University of Derby: Financial Markets Portfolio Analysis Report

VerifiedAdded on 2021/04/16

|11

|2172

|86

Report

AI Summary

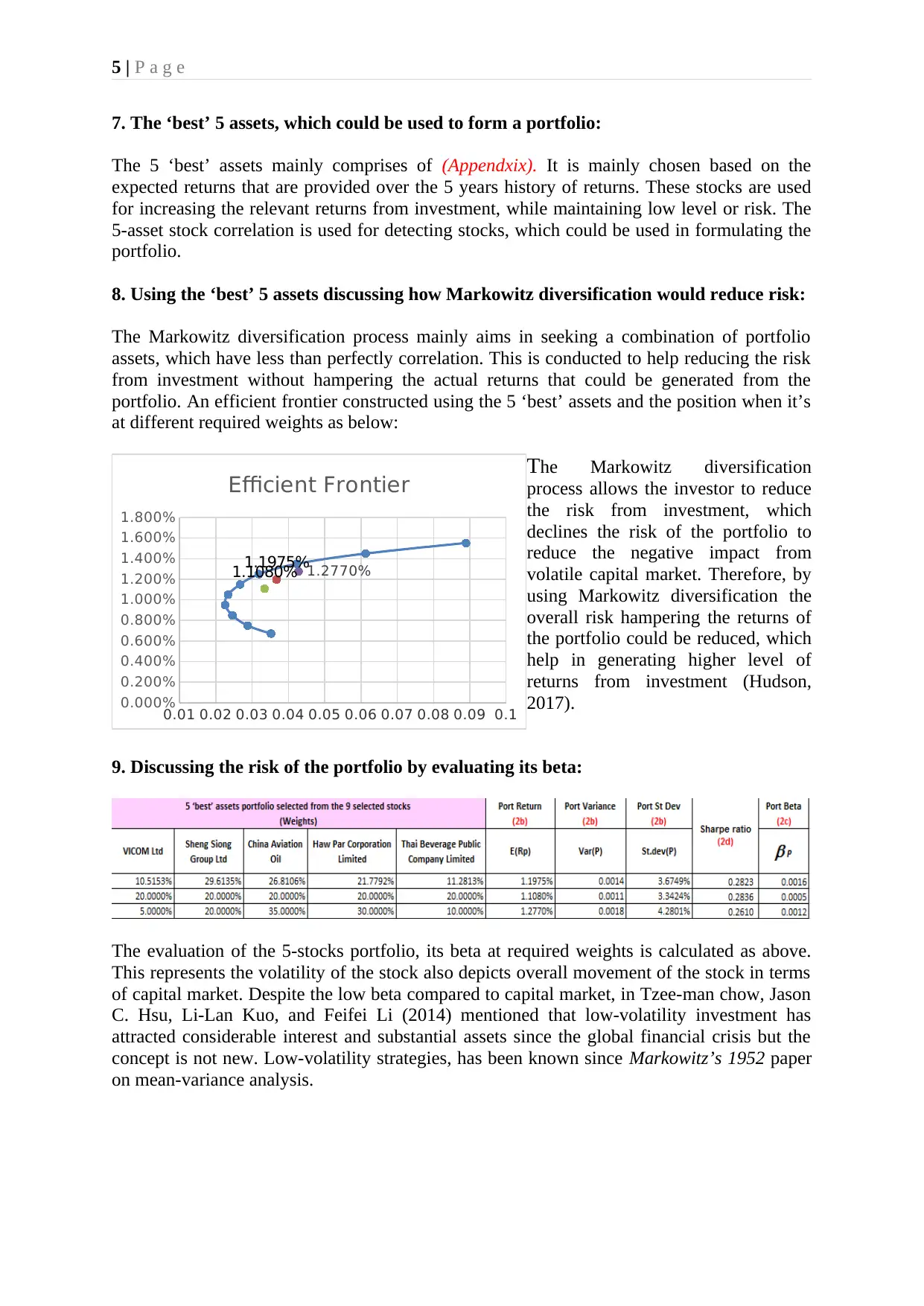

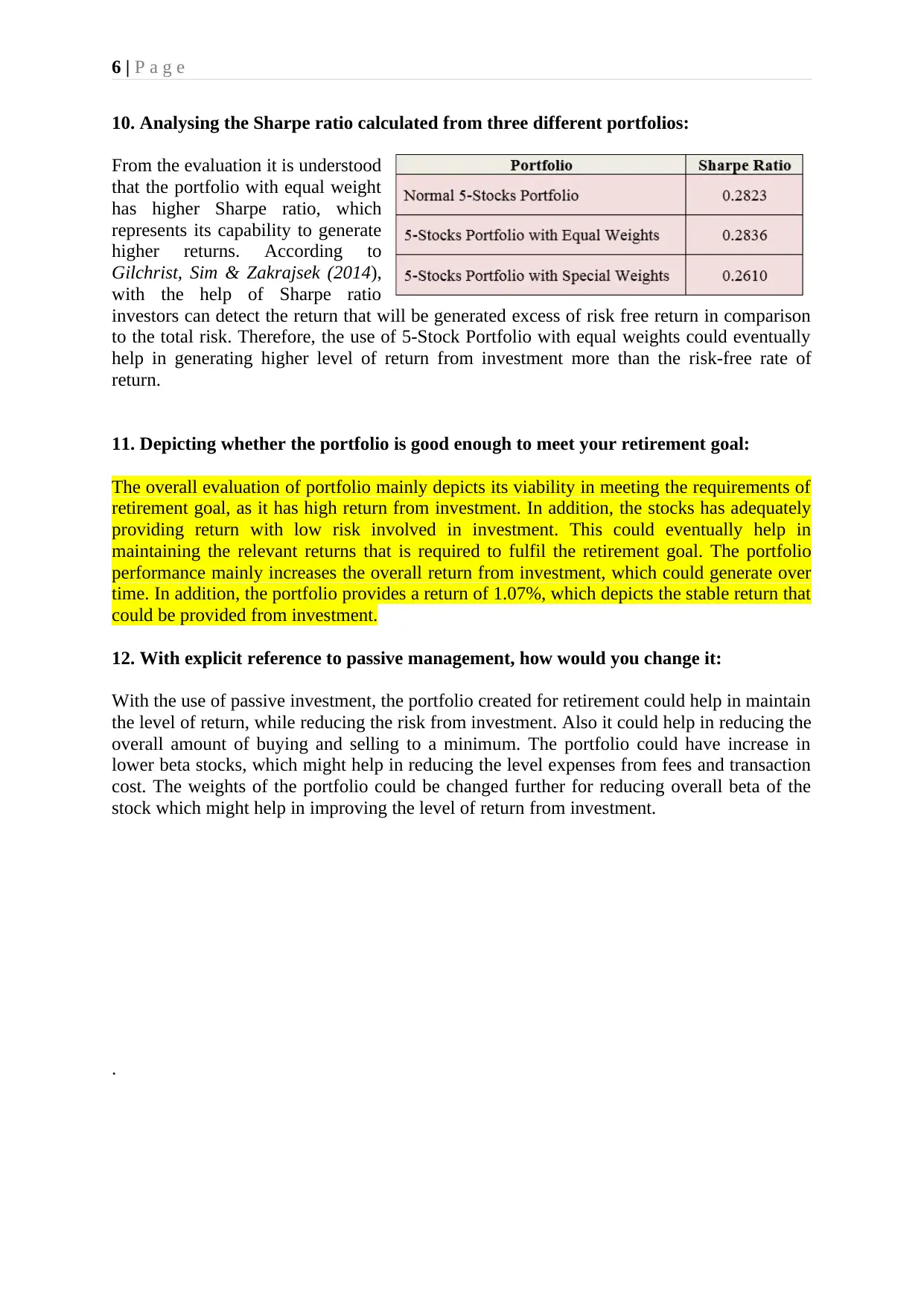

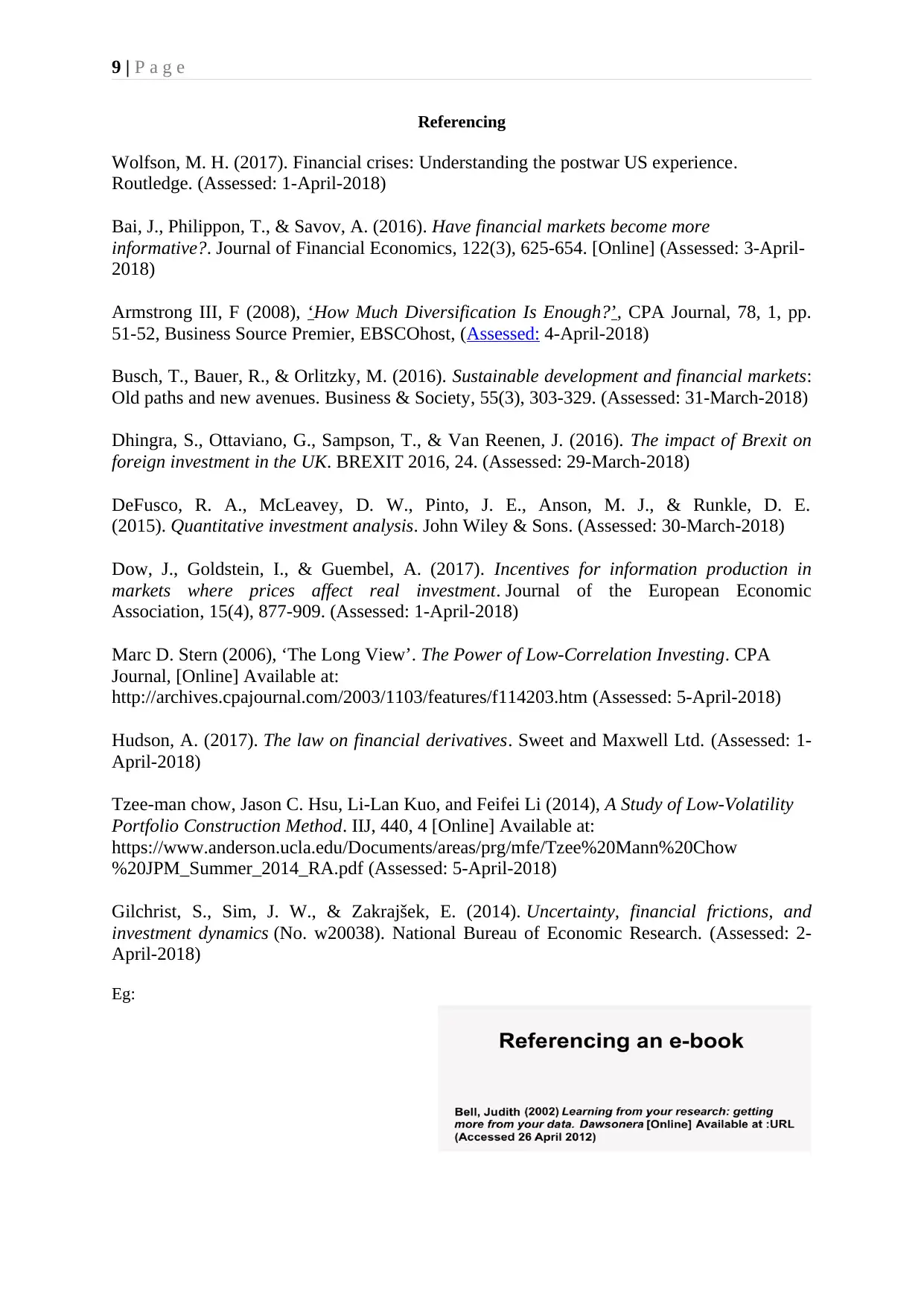

This report presents a detailed analysis of an investment portfolio, created for retirement purposes, focusing on risk minimization and return maximization. The analysis begins with a behavioral perspective on stock selection, emphasizing the choice of low-risk stocks like Wilmar International and Singapore Telecommunications. It then employs portfolio theory to determine asset allocation and mean-variance analysis. The report examines the diversification of an initial nine-asset portfolio across various sectors and evaluates its performance over the investment period, including the correlation between assets and the identification of the 'best' five assets. The Markowitz diversification process is discussed in terms of reducing risk, and the portfolio's beta and Sharpe ratio are analyzed. The report concludes by assessing the portfolio's suitability for meeting retirement goals and suggesting changes using passive management strategies. The analysis includes references to academic literature and financial concepts.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.