FINA6000: Analysis of IPOs and Financial Performance in Australia

VerifiedAdded on 2022/09/29

|13

|2794

|20

Report

AI Summary

This report provides a comprehensive analysis of Initial Public Offerings (IPOs) by Australian companies, focusing on the financial aspects of capital raising and its impact on firm performance. The analysis begins by evaluating the measures taken by three companies—National Storage, Sandon Capital Investments, and Pact Group—to initiate their IPOs, examining their fund-raising goals and the use of proceeds. The report then delves into the cost of equity calculations for these companies, assessing the minimum returns required post-IPO. A key aspect of the study is an analysis of the impact of underpricing in the Australian capital market, including an examination of first-day trading returns. Furthermore, the report investigates the relationship between IPO activities and the returns of the All Ordinaries Index, exploring how market performance influences IPOs. The returns provided by IPOs, both with and without dividends, are compared to assess the overall investment performance. The study concludes by synthesizing the key findings regarding the significance of IPOs in improving capital structure and financial accountability, offering insights for investors and companies alike.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

1

Table of Contents

Introduction:...............................................................................................................................2

a. Evaluating the measures that were taken by the three companies for initiating the initial

public offerings:.........................................................................................................................2

b. Understanding the cost of equity that is conducted for long term finance:...........................4

c. Analysing and authenticating the impact of under-pricing in a capital market:....................5

d. Understanding the Australian IPO activity:...........................................................................6

e. Understanding the returns provided by IPO without dividends:............................................8

f. Understanding the returns provided by IPO with dividends:.................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

1

Table of Contents

Introduction:...............................................................................................................................2

a. Evaluating the measures that were taken by the three companies for initiating the initial

public offerings:.........................................................................................................................2

b. Understanding the cost of equity that is conducted for long term finance:...........................4

c. Analysing and authenticating the impact of under-pricing in a capital market:....................5

d. Understanding the Australian IPO activity:...........................................................................6

e. Understanding the returns provided by IPO without dividends:............................................8

f. Understanding the returns provided by IPO with dividends:.................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

FINANCIAL MANAGEMENT

2

Introduction:

Initial public offerings are considered to be one of the essential components or

technique, which is used by the organisation for adequately acquiring the required level of

funds from the capital market. This technique is used for generating the required level of

funds for supporting further activities and increases their financial capability in the long run.

The information regarding the cost of equity that has changed after the initial public offerings

are also discussed which helps in detecting the level of minimum returns that need to be

provided by organisation after their IPO. The significance and problems that was associated

with the under-pricing measure are adequately conducted to detect its impact on the

Australian capital market. Furthermost, the IPO activities are evaluated and compared with

the Australian capital market to understand its relationship. Lastly, the performance of the

IPOs is mainly compared with the ALL Ordinary Index to detect the level income that would

be enjoyed by investors if they tend to support investments during the Initial public offerings.

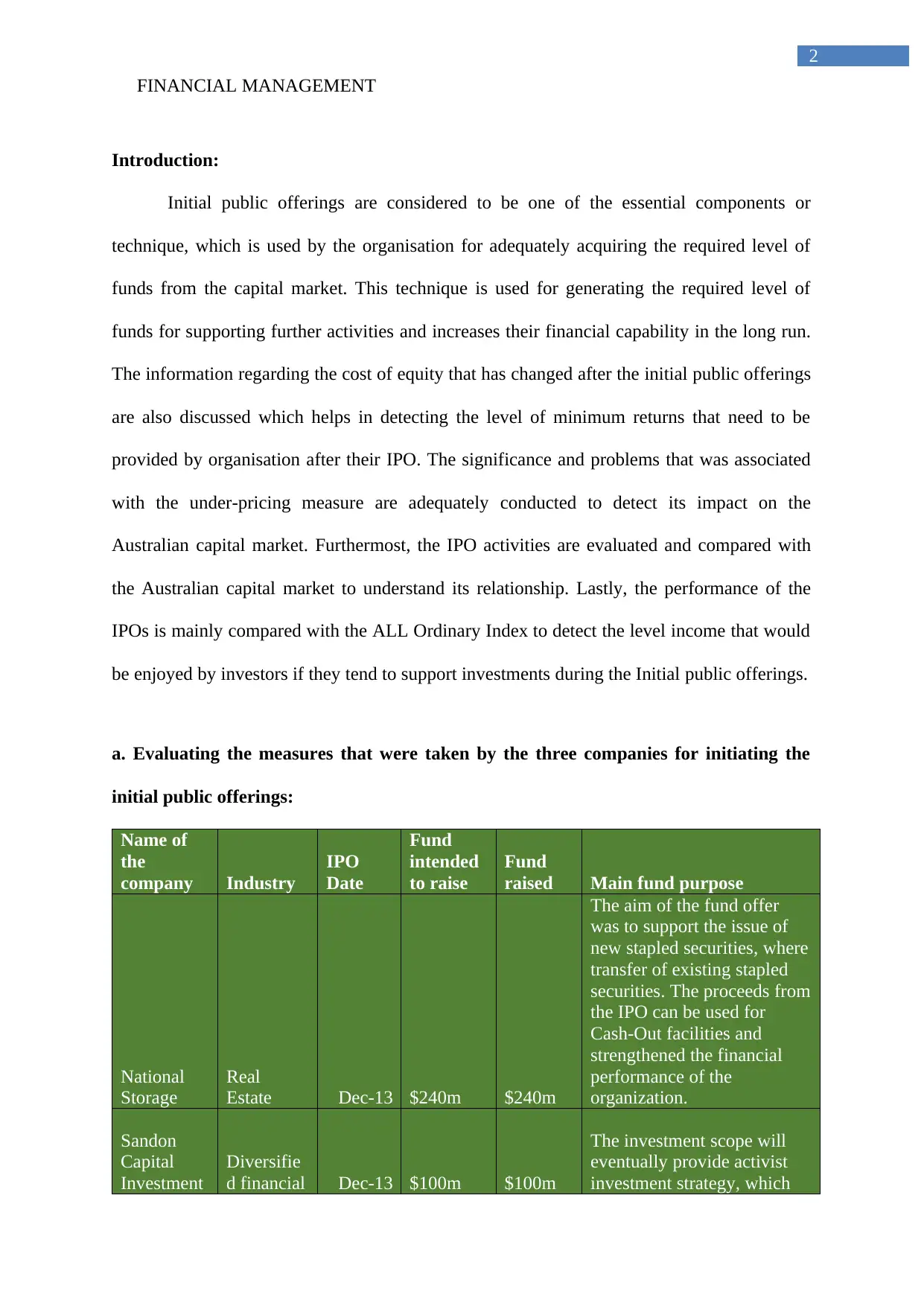

a. Evaluating the measures that were taken by the three companies for initiating the

initial public offerings:

Name of

the

company Industry

IPO

Date

Fund

intended

to raise

Fund

raised Main fund purpose

National

Storage

Real

Estate Dec-13 $240m $240m

The aim of the fund offer

was to support the issue of

new stapled securities, where

transfer of existing stapled

securities. The proceeds from

the IPO can be used for

Cash-Out facilities and

strengthened the financial

performance of the

organization.

Sandon

Capital

Investment

Diversifie

d financial Dec-13 $100m $100m

The investment scope will

eventually provide activist

investment strategy, which

2

Introduction:

Initial public offerings are considered to be one of the essential components or

technique, which is used by the organisation for adequately acquiring the required level of

funds from the capital market. This technique is used for generating the required level of

funds for supporting further activities and increases their financial capability in the long run.

The information regarding the cost of equity that has changed after the initial public offerings

are also discussed which helps in detecting the level of minimum returns that need to be

provided by organisation after their IPO. The significance and problems that was associated

with the under-pricing measure are adequately conducted to detect its impact on the

Australian capital market. Furthermost, the IPO activities are evaluated and compared with

the Australian capital market to understand its relationship. Lastly, the performance of the

IPOs is mainly compared with the ALL Ordinary Index to detect the level income that would

be enjoyed by investors if they tend to support investments during the Initial public offerings.

a. Evaluating the measures that were taken by the three companies for initiating the

initial public offerings:

Name of

the

company Industry

IPO

Date

Fund

intended

to raise

Fund

raised Main fund purpose

National

Storage

Real

Estate Dec-13 $240m $240m

The aim of the fund offer

was to support the issue of

new stapled securities, where

transfer of existing stapled

securities. The proceeds from

the IPO can be used for

Cash-Out facilities and

strengthened the financial

performance of the

organization.

Sandon

Capital

Investment

Diversifie

d financial Dec-13 $100m $100m

The investment scope will

eventually provide activist

investment strategy, which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT

3

s

would help in improving

their investment capacity. In

addition, the IPO would help

in delivering absolute

positive return over the

medium and long term

growth. The company aims

in generating high level of

dividends to the investors

who intend to generate high

level of return from

investment.

Pact Group Material Dec-13 $648.8m $648.8m

The main purpose of the

offer is to activate the listing

of the organization in ASX

and providing relevant option

for the liquid market. In

addition, the IPO would

provide financial flexibility

to pursue future growth

opportunities. This also

provide future access to

capital markets and realize a

portion of its investment,

while maintaining a

significant ongoing interest

in pact.

The above data has been derived from the prospectus of National Storage, Sandon

Capital Investments and Pact Group during the period of 2013. The prospectus directly

provided all the relevant information regarding the industry type, IPO date, funds intended to

raise and fund raised by the organization after the initial public offerings. Further analysis

was provided on the main purposes that were used by the management to initiate the public

offering, which is mainly required to provide relevant information to investors regarding the

main motive behind the public offerings (Asx.com.au, 2019).

The main reason behind the IPO of National Storage was to increase aim of the fund

offer was to support the issue of new stapled securities, where transfer of existing stapled

securities. The proceeds from the IPO can be used for Cash-Out facilities and improve the

3

s

would help in improving

their investment capacity. In

addition, the IPO would help

in delivering absolute

positive return over the

medium and long term

growth. The company aims

in generating high level of

dividends to the investors

who intend to generate high

level of return from

investment.

Pact Group Material Dec-13 $648.8m $648.8m

The main purpose of the

offer is to activate the listing

of the organization in ASX

and providing relevant option

for the liquid market. In

addition, the IPO would

provide financial flexibility

to pursue future growth

opportunities. This also

provide future access to

capital markets and realize a

portion of its investment,

while maintaining a

significant ongoing interest

in pact.

The above data has been derived from the prospectus of National Storage, Sandon

Capital Investments and Pact Group during the period of 2013. The prospectus directly

provided all the relevant information regarding the industry type, IPO date, funds intended to

raise and fund raised by the organization after the initial public offerings. Further analysis

was provided on the main purposes that were used by the management to initiate the public

offering, which is mainly required to provide relevant information to investors regarding the

main motive behind the public offerings (Asx.com.au, 2019).

The main reason behind the IPO of National Storage was to increase aim of the fund

offer was to support the issue of new stapled securities, where transfer of existing stapled

securities. The proceeds from the IPO can be used for Cash-Out facilities and improve the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

4

management’s capital financial opportunity. Furthermore, with Sandon Capital Investments

investment scope will eventually provide activist investment strategy and IPO would help in

delivering absolute positive return over the medium and long term growth. Therefore, the

company with the help of IPO was not to increase the level of returns that would be provided

to the investors over the period of time. Additionally, the Pact Group would initiate the IPO

for providing relevant option for the liquid market, which would help in financial flexibility

to pursue future growth opportunities. Thus, the management aims in increasing their capital

formation, which could help in generating high level of generating high level of income from

investment (Asx.com.au, 2019).

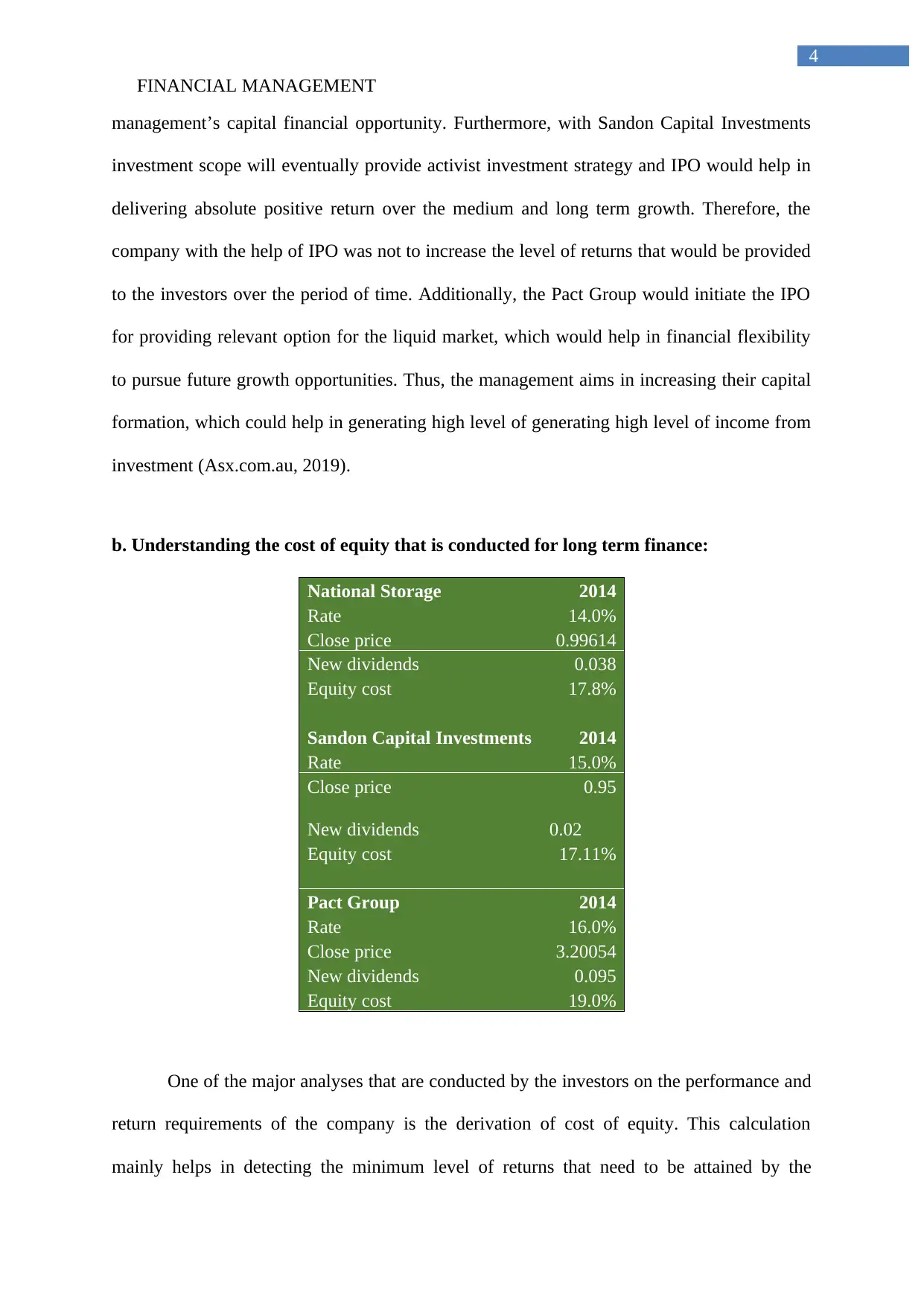

b. Understanding the cost of equity that is conducted for long term finance:

National Storage 2014

Rate 14.0%

Close price 0.99614

New dividends 0.038

Equity cost 17.8%

Sandon Capital Investments 2014

Rate 15.0%

Close price 0.95

New dividends 0.02

Equity cost 17.11%

Pact Group 2014

Rate 16.0%

Close price 3.20054

New dividends 0.095

Equity cost 19.0%

One of the major analyses that are conducted by the investors on the performance and

return requirements of the company is the derivation of cost of equity. This calculation

mainly helps in detecting the minimum level of returns that need to be attained by the

4

management’s capital financial opportunity. Furthermore, with Sandon Capital Investments

investment scope will eventually provide activist investment strategy and IPO would help in

delivering absolute positive return over the medium and long term growth. Therefore, the

company with the help of IPO was not to increase the level of returns that would be provided

to the investors over the period of time. Additionally, the Pact Group would initiate the IPO

for providing relevant option for the liquid market, which would help in financial flexibility

to pursue future growth opportunities. Thus, the management aims in increasing their capital

formation, which could help in generating high level of generating high level of income from

investment (Asx.com.au, 2019).

b. Understanding the cost of equity that is conducted for long term finance:

National Storage 2014

Rate 14.0%

Close price 0.99614

New dividends 0.038

Equity cost 17.8%

Sandon Capital Investments 2014

Rate 15.0%

Close price 0.95

New dividends 0.02

Equity cost 17.11%

Pact Group 2014

Rate 16.0%

Close price 3.20054

New dividends 0.095

Equity cost 19.0%

One of the major analyses that are conducted by the investors on the performance and

return requirements of the company is the derivation of cost of equity. This calculation

mainly helps in detecting the minimum level of returns that need to be attained by the

FINANCIAL MANAGEMENT

5

company to survive the dividend obligations from the capital market. The analysis has mainly

indicated that the overall cost of equity directly supports the organisation to understand the

level of minimum returns that could be generated from an investment. In the similar process

the overall cost of equity for each organisation depicted in the above table directly ranges

from 17% to 19%. Hoesli & MacGregor (2014) stated that with the help of equity cost

calculations organisation are able to understand the required rate of return, which needs to be

conducted for selecting the most appropriate investment options.

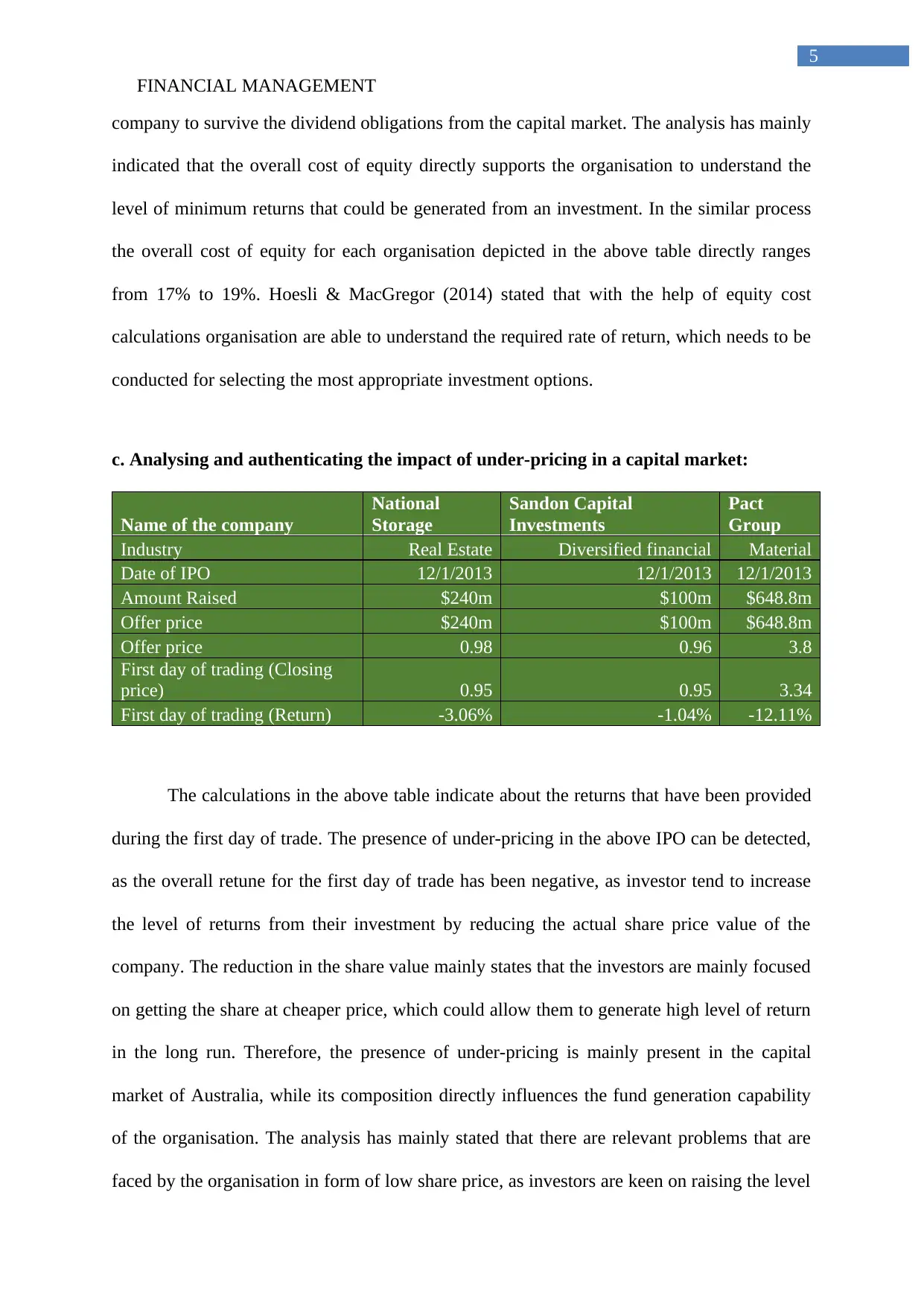

c. Analysing and authenticating the impact of under-pricing in a capital market:

Name of the company

National

Storage

Sandon Capital

Investments

Pact

Group

Industry Real Estate Diversified financial Material

Date of IPO 12/1/2013 12/1/2013 12/1/2013

Amount Raised $240m $100m $648.8m

Offer price $240m $100m $648.8m

Offer price 0.98 0.96 3.8

First day of trading (Closing

price) 0.95 0.95 3.34

First day of trading (Return) -3.06% -1.04% -12.11%

The calculations in the above table indicate about the returns that have been provided

during the first day of trade. The presence of under-pricing in the above IPO can be detected,

as the overall retune for the first day of trade has been negative, as investor tend to increase

the level of returns from their investment by reducing the actual share price value of the

company. The reduction in the share value mainly states that the investors are mainly focused

on getting the share at cheaper price, which could allow them to generate high level of return

in the long run. Therefore, the presence of under-pricing is mainly present in the capital

market of Australia, while its composition directly influences the fund generation capability

of the organisation. The analysis has mainly stated that there are relevant problems that are

faced by the organisation in form of low share price, as investors are keen on raising the level

5

company to survive the dividend obligations from the capital market. The analysis has mainly

indicated that the overall cost of equity directly supports the organisation to understand the

level of minimum returns that could be generated from an investment. In the similar process

the overall cost of equity for each organisation depicted in the above table directly ranges

from 17% to 19%. Hoesli & MacGregor (2014) stated that with the help of equity cost

calculations organisation are able to understand the required rate of return, which needs to be

conducted for selecting the most appropriate investment options.

c. Analysing and authenticating the impact of under-pricing in a capital market:

Name of the company

National

Storage

Sandon Capital

Investments

Pact

Group

Industry Real Estate Diversified financial Material

Date of IPO 12/1/2013 12/1/2013 12/1/2013

Amount Raised $240m $100m $648.8m

Offer price $240m $100m $648.8m

Offer price 0.98 0.96 3.8

First day of trading (Closing

price) 0.95 0.95 3.34

First day of trading (Return) -3.06% -1.04% -12.11%

The calculations in the above table indicate about the returns that have been provided

during the first day of trade. The presence of under-pricing in the above IPO can be detected,

as the overall retune for the first day of trade has been negative, as investor tend to increase

the level of returns from their investment by reducing the actual share price value of the

company. The reduction in the share value mainly states that the investors are mainly focused

on getting the share at cheaper price, which could allow them to generate high level of return

in the long run. Therefore, the presence of under-pricing is mainly present in the capital

market of Australia, while its composition directly influences the fund generation capability

of the organisation. The analysis has mainly stated that there are relevant problems that are

faced by the organisation in form of low share price, as investors are keen on raising the level

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT

6

of returns from their initial investment. Hence, the analysis directly states that underprizing

plagues the capital market of Australia.

Underprizing method is mainly used by the undertaken of the shares, who intendeds

to compete the share price selling process during the IPO, as it allows the organisation to

obtain the required level of returns from investment. However, the intention of the

underwriter is to complete the IPO process and allow the organisation to obtained adequate

level of funds for the future activities. Hence, both the investors and companies benefit from

the underprizing menthe, as investors are able to increase the level of return from their

investment, while companies are able to gather the required funds quickly (Chandra, 2017).

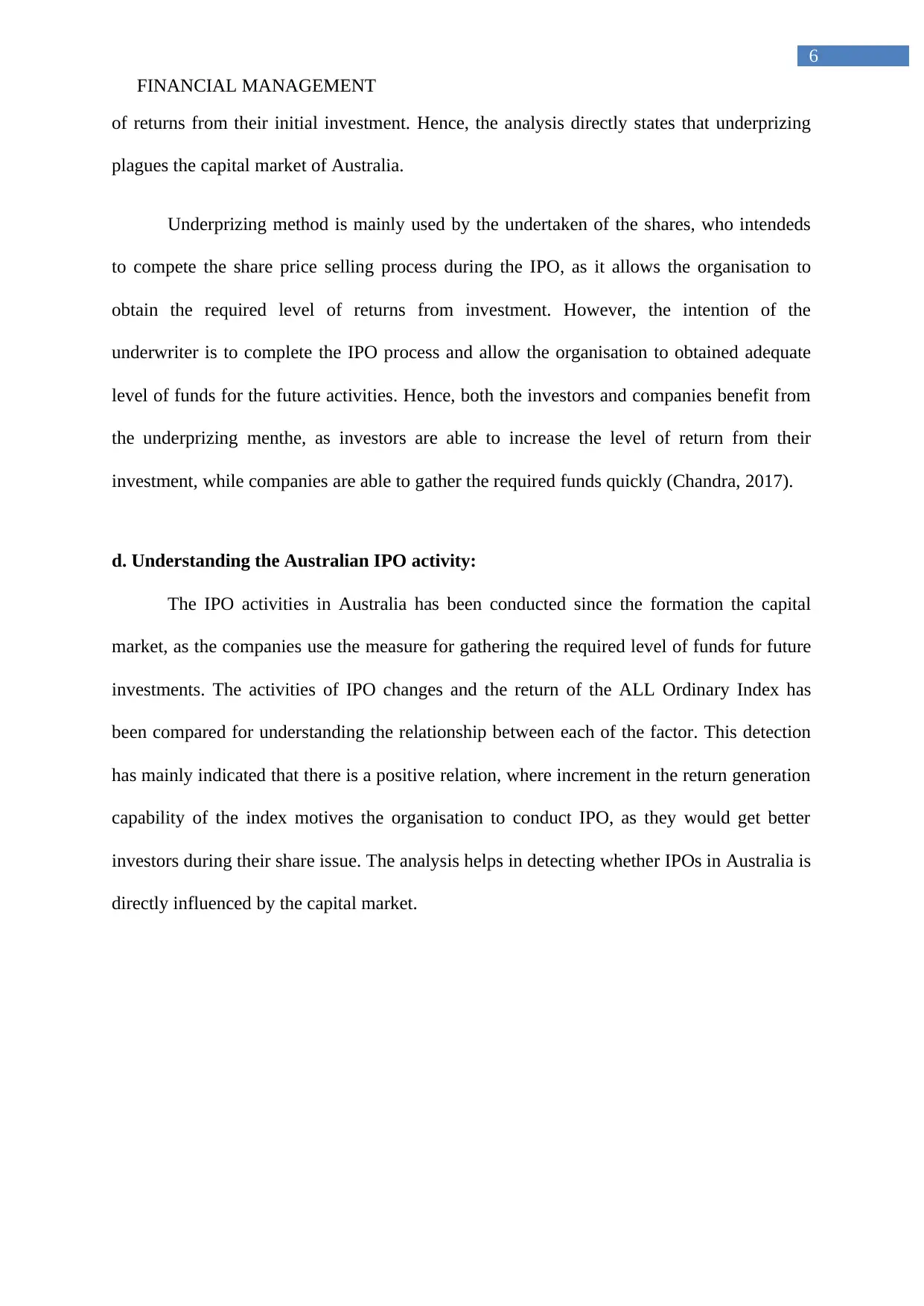

d. Understanding the Australian IPO activity:

The IPO activities in Australia has been conducted since the formation the capital

market, as the companies use the measure for gathering the required level of funds for future

investments. The activities of IPO changes and the return of the ALL Ordinary Index has

been compared for understanding the relationship between each of the factor. This detection

has mainly indicated that there is a positive relation, where increment in the return generation

capability of the index motives the organisation to conduct IPO, as they would get better

investors during their share issue. The analysis helps in detecting whether IPOs in Australia is

directly influenced by the capital market.

6

of returns from their initial investment. Hence, the analysis directly states that underprizing

plagues the capital market of Australia.

Underprizing method is mainly used by the undertaken of the shares, who intendeds

to compete the share price selling process during the IPO, as it allows the organisation to

obtain the required level of returns from investment. However, the intention of the

underwriter is to complete the IPO process and allow the organisation to obtained adequate

level of funds for the future activities. Hence, both the investors and companies benefit from

the underprizing menthe, as investors are able to increase the level of return from their

investment, while companies are able to gather the required funds quickly (Chandra, 2017).

d. Understanding the Australian IPO activity:

The IPO activities in Australia has been conducted since the formation the capital

market, as the companies use the measure for gathering the required level of funds for future

investments. The activities of IPO changes and the return of the ALL Ordinary Index has

been compared for understanding the relationship between each of the factor. This detection

has mainly indicated that there is a positive relation, where increment in the return generation

capability of the index motives the organisation to conduct IPO, as they would get better

investors during their share issue. The analysis helps in detecting whether IPOs in Australia is

directly influenced by the capital market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

7

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-100.000%

-50.000%

0.000%

50.000%

100.000%

150.000%

-71.154%

-44.000%

135.714%

6.061%

-51.429%

19.608% 19.672%

32.877%

-3.093%

22.340%

-42.972%

33.433%

-0.733%

-15.183%

13.466% 14.760%

0.663% -0.817% 7.007% 7.837%

Australian IPO Activity Return Activity of IPO

Return ALL Ordinary Index

The values of the IPO have been depicted in the above figure, where it is understood

that return of the IPO is linked with the activities of the IPO. Hence, whenever the return of

the capital market increases the overall activities of the IPO increases drastically. The return

of the market from 2008 to 2009 mainly increased by 33.433%, which led to the increment in

IPO activities from -44.00% to 135.714%. Thus, it can be stated that whether the overall

returns of the capital market increase the following year the level of IPO activities in the

Australian country raises to new levels whomever due to the introduction of the financial

crisis during 2008 and 2012 the overall IPO activities would be seen to deteriorate. Thus, it

could be clinched that IPO activities is positively linked with the capital market returns and

upward movements (Low, Yao& Faff, 2016).

7

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-100.000%

-50.000%

0.000%

50.000%

100.000%

150.000%

-71.154%

-44.000%

135.714%

6.061%

-51.429%

19.608% 19.672%

32.877%

-3.093%

22.340%

-42.972%

33.433%

-0.733%

-15.183%

13.466% 14.760%

0.663% -0.817% 7.007% 7.837%

Australian IPO Activity Return Activity of IPO

Return ALL Ordinary Index

The values of the IPO have been depicted in the above figure, where it is understood

that return of the IPO is linked with the activities of the IPO. Hence, whenever the return of

the capital market increases the overall activities of the IPO increases drastically. The return

of the market from 2008 to 2009 mainly increased by 33.433%, which led to the increment in

IPO activities from -44.00% to 135.714%. Thus, it can be stated that whether the overall

returns of the capital market increase the following year the level of IPO activities in the

Australian country raises to new levels whomever due to the introduction of the financial

crisis during 2008 and 2012 the overall IPO activities would be seen to deteriorate. Thus, it

could be clinched that IPO activities is positively linked with the capital market returns and

upward movements (Low, Yao& Faff, 2016).

FINANCIAL MANAGEMENT

8

e. Understanding the returns provided by IPO without dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

R eturn without dividends

All Ordinary Index National Storage

Sandon Capital Invetments Pact Group

The analysis of the above figure has mainly indicated that the return generation

capacity of the three IPOs listed during 2013 has mainly outperformed the market All

Ordinary Index. The All-ordinary Index is mainly considered to be one of the major

representor of the Australian capital market. The analysis has detected that All Ordinary

Index during three-year period was only able to generate 0.22%, while National Storage

incurred a return of 1.10%, Sandon Capital Investments generated a return of 0.33%, while

Pact Group obtained 1.91% during the period. The analysis has been detected that

performance of the all the three IPOs were adequate and could allow the investors to generate

high level of returns in the long run. Altuntas & Dereli (2015) stated that investors by using

the IPO issue are able to conduct relevant investments and grab stock at discount rate, which

might help in generating high level of returns in the long run.

8

e. Understanding the returns provided by IPO without dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

R eturn without dividends

All Ordinary Index National Storage

Sandon Capital Invetments Pact Group

The analysis of the above figure has mainly indicated that the return generation

capacity of the three IPOs listed during 2013 has mainly outperformed the market All

Ordinary Index. The All-ordinary Index is mainly considered to be one of the major

representor of the Australian capital market. The analysis has detected that All Ordinary

Index during three-year period was only able to generate 0.22%, while National Storage

incurred a return of 1.10%, Sandon Capital Investments generated a return of 0.33%, while

Pact Group obtained 1.91% during the period. The analysis has been detected that

performance of the all the three IPOs were adequate and could allow the investors to generate

high level of returns in the long run. Altuntas & Dereli (2015) stated that investors by using

the IPO issue are able to conduct relevant investments and grab stock at discount rate, which

might help in generating high level of returns in the long run.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL MANAGEMENT

9

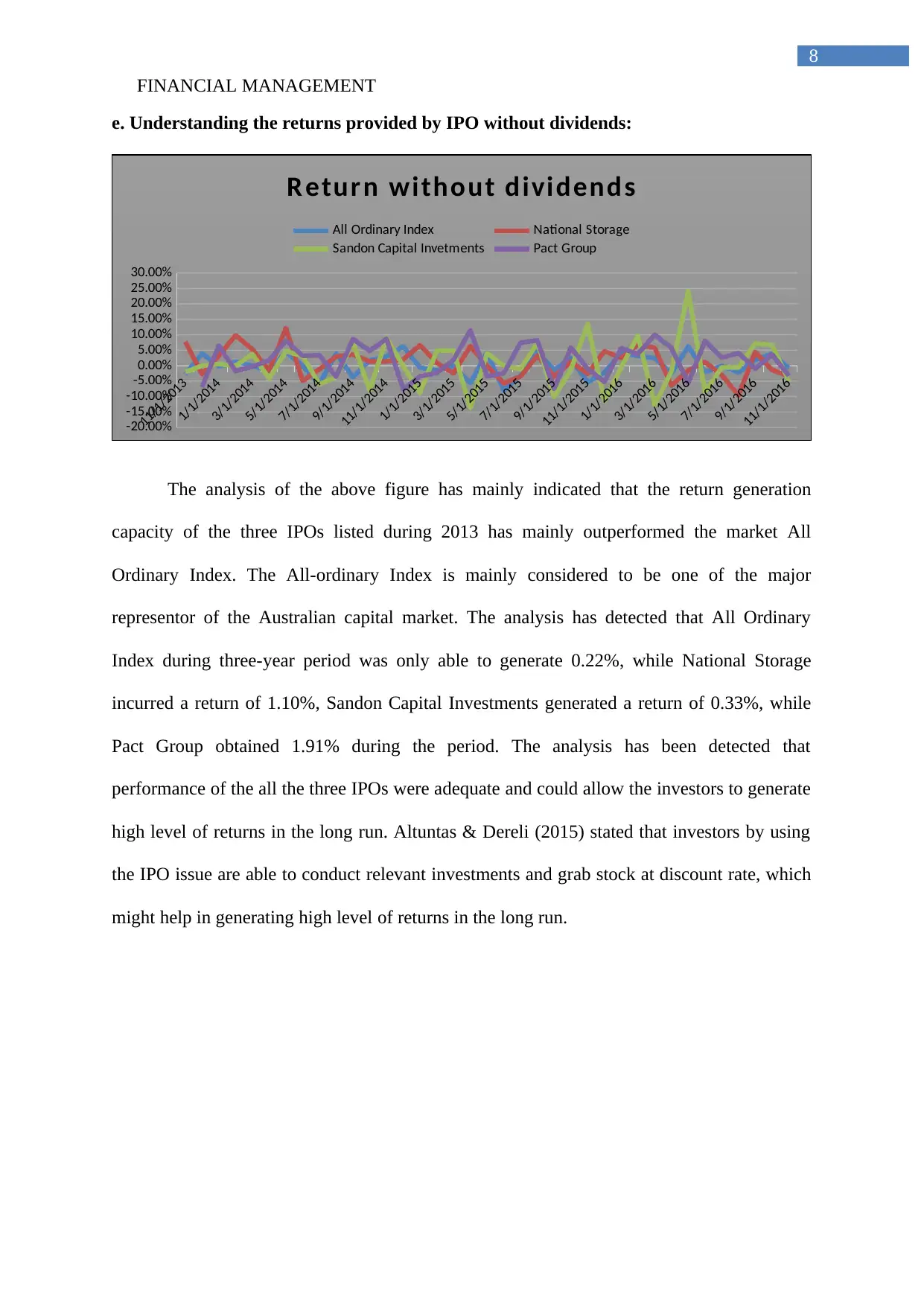

f. Understanding the returns provided by IPO with dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

R eturn with dividends

National Storage Sandon Capital Invetments Pact Group

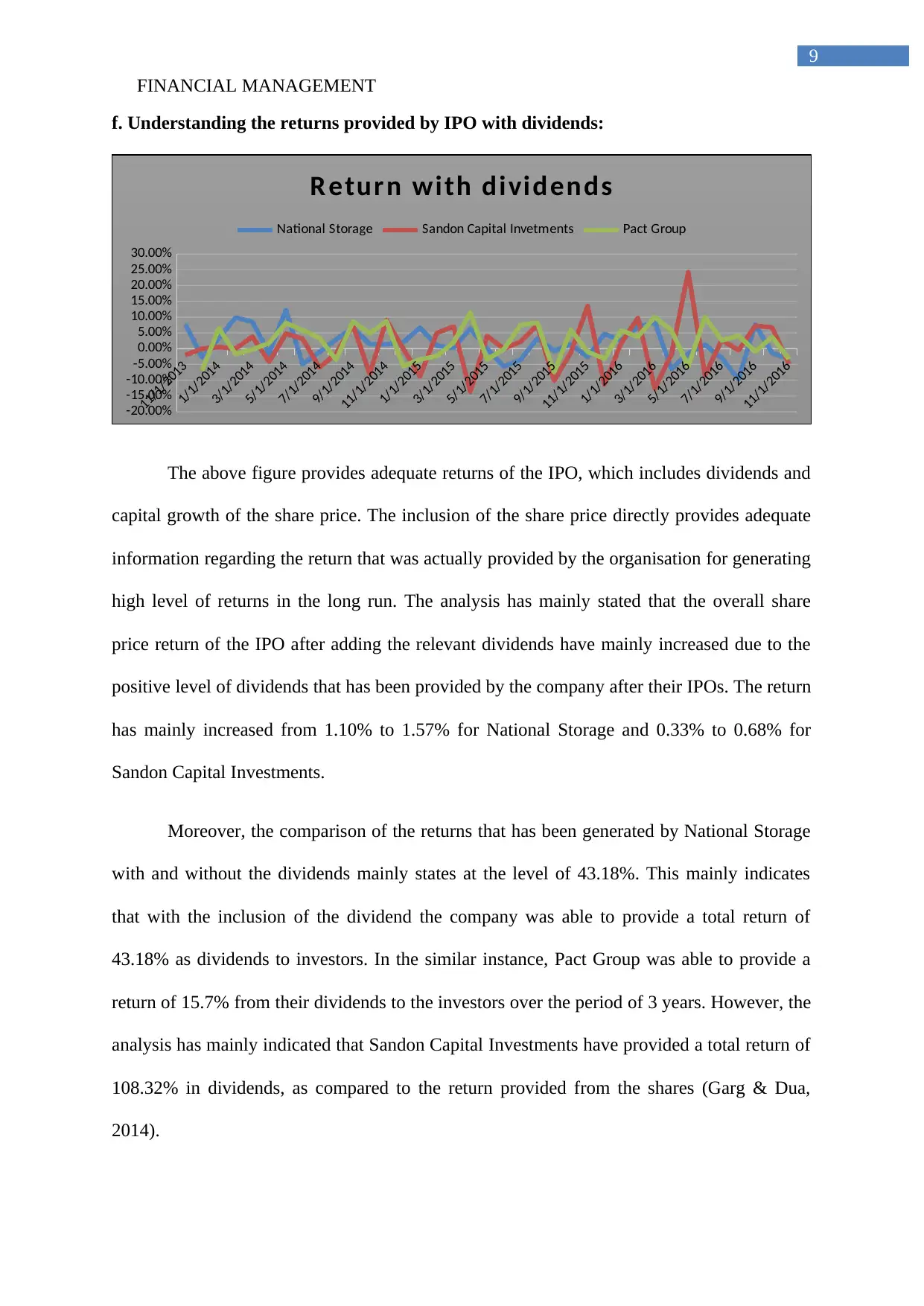

The above figure provides adequate returns of the IPO, which includes dividends and

capital growth of the share price. The inclusion of the share price directly provides adequate

information regarding the return that was actually provided by the organisation for generating

high level of returns in the long run. The analysis has mainly stated that the overall share

price return of the IPO after adding the relevant dividends have mainly increased due to the

positive level of dividends that has been provided by the company after their IPOs. The return

has mainly increased from 1.10% to 1.57% for National Storage and 0.33% to 0.68% for

Sandon Capital Investments.

Moreover, the comparison of the returns that has been generated by National Storage

with and without the dividends mainly states at the level of 43.18%. This mainly indicates

that with the inclusion of the dividend the company was able to provide a total return of

43.18% as dividends to investors. In the similar instance, Pact Group was able to provide a

return of 15.7% from their dividends to the investors over the period of 3 years. However, the

analysis has mainly indicated that Sandon Capital Investments have provided a total return of

108.32% in dividends, as compared to the return provided from the shares (Garg & Dua,

2014).

9

f. Understanding the returns provided by IPO with dividends:

11/1/2013

1/1/2014

3/1/2014

5/1/2014

7/1/2014

9/1/2014

11/1/2014

1/1/2015

3/1/2015

5/1/2015

7/1/2015

9/1/2015

11/1/2015

1/1/2016

3/1/2016

5/1/2016

7/1/2016

9/1/2016

11/1/2016

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

R eturn with dividends

National Storage Sandon Capital Invetments Pact Group

The above figure provides adequate returns of the IPO, which includes dividends and

capital growth of the share price. The inclusion of the share price directly provides adequate

information regarding the return that was actually provided by the organisation for generating

high level of returns in the long run. The analysis has mainly stated that the overall share

price return of the IPO after adding the relevant dividends have mainly increased due to the

positive level of dividends that has been provided by the company after their IPOs. The return

has mainly increased from 1.10% to 1.57% for National Storage and 0.33% to 0.68% for

Sandon Capital Investments.

Moreover, the comparison of the returns that has been generated by National Storage

with and without the dividends mainly states at the level of 43.18%. This mainly indicates

that with the inclusion of the dividend the company was able to provide a total return of

43.18% as dividends to investors. In the similar instance, Pact Group was able to provide a

return of 15.7% from their dividends to the investors over the period of 3 years. However, the

analysis has mainly indicated that Sandon Capital Investments have provided a total return of

108.32% in dividends, as compared to the return provided from the shares (Garg & Dua,

2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

10

Conclusion:

The analysis has mainly stated that the share price of three organizations that has been

analyzed in the above assessment directly indicates about the significance of initial public

offering. The main reasons behind the overall public offering are to improve the capital

structure of the organization and reduce any kind of negative impact on its progress and

financial accountability. The cost of capital of the IPO used before the public offering was

relatively zero, as there is no calculation for identifying the relevant cost rate. However, the

analysis has indicated that it used in Australia mainly occurred when the capital market is in

uptrend, file reduction in the capital market returns directly to downfall on the IPO activities.

The share price performance of the IPS is relatively evaluated for the three year period after

the initial public offering. This analysis directly indicated that the IPO had provided high

level of returns in comparison to the market index of Australia. This relatively indicates that

the IPOs conducted in Australia could eventually allow investors to generate high level of

returns from investment in the long run.

10

Conclusion:

The analysis has mainly stated that the share price of three organizations that has been

analyzed in the above assessment directly indicates about the significance of initial public

offering. The main reasons behind the overall public offering are to improve the capital

structure of the organization and reduce any kind of negative impact on its progress and

financial accountability. The cost of capital of the IPO used before the public offering was

relatively zero, as there is no calculation for identifying the relevant cost rate. However, the

analysis has indicated that it used in Australia mainly occurred when the capital market is in

uptrend, file reduction in the capital market returns directly to downfall on the IPO activities.

The share price performance of the IPS is relatively evaluated for the three year period after

the initial public offering. This analysis directly indicated that the IPO had provided high

level of returns in comparison to the market index of Australia. This relatively indicates that

the IPOs conducted in Australia could eventually allow investors to generate high level of

returns from investment in the long run.

FINANCIAL MANAGEMENT

11

References:

Altuntas, S., & Dereli, T. (2015). A novel approach based on DEMATEL method and patent

citation analysis for prioritizing a portfolio of investment projects. Expert systems

with Applications, 42(3), 1003-1012.

Asx.com.au. (2019). Asx.com.au. Retrieved 15 August 2019, from

https://www.asx.com.au/asxpdf/20131205/pdf/42ldz93ntc44s5.pdf

Asx.com.au. (2019). Asx.com.au. Retrieved 15 August 2019, from

https://www.asx.com.au/asxpdf/20131216/pdf/42ln422bn34l8l.pdf

Bauer, R., & Smeets, P. (2015). Social identification and investment decisions. Journal of

Economic Behavior & Organization, 117, 121-134.

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Runkle, D. E., & Anson, M. J.

(2015). Quantitative investment analysis. John Wiley & Sons.

Finance.yahoo.com. (2019). Finance.yahoo.com. Retrieved 15 August 2019, from

https://finance.yahoo.com/

Fundsfocus.com.au. (2019). Fundsfocus.com.au. Retrieved 15 August 2019, from

http://www.fundsfocus.com.au/managed-funds/pdfs/ipo/sandon-prospectus.pdf

Garg, R., & Dua, P. (2014). Foreign portfolio investment flows to India: determinants and

analysis. World Development, 59, 16-28.

11

References:

Altuntas, S., & Dereli, T. (2015). A novel approach based on DEMATEL method and patent

citation analysis for prioritizing a portfolio of investment projects. Expert systems

with Applications, 42(3), 1003-1012.

Asx.com.au. (2019). Asx.com.au. Retrieved 15 August 2019, from

https://www.asx.com.au/asxpdf/20131205/pdf/42ldz93ntc44s5.pdf

Asx.com.au. (2019). Asx.com.au. Retrieved 15 August 2019, from

https://www.asx.com.au/asxpdf/20131216/pdf/42ln422bn34l8l.pdf

Bauer, R., & Smeets, P. (2015). Social identification and investment decisions. Journal of

Economic Behavior & Organization, 117, 121-134.

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Runkle, D. E., & Anson, M. J.

(2015). Quantitative investment analysis. John Wiley & Sons.

Finance.yahoo.com. (2019). Finance.yahoo.com. Retrieved 15 August 2019, from

https://finance.yahoo.com/

Fundsfocus.com.au. (2019). Fundsfocus.com.au. Retrieved 15 August 2019, from

http://www.fundsfocus.com.au/managed-funds/pdfs/ipo/sandon-prospectus.pdf

Garg, R., & Dua, P. (2014). Foreign portfolio investment flows to India: determinants and

analysis. World Development, 59, 16-28.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.