Accounting for Managers: Investment Appraisal Methods and Analysis

VerifiedAdded on 2022/12/19

|6

|1278

|77

Homework Assignment

AI Summary

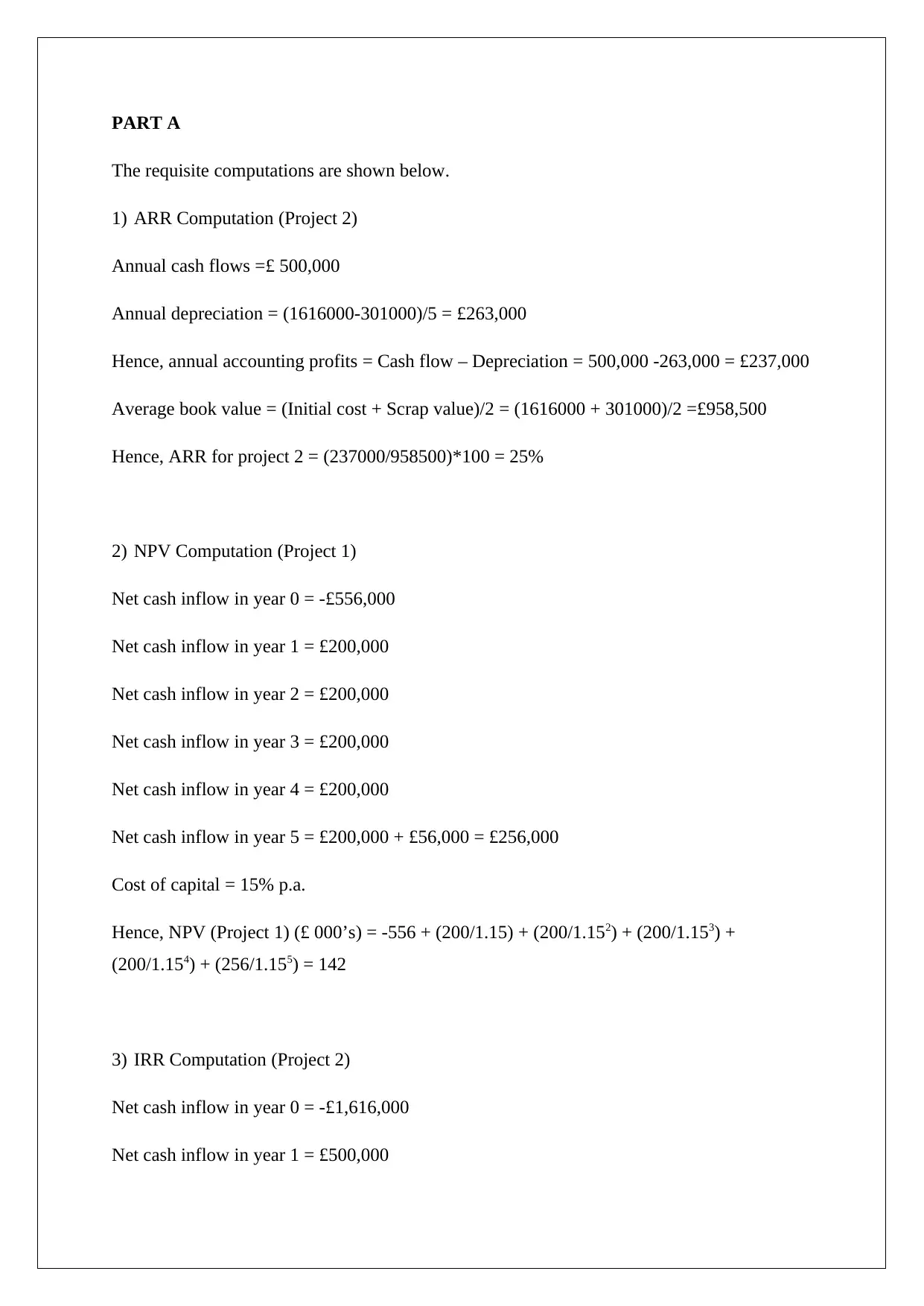

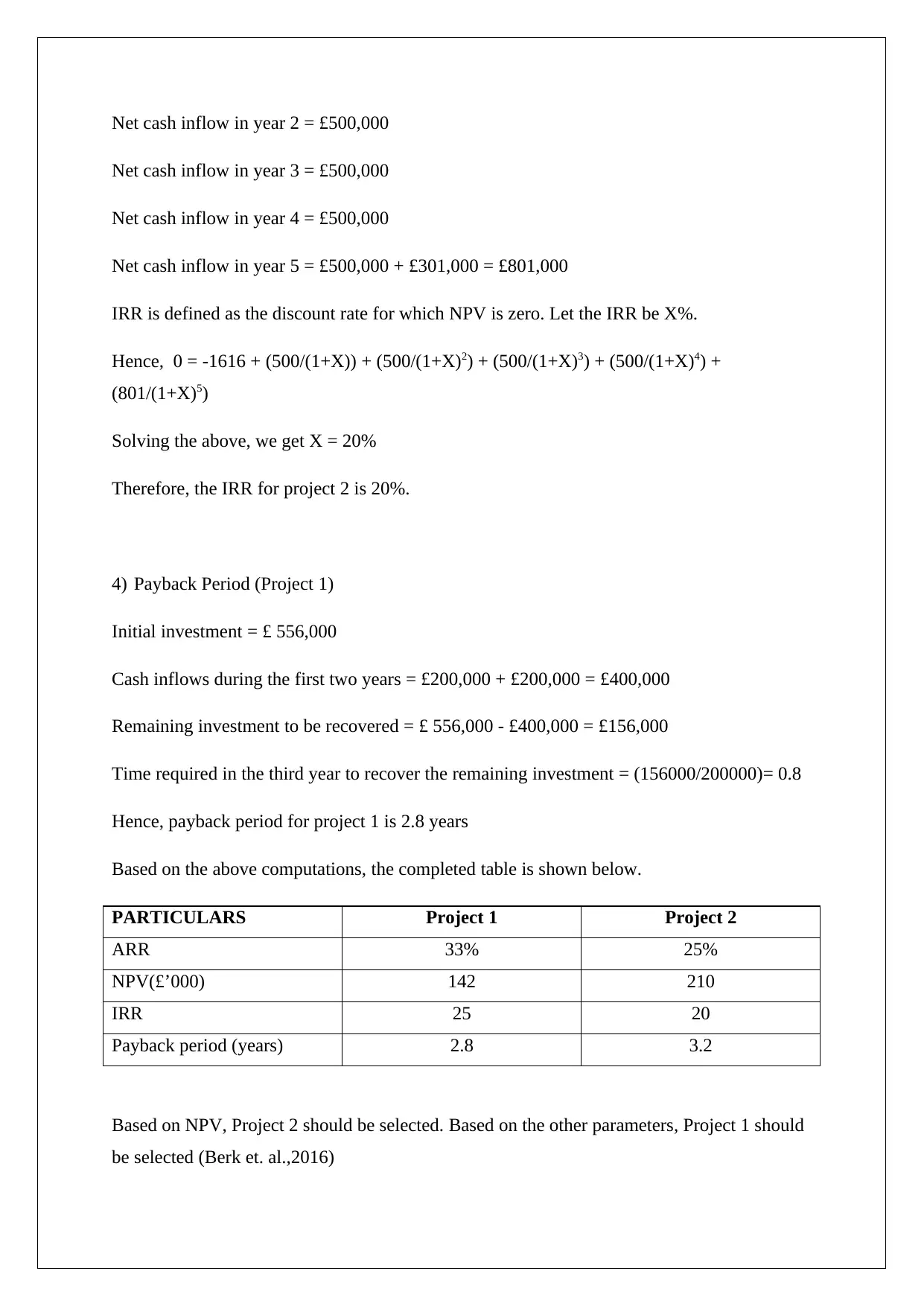

This homework assignment focuses on investment appraisal techniques within the context of accounting for managers. Part A involves detailed computations for two projects, calculating ARR, NPV, IRR, and payback period, and providing a comparative analysis to determine the most financially viable project based on different metrics. Part B delves into a critical discussion of the various investment appraisal methodologies, highlighting the strengths and weaknesses of each, such as NPV, IRR, ARR, and payback period. The assignment also addresses the role of external versus internal expertise in capital budgeting decisions, arguing that while external consultants can provide guidance, the ultimate decision-making responsibility should rest with the company's management due to their superior understanding of the business and its future prospects. The assignment utilizes various financial management references to support its analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.