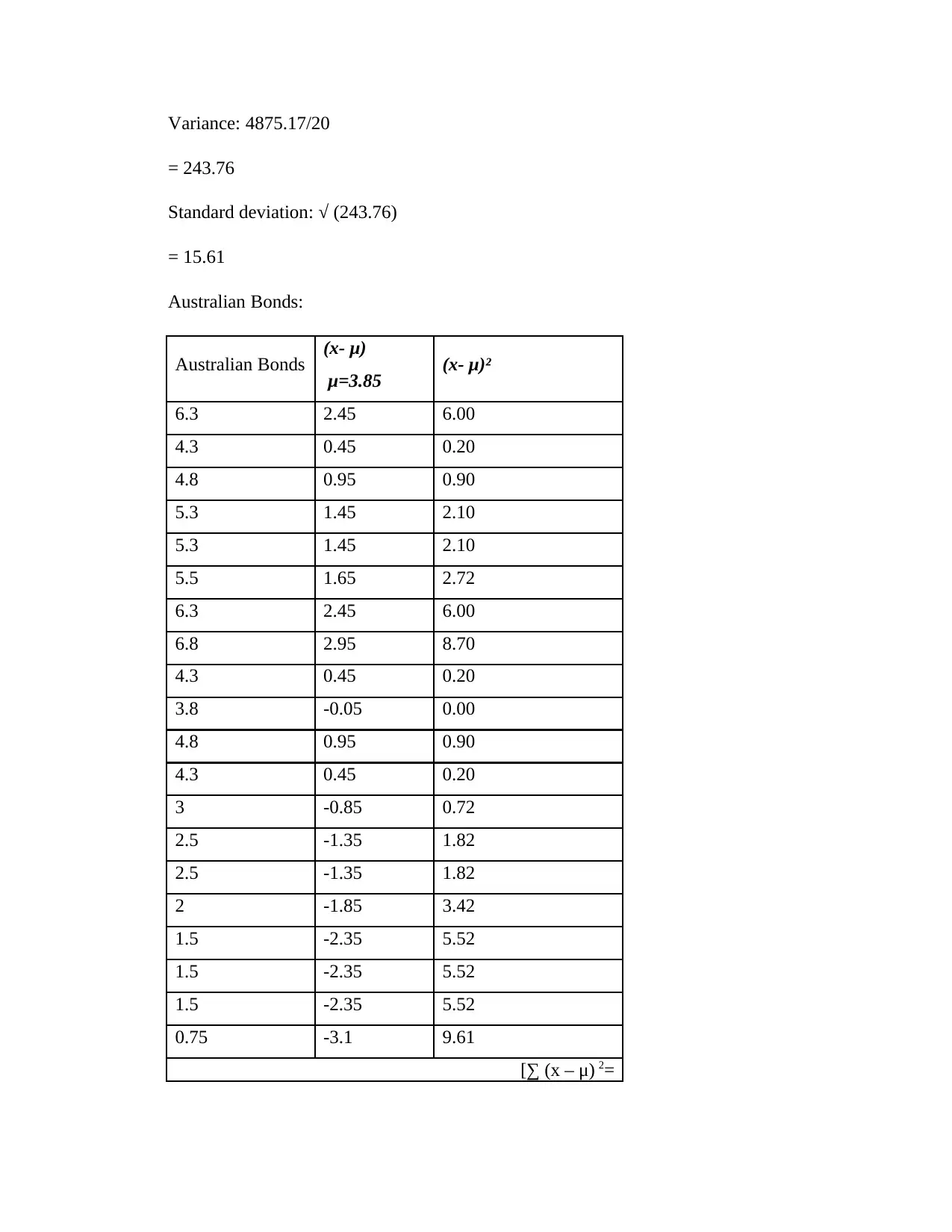

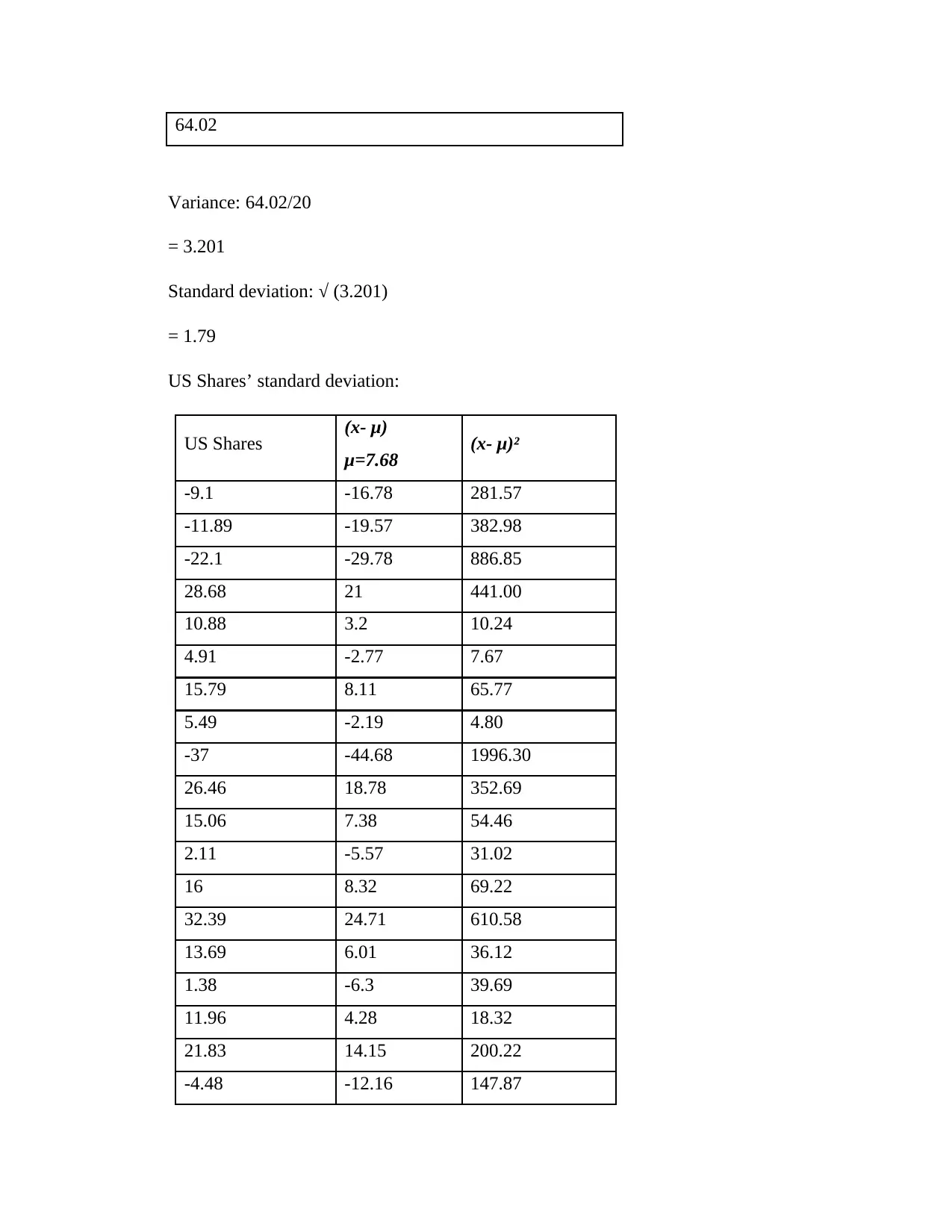

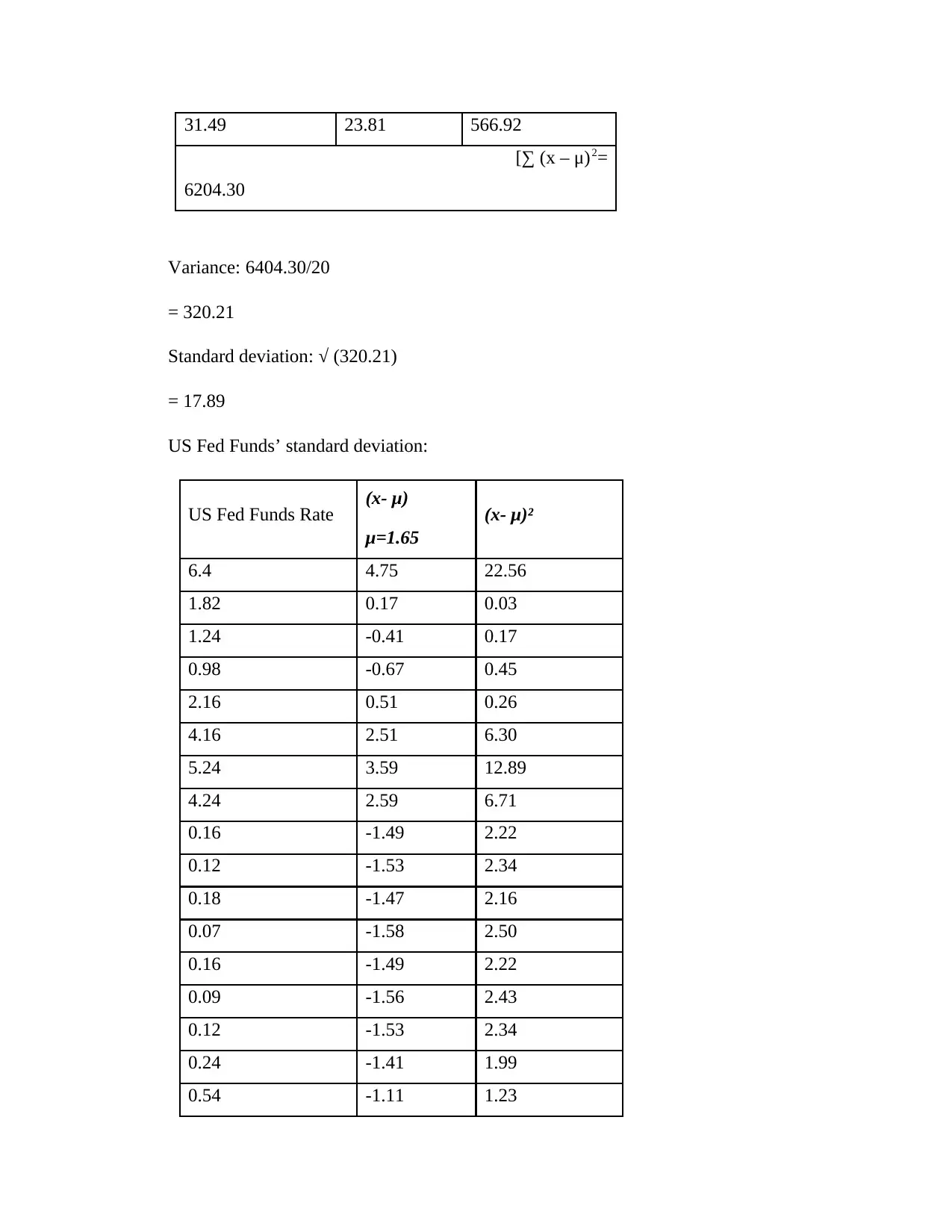

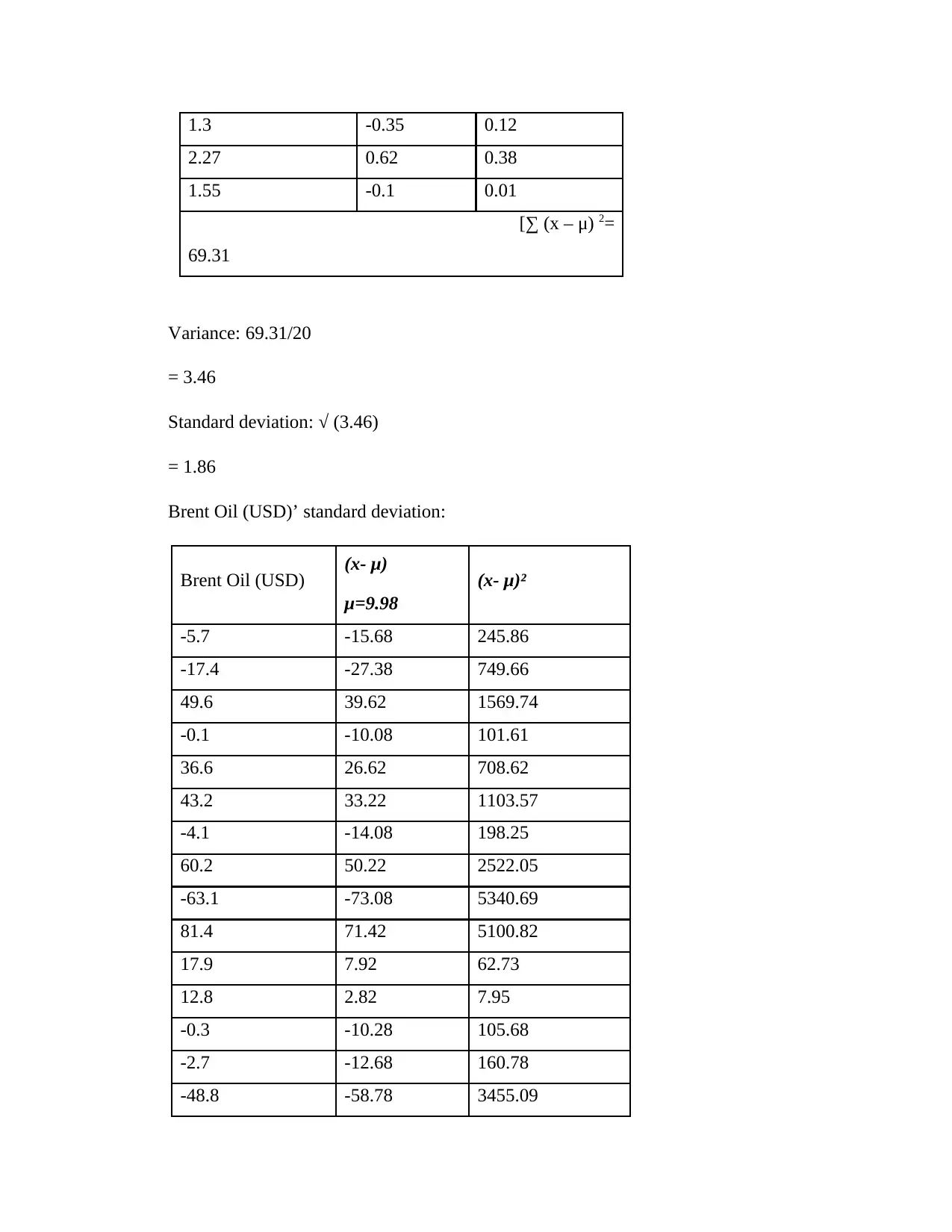

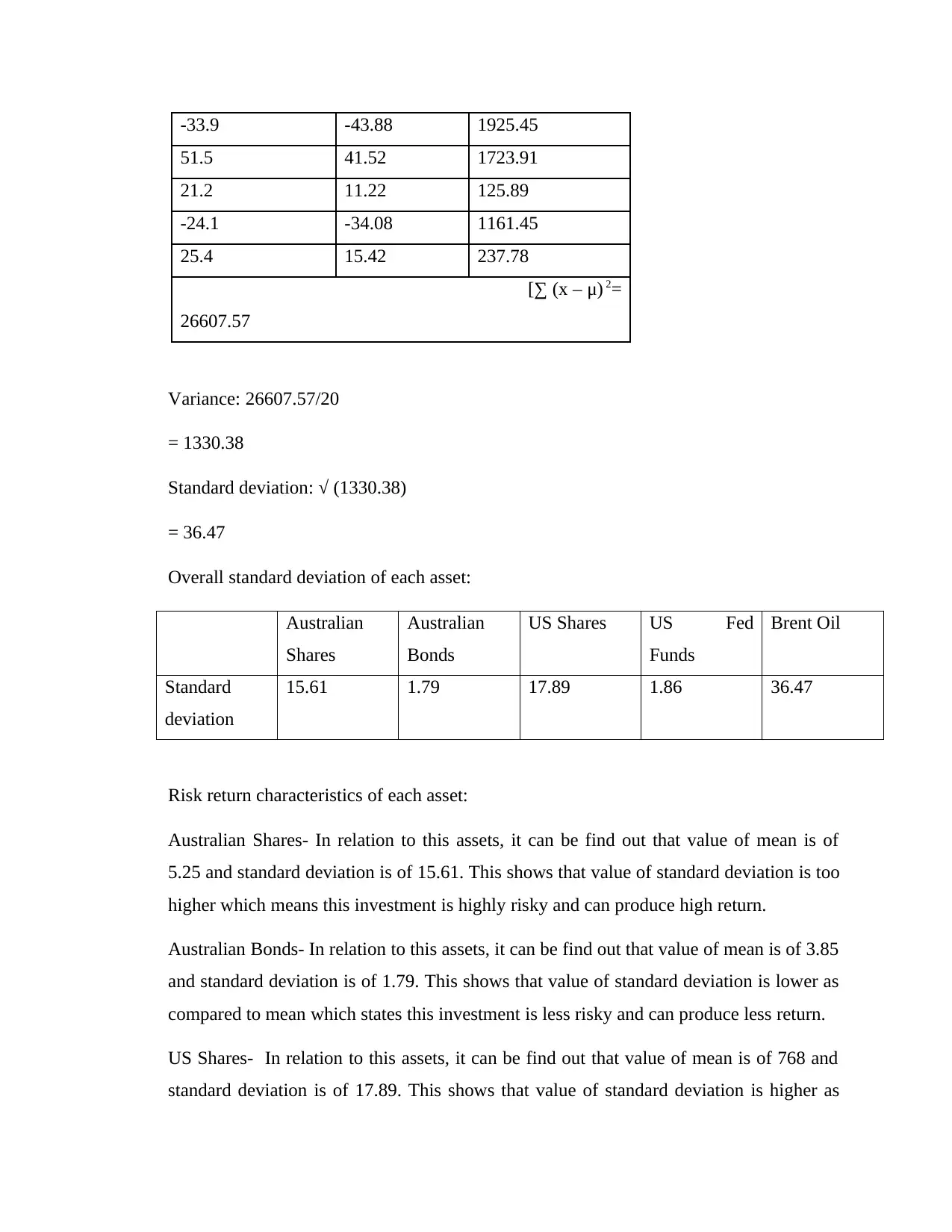

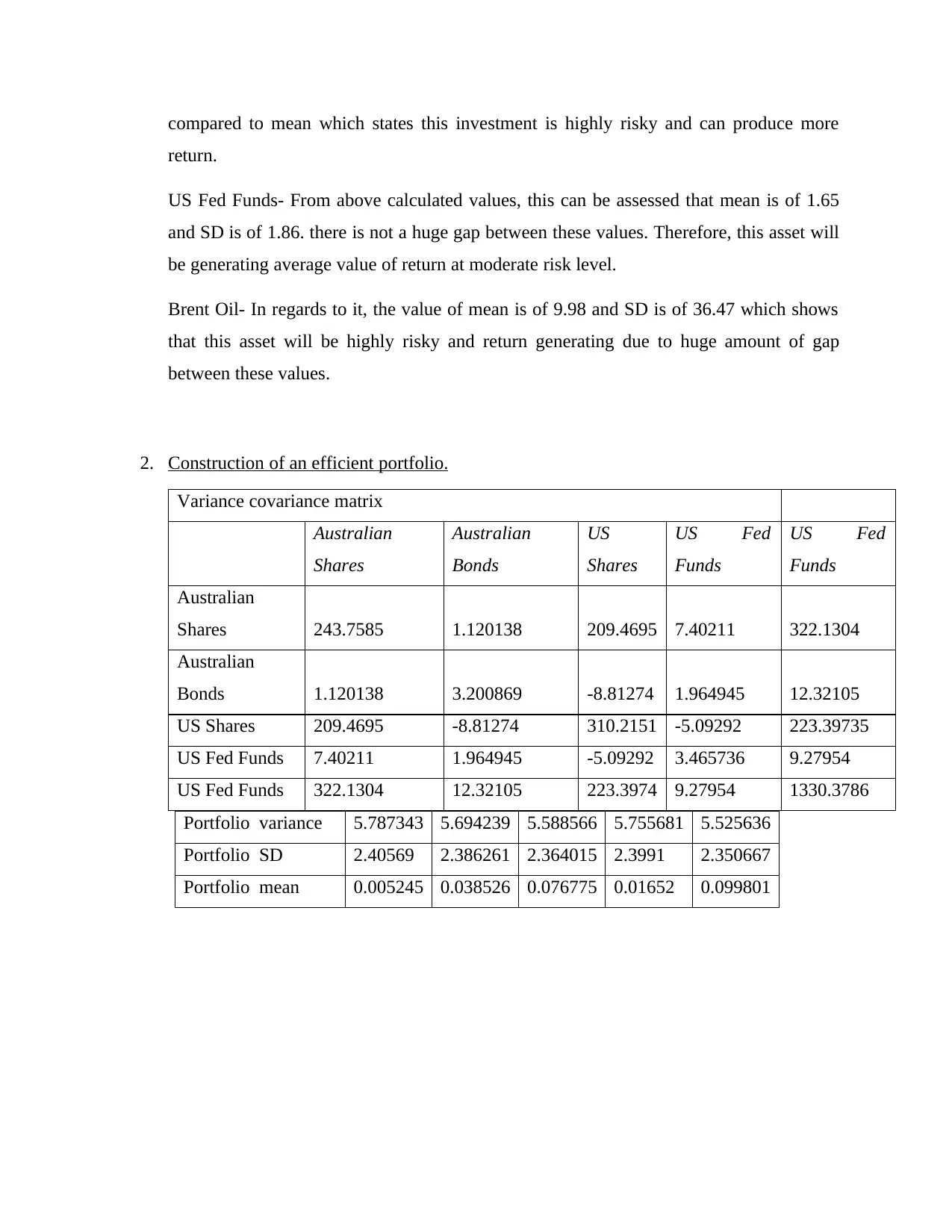

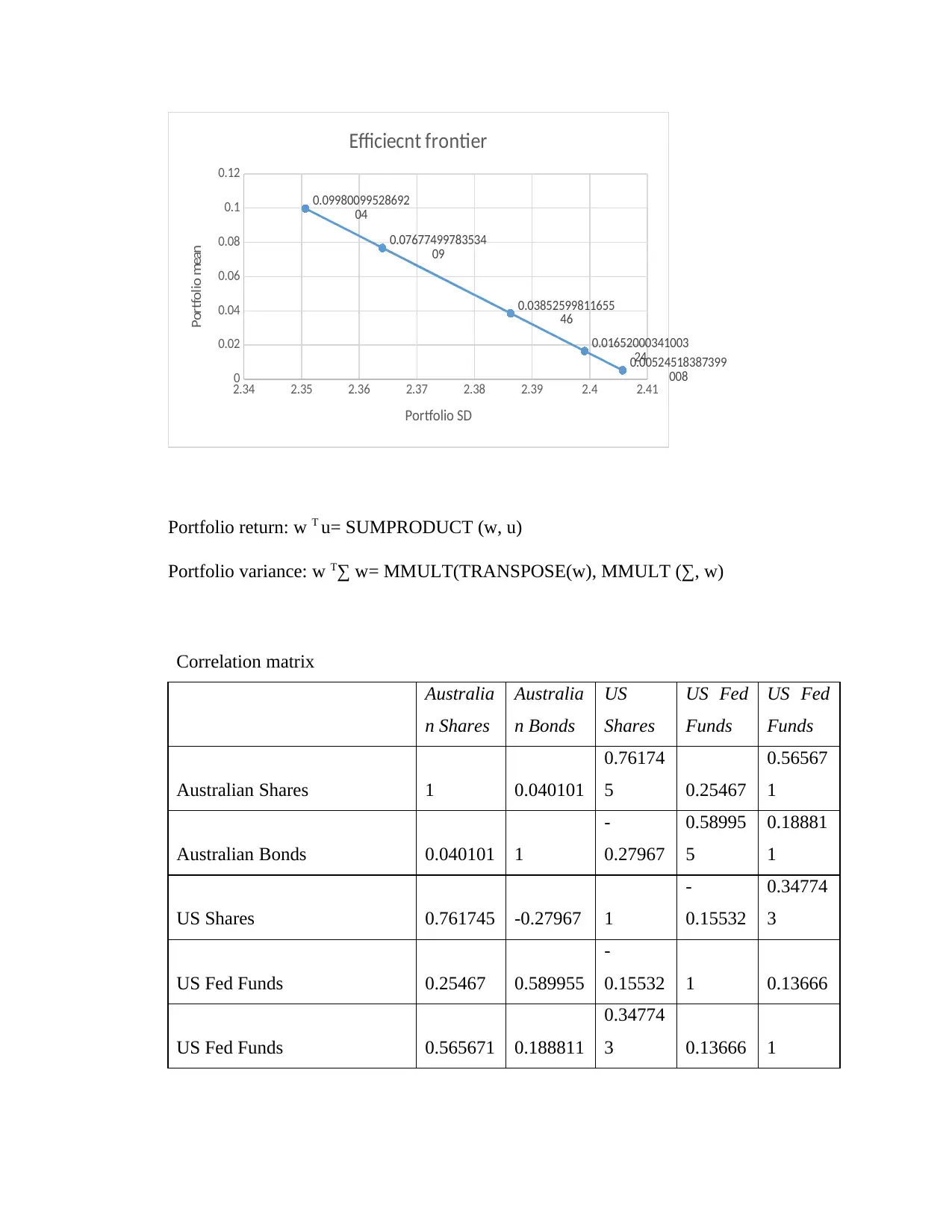

This report provides a detailed analysis of investment management principles, focusing on portfolio construction, risk-return characteristics, and the application of Modern Portfolio Theory (MPT). The report begins with an executive summary followed by the calculation of arithmetic mean (AM), geometric mean (GM), and standard deviation (σ) for five different asset classes: Australian Shares, Australian Bonds, US Shares, US Fed Funds, and Brent Oil. The analysis includes a variance-covariance matrix and the construction of an efficient portfolio, illustrating the relationship between risk and return. The report then delves into a discussion of MPT models, including the Markowitz mean-variance model and its limitations, before concluding with a discussion on diversification failure and its impact on portfolio performance. The findings highlight the importance of asset allocation in achieving high financial performance and minimizing risks, as demonstrated through the analysis of various asset classes.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.