Company Accounting Report: AASB Standards and Impairment Analysis

VerifiedAdded on 2022/11/18

|11

|1912

|379

Report

AI Summary

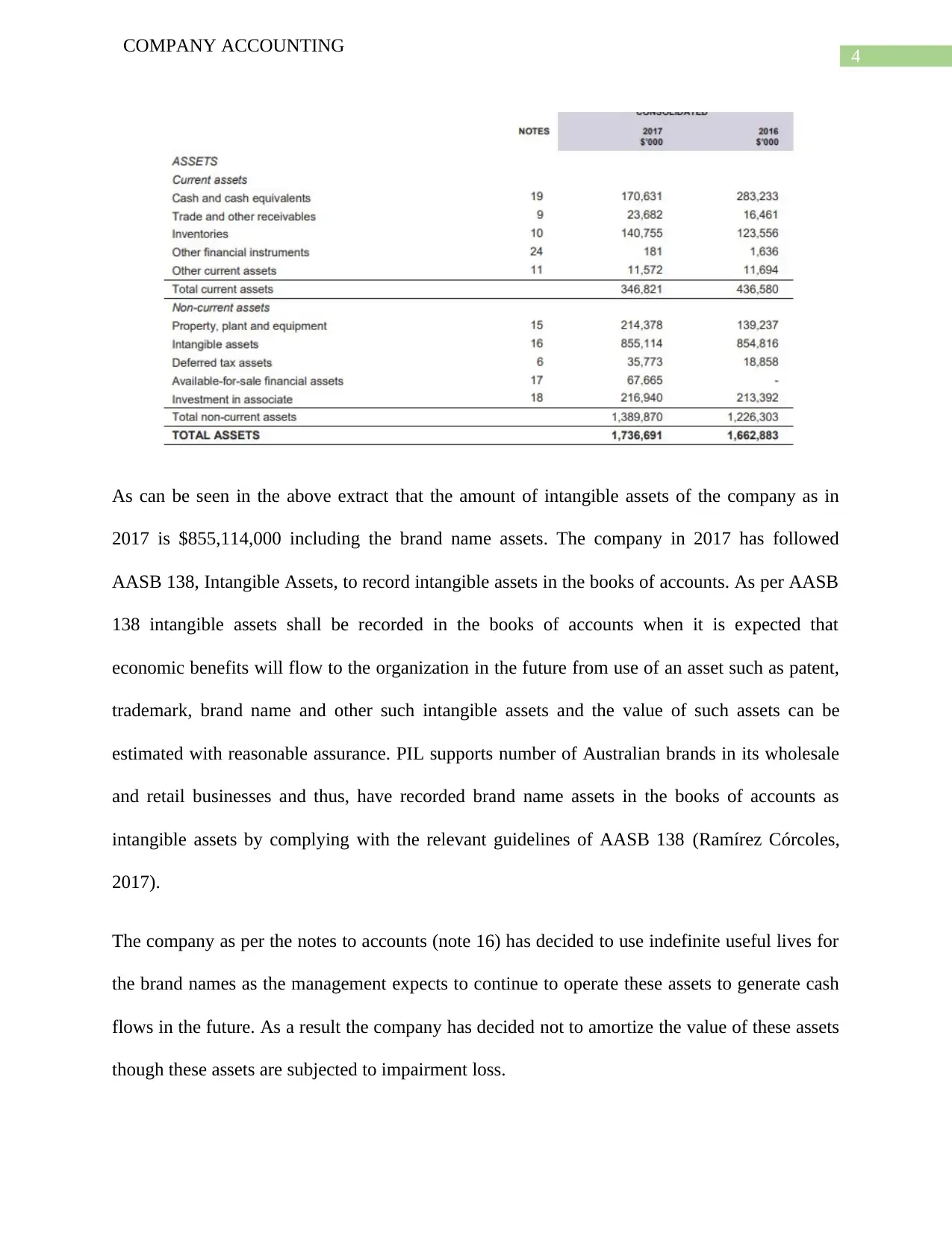

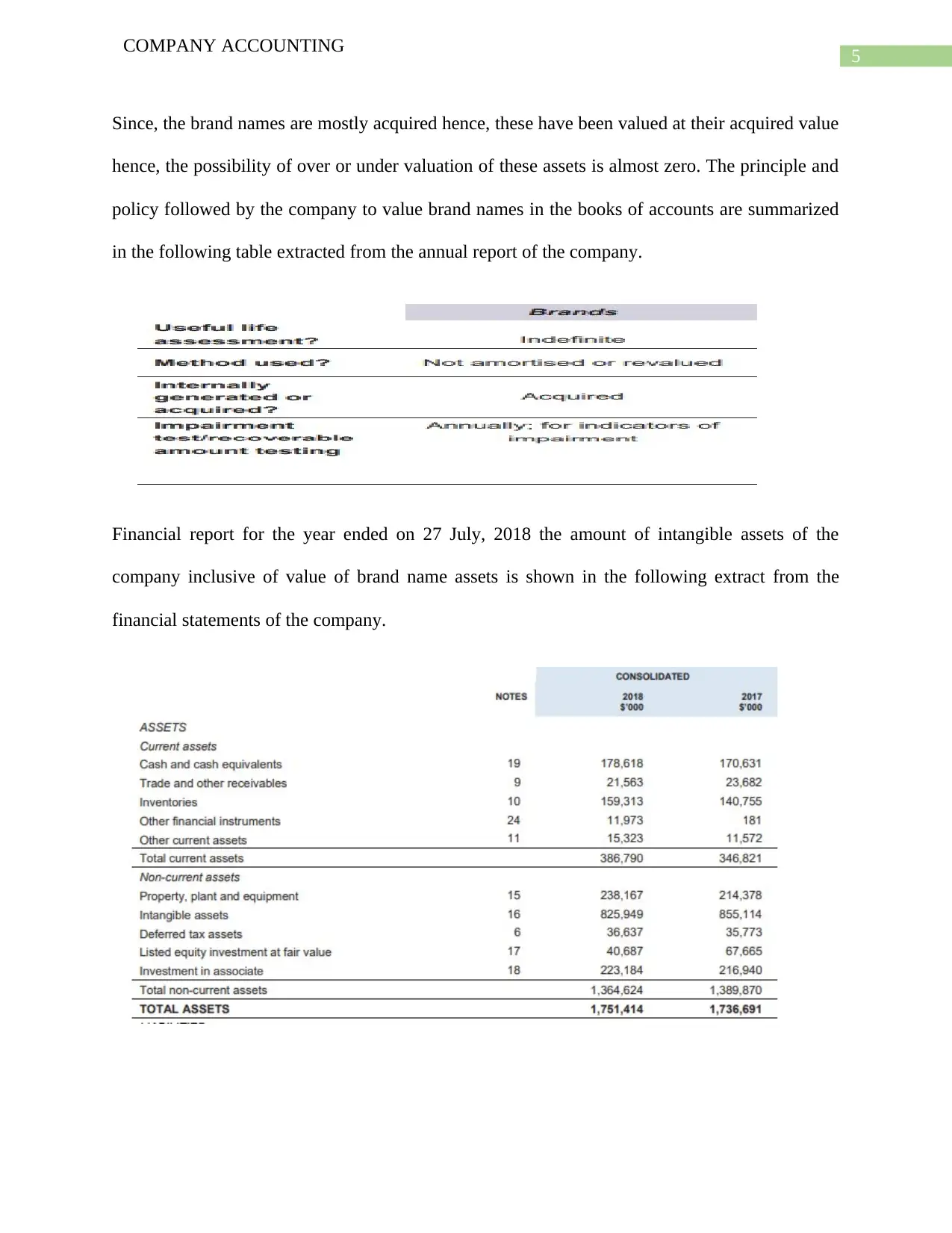

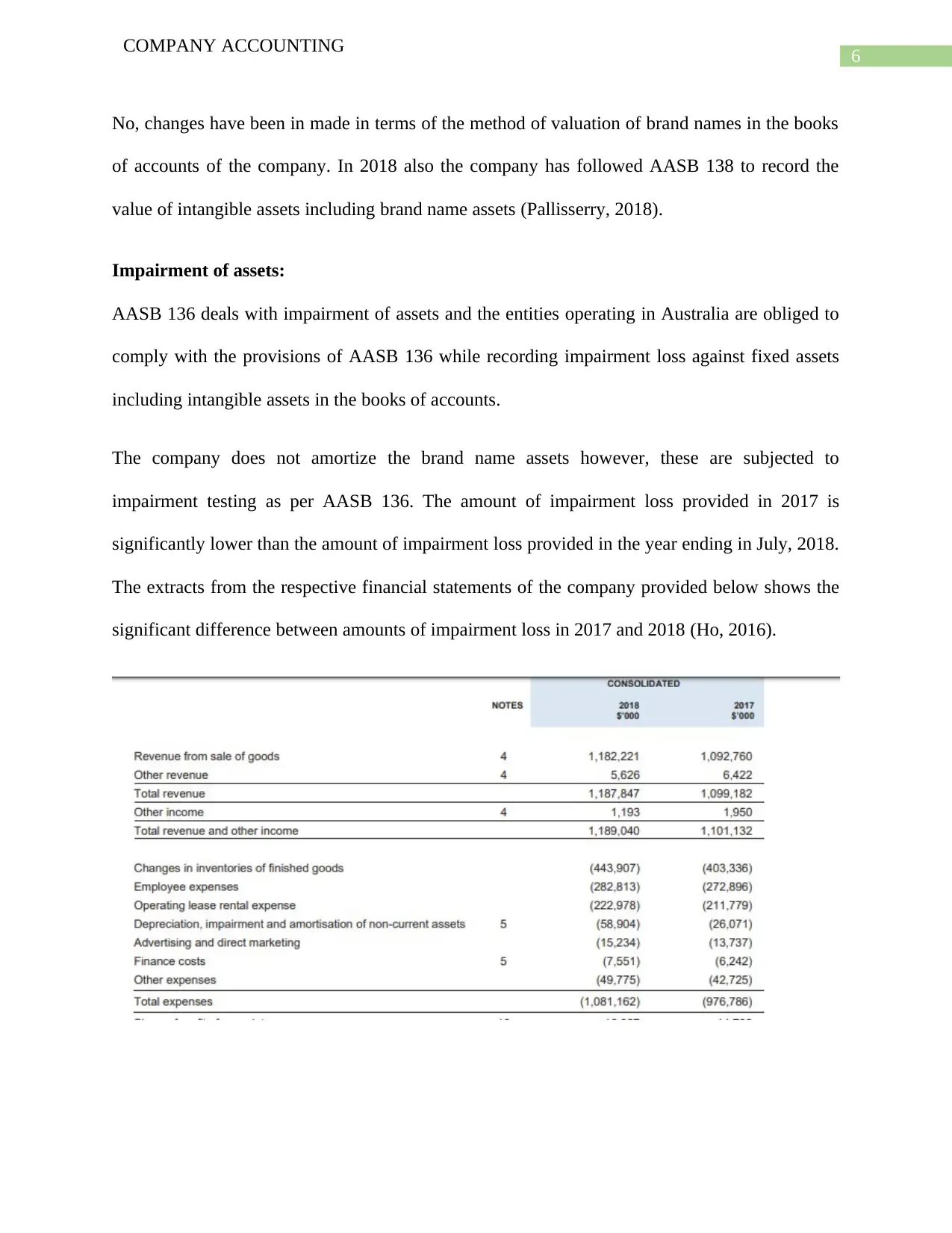

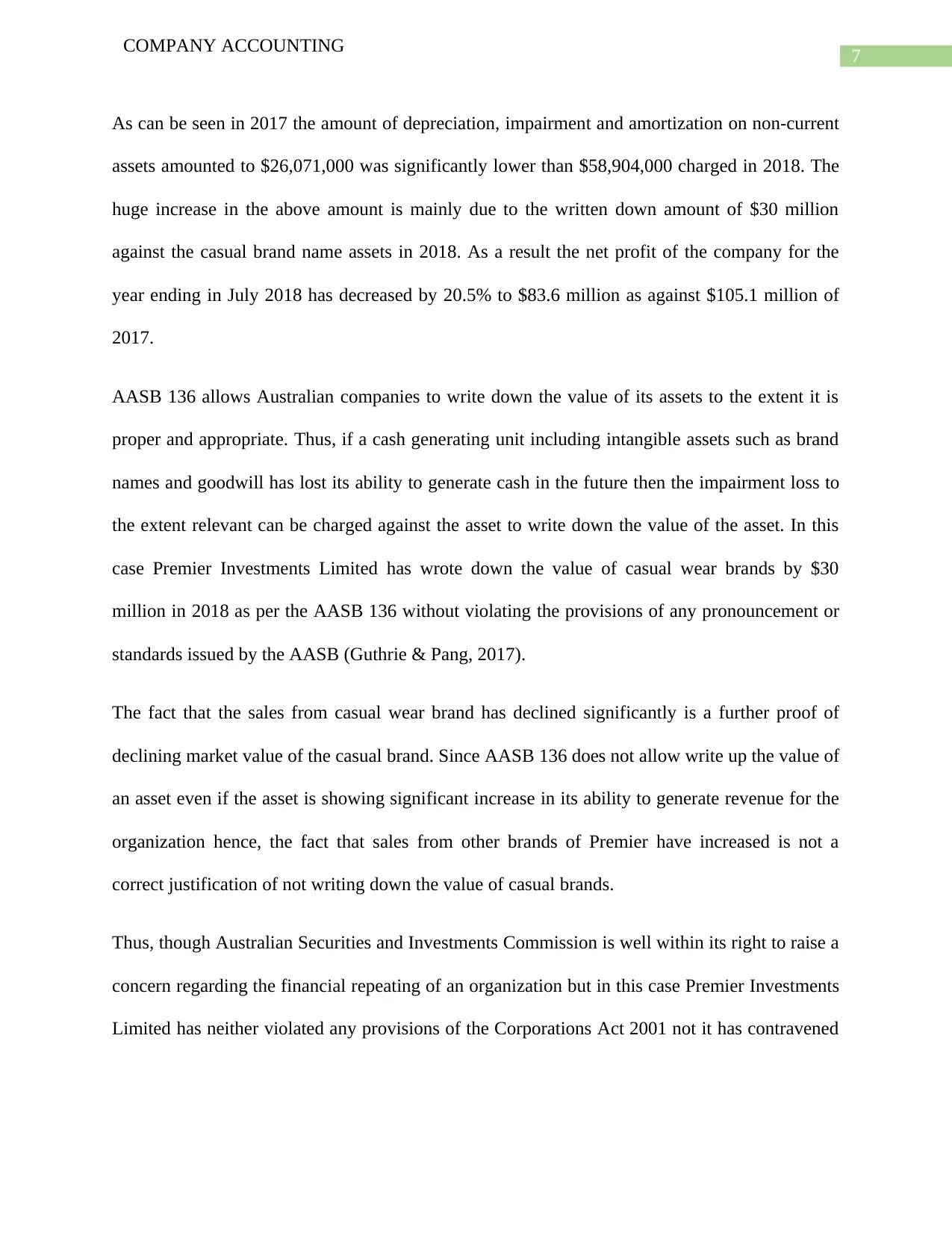

This report provides a detailed analysis of Premier Investments Limited's accounting practices, focusing on its compliance with Australian Accounting Standards (AASBs). The report examines the accounting treatment of brand name assets, their valuation, and the application of AASB 138 for intangible assets. It also explores the impairment of assets, particularly the $30 million write-down of casual brand assets in 2018, and its impact on the company's financial performance. The report discusses the application of AASB 136 regarding impairment and presents an alternative approach involving periodic amortization. The conclusion highlights the importance of true and fair presentation of financial performance and position, suggesting that while Premier Investments Limited complied with accounting standards, the significant write-down influenced the portrayal of the company's financial health. The report references key academic sources to support its findings.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.