Investment Profitability Analysis for XYZ plc: A Financial Report

VerifiedAdded on 2023/01/11

|7

|1231

|79

Report

AI Summary

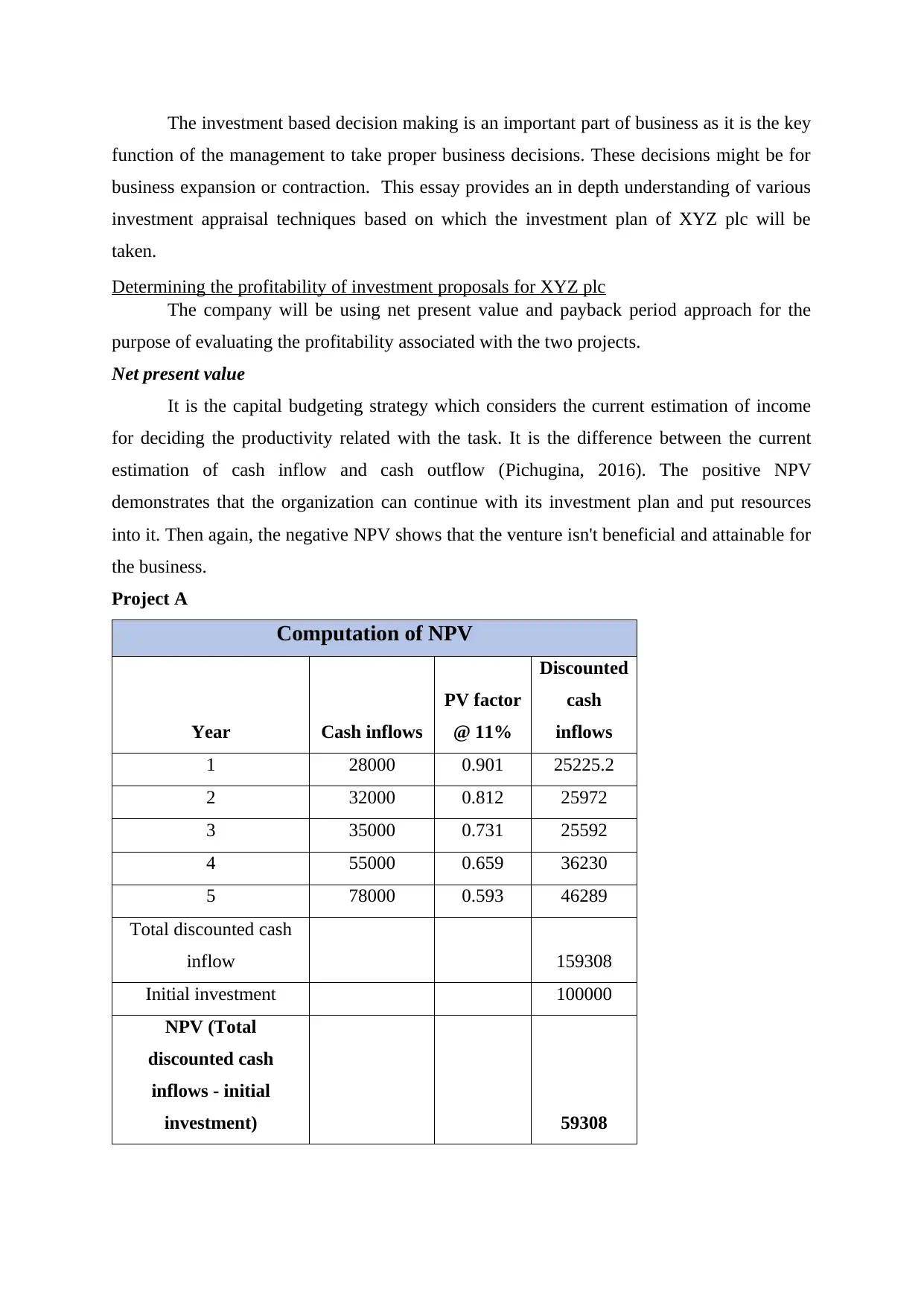

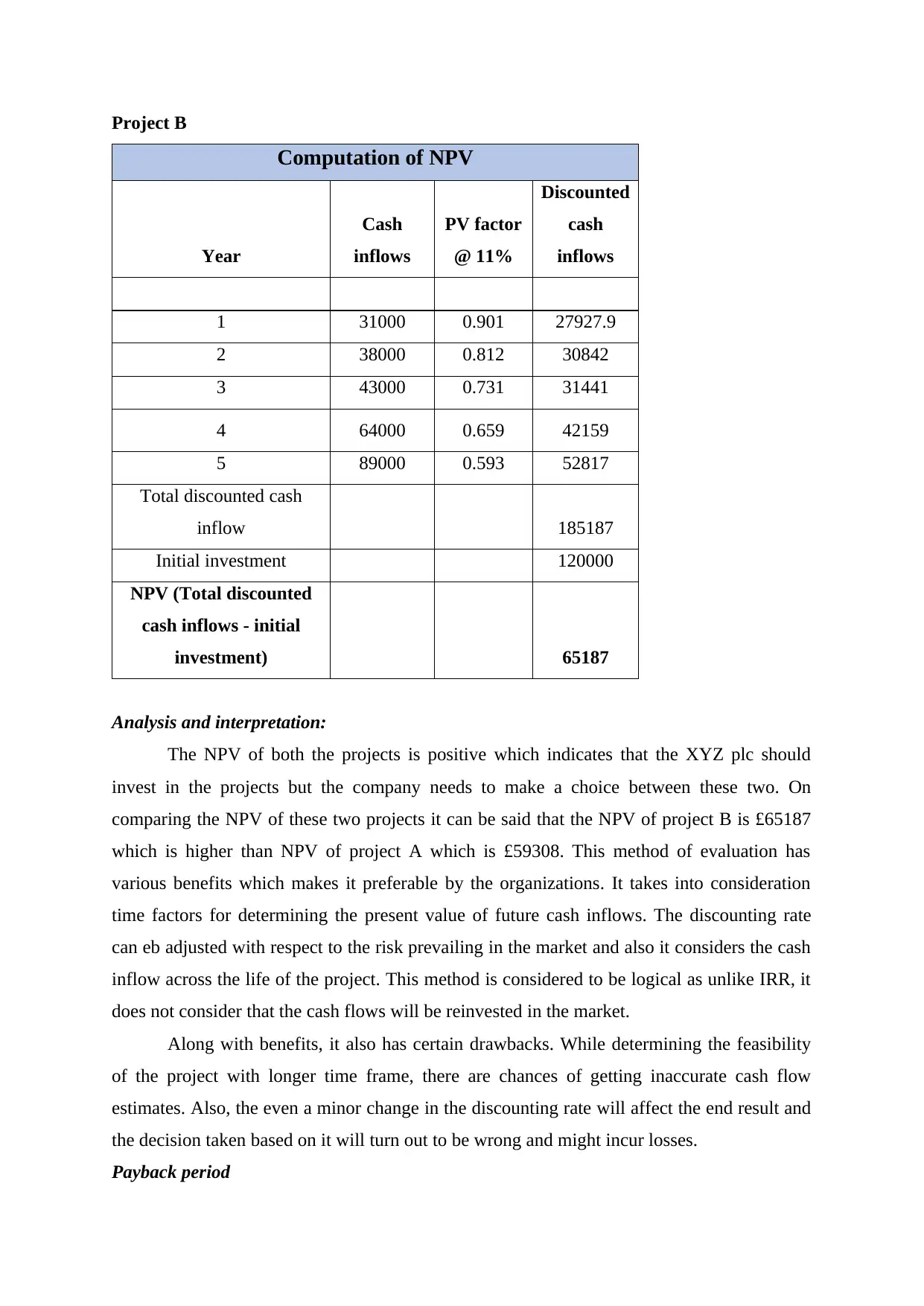

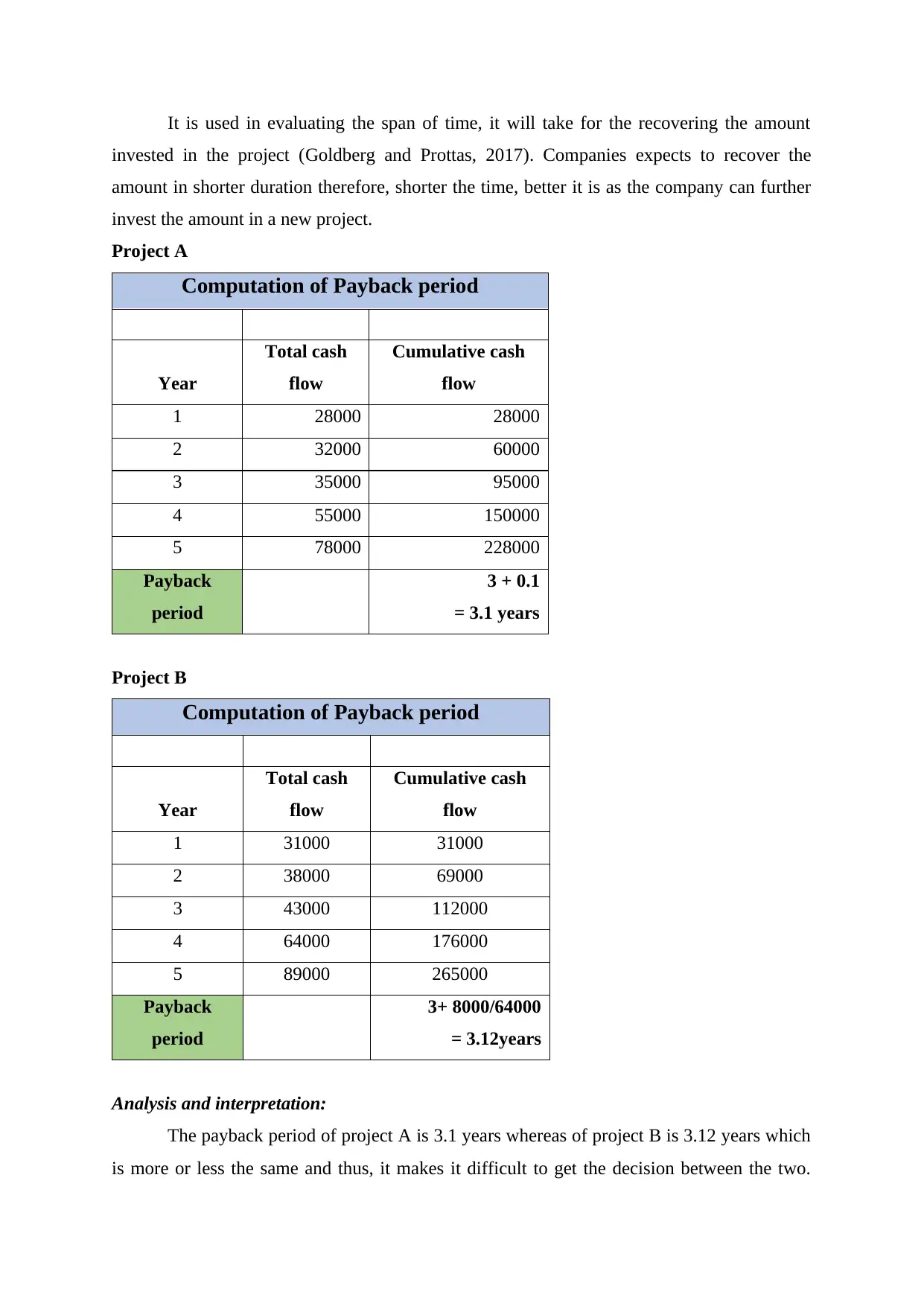

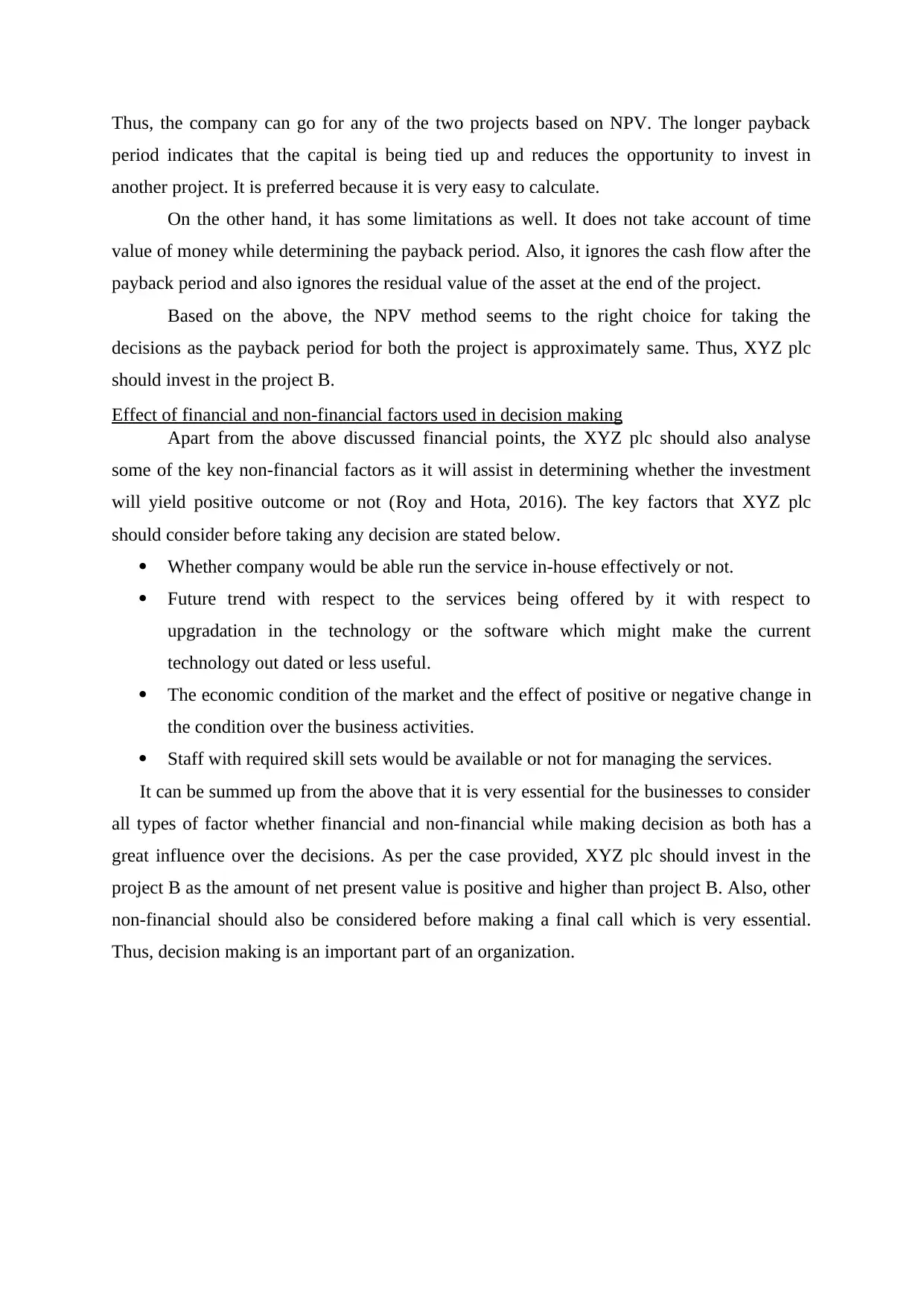

This report provides a detailed financial analysis of investment proposals for XYZ plc, focusing on determining project profitability. The analysis utilizes two primary investment appraisal techniques: Net Present Value (NPV) and Payback Period. The NPV method is employed to assess the present value of future cash inflows against the initial investment for two projects, Project A and Project B, and the results are interpreted to guide the investment decision. The payback period is calculated to determine the time required to recover the initial investment for both projects. The report then discusses the advantages and disadvantages of each method, providing a comparative analysis to support the final investment recommendation. Furthermore, the report extends beyond financial metrics, emphasizing the importance of considering non-financial factors such as operational feasibility, technological trends, market conditions, and availability of skilled staff. The conclusion recommends Project B as the preferred investment based on the financial analysis and the consideration of other key factors. The report underscores the significance of a comprehensive approach to investment decision-making within XYZ plc.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.