BUS633: Investment Analysis and Portfolio Analysis Report, Semester 1

VerifiedAdded on 2019/09/30

|11

|2980

|1588

Report

AI Summary

This report provides an in-depth analysis of a hypothetical five-asset investment portfolio, encompassing real estate, stocks, gold, bonds, and forward contracts. The analysis applies Modern Portfolio Theory to assess the risk and return characteristics of each asset class and the portfolio as a whole. The report explores diversification strategies to mitigate overall portfolio risk, emphasizing the importance of asset correlation. Valuation techniques such as the Capital Asset Pricing Model (CAPM) and the Dividend Discount Model are applied to evaluate the equity component of the portfolio, specifically focusing on Boeing shares. The report also delves into the valuation and risk assessment of bonds, considering yield to maturity and real rate of return, while addressing the limitations of these methods. Furthermore, the report discusses the role of forward contracts and gold in the portfolio, highlighting their respective risk profiles and strategic considerations. The paper concludes with an evaluation of portfolio beta and capital allocation line to maximize returns and reduce risk. This comprehensive analysis provides valuable insights into investment strategies and portfolio management.

Bus633 Investment Analysis and Portfolio Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................2

Portfolio of Assets......................................................................................................................2

Real Estate..............................................................................................................................2

Gold........................................................................................................................................3

Strategic actions for the reduction in portfolio risks..................................................................3

Conclusion..................................................................................................................................3

Introduction................................................................................................................................2

Portfolio of Assets......................................................................................................................2

Real Estate..............................................................................................................................2

Gold........................................................................................................................................3

Strategic actions for the reduction in portfolio risks..................................................................3

Conclusion..................................................................................................................................3

Portfolio Theory and Lessons learned

Introduction

Investments are made by individuals and organizations in order to grow their money from the

returns obtained from them. These investment options can be various types depending upon

the time frame and exposure to the market. Selecting the appropriate investment which is in

accordance with the risk return capability is important to avail the maximum out of such

investments.

When the various investments are combined together, it forms a portfolio which is less risky

than the individual investment assets (Awoga, 2011). The aim of this report is to analyse

Modern Portfolio Theory and review the five asset portfolio for their risk and return

capabilities.

The aim of this report is to analyse the risk return profile of a hypothetical portfolio based out

of five different asset classes. These assets would include, real estate, stocks, gold, bond, and

forward contracts. The process of diversification has been discussed in detail which helps to

reduce the overall risk of the portfolio.

This paper also applies dividend discount model and capital asset pricing model which would

be applied for the evaluation of stocks. This paper also discusses portfolio beta which

indicate the sensitivity of the asset classes with the changes in the market. Based on these

concepts of asset and modern portfolio theory, the risk and return of the entire portfolio has

been evaluated.

Modern Portfolio Theory and the related assets

This theory is based on assembling of assets in a manner which maximises the total return at

a given level of risk. Thus various kinds of financial assets are used and combined together

for investment. This theory was introduced by Harry Markowitz in the year 1952. Some of

the important features of this theory are as follows:

Diversification- This theory indicates that the overall portfolio risk can be reduced by holding

the assets which are not perfectly positively related. The correlation between the asset pair

plays an important role to determine the portfolio’s return variance.

Introduction

Investments are made by individuals and organizations in order to grow their money from the

returns obtained from them. These investment options can be various types depending upon

the time frame and exposure to the market. Selecting the appropriate investment which is in

accordance with the risk return capability is important to avail the maximum out of such

investments.

When the various investments are combined together, it forms a portfolio which is less risky

than the individual investment assets (Awoga, 2011). The aim of this report is to analyse

Modern Portfolio Theory and review the five asset portfolio for their risk and return

capabilities.

The aim of this report is to analyse the risk return profile of a hypothetical portfolio based out

of five different asset classes. These assets would include, real estate, stocks, gold, bond, and

forward contracts. The process of diversification has been discussed in detail which helps to

reduce the overall risk of the portfolio.

This paper also applies dividend discount model and capital asset pricing model which would

be applied for the evaluation of stocks. This paper also discusses portfolio beta which

indicate the sensitivity of the asset classes with the changes in the market. Based on these

concepts of asset and modern portfolio theory, the risk and return of the entire portfolio has

been evaluated.

Modern Portfolio Theory and the related assets

This theory is based on assembling of assets in a manner which maximises the total return at

a given level of risk. Thus various kinds of financial assets are used and combined together

for investment. This theory was introduced by Harry Markowitz in the year 1952. Some of

the important features of this theory are as follows:

Diversification- This theory indicates that the overall portfolio risk can be reduced by holding

the assets which are not perfectly positively related. The correlation between the asset pair

plays an important role to determine the portfolio’s return variance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expected return and risk- This theory makes an assumption that the investors are risk averse

and would try to choose that portfolio which provides less risk with the same expected

returns. However the individual risk profile of the investor may differ which allow them to

select a portfolio with high risk and return.

Capital Allocation line- Modern Portfolio theory indicates the best possible allocation of the

assets which maximises the return from the entire investment. The efficient frontier indicate

the best return possible at a given rate of risk. The tangency point is the best capital allocation

line which indicate the maximum profit the investor can expect out of the portfolio.

Mutual Fund Theorem- The mutual fund theorem is also supportive of the modern portfolio

theory. It indicates that in the case of the risk free asset, any portfolio on the efficient frontier

can be achieved if it lies between the two mutual funds.

Risk free asset- This is one of the important part of the modern portfolio theory. It is one of

the tangency point to the efficient frontier hyperbola.

Using these theories, we would allocate the resources in various assets in order to attain

maximum return from the portfolio.

Portfolio of Assets

The five assets would be allocation in the proportion as follows:

Bonds- 35%

Shares- 30%

Forward Contracts- 15%

Gold- 5%

Real estate- 15%

These allocation would be altered depending upon the market situations and also till the

capital allocation line is tangent to the efficient frontier of the portfolio. Such is an optimal

situation as any combination of portfolio would not be able to provide the return which is

higher than the equilibrium tangency point.

The five assets which have been evaluated to be included in a portfolio are as follows:

and would try to choose that portfolio which provides less risk with the same expected

returns. However the individual risk profile of the investor may differ which allow them to

select a portfolio with high risk and return.

Capital Allocation line- Modern Portfolio theory indicates the best possible allocation of the

assets which maximises the return from the entire investment. The efficient frontier indicate

the best return possible at a given rate of risk. The tangency point is the best capital allocation

line which indicate the maximum profit the investor can expect out of the portfolio.

Mutual Fund Theorem- The mutual fund theorem is also supportive of the modern portfolio

theory. It indicates that in the case of the risk free asset, any portfolio on the efficient frontier

can be achieved if it lies between the two mutual funds.

Risk free asset- This is one of the important part of the modern portfolio theory. It is one of

the tangency point to the efficient frontier hyperbola.

Using these theories, we would allocate the resources in various assets in order to attain

maximum return from the portfolio.

Portfolio of Assets

The five assets would be allocation in the proportion as follows:

Bonds- 35%

Shares- 30%

Forward Contracts- 15%

Gold- 5%

Real estate- 15%

These allocation would be altered depending upon the market situations and also till the

capital allocation line is tangent to the efficient frontier of the portfolio. Such is an optimal

situation as any combination of portfolio would not be able to provide the return which is

higher than the equilibrium tangency point.

The five assets which have been evaluated to be included in a portfolio are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate

Real estate is one of the investment asset which provides an exposure to the infrastructure

development in a country. The return of this asset class is directly proportional to the growth

and development of the country. When an economy grows, the per capita income of its

population also increases which allow them to buy houses for residential and commercial

activities. Thus this is one such sector which is directly related with the economic booms and

recessions.

Thus to include this investment class in the portfolio, Viking Constructions in Connecticut,

USA has been chosen. An apartment has been selected in this property for investment. This is

one of the developing cities of United States. According to 2015 data, the population of this

city was approximately 895,841. This property has been selected as it is managed and built

by one of the popular constructor. The cost of this property is estimated to be $150,000 with

the potential to generate income around $8000 annually.

There will be various identified risks with the management and handling of this asset class.

For example there would be a monthly payment towards the maintenance fees of the property

(Berkman, 2012). Apart from such payment, there are risks associated with various

contingencies like emergency situations, etc. Thus planning for such risks would help reduce

the overall risk related with the asset. However there would be certain tax benefits which

would be experienced in relation with the investment in real estate property.

Gold

The expose to commodity asset like gold would help to reduce the overall risk of the

combined portfolio. Gold is one such commodity which is highly popular and has been

around since a very long term. This metal is invested by all for both long term and short term

investments. The investment in this asset class is exposed to risks related with uncertainties

related with the fluctuation in prices. The movement in price of this investment asset is

similar to that of shares. It is entirely dependent on the forces of demand and supply.

In order to restrict the risk faced through this asset, inflation hedge would be one of the

constructive solution (Bukhvalova, 2013). As the economists Phillips suggested, the inflation

rate is directly proportional to the level of demand in global economy, this risk should be

strategically mitigated. Apart from the inflationary risk, there is other risk related with the

investment in this asset. These risks are risk of theft, risk of loss and risk related with the

Real estate is one of the investment asset which provides an exposure to the infrastructure

development in a country. The return of this asset class is directly proportional to the growth

and development of the country. When an economy grows, the per capita income of its

population also increases which allow them to buy houses for residential and commercial

activities. Thus this is one such sector which is directly related with the economic booms and

recessions.

Thus to include this investment class in the portfolio, Viking Constructions in Connecticut,

USA has been chosen. An apartment has been selected in this property for investment. This is

one of the developing cities of United States. According to 2015 data, the population of this

city was approximately 895,841. This property has been selected as it is managed and built

by one of the popular constructor. The cost of this property is estimated to be $150,000 with

the potential to generate income around $8000 annually.

There will be various identified risks with the management and handling of this asset class.

For example there would be a monthly payment towards the maintenance fees of the property

(Berkman, 2012). Apart from such payment, there are risks associated with various

contingencies like emergency situations, etc. Thus planning for such risks would help reduce

the overall risk related with the asset. However there would be certain tax benefits which

would be experienced in relation with the investment in real estate property.

Gold

The expose to commodity asset like gold would help to reduce the overall risk of the

combined portfolio. Gold is one such commodity which is highly popular and has been

around since a very long term. This metal is invested by all for both long term and short term

investments. The investment in this asset class is exposed to risks related with uncertainties

related with the fluctuation in prices. The movement in price of this investment asset is

similar to that of shares. It is entirely dependent on the forces of demand and supply.

In order to restrict the risk faced through this asset, inflation hedge would be one of the

constructive solution (Bukhvalova, 2013). As the economists Phillips suggested, the inflation

rate is directly proportional to the level of demand in global economy, this risk should be

strategically mitigated. Apart from the inflationary risk, there is other risk related with the

investment in this asset. These risks are risk of theft, risk of loss and risk related with the

interest payments. Therefore the value of investment in gold has been kept at a level of 5% in

the total portfolio.

Another diminishing factors is that gold as an investment does not earn any dividends or

interest as shares and bonds. Therefore this investment would only generate returns when it is

sold in the market at higher prices.

Forward Contracts

The investment portfolio also contain forward contracts which is based on the future price

movements of the underlying assets. These contracts require continuous management and

tracking of the market. In order to determine the return from the future, fundamental and

technical analysis would be used (Jones, 2017). The fundamental analysis would identify and

examine the underlying situations which would lead to movement in the prices of the asset.

On the other hand, the technical analysis would help in evaluation of the forward contract for

its return capability. These two types of analysis would help predict the future price

movements.

Apart from these two analysis, various charts and tools would be used to determine the future

price movements. I would take the help of financial analysts and advisors to determine the

lucrative investment opportunities.

Bonds

The investments in bond would form around 35% of my investment in the total portfolio. The

valuation of bonds can be done in various ways. The most important is the bond’s yield to

maturity which can easily be calculated. An example of investment in bond is as follows:

Suppose we hold a bond with the face value of $100 and have 30 months of maturity. It is

available at discount rate of $95.92. It also pays coupon semi-annually at the rate of 5%.

Therefore the yield of the bond would be 5.21%. However this method of bond evaluation

has certain limitations. This method do not consider the effect of taxes which we need to pay

on the bonds. Therefore some of the financial analysts indicate this method as gross

redemption yield (Julianto, 2013). Another major limitation of this method is that it does not

take into consideration the selling or the purchasing costs.

the total portfolio.

Another diminishing factors is that gold as an investment does not earn any dividends or

interest as shares and bonds. Therefore this investment would only generate returns when it is

sold in the market at higher prices.

Forward Contracts

The investment portfolio also contain forward contracts which is based on the future price

movements of the underlying assets. These contracts require continuous management and

tracking of the market. In order to determine the return from the future, fundamental and

technical analysis would be used (Jones, 2017). The fundamental analysis would identify and

examine the underlying situations which would lead to movement in the prices of the asset.

On the other hand, the technical analysis would help in evaluation of the forward contract for

its return capability. These two types of analysis would help predict the future price

movements.

Apart from these two analysis, various charts and tools would be used to determine the future

price movements. I would take the help of financial analysts and advisors to determine the

lucrative investment opportunities.

Bonds

The investments in bond would form around 35% of my investment in the total portfolio. The

valuation of bonds can be done in various ways. The most important is the bond’s yield to

maturity which can easily be calculated. An example of investment in bond is as follows:

Suppose we hold a bond with the face value of $100 and have 30 months of maturity. It is

available at discount rate of $95.92. It also pays coupon semi-annually at the rate of 5%.

Therefore the yield of the bond would be 5.21%. However this method of bond evaluation

has certain limitations. This method do not consider the effect of taxes which we need to pay

on the bonds. Therefore some of the financial analysts indicate this method as gross

redemption yield (Julianto, 2013). Another major limitation of this method is that it does not

take into consideration the selling or the purchasing costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This method is also criticised as it make certain assumptions about the future which is

unpredictable. Some of these assumptions which may not hold true are as follows:

The bond may not be held by the investor till maturity.

The investor may not reinvest all the coupons received from the bond.

The issuer of the bond may default and do not pay the proceeds at the end of the

period.

Because of these limitations, there are various other methods proposed by the financial

experts. We can also evaluate the value of the bond through determining the real rate of

return. This can be easily calculated through subtracting the inflation rate from the yield rate.

Suppose a bond has a yield of 5% and the inflation rate is 3%. The real rate of return in such

case would be 2%.

The bonds of the companies are subjected to various risks related with the issuing company

performance. The short term and long term liquidity position of the companies should be

evaluated from the financial statement in order to be sure of the creditworthiness of their

financial position. In the recent past, there has been some companies which has filed for

bankruptcy when they were unable to pay to their creditors.

Equity Shares

The equity would form 30% of the total investment in the portfolio. The stocks of high return

companies operating in various sectors would be selected for investment. These shares which

provide high returns are also subjected to high risks related with the fluctuations in the price

movement.

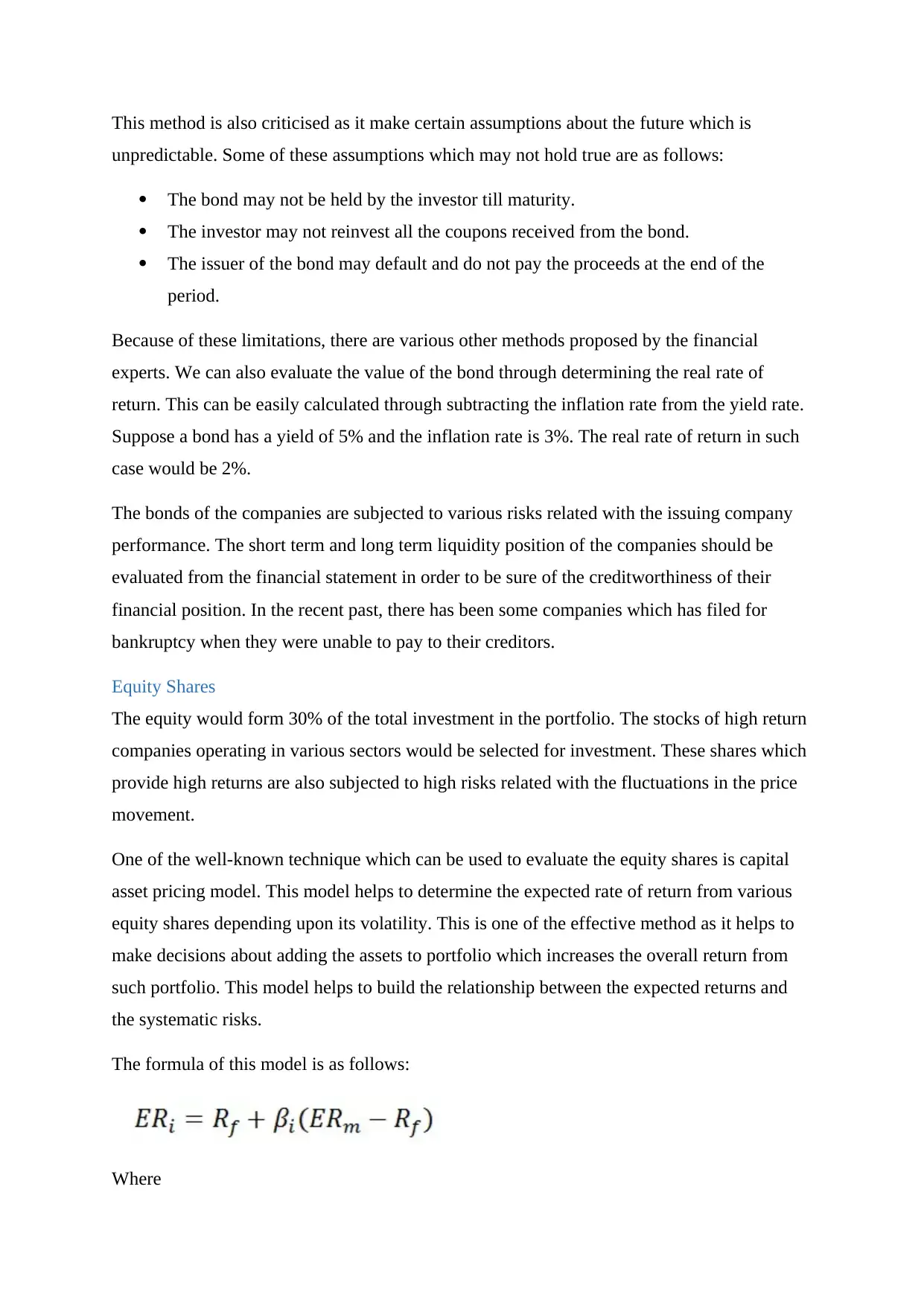

One of the well-known technique which can be used to evaluate the equity shares is capital

asset pricing model. This model helps to determine the expected rate of return from various

equity shares depending upon its volatility. This is one of the effective method as it helps to

make decisions about adding the assets to portfolio which increases the overall return from

such portfolio. This model helps to build the relationship between the expected returns and

the systematic risks.

The formula of this model is as follows:

Where

unpredictable. Some of these assumptions which may not hold true are as follows:

The bond may not be held by the investor till maturity.

The investor may not reinvest all the coupons received from the bond.

The issuer of the bond may default and do not pay the proceeds at the end of the

period.

Because of these limitations, there are various other methods proposed by the financial

experts. We can also evaluate the value of the bond through determining the real rate of

return. This can be easily calculated through subtracting the inflation rate from the yield rate.

Suppose a bond has a yield of 5% and the inflation rate is 3%. The real rate of return in such

case would be 2%.

The bonds of the companies are subjected to various risks related with the issuing company

performance. The short term and long term liquidity position of the companies should be

evaluated from the financial statement in order to be sure of the creditworthiness of their

financial position. In the recent past, there has been some companies which has filed for

bankruptcy when they were unable to pay to their creditors.

Equity Shares

The equity would form 30% of the total investment in the portfolio. The stocks of high return

companies operating in various sectors would be selected for investment. These shares which

provide high returns are also subjected to high risks related with the fluctuations in the price

movement.

One of the well-known technique which can be used to evaluate the equity shares is capital

asset pricing model. This model helps to determine the expected rate of return from various

equity shares depending upon its volatility. This is one of the effective method as it helps to

make decisions about adding the assets to portfolio which increases the overall return from

such portfolio. This model helps to build the relationship between the expected returns and

the systematic risks.

The formula of this model is as follows:

Where

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

E (Ri) is the expected rate of return from the asset

Rf is the risk free rate

Bi if the beta which indicate the volatility of the asset in relation to market

E(Rm) is the expected rate of return from a market portfolio

Thus the selected company whose stock would be purchased is Boeing. It is one of the

airplane manufacturing company which has record of strong performance. We would try to

evaluate the expected rate of return from Boeing shares (Maio & Santa-Clara, 2012). The risk

free rate is the Treasury bill rate which is 1.5% in United States. The market beta for the

shares of Boeing is 1.33 and the expected return from market portfolio is 10%. Therefore the

required rate of return would be 14.8%. This is expected from the investors of the equity

shares in the company.

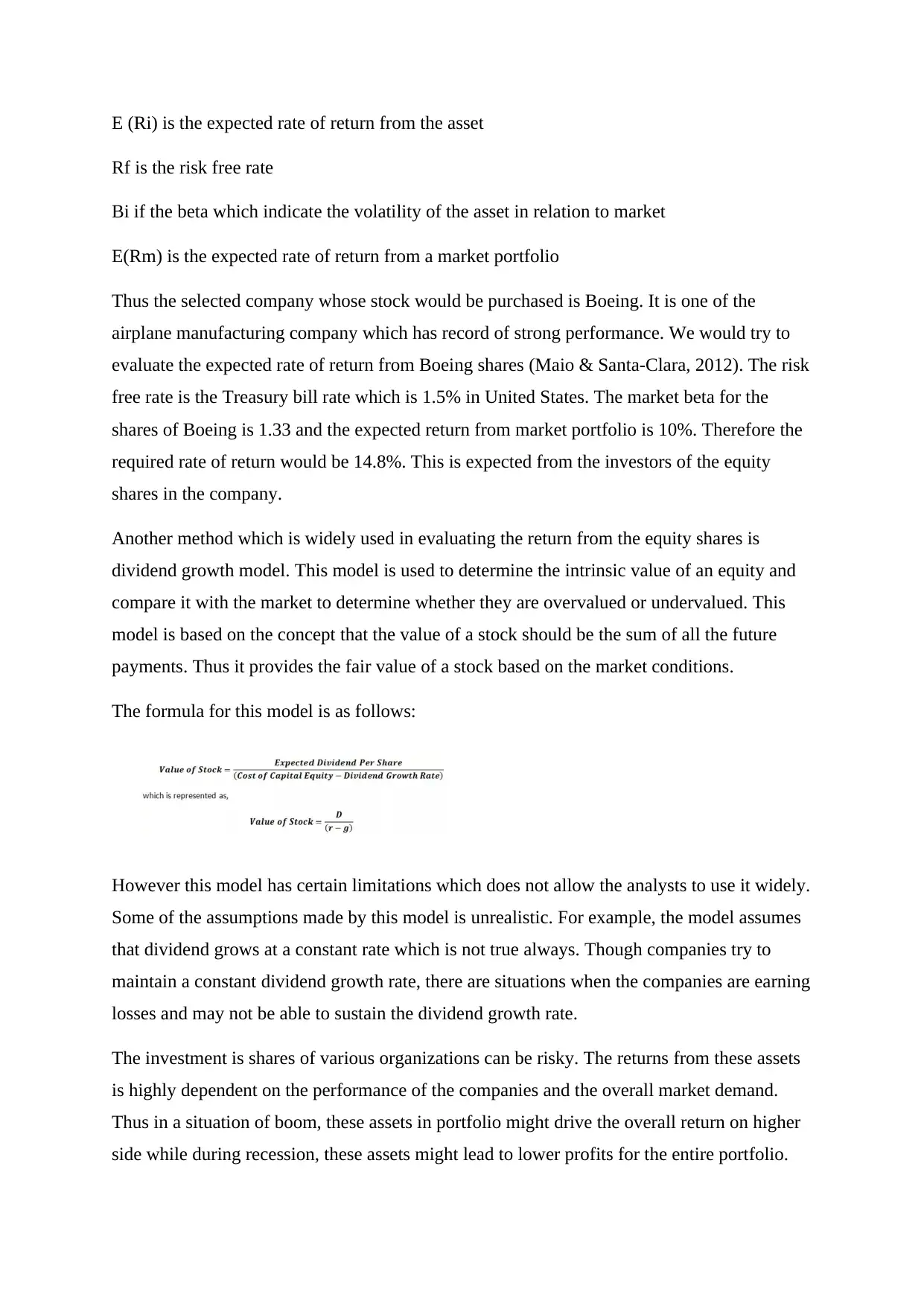

Another method which is widely used in evaluating the return from the equity shares is

dividend growth model. This model is used to determine the intrinsic value of an equity and

compare it with the market to determine whether they are overvalued or undervalued. This

model is based on the concept that the value of a stock should be the sum of all the future

payments. Thus it provides the fair value of a stock based on the market conditions.

The formula for this model is as follows:

However this model has certain limitations which does not allow the analysts to use it widely.

Some of the assumptions made by this model is unrealistic. For example, the model assumes

that dividend grows at a constant rate which is not true always. Though companies try to

maintain a constant dividend growth rate, there are situations when the companies are earning

losses and may not be able to sustain the dividend growth rate.

The investment is shares of various organizations can be risky. The returns from these assets

is highly dependent on the performance of the companies and the overall market demand.

Thus in a situation of boom, these assets in portfolio might drive the overall return on higher

side while during recession, these assets might lead to lower profits for the entire portfolio.

Rf is the risk free rate

Bi if the beta which indicate the volatility of the asset in relation to market

E(Rm) is the expected rate of return from a market portfolio

Thus the selected company whose stock would be purchased is Boeing. It is one of the

airplane manufacturing company which has record of strong performance. We would try to

evaluate the expected rate of return from Boeing shares (Maio & Santa-Clara, 2012). The risk

free rate is the Treasury bill rate which is 1.5% in United States. The market beta for the

shares of Boeing is 1.33 and the expected return from market portfolio is 10%. Therefore the

required rate of return would be 14.8%. This is expected from the investors of the equity

shares in the company.

Another method which is widely used in evaluating the return from the equity shares is

dividend growth model. This model is used to determine the intrinsic value of an equity and

compare it with the market to determine whether they are overvalued or undervalued. This

model is based on the concept that the value of a stock should be the sum of all the future

payments. Thus it provides the fair value of a stock based on the market conditions.

The formula for this model is as follows:

However this model has certain limitations which does not allow the analysts to use it widely.

Some of the assumptions made by this model is unrealistic. For example, the model assumes

that dividend grows at a constant rate which is not true always. Though companies try to

maintain a constant dividend growth rate, there are situations when the companies are earning

losses and may not be able to sustain the dividend growth rate.

The investment is shares of various organizations can be risky. The returns from these assets

is highly dependent on the performance of the companies and the overall market demand.

Thus in a situation of boom, these assets in portfolio might drive the overall return on higher

side while during recession, these assets might lead to lower profits for the entire portfolio.

Hence their allocation is one of the concern areas and should be continuously to make any

strategic changes in the investment.

Strategic actions for the reduction in portfolio risks

Any investment portfolio is basically exposed to five different types of risks which are as

follows:

Allocation risks- These risks relate with the risk and return profile of an investor

choosing to invest in such assets. Thus the risk taking capability of the investors

should be matched with the riskiness of the asset.

Political risks- Political risks relate with the political instability in the country which

affects the return of various asset classes (Muralidhar, 2014).

Business risks- These risks relate with the business management risk of an

organization. Thus there can be changes in the external and internal working

environment which affects the performance of the company.

Call risks- These risks relate to a situation when the issuing company pays back the

debt before the maturity date.

Dividend risks- These risks arises when an organization decide to reduce the dividend

paid on share in some years.

Thus for an investor looking forward to build a portfolio, must analyse these external factors

which might affects the profitability and return from such assets.

Conclusion

Based on the above analysis of various investment options which can help reduce the overall

risk of the portfolio, selecting the appropriate investment which matches the risk and return

profile is a challenge. The amount of investment in each category of asset should be directly

proportional to the expected returns from those assets and the associated risks. A well-

diversified portfolio is one which helps an investor with reducing the overall risk it faces by

holding the individual assets.

The above presented analysis of a hypothetical portfolio evaluates the methods used for

determine the returns and their dependency on various market factors. Apart from the

inherent risk of each of the assets, they are subjected to various external environmental factor

like political, legal, social, economic environment for meeting the expected returns

(Vermorken, Medda & Schröder, 2012).

strategic changes in the investment.

Strategic actions for the reduction in portfolio risks

Any investment portfolio is basically exposed to five different types of risks which are as

follows:

Allocation risks- These risks relate with the risk and return profile of an investor

choosing to invest in such assets. Thus the risk taking capability of the investors

should be matched with the riskiness of the asset.

Political risks- Political risks relate with the political instability in the country which

affects the return of various asset classes (Muralidhar, 2014).

Business risks- These risks relate with the business management risk of an

organization. Thus there can be changes in the external and internal working

environment which affects the performance of the company.

Call risks- These risks relate to a situation when the issuing company pays back the

debt before the maturity date.

Dividend risks- These risks arises when an organization decide to reduce the dividend

paid on share in some years.

Thus for an investor looking forward to build a portfolio, must analyse these external factors

which might affects the profitability and return from such assets.

Conclusion

Based on the above analysis of various investment options which can help reduce the overall

risk of the portfolio, selecting the appropriate investment which matches the risk and return

profile is a challenge. The amount of investment in each category of asset should be directly

proportional to the expected returns from those assets and the associated risks. A well-

diversified portfolio is one which helps an investor with reducing the overall risk it faces by

holding the individual assets.

The above presented analysis of a hypothetical portfolio evaluates the methods used for

determine the returns and their dependency on various market factors. Apart from the

inherent risk of each of the assets, they are subjected to various external environmental factor

like political, legal, social, economic environment for meeting the expected returns

(Vermorken, Medda & Schröder, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

However proper allocation and planning is required for this portfolio to be successful.

Depending upon the situations of the market, some changes may be required in allocation in

order to achieve the desired return from the portfolio.

Depending upon the situations of the market, some changes may be required in allocation in

order to achieve the desired return from the portfolio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Awoga, O. (2011). Fair Valuation of Illiquid Assets. SSRN Electronic Journal. doi:

10.2139/ssrn.3048471

Berkman, H. (2012). The Capital Asset Pricing Model: A Revolutionary Idea in

Finance!. Abacus, 49, 32-35. doi: 10.1111/j.1467-6281.2012.00381.x

Bukhvalova, B. (2013). Portfolio Monitoring Costs, Mutual Fund Fees and Portfolio

Diversification. SSRN Electronic Journal. doi: 10.2139/ssrn.2348475

Jones, C. (2017). Modern Portfolio Theory, Digital Portfolio Theory and Intertemporal

Portfolio Choice. SSRN Electronic Journal. doi: 10.2139/ssrn.2956060

Julianto, L. (2013). Comparative Study between Capital Asset Pricing Model and Arbitrage

Pricing Theory in Indonesian Capital Market during Period 2008-2012. Asia Pacific

Management And Business Application, 2(2), 111-119. doi:

10.21776/ub.apmba.2013.002.02.3

Maio, P., & Santa-Clara, P. (2012). Dividend Yields, Dividend Growth, and Return

Predictability in the Cross-Section of Stocks. SSRN Electronic Journal. doi:

10.2139/ssrn.2158406

Muralidhar, A. (2014). Modern Prospect Theory: The Missing Link Between Modern

Portfolio Theory and Prospect Theory. SSRN Electronic Journal. doi:

10.2139/ssrn.2492603

Vermorken, M., Medda, F., & Schröder, T. (2012). The Diversification Delta: A Higher-

Moment Measure for Portfolio Diversification. The Journal Of Portfolio

Management, 39(1), 67-74. doi: 10.3905/jpm.2012.39.1.067

Awoga, O. (2011). Fair Valuation of Illiquid Assets. SSRN Electronic Journal. doi:

10.2139/ssrn.3048471

Berkman, H. (2012). The Capital Asset Pricing Model: A Revolutionary Idea in

Finance!. Abacus, 49, 32-35. doi: 10.1111/j.1467-6281.2012.00381.x

Bukhvalova, B. (2013). Portfolio Monitoring Costs, Mutual Fund Fees and Portfolio

Diversification. SSRN Electronic Journal. doi: 10.2139/ssrn.2348475

Jones, C. (2017). Modern Portfolio Theory, Digital Portfolio Theory and Intertemporal

Portfolio Choice. SSRN Electronic Journal. doi: 10.2139/ssrn.2956060

Julianto, L. (2013). Comparative Study between Capital Asset Pricing Model and Arbitrage

Pricing Theory in Indonesian Capital Market during Period 2008-2012. Asia Pacific

Management And Business Application, 2(2), 111-119. doi:

10.21776/ub.apmba.2013.002.02.3

Maio, P., & Santa-Clara, P. (2012). Dividend Yields, Dividend Growth, and Return

Predictability in the Cross-Section of Stocks. SSRN Electronic Journal. doi:

10.2139/ssrn.2158406

Muralidhar, A. (2014). Modern Prospect Theory: The Missing Link Between Modern

Portfolio Theory and Prospect Theory. SSRN Electronic Journal. doi:

10.2139/ssrn.2492603

Vermorken, M., Medda, F., & Schröder, T. (2012). The Diversification Delta: A Higher-

Moment Measure for Portfolio Diversification. The Journal Of Portfolio

Management, 39(1), 67-74. doi: 10.3905/jpm.2012.39.1.067

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.