Accounting and Finance Report: Breakeven, Investment Appraisal

VerifiedAdded on 2021/02/21

|18

|3874

|28

Report

AI Summary

This report provides a detailed analysis of accounting and finance principles, focusing on breakeven analysis and investment appraisal techniques. Part A examines an income statement, while Part B delves into breakeven analysis, margin of safety calculations, and profit computations under different sales scenarios. It also explores the assumptions and usefulness of the breakeven model. Part C analyzes capital budgeting techniques, including payback period, net present value (NPV), and average rate of return (ARR), comparing their benefits and limitations. The report includes calculations, interpretations, and working notes to support its findings, offering a comprehensive overview of financial analysis and decision-making. This report is a valuable resource for students studying finance and accounting, with practical implications for business operations and investment strategies.

Accounting and Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION ..........................................................................................................................3

PART A...........................................................................................................................................4

PART B............................................................................................................................................4

A. Calculation of contribution per unit........................................................................................4

B. Evaluation of breakeven analysis and the margin of safety....................................................5

C. calculation of profits if the company produces and sells more number of units at same

selling price per unit.....................................................................................................................5

D Computation of the net profits after increasing the sales units and per unit price...................6

E Identifying and explaining the assumptions of the breakeven analysis model and its

usefulness.....................................................................................................................................6

PART C............................................................................................................................................8

b. Analyzing the benefits and the limitations of the different capital or investment appraisal

technique....................................................................................................................................10

c. Explaining and evaluating the advantages and disadvantages of various planning tools......12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

PART A...........................................................................................................................................4

PART B............................................................................................................................................4

A. Calculation of contribution per unit........................................................................................4

B. Evaluation of breakeven analysis and the margin of safety....................................................5

C. calculation of profits if the company produces and sells more number of units at same

selling price per unit.....................................................................................................................5

D Computation of the net profits after increasing the sales units and per unit price...................6

E Identifying and explaining the assumptions of the breakeven analysis model and its

usefulness.....................................................................................................................................6

PART C............................................................................................................................................8

b. Analyzing the benefits and the limitations of the different capital or investment appraisal

technique....................................................................................................................................10

c. Explaining and evaluating the advantages and disadvantages of various planning tools......12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

The amount of money and the credit invested in the business. It includes the procurement,

allocation and utilization of the funds for smooth functioning of the operations of the

organization is called as accounting and finance. Basically, this report is entirely based on

different aspects of the accounting concepts and the business finance. The study provides the

deep insights on the breakeven analysis and various investment appraisal techniques with their

pros and cons. Furthermore it describes the benefits and the limitations of different budgets.

Several practical implications are also included in the study.

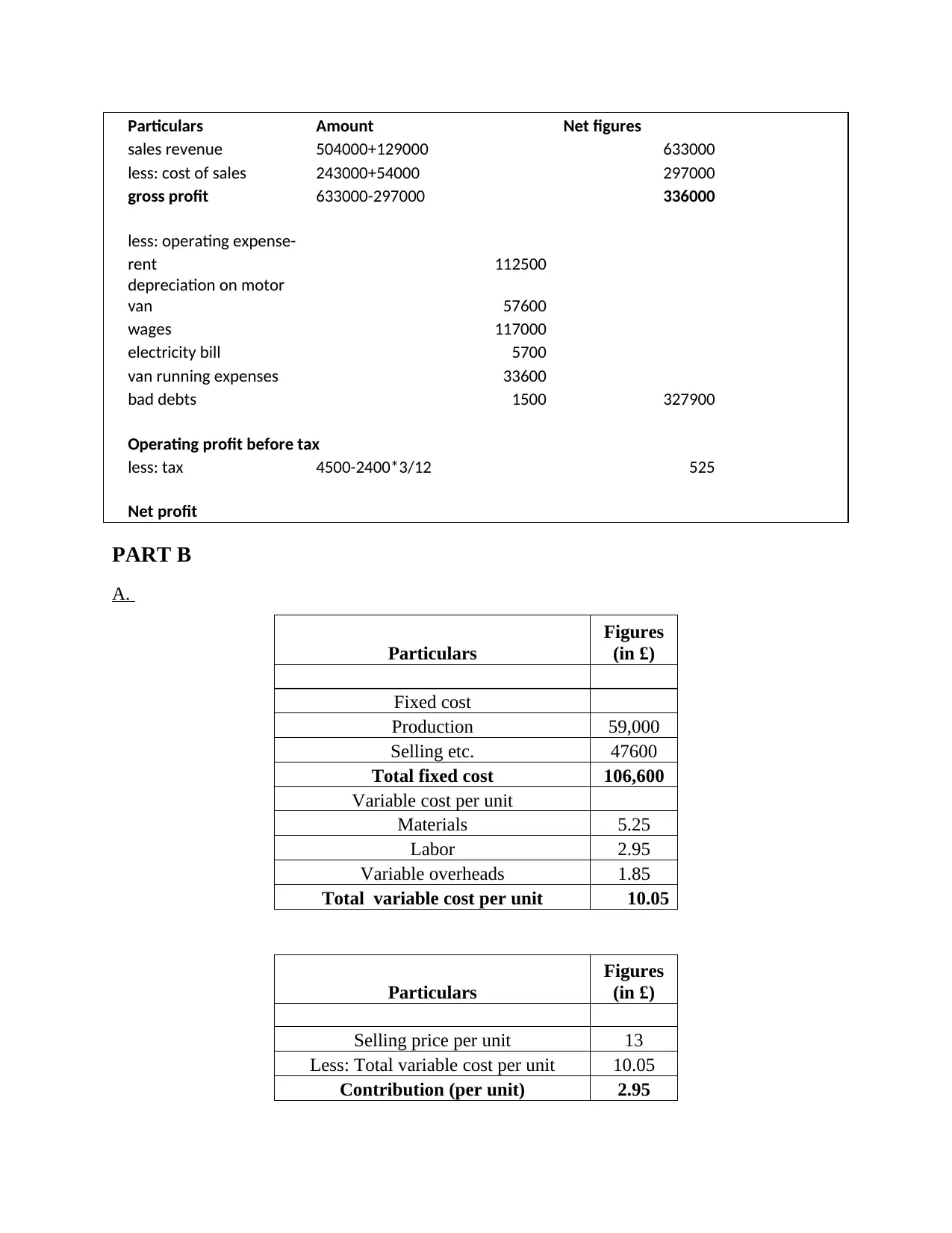

PART A

Dexter Plc

Income statement for the

year ended 31st December

2018

The amount of money and the credit invested in the business. It includes the procurement,

allocation and utilization of the funds for smooth functioning of the operations of the

organization is called as accounting and finance. Basically, this report is entirely based on

different aspects of the accounting concepts and the business finance. The study provides the

deep insights on the breakeven analysis and various investment appraisal techniques with their

pros and cons. Furthermore it describes the benefits and the limitations of different budgets.

Several practical implications are also included in the study.

PART A

Dexter Plc

Income statement for the

year ended 31st December

2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount Net figures

sales revenue 504000+129000 633000

less: cost of sales 243000+54000 297000

gross profit 633000-297000 336000

less: operating expense-

rent 112500

depreciation on motor

van 57600

wages 117000

electricity bill 5700

van running expenses 33600

bad debts 1500 327900

Operating profit before tax

less: tax 4500-2400*3/12 525

Net profit

PART B

A.

Particulars

Figures

(in £)

Fixed cost

Production 59,000

Selling etc. 47600

Total fixed cost 106,600

Variable cost per unit

Materials 5.25

Labor 2.95

Variable overheads 1.85

Total variable cost per unit 10.05

Particulars

Figures

(in £)

Selling price per unit 13

Less: Total variable cost per unit 10.05

Contribution (per unit) 2.95

sales revenue 504000+129000 633000

less: cost of sales 243000+54000 297000

gross profit 633000-297000 336000

less: operating expense-

rent 112500

depreciation on motor

van 57600

wages 117000

electricity bill 5700

van running expenses 33600

bad debts 1500 327900

Operating profit before tax

less: tax 4500-2400*3/12 525

Net profit

PART B

A.

Particulars

Figures

(in £)

Fixed cost

Production 59,000

Selling etc. 47600

Total fixed cost 106,600

Variable cost per unit

Materials 5.25

Labor 2.95

Variable overheads 1.85

Total variable cost per unit 10.05

Particulars

Figures

(in £)

Selling price per unit 13

Less: Total variable cost per unit 10.05

Contribution (per unit) 2.95

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

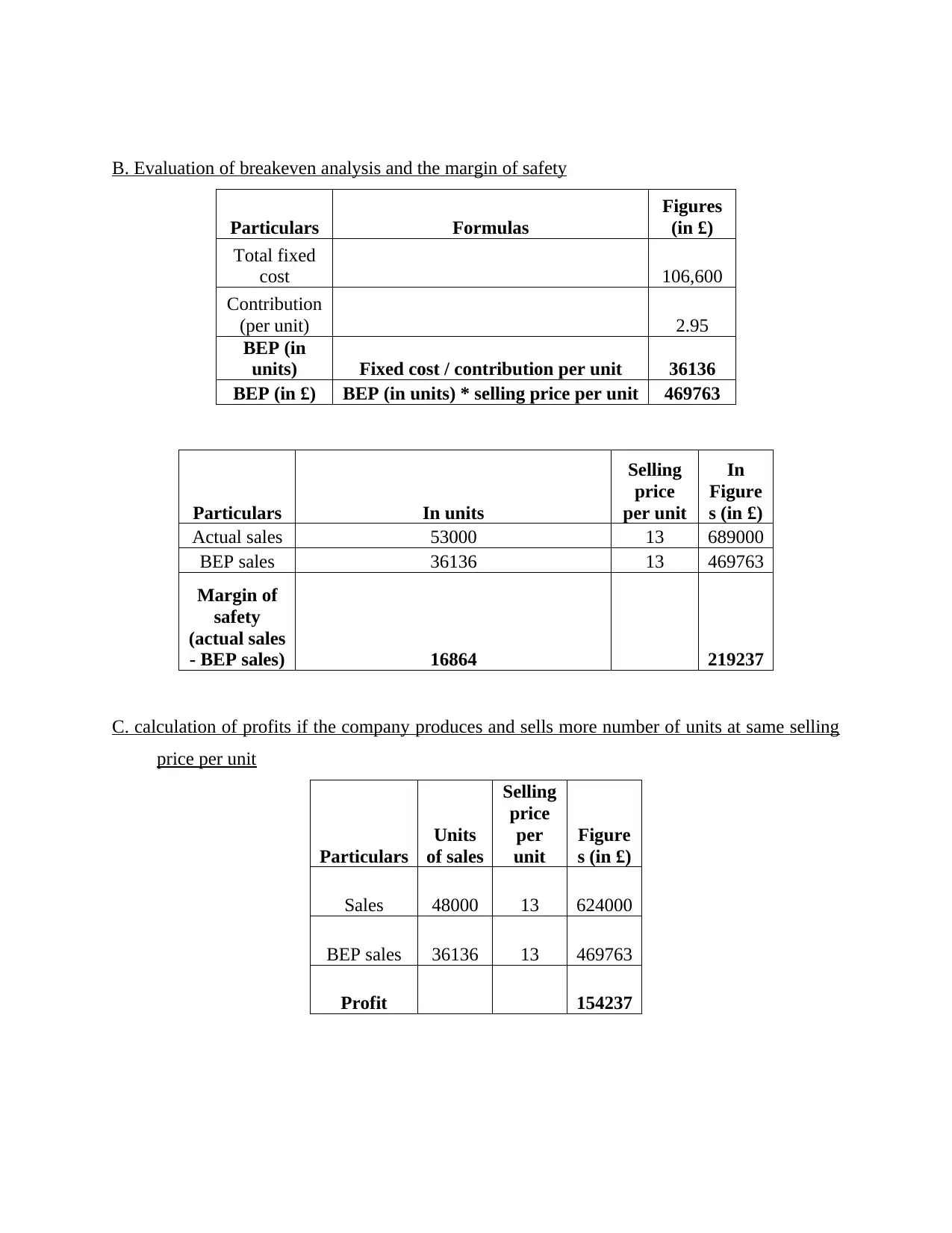

B. Evaluation of breakeven analysis and the margin of safety

Particulars Formulas

Figures

(in £)

Total fixed

cost 106,600

Contribution

(per unit) 2.95

BEP (in

units) Fixed cost / contribution per unit 36136

BEP (in £) BEP (in units) * selling price per unit 469763

Particulars In units

Selling

price

per unit

In

Figure

s (in £)

Actual sales 53000 13 689000

BEP sales 36136 13 469763

Margin of

safety

(actual sales

- BEP sales) 16864 219237

C. calculation of profits if the company produces and sells more number of units at same selling

price per unit

Particulars

Units

of sales

Selling

price

per

unit

Figure

s (in £)

Sales 48000 13 624000

BEP sales 36136 13 469763

Profit 154237

Particulars Formulas

Figures

(in £)

Total fixed

cost 106,600

Contribution

(per unit) 2.95

BEP (in

units) Fixed cost / contribution per unit 36136

BEP (in £) BEP (in units) * selling price per unit 469763

Particulars In units

Selling

price

per unit

In

Figure

s (in £)

Actual sales 53000 13 689000

BEP sales 36136 13 469763

Margin of

safety

(actual sales

- BEP sales) 16864 219237

C. calculation of profits if the company produces and sells more number of units at same selling

price per unit

Particulars

Units

of sales

Selling

price

per

unit

Figure

s (in £)

Sales 48000 13 624000

BEP sales 36136 13 469763

Profit 154237

D Computation of the net profits after increasing the sales units and per unit price

particular

s units

per

price

Amo

unt

Sales 56160 14.17

7957

87.2

variable

cost 56160 10

5616

00

contribution 4.17

less: revised fixed cost

Profits

1891

87.2

Interpretation- From the above analysis it has been analyzed that revised selling price

and the sales unit provides better results of profits after paying off the increased fixed cost

because the margin of the sales increases and the units also rises. Thus, this strategy of Philly

limited is considered as good as it earns higher profits by adopting this strategy.

Working note-

Particulars formula

sell

ing

pri

ce

per

uni

t(ri

ses

by

9

%)

old selling

price 13

Revised

selling

price 13+9% 14.17

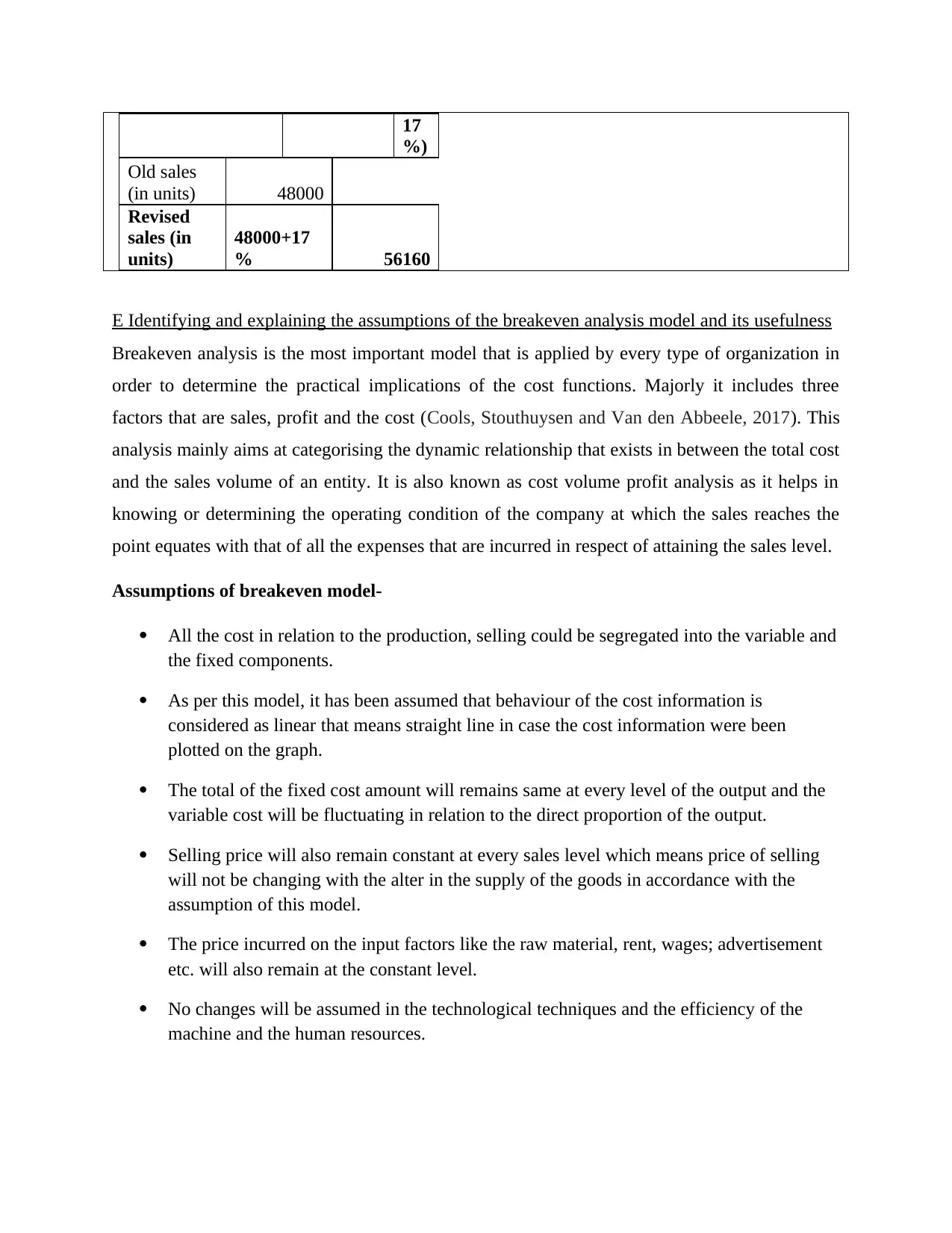

Particulars formula uni

t

sal

es(

rai

sed

by

particular

s units

per

price

Amo

unt

Sales 56160 14.17

7957

87.2

variable

cost 56160 10

5616

00

contribution 4.17

less: revised fixed cost

Profits

1891

87.2

Interpretation- From the above analysis it has been analyzed that revised selling price

and the sales unit provides better results of profits after paying off the increased fixed cost

because the margin of the sales increases and the units also rises. Thus, this strategy of Philly

limited is considered as good as it earns higher profits by adopting this strategy.

Working note-

Particulars formula

sell

ing

pri

ce

per

uni

t(ri

ses

by

9

%)

old selling

price 13

Revised

selling

price 13+9% 14.17

Particulars formula uni

t

sal

es(

rai

sed

by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

17

%)

Old sales

(in units) 48000

Revised

sales (in

units)

48000+17

% 56160

E Identifying and explaining the assumptions of the breakeven analysis model and its usefulness

Breakeven analysis is the most important model that is applied by every type of organization in

order to determine the practical implications of the cost functions. Majorly it includes three

factors that are sales, profit and the cost (Cools, Stouthuysen and Van den Abbeele, 2017). This

analysis mainly aims at categorising the dynamic relationship that exists in between the total cost

and the sales volume of an entity. It is also known as cost volume profit analysis as it helps in

knowing or determining the operating condition of the company at which the sales reaches the

point equates with that of all the expenses that are incurred in respect of attaining the sales level.

Assumptions of breakeven model-

All the cost in relation to the production, selling could be segregated into the variable and

the fixed components.

As per this model, it has been assumed that behaviour of the cost information is

considered as linear that means straight line in case the cost information were been

plotted on the graph.

The total of the fixed cost amount will remains same at every level of the output and the

variable cost will be fluctuating in relation to the direct proportion of the output.

Selling price will also remain constant at every sales level which means price of selling

will not be changing with the alter in the supply of the goods in accordance with the

assumption of this model.

The price incurred on the input factors like the raw material, rent, wages; advertisement

etc. will also remain at the constant level.

No changes will be assumed in the technological techniques and the efficiency of the

machine and the human resources.

%)

Old sales

(in units) 48000

Revised

sales (in

units)

48000+17

% 56160

E Identifying and explaining the assumptions of the breakeven analysis model and its usefulness

Breakeven analysis is the most important model that is applied by every type of organization in

order to determine the practical implications of the cost functions. Majorly it includes three

factors that are sales, profit and the cost (Cools, Stouthuysen and Van den Abbeele, 2017). This

analysis mainly aims at categorising the dynamic relationship that exists in between the total cost

and the sales volume of an entity. It is also known as cost volume profit analysis as it helps in

knowing or determining the operating condition of the company at which the sales reaches the

point equates with that of all the expenses that are incurred in respect of attaining the sales level.

Assumptions of breakeven model-

All the cost in relation to the production, selling could be segregated into the variable and

the fixed components.

As per this model, it has been assumed that behaviour of the cost information is

considered as linear that means straight line in case the cost information were been

plotted on the graph.

The total of the fixed cost amount will remains same at every level of the output and the

variable cost will be fluctuating in relation to the direct proportion of the output.

Selling price will also remain constant at every sales level which means price of selling

will not be changing with the alter in the supply of the goods in accordance with the

assumption of this model.

The price incurred on the input factors like the raw material, rent, wages; advertisement

etc. will also remain at the constant level.

No changes will be assumed in the technological techniques and the efficiency of the

machine and the human resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The model assumes that comparison between the cost and the revenue on the basis of the

common activity (de Campos and Rodrigues, 2016). For instance- sales value of products

and units produced.

Sales volume and the output is been assumed as the relevant factor that affects the cost.

Usefulness of this model in varying business-

It is most useful tool for those businesses has been witnessed with several business decisions and

in dealing with the uncertainty. It enables the manufacturing organization in determining its sales

volume and also in forecasting the profits by anticipating the revenues and the cost (Hazır,

2015). This model assists the enterprise in appraising the changing effects on the sales volume

and the production cost. It helps in making the intra firm comparisons in terms of their

profitability.

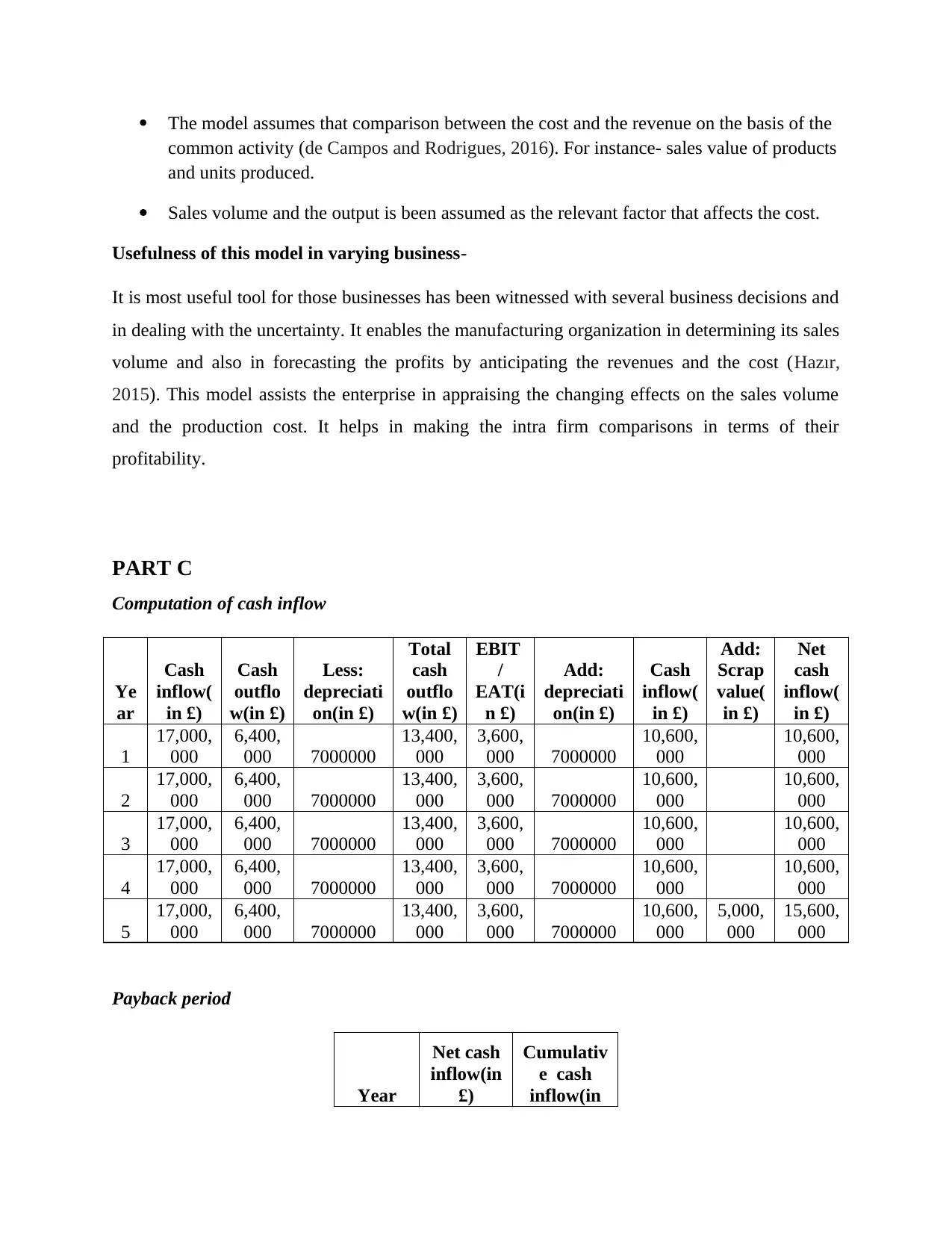

PART C

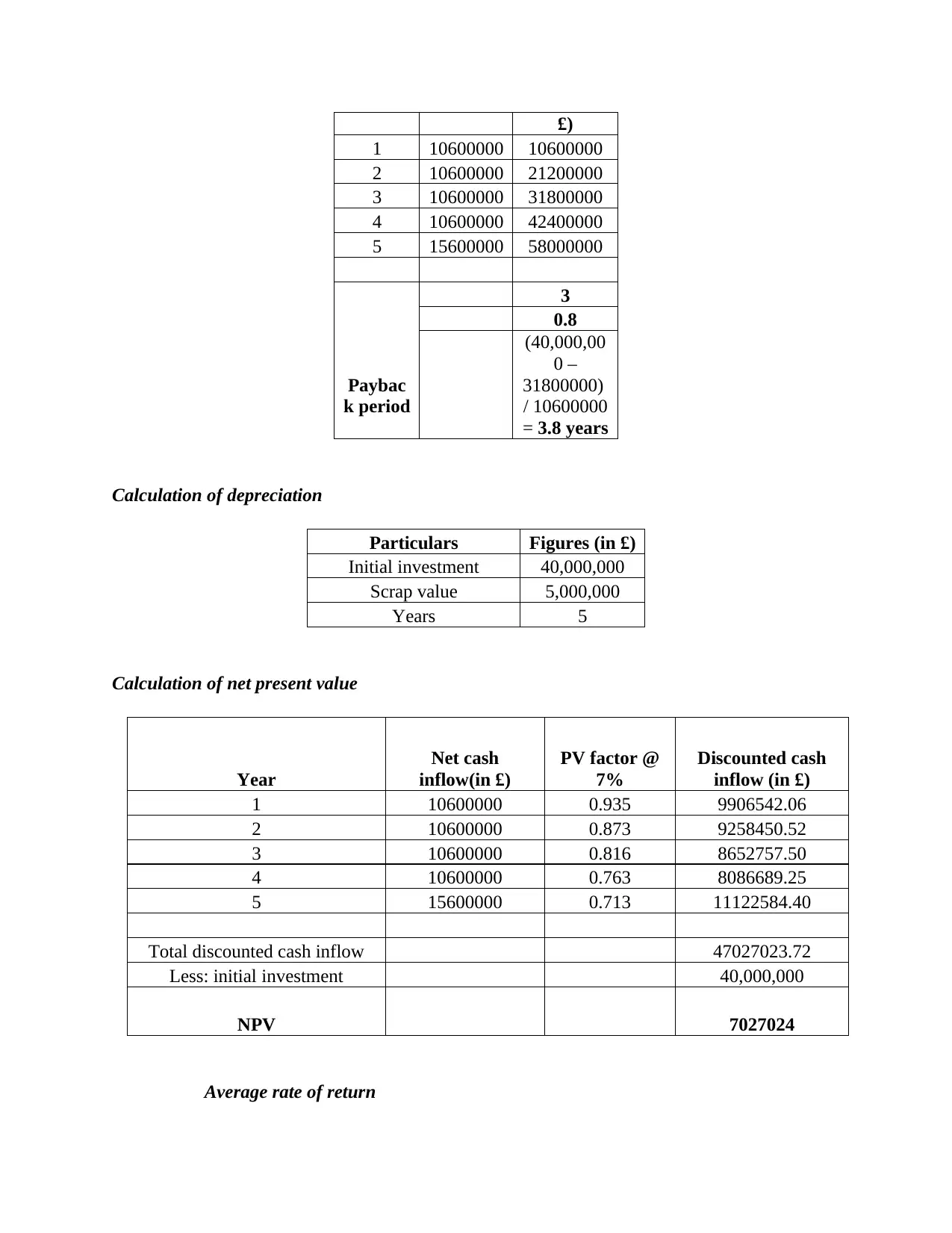

Computation of cash inflow

Ye

ar

Cash

inflow(

in £)

Cash

outflo

w(in £)

Less:

depreciati

on(in £)

Total

cash

outflo

w(in £)

EBIT

/

EAT(i

n £)

Add:

depreciati

on(in £)

Cash

inflow(

in £)

Add:

Scrap

value(

in £)

Net

cash

inflow(

in £)

1

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

2

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

3

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

4

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

5

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

5,000,

000

15,600,

000

Payback period

Year

Net cash

inflow(in

£)

Cumulativ

e cash

inflow(in

common activity (de Campos and Rodrigues, 2016). For instance- sales value of products

and units produced.

Sales volume and the output is been assumed as the relevant factor that affects the cost.

Usefulness of this model in varying business-

It is most useful tool for those businesses has been witnessed with several business decisions and

in dealing with the uncertainty. It enables the manufacturing organization in determining its sales

volume and also in forecasting the profits by anticipating the revenues and the cost (Hazır,

2015). This model assists the enterprise in appraising the changing effects on the sales volume

and the production cost. It helps in making the intra firm comparisons in terms of their

profitability.

PART C

Computation of cash inflow

Ye

ar

Cash

inflow(

in £)

Cash

outflo

w(in £)

Less:

depreciati

on(in £)

Total

cash

outflo

w(in £)

EBIT

/

EAT(i

n £)

Add:

depreciati

on(in £)

Cash

inflow(

in £)

Add:

Scrap

value(

in £)

Net

cash

inflow(

in £)

1

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

2

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

3

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

4

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

10,600,

000

5

17,000,

000

6,400,

000 7000000

13,400,

000

3,600,

000 7000000

10,600,

000

5,000,

000

15,600,

000

Payback period

Year

Net cash

inflow(in

£)

Cumulativ

e cash

inflow(in

£)

1 10600000 10600000

2 10600000 21200000

3 10600000 31800000

4 10600000 42400000

5 15600000 58000000

Paybac

k period

3

0.8

(40,000,00

0 –

31800000)

/ 10600000

= 3.8 years

Calculation of depreciation

Particulars Figures (in £)

Initial investment 40,000,000

Scrap value 5,000,000

Years 5

Calculation of net present value

Year

Net cash

inflow(in £)

PV factor @

7%

Discounted cash

inflow (in £)

1 10600000 0.935 9906542.06

2 10600000 0.873 9258450.52

3 10600000 0.816 8652757.50

4 10600000 0.763 8086689.25

5 15600000 0.713 11122584.40

Total discounted cash inflow 47027023.72

Less: initial investment 40,000,000

NPV 7027024

Average rate of return

1 10600000 10600000

2 10600000 21200000

3 10600000 31800000

4 10600000 42400000

5 15600000 58000000

Paybac

k period

3

0.8

(40,000,00

0 –

31800000)

/ 10600000

= 3.8 years

Calculation of depreciation

Particulars Figures (in £)

Initial investment 40,000,000

Scrap value 5,000,000

Years 5

Calculation of net present value

Year

Net cash

inflow(in £)

PV factor @

7%

Discounted cash

inflow (in £)

1 10600000 0.935 9906542.06

2 10600000 0.873 9258450.52

3 10600000 0.816 8652757.50

4 10600000 0.763 8086689.25

5 15600000 0.713 11122584.40

Total discounted cash inflow 47027023.72

Less: initial investment 40,000,000

NPV 7027024

Average rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

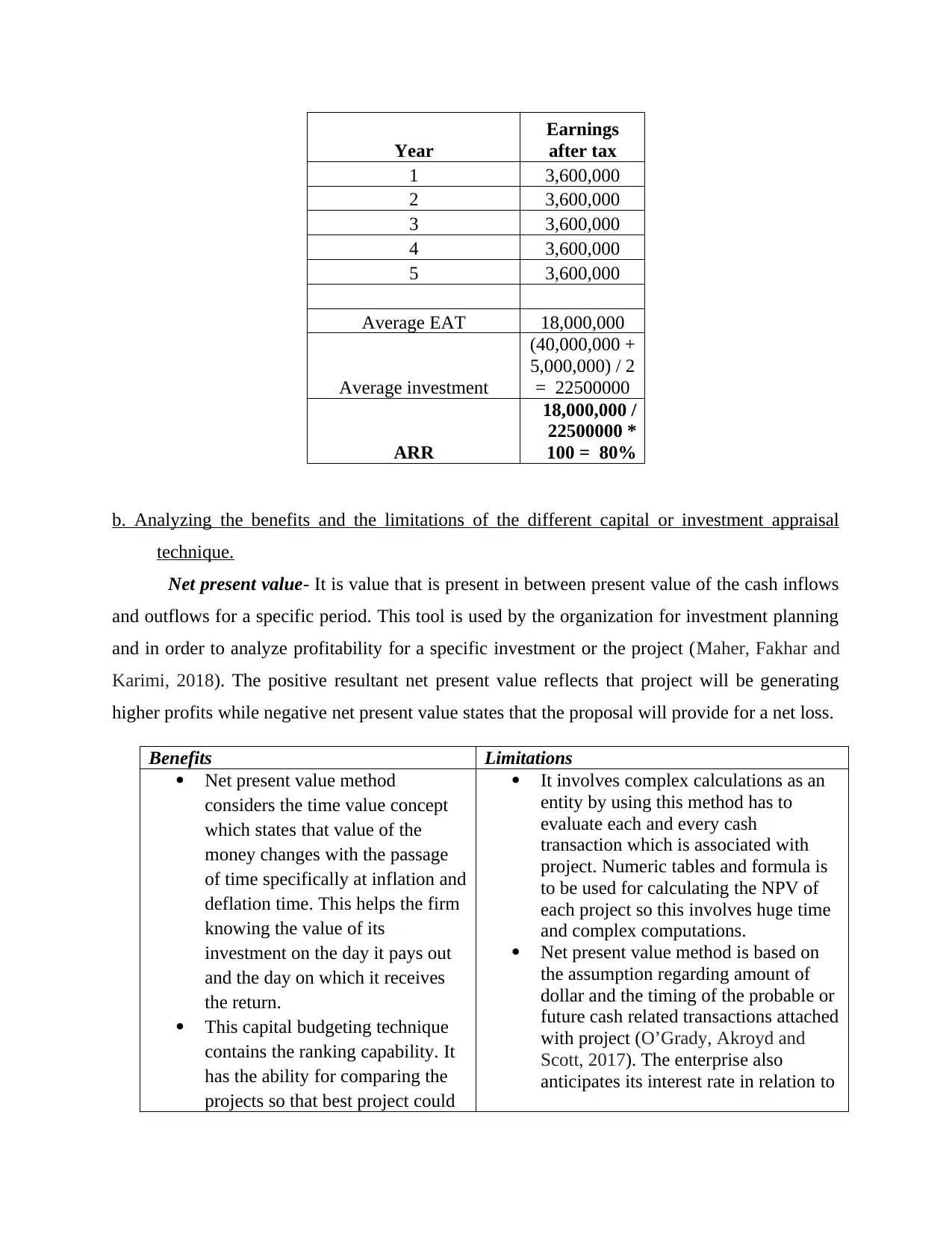

Year

Earnings

after tax

1 3,600,000

2 3,600,000

3 3,600,000

4 3,600,000

5 3,600,000

Average EAT 18,000,000

Average investment

(40,000,000 +

5,000,000) / 2

= 22500000

ARR

18,000,000 /

22500000 *

100 = 80%

b. Analyzing the benefits and the limitations of the different capital or investment appraisal

technique.

Net present value- It is value that is present in between present value of the cash inflows

and outflows for a specific period. This tool is used by the organization for investment planning

and in order to analyze profitability for a specific investment or the project (Maher, Fakhar and

Karimi, 2018). The positive resultant net present value reflects that project will be generating

higher profits while negative net present value states that the proposal will provide for a net loss.

Benefits Limitations

Net present value method

considers the time value concept

which states that value of the

money changes with the passage

of time specifically at inflation and

deflation time. This helps the firm

knowing the value of its

investment on the day it pays out

and the day on which it receives

the return.

This capital budgeting technique

contains the ranking capability. It

has the ability for comparing the

projects so that best project could

It involves complex calculations as an

entity by using this method has to

evaluate each and every cash

transaction which is associated with

project. Numeric tables and formula is

to be used for calculating the NPV of

each project so this involves huge time

and complex computations.

Net present value method is based on

the assumption regarding amount of

dollar and the timing of the probable or

future cash related transactions attached

with project (O’Grady, Akroyd and

Scott, 2017). The enterprise also

anticipates its interest rate in relation to

Earnings

after tax

1 3,600,000

2 3,600,000

3 3,600,000

4 3,600,000

5 3,600,000

Average EAT 18,000,000

Average investment

(40,000,000 +

5,000,000) / 2

= 22500000

ARR

18,000,000 /

22500000 *

100 = 80%

b. Analyzing the benefits and the limitations of the different capital or investment appraisal

technique.

Net present value- It is value that is present in between present value of the cash inflows

and outflows for a specific period. This tool is used by the organization for investment planning

and in order to analyze profitability for a specific investment or the project (Maher, Fakhar and

Karimi, 2018). The positive resultant net present value reflects that project will be generating

higher profits while negative net present value states that the proposal will provide for a net loss.

Benefits Limitations

Net present value method

considers the time value concept

which states that value of the

money changes with the passage

of time specifically at inflation and

deflation time. This helps the firm

knowing the value of its

investment on the day it pays out

and the day on which it receives

the return.

This capital budgeting technique

contains the ranking capability. It

has the ability for comparing the

projects so that best project could

It involves complex calculations as an

entity by using this method has to

evaluate each and every cash

transaction which is associated with

project. Numeric tables and formula is

to be used for calculating the NPV of

each project so this involves huge time

and complex computations.

Net present value method is based on

the assumption regarding amount of

dollar and the timing of the probable or

future cash related transactions attached

with project (O’Grady, Akroyd and

Scott, 2017). The enterprise also

anticipates its interest rate in relation to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be chosen (Mathur, 2019). The

proposal that results highest value

is been viewed as highest yield

will be ascertain to the enterprise.

duration of project. Inaccurate

estimations results in inaccurate

evaluation of NPV for a particular

project which in turn leads to loss for

the company.

Accounting rate of return- It is the appraisal technique that measures annual earnings

and the profits which is been expected to achieve from an investment made. It is also called as

average rate of the return. It helps the investors in analyzing the risk associated with the

investment made and helps in determining that earnings are greater over the acceptance of the

level of risk (Pellerin and Perrier, 2018). It computes the rate of return gained by the investor on

its investments.

Benefits Limitations

This method is simple and easy to

understand as it considers savings or

the total of profits over entire period

for the economic life of project.

Accounting rate of return method

helps in recognizing concept of the

net earnings which is considered as

the vital aspect of the investment

proposal.

It facilitates comparison between the

new product proposal and the cost

reducing proposal or the other

competitive nature projects.

This method provides the clear

picture relating to the profitability

that will be attaining from the

project.

For measuring the current

performance, this method is counted

to be most suitable.

Different results are been evaluated in

respect of the return by applying the

return on investment method and the

ARR. This creates a problem for the

company in making the decision and

develops ambiguity with respect to the

project yield.

Time factor is ignored by this method

as it selects the alternative uses of the

funds which are considered as the

primary weakness of this method.

Average rate of return method does not

take into account the external factors

which has the direct impact on the

profitability of project.

proposal that results highest value

is been viewed as highest yield

will be ascertain to the enterprise.

duration of project. Inaccurate

estimations results in inaccurate

evaluation of NPV for a particular

project which in turn leads to loss for

the company.

Accounting rate of return- It is the appraisal technique that measures annual earnings

and the profits which is been expected to achieve from an investment made. It is also called as

average rate of the return. It helps the investors in analyzing the risk associated with the

investment made and helps in determining that earnings are greater over the acceptance of the

level of risk (Pellerin and Perrier, 2018). It computes the rate of return gained by the investor on

its investments.

Benefits Limitations

This method is simple and easy to

understand as it considers savings or

the total of profits over entire period

for the economic life of project.

Accounting rate of return method

helps in recognizing concept of the

net earnings which is considered as

the vital aspect of the investment

proposal.

It facilitates comparison between the

new product proposal and the cost

reducing proposal or the other

competitive nature projects.

This method provides the clear

picture relating to the profitability

that will be attaining from the

project.

For measuring the current

performance, this method is counted

to be most suitable.

Different results are been evaluated in

respect of the return by applying the

return on investment method and the

ARR. This creates a problem for the

company in making the decision and

develops ambiguity with respect to the

project yield.

Time factor is ignored by this method

as it selects the alternative uses of the

funds which are considered as the

primary weakness of this method.

Average rate of return method does not

take into account the external factors

which has the direct impact on the

profitability of project.

Payback period- It refers to the appraisal tool that states the amount of the time taken for

recovering the cost from an investment. On the other hand, it is the length of time where the

investment reaches the breakeven point. Investment Desirability is directly related to the payback

period (Nemec and de Vries, 2019). Payback period which is small, reflect the more than

investment as more fascinating. This method is used by the company in order to assess the cost

of saving with the application of the energy efficient technology.

Benefits Limitations

Payback period method is the

simplest method as it requires few

inputs and is very easy in

calculating in comparison to other

appraisal methods. This enables the

managers in making quick

decisions.

It is most useful method in the case

of the uncertainty as the projects

with the shorter payback period

assist in reducing the possibility of

the loss due to the obsolescence.

Payback period provides the useful

information relating to the liquidity

of the company which is crucial for

the company having limited

resources. It provides lower risk

which in turn leads to recovery of

the cost for reinvesting into the

other profitable opportunities.

This method of capital budgeting

ignores the time value factor which is

very crucial concept of the business.

This results in distortion of the correct

value of cash flows.

This method fails in considering all the

cash flows and only takes into account

the time in which the initial investment

is been recovered.

Payback period does not consider the

normal scenarios that every business

faces (Nguyen, Weigel and Hiebl,

2018). This leads to an unrealistic

method as it requires further investment

in coming years and have irregular

inflow of cash.

It ignores the evaluation of the

profitability as it does not guarantee

that shorter payback period of the

project will result in earnings.

c. Explaining and evaluating the advantages and disadvantages of various planning tools.

Zero based budget- It refers to the budgets which is used by company to start their

budgets from starting. Thus, the budgets itself named as zero base which means that no profits

are incurred from the previous projects and the expenses which are incurred results to zero. The

main objective of these budgets is to reduce the unnecessary cost which is incurred by the

company at the time of dealing in different department and continue the production activity.

Advantages Disadvantages

It is considered to be most flexible It is the time consuming method as it

recovering the cost from an investment. On the other hand, it is the length of time where the

investment reaches the breakeven point. Investment Desirability is directly related to the payback

period (Nemec and de Vries, 2019). Payback period which is small, reflect the more than

investment as more fascinating. This method is used by the company in order to assess the cost

of saving with the application of the energy efficient technology.

Benefits Limitations

Payback period method is the

simplest method as it requires few

inputs and is very easy in

calculating in comparison to other

appraisal methods. This enables the

managers in making quick

decisions.

It is most useful method in the case

of the uncertainty as the projects

with the shorter payback period

assist in reducing the possibility of

the loss due to the obsolescence.

Payback period provides the useful

information relating to the liquidity

of the company which is crucial for

the company having limited

resources. It provides lower risk

which in turn leads to recovery of

the cost for reinvesting into the

other profitable opportunities.

This method of capital budgeting

ignores the time value factor which is

very crucial concept of the business.

This results in distortion of the correct

value of cash flows.

This method fails in considering all the

cash flows and only takes into account

the time in which the initial investment

is been recovered.

Payback period does not consider the

normal scenarios that every business

faces (Nguyen, Weigel and Hiebl,

2018). This leads to an unrealistic

method as it requires further investment

in coming years and have irregular

inflow of cash.

It ignores the evaluation of the

profitability as it does not guarantee

that shorter payback period of the

project will result in earnings.

c. Explaining and evaluating the advantages and disadvantages of various planning tools.

Zero based budget- It refers to the budgets which is used by company to start their

budgets from starting. Thus, the budgets itself named as zero base which means that no profits

are incurred from the previous projects and the expenses which are incurred results to zero. The

main objective of these budgets is to reduce the unnecessary cost which is incurred by the

company at the time of dealing in different department and continue the production activity.

Advantages Disadvantages

It is considered to be most flexible It is the time consuming method as it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.