Investment and Portfolio Management: Share Market and Risk Analysis

VerifiedAdded on 2023/06/10

|12

|2483

|51

Report

AI Summary

This report provides a detailed analysis of investment and portfolio management, covering key concepts such as risk and return, systematic and unsystematic risk, and different types of securities. It includes calculations for portfolio beta, Sharpe ratio, and Treynor's ratio, along with a discussion on compensation schemes for financial managers. The report also examines venture capital financing, dividend growth models for share valuation, and price-earnings ratios. Furthermore, it delves into bond valuation, the segmented market theory, and the sensitivity of long-term loans to interest rate changes. The document concludes with references to relevant books and journals. Desklib provides this and other solved assignments to aid students in their studies.

INVESTMENT

AND

PORTFOLIO

MANAGEMENT

AND

PORTFOLIO

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

TASK:..............................................................................................................................................2

Question No 1..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

Question No 2..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

Question No 3..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

Question No 4..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

REFERENCES................................................................................................................................3

TASK:..............................................................................................................................................2

Question No 1..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

Question No 2..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

Question No 3..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

Question No 4..................................................................................................................................2

a).............................................................................................................................................2

b).............................................................................................................................................2

c).............................................................................................................................................2

REFERENCES................................................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK:

Question No 1

a)

Risk and return are the two different terminology that are being used in the share market that

indicates the market fluctuations. The returns denote the income that has been generated with the

investment made in the particular security and risk in the deviation that arise when the market

price of the share being collapsed suddenly. Risk return trade off simply means that potential

return arises with the increase in risk

b)

Python is the language that is being used as to support language for the software developers for

building the control and management, testing and in many other ways.

c)

Unsystematic risk is as risk specific to a company or the industry whereas systematic risk is the

risk which has been related to broader market. On the basis of the table below it has been

concluded that Share 1 has more systematic risk and share 2 has more unsystematic risk because

there is the constant increase in the share price of Share 1 and share 2 does not have constant

growth rate. The example of the systematic risk is change in the rate of inflation, risk in the

unemployment rates, the rate of poverty in the country has been increased, changes in the interest

rates. On the other hand the example of unsystematic risk could be higher rate of the employee

turnover, strike made by the employees, cost of operational activities increases and so on.

Question No 2

(a)

In general, there are two type of securities in which a person can make investments, these are

risk free securities and risk associated securities.

Risk free securities are those securities which have no risk involved, for example: - Government

bonds, other Government securities, treasury bills etc.

Question No 1

a)

Risk and return are the two different terminology that are being used in the share market that

indicates the market fluctuations. The returns denote the income that has been generated with the

investment made in the particular security and risk in the deviation that arise when the market

price of the share being collapsed suddenly. Risk return trade off simply means that potential

return arises with the increase in risk

b)

Python is the language that is being used as to support language for the software developers for

building the control and management, testing and in many other ways.

c)

Unsystematic risk is as risk specific to a company or the industry whereas systematic risk is the

risk which has been related to broader market. On the basis of the table below it has been

concluded that Share 1 has more systematic risk and share 2 has more unsystematic risk because

there is the constant increase in the share price of Share 1 and share 2 does not have constant

growth rate. The example of the systematic risk is change in the rate of inflation, risk in the

unemployment rates, the rate of poverty in the country has been increased, changes in the interest

rates. On the other hand the example of unsystematic risk could be higher rate of the employee

turnover, strike made by the employees, cost of operational activities increases and so on.

Question No 2

(a)

In general, there are two type of securities in which a person can make investments, these are

risk free securities and risk associated securities.

Risk free securities are those securities which have no risk involved, for example: - Government

bonds, other Government securities, treasury bills etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

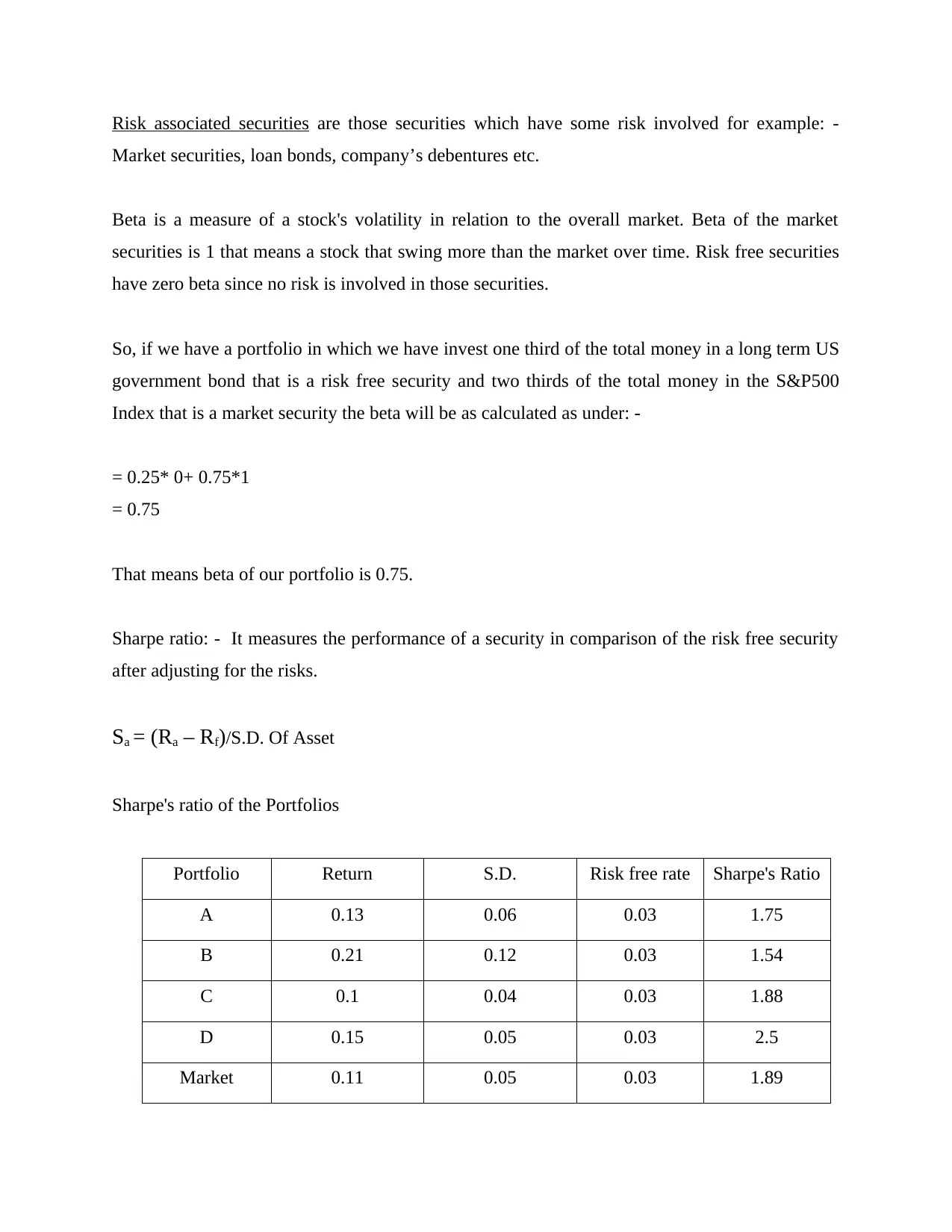

Risk associated securities are those securities which have some risk involved for example: -

Market securities, loan bonds, company’s debentures etc.

Beta is a measure of a stock's volatility in relation to the overall market. Beta of the market

securities is 1 that means a stock that swing more than the market over time. Risk free securities

have zero beta since no risk is involved in those securities.

So, if we have a portfolio in which we have invest one third of the total money in a long term US

government bond that is a risk free security and two thirds of the total money in the S&P500

Index that is a market security the beta will be as calculated as under: -

= 0.25* 0+ 0.75*1

= 0.75

That means beta of our portfolio is 0.75.

Sharpe ratio: - It measures the performance of a security in comparison of the risk free security

after adjusting for the risks.

Sa = (Ra – Rf)/S.D. Of Asset

Sharpe's ratio of the Portfolios

Portfolio Return S.D. Risk free rate Sharpe's Ratio

A 0.13 0.06 0.03 1.75

B 0.21 0.12 0.03 1.54

C 0.1 0.04 0.03 1.88

D 0.15 0.05 0.03 2.5

Market 0.11 0.05 0.03 1.89

Market securities, loan bonds, company’s debentures etc.

Beta is a measure of a stock's volatility in relation to the overall market. Beta of the market

securities is 1 that means a stock that swing more than the market over time. Risk free securities

have zero beta since no risk is involved in those securities.

So, if we have a portfolio in which we have invest one third of the total money in a long term US

government bond that is a risk free security and two thirds of the total money in the S&P500

Index that is a market security the beta will be as calculated as under: -

= 0.25* 0+ 0.75*1

= 0.75

That means beta of our portfolio is 0.75.

Sharpe ratio: - It measures the performance of a security in comparison of the risk free security

after adjusting for the risks.

Sa = (Ra – Rf)/S.D. Of Asset

Sharpe's ratio of the Portfolios

Portfolio Return S.D. Risk free rate Sharpe's Ratio

A 0.13 0.06 0.03 1.75

B 0.21 0.12 0.03 1.54

C 0.1 0.04 0.03 1.88

D 0.15 0.05 0.03 2.5

Market 0.11 0.05 0.03 1.89

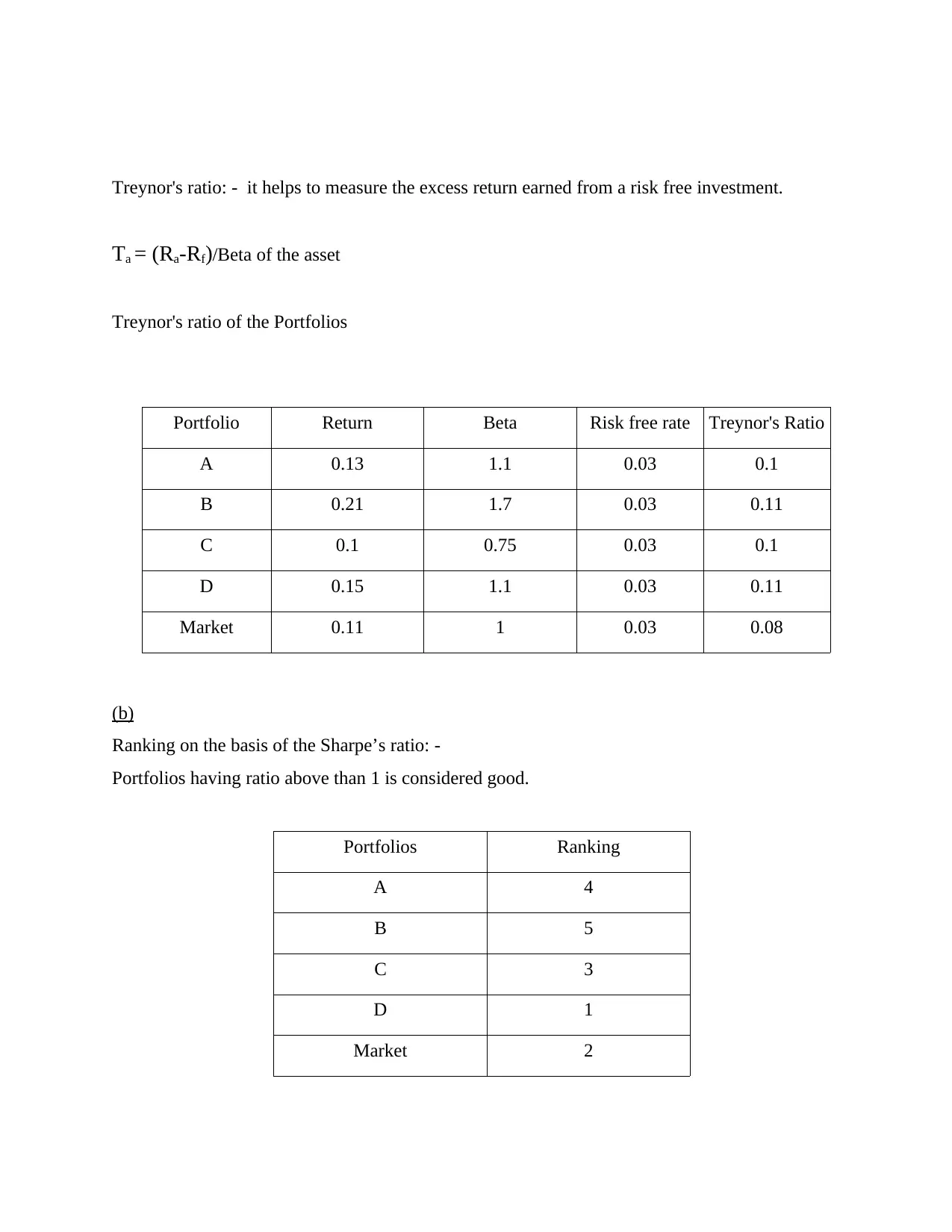

Treynor's ratio: - it helps to measure the excess return earned from a risk free investment.

Ta = (Ra-Rf)/Beta of the asset

Treynor's ratio of the Portfolios

Portfolio Return Beta Risk free rate Treynor's Ratio

A 0.13 1.1 0.03 0.1

B 0.21 1.7 0.03 0.11

C 0.1 0.75 0.03 0.1

D 0.15 1.1 0.03 0.11

Market 0.11 1 0.03 0.08

(b)

Ranking on the basis of the Sharpe’s ratio: -

Portfolios having ratio above than 1 is considered good.

Portfolios Ranking

A 4

B 5

C 3

D 1

Market 2

Ta = (Ra-Rf)/Beta of the asset

Treynor's ratio of the Portfolios

Portfolio Return Beta Risk free rate Treynor's Ratio

A 0.13 1.1 0.03 0.1

B 0.21 1.7 0.03 0.11

C 0.1 0.75 0.03 0.1

D 0.15 1.1 0.03 0.11

Market 0.11 1 0.03 0.08

(b)

Ranking on the basis of the Sharpe’s ratio: -

Portfolios having ratio above than 1 is considered good.

Portfolios Ranking

A 4

B 5

C 3

D 1

Market 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

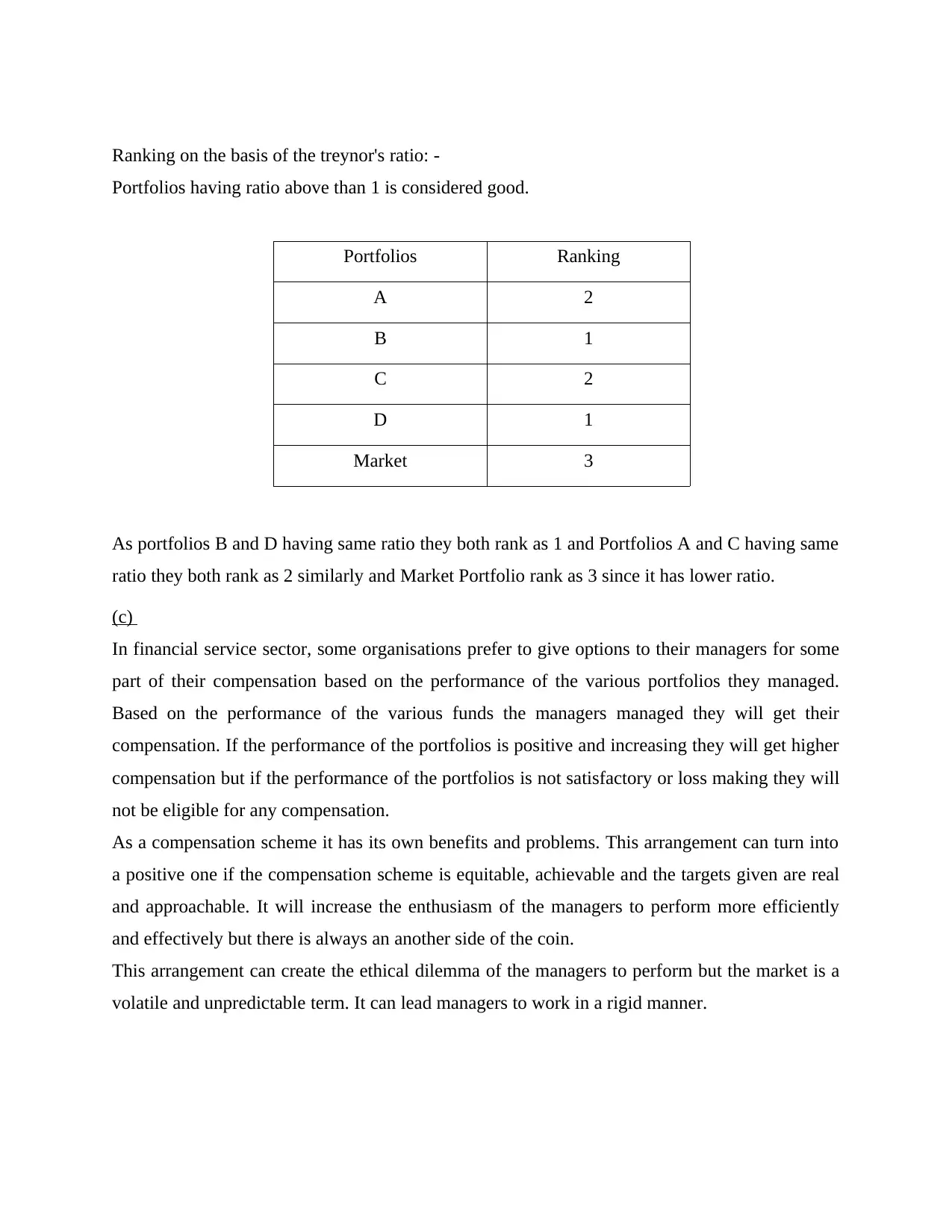

Ranking on the basis of the treynor's ratio: -

Portfolios having ratio above than 1 is considered good.

Portfolios Ranking

A 2

B 1

C 2

D 1

Market 3

As portfolios B and D having same ratio they both rank as 1 and Portfolios A and C having same

ratio they both rank as 2 similarly and Market Portfolio rank as 3 since it has lower ratio.

(c)

In financial service sector, some organisations prefer to give options to their managers for some

part of their compensation based on the performance of the various portfolios they managed.

Based on the performance of the various funds the managers managed they will get their

compensation. If the performance of the portfolios is positive and increasing they will get higher

compensation but if the performance of the portfolios is not satisfactory or loss making they will

not be eligible for any compensation.

As a compensation scheme it has its own benefits and problems. This arrangement can turn into

a positive one if the compensation scheme is equitable, achievable and the targets given are real

and approachable. It will increase the enthusiasm of the managers to perform more efficiently

and effectively but there is always an another side of the coin.

This arrangement can create the ethical dilemma of the managers to perform but the market is a

volatile and unpredictable term. It can lead managers to work in a rigid manner.

Portfolios having ratio above than 1 is considered good.

Portfolios Ranking

A 2

B 1

C 2

D 1

Market 3

As portfolios B and D having same ratio they both rank as 1 and Portfolios A and C having same

ratio they both rank as 2 similarly and Market Portfolio rank as 3 since it has lower ratio.

(c)

In financial service sector, some organisations prefer to give options to their managers for some

part of their compensation based on the performance of the various portfolios they managed.

Based on the performance of the various funds the managers managed they will get their

compensation. If the performance of the portfolios is positive and increasing they will get higher

compensation but if the performance of the portfolios is not satisfactory or loss making they will

not be eligible for any compensation.

As a compensation scheme it has its own benefits and problems. This arrangement can turn into

a positive one if the compensation scheme is equitable, achievable and the targets given are real

and approachable. It will increase the enthusiasm of the managers to perform more efficiently

and effectively but there is always an another side of the coin.

This arrangement can create the ethical dilemma of the managers to perform but the market is a

volatile and unpredictable term. It can lead managers to work in a rigid manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question No 3

a)

The private partnership firm is the voluntary association which can be started by the two person

only but not more than 50 members. In case of partnership firm, the transfer of share is limited to

its members only. Further in case of partnership firm the share that are being allotted to the

members are not freely transferable to anyone else. The legal process for registration of the firm

is very limited and easily registered with the government. On the other hand, the venture capital

financing is the form of private equity and the type of financing that has been provided by the

investors to start-up companies and small businesses that are believed to have the long term

growth potential. The examples of venture capital are the investment banks, insurance companies

or the pension funds etc.

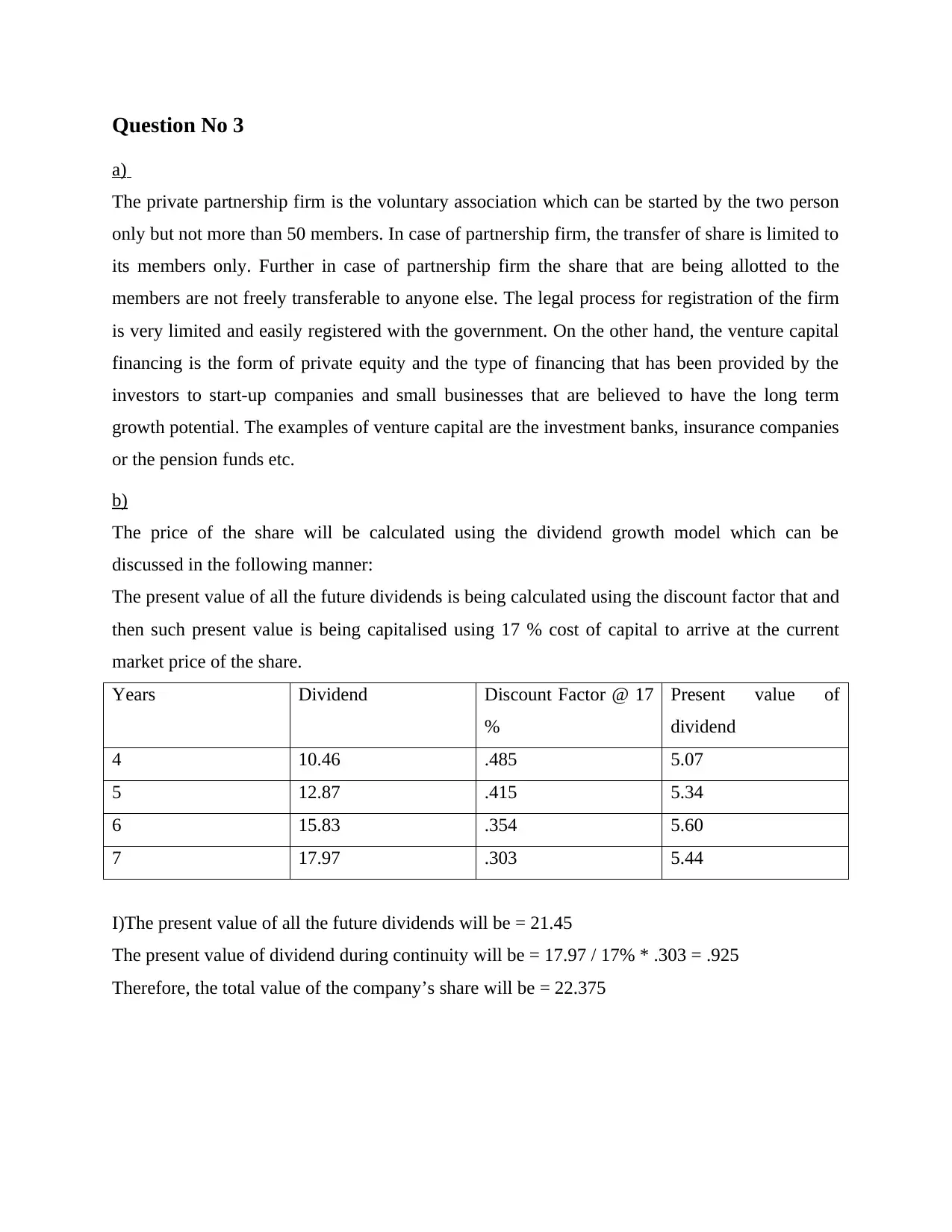

b)

The price of the share will be calculated using the dividend growth model which can be

discussed in the following manner:

The present value of all the future dividends is being calculated using the discount factor that and

then such present value is being capitalised using 17 % cost of capital to arrive at the current

market price of the share.

Years Dividend Discount Factor @ 17

%

Present value of

dividend

4 10.46 .485 5.07

5 12.87 .415 5.34

6 15.83 .354 5.60

7 17.97 .303 5.44

I)The present value of all the future dividends will be = 21.45

The present value of dividend during continuity will be = 17.97 / 17% * .303 = .925

Therefore, the total value of the company’s share will be = 22.375

a)

The private partnership firm is the voluntary association which can be started by the two person

only but not more than 50 members. In case of partnership firm, the transfer of share is limited to

its members only. Further in case of partnership firm the share that are being allotted to the

members are not freely transferable to anyone else. The legal process for registration of the firm

is very limited and easily registered with the government. On the other hand, the venture capital

financing is the form of private equity and the type of financing that has been provided by the

investors to start-up companies and small businesses that are believed to have the long term

growth potential. The examples of venture capital are the investment banks, insurance companies

or the pension funds etc.

b)

The price of the share will be calculated using the dividend growth model which can be

discussed in the following manner:

The present value of all the future dividends is being calculated using the discount factor that and

then such present value is being capitalised using 17 % cost of capital to arrive at the current

market price of the share.

Years Dividend Discount Factor @ 17

%

Present value of

dividend

4 10.46 .485 5.07

5 12.87 .415 5.34

6 15.83 .354 5.60

7 17.97 .303 5.44

I)The present value of all the future dividends will be = 21.45

The present value of dividend during continuity will be = 17.97 / 17% * .303 = .925

Therefore, the total value of the company’s share will be = 22.375

ii) The value that has been calculated using dividend growth model has been 22.375. However,

its market price is $38.45. Therefore, it has been concluded that the share price is overvalued in

the market therefore it is not worth full for the Lara William to make the investment in the same.

c)

The formula for calculating price earnings ratio:

PE Ratio = (MPS / EPS)

It has been given that company pays the dividend 50 % of its earnings. The recently they have

paid the dividend of $3.35. Therefore, their earning per share would be $6.70. The expectation of

the investor for the company has been 9% as the return from ABC shares.

The earning per share will be = 6.70 and market price per share will be calculated on the basis of

capitalising the dividend that is 3.25 / 9%, therefore MPS arrived to be 36.11

Therefore, PE ratio of the ABC company will be = 36.11 / 6.70 = 5.39 Times

ii) If the return of investment is 7% then MPS will be = 3.25 / 7% = 46.43

Therefore PE ratio will be = 46.43 / 6.70 = 6.93 Times

Question No 4

a)

This theory states that the long term and short-term interest rates are not related to each other. It

also states that the rate of bond for the different time period securities should be considered

separately like items in different market for debt securities. Another name of this theory has been

segmented market theory. This theory is based on the belief that every segment of the bond

securities mainly consists of the investor whose preference is to invest in those securities on

those securities who are having specific duration like short duration, intermediate duration and

long-term duration. This theory further states that the market for the buyer and the seller have the

different characteristics and the motivation. This theory is based on the habits of the investor and

their types such as individual investor are being different from the institutional investor such as

banks, insurance companies and so on. Bank will invest in those securities only whose duration

are being less, on the other hand the insurance companies will invest in those securities whose

duration are more than 1 year.

its market price is $38.45. Therefore, it has been concluded that the share price is overvalued in

the market therefore it is not worth full for the Lara William to make the investment in the same.

c)

The formula for calculating price earnings ratio:

PE Ratio = (MPS / EPS)

It has been given that company pays the dividend 50 % of its earnings. The recently they have

paid the dividend of $3.35. Therefore, their earning per share would be $6.70. The expectation of

the investor for the company has been 9% as the return from ABC shares.

The earning per share will be = 6.70 and market price per share will be calculated on the basis of

capitalising the dividend that is 3.25 / 9%, therefore MPS arrived to be 36.11

Therefore, PE ratio of the ABC company will be = 36.11 / 6.70 = 5.39 Times

ii) If the return of investment is 7% then MPS will be = 3.25 / 7% = 46.43

Therefore PE ratio will be = 46.43 / 6.70 = 6.93 Times

Question No 4

a)

This theory states that the long term and short-term interest rates are not related to each other. It

also states that the rate of bond for the different time period securities should be considered

separately like items in different market for debt securities. Another name of this theory has been

segmented market theory. This theory is based on the belief that every segment of the bond

securities mainly consists of the investor whose preference is to invest in those securities on

those securities who are having specific duration like short duration, intermediate duration and

long-term duration. This theory further states that the market for the buyer and the seller have the

different characteristics and the motivation. This theory is based on the habits of the investor and

their types such as individual investor are being different from the institutional investor such as

banks, insurance companies and so on. Bank will invest in those securities only whose duration

are being less, on the other hand the insurance companies will invest in those securities whose

duration are more than 1 year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b)

Bond valuation is the process for determining the value of the bond so that fair price could be

arrived. This would calculation relating to cash flow in the form of interest that are being

received by the investor when they invest in the bond of the particular company. In order to

calculate the value of the bonds, dividend discount model is to be used accordingly. It is a

financial model that values of bond at the discounted value of the future interest payments.

Under this model, the price of a share that will be traded is calculated by the PV of all expected

future dividend payment discounted by an appropriate risk- adjusted rate. The dividend discount

model price is the intrinsic value of the bond i.e.

Intrinsic value = Sum of PV of future cash flows

The Price of the bond is being calculated below:

40/ (1+.04)1 + 40 / (1.04)2 + 40/ (1.04)3 +1000/ (1.04)9

= 999.99

The bond is being considered to be at PAR value.

c)

The long-term loan is very sensitive to the interest rates changes that has been taken place in the

market. The reason for the same is that the income that has been generated by the bonds is of

fixed nature. The intention of the investor is to purchase the corporate bond as they are willing to

acquire the portion of the debt capital of the company. When the company issues debt, it contains

specific rate of interest attached to it and it is issued for the specific term so that the fund that are

being raised so far will be utilised by the corporate for investment purpose.

There are higher chances that there may be the change in interest rates and if the interest rates

increases then it will create negative effect on the price of bond. In that situation the investor

prefers to invest in long term bonds having the maturity value for more than 5 years. The

duration long term bonds are always higher as compare to short duration of bonds.

The changes in the interest rate has the deep impact on the price of the bonds. The rate of interest

changes when there is an absolute level of interest rate fluctuates. The risk that has been attached

interest rate directly affects the value that has been hold by fixed income securities.

Bond valuation is the process for determining the value of the bond so that fair price could be

arrived. This would calculation relating to cash flow in the form of interest that are being

received by the investor when they invest in the bond of the particular company. In order to

calculate the value of the bonds, dividend discount model is to be used accordingly. It is a

financial model that values of bond at the discounted value of the future interest payments.

Under this model, the price of a share that will be traded is calculated by the PV of all expected

future dividend payment discounted by an appropriate risk- adjusted rate. The dividend discount

model price is the intrinsic value of the bond i.e.

Intrinsic value = Sum of PV of future cash flows

The Price of the bond is being calculated below:

40/ (1+.04)1 + 40 / (1.04)2 + 40/ (1.04)3 +1000/ (1.04)9

= 999.99

The bond is being considered to be at PAR value.

c)

The long-term loan is very sensitive to the interest rates changes that has been taken place in the

market. The reason for the same is that the income that has been generated by the bonds is of

fixed nature. The intention of the investor is to purchase the corporate bond as they are willing to

acquire the portion of the debt capital of the company. When the company issues debt, it contains

specific rate of interest attached to it and it is issued for the specific term so that the fund that are

being raised so far will be utilised by the corporate for investment purpose.

There are higher chances that there may be the change in interest rates and if the interest rates

increases then it will create negative effect on the price of bond. In that situation the investor

prefers to invest in long term bonds having the maturity value for more than 5 years. The

duration long term bonds are always higher as compare to short duration of bonds.

The changes in the interest rate has the deep impact on the price of the bonds. The rate of interest

changes when there is an absolute level of interest rate fluctuates. The risk that has been attached

interest rate directly affects the value that has been hold by fixed income securities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abinzano, I., Campion, M.J., and Raventós-Pujol, A., 2021. Sports Betting and The Black-

Litterman Model: A New Portfolio-Management Perspective. International Journal of

Sport Finance, 16(4).

Al Janabi, M.A., 2020. Multivariate portfolio optimization under illiquid market prospects: a

review of theoretical algorithms and practical techniques for liquidity risk

management. Journal of Modelling in Management.

Elkamhi, R., Lee, J.S. and Sadik, S., 2021. Bridging the Gap between Strategic Allocation and

Investment Risk. The Journal of Portfolio Management, 47(6), pp.89-100.

Ilyas, U., Butt, M.U. and Gulzar, M., 2022. An application of panel ARDL model with

cointegration for portfolio management. International Journal of Economics and

Business Research, 23(3), pp.275-298.

Irukulapati, J., Hsu, D.F. and Schweikert, C., 2018, July. Long-term portfolio management using

attribute selection and combinatorial fusion. In 2018 IEEE 17th International

Conference on Cognitive Informatics & Cognitive Computing (ICCI* CC) (pp. 593-

599). IEEE.

Konstantinov, G.S., 2022. Practical Applications of What Portfolio in Europe Makes

Sense? Practical Applications.

Lee, W. and Liu, P., 2021. Work Harder: Diligent Rebalancing and Investment Horizon. The

Journal of Portfolio Management, 47(3), pp.17-34.

Shanat, F., Al-Munayes, S., and Ameen, A., 2018, December. Corporate Portfolio Management

in NOCs: The Implementation Dilemma in Real-Life Business. In SPE International

Heavy Oil Conference and Exhibition. OnePetro.

Wang, J.N., Liu, H.C., and Hsu, Y.T., 2019. Economic benefits of technical analysis in portfolio

management: Evidence from global stock markets. International Journal of Finance &

Economics, 24(2), pp.890-902.

Weinmayer, K. and Rammerstorfer, M., 2022. Efficiency of Socially Responsible Investments in

the Context of Portfolio Management. Available at SSRN 4039593.

Books and Journals

Abinzano, I., Campion, M.J., and Raventós-Pujol, A., 2021. Sports Betting and The Black-

Litterman Model: A New Portfolio-Management Perspective. International Journal of

Sport Finance, 16(4).

Al Janabi, M.A., 2020. Multivariate portfolio optimization under illiquid market prospects: a

review of theoretical algorithms and practical techniques for liquidity risk

management. Journal of Modelling in Management.

Elkamhi, R., Lee, J.S. and Sadik, S., 2021. Bridging the Gap between Strategic Allocation and

Investment Risk. The Journal of Portfolio Management, 47(6), pp.89-100.

Ilyas, U., Butt, M.U. and Gulzar, M., 2022. An application of panel ARDL model with

cointegration for portfolio management. International Journal of Economics and

Business Research, 23(3), pp.275-298.

Irukulapati, J., Hsu, D.F. and Schweikert, C., 2018, July. Long-term portfolio management using

attribute selection and combinatorial fusion. In 2018 IEEE 17th International

Conference on Cognitive Informatics & Cognitive Computing (ICCI* CC) (pp. 593-

599). IEEE.

Konstantinov, G.S., 2022. Practical Applications of What Portfolio in Europe Makes

Sense? Practical Applications.

Lee, W. and Liu, P., 2021. Work Harder: Diligent Rebalancing and Investment Horizon. The

Journal of Portfolio Management, 47(3), pp.17-34.

Shanat, F., Al-Munayes, S., and Ameen, A., 2018, December. Corporate Portfolio Management

in NOCs: The Implementation Dilemma in Real-Life Business. In SPE International

Heavy Oil Conference and Exhibition. OnePetro.

Wang, J.N., Liu, H.C., and Hsu, Y.T., 2019. Economic benefits of technical analysis in portfolio

management: Evidence from global stock markets. International Journal of Finance &

Economics, 24(2), pp.890-902.

Weinmayer, K. and Rammerstorfer, M., 2022. Efficiency of Socially Responsible Investments in

the Context of Portfolio Management. Available at SSRN 4039593.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.