Taxation Report: Analysis of Deductions in Partnership and Investment

VerifiedAdded on 2020/05/01

|7

|530

|85

Report

AI Summary

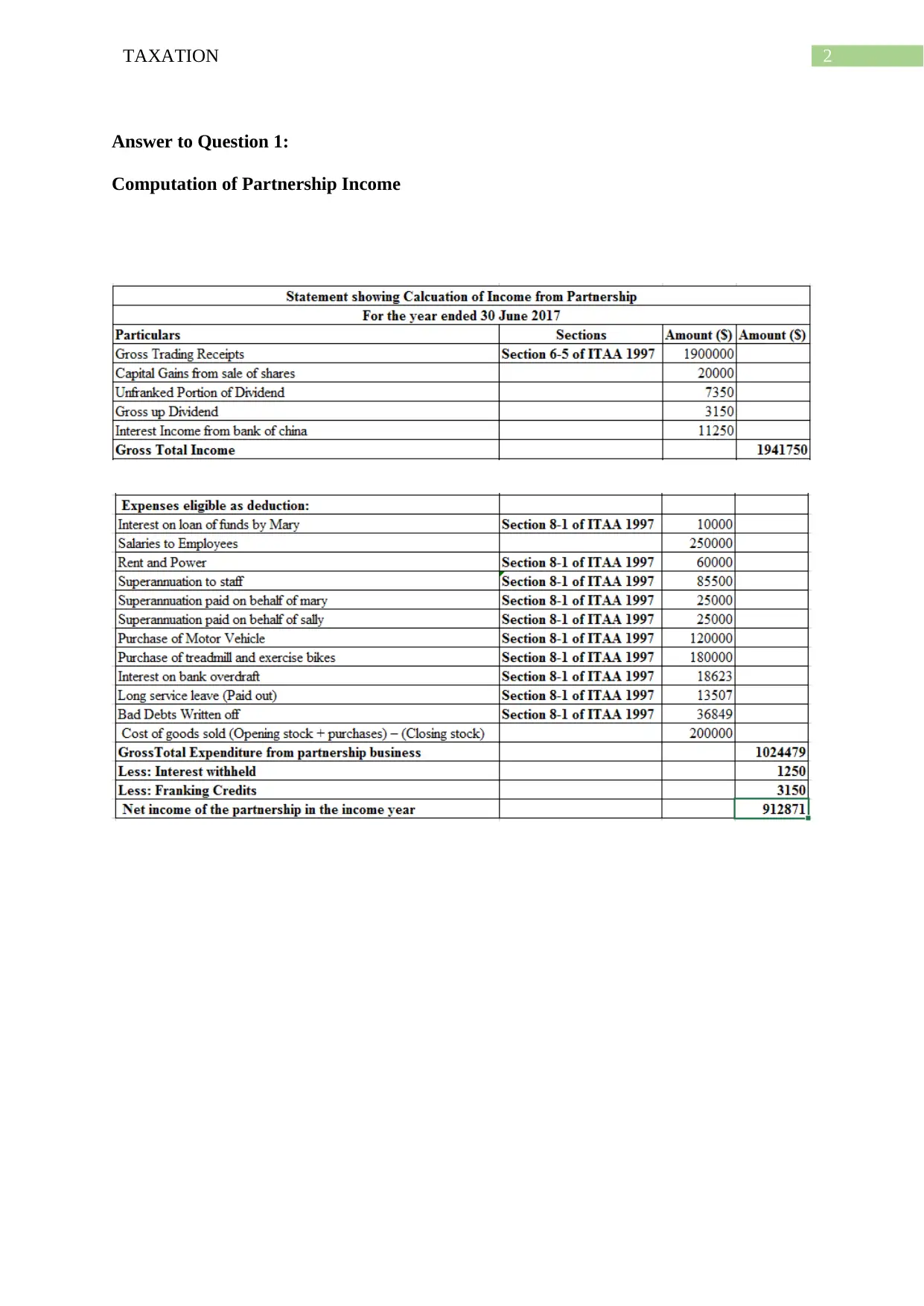

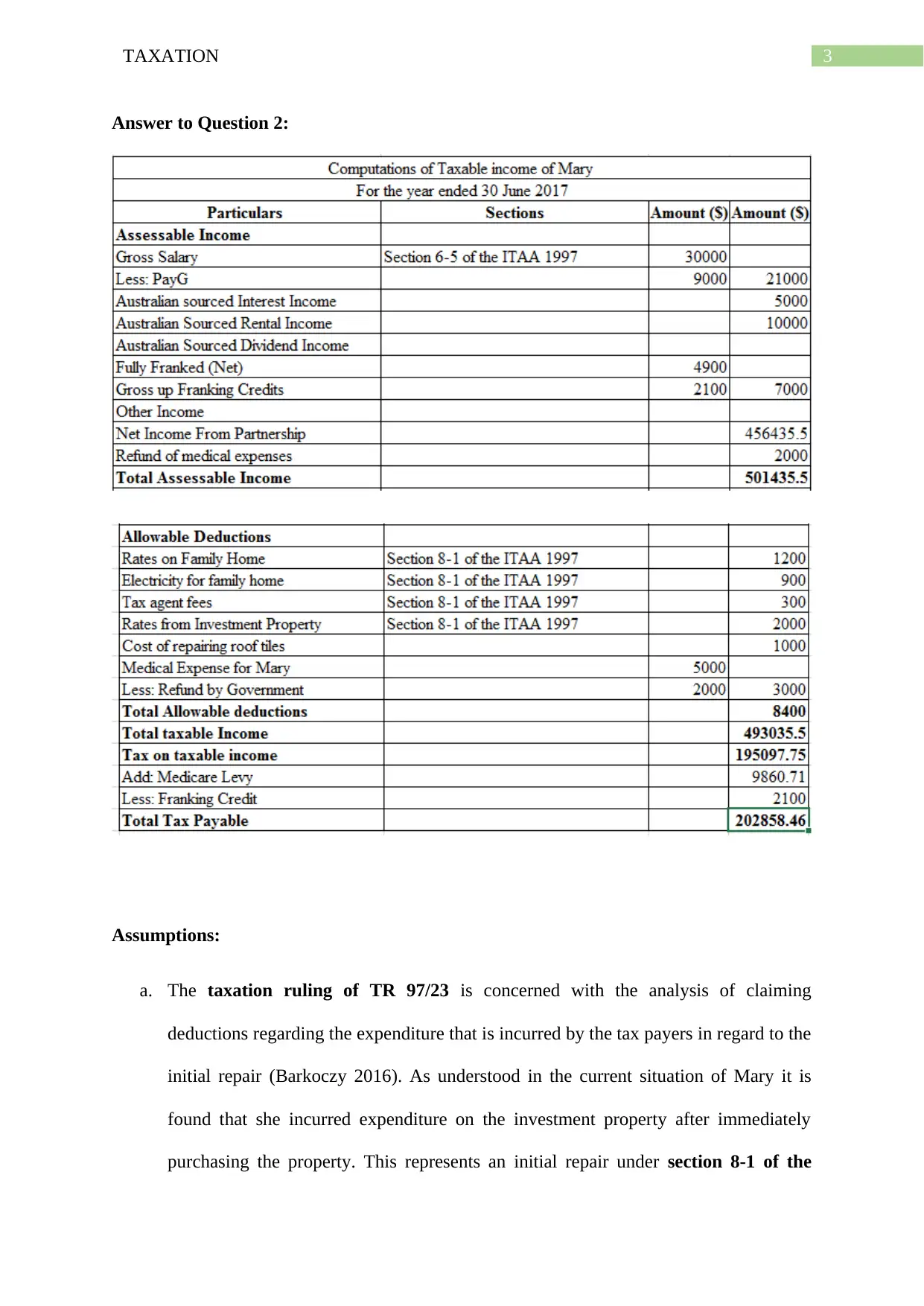

This report, focusing on taxation, provides an analysis of deductions related to investment properties and partnerships. It begins by examining the implications of the taxation ruling TR 97/23, specifically addressing the initial repair of investment properties and the classification of related expenditures, concluding that repainting costs are considered capital expenditure and thus, not allowable deductions. The report then moves on to the taxation ruling of TR 2005/7, discussing the treatment of partnership salaries and their non-deductible status under section 8-1 of the ITAA 1997. Furthermore, the report discusses capital expenditure, such as extending a bathroom in an investment property, referencing section 25-10 (3) of the ITAA 1997 and the Hallstroms Pty Ltd v. FC of T (1946) case, which confirms that expenses incurred to extend a profit-making structure are not deductible. Lastly, the report addresses the non-deductibility of private expenditures, referencing section 51-(1) of the ITAA 1936, by stating that expenses incurred by Mary to maintain her father's bills are not permissible deductions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.