Finance Report: Investment Portfolio Analysis and Valuation Techniques

VerifiedAdded on 2021/02/18

|9

|2160

|84

Report

AI Summary

This finance report analyzes the Charlotte Lynch case, focusing on investment portfolio analysis and valuation techniques. It calculates the expected rate of return and standard deviation under different economic scenarios, including rapid expansion, modest growth, no growth, and recession. The report also calculates the risk-reward ratio, compares it to an ideal ratio, and assesses the expected rate of return using the Capital Asset Pricing Model (CAPM). Furthermore, the report examines the downsides of Discounted Cash Flow (DCF) analysis, addressing biased cash flow forecasts and managerial optimism. It discusses adjustments to the DCF formula, the incorporation of country risk premiums, and the importance of considering both temporary and permanent downsides in cash flow projections. The report concludes by recommending a two-part valuation approach for projects with downsides, where the base cash flows are discounted at the cost of capital, and variations between downside and base forecasts are addressed separately.

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................1

1. Calculate Expected rate of return and standard deviation.......................................................1

Standard deviation.......................................................................................................................1

2. Calculation of Risk to reward ratio as measurement of risk...................................................2

3. Calculation of expected rate of return with context of Capital asset pricing model...............2

Downsides and DCF: Valuing Biased Cash flow forecasts........................................................3

REFERENCES................................................................................................................................6

EXECUTIVE SUMMARY.............................................................................................................1

1. Calculate Expected rate of return and standard deviation.......................................................1

Standard deviation.......................................................................................................................1

2. Calculation of Risk to reward ratio as measurement of risk...................................................2

3. Calculation of expected rate of return with context of Capital asset pricing model...............2

Downsides and DCF: Valuing Biased Cash flow forecasts........................................................3

REFERENCES................................................................................................................................6

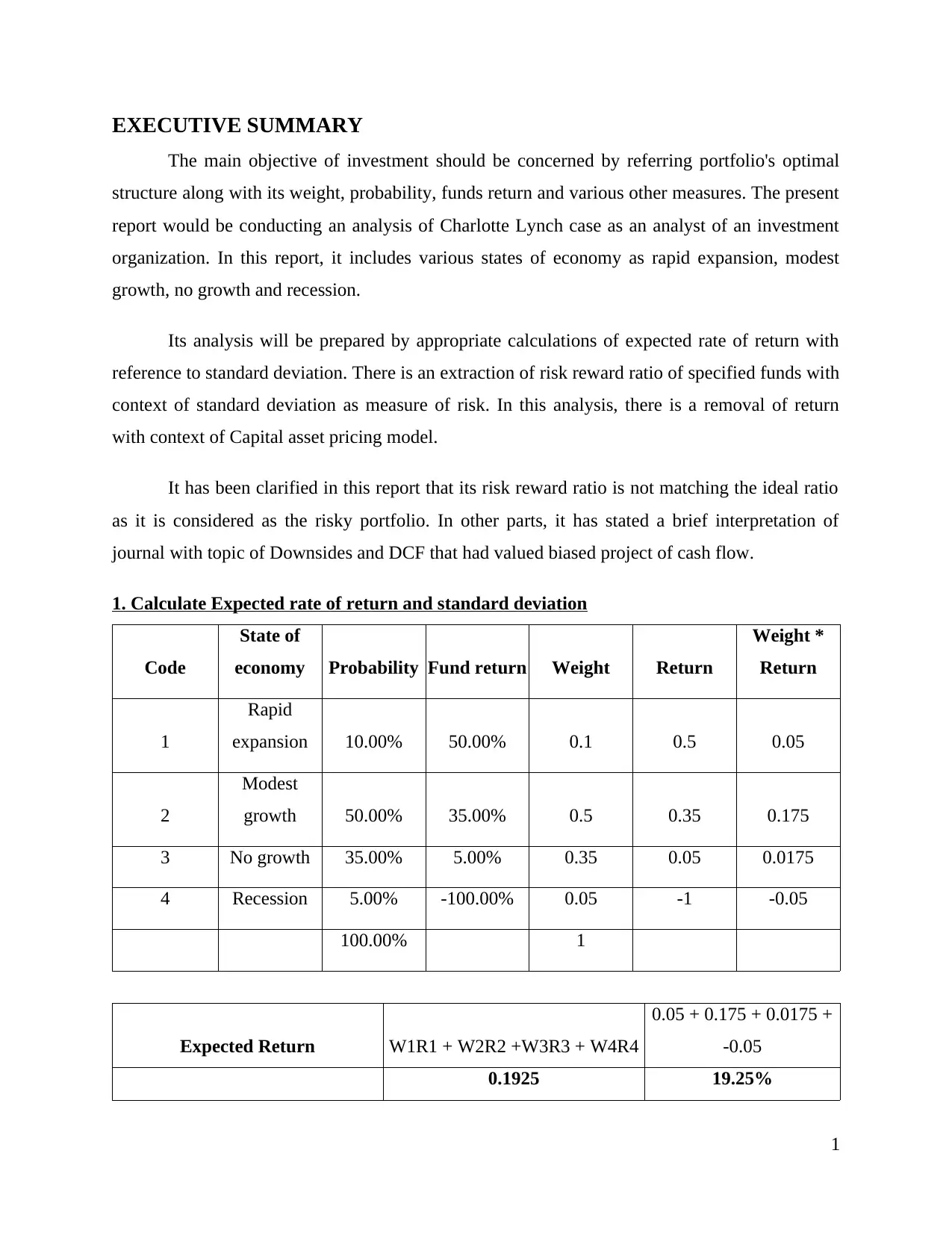

EXECUTIVE SUMMARY

The main objective of investment should be concerned by referring portfolio's optimal

structure along with its weight, probability, funds return and various other measures. The present

report would be conducting an analysis of Charlotte Lynch case as an analyst of an investment

organization. In this report, it includes various states of economy as rapid expansion, modest

growth, no growth and recession.

Its analysis will be prepared by appropriate calculations of expected rate of return with

reference to standard deviation. There is an extraction of risk reward ratio of specified funds with

context of standard deviation as measure of risk. In this analysis, there is a removal of return

with context of Capital asset pricing model.

It has been clarified in this report that its risk reward ratio is not matching the ideal ratio

as it is considered as the risky portfolio. In other parts, it has stated a brief interpretation of

journal with topic of Downsides and DCF that had valued biased project of cash flow.

1. Calculate Expected rate of return and standard deviation

Code

State of

economy Probability Fund return Weight Return

Weight *

Return

1

Rapid

expansion 10.00% 50.00% 0.1 0.5 0.05

2

Modest

growth 50.00% 35.00% 0.5 0.35 0.175

3 No growth 35.00% 5.00% 0.35 0.05 0.0175

4 Recession 5.00% -100.00% 0.05 -1 -0.05

100.00% 1

Expected Return W1R1 + W2R2 +W3R3 + W4R4

0.05 + 0.175 + 0.0175 +

-0.05

0.1925 19.25%

1

The main objective of investment should be concerned by referring portfolio's optimal

structure along with its weight, probability, funds return and various other measures. The present

report would be conducting an analysis of Charlotte Lynch case as an analyst of an investment

organization. In this report, it includes various states of economy as rapid expansion, modest

growth, no growth and recession.

Its analysis will be prepared by appropriate calculations of expected rate of return with

reference to standard deviation. There is an extraction of risk reward ratio of specified funds with

context of standard deviation as measure of risk. In this analysis, there is a removal of return

with context of Capital asset pricing model.

It has been clarified in this report that its risk reward ratio is not matching the ideal ratio

as it is considered as the risky portfolio. In other parts, it has stated a brief interpretation of

journal with topic of Downsides and DCF that had valued biased project of cash flow.

1. Calculate Expected rate of return and standard deviation

Code

State of

economy Probability Fund return Weight Return

Weight *

Return

1

Rapid

expansion 10.00% 50.00% 0.1 0.5 0.05

2

Modest

growth 50.00% 35.00% 0.5 0.35 0.175

3 No growth 35.00% 5.00% 0.35 0.05 0.0175

4 Recession 5.00% -100.00% 0.05 -1 -0.05

100.00% 1

Expected Return W1R1 + W2R2 +W3R3 + W4R4

0.05 + 0.175 + 0.0175 +

-0.05

0.1925 19.25%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard deviation

Standard Deviation

State of economy Probability Fund return Expected return

Rapid expansion 10.00% 50.00% 0.05

Modest growth 50.00% 35.00% 0.175

No growth 35.00% 5.00% 0.0175

Variance

Rapid expansion 0

Modest growth 0.012403125

No growth 0.0071071875

0.0203659375 2.04%

Standard Deviation 0.1427092762 14.27%

2. Calculation of Risk to reward ratio as measurement of risk

Risk Reward

(Standard deviation) / (Portfolio return – Risk

Free)

(14.27%) / (19.25% - 4.50%) 0.96

3. Calculation of expected rate of return with context of Capital asset pricing model

Given

Risk free rate 4.50%

Market risk premium 5.50%

Beta 3.55

Capital Asset pricing Model Rf + B (Rm - Rf)

8.05%

2

Standard Deviation

State of economy Probability Fund return Expected return

Rapid expansion 10.00% 50.00% 0.05

Modest growth 50.00% 35.00% 0.175

No growth 35.00% 5.00% 0.0175

Variance

Rapid expansion 0

Modest growth 0.012403125

No growth 0.0071071875

0.0203659375 2.04%

Standard Deviation 0.1427092762 14.27%

2. Calculation of Risk to reward ratio as measurement of risk

Risk Reward

(Standard deviation) / (Portfolio return – Risk

Free)

(14.27%) / (19.25% - 4.50%) 0.96

3. Calculation of expected rate of return with context of Capital asset pricing model

Given

Risk free rate 4.50%

Market risk premium 5.50%

Beta 3.55

Capital Asset pricing Model Rf + B (Rm - Rf)

8.05%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expected rate of return is considered as loss or profit which has been anticipated with

context of investment and is referred as expected rate of return. It is used for measuring

probabilities which had been intended to reflect likelihood of specified investment as it is

generating positive return of 19.25%. The highest probability that had been gained through

modest growth with reference to the state of economy but huge returns are given by Rapid

Expansion (state of economy).

For further analysis, its standard deviation and variance had been extracted as it measures

volatility of specified investment. It is considered as historical volatility from investor’s

perspective for gauging appropriate amount (Standard deviation, 2015). The standard deviation

of investment is 14.27% with expected return of 19.25%.

In the same series, it had been justified about Sharpe or risk reward ratio of 0.96 with risk

free rate of 4.50% as its portfolio return as 19.25%. It offers measurement of gains which are

against predictable investment as it is against risk of loss. But in this scenario, it is not acceptable

as it has not achieved till 1: 1 or 2: 1 (twice return). While, analysing return via Capital asset

pricing model it is extracted as 8.05% by considering market premium as 5.50% (Expected rate

of return, 2018).

Downsides and DCF: Valuing Biased Cash flow forecasts

DCF Analysis is a tool that is used widely in the finance sector for analysis of the

discounted and the expected cash flow; this has the forecasting property to manage financial

matters of any company.

The method of discounted cash flow highly relies on expected cash. In various events of

downside with low probability, it had been avoided so projection of anticipated cash flow had

been delivered via analysts and corporate managers towards positive and biased results. These

particular forecasts should be modified with its implication of valuations in its outcome.

In the same series, various organizations counter managerial optimism with context of

sources for upward bias for application of cash flow which is extracted from projects of past for

altering projections of the same.

This journal is laying focus on DCF model which could be adopted for projecting value

of cash flow along with various measures of bias on upward side with expected cash flows. The

formula of DCF had been altered with practice for involvement of increment in discounted rate

of DCF. In this investment, there are various assumptions which are assessed via terminal value

3

context of investment and is referred as expected rate of return. It is used for measuring

probabilities which had been intended to reflect likelihood of specified investment as it is

generating positive return of 19.25%. The highest probability that had been gained through

modest growth with reference to the state of economy but huge returns are given by Rapid

Expansion (state of economy).

For further analysis, its standard deviation and variance had been extracted as it measures

volatility of specified investment. It is considered as historical volatility from investor’s

perspective for gauging appropriate amount (Standard deviation, 2015). The standard deviation

of investment is 14.27% with expected return of 19.25%.

In the same series, it had been justified about Sharpe or risk reward ratio of 0.96 with risk

free rate of 4.50% as its portfolio return as 19.25%. It offers measurement of gains which are

against predictable investment as it is against risk of loss. But in this scenario, it is not acceptable

as it has not achieved till 1: 1 or 2: 1 (twice return). While, analysing return via Capital asset

pricing model it is extracted as 8.05% by considering market premium as 5.50% (Expected rate

of return, 2018).

Downsides and DCF: Valuing Biased Cash flow forecasts

DCF Analysis is a tool that is used widely in the finance sector for analysis of the

discounted and the expected cash flow; this has the forecasting property to manage financial

matters of any company.

The method of discounted cash flow highly relies on expected cash. In various events of

downside with low probability, it had been avoided so projection of anticipated cash flow had

been delivered via analysts and corporate managers towards positive and biased results. These

particular forecasts should be modified with its implication of valuations in its outcome.

In the same series, various organizations counter managerial optimism with context of

sources for upward bias for application of cash flow which is extracted from projects of past for

altering projections of the same.

This journal is laying focus on DCF model which could be adopted for projecting value

of cash flow along with various measures of bias on upward side with expected cash flows. The

formula of DCF had been altered with practice for involvement of increment in discounted rate

of DCF. In this investment, there are various assumptions which are assessed via terminal value

3

and this activity must be accomplished for attaining achievement in approximation. The risk

related to failure is directly implicated in rate of discount whose range is between 35% to 80%,

along with decrement in these rates due to advancement of project with its stages of

development.

The valuation with context to international organizations or projects consider country risk

premium, along with link to discounted rate. It could be justified as method for altering with

context to inflation which is expected as it might be reflected in other aspects for tendency of

underestimating systematic risk.

In this specific scenario, interpretation of various discounted rates along with function of

adjustments for projection of cash flow that consists of biases on upward aspect due to outcomes

in positive standards. It could be easily acceptable with application of premium of country risk

for changing all expected cash flow to avoid the downside scenarios with reference to political

risk such as huge taxes and different expropriation form.

Generally, low probability had been avoided for downside events for predicting in

positive aspect. There is huge requirement for altering its forecasts for the purpose of extracting

and using for valuation aspect. These specific downsides are accounted through practitioners for

increment of rate of discount which is beyond cost of capital on basis of market; as on its

contrary, various academics have given huge preference to alteration in projecting cash flow for

their own basis.

In this article, it had been articulated about proper adjustment with context to formula of

DCF which is highly dependent on nature which had excluded downside. When there is adoption

of assumption for eliminating downside on temporary aspects as in large activity, loss due to

weather and proper adjustment with context of formula of DCF for declining projection via

expected downside and discounted rate that had been set for market-based cost of capital in

balanced format.

Usually, if scenario of elimination of downside is considered as permanent with context

of cash flow, which is subsequent and is not expected for recovering on event of occurrence of

downside. In this journal, there is an interpretation with various examples, and along with, its

application for adjusting DCF with context of downside on temporary aspects as for forecasting

with its specific assumptions. There is presence of different projects which might eliminate

4

related to failure is directly implicated in rate of discount whose range is between 35% to 80%,

along with decrement in these rates due to advancement of project with its stages of

development.

The valuation with context to international organizations or projects consider country risk

premium, along with link to discounted rate. It could be justified as method for altering with

context to inflation which is expected as it might be reflected in other aspects for tendency of

underestimating systematic risk.

In this specific scenario, interpretation of various discounted rates along with function of

adjustments for projection of cash flow that consists of biases on upward aspect due to outcomes

in positive standards. It could be easily acceptable with application of premium of country risk

for changing all expected cash flow to avoid the downside scenarios with reference to political

risk such as huge taxes and different expropriation form.

Generally, low probability had been avoided for downside events for predicting in

positive aspect. There is huge requirement for altering its forecasts for the purpose of extracting

and using for valuation aspect. These specific downsides are accounted through practitioners for

increment of rate of discount which is beyond cost of capital on basis of market; as on its

contrary, various academics have given huge preference to alteration in projecting cash flow for

their own basis.

In this article, it had been articulated about proper adjustment with context to formula of

DCF which is highly dependent on nature which had excluded downside. When there is adoption

of assumption for eliminating downside on temporary aspects as in large activity, loss due to

weather and proper adjustment with context of formula of DCF for declining projection via

expected downside and discounted rate that had been set for market-based cost of capital in

balanced format.

Usually, if scenario of elimination of downside is considered as permanent with context

of cash flow, which is subsequent and is not expected for recovering on event of occurrence of

downside. In this journal, there is an interpretation with various examples, and along with, its

application for adjusting DCF with context of downside on temporary aspects as for forecasting

with its specific assumptions. There is presence of different projects which might eliminate

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

downside as it is permanent along with absence or little prospect with reference of recovery due

to occurrence of downside.

In the same series, example of organizations for venture capital must avoid probability of

catastrophic failure with context of technology, where is absence of subsequent cash flow. In this

series, project would be valued for altering DCF with permanent rate of discount of downside for

projecting success times of technology's probability with reference to discounting rate which

equalise its aggregate of cost of capital along with probability of failure of technology.

Generally, it had forecasted about eliminating downside which is not matching with

permanent or downside model. During this occurrence, the first choice is with reference to

extract variances among values of cash flow which is forecasted and expected as it helps in

deriving formula of DCF adjustments that is directly matching to models.

For instance, the first model helps in projecting elimination of occurrence of downside

which directly alters probability for attaining projected cash flow. In the same series, there are

numerous examples which are considered fit to this specific criteria of hybrid downside and they

consist of labour strike as there is always subsequent cash flows which is decreased to higher

wages.

The outcome of formula of DCF which is adjusted along with value of cash flow as it is

discounted through cost of capital and difference had been added among expected value for

forecasting downside cash flows through rate which consist of capital’s cost and chances for

occurring of downside. In this similar aspect, adjustments for upward for discounted rate which

is applied to specific proportion of the forecasted cash flow.

In the same series, approaches of two parts for valuation aspect might provide general

approach for valuation of projected cash flow in an optimistic aspect. For instance, if any

manager is providing valuation to project which consists of downside in conservative aspect and

projecting base in very optimistic view. In this scenario, manager must be inclined for following

existing practice and projecting value of forecasts for its uses with application for rate of

discounts which is excess to its cost of capital.

On the basis of this specific journal, it had been recommended that there should be prior

assessment through manager due to occurrence of downside with context of temporary or

permanent aspect. If it is temporary, then there should be adjustment of base cash flows for

projecting downward with probability weighted average and valuation of deflated cash flow with

5

to occurrence of downside.

In the same series, example of organizations for venture capital must avoid probability of

catastrophic failure with context of technology, where is absence of subsequent cash flow. In this

series, project would be valued for altering DCF with permanent rate of discount of downside for

projecting success times of technology's probability with reference to discounting rate which

equalise its aggregate of cost of capital along with probability of failure of technology.

Generally, it had forecasted about eliminating downside which is not matching with

permanent or downside model. During this occurrence, the first choice is with reference to

extract variances among values of cash flow which is forecasted and expected as it helps in

deriving formula of DCF adjustments that is directly matching to models.

For instance, the first model helps in projecting elimination of occurrence of downside

which directly alters probability for attaining projected cash flow. In the same series, there are

numerous examples which are considered fit to this specific criteria of hybrid downside and they

consist of labour strike as there is always subsequent cash flows which is decreased to higher

wages.

The outcome of formula of DCF which is adjusted along with value of cash flow as it is

discounted through cost of capital and difference had been added among expected value for

forecasting downside cash flows through rate which consist of capital’s cost and chances for

occurring of downside. In this similar aspect, adjustments for upward for discounted rate which

is applied to specific proportion of the forecasted cash flow.

In the same series, approaches of two parts for valuation aspect might provide general

approach for valuation of projected cash flow in an optimistic aspect. For instance, if any

manager is providing valuation to project which consists of downside in conservative aspect and

projecting base in very optimistic view. In this scenario, manager must be inclined for following

existing practice and projecting value of forecasts for its uses with application for rate of

discounts which is excess to its cost of capital.

On the basis of this specific journal, it had been recommended that there should be prior

assessment through manager due to occurrence of downside with context of temporary or

permanent aspect. If it is temporary, then there should be adjustment of base cash flows for

projecting downward with probability weighted average and valuation of deflated cash flow with

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

context to cost of capital. However, there is belief of manager that occurrence of downside

would be permanent due to recognition of occurrence of domestic. It should also gain capability

for revealing persistent high confidence with respect to economic environment because of

technological victory with long run viability and effectiveness with reference to project. The

general belief of manager of downside occurrence always gives signals for lowering permanent

cash flow.

Along with this permanent downside, this analysis has indicated that valuation should not

be prepared by manager because of forecasting with context of discounted rate which is inflated.

Rather, the manager must value this specific project as combination of two parts. In its initial

contribution, the cash flows of downside are discounted at specific capital's cost (Ruback, 2011).

With its different aspect, variations among downside and base forecasts that must be

capable at specific rate for discount and should equalise aggregate of its cost of capital along

with chances of occurring of downside. Further, it would be concluded by giving outcomes as

high value for the purpose of better decision and then initial indication of manager had been

followed for simple discounting, as it would be forecasting in an optimistic aspect through a rate

of discount which is inflated.

6

would be permanent due to recognition of occurrence of domestic. It should also gain capability

for revealing persistent high confidence with respect to economic environment because of

technological victory with long run viability and effectiveness with reference to project. The

general belief of manager of downside occurrence always gives signals for lowering permanent

cash flow.

Along with this permanent downside, this analysis has indicated that valuation should not

be prepared by manager because of forecasting with context of discounted rate which is inflated.

Rather, the manager must value this specific project as combination of two parts. In its initial

contribution, the cash flows of downside are discounted at specific capital's cost (Ruback, 2011).

With its different aspect, variations among downside and base forecasts that must be

capable at specific rate for discount and should equalise aggregate of its cost of capital along

with chances of occurring of downside. Further, it would be concluded by giving outcomes as

high value for the purpose of better decision and then initial indication of manager had been

followed for simple discounting, as it would be forecasting in an optimistic aspect through a rate

of discount which is inflated.

6

REFERENCES

Books and Journals

Ruback. S. R., 2011. Journal of Applied Corporate Finance: Downsides and DCF. Vol (23), pp.

Online

Expected rate of return. 2018. [Online]. Available

through:<https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/

expected-return/>

Standard deviation. 2015. [Online]. Available

through:<http://news.morningstar.com/classroom2/course.asp?docid=2927&page=2>

7

Books and Journals

Ruback. S. R., 2011. Journal of Applied Corporate Finance: Downsides and DCF. Vol (23), pp.

Online

Expected rate of return. 2018. [Online]. Available

through:<https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/

expected-return/>

Standard deviation. 2015. [Online]. Available

through:<http://news.morningstar.com/classroom2/course.asp?docid=2927&page=2>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.