Analysis of the Impact of IPOs on Firm's Performance in Australia

VerifiedAdded on 2023/01/16

|11

|3146

|46

Report

AI Summary

This report analyzes the impact of Initial Public Offerings (IPOs) on the performance of firms, focusing on three ASX-listed companies: Z Energy Limited, iSelect Australia, and DroneShield Limited. The study examines the costs associated with IPOs, including the impact on the firm's cost of equity and the phenomenon of underpricing. The report evaluates the use of capital raised from IPOs, analyzing market price movements during the IPO process, and assessing the overall IPO activity on the ASX from 2007 to 2017. Furthermore, it critically evaluates the performance of shares and the impact of IPOs on shareholder value, considering arguments for and against the idea that IPOs increase shareholder value. The report concludes that IPOs are costly and not profitable for the long run, with underpricing increasing the cost of equity.

Running head: ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

Analysis of the Impact of IPOs on the Firm’s Performance:

Name of the Student:

Name of the University:

Student ID:

Author note:

Analysis of the Impact of IPOs on the Firm’s Performance:

Name of the Student:

Name of the University:

Student ID:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

Executive Summary

The study titled “Analysis of the Impact of IPOs on the Firm’s Performance” is an analysis of the

Initial Public Offerings (IPO) of three ASX listed companies, Z Energy Limited, iSelect Australia

and DroneShield Limited and the impact of the IPOs in the shareholder’s value is identified. The

study focuses on the overall analysis of IPOs in the Australian market by evaluating IPO activities

in the Australian market for a 10 year period, from 2007 to 2017. The study concludes that IPOs are

costly and not profitable for long run, more than 5 years and the effect of under-pricing increases

the cost of equity.

Executive Summary

The study titled “Analysis of the Impact of IPOs on the Firm’s Performance” is an analysis of the

Initial Public Offerings (IPO) of three ASX listed companies, Z Energy Limited, iSelect Australia

and DroneShield Limited and the impact of the IPOs in the shareholder’s value is identified. The

study focuses on the overall analysis of IPOs in the Australian market by evaluating IPO activities

in the Australian market for a 10 year period, from 2007 to 2017. The study concludes that IPOs are

costly and not profitable for long run, more than 5 years and the effect of under-pricing increases

the cost of equity.

2ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

Table of Contents

Introduction..........................................................................................................................................3

Use of Capital Raised from IPO:.........................................................................................................3

Effect of IPO in the Firm’s Cost of Equity:.........................................................................................4

Analysis of Market Price during IPO:.................................................................................................5

Analysis of IPO activity on the ASX:..................................................................................................6

Critical Evaluation of Shares Performance:.........................................................................................7

Conclusion...........................................................................................................................................8

References............................................................................................................................................9

Table of Contents

Introduction..........................................................................................................................................3

Use of Capital Raised from IPO:.........................................................................................................3

Effect of IPO in the Firm’s Cost of Equity:.........................................................................................4

Analysis of Market Price during IPO:.................................................................................................5

Analysis of IPO activity on the ASX:..................................................................................................6

Critical Evaluation of Shares Performance:.........................................................................................7

Conclusion...........................................................................................................................................8

References............................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

Introduction

The Australian Securities Exchange (ASX) is primary securities exchange market of

Australia and have many listed companies, including new and old companies, offering IPOs for

raising capitals. The half year IPO report of 2018, have posted that ASX have listed the second

maximum amount of Initial Public Offerings on 2018. In the study three Initial Public Offerings are

selected in the period between the years, 2007 to 2013, which are Z Energy limited raised IPO of

$660m in 2013 in ASX, iSelect Australia raised IPO of A$215m in 2013 and DroneShield Limited

raised IPO of $0.99 per share in 2014. These IPOs are used to study the impact of capital raising

through IPO in the financial performance of the company.

Z Energy limited is a New Zealand based fuel distributor, and has been listed in ASX as

well as the NZX. Z Energy has its service station in 305 locations across New Zealand and

Australia. iSelect is one of the largest insurance distributing agency of Australia, which provides

different insurance services, including health insurance, life insurance, car insurance and others.

DroneShield Limited engages is a company that provides services related to the technology

securities support founded in 2014, headquartered at Sydney, Australia. DroneShield Limited

develops and provide software and hardware technologies to detect drones and security all over the

world.

Use of Capital Raised from IPO:

iSelect have issued initial public offering of A$215m, in 24th June, 2013, where they have

issued 116.4 million fully paid ordinary shares at $1.85 each, but due to a drop of 15.7% in the

market share, the stock’s value fell to $1.56. The Company provides health insurance comparison

services in websites as its primary service. In between the late 2013 and the early 2014, the

company claims to do a major investment in their data mining and analytics function, by investing

in more in the marketing, which is expected to be extract from the capital raised. In the annual

report 2013-14 of the company, the value of the property, plant and equipment have increased by

Introduction

The Australian Securities Exchange (ASX) is primary securities exchange market of

Australia and have many listed companies, including new and old companies, offering IPOs for

raising capitals. The half year IPO report of 2018, have posted that ASX have listed the second

maximum amount of Initial Public Offerings on 2018. In the study three Initial Public Offerings are

selected in the period between the years, 2007 to 2013, which are Z Energy limited raised IPO of

$660m in 2013 in ASX, iSelect Australia raised IPO of A$215m in 2013 and DroneShield Limited

raised IPO of $0.99 per share in 2014. These IPOs are used to study the impact of capital raising

through IPO in the financial performance of the company.

Z Energy limited is a New Zealand based fuel distributor, and has been listed in ASX as

well as the NZX. Z Energy has its service station in 305 locations across New Zealand and

Australia. iSelect is one of the largest insurance distributing agency of Australia, which provides

different insurance services, including health insurance, life insurance, car insurance and others.

DroneShield Limited engages is a company that provides services related to the technology

securities support founded in 2014, headquartered at Sydney, Australia. DroneShield Limited

develops and provide software and hardware technologies to detect drones and security all over the

world.

Use of Capital Raised from IPO:

iSelect have issued initial public offering of A$215m, in 24th June, 2013, where they have

issued 116.4 million fully paid ordinary shares at $1.85 each, but due to a drop of 15.7% in the

market share, the stock’s value fell to $1.56. The Company provides health insurance comparison

services in websites as its primary service. In between the late 2013 and the early 2014, the

company claims to do a major investment in their data mining and analytics function, by investing

in more in the marketing, which is expected to be extract from the capital raised. In the annual

report 2013-14 of the company, the value of the property, plant and equipment have increased by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

an amount of $756,000, which means the company’s investments on technology related assets have

increased and the investment made from the increased capital. However, the raised capital is not

used to contribute working capital as per the annual report.

Z Energy is one of the largest fuel distributor in the energy industry in Australia. In the 3rd

quarter of 2013, the company have raised and issued Initial Public Offering of $677m, which was

the 5th highest capital raised from IPO in the globe, in 2013. The company have used IPO to invest

in a project of making biodiesel, also named as an alternative energy future. The company have

invested $22m in total from the capital raised. Z energy also have not include any investment on the

Working capital of the company from the capital raise from the IPO.

DroneShield is a drone detection company that have introduced its Initial Public Offerings

in June 24, 2014 of $7 million. The company have started its trading at $7 million, and then giving

it a market capitalisation of a total of $27 million till date. DroneShield have raised a huge amount

of capital from the IPO, and used the amount raised in couple of investments such as the company

have initiated an new idea for developing a new software for drone detection. Thus, the company

have used some of the amount from the capital raised to develop the idea.

Effect of IPO in the Firm’s Cost of Equity:

“IPOs are a costly way of raising long term finance for corporations”. The statement states

that preparing IPO is very expensive, complex and time consuming and it is true, because for

preparing IPO, a company generally needs a minimum of six to nine months, thus the process takes

a lot of time and cost. The process take time because before offerings, the needs to present a

disclosure and prepare report, to put the affairs with respect to the Australian Securities and

Investment Commission. (ASIC), and this process needs to appoint various specialists, thus it

requires a lot of costs.

In the annual report of the Z Energy, we can see that after 3rd quarter, the cost of equity of

the company for the period raised, because the value of the market rate of return have increased

an amount of $756,000, which means the company’s investments on technology related assets have

increased and the investment made from the increased capital. However, the raised capital is not

used to contribute working capital as per the annual report.

Z Energy is one of the largest fuel distributor in the energy industry in Australia. In the 3rd

quarter of 2013, the company have raised and issued Initial Public Offering of $677m, which was

the 5th highest capital raised from IPO in the globe, in 2013. The company have used IPO to invest

in a project of making biodiesel, also named as an alternative energy future. The company have

invested $22m in total from the capital raised. Z energy also have not include any investment on the

Working capital of the company from the capital raise from the IPO.

DroneShield is a drone detection company that have introduced its Initial Public Offerings

in June 24, 2014 of $7 million. The company have started its trading at $7 million, and then giving

it a market capitalisation of a total of $27 million till date. DroneShield have raised a huge amount

of capital from the IPO, and used the amount raised in couple of investments such as the company

have initiated an new idea for developing a new software for drone detection. Thus, the company

have used some of the amount from the capital raised to develop the idea.

Effect of IPO in the Firm’s Cost of Equity:

“IPOs are a costly way of raising long term finance for corporations”. The statement states

that preparing IPO is very expensive, complex and time consuming and it is true, because for

preparing IPO, a company generally needs a minimum of six to nine months, thus the process takes

a lot of time and cost. The process take time because before offerings, the needs to present a

disclosure and prepare report, to put the affairs with respect to the Australian Securities and

Investment Commission. (ASIC), and this process needs to appoint various specialists, thus it

requires a lot of costs.

In the annual report of the Z Energy, we can see that after 3rd quarter, the cost of equity of

the company for the period raised, because the value of the market rate of return have increased

5ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

due to the increase in number of shares. Similarly in the annual report of iSelect, it is seen that after

24th June, 2013, 116.4 million shares are added to the existing shares of the company, value of

equity also increased with the expected rate of return and hence the cost of capital of iSelect have

also got affected.

Analysis of Market Price during IPO:

Z Energy’s IPO have been issued in 23rd of August, 2013 at a price $3.30 and the closing

price for that day was $3.25. The value of per share of the company seemed to be under-priced at

the end of the first day of the issue. The issued price is reduced to $0.05 per share at the end of the

first day of the issue. This is due to the overall market impact, on the energy industry, not due to a

specific reason for Z Energy, because at that day, the highest price touched by the share is $3.38.

iSelect’s IPO have been issued in 28th June, 2013, with a issued price of $1.68 per share

and closed with a market price of $1.70 per share. It has been seen that at the end of the first day of

the issue of IPO, the price per share of the company have accelerated and the price did not

underlined like Z Energy. The reason behind the under-pricing of shares of the Z Energy is due to

the overall crisis in the energy industry, hence from the empirical evidence, it can be concluded that

the under-pricing of the market value of the issued share differs from industry to industry.

As mentioned in the ASX, DroneShield have started its trading by introduced its IPO at 24

june, 2014. At that date, the opening value of the stock was $0.2400 per share, while the closing

value of the stock is resulted to $0.2300 per share, which shows that the market price per share of

the company have decreased at the end of the first day, i.e. the market price of the IPO have

underpriced. As the effect of a IPO, shares introduced are underpriced. The other reason mentioned

by different researchers is that the company is new and have brand new and experimental business

model, thus the investors have shown less trusts on the company.

due to the increase in number of shares. Similarly in the annual report of iSelect, it is seen that after

24th June, 2013, 116.4 million shares are added to the existing shares of the company, value of

equity also increased with the expected rate of return and hence the cost of capital of iSelect have

also got affected.

Analysis of Market Price during IPO:

Z Energy’s IPO have been issued in 23rd of August, 2013 at a price $3.30 and the closing

price for that day was $3.25. The value of per share of the company seemed to be under-priced at

the end of the first day of the issue. The issued price is reduced to $0.05 per share at the end of the

first day of the issue. This is due to the overall market impact, on the energy industry, not due to a

specific reason for Z Energy, because at that day, the highest price touched by the share is $3.38.

iSelect’s IPO have been issued in 28th June, 2013, with a issued price of $1.68 per share

and closed with a market price of $1.70 per share. It has been seen that at the end of the first day of

the issue of IPO, the price per share of the company have accelerated and the price did not

underlined like Z Energy. The reason behind the under-pricing of shares of the Z Energy is due to

the overall crisis in the energy industry, hence from the empirical evidence, it can be concluded that

the under-pricing of the market value of the issued share differs from industry to industry.

As mentioned in the ASX, DroneShield have started its trading by introduced its IPO at 24

june, 2014. At that date, the opening value of the stock was $0.2400 per share, while the closing

value of the stock is resulted to $0.2300 per share, which shows that the market price per share of

the company have decreased at the end of the first day, i.e. the market price of the IPO have

underpriced. As the effect of a IPO, shares introduced are underpriced. The other reason mentioned

by different researchers is that the company is new and have brand new and experimental business

model, thus the investors have shown less trusts on the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

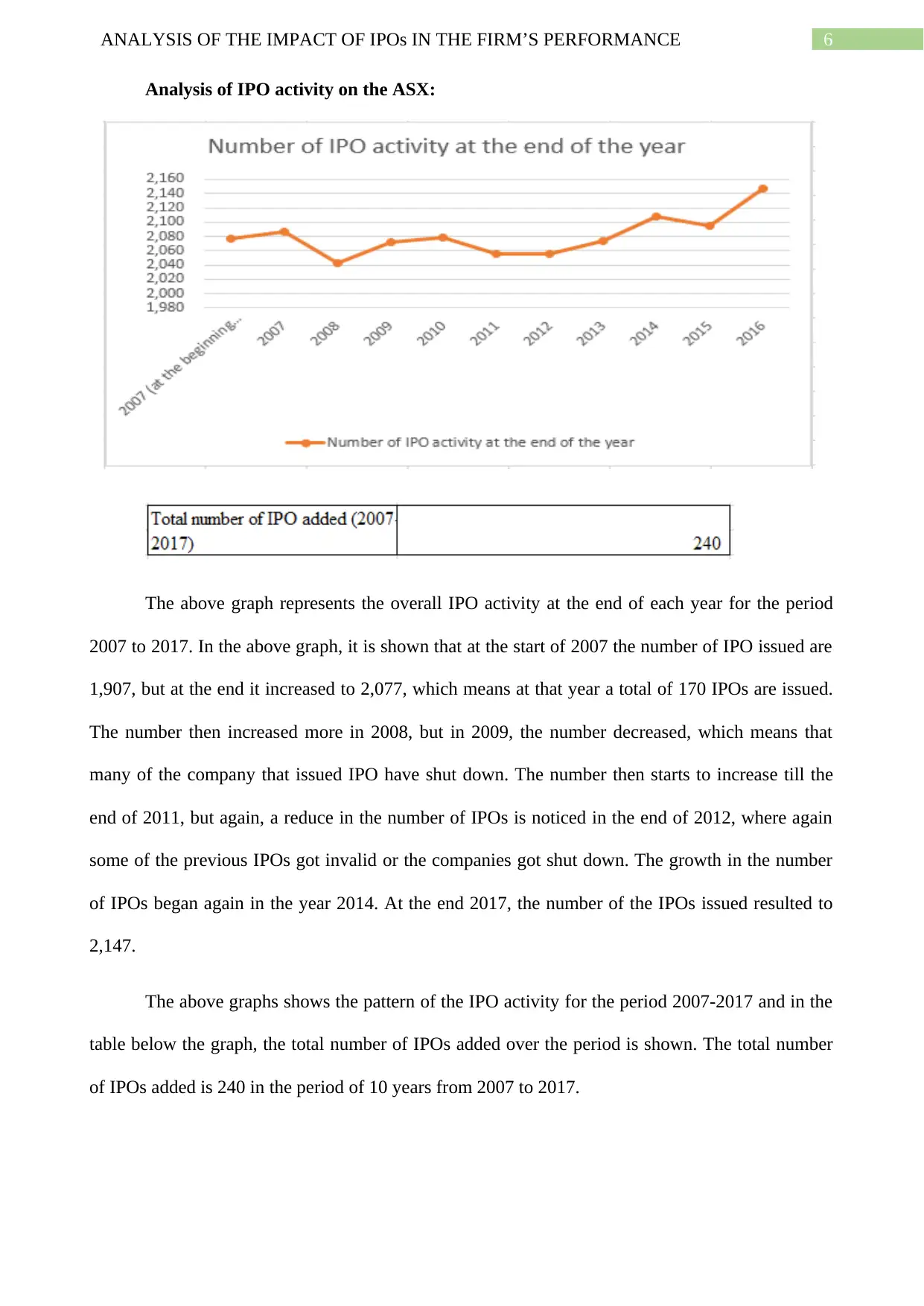

Analysis of IPO activity on the ASX:

The above graph represents the overall IPO activity at the end of each year for the period

2007 to 2017. In the above graph, it is shown that at the start of 2007 the number of IPO issued are

1,907, but at the end it increased to 2,077, which means at that year a total of 170 IPOs are issued.

The number then increased more in 2008, but in 2009, the number decreased, which means that

many of the company that issued IPO have shut down. The number then starts to increase till the

end of 2011, but again, a reduce in the number of IPOs is noticed in the end of 2012, where again

some of the previous IPOs got invalid or the companies got shut down. The growth in the number

of IPOs began again in the year 2014. At the end 2017, the number of the IPOs issued resulted to

2,147.

The above graphs shows the pattern of the IPO activity for the period 2007-2017 and in the

table below the graph, the total number of IPOs added over the period is shown. The total number

of IPOs added is 240 in the period of 10 years from 2007 to 2017.

Analysis of IPO activity on the ASX:

The above graph represents the overall IPO activity at the end of each year for the period

2007 to 2017. In the above graph, it is shown that at the start of 2007 the number of IPO issued are

1,907, but at the end it increased to 2,077, which means at that year a total of 170 IPOs are issued.

The number then increased more in 2008, but in 2009, the number decreased, which means that

many of the company that issued IPO have shut down. The number then starts to increase till the

end of 2011, but again, a reduce in the number of IPOs is noticed in the end of 2012, where again

some of the previous IPOs got invalid or the companies got shut down. The growth in the number

of IPOs began again in the year 2014. At the end 2017, the number of the IPOs issued resulted to

2,147.

The above graphs shows the pattern of the IPO activity for the period 2007-2017 and in the

table below the graph, the total number of IPOs added over the period is shown. The total number

of IPOs added is 240 in the period of 10 years from 2007 to 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

Critical Evaluation of Shares Performance:

Different company issues IPOs for different purposes, out of which the most common

objectives that is mentioned by different researchers’ are- (i) for the motive to convert a private

sector company to a public sector company, or (ii) for motive to convert a public sector company to

a private sector. However in this study, both the company have issued their IPO for the first time,

started as a fresh company. Both the company is a private company, and has no history of being

public sector. From the above analysis it can be said that the companies’ only motive is to increase

its share price in the market.

As discussed above, due to capital raised from the IPO increase the cost of capital, but due

to issue of new shares, the market price per share remains high, and also the valuation of the

company also increases. Thus the company’s earning by shares also increases and hence, due to

this the shareholder’s value also increases. However, there also some arguments against the concept

that IPO increases shareholder’s value or add value to the firm, stating that IPO don not add value

given that on the average of shares price performance in 3-5 years of the company after IPO’s poor

performance.

Michelle Lowry, Micah S. Officer and G. William Schwert, have argued in their book

named “The Variability of IPO Initial Returns”, about the IPO’s returns being variable and not

constant. They, in their argument states that IPOs are under-priced on average, which means that

the trading price of a share or stock in the secondary market is on average much higher than its IPO

value and also the monthly initial returns of IPO are not stable and fluctuates over period. Hence, in

such case IPOs issued by the companies cannot increase shareholders value, due variable market

price.

Considering the impact of under-pricing, only the share price of the Z Energy Limited have

under-priced in the first day of the issue, while the shares price of iSelect have accelerated at the

end of the first day of the issue. Considering the five days data of the share price of the Z Energy, it

Critical Evaluation of Shares Performance:

Different company issues IPOs for different purposes, out of which the most common

objectives that is mentioned by different researchers’ are- (i) for the motive to convert a private

sector company to a public sector company, or (ii) for motive to convert a public sector company to

a private sector. However in this study, both the company have issued their IPO for the first time,

started as a fresh company. Both the company is a private company, and has no history of being

public sector. From the above analysis it can be said that the companies’ only motive is to increase

its share price in the market.

As discussed above, due to capital raised from the IPO increase the cost of capital, but due

to issue of new shares, the market price per share remains high, and also the valuation of the

company also increases. Thus the company’s earning by shares also increases and hence, due to

this the shareholder’s value also increases. However, there also some arguments against the concept

that IPO increases shareholder’s value or add value to the firm, stating that IPO don not add value

given that on the average of shares price performance in 3-5 years of the company after IPO’s poor

performance.

Michelle Lowry, Micah S. Officer and G. William Schwert, have argued in their book

named “The Variability of IPO Initial Returns”, about the IPO’s returns being variable and not

constant. They, in their argument states that IPOs are under-priced on average, which means that

the trading price of a share or stock in the secondary market is on average much higher than its IPO

value and also the monthly initial returns of IPO are not stable and fluctuates over period. Hence, in

such case IPOs issued by the companies cannot increase shareholders value, due variable market

price.

Considering the impact of under-pricing, only the share price of the Z Energy Limited have

under-priced in the first day of the issue, while the shares price of iSelect have accelerated at the

end of the first day of the issue. Considering the five days data of the share price of the Z Energy, it

8ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

can be said that the return from the IPO is very fluctuating and not very constant and the share

price of the company have under-priced over the initial 4 days period, but on the 5th day the stock

seemed to be accelerated.

In the first day of the issue, iSelect have not seen any under-pricing in its IPO, but by

considering the 5 days data of iSelect, it can be noticed that its market share price have also shown

a decline in the market, which proves the point that every IPOs are under-priced at some point ofd

time, but after the 5 days period the market share price of iSelect have accelerated again, and in the

currently holding a very strong position in the ASX lists. Even after the impact of under-pricing, it

has not affected the shareholder’s value of the company, because the company’s earnings by share

as shown in the annual report, had no negative impact.

Conclusion

From the above study and analysis, it can be concluded that IPOs are very expensive and

costly than debt financing, and as discussed in the last paragraph of the study, the medium to long

run performance of a new public company is poor. The study states that the poor performance of a

new public company in the share market for long run is due under-pricing of Initial Public

Offerings in the initial stage. The study states a relevant argument of on the concept and impact of

the extent of under-pricing of the IPOs in the industries and concludes that the extent of under-

pricing differs from industry to industry and hence not an universal theory. The study also

concludes that cost of IPO is costly, because the capital raised from IPOs changes the cost of equity

of the company, irrespective to the type of industry.

The study also concludes that the overall pattern of IPO activity in the Australian market is

cyclical and thus depends on the number of business survives in the market for long run. The study

states that in Australian Securities and Exchange market there is a total of 240 IPO’s registered or

added between the period 2007 and 2017.

can be said that the return from the IPO is very fluctuating and not very constant and the share

price of the company have under-priced over the initial 4 days period, but on the 5th day the stock

seemed to be accelerated.

In the first day of the issue, iSelect have not seen any under-pricing in its IPO, but by

considering the 5 days data of iSelect, it can be noticed that its market share price have also shown

a decline in the market, which proves the point that every IPOs are under-priced at some point ofd

time, but after the 5 days period the market share price of iSelect have accelerated again, and in the

currently holding a very strong position in the ASX lists. Even after the impact of under-pricing, it

has not affected the shareholder’s value of the company, because the company’s earnings by share

as shown in the annual report, had no negative impact.

Conclusion

From the above study and analysis, it can be concluded that IPOs are very expensive and

costly than debt financing, and as discussed in the last paragraph of the study, the medium to long

run performance of a new public company is poor. The study states that the poor performance of a

new public company in the share market for long run is due under-pricing of Initial Public

Offerings in the initial stage. The study states a relevant argument of on the concept and impact of

the extent of under-pricing of the IPOs in the industries and concludes that the extent of under-

pricing differs from industry to industry and hence not an universal theory. The study also

concludes that cost of IPO is costly, because the capital raised from IPOs changes the cost of equity

of the company, irrespective to the type of industry.

The study also concludes that the overall pattern of IPO activity in the Australian market is

cyclical and thus depends on the number of business survives in the market for long run. The study

states that in Australian Securities and Exchange market there is a total of 240 IPO’s registered or

added between the period 2007 and 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

References

(2019). Retrieved from

http://www.annualreports.com/HostedData/AnnualReportArchive/i/ASX_ISU_2014.pdf

(2019). Retrieved from https://investor-centre.z.co.nz/investor-centre/assets/Uploads/Z-2014-

Annual-Report-Final2.pdf

(2019). Retrieved from https://www.ey.com/Publication/vwLUAssets/EY_-

_Global_IPO_Trends_Q4_2013/$FILE/EY-Global-IPO-Trends-Q4-2013.pdf

(2019). Retrieved from https://www.ey.com/Publication/vwLUAssets/EY-Global-IPO-Trends-

Report-Q3-2013/%24FILE/EY-Global-IPO-Trends-Report-Q3-2013.pdf

Al-Yahyaee, K. H. (2014). Shareholder wealth effects of stock dividends in a unique

environment. Journal of International Financial Markets, Institutions and Money, 28, 66-

81.

Bottazzi, L. (2015). Underpricing and voluntary disclosure: The case of mining IPOs in

Australia. Journal of Economic & Financial Studies, 3(02), 18-29.

Boulanouar, Z., & Alqahtani, F. (2016). IPO underpricing in the insurance industry and the effect

of Sharia compliance: Evidence from Saudi Arabian market. International Journal of

Islamic and Middle Eastern Finance and Management, 9(3), 314-332.

Butler, A. W., Keefe, M. O. C., & Kieschnick, R. (2014). Robust determinants of IPO underpricing

and their implications for IPO research. Journal of Corporate Finance, 27, 367-383.

Çolak, G., Durnev, A., & Qian, Y. (2017). Political uncertainty and IPO activity: Evidence from

US gubernatorial elections. Journal of Financial and Quantitative Analysis, 52(6), 2523-

2564.

Ferguson, A., & Lam, P. (2015). Backdoor listings in Australia. JASSA, (1), 24.

References

(2019). Retrieved from

http://www.annualreports.com/HostedData/AnnualReportArchive/i/ASX_ISU_2014.pdf

(2019). Retrieved from https://investor-centre.z.co.nz/investor-centre/assets/Uploads/Z-2014-

Annual-Report-Final2.pdf

(2019). Retrieved from https://www.ey.com/Publication/vwLUAssets/EY_-

_Global_IPO_Trends_Q4_2013/$FILE/EY-Global-IPO-Trends-Q4-2013.pdf

(2019). Retrieved from https://www.ey.com/Publication/vwLUAssets/EY-Global-IPO-Trends-

Report-Q3-2013/%24FILE/EY-Global-IPO-Trends-Report-Q3-2013.pdf

Al-Yahyaee, K. H. (2014). Shareholder wealth effects of stock dividends in a unique

environment. Journal of International Financial Markets, Institutions and Money, 28, 66-

81.

Bottazzi, L. (2015). Underpricing and voluntary disclosure: The case of mining IPOs in

Australia. Journal of Economic & Financial Studies, 3(02), 18-29.

Boulanouar, Z., & Alqahtani, F. (2016). IPO underpricing in the insurance industry and the effect

of Sharia compliance: Evidence from Saudi Arabian market. International Journal of

Islamic and Middle Eastern Finance and Management, 9(3), 314-332.

Butler, A. W., Keefe, M. O. C., & Kieschnick, R. (2014). Robust determinants of IPO underpricing

and their implications for IPO research. Journal of Corporate Finance, 27, 367-383.

Çolak, G., Durnev, A., & Qian, Y. (2017). Political uncertainty and IPO activity: Evidence from

US gubernatorial elections. Journal of Financial and Quantitative Analysis, 52(6), 2523-

2564.

Ferguson, A., & Lam, P. (2015). Backdoor listings in Australia. JASSA, (1), 24.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ANALYSIS OF THE IMPACT OF IPOs IN THE FIRM’S PERFORMANCE

Firth, M., & Gounopoulos, D. (2017). IFRS adoption and management earnings forecasts of

Australian IPOs. Available at SSRN 2199034.

Katti, S., & Phani, B. V. (2016). Underpricing of initial public offerings: a literature

review. Universal Journal of Accounting and Finance, 4(2), 35-52.

Liu, M., & Forester, C. (2014). IPOs, operating activities, and IPO underperformance. The Journal

of Business and Economic Studies, 20(1), 1.

Lowry, M., Officer, M. S., & Schwert, G. W. (2010). The variability of IPO initial returns. The

Journal of Finance, 65(2), 425-465.

Meluzín, T., & Zinecker, M. (2016). Trends in IPOs: the evidence from cee capital

markets. Equilibrium. Quarterly Journal of Economics and Economic Policy, 11(2), 327-

341.

Ofori‐Sasu, D., Abor, J. Y., & Osei, A. K. (2017). Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review, 29(2), 293-304.

Firth, M., & Gounopoulos, D. (2017). IFRS adoption and management earnings forecasts of

Australian IPOs. Available at SSRN 2199034.

Katti, S., & Phani, B. V. (2016). Underpricing of initial public offerings: a literature

review. Universal Journal of Accounting and Finance, 4(2), 35-52.

Liu, M., & Forester, C. (2014). IPOs, operating activities, and IPO underperformance. The Journal

of Business and Economic Studies, 20(1), 1.

Lowry, M., Officer, M. S., & Schwert, G. W. (2010). The variability of IPO initial returns. The

Journal of Finance, 65(2), 425-465.

Meluzín, T., & Zinecker, M. (2016). Trends in IPOs: the evidence from cee capital

markets. Equilibrium. Quarterly Journal of Economics and Economic Policy, 11(2), 327-

341.

Ofori‐Sasu, D., Abor, J. Y., & Osei, A. K. (2017). Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review, 29(2), 293-304.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.