MIS775: Investment Portfolio Optimisation with Decision Models

VerifiedAdded on 2022/09/22

|19

|803

|25

Project

AI Summary

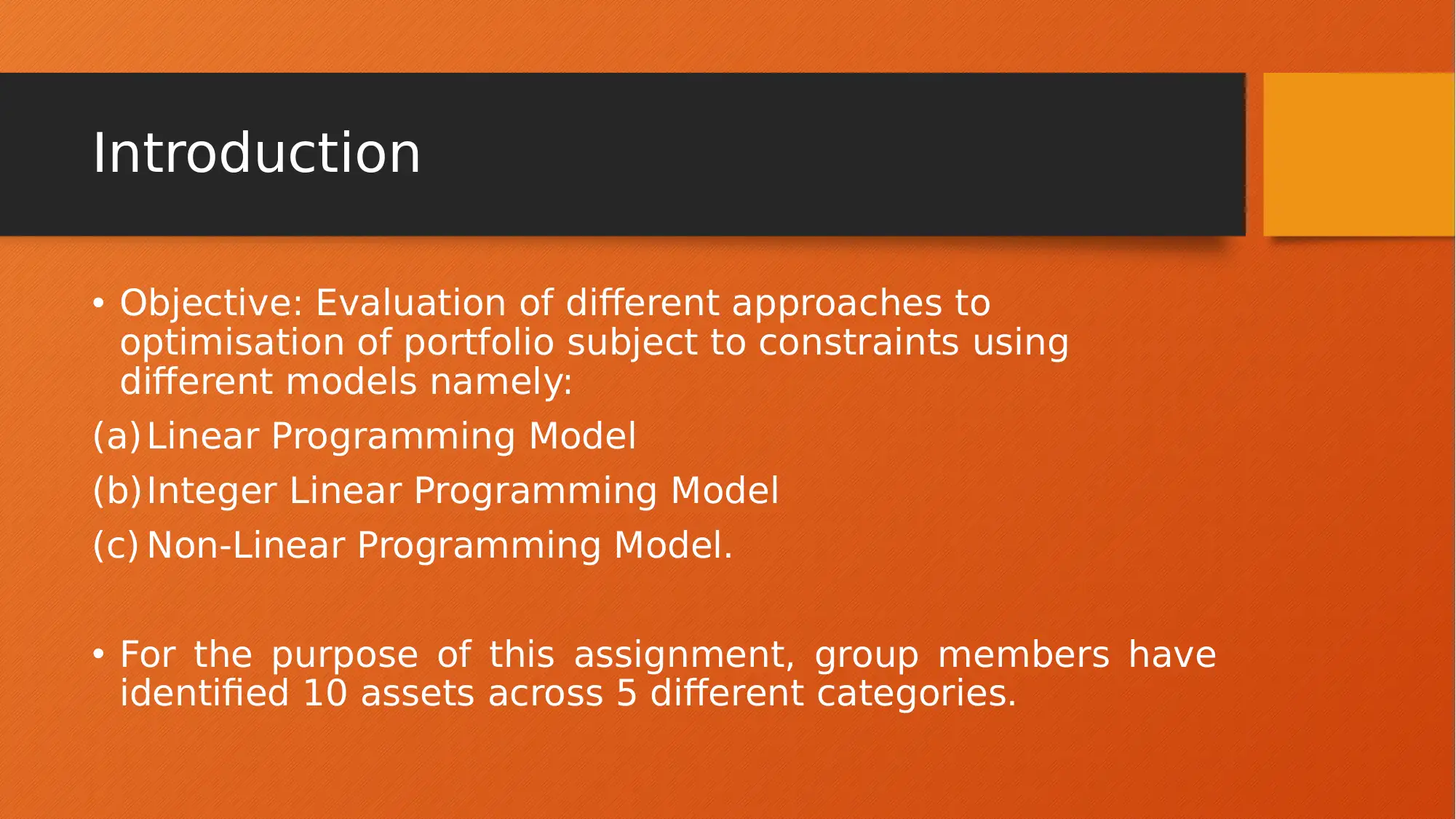

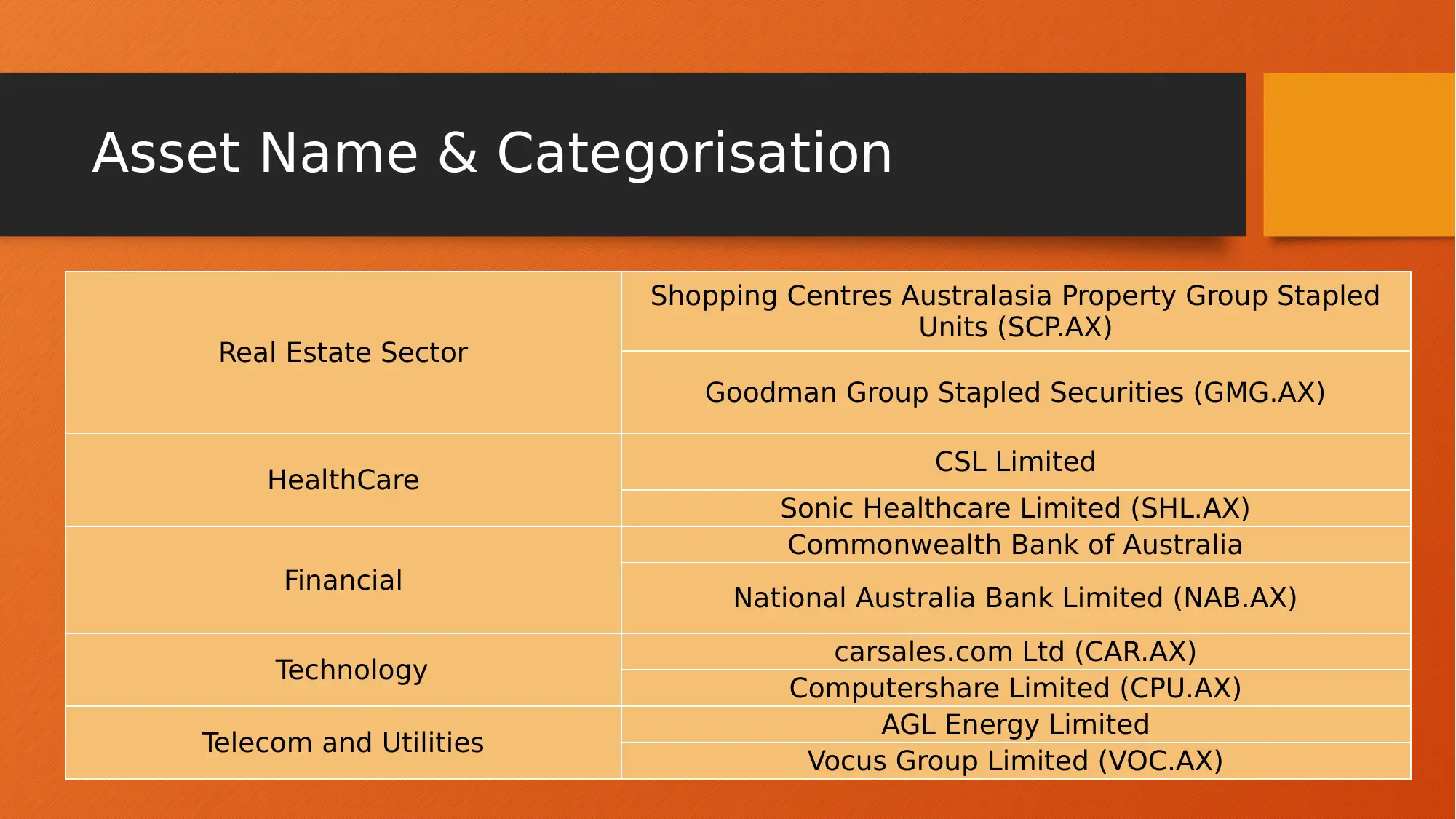

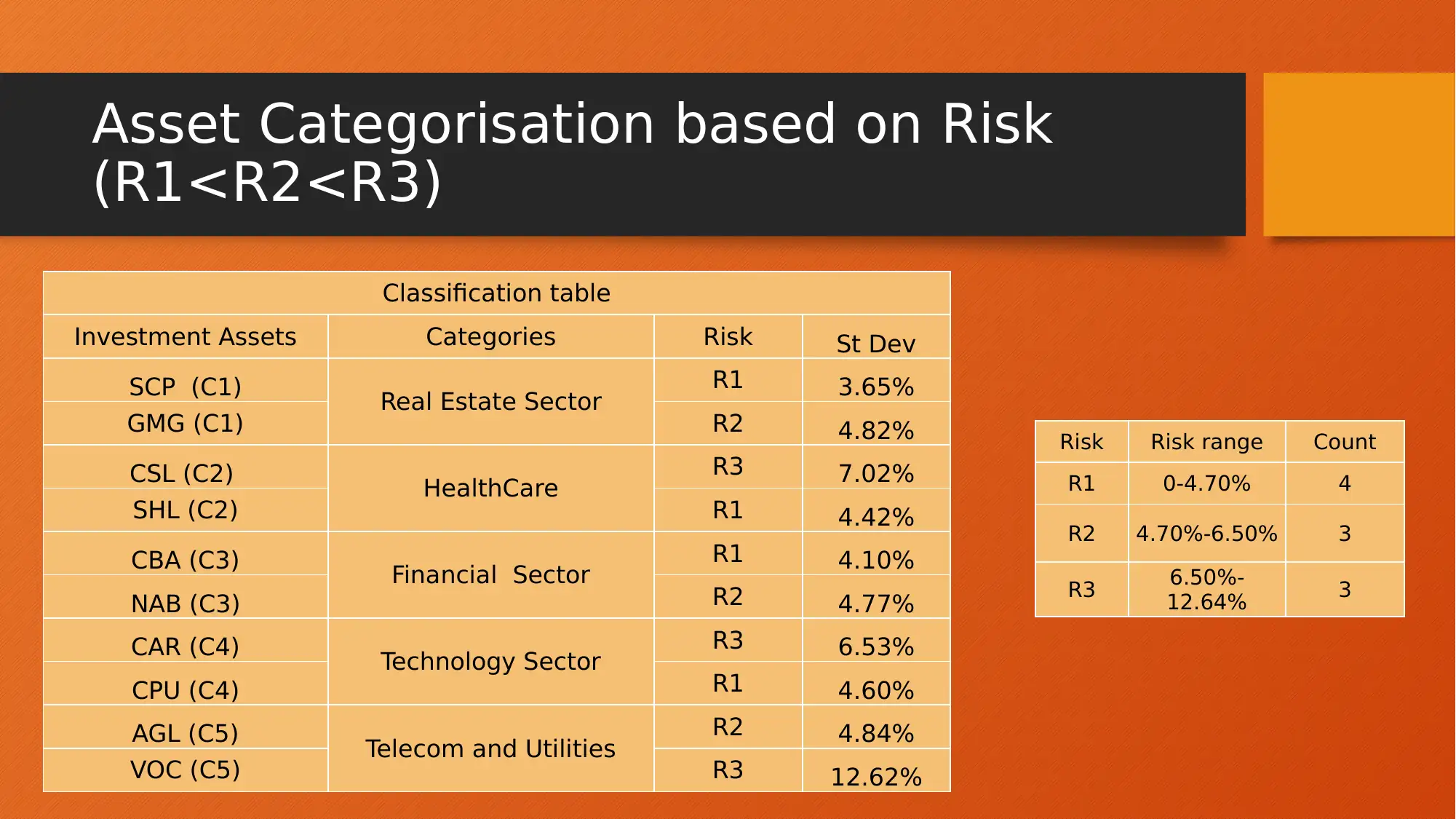

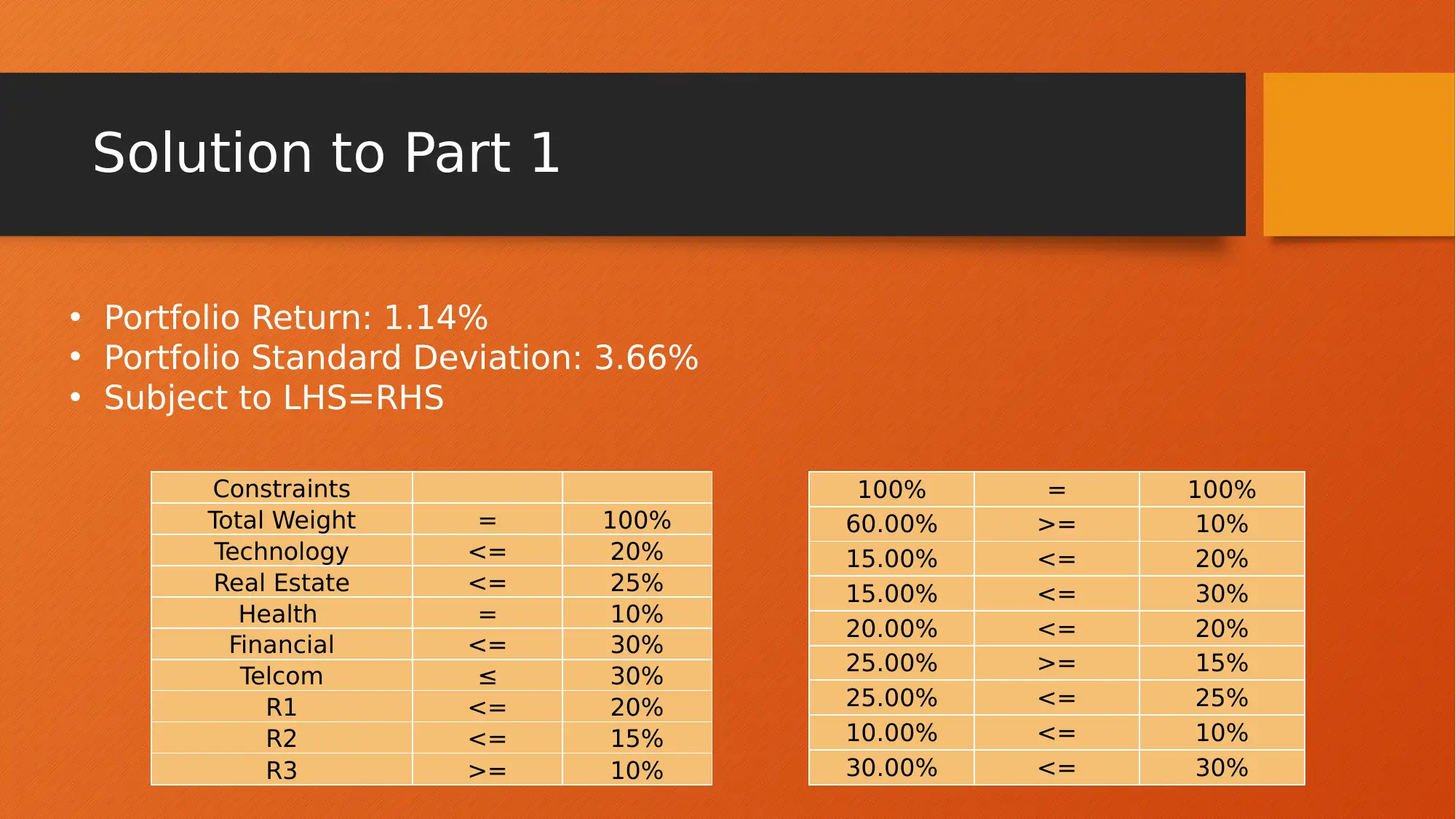

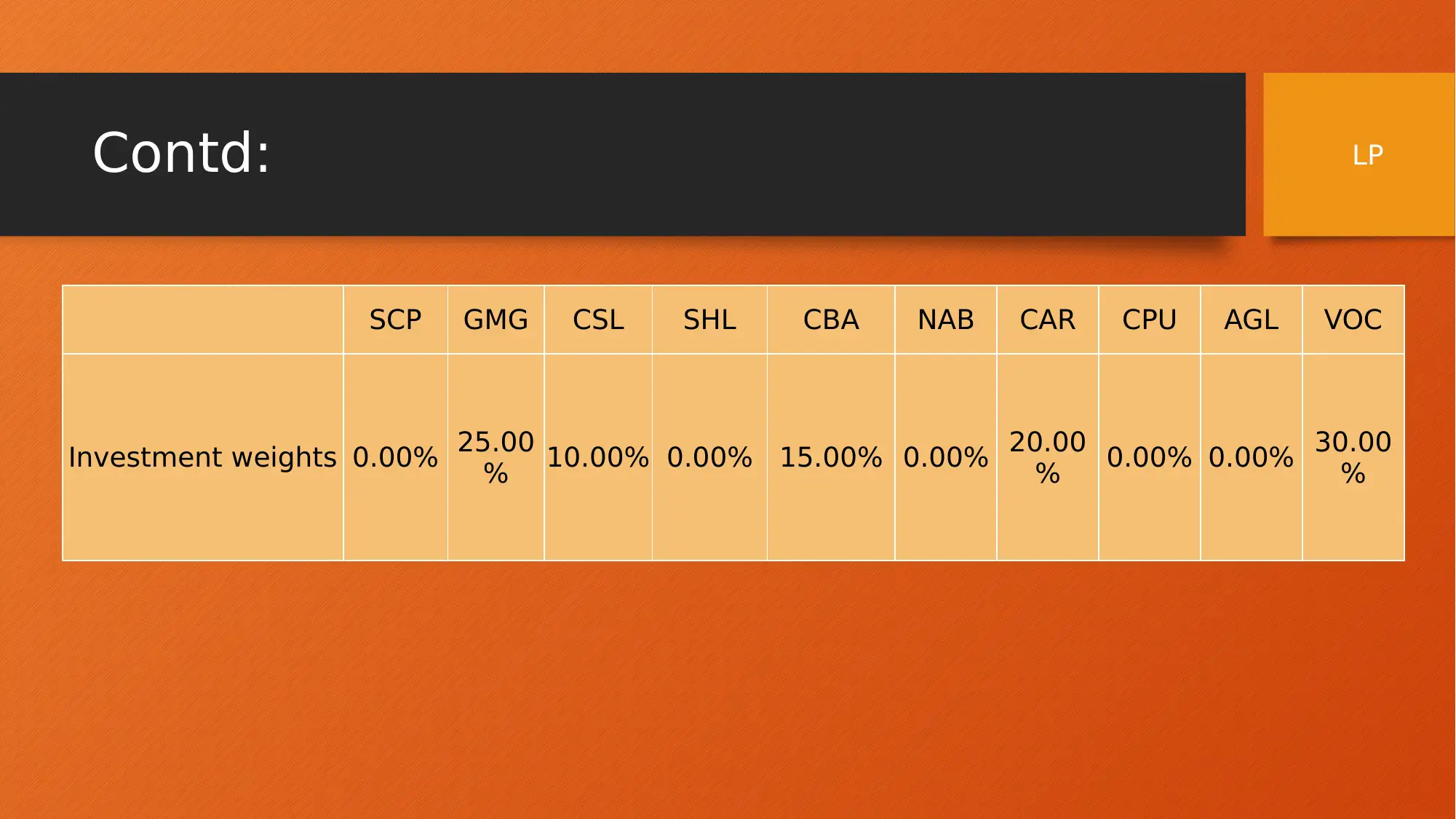

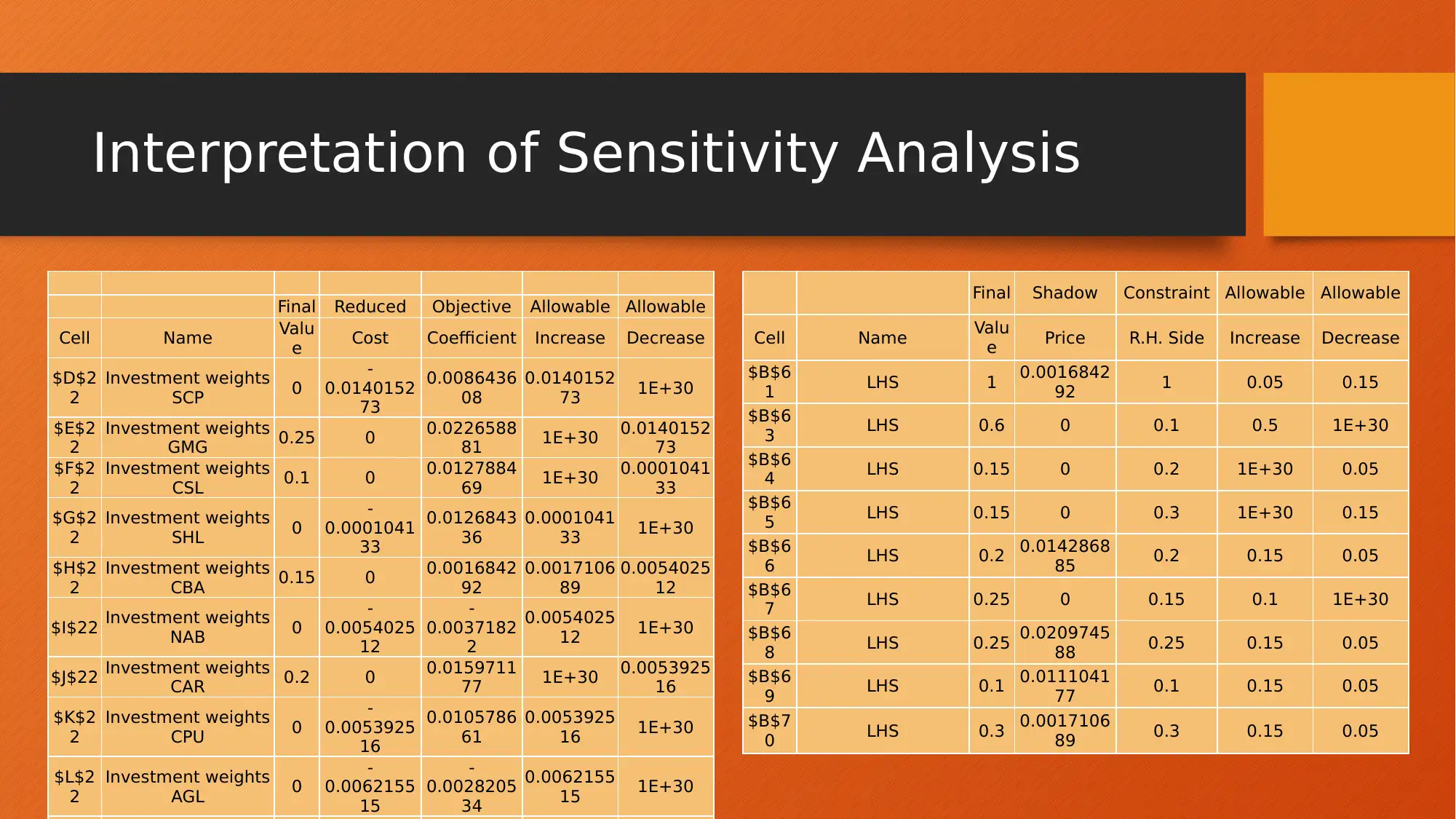

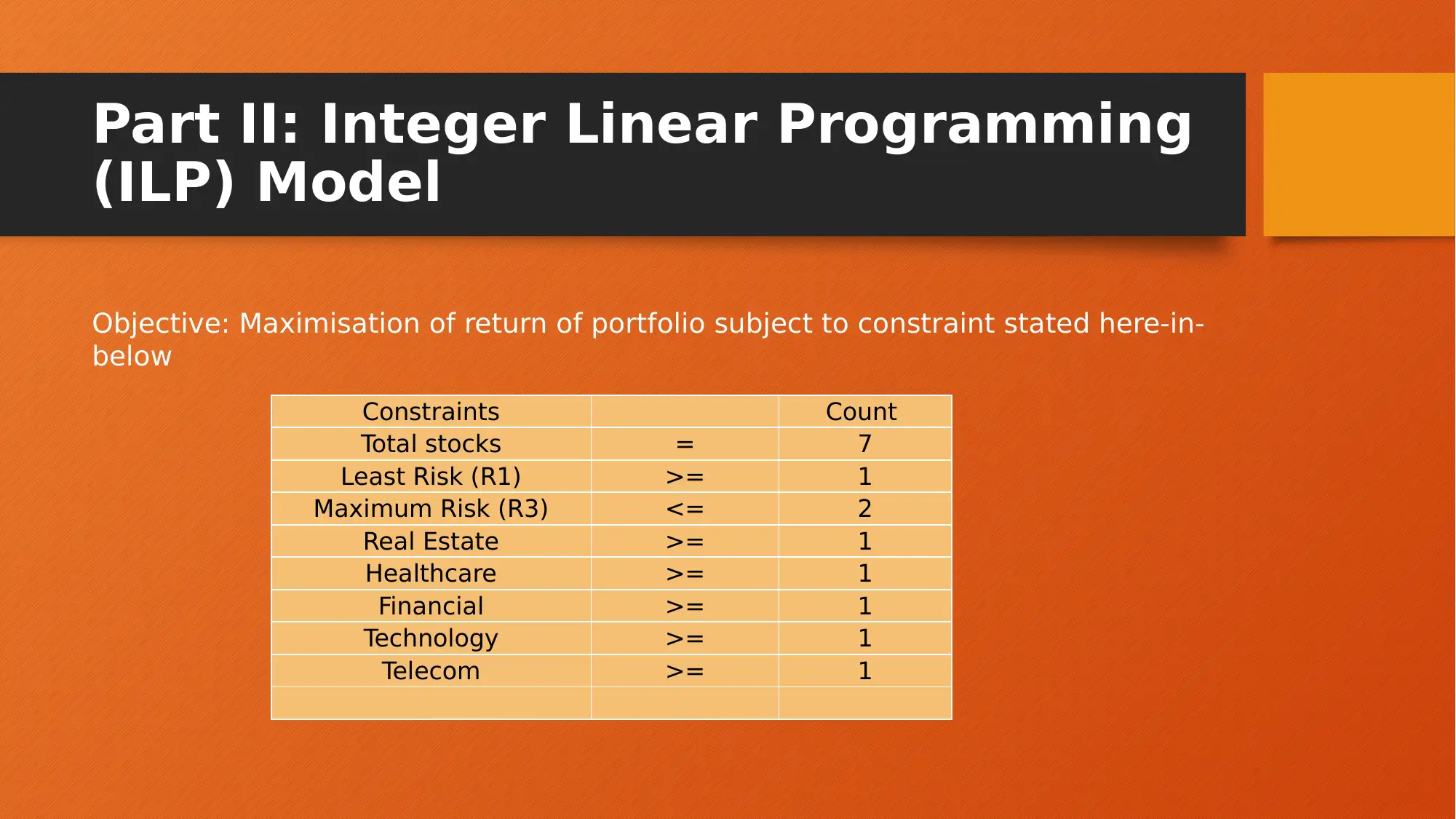

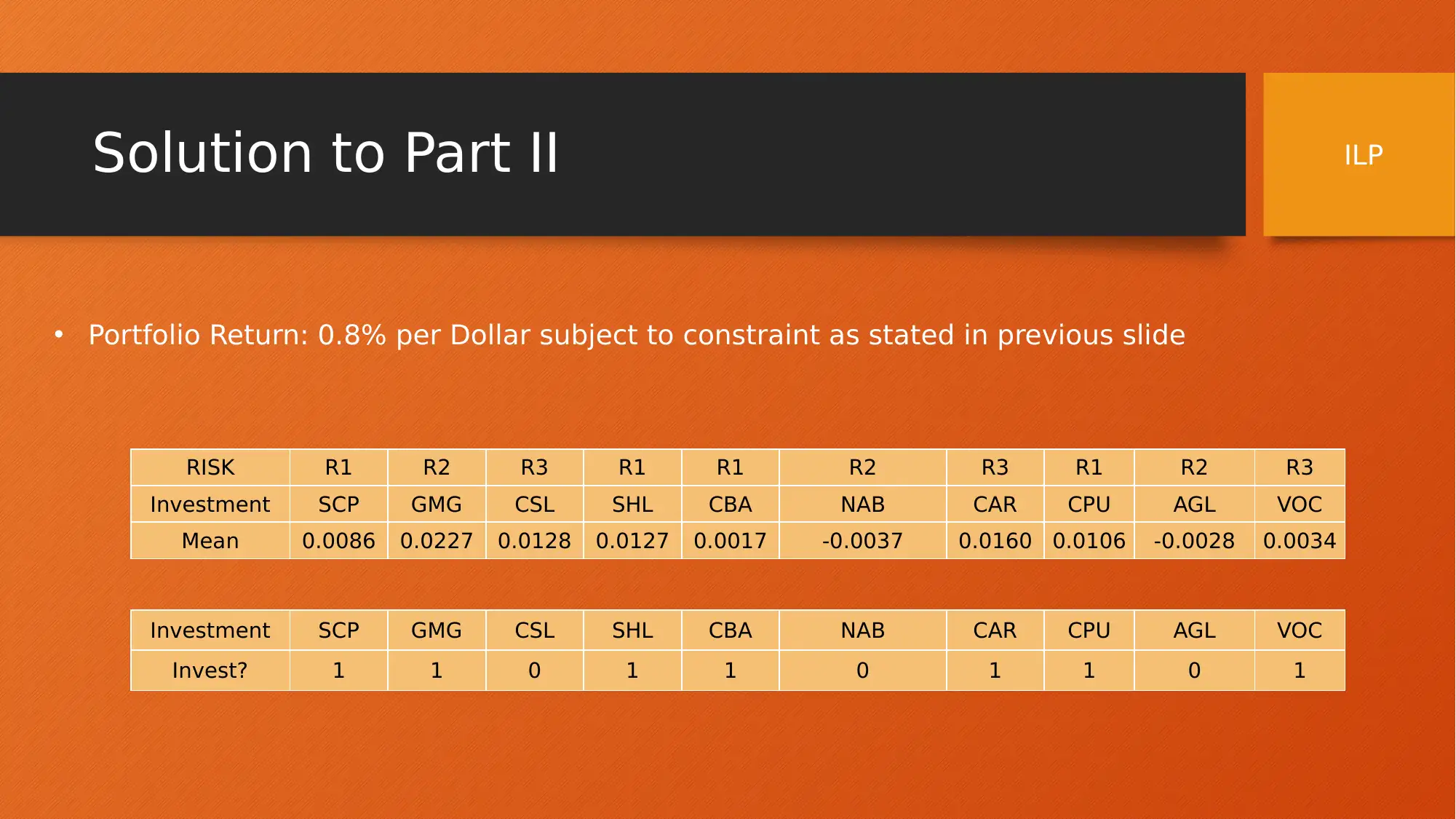

This project report presents an analysis of investment portfolio optimisation using three different modelling approaches: Linear Programming (LP), Integer Linear Programming (ILP), and Non-Linear Programming (NLP). The analysis is conducted using financial data of 10 assets across five different categories, with data collected over a period of 37 months, and the objective is to maximize portfolio return. The report details the formulation of each model, including objective functions and constraints, and presents the results obtained from each model, including portfolio returns, standard deviations, and asset weights. The LP model provides insights through sensitivity analysis. The NLP model explores different objectives, such as maximizing return with risk constraints and maximizing utility with various risk aversion parameters (r). The report concludes with a comparison of the models, highlighting the NLP B model as the most optimized portfolio, offering the highest return for a given risk level and recommending a strategy of fixed return with minimum risk.

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.