Student's Investment Policy Statement Workbook for M & S Ford

VerifiedAdded on 2023/02/01

|16

|3980

|67

Project

AI Summary

This investment policy statement workbook, prepared by a student, meticulously analyzes the financial situation of Michel and Susan Ford. It begins with a comprehensive overview of their current financial standing, detailing personal information, assets, liabilities, and current cash flow. The workbook then outlines their financial objectives, including primary and secondary goals, and performs a five-year cash flow analysis. It establishes return and risk objectives, incorporating a risk profile questionnaire to assess their tolerance for investment volatility. Constraints are identified, and a proposed asset allocation strategy is presented. Finally, the document covers portfolio monitoring, review processes, and an action plan to ensure the Fords stay on track with their financial goals. The analysis encompasses various aspects of financial planning, including retirement planning, and guides the development of a suitable investment strategy. The document concludes with an authority to proceed, indicating the steps required for the implementation of the plan.

Investment Policy Statement

Workbook

[Michel & Susan Ford]

5 May 2019

Prepared by[Student]

Student No[sxxxxxxx]

Workbook

[Michel & Susan Ford]

5 May 2019

Prepared by[Student]

Student No[sxxxxxxx]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

◉Current Financial Situation......................................................................................3

Personal details............................................................................................................................................. 3

Assets & Liabilities........................................................................................................................................ 3

Current Cash flow.......................................................................................................................................... 4

◉Financial Objectives................................................................................................ 5

Primary Goals................................................................................................................................................ 5

Secondary Goals........................................................................................................................................... 5

Five Year Cash Flow Analysis......................................................................................................................... 6

Return Objective........................................................................................................................................... 7

Risk Objective............................................................................................................................................... 7

RBS Morgans Risk Profile Questionnaire........................................................................................................ 9

◉Constraints........................................................................................................... 14

◉Proposed Asset Allocation.....................................................................................16

◉Portfolio Monitoring and Review............................................................................16

Action plan.................................................................................................................................................. 16

Staying ‘on target’...................................................................................................................................... 16

Authority to proceed............................................................................................... 17

Investment Policy Statement Workbook for M & S Ford 2

◉Current Financial Situation......................................................................................3

Personal details............................................................................................................................................. 3

Assets & Liabilities........................................................................................................................................ 3

Current Cash flow.......................................................................................................................................... 4

◉Financial Objectives................................................................................................ 5

Primary Goals................................................................................................................................................ 5

Secondary Goals........................................................................................................................................... 5

Five Year Cash Flow Analysis......................................................................................................................... 6

Return Objective........................................................................................................................................... 7

Risk Objective............................................................................................................................................... 7

RBS Morgans Risk Profile Questionnaire........................................................................................................ 9

◉Constraints........................................................................................................... 14

◉Proposed Asset Allocation.....................................................................................16

◉Portfolio Monitoring and Review............................................................................16

Action plan.................................................................................................................................................. 16

Staying ‘on target’...................................................................................................................................... 16

Authority to proceed............................................................................................... 17

Investment Policy Statement Workbook for M & S Ford 2

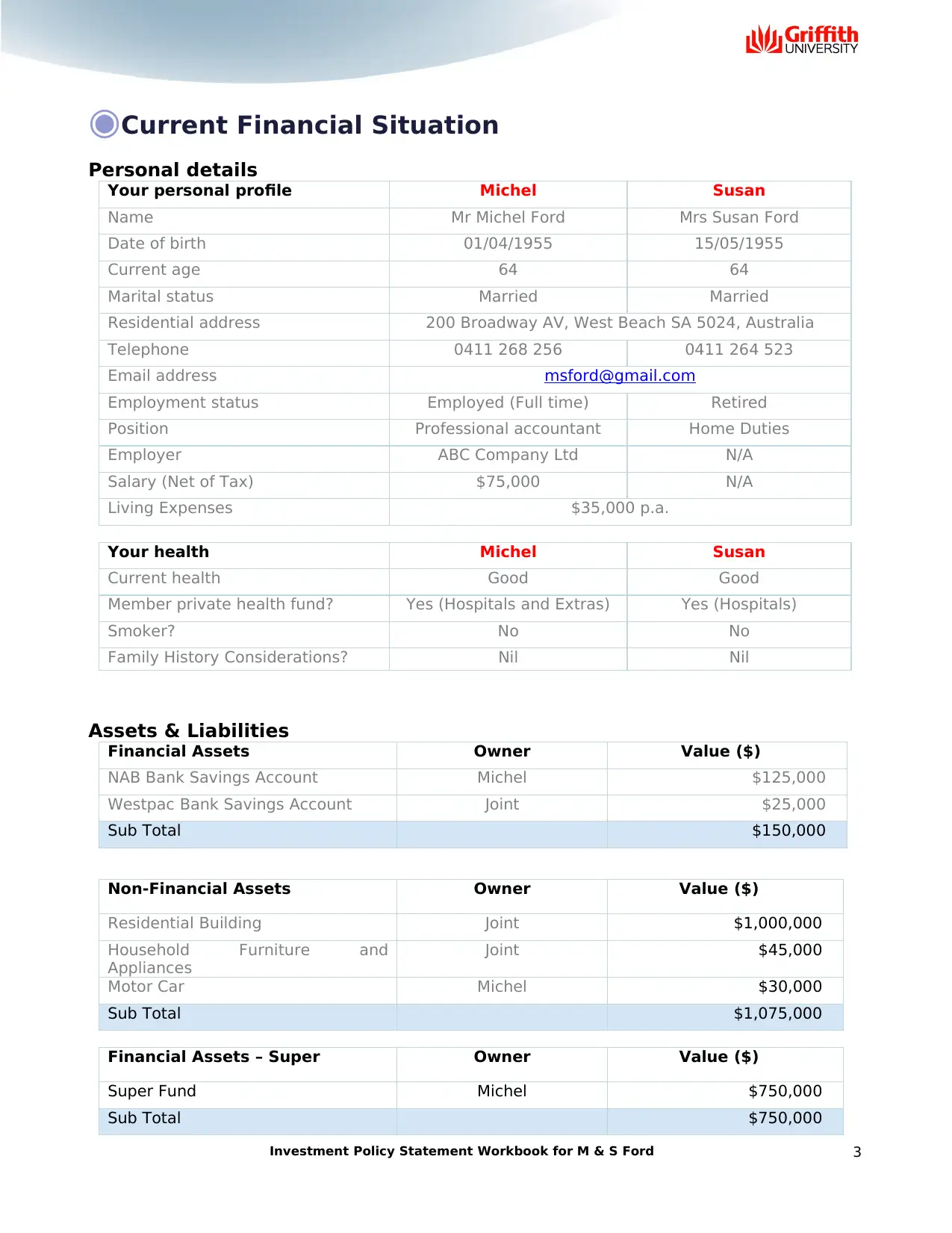

◉Current Financial Situation

Personal details

Your personal profile Michel Susan

Name Mr Michel Ford Mrs Susan Ford

Date of birth 01/04/1955 15/05/1955

Current age 64 64

Marital status Married Married

Residential address 200 Broadway AV, West Beach SA 5024, Australia

Telephone 0411 268 256 0411 264 523

Email address msford@gmail.com

Employment status Employed (Full time) Retired

Position Professional accountant Home Duties

Employer ABC Company Ltd N/A

Salary (Net of Tax) $75,000 N/A

Living Expenses $35,000 p.a.

Your health Michel Susan

Current health Good Good

Member private health fund? Yes (Hospitals and Extras) Yes (Hospitals)

Smoker? No No

Family History Considerations? Nil Nil

Assets & Liabilities

Financial Assets Owner Value ($)

NAB Bank Savings Account Michel $125,000

Westpac Bank Savings Account Joint $25,000

Sub Total $150,000

Non-Financial Assets Owner Value ($)

Residential Building Joint $1,000,000

Household Furniture and

Appliances

Joint $45,000

Motor Car Michel $30,000

Sub Total $1,075,000

Financial Assets – Super Owner Value ($)

Super Fund Michel $750,000

Sub Total $750,000

Investment Policy Statement Workbook for M & S Ford 3

Personal details

Your personal profile Michel Susan

Name Mr Michel Ford Mrs Susan Ford

Date of birth 01/04/1955 15/05/1955

Current age 64 64

Marital status Married Married

Residential address 200 Broadway AV, West Beach SA 5024, Australia

Telephone 0411 268 256 0411 264 523

Email address msford@gmail.com

Employment status Employed (Full time) Retired

Position Professional accountant Home Duties

Employer ABC Company Ltd N/A

Salary (Net of Tax) $75,000 N/A

Living Expenses $35,000 p.a.

Your health Michel Susan

Current health Good Good

Member private health fund? Yes (Hospitals and Extras) Yes (Hospitals)

Smoker? No No

Family History Considerations? Nil Nil

Assets & Liabilities

Financial Assets Owner Value ($)

NAB Bank Savings Account Michel $125,000

Westpac Bank Savings Account Joint $25,000

Sub Total $150,000

Non-Financial Assets Owner Value ($)

Residential Building Joint $1,000,000

Household Furniture and

Appliances

Joint $45,000

Motor Car Michel $30,000

Sub Total $1,075,000

Financial Assets – Super Owner Value ($)

Super Fund Michel $750,000

Sub Total $750,000

Investment Policy Statement Workbook for M & S Ford 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assets Total $1,975,000

Liabilities Owner Value ($)

Credit cards, home loans, HECS

debt, business debt Joint $0

Liabilities Total $0

Total Net Worth $1,975,000

Dependents Current Age D.O.B. Financially

Dependent

Jonny Ford 25 10/04/1994 No

Current Cash flow

Income Amount

Michel’s Salaries $75,000

Interest Income $3,000

Total Income $78,000

Expenses Amount

Daily Living Expenses $55,000

Total Expenses $55,000

Estimated Cash Surplus/Deficit $24,000

Investment Policy Statement Workbook for M & S Ford 4

Liabilities Owner Value ($)

Credit cards, home loans, HECS

debt, business debt Joint $0

Liabilities Total $0

Total Net Worth $1,975,000

Dependents Current Age D.O.B. Financially

Dependent

Jonny Ford 25 10/04/1994 No

Current Cash flow

Income Amount

Michel’s Salaries $75,000

Interest Income $3,000

Total Income $78,000

Expenses Amount

Daily Living Expenses $55,000

Total Expenses $55,000

Estimated Cash Surplus/Deficit $24,000

Investment Policy Statement Workbook for M & S Ford 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

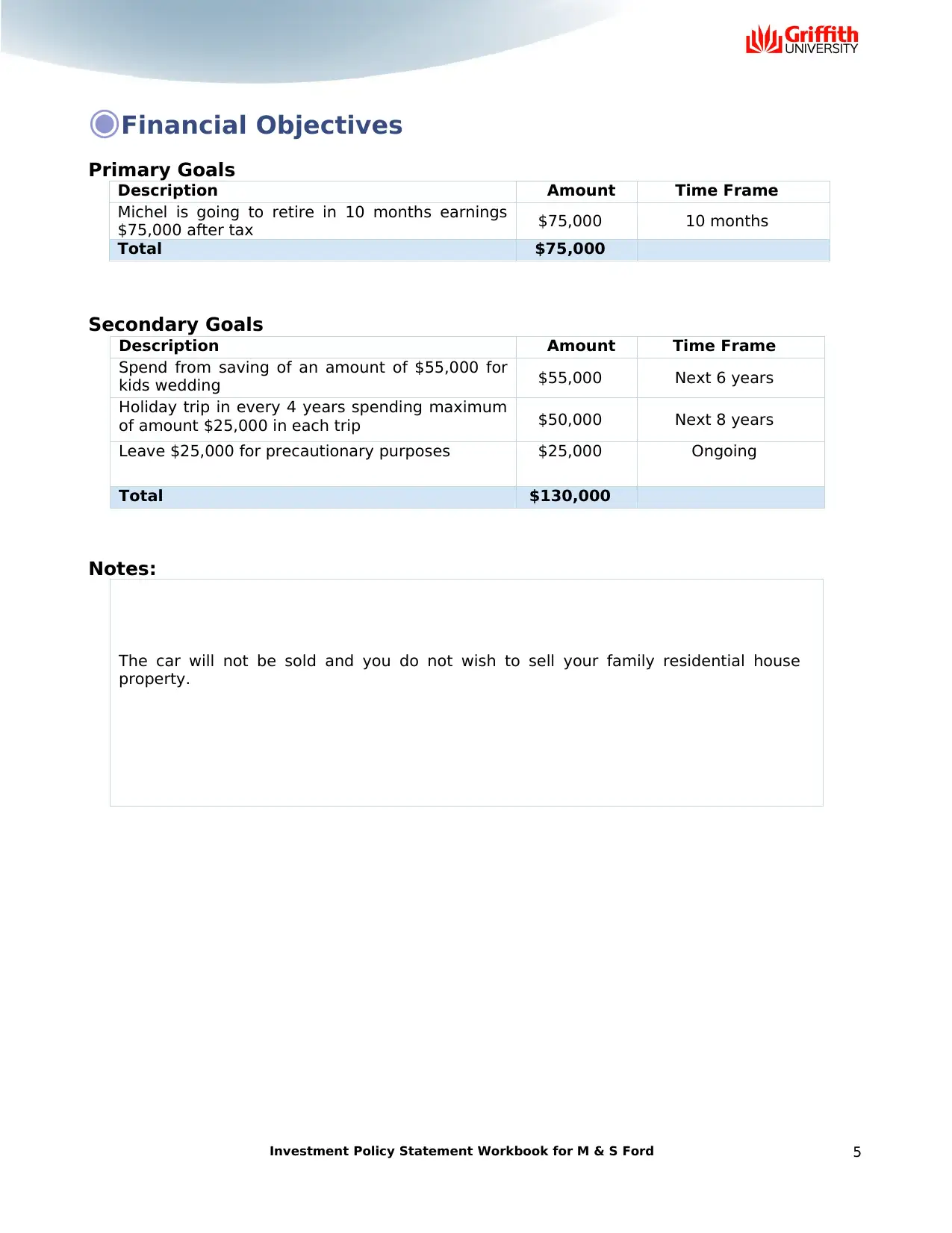

◉Financial Objectives

Primary Goals

Description Amount Time Frame

Michel is going to retire in 10 months earnings

$75,000 after tax $75,000 10 months

Total $75,000

Secondary Goals

Description Amount Time Frame

Spend from saving of an amount of $55,000 for

kids wedding $55,000 Next 6 years

Holiday trip in every 4 years spending maximum

of amount $25,000 in each trip $50,000 Next 8 years

Leave $25,000 for precautionary purposes $25,000 Ongoing

Total $130,000

Notes:

The car will not be sold and you do not wish to sell your family residential house

property.

Investment Policy Statement Workbook for M & S Ford 5

Primary Goals

Description Amount Time Frame

Michel is going to retire in 10 months earnings

$75,000 after tax $75,000 10 months

Total $75,000

Secondary Goals

Description Amount Time Frame

Spend from saving of an amount of $55,000 for

kids wedding $55,000 Next 6 years

Holiday trip in every 4 years spending maximum

of amount $25,000 in each trip $50,000 Next 8 years

Leave $25,000 for precautionary purposes $25,000 Ongoing

Total $130,000

Notes:

The car will not be sold and you do not wish to sell your family residential house

property.

Investment Policy Statement Workbook for M & S Ford 5

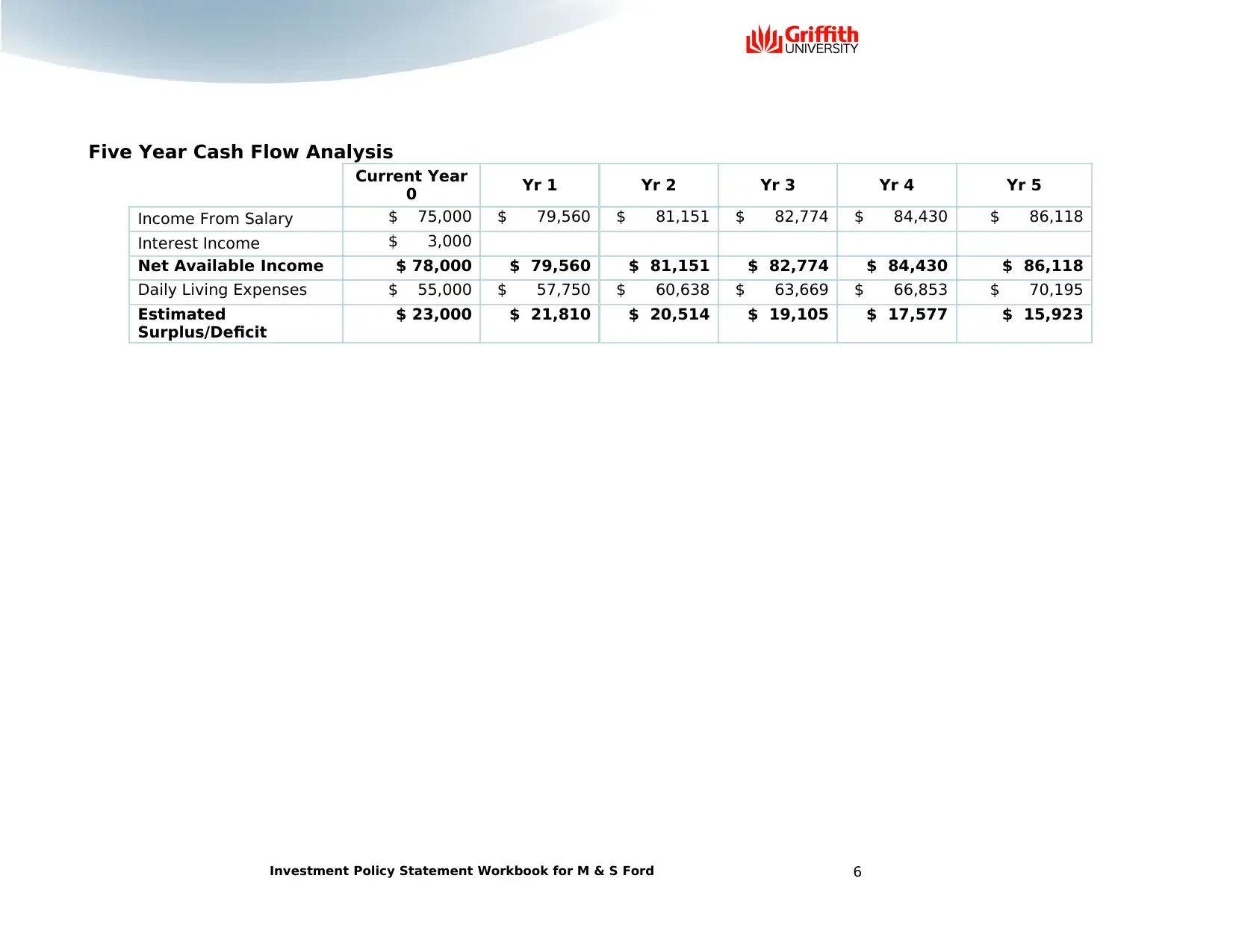

Five Year Cash Flow Analysis

Current Year

0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Income From Salary $ 75,000 $ 79,560 $ 81,151 $ 82,774 $ 84,430 $ 86,118

Interest Income $ 3,000

Net Available Income $ 78,000 $ 79,560 $ 81,151 $ 82,774 $ 84,430 $ 86,118

Daily Living Expenses $ 55,000 $ 57,750 $ 60,638 $ 63,669 $ 66,853 $ 70,195

Estimated

Surplus/Deficit

$ 23,000 $ 21,810 $ 20,514 $ 19,105 $ 17,577 $ 15,923

Investment Policy Statement Workbook for M & S Ford 6

Current Year

0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Income From Salary $ 75,000 $ 79,560 $ 81,151 $ 82,774 $ 84,430 $ 86,118

Interest Income $ 3,000

Net Available Income $ 78,000 $ 79,560 $ 81,151 $ 82,774 $ 84,430 $ 86,118

Daily Living Expenses $ 55,000 $ 57,750 $ 60,638 $ 63,669 $ 66,853 $ 70,195

Estimated

Surplus/Deficit

$ 23,000 $ 21,810 $ 20,514 $ 19,105 $ 17,577 $ 15,923

Investment Policy Statement Workbook for M & S Ford 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return Objective

Investable Assets Amount Percent of Net Worth

Allocated Pension (Mr Ford) $375,000 50%

Allocated Pension (Mrs Ford) $375,000 50%

Total $750,000 100%

Return Objective Amount After tax nominal rate of

return

Distribution in Year 2 $81,151 $81,151

Divided by investible assets $750,000 6.5%

Plus Expected Inflation 5% 11.5%

Risk Objective

Can the investor accommodate volatility and negative short-term returns given the

financial needs and goals provided?

Based on the discussion we had, Mr and Mrs Ford can assume certain level of

volatility and short term fluctuation in the returns but they do not wish to assume a

high level of risk and volatility in the return

Are the goals critical? A low margin for error can reduce the portfolio’s ability to

accommodate volatility and negative short-term returns.

Mr and Mrs Ford advised with $55,000, they can comfortably and fulfils some of

their expectations and intrastate travels

How large an investment shortfall can the portfolio bear?

As discussed with Mr and Mrs Ford, they can accept a drop of up to -12% in their

investment

How willing is the client to take risk?

Based on our discussion with Mr and Mrs Ford, they are willing to assume risk to

generate higher return and they can invest in the growth fund

Investment Policy Statement Workbook for M & S Ford 7

Investable Assets Amount Percent of Net Worth

Allocated Pension (Mr Ford) $375,000 50%

Allocated Pension (Mrs Ford) $375,000 50%

Total $750,000 100%

Return Objective Amount After tax nominal rate of

return

Distribution in Year 2 $81,151 $81,151

Divided by investible assets $750,000 6.5%

Plus Expected Inflation 5% 11.5%

Risk Objective

Can the investor accommodate volatility and negative short-term returns given the

financial needs and goals provided?

Based on the discussion we had, Mr and Mrs Ford can assume certain level of

volatility and short term fluctuation in the returns but they do not wish to assume a

high level of risk and volatility in the return

Are the goals critical? A low margin for error can reduce the portfolio’s ability to

accommodate volatility and negative short-term returns.

Mr and Mrs Ford advised with $55,000, they can comfortably and fulfils some of

their expectations and intrastate travels

How large an investment shortfall can the portfolio bear?

As discussed with Mr and Mrs Ford, they can accept a drop of up to -12% in their

investment

How willing is the client to take risk?

Based on our discussion with Mr and Mrs Ford, they are willing to assume risk to

generate higher return and they can invest in the growth fund

Investment Policy Statement Workbook for M & S Ford 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

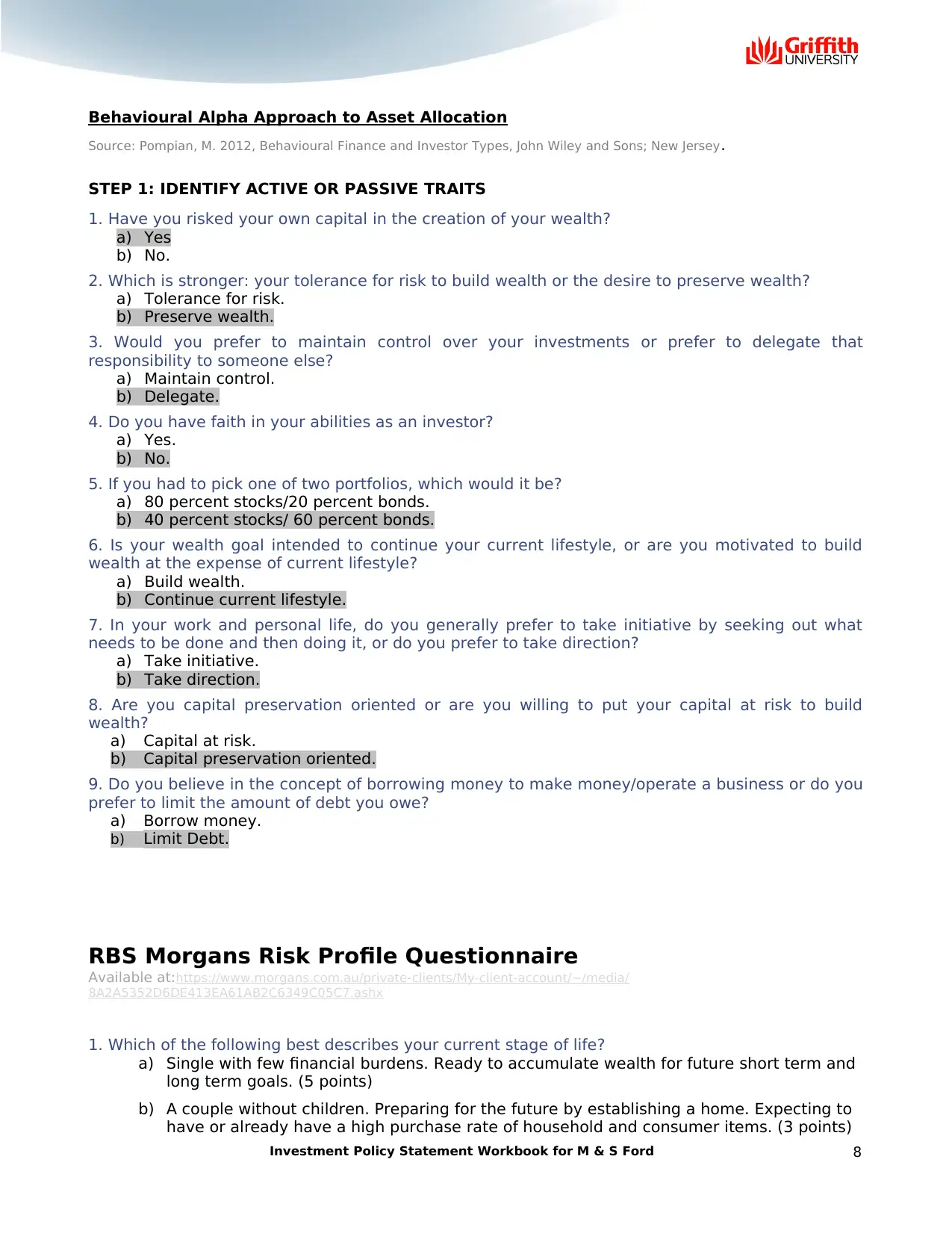

Behavioural Alpha Approach to Asset Allocation

Source: Pompian, M. 2012, Behavioural Finance and Investor Types, John Wiley and Sons; New Jersey.

STEP 1: IDENTIFY ACTIVE OR PASSIVE TRAITS

1. Have you risked your own capital in the creation of your wealth?

a) Yes

b) No.

2. Which is stronger: your tolerance for risk to build wealth or the desire to preserve wealth?

a) Tolerance for risk.

b) Preserve wealth.

3. Would you prefer to maintain control over your investments or prefer to delegate that

responsibility to someone else?

a) Maintain control.

b) Delegate.

4. Do you have faith in your abilities as an investor?

a) Yes.

b) No.

5. If you had to pick one of two portfolios, which would it be?

a) 80 percent stocks/20 percent bonds.

b) 40 percent stocks/ 60 percent bonds.

6. Is your wealth goal intended to continue your current lifestyle, or are you motivated to build

wealth at the expense of current lifestyle?

a) Build wealth.

b) Continue current lifestyle.

7. In your work and personal life, do you generally prefer to take initiative by seeking out what

needs to be done and then doing it, or do you prefer to take direction?

a) Take initiative.

b) Take direction.

8. Are you capital preservation oriented or are you willing to put your capital at risk to build

wealth?

a) Capital at risk.

b) Capital preservation oriented.

9. Do you believe in the concept of borrowing money to make money/operate a business or do you

prefer to limit the amount of debt you owe?

a) Borrow money.

b) Limit Debt.

RBS Morgans Risk Profile Questionnaire

Available at:https://www.morgans.com.au/private-clients/My-client-account/~/media/

8A2A5352D6DE413EA61AB2C6349C05C7.ashx

1. Which of the following best describes your current stage of life?

a) Single with few financial burdens. Ready to accumulate wealth for future short term and

long term goals. (5 points)

b) A couple without children. Preparing for the future by establishing a home. Expecting to

have or already have a high purchase rate of household and consumer items. (3 points)

Investment Policy Statement Workbook for M & S Ford 8

Source: Pompian, M. 2012, Behavioural Finance and Investor Types, John Wiley and Sons; New Jersey.

STEP 1: IDENTIFY ACTIVE OR PASSIVE TRAITS

1. Have you risked your own capital in the creation of your wealth?

a) Yes

b) No.

2. Which is stronger: your tolerance for risk to build wealth or the desire to preserve wealth?

a) Tolerance for risk.

b) Preserve wealth.

3. Would you prefer to maintain control over your investments or prefer to delegate that

responsibility to someone else?

a) Maintain control.

b) Delegate.

4. Do you have faith in your abilities as an investor?

a) Yes.

b) No.

5. If you had to pick one of two portfolios, which would it be?

a) 80 percent stocks/20 percent bonds.

b) 40 percent stocks/ 60 percent bonds.

6. Is your wealth goal intended to continue your current lifestyle, or are you motivated to build

wealth at the expense of current lifestyle?

a) Build wealth.

b) Continue current lifestyle.

7. In your work and personal life, do you generally prefer to take initiative by seeking out what

needs to be done and then doing it, or do you prefer to take direction?

a) Take initiative.

b) Take direction.

8. Are you capital preservation oriented or are you willing to put your capital at risk to build

wealth?

a) Capital at risk.

b) Capital preservation oriented.

9. Do you believe in the concept of borrowing money to make money/operate a business or do you

prefer to limit the amount of debt you owe?

a) Borrow money.

b) Limit Debt.

RBS Morgans Risk Profile Questionnaire

Available at:https://www.morgans.com.au/private-clients/My-client-account/~/media/

8A2A5352D6DE413EA61AB2C6349C05C7.ashx

1. Which of the following best describes your current stage of life?

a) Single with few financial burdens. Ready to accumulate wealth for future short term and

long term goals. (5 points)

b) A couple without children. Preparing for the future by establishing a home. Expecting to

have or already have a high purchase rate of household and consumer items. (3 points)

Investment Policy Statement Workbook for M & S Ford 8

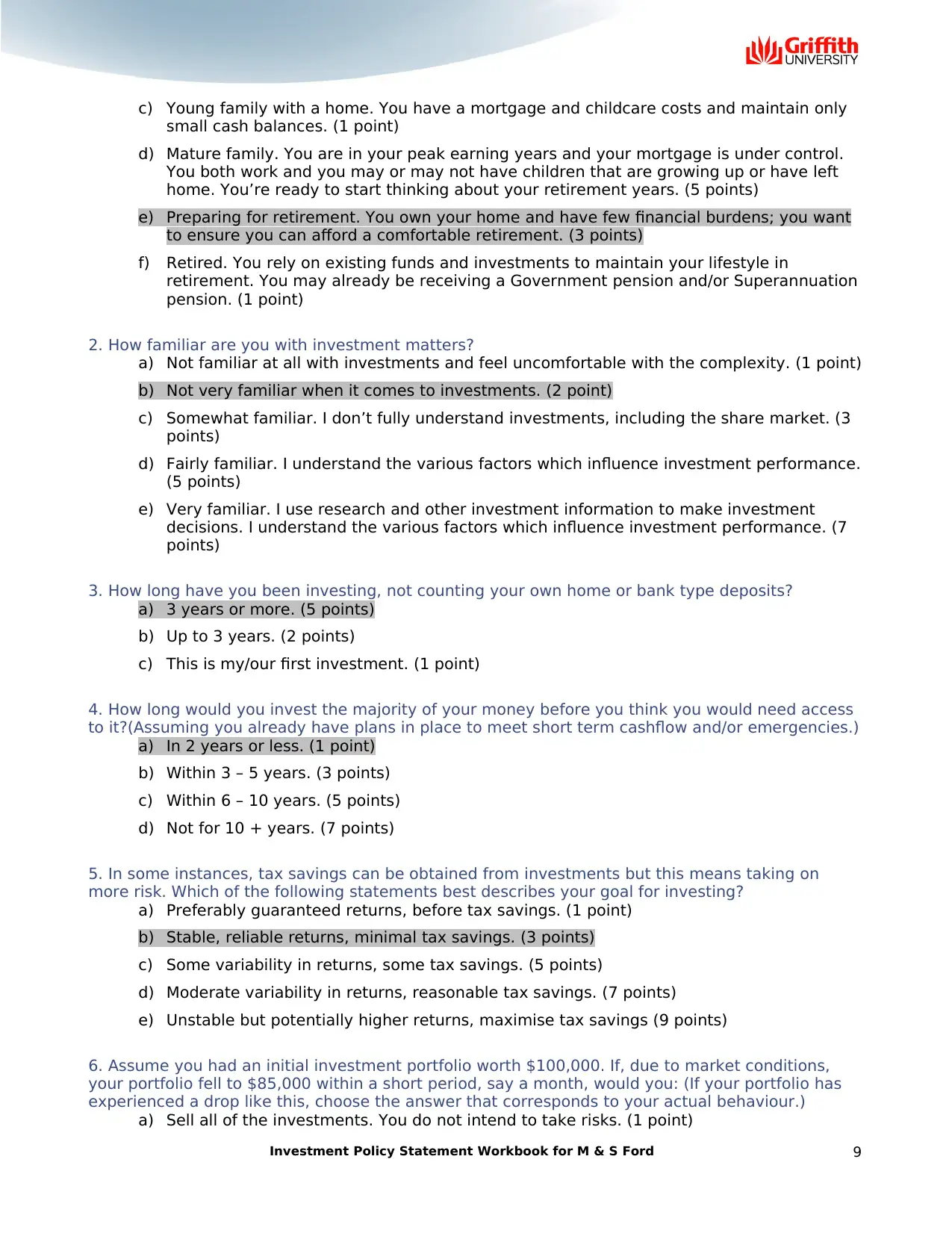

c) Young family with a home. You have a mortgage and childcare costs and maintain only

small cash balances. (1 point)

d) Mature family. You are in your peak earning years and your mortgage is under control.

You both work and you may or may not have children that are growing up or have left

home. You’re ready to start thinking about your retirement years. (5 points)

e) Preparing for retirement. You own your home and have few financial burdens; you want

to ensure you can afford a comfortable retirement. (3 points)

f) Retired. You rely on existing funds and investments to maintain your lifestyle in

retirement. You may already be receiving a Government pension and/or Superannuation

pension. (1 point)

2. How familiar are you with investment matters?

a) Not familiar at all with investments and feel uncomfortable with the complexity. (1 point)

b) Not very familiar when it comes to investments. (2 point)

c) Somewhat familiar. I don’t fully understand investments, including the share market. (3

points)

d) Fairly familiar. I understand the various factors which influence investment performance.

(5 points)

e) Very familiar. I use research and other investment information to make investment

decisions. I understand the various factors which influence investment performance. (7

points)

3. How long have you been investing, not counting your own home or bank type deposits?

a) 3 years or more. (5 points)

b) Up to 3 years. (2 points)

c) This is my/our first investment. (1 point)

4. How long would you invest the majority of your money before you think you would need access

to it?(Assuming you already have plans in place to meet short term cashflow and/or emergencies.)

a) In 2 years or less. (1 point)

b) Within 3 – 5 years. (3 points)

c) Within 6 – 10 years. (5 points)

d) Not for 10 + years. (7 points)

5. In some instances, tax savings can be obtained from investments but this means taking on

more risk. Which of the following statements best describes your goal for investing?

a) Preferably guaranteed returns, before tax savings. (1 point)

b) Stable, reliable returns, minimal tax savings. (3 points)

c) Some variability in returns, some tax savings. (5 points)

d) Moderate variability in returns, reasonable tax savings. (7 points)

e) Unstable but potentially higher returns, maximise tax savings (9 points)

6. Assume you had an initial investment portfolio worth $100,000. If, due to market conditions,

your portfolio fell to $85,000 within a short period, say a month, would you: (If your portfolio has

experienced a drop like this, choose the answer that corresponds to your actual behaviour.)

a) Sell all of the investments. You do not intend to take risks. (1 point)

Investment Policy Statement Workbook for M & S Ford 9

small cash balances. (1 point)

d) Mature family. You are in your peak earning years and your mortgage is under control.

You both work and you may or may not have children that are growing up or have left

home. You’re ready to start thinking about your retirement years. (5 points)

e) Preparing for retirement. You own your home and have few financial burdens; you want

to ensure you can afford a comfortable retirement. (3 points)

f) Retired. You rely on existing funds and investments to maintain your lifestyle in

retirement. You may already be receiving a Government pension and/or Superannuation

pension. (1 point)

2. How familiar are you with investment matters?

a) Not familiar at all with investments and feel uncomfortable with the complexity. (1 point)

b) Not very familiar when it comes to investments. (2 point)

c) Somewhat familiar. I don’t fully understand investments, including the share market. (3

points)

d) Fairly familiar. I understand the various factors which influence investment performance.

(5 points)

e) Very familiar. I use research and other investment information to make investment

decisions. I understand the various factors which influence investment performance. (7

points)

3. How long have you been investing, not counting your own home or bank type deposits?

a) 3 years or more. (5 points)

b) Up to 3 years. (2 points)

c) This is my/our first investment. (1 point)

4. How long would you invest the majority of your money before you think you would need access

to it?(Assuming you already have plans in place to meet short term cashflow and/or emergencies.)

a) In 2 years or less. (1 point)

b) Within 3 – 5 years. (3 points)

c) Within 6 – 10 years. (5 points)

d) Not for 10 + years. (7 points)

5. In some instances, tax savings can be obtained from investments but this means taking on

more risk. Which of the following statements best describes your goal for investing?

a) Preferably guaranteed returns, before tax savings. (1 point)

b) Stable, reliable returns, minimal tax savings. (3 points)

c) Some variability in returns, some tax savings. (5 points)

d) Moderate variability in returns, reasonable tax savings. (7 points)

e) Unstable but potentially higher returns, maximise tax savings (9 points)

6. Assume you had an initial investment portfolio worth $100,000. If, due to market conditions,

your portfolio fell to $85,000 within a short period, say a month, would you: (If your portfolio has

experienced a drop like this, choose the answer that corresponds to your actual behaviour.)

a) Sell all of the investments. You do not intend to take risks. (1 point)

Investment Policy Statement Workbook for M & S Ford 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

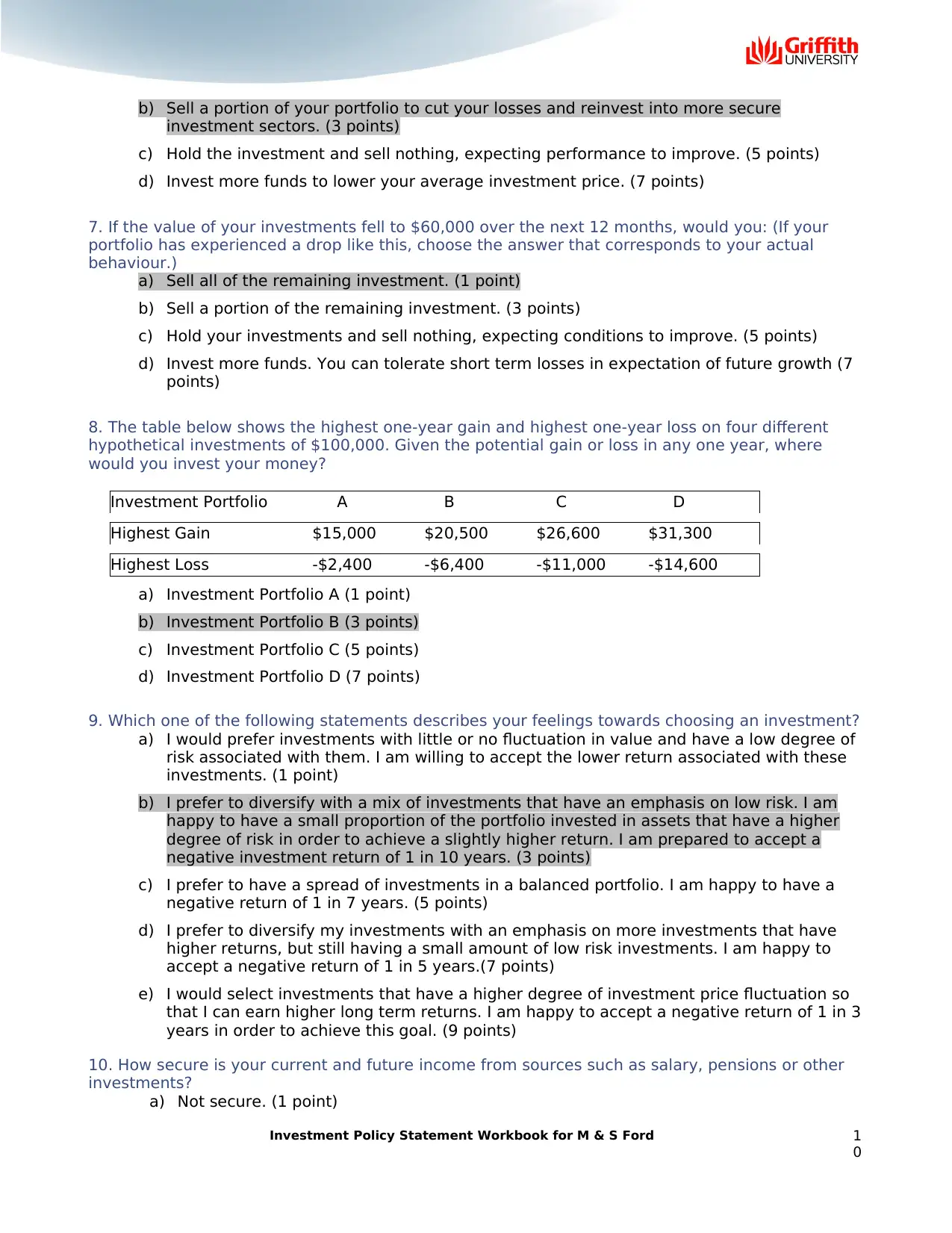

b) Sell a portion of your portfolio to cut your losses and reinvest into more secure

investment sectors. (3 points)

c) Hold the investment and sell nothing, expecting performance to improve. (5 points)

d) Invest more funds to lower your average investment price. (7 points)

7. If the value of your investments fell to $60,000 over the next 12 months, would you: (If your

portfolio has experienced a drop like this, choose the answer that corresponds to your actual

behaviour.)

a) Sell all of the remaining investment. (1 point)

b) Sell a portion of the remaining investment. (3 points)

c) Hold your investments and sell nothing, expecting conditions to improve. (5 points)

d) Invest more funds. You can tolerate short term losses in expectation of future growth (7

points)

8. The table below shows the highest one-year gain and highest one-year loss on four different

hypothetical investments of $100,000. Given the potential gain or loss in any one year, where

would you invest your money?

Investment Portfolio A B C D

Highest Gain $15,000 $20,500 $26,600 $31,300

Highest Loss -$2,400 -$6,400 -$11,000 -$14,600

a) Investment Portfolio A (1 point)

b) Investment Portfolio B (3 points)

c) Investment Portfolio C (5 points)

d) Investment Portfolio D (7 points)

9. Which one of the following statements describes your feelings towards choosing an investment?

a) I would prefer investments with little or no fluctuation in value and have a low degree of

risk associated with them. I am willing to accept the lower return associated with these

investments. (1 point)

b) I prefer to diversify with a mix of investments that have an emphasis on low risk. I am

happy to have a small proportion of the portfolio invested in assets that have a higher

degree of risk in order to achieve a slightly higher return. I am prepared to accept a

negative investment return of 1 in 10 years. (3 points)

c) I prefer to have a spread of investments in a balanced portfolio. I am happy to have a

negative return of 1 in 7 years. (5 points)

d) I prefer to diversify my investments with an emphasis on more investments that have

higher returns, but still having a small amount of low risk investments. I am happy to

accept a negative return of 1 in 5 years.(7 points)

e) I would select investments that have a higher degree of investment price fluctuation so

that I can earn higher long term returns. I am happy to accept a negative return of 1 in 3

years in order to achieve this goal. (9 points)

10. How secure is your current and future income from sources such as salary, pensions or other

investments?

a) Not secure. (1 point)

Investment Policy Statement Workbook for M & S Ford 1

0

investment sectors. (3 points)

c) Hold the investment and sell nothing, expecting performance to improve. (5 points)

d) Invest more funds to lower your average investment price. (7 points)

7. If the value of your investments fell to $60,000 over the next 12 months, would you: (If your

portfolio has experienced a drop like this, choose the answer that corresponds to your actual

behaviour.)

a) Sell all of the remaining investment. (1 point)

b) Sell a portion of the remaining investment. (3 points)

c) Hold your investments and sell nothing, expecting conditions to improve. (5 points)

d) Invest more funds. You can tolerate short term losses in expectation of future growth (7

points)

8. The table below shows the highest one-year gain and highest one-year loss on four different

hypothetical investments of $100,000. Given the potential gain or loss in any one year, where

would you invest your money?

Investment Portfolio A B C D

Highest Gain $15,000 $20,500 $26,600 $31,300

Highest Loss -$2,400 -$6,400 -$11,000 -$14,600

a) Investment Portfolio A (1 point)

b) Investment Portfolio B (3 points)

c) Investment Portfolio C (5 points)

d) Investment Portfolio D (7 points)

9. Which one of the following statements describes your feelings towards choosing an investment?

a) I would prefer investments with little or no fluctuation in value and have a low degree of

risk associated with them. I am willing to accept the lower return associated with these

investments. (1 point)

b) I prefer to diversify with a mix of investments that have an emphasis on low risk. I am

happy to have a small proportion of the portfolio invested in assets that have a higher

degree of risk in order to achieve a slightly higher return. I am prepared to accept a

negative investment return of 1 in 10 years. (3 points)

c) I prefer to have a spread of investments in a balanced portfolio. I am happy to have a

negative return of 1 in 7 years. (5 points)

d) I prefer to diversify my investments with an emphasis on more investments that have

higher returns, but still having a small amount of low risk investments. I am happy to

accept a negative return of 1 in 5 years.(7 points)

e) I would select investments that have a higher degree of investment price fluctuation so

that I can earn higher long term returns. I am happy to accept a negative return of 1 in 3

years in order to achieve this goal. (9 points)

10. How secure is your current and future income from sources such as salary, pensions or other

investments?

a) Not secure. (1 point)

Investment Policy Statement Workbook for M & S Ford 1

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

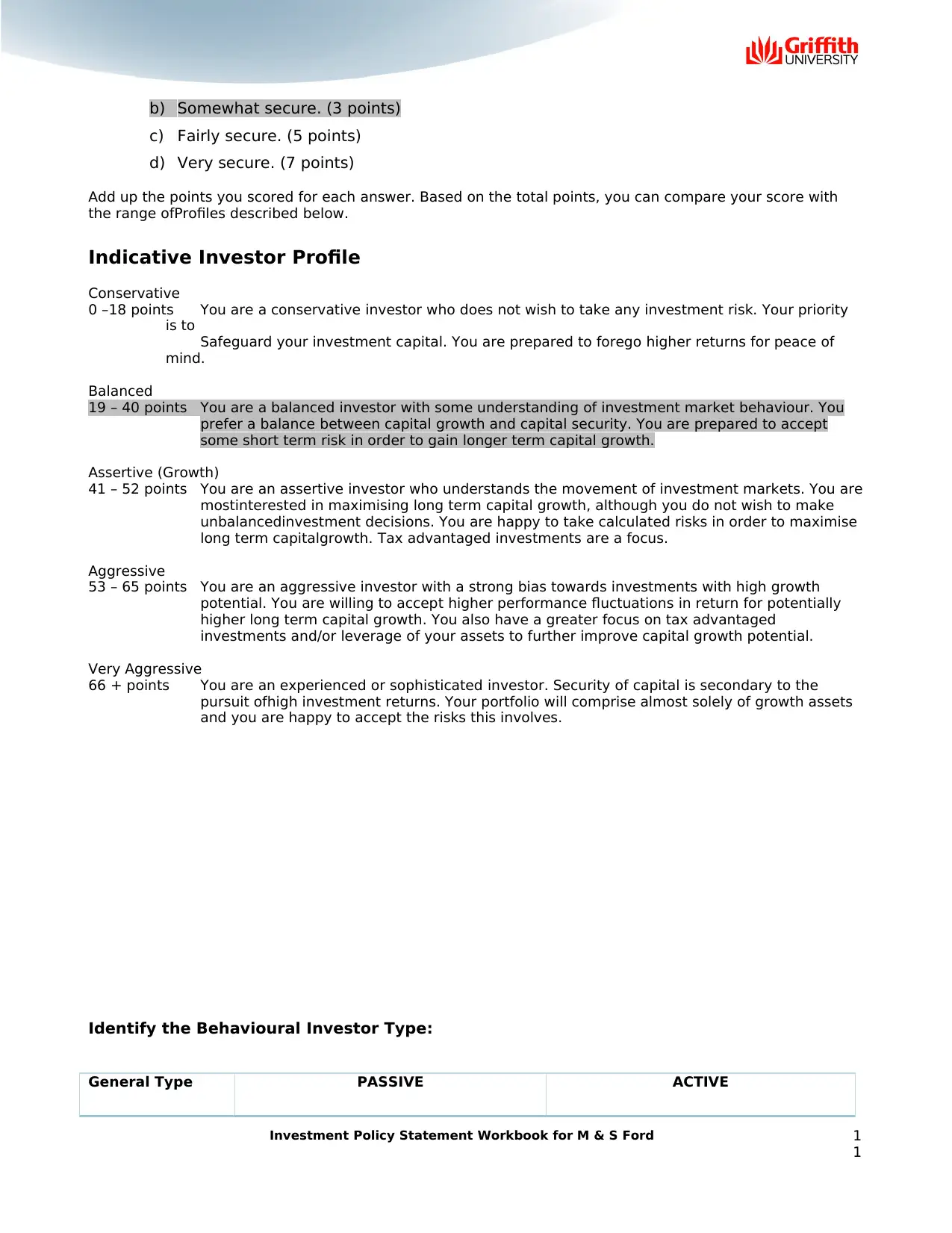

b) Somewhat secure. (3 points)

c) Fairly secure. (5 points)

d) Very secure. (7 points)

Add up the points you scored for each answer. Based on the total points, you can compare your score with

the range ofProfiles described below.26 - AFSL Licence 235410)

Questionnaire

Risk Profile Questionnaire

Indicative Investor Profile

Conservative

0 –18 points You are a conservative investor who does not wish to take any investment risk. Your priority

is to

Safeguard your investment capital. You are prepared to forego higher returns for peace of

mind.

Balanced

19 – 40 points You are a balanced investor with some understanding of investment market behaviour. You

prefer a balance between capital growth and capital security. You are prepared to accept

some short term risk in order to gain longer term capital growth.

Assertive (Growth)

41 – 52 points You are an assertive investor who understands the movement of investment markets. You are

mostinterested in maximising long term capital growth, although you do not wish to make

unbalancedinvestment decisions. You are happy to take calculated risks in order to maximise

long term capitalgrowth. Tax advantaged investments are a focus.

Aggressive

53 – 65 points You are an aggressive investor with a strong bias towards investments with high growth

potential. You are willing to accept higher performance fluctuations in return for potentially

higher long term capital growth. You also have a greater focus on tax advantaged

investments and/or leverage of your assets to further improve capital growth potential.

Very Aggressive

66 + points You are an experienced or sophisticated investor. Security of capital is secondary to the

pursuit ofhigh investment returns. Your portfolio will comprise almost solely of growth assets

and you are happy to accept the risks this involves.

Identify the Behavioural Investor Type:

General Type PASSIVE ACTIVE

Investment Policy Statement Workbook for M & S Ford 1

1

c) Fairly secure. (5 points)

d) Very secure. (7 points)

Add up the points you scored for each answer. Based on the total points, you can compare your score with

the range ofProfiles described below.26 - AFSL Licence 235410)

Questionnaire

Risk Profile Questionnaire

Indicative Investor Profile

Conservative

0 –18 points You are a conservative investor who does not wish to take any investment risk. Your priority

is to

Safeguard your investment capital. You are prepared to forego higher returns for peace of

mind.

Balanced

19 – 40 points You are a balanced investor with some understanding of investment market behaviour. You

prefer a balance between capital growth and capital security. You are prepared to accept

some short term risk in order to gain longer term capital growth.

Assertive (Growth)

41 – 52 points You are an assertive investor who understands the movement of investment markets. You are

mostinterested in maximising long term capital growth, although you do not wish to make

unbalancedinvestment decisions. You are happy to take calculated risks in order to maximise

long term capitalgrowth. Tax advantaged investments are a focus.

Aggressive

53 – 65 points You are an aggressive investor with a strong bias towards investments with high growth

potential. You are willing to accept higher performance fluctuations in return for potentially

higher long term capital growth. You also have a greater focus on tax advantaged

investments and/or leverage of your assets to further improve capital growth potential.

Very Aggressive

66 + points You are an experienced or sophisticated investor. Security of capital is secondary to the

pursuit ofhigh investment returns. Your portfolio will comprise almost solely of growth assets

and you are happy to accept the risks this involves.

Identify the Behavioural Investor Type:

General Type PASSIVE ACTIVE

Investment Policy Statement Workbook for M & S Ford 1

1

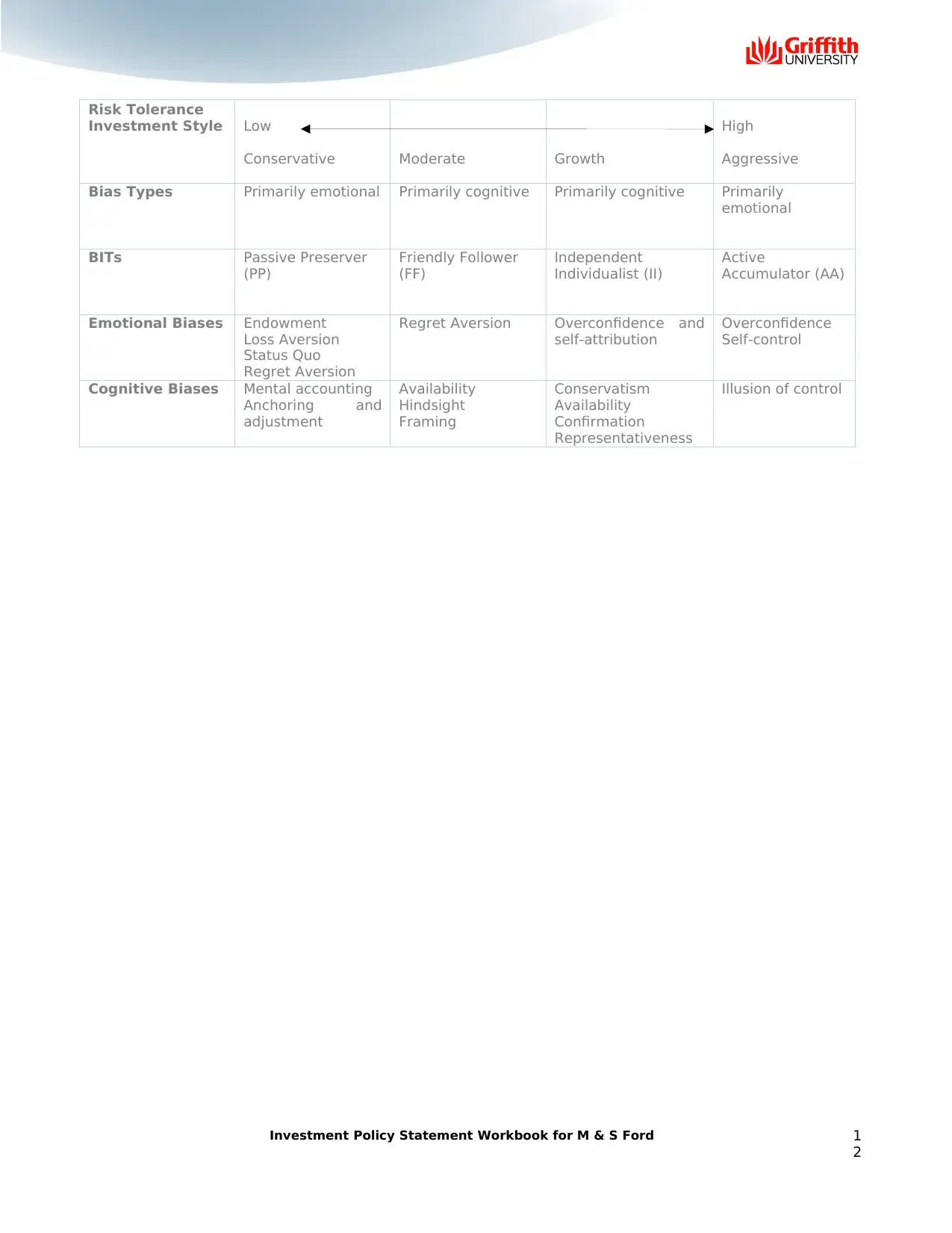

Risk Tolerance

Investment Style Low

Conservative Moderate Growth

High

Aggressive

Bias Types Primarily emotional Primarily cognitive Primarily cognitive Primarily

emotional

BITs Passive Preserver

(PP)

Friendly Follower

(FF)

Independent

Individualist (II)

Active

Accumulator (AA)

Emotional Biases Endowment

Loss Aversion

Status Quo

Regret Aversion

Regret Aversion Overconfidence and

self-attribution

Overconfidence

Self-control

Cognitive Biases Mental accounting

Anchoring and

adjustment

Availability

Hindsight

Framing

Conservatism

Availability

Confirmation

Representativeness

Illusion of control

Investment Policy Statement Workbook for M & S Ford 1

2

Investment Style Low

Conservative Moderate Growth

High

Aggressive

Bias Types Primarily emotional Primarily cognitive Primarily cognitive Primarily

emotional

BITs Passive Preserver

(PP)

Friendly Follower

(FF)

Independent

Individualist (II)

Active

Accumulator (AA)

Emotional Biases Endowment

Loss Aversion

Status Quo

Regret Aversion

Regret Aversion Overconfidence and

self-attribution

Overconfidence

Self-control

Cognitive Biases Mental accounting

Anchoring and

adjustment

Availability

Hindsight

Framing

Conservatism

Availability

Confirmation

Representativeness

Illusion of control

Investment Policy Statement Workbook for M & S Ford 1

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

![Managerial Accounting Assignment Solution - [University] [Semester]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fnr%2Feb6ffb76356e457ab3cc2da237f03df4.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.