Investment and Portfolio Management: Fama-French Model Analysis

VerifiedAdded on 2021/04/21

|12

|2987

|54

Project

AI Summary

This project analyzes investment and portfolio management, focusing on the Fama-French model. Part A examines the model's findings, factors influencing stock returns, risk measures, implications of the CAPM and Fama-French models, and summarizes an academic paper on the subject. Part B involves calculating the expected return and standard deviation for minimum-variance and optimal risky portfolios, along with related financial metrics. The analysis includes detailed calculations of portfolio weights, expected returns, standard deviations, and Sharpe ratios, providing a comprehensive overview of portfolio construction and risk management. The project utilizes financial data and formulas to evaluate investment strategies and risk-return trade-offs, showcasing the practical application of financial models.

Running head: INVESTMENT AND PORTFOLIO MANAGEMENT

Investment and Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Investment and Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT AND PORTFOLIO MANAGEMENT

1

Table of Contents

PART A:.....................................................................................................................................2

1. Stating the finding on investment:.........................................................................................2

2. Stating the factors examined by Fama-French that might explain stock returns:..................2

3. Stating the measure of risk implemented by Fama-French model for the investors:.............3

4. Describing the implications of CAPM model and Fama-French model on investors:..........3

5. Providing summary of the academic paper and the reason Fama-French model was used in

the paper:....................................................................................................................................4

PART B:.....................................................................................................................................7

a) Depicting the expected return and standard deviation of the minimum-variance portfolio:. 7

b) Depicting the expected return and standard deviation of optimal risky portfolio:................9

c.i) Calculating standard derivation of the portfolio:...............................................................10

c.ii) Calculating the portion of T-bill fund and each of the two risky funds:..........................11

Reference and Bibliography:....................................................................................................12

1

Table of Contents

PART A:.....................................................................................................................................2

1. Stating the finding on investment:.........................................................................................2

2. Stating the factors examined by Fama-French that might explain stock returns:..................2

3. Stating the measure of risk implemented by Fama-French model for the investors:.............3

4. Describing the implications of CAPM model and Fama-French model on investors:..........3

5. Providing summary of the academic paper and the reason Fama-French model was used in

the paper:....................................................................................................................................4

PART B:.....................................................................................................................................7

a) Depicting the expected return and standard deviation of the minimum-variance portfolio:. 7

b) Depicting the expected return and standard deviation of optimal risky portfolio:................9

c.i) Calculating standard derivation of the portfolio:...............................................................10

c.ii) Calculating the portion of T-bill fund and each of the two risky funds:..........................11

Reference and Bibliography:....................................................................................................12

INVESTMENT AND PORTFOLIO MANAGEMENT

2

PART A:

1. Stating the finding on investment:

The researcher in the article mainly indicates the performance of value stock in

accordance with growth stocks. The researcher highlighted the misgivings in growth stock

and benefits provided by value stocks. In addition, the researcher pointed out the investors in

expectation of higher return from growth stock increase its value, which does not occur at

last. The researcher has conducted relevant evaluation and detect the validity of capital asset

pricing model. Moreover, the financial performance of the companies consists of growth

stock do not provide all the relevant return to the shareholder. On the other hand, the

researcher pointed out the value stock being undervalued can provide high return from

investment to the investors. The researcher also pointed out the financial performance of

value stock were more than growth stocks, as founded in US Stocks (Chandra 2017).

2. Stating the factors examined by Fama-French that might explain stock returns:

Fama-French states relevant factors for analysing the overall financial performance of

the company and detect overall growth, which could increase return from investment.

Moreover, Fama-French mainly states that two factors are needed for analysing the overall

average return of the stocks. The factors are market risk factors and value growth risk factor,

which is indicated by Fama-French that the use of both the factors could help in detecting the

actual returns from investment. The identified factors might help in detecting the actual

returns of the company, which might allow the investor to identify stock with least returns.

The value growth factors are mainly detected by differentiating between international

portfolio of high book-to-market stock and the return provided by portfolios with low book-

to-market stocks. In this context, Pagdin and Hardy (2017) mentioned that Fama-French

2

PART A:

1. Stating the finding on investment:

The researcher in the article mainly indicates the performance of value stock in

accordance with growth stocks. The researcher highlighted the misgivings in growth stock

and benefits provided by value stocks. In addition, the researcher pointed out the investors in

expectation of higher return from growth stock increase its value, which does not occur at

last. The researcher has conducted relevant evaluation and detect the validity of capital asset

pricing model. Moreover, the financial performance of the companies consists of growth

stock do not provide all the relevant return to the shareholder. On the other hand, the

researcher pointed out the value stock being undervalued can provide high return from

investment to the investors. The researcher also pointed out the financial performance of

value stock were more than growth stocks, as founded in US Stocks (Chandra 2017).

2. Stating the factors examined by Fama-French that might explain stock returns:

Fama-French states relevant factors for analysing the overall financial performance of

the company and detect overall growth, which could increase return from investment.

Moreover, Fama-French mainly states that two factors are needed for analysing the overall

average return of the stocks. The factors are market risk factors and value growth risk factor,

which is indicated by Fama-French that the use of both the factors could help in detecting the

actual returns from investment. The identified factors might help in detecting the actual

returns of the company, which might allow the investor to identify stock with least returns.

The value growth factors are mainly detected by differentiating between international

portfolio of high book-to-market stock and the return provided by portfolios with low book-

to-market stocks. In this context, Pagdin and Hardy (2017) mentioned that Fama-French

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT AND PORTFOLIO MANAGEMENT

3

models is helpful in detecting stock with the low risk, which could help in geniting high level

of return from investment.

3. Stating the measure of risk implemented by Fama-French model for the investors:

The Fama-French model mainly focuses its overall risk measure on two different

forms, which could help in detecting stocks returns and increase profits from investments.

The risk attributes are market risk factor and a value-growth risk factor, which is needed for

analysing the actual risk hindering operational capability of the company. Moreover, CAPM

model mainly focuses on one factor, which does not help in detecting the actual financial

position of the company. Furthermore, the risk implementation of Fama-French might help in

generating high level of profits. The market risk factor helps in evaluating the actual returns

from investment, which could be provided by a stock. In addition, the value-growth factor

would allow investors in detection the actual value of stock and the return it could provide

from investment (Kashyap 2016).

4. Describing the implications of CAPM model and Fama-French model on investors:

CAPM model mainly has relevant implications to the investors, which help in

detecting the risk and return from investment. In addition, the CAPM model helps in

determining the return and risk in stocks. This might help in detecting return and risk

involved in investments of the company, which might allow investors to generate high level

of returns. Raab and Stahn (2017) stated that CAPM model evaluates beta and expected

return of stocks, which is essential to create portfolio with low risk and high returns.

Moreover, the Fama-French model is used in evaluating examine multi-factor models,

which could help in detecting risk that could impact expected return of stock. In addition, the

Fama-French model evaluates two additional dimensions of risk that get rewarded nature of

3

models is helpful in detecting stock with the low risk, which could help in geniting high level

of return from investment.

3. Stating the measure of risk implemented by Fama-French model for the investors:

The Fama-French model mainly focuses its overall risk measure on two different

forms, which could help in detecting stocks returns and increase profits from investments.

The risk attributes are market risk factor and a value-growth risk factor, which is needed for

analysing the actual risk hindering operational capability of the company. Moreover, CAPM

model mainly focuses on one factor, which does not help in detecting the actual financial

position of the company. Furthermore, the risk implementation of Fama-French might help in

generating high level of profits. The market risk factor helps in evaluating the actual returns

from investment, which could be provided by a stock. In addition, the value-growth factor

would allow investors in detection the actual value of stock and the return it could provide

from investment (Kashyap 2016).

4. Describing the implications of CAPM model and Fama-French model on investors:

CAPM model mainly has relevant implications to the investors, which help in

detecting the risk and return from investment. In addition, the CAPM model helps in

determining the return and risk in stocks. This might help in detecting return and risk

involved in investments of the company, which might allow investors to generate high level

of returns. Raab and Stahn (2017) stated that CAPM model evaluates beta and expected

return of stocks, which is essential to create portfolio with low risk and high returns.

Moreover, the Fama-French model is used in evaluating examine multi-factor models,

which could help in detecting risk that could impact expected return of stock. In addition, the

Fama-French model evaluates two additional dimensions of risk that get rewarded nature of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT AND PORTFOLIO MANAGEMENT

4

returns. The second implications are that value stock have higher returns than growth stock in

the market all around the world. Moreover, the earnings-to-price, cash flow-to price and

dividend-to-price is evaluated for detecting the actual financial capability of the stock to

generate high returns.

5. Providing summary of the academic paper and the reason Fama-French model was

used in the paper:

The overall academic paper “The Five-Factor Fama-French Model: International

Evidence” writer by Nusret Cakici, states the impact of Fama-French Model in detecting

returns of the stock (Cakici 2015). In addition, the financial market of 23 countries are mainly

evaluated to determine financial performance of the organisation. Moreover, the researcher in

academic paper has effectively depicted the overall use of five-factor model, which could

help in detecting the financial performance of the organisation. Furthermore, the data used

from 23 stock market is evaluated based on Fama-French Model for determining the impact

of extra two factors, whether they add explanatory power or a much weaker in Japan and

Asian portfolios. The research paper mainly evaluates the gross profitability and investment

factors include in Five-Factor Fama-French Model and whether its calculation could help in

understanding the return form investment.

The discussion section of the academic paper in panel A that mainly indicates the

intercepts from the Fama-French three-factor regressions for the 25 size-book-to-market

portfolios. In addition, the panel B section provides intercepts from the Fama-French five-

factor regressions, and their t-statistics. Both the analysis part might help in detecting the

financial viability of Fama-French three-factor and Fama-French five-factor. The regression

analysis mainly helps in detecting that lower number of significant alphas, which could help

in detecting performance of the model. The results of the regression analysis mainly help in

4

returns. The second implications are that value stock have higher returns than growth stock in

the market all around the world. Moreover, the earnings-to-price, cash flow-to price and

dividend-to-price is evaluated for detecting the actual financial capability of the stock to

generate high returns.

5. Providing summary of the academic paper and the reason Fama-French model was

used in the paper:

The overall academic paper “The Five-Factor Fama-French Model: International

Evidence” writer by Nusret Cakici, states the impact of Fama-French Model in detecting

returns of the stock (Cakici 2015). In addition, the financial market of 23 countries are mainly

evaluated to determine financial performance of the organisation. Moreover, the researcher in

academic paper has effectively depicted the overall use of five-factor model, which could

help in detecting the financial performance of the organisation. Furthermore, the data used

from 23 stock market is evaluated based on Fama-French Model for determining the impact

of extra two factors, whether they add explanatory power or a much weaker in Japan and

Asian portfolios. The research paper mainly evaluates the gross profitability and investment

factors include in Five-Factor Fama-French Model and whether its calculation could help in

understanding the return form investment.

The discussion section of the academic paper in panel A that mainly indicates the

intercepts from the Fama-French three-factor regressions for the 25 size-book-to-market

portfolios. In addition, the panel B section provides intercepts from the Fama-French five-

factor regressions, and their t-statistics. Both the analysis part might help in detecting the

financial viability of Fama-French three-factor and Fama-French five-factor. The regression

analysis mainly helps in detecting that lower number of significant alphas, which could help

in detecting performance of the model. The results of the regression analysis mainly help in

INVESTMENT AND PORTFOLIO MANAGEMENT

5

understanding the significance of alphas for the 5-factor model and 3-factor model. This

relatively helps in identifying the financial performance of the company. However, the

academic paper indicates that 5-factor model does not provide adequate measure or better

description of average returns than three-factor model for the portfolios. This relatively

indicates that the three-factor model is sufficient for the analysis of the return provide by the

portfolios (Cakici 2015).

However, from the evaluation it could be detected that five-factor model is considered

doubtful for major of the countries such as Japan and Asia-Pacific. However, the academic

paper also states that three-factor model is much better option for the investors, as it applies

to all the territories of the world and allows investor to detect actual return that will be

provide from investment (Cakici 2015). Moreover, the objective of academic paper is to

detect the impact of gross profitability and investment, as a relevant factor of five-factor

Fame-French model. In addition, the researcher indicates that the new factors do not have any

explanatory power for the stocks listed in Japan and Asia Pacific. The academic paper sheds

light on the five-factor Fame-French model and how it could not provide all the relevant help

to the investor in different reigns of the world.

The researcher focuses on the results obtained from the academic paper, which states

that five-factor Fame-French model perform much better in regional condition in comparison

with the global condition. Furthermore, the academic paper’s outcome indicates that markets

all around the world are not fully integrated, which relatively reduces the impact of five-

factor Fame-French model on different markets all around the world. However, from the

evaluation it could be detected that the five-factor Fame-French model has fairly performed

in US market. The calculation of SMB, HML, RMW, and CMA is conducted in the research

report, which might help in depicting the overall significance of five-factor Fame-French

5

understanding the significance of alphas for the 5-factor model and 3-factor model. This

relatively helps in identifying the financial performance of the company. However, the

academic paper indicates that 5-factor model does not provide adequate measure or better

description of average returns than three-factor model for the portfolios. This relatively

indicates that the three-factor model is sufficient for the analysis of the return provide by the

portfolios (Cakici 2015).

However, from the evaluation it could be detected that five-factor model is considered

doubtful for major of the countries such as Japan and Asia-Pacific. However, the academic

paper also states that three-factor model is much better option for the investors, as it applies

to all the territories of the world and allows investor to detect actual return that will be

provide from investment (Cakici 2015). Moreover, the objective of academic paper is to

detect the impact of gross profitability and investment, as a relevant factor of five-factor

Fame-French model. In addition, the researcher indicates that the new factors do not have any

explanatory power for the stocks listed in Japan and Asia Pacific. The academic paper sheds

light on the five-factor Fame-French model and how it could not provide all the relevant help

to the investor in different reigns of the world.

The researcher focuses on the results obtained from the academic paper, which states

that five-factor Fame-French model perform much better in regional condition in comparison

with the global condition. Furthermore, the academic paper’s outcome indicates that markets

all around the world are not fully integrated, which relatively reduces the impact of five-

factor Fame-French model on different markets all around the world. However, from the

evaluation it could be detected that the five-factor Fame-French model has fairly performed

in US market. The calculation of SMB, HML, RMW, and CMA is conducted in the research

report, which might help in depicting the overall significance of five-factor Fame-French

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT AND PORTFOLIO MANAGEMENT

6

model. The researcher has used T-test, correlation, and other statistical tools for deriving the

relationship between the calculation of different five-factor of Fame-French model.

The result section of the academic paper mainly indicates the correlation between

Global, North America and Europe, which helps in deriving the efficiency and attractiveness

of five-factor Fame-French model in identifying the stock with high value. However, the

result also indicates that correlation between Japan and Asia Pacific are relatively different in

comparison with Global, North America and Europe markets. This relatively indicates the

vulnerability of five-factor Fame-French model in identifying the stock with high value,

which could be used by investors.

Moreover, the academic paper sheds light on the fact that five-factor Fame-French

model is not always the best possible options for evaluation. This derivation is concluded by

evaluating the 25 size-book-to-market portfolios, the 25 size-GP portfolios, and the 25 size-

Investment portfolios, where their applicability is in doubt for other regions of the world. The

researcher indicates that the five-factor Fame-French model is not a viable approach for other

countries or regions of the world, as it would not provide the accurate data for the evaluation.

The result also evaluates the impact of RMW, CMA and HML, which could help investors in

their decision-making process. Moreover, from the valuation it could be detected that RMW

and CMA has smaller magnitude than HML, which might not help in detecting the actual

return capability of the stock.

The results of the research also evaluate the Asset pricing test, which relatively

suggest that Five Factor Model is not an adequate model for investor. According to the Asset

pricing test, GP portfolios, size investment portfolios and size-book-to-market portfolios has

not performed adequately and indicates that they cannot function in other regions of the

world. However, from the valuation it is also indicated that asset pricing test suggest that

6

model. The researcher has used T-test, correlation, and other statistical tools for deriving the

relationship between the calculation of different five-factor of Fame-French model.

The result section of the academic paper mainly indicates the correlation between

Global, North America and Europe, which helps in deriving the efficiency and attractiveness

of five-factor Fame-French model in identifying the stock with high value. However, the

result also indicates that correlation between Japan and Asia Pacific are relatively different in

comparison with Global, North America and Europe markets. This relatively indicates the

vulnerability of five-factor Fame-French model in identifying the stock with high value,

which could be used by investors.

Moreover, the academic paper sheds light on the fact that five-factor Fame-French

model is not always the best possible options for evaluation. This derivation is concluded by

evaluating the 25 size-book-to-market portfolios, the 25 size-GP portfolios, and the 25 size-

Investment portfolios, where their applicability is in doubt for other regions of the world. The

researcher indicates that the five-factor Fame-French model is not a viable approach for other

countries or regions of the world, as it would not provide the accurate data for the evaluation.

The result also evaluates the impact of RMW, CMA and HML, which could help investors in

their decision-making process. Moreover, from the valuation it could be detected that RMW

and CMA has smaller magnitude than HML, which might not help in detecting the actual

return capability of the stock.

The results of the research also evaluate the Asset pricing test, which relatively

suggest that Five Factor Model is not an adequate model for investor. According to the Asset

pricing test, GP portfolios, size investment portfolios and size-book-to-market portfolios has

not performed adequately and indicates that they cannot function in other regions of the

world. However, from the valuation it is also indicated that asset pricing test suggest that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT AND PORTFOLIO MANAGEMENT

7

regional factors always perform better in comparison to the Global factors. this indicates that

the use of Five Factor Fama French model could eventually allow investing to support their

investing me within the regional limits. This would eventually help in improving the return

generation capacity of the investors. The researcher also portrays that the use of Fama French

model could allow investors to support the investing needs nationally, while the problems

might rise during the international investment schemes. Lastly, the academic paper possess

doubt on the applicability of Five Factor Model in performing adequately all around the

world. The research also states that viability of the model falls when investing in the markets

of Japan and Asia Pacific. This relatively limits the capability of Five Factor Model in

supporting investors during their investment schemes.

PART B:

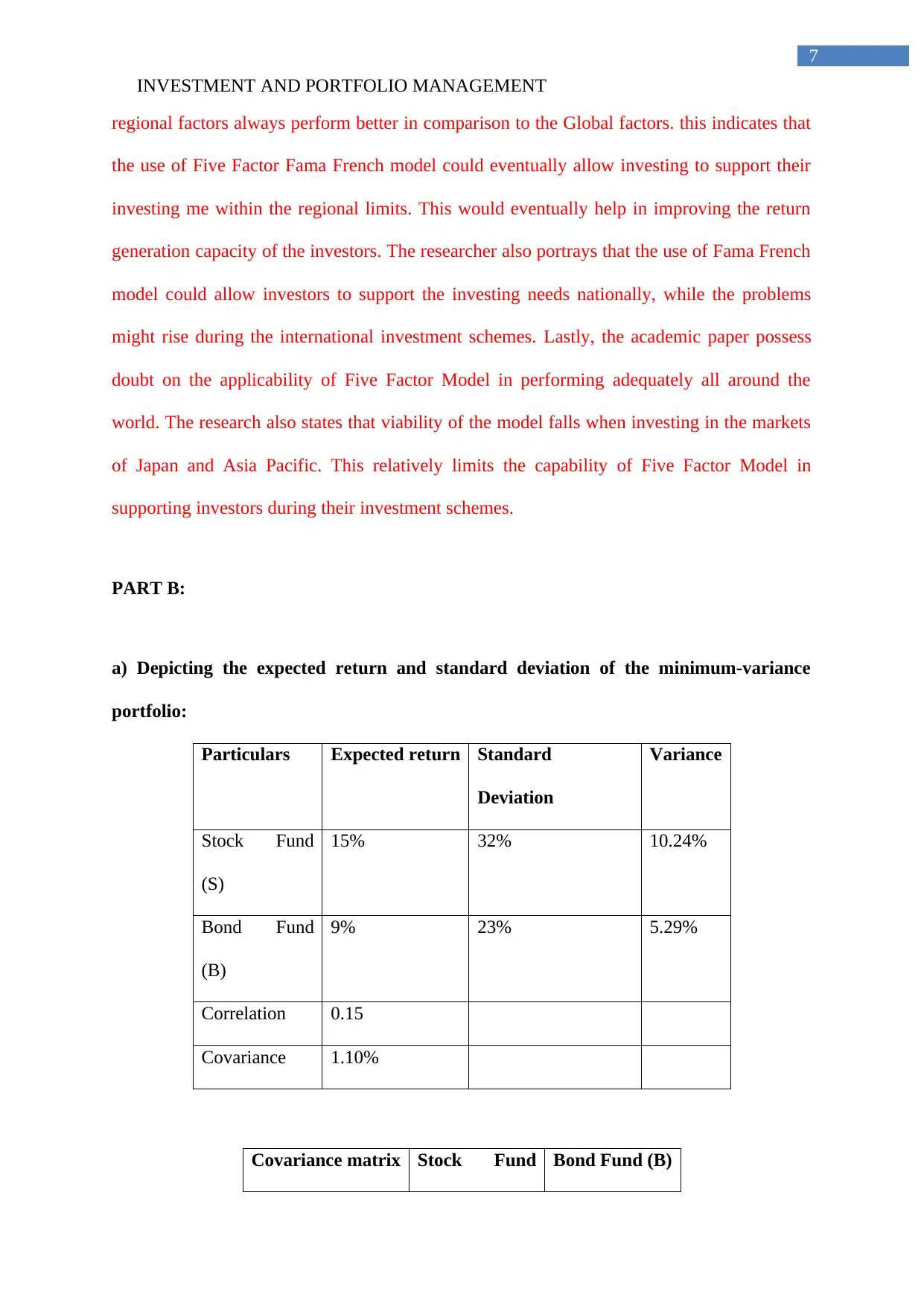

a) Depicting the expected return and standard deviation of the minimum-variance

portfolio:

Particulars Expected return Standard

Deviation

Variance

Stock Fund

(S)

15% 32% 10.24%

Bond Fund

(B)

9% 23% 5.29%

Correlation 0.15

Covariance 1.10%

Covariance matrix Stock Fund Bond Fund (B)

7

regional factors always perform better in comparison to the Global factors. this indicates that

the use of Five Factor Fama French model could eventually allow investing to support their

investing me within the regional limits. This would eventually help in improving the return

generation capacity of the investors. The researcher also portrays that the use of Fama French

model could allow investors to support the investing needs nationally, while the problems

might rise during the international investment schemes. Lastly, the academic paper possess

doubt on the applicability of Five Factor Model in performing adequately all around the

world. The research also states that viability of the model falls when investing in the markets

of Japan and Asia Pacific. This relatively limits the capability of Five Factor Model in

supporting investors during their investment schemes.

PART B:

a) Depicting the expected return and standard deviation of the minimum-variance

portfolio:

Particulars Expected return Standard

Deviation

Variance

Stock Fund

(S)

15% 32% 10.24%

Bond Fund

(B)

9% 23% 5.29%

Correlation 0.15

Covariance 1.10%

Covariance matrix Stock Fund Bond Fund (B)

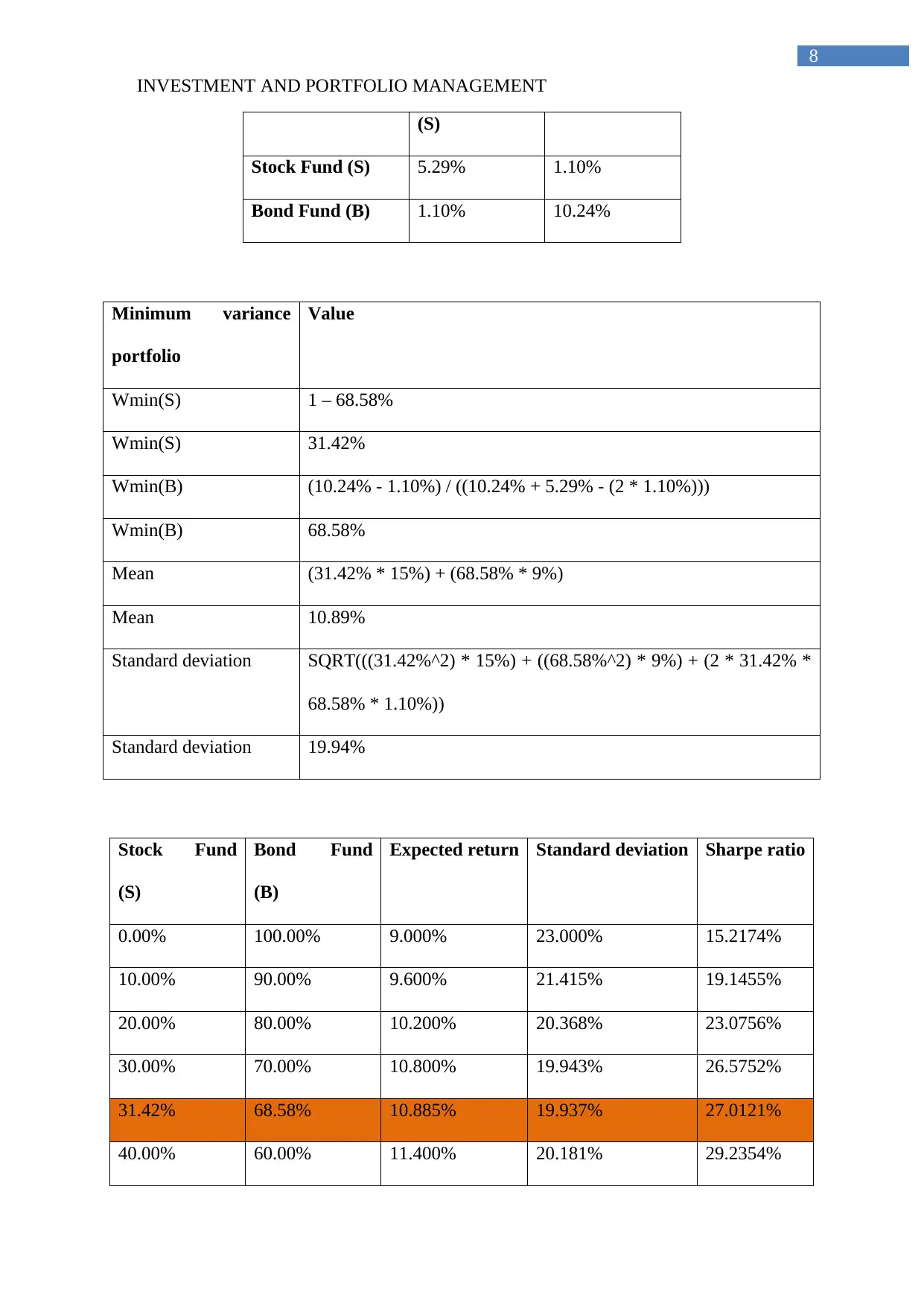

INVESTMENT AND PORTFOLIO MANAGEMENT

8

(S)

Stock Fund (S) 5.29% 1.10%

Bond Fund (B) 1.10% 10.24%

Minimum variance

portfolio

Value

Wmin(S) 1 – 68.58%

Wmin(S) 31.42%

Wmin(B) (10.24% - 1.10%) / ((10.24% + 5.29% - (2 * 1.10%)))

Wmin(B) 68.58%

Mean (31.42% * 15%) + (68.58% * 9%)

Mean 10.89%

Standard deviation SQRT(((31.42%^2) * 15%) + ((68.58%^2) * 9%) + (2 * 31.42% *

68.58% * 1.10%))

Standard deviation 19.94%

Stock Fund

(S)

Bond Fund

(B)

Expected return Standard deviation Sharpe ratio

0.00% 100.00% 9.000% 23.000% 15.2174%

10.00% 90.00% 9.600% 21.415% 19.1455%

20.00% 80.00% 10.200% 20.368% 23.0756%

30.00% 70.00% 10.800% 19.943% 26.5752%

31.42% 68.58% 10.885% 19.937% 27.0121%

40.00% 60.00% 11.400% 20.181% 29.2354%

8

(S)

Stock Fund (S) 5.29% 1.10%

Bond Fund (B) 1.10% 10.24%

Minimum variance

portfolio

Value

Wmin(S) 1 – 68.58%

Wmin(S) 31.42%

Wmin(B) (10.24% - 1.10%) / ((10.24% + 5.29% - (2 * 1.10%)))

Wmin(B) 68.58%

Mean (31.42% * 15%) + (68.58% * 9%)

Mean 10.89%

Standard deviation SQRT(((31.42%^2) * 15%) + ((68.58%^2) * 9%) + (2 * 31.42% *

68.58% * 1.10%))

Standard deviation 19.94%

Stock Fund

(S)

Bond Fund

(B)

Expected return Standard deviation Sharpe ratio

0.00% 100.00% 9.000% 23.000% 15.2174%

10.00% 90.00% 9.600% 21.415% 19.1455%

20.00% 80.00% 10.200% 20.368% 23.0756%

30.00% 70.00% 10.800% 19.943% 26.5752%

31.42% 68.58% 10.885% 19.937% 27.0121%

40.00% 60.00% 11.400% 20.181% 29.2354%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INVESTMENT AND PORTFOLIO MANAGEMENT

9

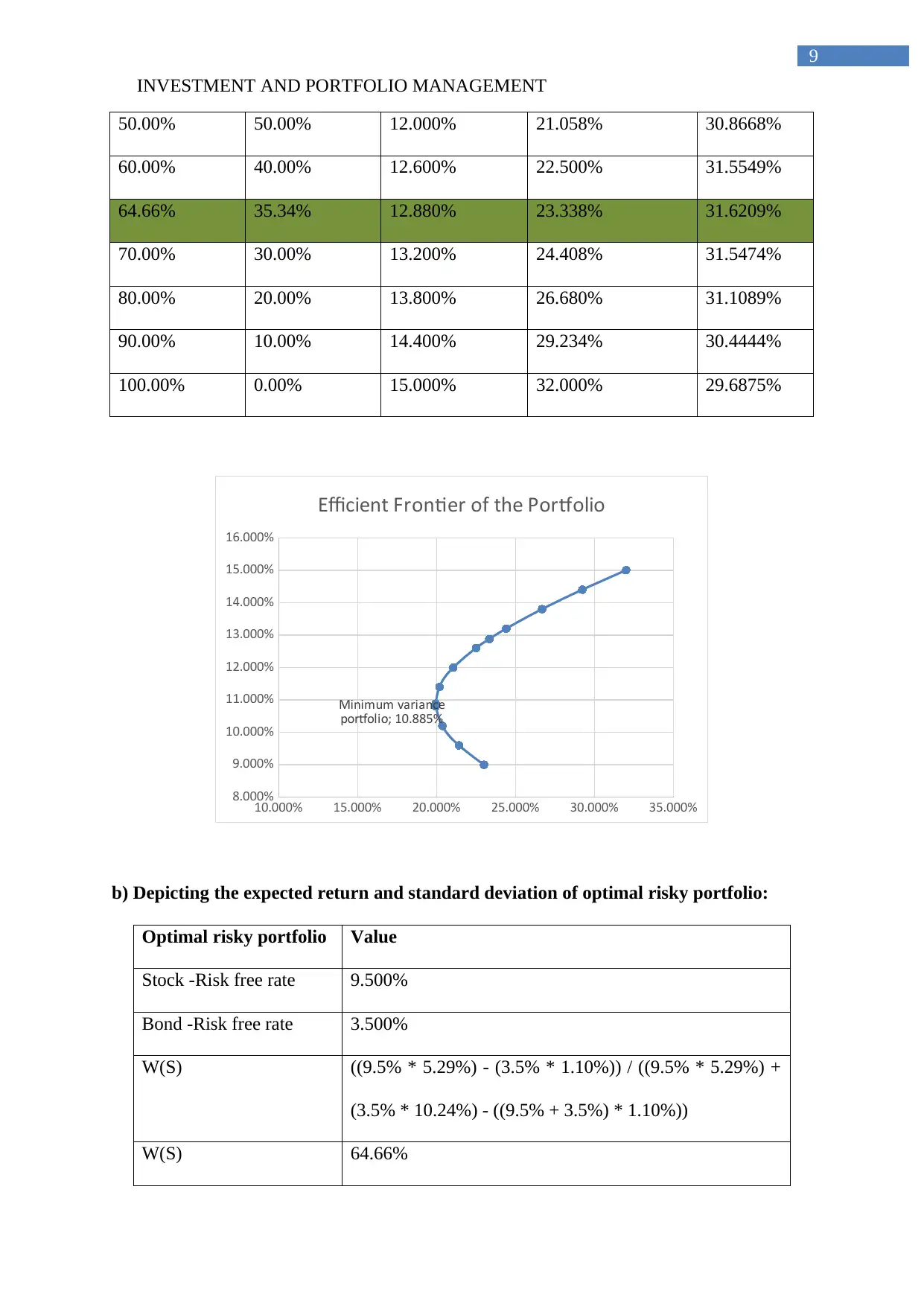

50.00% 50.00% 12.000% 21.058% 30.8668%

60.00% 40.00% 12.600% 22.500% 31.5549%

64.66% 35.34% 12.880% 23.338% 31.6209%

70.00% 30.00% 13.200% 24.408% 31.5474%

80.00% 20.00% 13.800% 26.680% 31.1089%

90.00% 10.00% 14.400% 29.234% 30.4444%

100.00% 0.00% 15.000% 32.000% 29.6875%

10.000% 15.000% 20.000% 25.000% 30.000% 35.000%

8.000%

9.000%

10.000%

11.000%

12.000%

13.000%

14.000%

15.000%

16.000%

Minimum variance

portfolio; 10.885%

Efficient Frontier of the Portfolio

b) Depicting the expected return and standard deviation of optimal risky portfolio:

Optimal risky portfolio Value

Stock -Risk free rate 9.500%

Bond -Risk free rate 3.500%

W(S) ((9.5% * 5.29%) - (3.5% * 1.10%)) / ((9.5% * 5.29%) +

(3.5% * 10.24%) - ((9.5% + 3.5%) * 1.10%))

W(S) 64.66%

9

50.00% 50.00% 12.000% 21.058% 30.8668%

60.00% 40.00% 12.600% 22.500% 31.5549%

64.66% 35.34% 12.880% 23.338% 31.6209%

70.00% 30.00% 13.200% 24.408% 31.5474%

80.00% 20.00% 13.800% 26.680% 31.1089%

90.00% 10.00% 14.400% 29.234% 30.4444%

100.00% 0.00% 15.000% 32.000% 29.6875%

10.000% 15.000% 20.000% 25.000% 30.000% 35.000%

8.000%

9.000%

10.000%

11.000%

12.000%

13.000%

14.000%

15.000%

16.000%

Minimum variance

portfolio; 10.885%

Efficient Frontier of the Portfolio

b) Depicting the expected return and standard deviation of optimal risky portfolio:

Optimal risky portfolio Value

Stock -Risk free rate 9.500%

Bond -Risk free rate 3.500%

W(S) ((9.5% * 5.29%) - (3.5% * 1.10%)) / ((9.5% * 5.29%) +

(3.5% * 10.24%) - ((9.5% + 3.5%) * 1.10%))

W(S) 64.66%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INVESTMENT AND PORTFOLIO MANAGEMENT

10

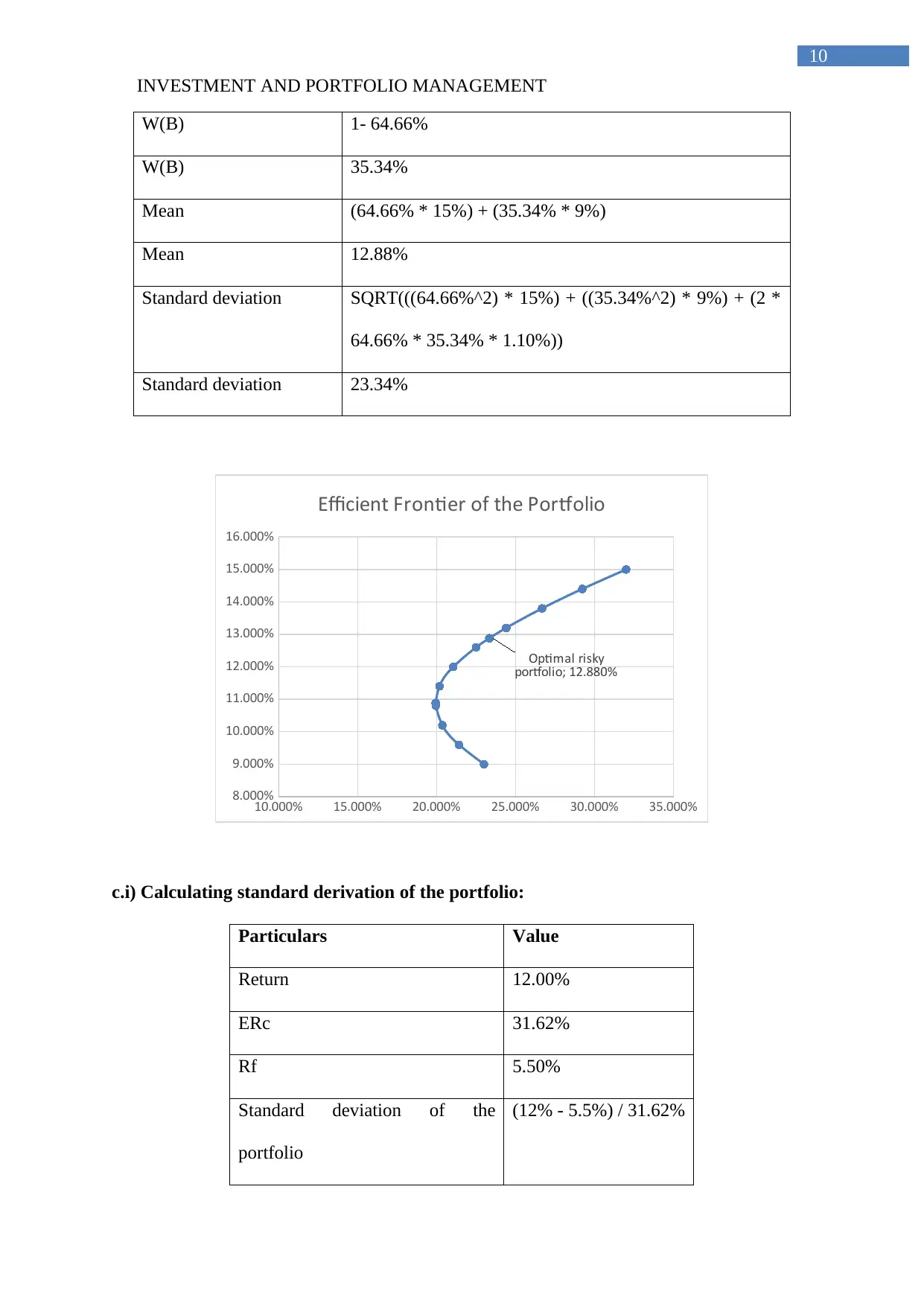

W(B) 1- 64.66%

W(B) 35.34%

Mean (64.66% * 15%) + (35.34% * 9%)

Mean 12.88%

Standard deviation SQRT(((64.66%^2) * 15%) + ((35.34%^2) * 9%) + (2 *

64.66% * 35.34% * 1.10%))

Standard deviation 23.34%

10.000% 15.000% 20.000% 25.000% 30.000% 35.000%

8.000%

9.000%

10.000%

11.000%

12.000%

13.000%

14.000%

15.000%

16.000%

Optimal risky

portfolio; 12.880%

Efficient Frontier of the Portfolio

c.i) Calculating standard derivation of the portfolio:

Particulars Value

Return 12.00%

ERc 31.62%

Rf 5.50%

Standard deviation of the

portfolio

(12% - 5.5%) / 31.62%

10

W(B) 1- 64.66%

W(B) 35.34%

Mean (64.66% * 15%) + (35.34% * 9%)

Mean 12.88%

Standard deviation SQRT(((64.66%^2) * 15%) + ((35.34%^2) * 9%) + (2 *

64.66% * 35.34% * 1.10%))

Standard deviation 23.34%

10.000% 15.000% 20.000% 25.000% 30.000% 35.000%

8.000%

9.000%

10.000%

11.000%

12.000%

13.000%

14.000%

15.000%

16.000%

Optimal risky

portfolio; 12.880%

Efficient Frontier of the Portfolio

c.i) Calculating standard derivation of the portfolio:

Particulars Value

Return 12.00%

ERc 31.62%

Rf 5.50%

Standard deviation of the

portfolio

(12% - 5.5%) / 31.62%

INVESTMENT AND PORTFOLIO MANAGEMENT

11

Standard deviation of the

portfolio

20.56%

From the above table, standard deviation of the portfolio is calculated, which is at the

levels of 20.56%. The standard deviation is detected by detecting the overall reward to

variability ratio for identifying the actual risk involved in investment. Moreover, the use of

optimal CAL has helped in identifying the overall standard deviation of the portfolio. Stettina

and Horz (2015) stated that the detection of risk is essential to understand the risk to reward

ratio provided from investment.

c.ii) Calculating the portion of T-bill fund and each of the two risky funds:

Particulars Value

Rf 5.50%

Mean 12.88%

Return 12.00%

Proportion without T-bill fund (12% - 5.5%) / (12.88%-5.5%)

Proportion without T-bill fund 88.08%

Proportion with T-bill fund 1- 88.08%

Proportion with T-bill fund 11.92%

The calculation of T-bill portion in the portfolio is detected by using the means of any

portfolio along with optimal CAL. This has helped in detecting the actual funds of the

portfolio, which consist of T=bill fund. The 11.92% of the fund is contributed by T-bill,

which could help in reducing risk from investment. Aouni, Colapinto and La (2014)

11

Standard deviation of the

portfolio

20.56%

From the above table, standard deviation of the portfolio is calculated, which is at the

levels of 20.56%. The standard deviation is detected by detecting the overall reward to

variability ratio for identifying the actual risk involved in investment. Moreover, the use of

optimal CAL has helped in identifying the overall standard deviation of the portfolio. Stettina

and Horz (2015) stated that the detection of risk is essential to understand the risk to reward

ratio provided from investment.

c.ii) Calculating the portion of T-bill fund and each of the two risky funds:

Particulars Value

Rf 5.50%

Mean 12.88%

Return 12.00%

Proportion without T-bill fund (12% - 5.5%) / (12.88%-5.5%)

Proportion without T-bill fund 88.08%

Proportion with T-bill fund 1- 88.08%

Proportion with T-bill fund 11.92%

The calculation of T-bill portion in the portfolio is detected by using the means of any

portfolio along with optimal CAL. This has helped in detecting the actual funds of the

portfolio, which consist of T=bill fund. The 11.92% of the fund is contributed by T-bill,

which could help in reducing risk from investment. Aouni, Colapinto and La (2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.