Investment Analysis Project: Portfolio Optimization and Analysis

VerifiedAdded on 2020/05/11

|4

|690

|63

Project

AI Summary

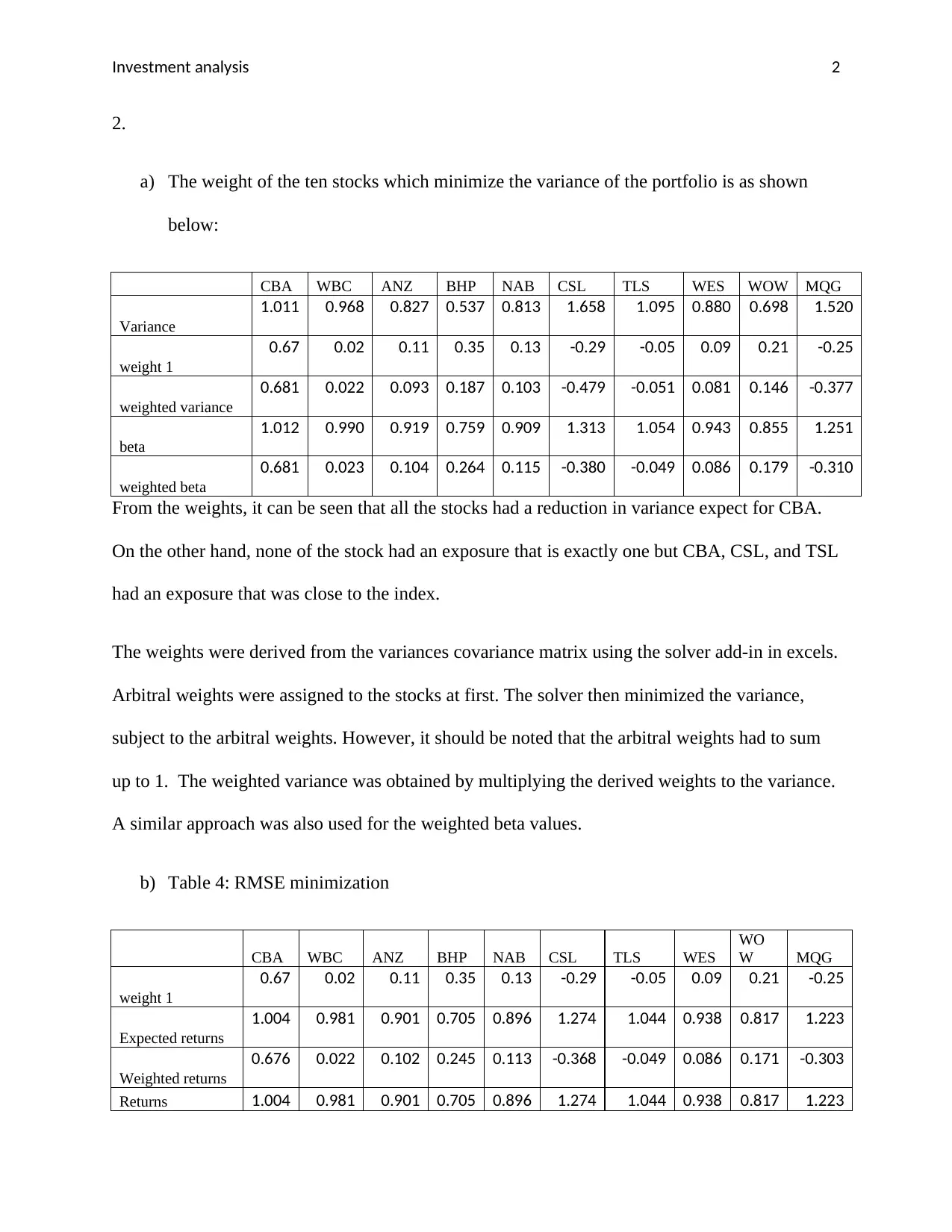

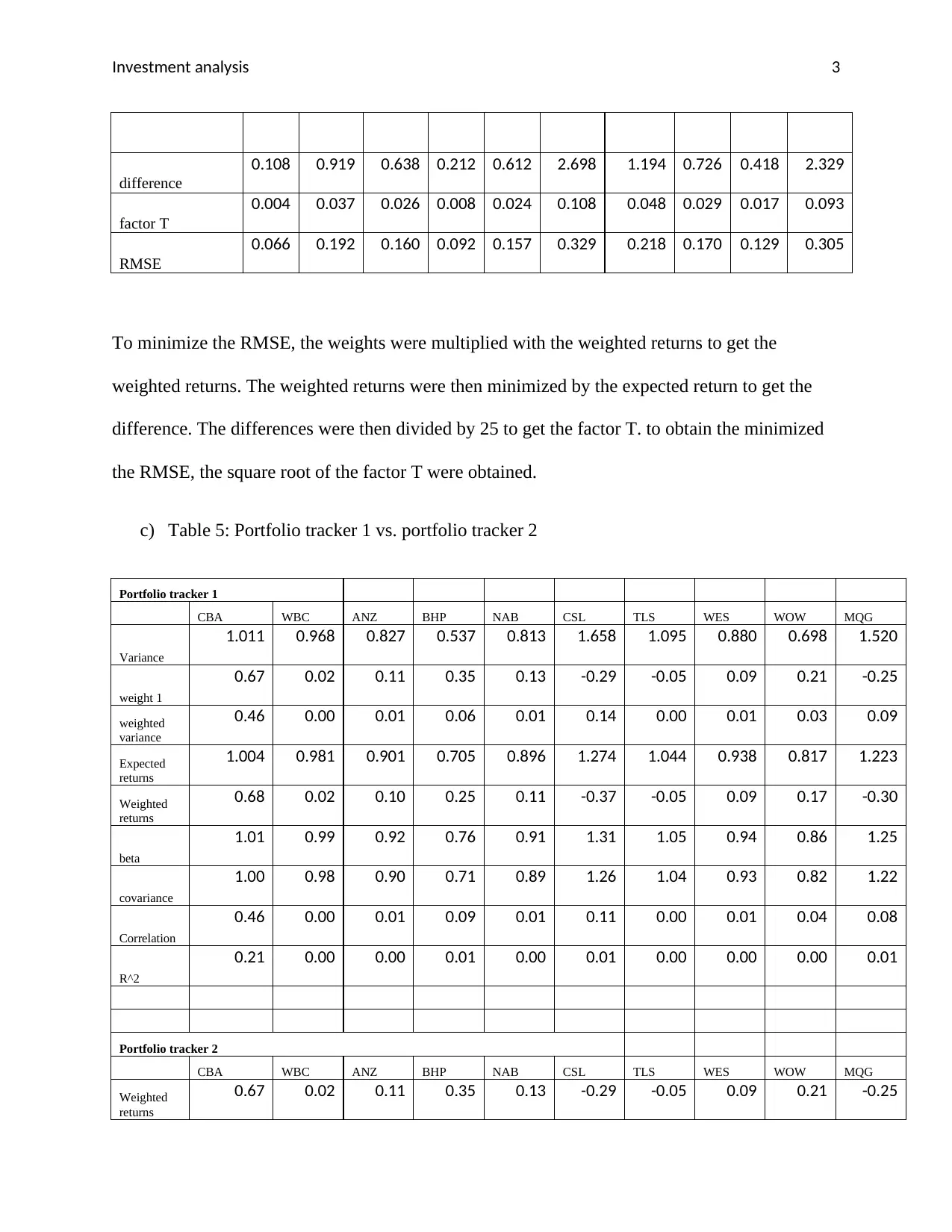

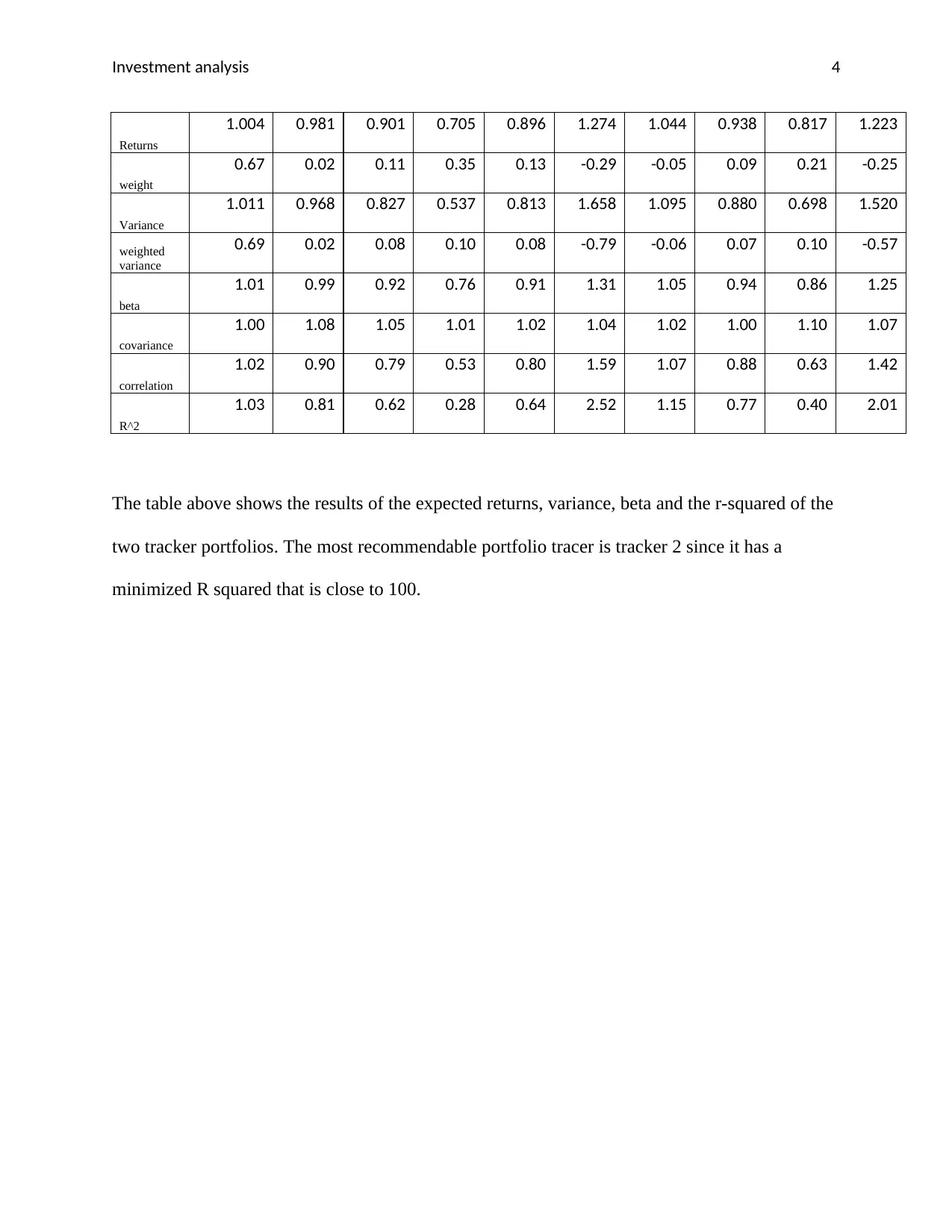

This investment analysis project examines portfolio optimization and performance. It begins by calculating the weights of ten stocks to minimize portfolio variance, presenting the weighted variance and beta for each stock. The analysis then proceeds to minimize the Root Mean Square Error (RMSE) by calculating weighted returns and differences from expected returns. Finally, the project compares two portfolio trackers, evaluating their expected returns, variance, beta, covariance, correlation, and R-squared values to determine the most recommendable portfolio tracker, which is determined to be tracker 2 due to its R-squared value being close to 100.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.