FINA6000 Managing Finance: Australian IPO Performance Analysis

VerifiedAdded on 2022/10/03

|14

|3123

|16

Report

AI Summary

This report undertakes a comprehensive analysis of Initial Public Offerings (IPOs) in the Australian market, focusing on the case studies of Steadfast Group, GDI Property, and Meridian Energy. The study investigates the motivations behind IPOs, the amounts raised, and the allocation of funds, while also addressing the phenomenon of underpricing and its implications. It examines the relationship between IPO activity and overall market conditions in Australia, providing insights into the number of IPOs conducted between 2007 and 2017. Furthermore, the report evaluates the performance of the selected companies within three years after their IPOs, considering both scenarios with and without dividends, and comparing their performance to the All Ordinary Index. The analysis incorporates financial data, including share prices, growth rates, dividends, and cost of equity, to assess the investment potential and market dynamics of IPOs.

ASSIGNMENT COVER SHEET

Please refer to the Academic Integrity Policy on the Torrens University website before completing the form.

SECTION 1: PERSONAL DETAILS

First Name Surname Student ID

College Course

SECTION 2: ASSIGNMENT INFORMATION

Subject Name Lecturer Name

Assignment Title Word Count

Is your assignment being submitted on or before the published due date? if yes, skip to declaration

SECTION 2A: ASSIGNMENT EXTENSION

Have you been approved for an

extension? (if no skip to declaration)

Who approved your extension

What is the approved extension date?

SECTION 3: DECLARATION

I declare that except where I have referenced, the work I am submitting in this attachment is my own work

I acknowledge and agree that the assessor of this assignment may, for the purpose of authenticating this

assignment, reproduce it for the purpose of detecting plagiarism

I have read and am aware of the Academic Integrity Policy available on the Torrens University Education

website

Student Signature Date

RECEIPT - INDIVIDUAL ASSIGNMENT COVER SHEET - STUDENT COPY

First

Name

Surnam

e

Student ID

Please refer to the Academic Integrity Policy on the Torrens University website before completing the form.

SECTION 1: PERSONAL DETAILS

First Name Surname Student ID

College Course

SECTION 2: ASSIGNMENT INFORMATION

Subject Name Lecturer Name

Assignment Title Word Count

Is your assignment being submitted on or before the published due date? if yes, skip to declaration

SECTION 2A: ASSIGNMENT EXTENSION

Have you been approved for an

extension? (if no skip to declaration)

Who approved your extension

What is the approved extension date?

SECTION 3: DECLARATION

I declare that except where I have referenced, the work I am submitting in this attachment is my own work

I acknowledge and agree that the assessor of this assignment may, for the purpose of authenticating this

assignment, reproduce it for the purpose of detecting plagiarism

I have read and am aware of the Academic Integrity Policy available on the Torrens University Education

website

Student Signature Date

RECEIPT - INDIVIDUAL ASSIGNMENT COVER SHEET - STUDENT COPY

First

Name

Surnam

e

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: MANAGING FINANCE

Subject Name:

Lecturer Name:

Assignment Title:

Received by

full name, signature & date:

Torrens University Australia operates through the following legal entity: Torrens University Australia Pty Ltd, ABN 99 154 937 005, HE PRV12209, RTO No. 41343,

CRICOS 03389E

Subject Name:

Lecturer Name:

Assignment Title:

Received by

full name, signature & date:

Torrens University Australia operates through the following legal entity: Torrens University Australia Pty Ltd, ABN 99 154 937 005, HE PRV12209, RTO No. 41343,

CRICOS 03389E

MANAGING FINANCE

1

Table of Contents

Introduction:...............................................................................................................................2

1. Providing information regarding the approbator decisions that was made by the

organisation while undertaking of the IPO:...............................................................................2

2. Understanding the presence of under-pricing with the IPOs:................................................5

3. Determining the IPO activity with the Market conditions of Australia:................................6

4. The performance within three years after the IPO without dividends:..................................8

5. The performance within three years after the IPO with dividends:.......................................9

Conclusion:................................................................................................................................9

References and Bibliography:..................................................................................................11

1

Table of Contents

Introduction:...............................................................................................................................2

1. Providing information regarding the approbator decisions that was made by the

organisation while undertaking of the IPO:...............................................................................2

2. Understanding the presence of under-pricing with the IPOs:................................................5

3. Determining the IPO activity with the Market conditions of Australia:................................6

4. The performance within three years after the IPO without dividends:..................................8

5. The performance within three years after the IPO with dividends:.......................................9

Conclusion:................................................................................................................................9

References and Bibliography:..................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGING FINANCE

2

Introduction:

The report provides information on the overall measures that needs to be taken into

consideration for detecting the significant levels of measures that were taken by the

organisation while conducting their IPOs. The report provides adequate analysis on the

overall share price conditions of the IPOs that were conducted by Steadfast Group, GDI

Property and Meridian Energy. The IPOs is considered to be one of the most effective way in

attaining the required level of funds to support their expansion and other activities. Further

analysis on the under-pricing conditions that haunts the existence of the IPOs are mainly

depicted in the assessment, which helps in deterring the level of problems that is faced by

companies all over the world while initiating their public offerings. The discussion on the

share price conditions and the return generation capability are adequately depicted in the

assessment, which can help investors to determine the level of income that could be

generated from an investment.

1. Providing information regarding the approbator decisions that was made by the

organisation while undertaking of the IPO:

Company

Name

Indust

ry

Date of

IPO

Amount

intended

to raise

Amount

actually

raised The purpose of the funds

Steadfast

Group

Insura

nce Aug-13 $333.7m $333.7m

The main purpose of the IPO is

to provide Steadfast with a

liquid market for its Shares,

support the fund for

Acquisitions, enhance

Steadfast’s financial flexibility,

enhanced access to capital

markets, and repay in part of

the existing deb

2

Introduction:

The report provides information on the overall measures that needs to be taken into

consideration for detecting the significant levels of measures that were taken by the

organisation while conducting their IPOs. The report provides adequate analysis on the

overall share price conditions of the IPOs that were conducted by Steadfast Group, GDI

Property and Meridian Energy. The IPOs is considered to be one of the most effective way in

attaining the required level of funds to support their expansion and other activities. Further

analysis on the under-pricing conditions that haunts the existence of the IPOs are mainly

depicted in the assessment, which helps in deterring the level of problems that is faced by

companies all over the world while initiating their public offerings. The discussion on the

share price conditions and the return generation capability are adequately depicted in the

assessment, which can help investors to determine the level of income that could be

generated from an investment.

1. Providing information regarding the approbator decisions that was made by the

organisation while undertaking of the IPO:

Company

Name

Indust

ry

Date of

IPO

Amount

intended

to raise

Amount

actually

raised The purpose of the funds

Steadfast

Group

Insura

nce Aug-13 $333.7m $333.7m

The main purpose of the IPO is

to provide Steadfast with a

liquid market for its Shares,

support the fund for

Acquisitions, enhance

Steadfast’s financial flexibility,

enhanced access to capital

markets, and repay in part of

the existing deb

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGING FINANCE

3

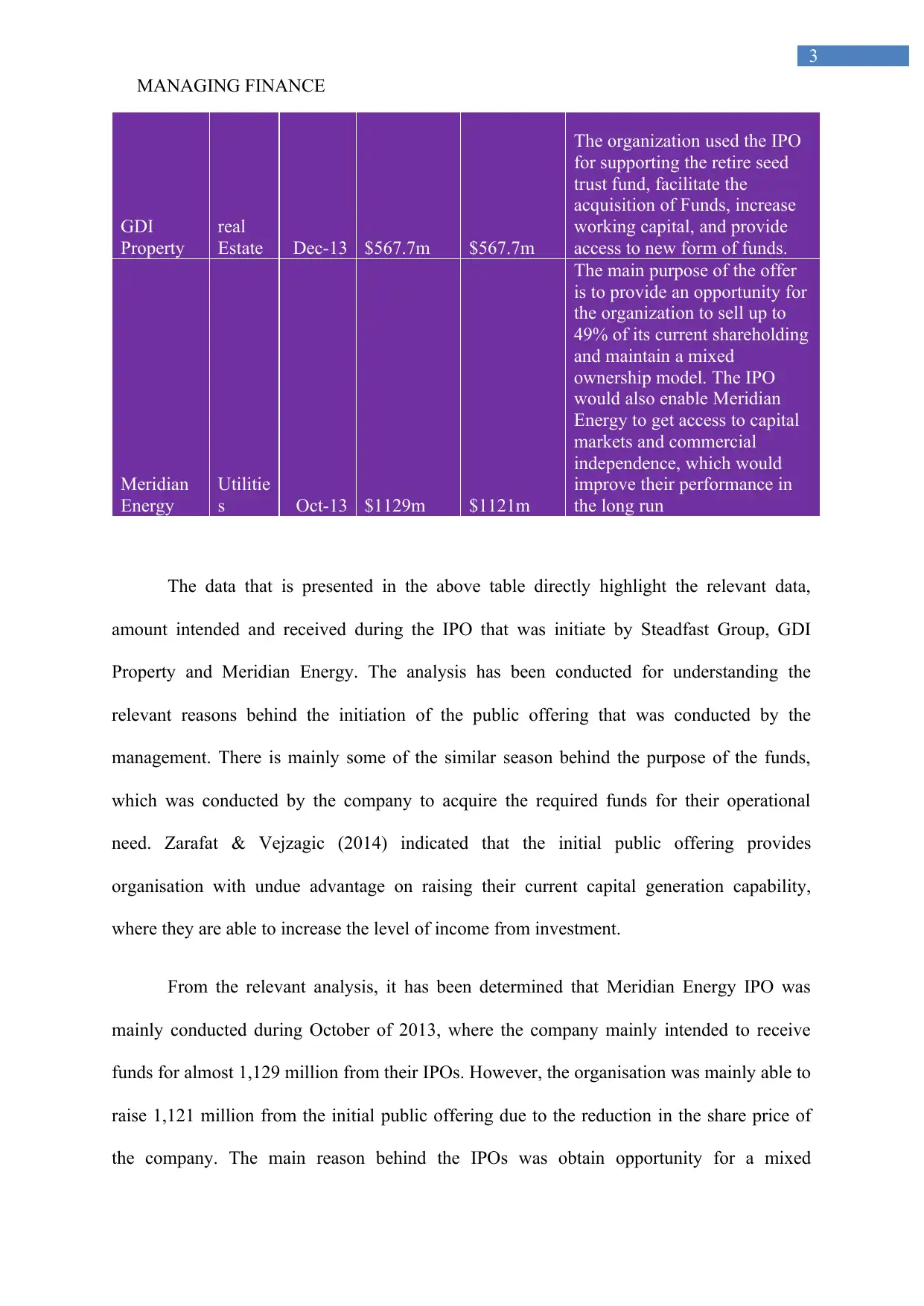

GDI

Property

real

Estate Dec-13 $567.7m $567.7m

The organization used the IPO

for supporting the retire seed

trust fund, facilitate the

acquisition of Funds, increase

working capital, and provide

access to new form of funds.

Meridian

Energy

Utilitie

s Oct-13 $1129m $1121m

The main purpose of the offer

is to provide an opportunity for

the organization to sell up to

49% of its current shareholding

and maintain a mixed

ownership model. The IPO

would also enable Meridian

Energy to get access to capital

markets and commercial

independence, which would

improve their performance in

the long run

The data that is presented in the above table directly highlight the relevant data,

amount intended and received during the IPO that was initiate by Steadfast Group, GDI

Property and Meridian Energy. The analysis has been conducted for understanding the

relevant reasons behind the initiation of the public offering that was conducted by the

management. There is mainly some of the similar season behind the purpose of the funds,

which was conducted by the company to acquire the required funds for their operational

need. Zarafat & Vejzagic (2014) indicated that the initial public offering provides

organisation with undue advantage on raising their current capital generation capability,

where they are able to increase the level of income from investment.

From the relevant analysis, it has been determined that Meridian Energy IPO was

mainly conducted during October of 2013, where the company mainly intended to receive

funds for almost 1,129 million from their IPOs. However, the organisation was mainly able to

raise 1,121 million from the initial public offering due to the reduction in the share price of

the company. The main reason behind the IPOs was obtain opportunity for a mixed

3

GDI

Property

real

Estate Dec-13 $567.7m $567.7m

The organization used the IPO

for supporting the retire seed

trust fund, facilitate the

acquisition of Funds, increase

working capital, and provide

access to new form of funds.

Meridian

Energy

Utilitie

s Oct-13 $1129m $1121m

The main purpose of the offer

is to provide an opportunity for

the organization to sell up to

49% of its current shareholding

and maintain a mixed

ownership model. The IPO

would also enable Meridian

Energy to get access to capital

markets and commercial

independence, which would

improve their performance in

the long run

The data that is presented in the above table directly highlight the relevant data,

amount intended and received during the IPO that was initiate by Steadfast Group, GDI

Property and Meridian Energy. The analysis has been conducted for understanding the

relevant reasons behind the initiation of the public offering that was conducted by the

management. There is mainly some of the similar season behind the purpose of the funds,

which was conducted by the company to acquire the required funds for their operational

need. Zarafat & Vejzagic (2014) indicated that the initial public offering provides

organisation with undue advantage on raising their current capital generation capability,

where they are able to increase the level of income from investment.

From the relevant analysis, it has been determined that Meridian Energy IPO was

mainly conducted during October of 2013, where the company mainly intended to receive

funds for almost 1,129 million from their IPOs. However, the organisation was mainly able to

raise 1,121 million from the initial public offering due to the reduction in the share price of

the company. The main reason behind the IPOs was obtain opportunity for a mixed

MANAGING FINANCE

4

ownership model and get access to capital markets and commercial independence. This

would eventually allow the management to support their relevant investment decisions after

getting the required level of funds to conduct relevant operations (Asx.com.au, 2019).

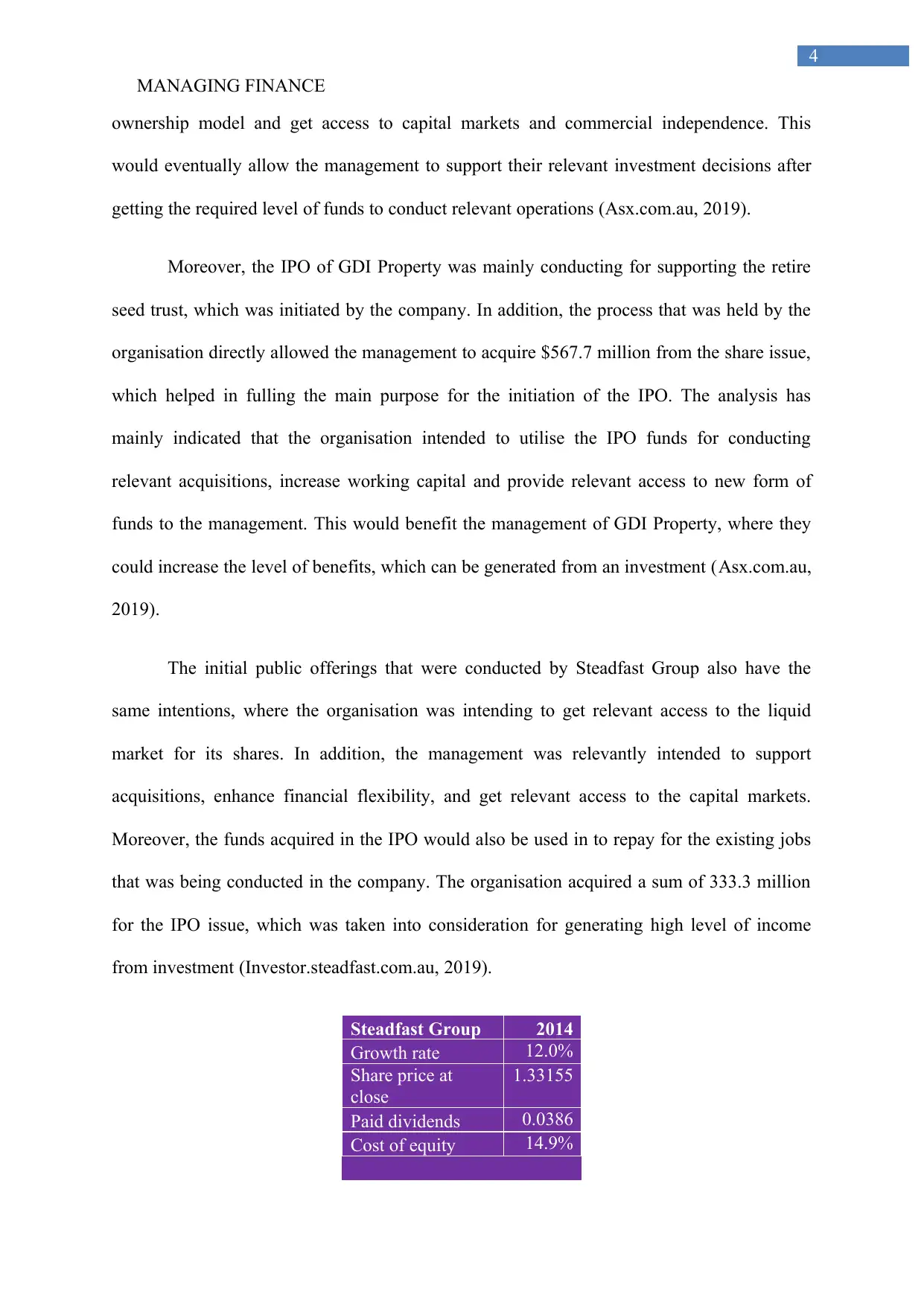

Moreover, the IPO of GDI Property was mainly conducting for supporting the retire

seed trust, which was initiated by the company. In addition, the process that was held by the

organisation directly allowed the management to acquire $567.7 million from the share issue,

which helped in fulling the main purpose for the initiation of the IPO. The analysis has

mainly indicated that the organisation intended to utilise the IPO funds for conducting

relevant acquisitions, increase working capital and provide relevant access to new form of

funds to the management. This would benefit the management of GDI Property, where they

could increase the level of benefits, which can be generated from an investment (Asx.com.au,

2019).

The initial public offerings that were conducted by Steadfast Group also have the

same intentions, where the organisation was intending to get relevant access to the liquid

market for its shares. In addition, the management was relevantly intended to support

acquisitions, enhance financial flexibility, and get relevant access to the capital markets.

Moreover, the funds acquired in the IPO would also be used in to repay for the existing jobs

that was being conducted in the company. The organisation acquired a sum of 333.3 million

for the IPO issue, which was taken into consideration for generating high level of income

from investment (Investor.steadfast.com.au, 2019).

Steadfast Group 2014

Growth rate 12.0%

Share price at

close

1.33155

Paid dividends 0.0386

Cost of equity 14.9%

4

ownership model and get access to capital markets and commercial independence. This

would eventually allow the management to support their relevant investment decisions after

getting the required level of funds to conduct relevant operations (Asx.com.au, 2019).

Moreover, the IPO of GDI Property was mainly conducting for supporting the retire

seed trust, which was initiated by the company. In addition, the process that was held by the

organisation directly allowed the management to acquire $567.7 million from the share issue,

which helped in fulling the main purpose for the initiation of the IPO. The analysis has

mainly indicated that the organisation intended to utilise the IPO funds for conducting

relevant acquisitions, increase working capital and provide relevant access to new form of

funds to the management. This would benefit the management of GDI Property, where they

could increase the level of benefits, which can be generated from an investment (Asx.com.au,

2019).

The initial public offerings that were conducted by Steadfast Group also have the

same intentions, where the organisation was intending to get relevant access to the liquid

market for its shares. In addition, the management was relevantly intended to support

acquisitions, enhance financial flexibility, and get relevant access to the capital markets.

Moreover, the funds acquired in the IPO would also be used in to repay for the existing jobs

that was being conducted in the company. The organisation acquired a sum of 333.3 million

for the IPO issue, which was taken into consideration for generating high level of income

from investment (Investor.steadfast.com.au, 2019).

Steadfast Group 2014

Growth rate 12.0%

Share price at

close

1.33155

Paid dividends 0.0386

Cost of equity 14.9%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGING FINANCE

5

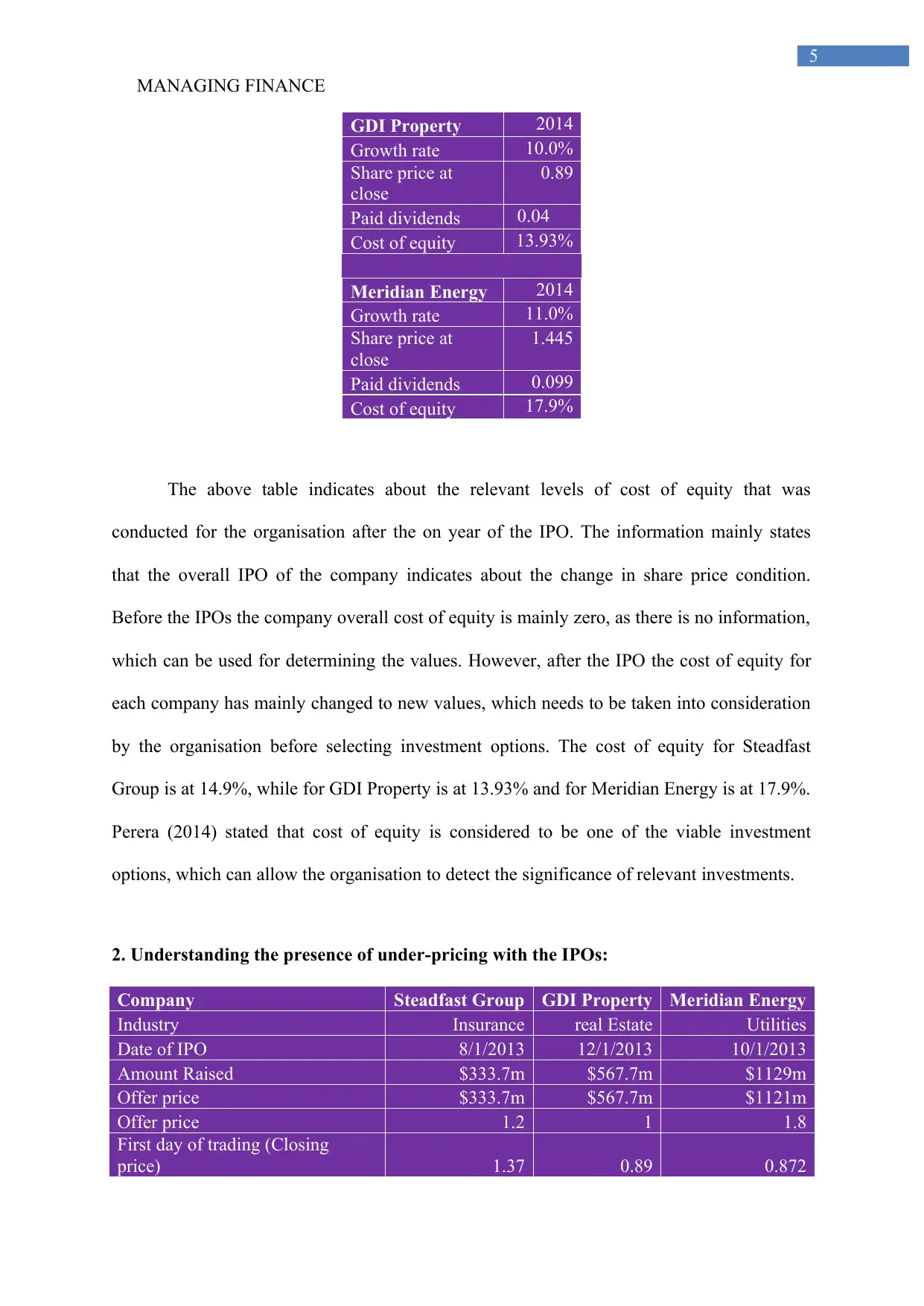

GDI Property 2014

Growth rate 10.0%

Share price at

close

0.89

Paid dividends 0.04

Cost of equity 13.93%

Meridian Energy 2014

Growth rate 11.0%

Share price at

close

1.445

Paid dividends 0.099

Cost of equity 17.9%

The above table indicates about the relevant levels of cost of equity that was

conducted for the organisation after the on year of the IPO. The information mainly states

that the overall IPO of the company indicates about the change in share price condition.

Before the IPOs the company overall cost of equity is mainly zero, as there is no information,

which can be used for determining the values. However, after the IPO the cost of equity for

each company has mainly changed to new values, which needs to be taken into consideration

by the organisation before selecting investment options. The cost of equity for Steadfast

Group is at 14.9%, while for GDI Property is at 13.93% and for Meridian Energy is at 17.9%.

Perera (2014) stated that cost of equity is considered to be one of the viable investment

options, which can allow the organisation to detect the significance of relevant investments.

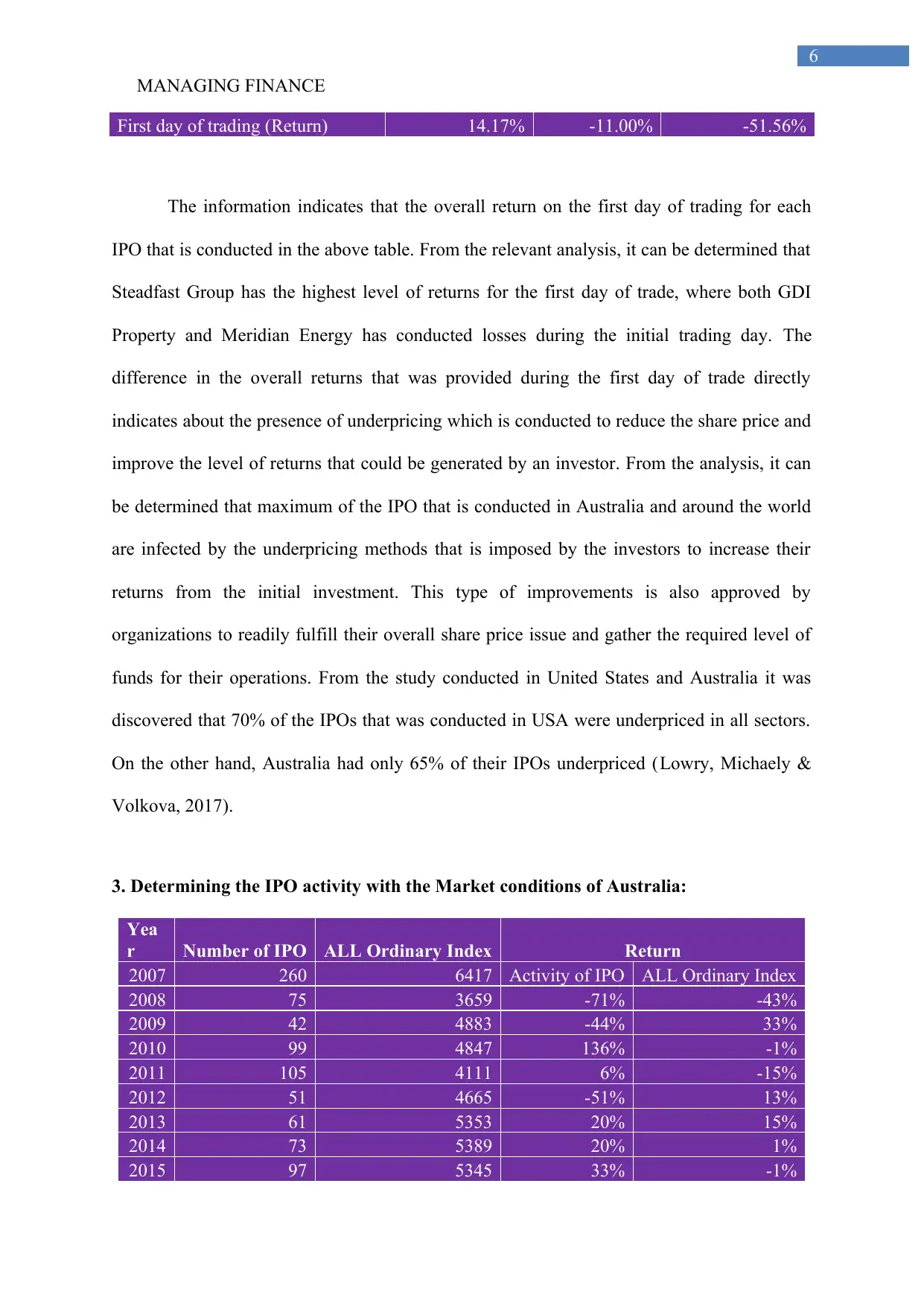

2. Understanding the presence of under-pricing with the IPOs:

Company Steadfast Group GDI Property Meridian Energy

Industry Insurance real Estate Utilities

Date of IPO 8/1/2013 12/1/2013 10/1/2013

Amount Raised $333.7m $567.7m $1129m

Offer price $333.7m $567.7m $1121m

Offer price 1.2 1 1.8

First day of trading (Closing

price) 1.37 0.89 0.872

5

GDI Property 2014

Growth rate 10.0%

Share price at

close

0.89

Paid dividends 0.04

Cost of equity 13.93%

Meridian Energy 2014

Growth rate 11.0%

Share price at

close

1.445

Paid dividends 0.099

Cost of equity 17.9%

The above table indicates about the relevant levels of cost of equity that was

conducted for the organisation after the on year of the IPO. The information mainly states

that the overall IPO of the company indicates about the change in share price condition.

Before the IPOs the company overall cost of equity is mainly zero, as there is no information,

which can be used for determining the values. However, after the IPO the cost of equity for

each company has mainly changed to new values, which needs to be taken into consideration

by the organisation before selecting investment options. The cost of equity for Steadfast

Group is at 14.9%, while for GDI Property is at 13.93% and for Meridian Energy is at 17.9%.

Perera (2014) stated that cost of equity is considered to be one of the viable investment

options, which can allow the organisation to detect the significance of relevant investments.

2. Understanding the presence of under-pricing with the IPOs:

Company Steadfast Group GDI Property Meridian Energy

Industry Insurance real Estate Utilities

Date of IPO 8/1/2013 12/1/2013 10/1/2013

Amount Raised $333.7m $567.7m $1129m

Offer price $333.7m $567.7m $1121m

Offer price 1.2 1 1.8

First day of trading (Closing

price) 1.37 0.89 0.872

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGING FINANCE

6

First day of trading (Return) 14.17% -11.00% -51.56%

The information indicates that the overall return on the first day of trading for each

IPO that is conducted in the above table. From the relevant analysis, it can be determined that

Steadfast Group has the highest level of returns for the first day of trade, where both GDI

Property and Meridian Energy has conducted losses during the initial trading day. The

difference in the overall returns that was provided during the first day of trade directly

indicates about the presence of underpricing which is conducted to reduce the share price and

improve the level of returns that could be generated by an investor. From the analysis, it can

be determined that maximum of the IPO that is conducted in Australia and around the world

are infected by the underpricing methods that is imposed by the investors to increase their

returns from the initial investment. This type of improvements is also approved by

organizations to readily fulfill their overall share price issue and gather the required level of

funds for their operations. From the study conducted in United States and Australia it was

discovered that 70% of the IPOs that was conducted in USA were underpriced in all sectors.

On the other hand, Australia had only 65% of their IPOs underpriced (Lowry, Michaely &

Volkova, 2017).

3. Determining the IPO activity with the Market conditions of Australia:

Yea

r Number of IPO ALL Ordinary Index Return

2007 260 6417 Activity of IPO ALL Ordinary Index

2008 75 3659 -71% -43%

2009 42 4883 -44% 33%

2010 99 4847 136% -1%

2011 105 4111 6% -15%

2012 51 4665 -51% 13%

2013 61 5353 20% 15%

2014 73 5389 20% 1%

2015 97 5345 33% -1%

6

First day of trading (Return) 14.17% -11.00% -51.56%

The information indicates that the overall return on the first day of trading for each

IPO that is conducted in the above table. From the relevant analysis, it can be determined that

Steadfast Group has the highest level of returns for the first day of trade, where both GDI

Property and Meridian Energy has conducted losses during the initial trading day. The

difference in the overall returns that was provided during the first day of trade directly

indicates about the presence of underpricing which is conducted to reduce the share price and

improve the level of returns that could be generated by an investor. From the analysis, it can

be determined that maximum of the IPO that is conducted in Australia and around the world

are infected by the underpricing methods that is imposed by the investors to increase their

returns from the initial investment. This type of improvements is also approved by

organizations to readily fulfill their overall share price issue and gather the required level of

funds for their operations. From the study conducted in United States and Australia it was

discovered that 70% of the IPOs that was conducted in USA were underpriced in all sectors.

On the other hand, Australia had only 65% of their IPOs underpriced (Lowry, Michaely &

Volkova, 2017).

3. Determining the IPO activity with the Market conditions of Australia:

Yea

r Number of IPO ALL Ordinary Index Return

2007 260 6417 Activity of IPO ALL Ordinary Index

2008 75 3659 -71% -43%

2009 42 4883 -44% 33%

2010 99 4847 136% -1%

2011 105 4111 6% -15%

2012 51 4665 -51% 13%

2013 61 5353 20% 15%

2014 73 5389 20% 1%

2015 97 5345 33% -1%

MANAGING FINANCE

7

2016 94 5719 -3% 7%

2017 115 6167 22% 8%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-100%

-50%

0%

50%

100%

150%

-71%

-44%

136%

6%

-51%

20% 20% 33%

-3%

22%

-43%

33%

-1%

-15%

13% 15% 1% -1% 7% 8%

Activity of IPO

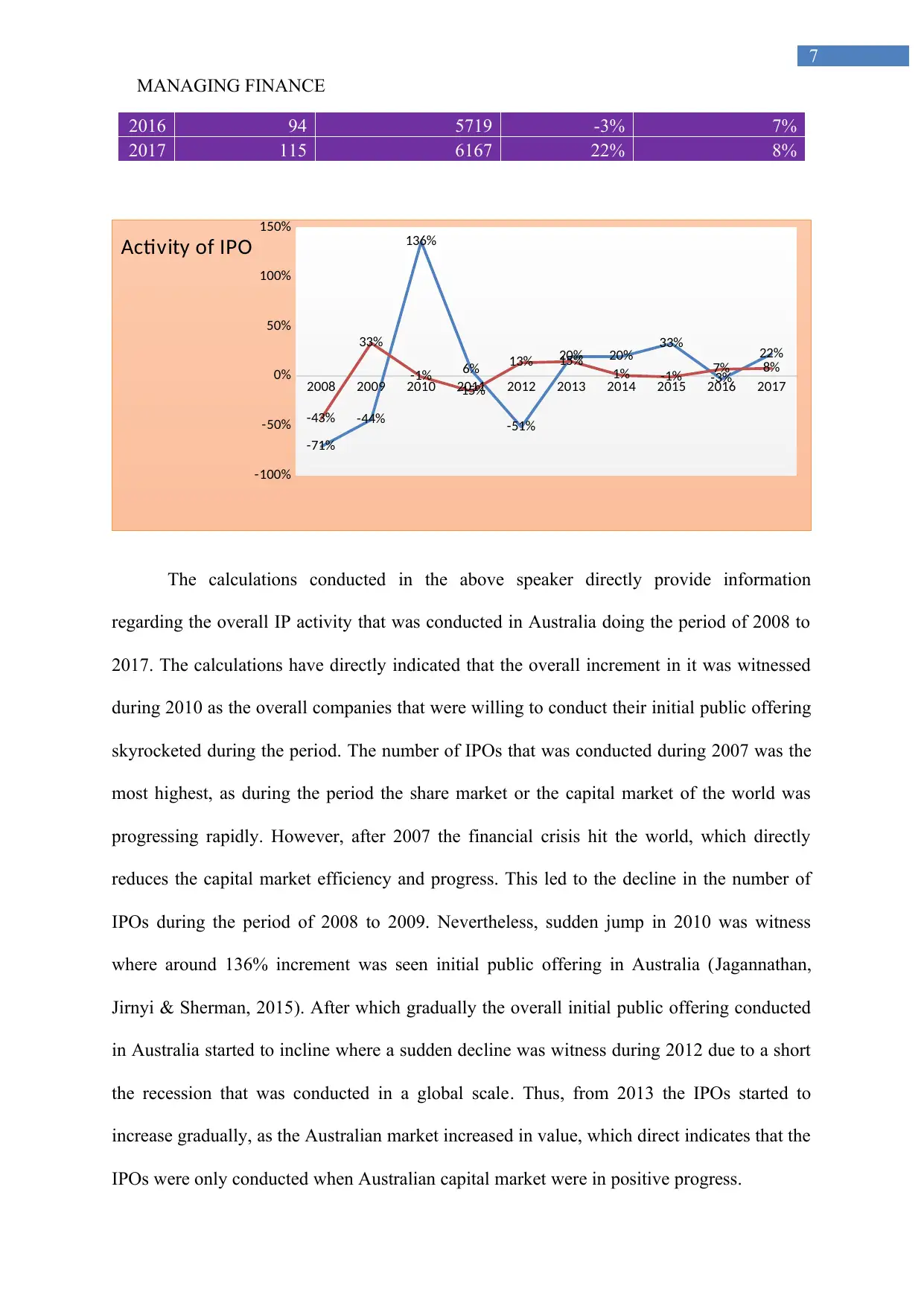

The calculations conducted in the above speaker directly provide information

regarding the overall IP activity that was conducted in Australia doing the period of 2008 to

2017. The calculations have directly indicated that the overall increment in it was witnessed

during 2010 as the overall companies that were willing to conduct their initial public offering

skyrocketed during the period. The number of IPOs that was conducted during 2007 was the

most highest, as during the period the share market or the capital market of the world was

progressing rapidly. However, after 2007 the financial crisis hit the world, which directly

reduces the capital market efficiency and progress. This led to the decline in the number of

IPOs during the period of 2008 to 2009. Nevertheless, sudden jump in 2010 was witness

where around 136% increment was seen initial public offering in Australia (Jagannathan,

Jirnyi & Sherman, 2015). After which gradually the overall initial public offering conducted

in Australia started to incline where a sudden decline was witness during 2012 due to a short

the recession that was conducted in a global scale. Thus, from 2013 the IPOs started to

increase gradually, as the Australian market increased in value, which direct indicates that the

IPOs were only conducted when Australian capital market were in positive progress.

7

2016 94 5719 -3% 7%

2017 115 6167 22% 8%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-100%

-50%

0%

50%

100%

150%

-71%

-44%

136%

6%

-51%

20% 20% 33%

-3%

22%

-43%

33%

-1%

-15%

13% 15% 1% -1% 7% 8%

Activity of IPO

The calculations conducted in the above speaker directly provide information

regarding the overall IP activity that was conducted in Australia doing the period of 2008 to

2017. The calculations have directly indicated that the overall increment in it was witnessed

during 2010 as the overall companies that were willing to conduct their initial public offering

skyrocketed during the period. The number of IPOs that was conducted during 2007 was the

most highest, as during the period the share market or the capital market of the world was

progressing rapidly. However, after 2007 the financial crisis hit the world, which directly

reduces the capital market efficiency and progress. This led to the decline in the number of

IPOs during the period of 2008 to 2009. Nevertheless, sudden jump in 2010 was witness

where around 136% increment was seen initial public offering in Australia (Jagannathan,

Jirnyi & Sherman, 2015). After which gradually the overall initial public offering conducted

in Australia started to incline where a sudden decline was witness during 2012 due to a short

the recession that was conducted in a global scale. Thus, from 2013 the IPOs started to

increase gradually, as the Australian market increased in value, which direct indicates that the

IPOs were only conducted when Australian capital market were in positive progress.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGING FINANCE

8

4. The performance within three years after the IPO without dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return without dividends

All Ordinary Index Steadfast Group GDI Property Meridian Energy

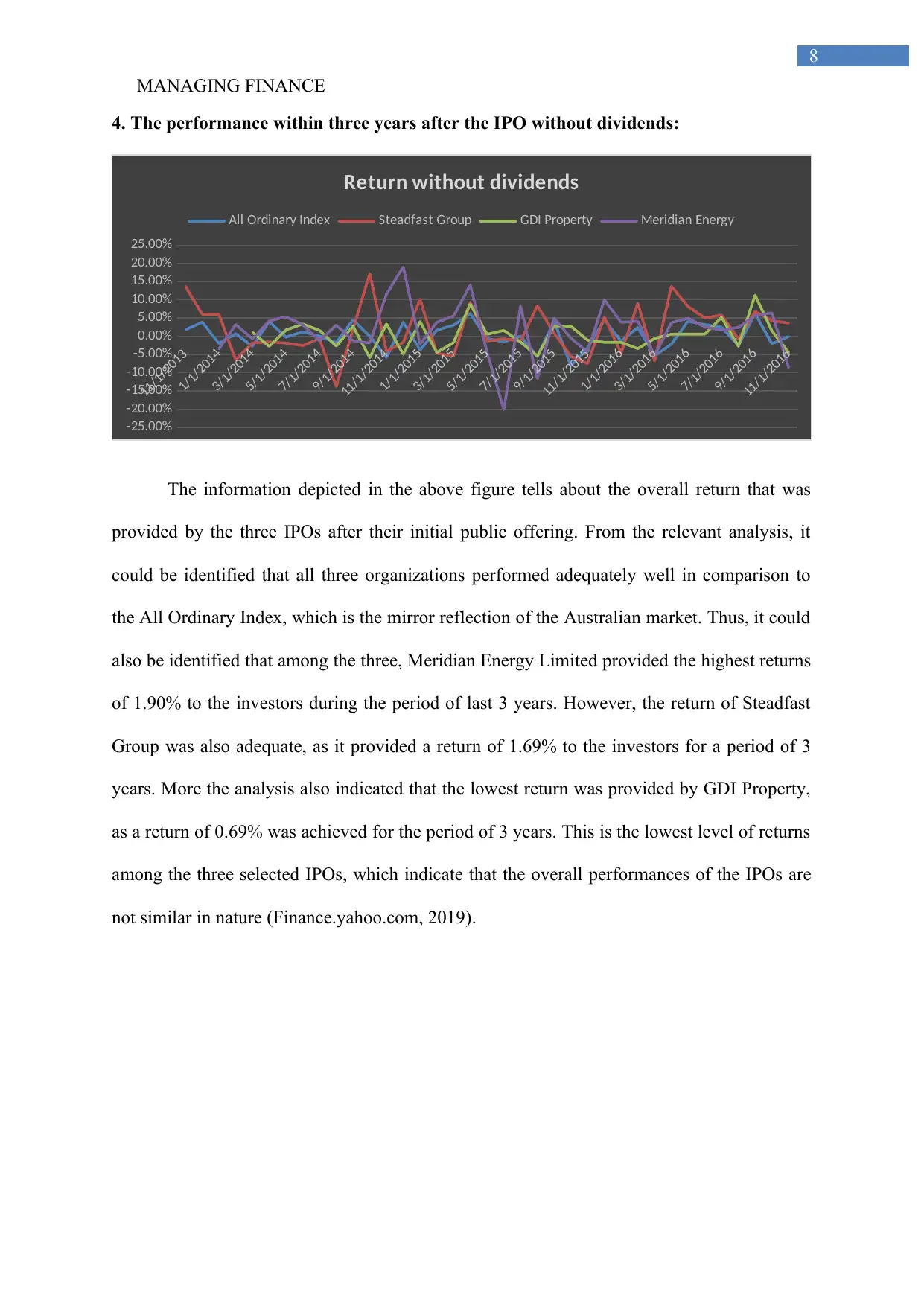

The information depicted in the above figure tells about the overall return that was

provided by the three IPOs after their initial public offering. From the relevant analysis, it

could be identified that all three organizations performed adequately well in comparison to

the All Ordinary Index, which is the mirror reflection of the Australian market. Thus, it could

also be identified that among the three, Meridian Energy Limited provided the highest returns

of 1.90% to the investors during the period of last 3 years. However, the return of Steadfast

Group was also adequate, as it provided a return of 1.69% to the investors for a period of 3

years. More the analysis also indicated that the lowest return was provided by GDI Property,

as a return of 0.69% was achieved for the period of 3 years. This is the lowest level of returns

among the three selected IPOs, which indicate that the overall performances of the IPOs are

not similar in nature (Finance.yahoo.com, 2019).

8

4. The performance within three years after the IPO without dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return without dividends

All Ordinary Index Steadfast Group GDI Property Meridian Energy

The information depicted in the above figure tells about the overall return that was

provided by the three IPOs after their initial public offering. From the relevant analysis, it

could be identified that all three organizations performed adequately well in comparison to

the All Ordinary Index, which is the mirror reflection of the Australian market. Thus, it could

also be identified that among the three, Meridian Energy Limited provided the highest returns

of 1.90% to the investors during the period of last 3 years. However, the return of Steadfast

Group was also adequate, as it provided a return of 1.69% to the investors for a period of 3

years. More the analysis also indicated that the lowest return was provided by GDI Property,

as a return of 0.69% was achieved for the period of 3 years. This is the lowest level of returns

among the three selected IPOs, which indicate that the overall performances of the IPOs are

not similar in nature (Finance.yahoo.com, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGING FINANCE

9

5. The performance within three years after the IPO with dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return with dividends

Steadfast Group GDI Property Meridian Energy

All Ordinary

Index

Steadfast

Group

GDI

Property

Meridian

Energy

Return with

dividends 0.27% 2.03% 0.92% 2.23%

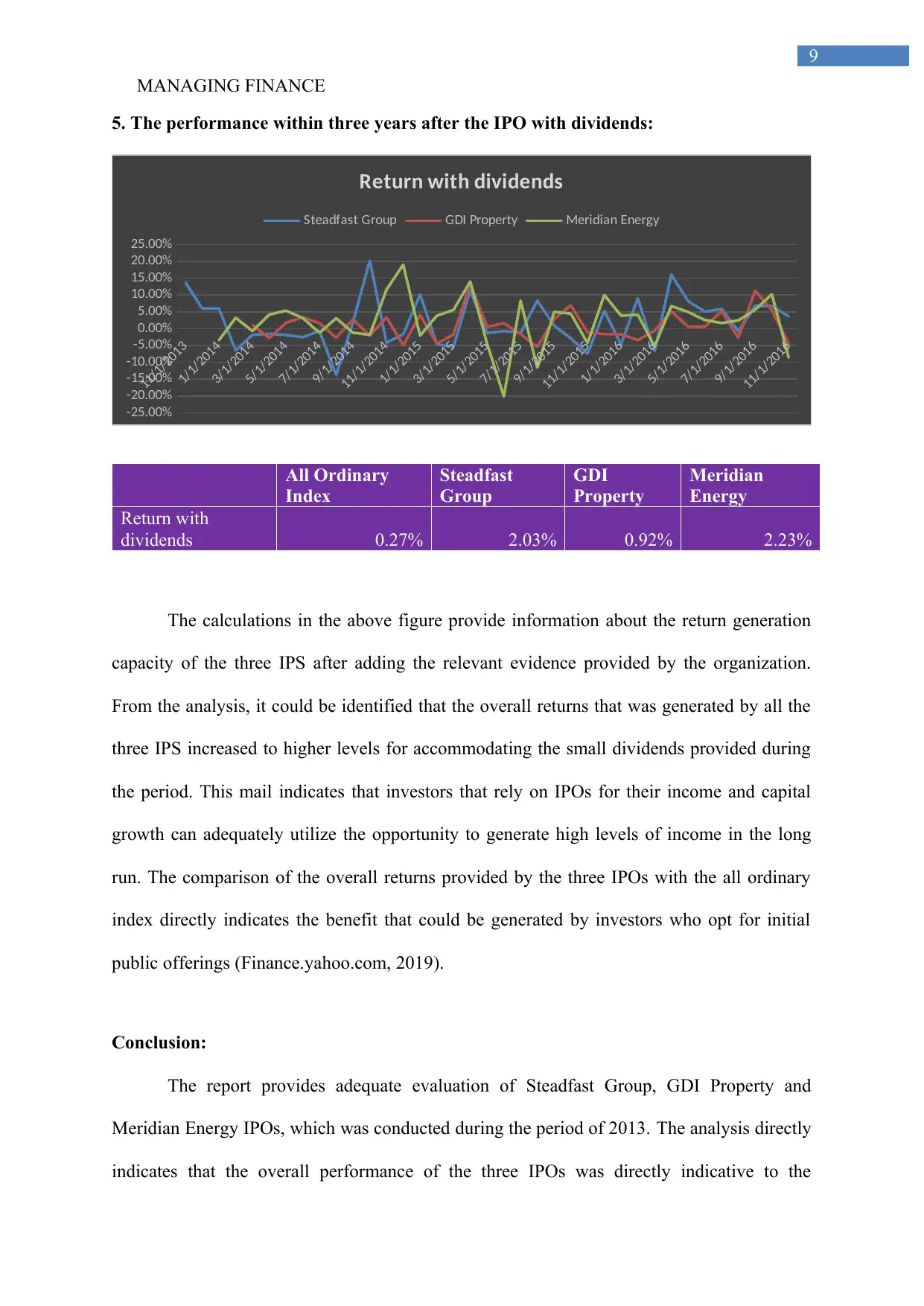

The calculations in the above figure provide information about the return generation

capacity of the three IPS after adding the relevant evidence provided by the organization.

From the analysis, it could be identified that the overall returns that was generated by all the

three IPS increased to higher levels for accommodating the small dividends provided during

the period. This mail indicates that investors that rely on IPOs for their income and capital

growth can adequately utilize the opportunity to generate high levels of income in the long

run. The comparison of the overall returns provided by the three IPOs with the all ordinary

index directly indicates the benefit that could be generated by investors who opt for initial

public offerings (Finance.yahoo.com, 2019).

Conclusion:

The report provides adequate evaluation of Steadfast Group, GDI Property and

Meridian Energy IPOs, which was conducted during the period of 2013. The analysis directly

indicates that the overall performance of the three IPOs was directly indicative to the

9

5. The performance within three years after the IPO with dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return with dividends

Steadfast Group GDI Property Meridian Energy

All Ordinary

Index

Steadfast

Group

GDI

Property

Meridian

Energy

Return with

dividends 0.27% 2.03% 0.92% 2.23%

The calculations in the above figure provide information about the return generation

capacity of the three IPS after adding the relevant evidence provided by the organization.

From the analysis, it could be identified that the overall returns that was generated by all the

three IPS increased to higher levels for accommodating the small dividends provided during

the period. This mail indicates that investors that rely on IPOs for their income and capital

growth can adequately utilize the opportunity to generate high levels of income in the long

run. The comparison of the overall returns provided by the three IPOs with the all ordinary

index directly indicates the benefit that could be generated by investors who opt for initial

public offerings (Finance.yahoo.com, 2019).

Conclusion:

The report provides adequate evaluation of Steadfast Group, GDI Property and

Meridian Energy IPOs, which was conducted during the period of 2013. The analysis directly

indicates that the overall performance of the three IPOs was directly indicative to the

MANAGING FINANCE

10

performance of the organization and the attributes of their industry. The companies were able

to generate high level of returns in comparison to the All Ordinary Index, which indicates

about the significance of initial public offerings that could allow investors to increase their

investment scope and return generation capability. The presence of underpricing in IPOs is

also justified, as it benefits both the companies and investors in the long run. Further

evaluation indicated about the relationships that are present between the market performance

and IPO activity in Australia, which is significant.

10

performance of the organization and the attributes of their industry. The companies were able

to generate high level of returns in comparison to the All Ordinary Index, which indicates

about the significance of initial public offerings that could allow investors to increase their

investment scope and return generation capability. The presence of underpricing in IPOs is

also justified, as it benefits both the companies and investors in the long run. Further

evaluation indicated about the relationships that are present between the market performance

and IPO activity in Australia, which is significant.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.