Finance Report: Australian IPO Performance and Underpricing

VerifiedAdded on 2021/05/27

|16

|3714

|155

Report

AI Summary

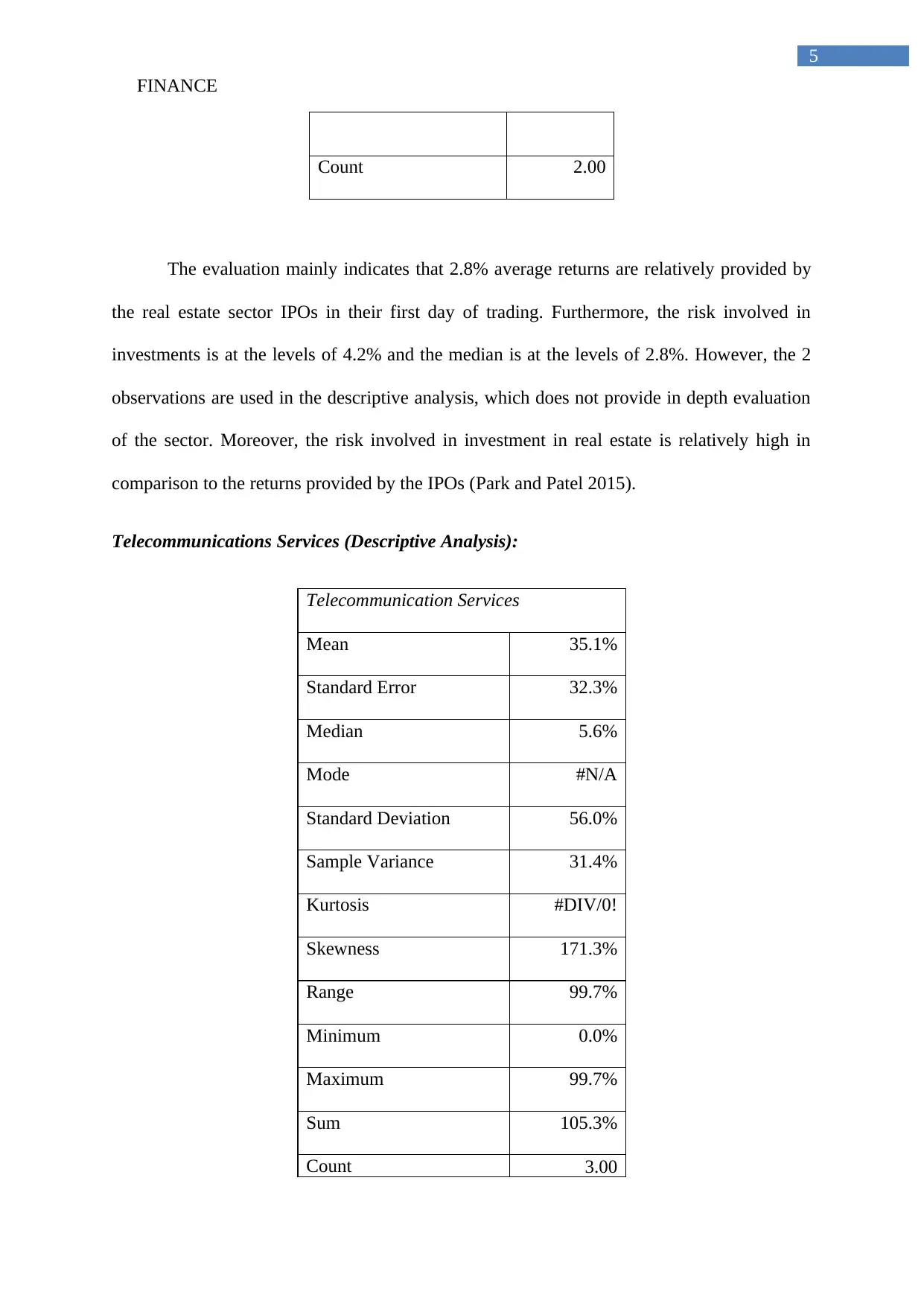

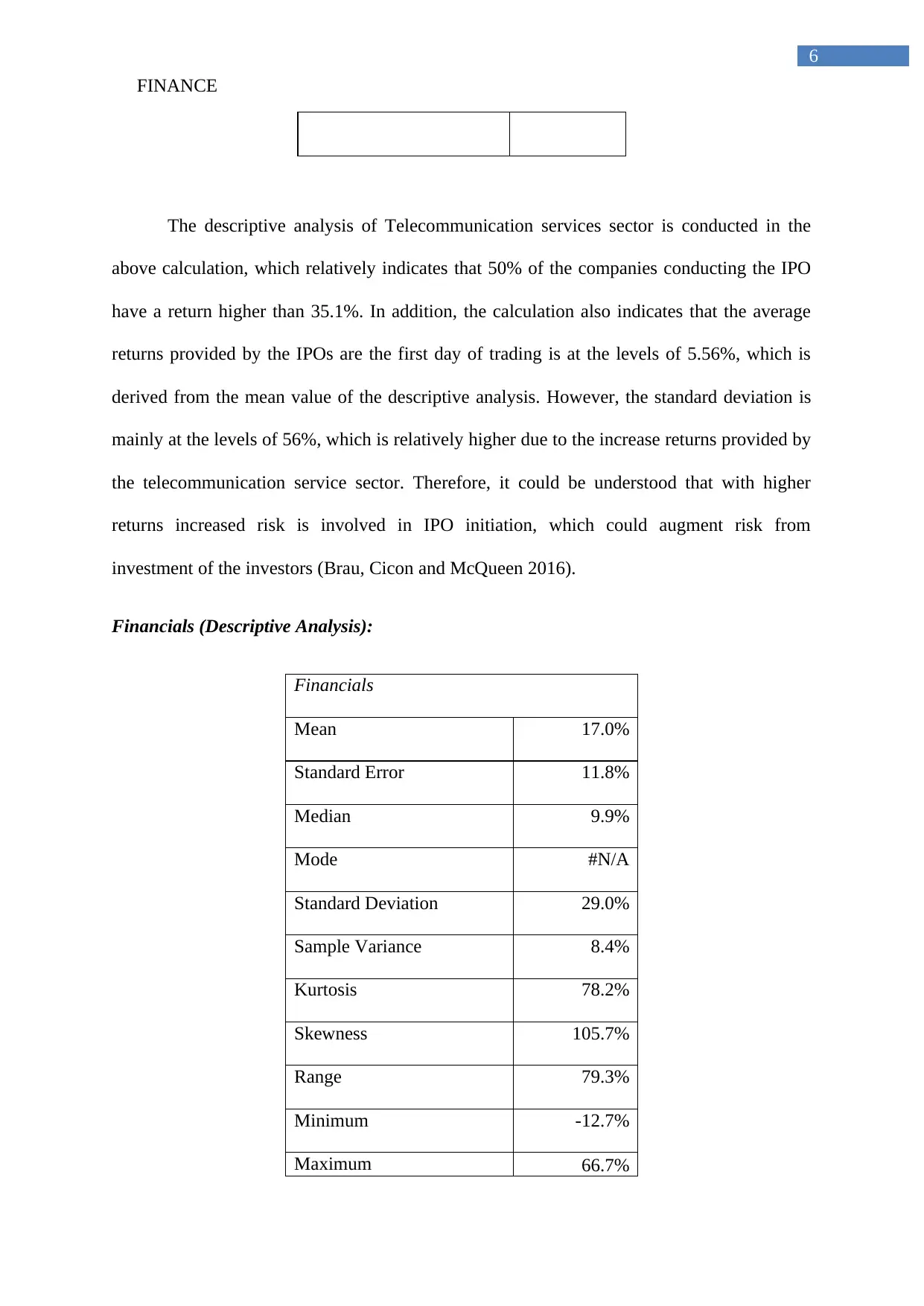

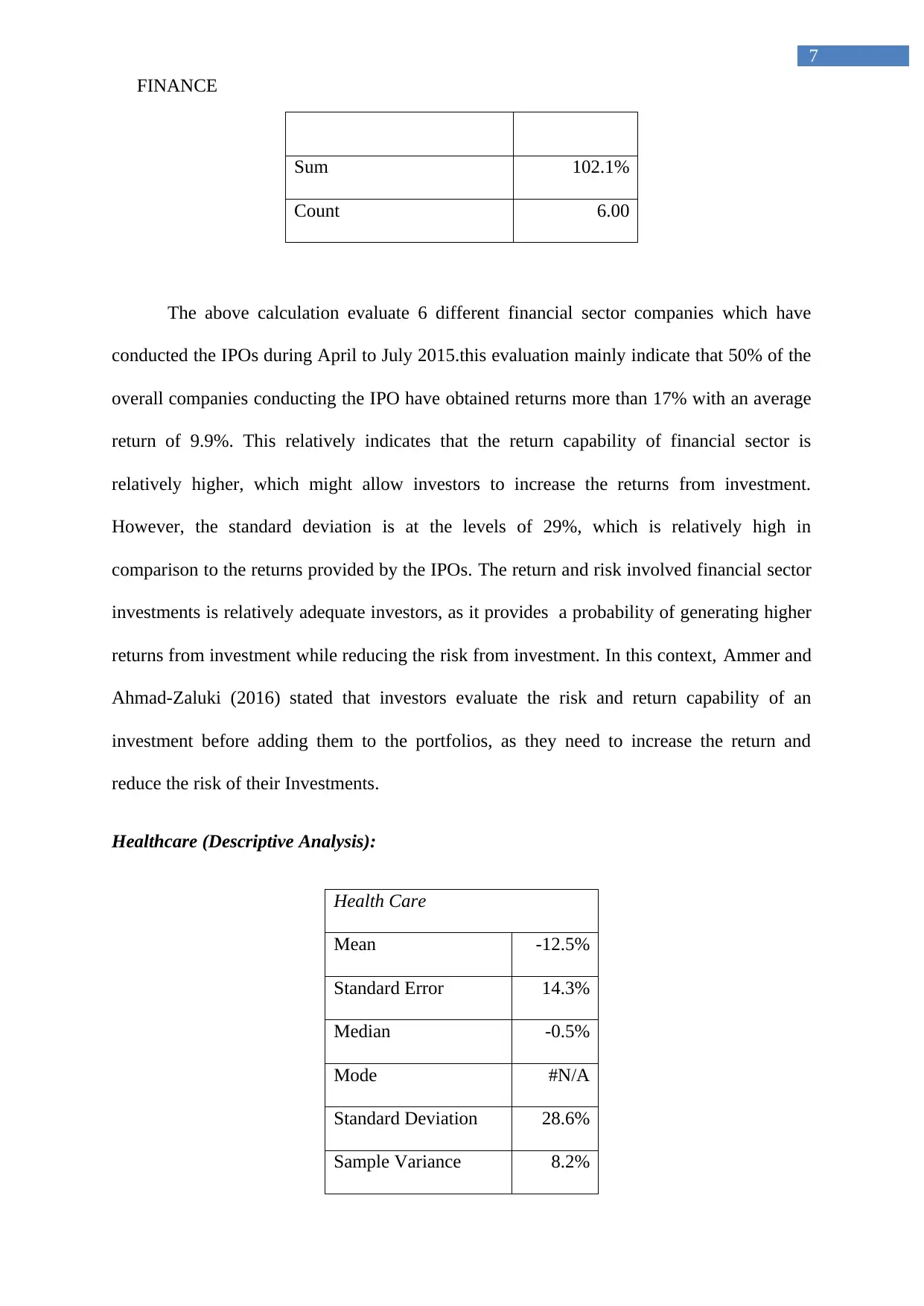

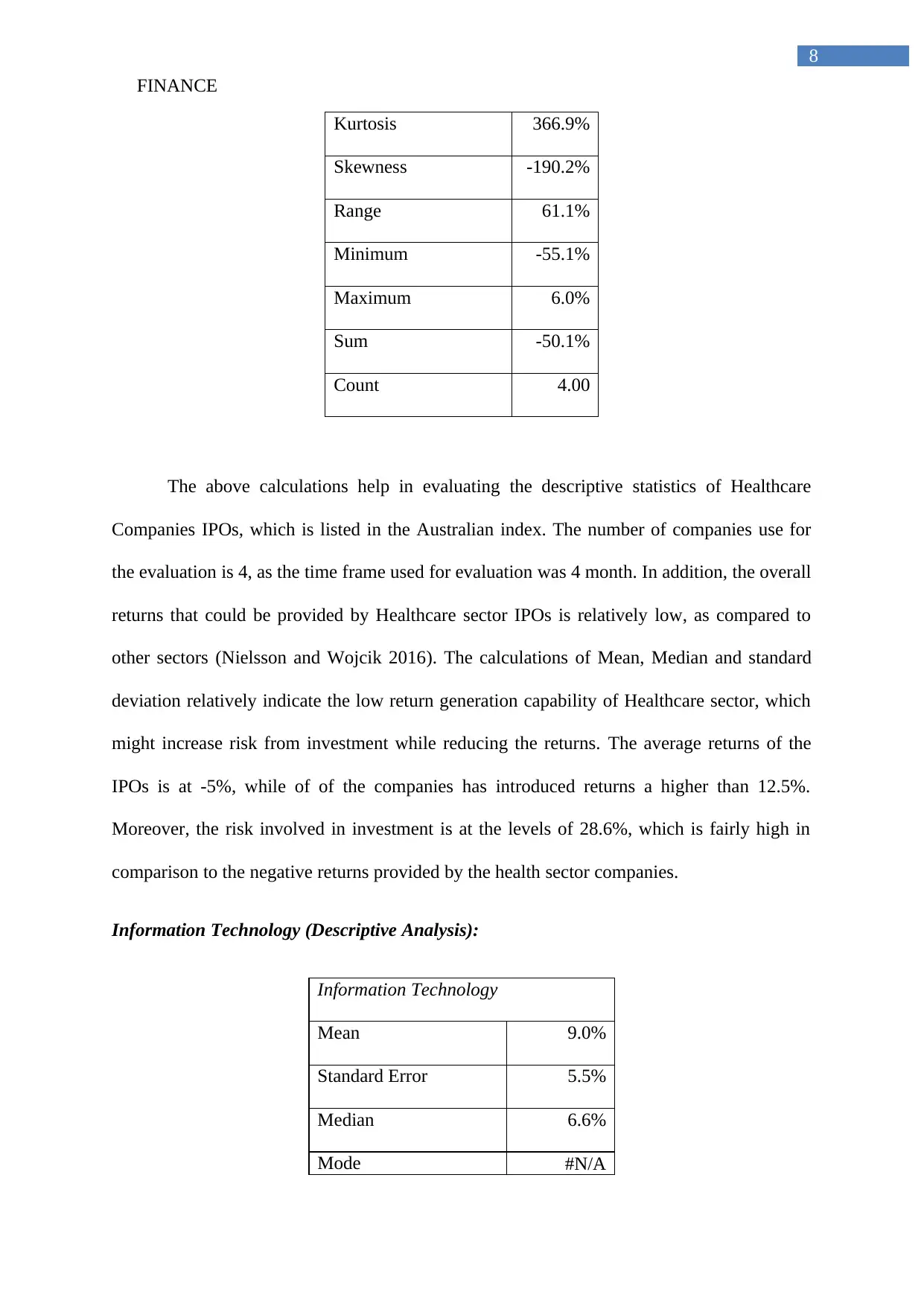

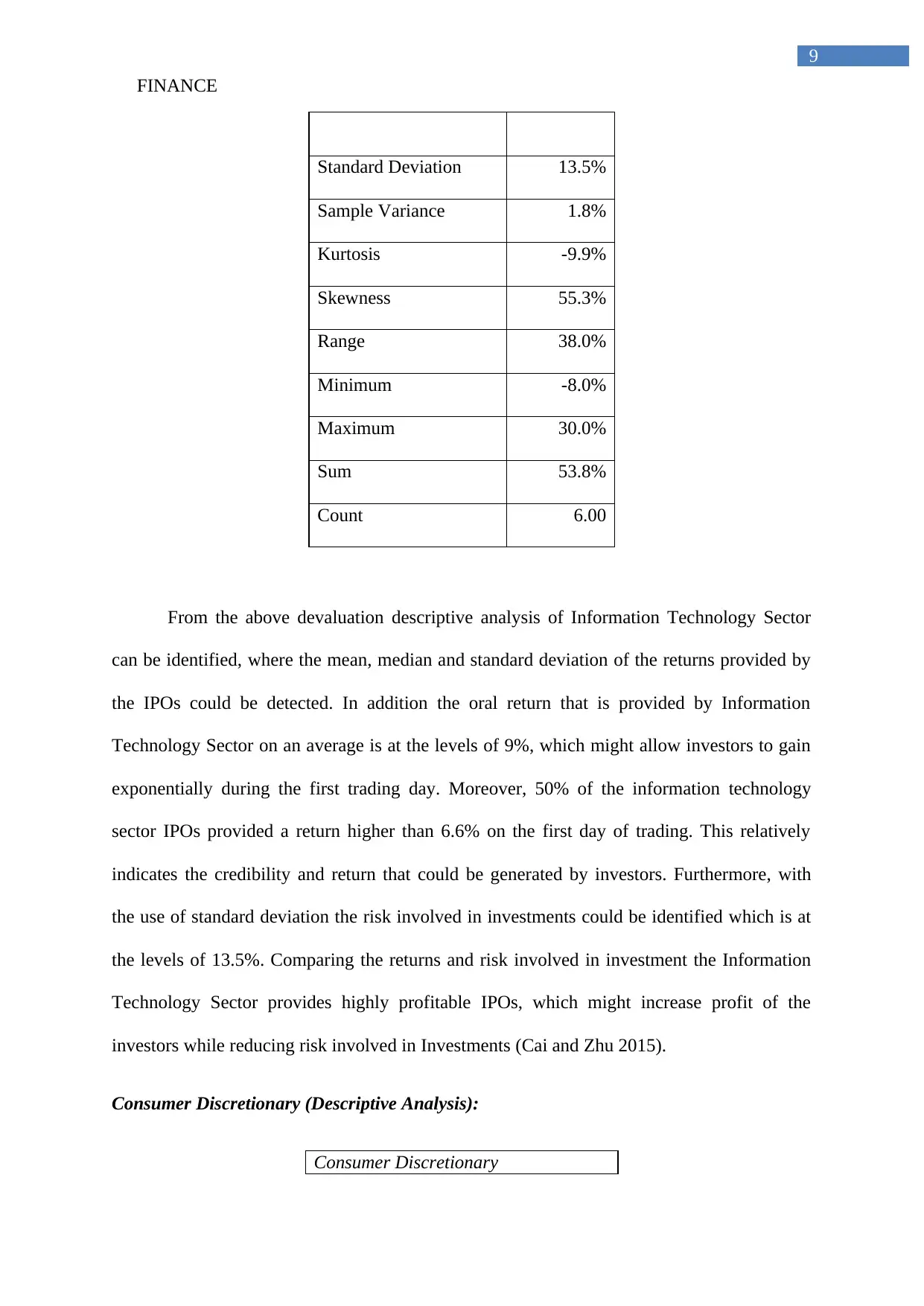

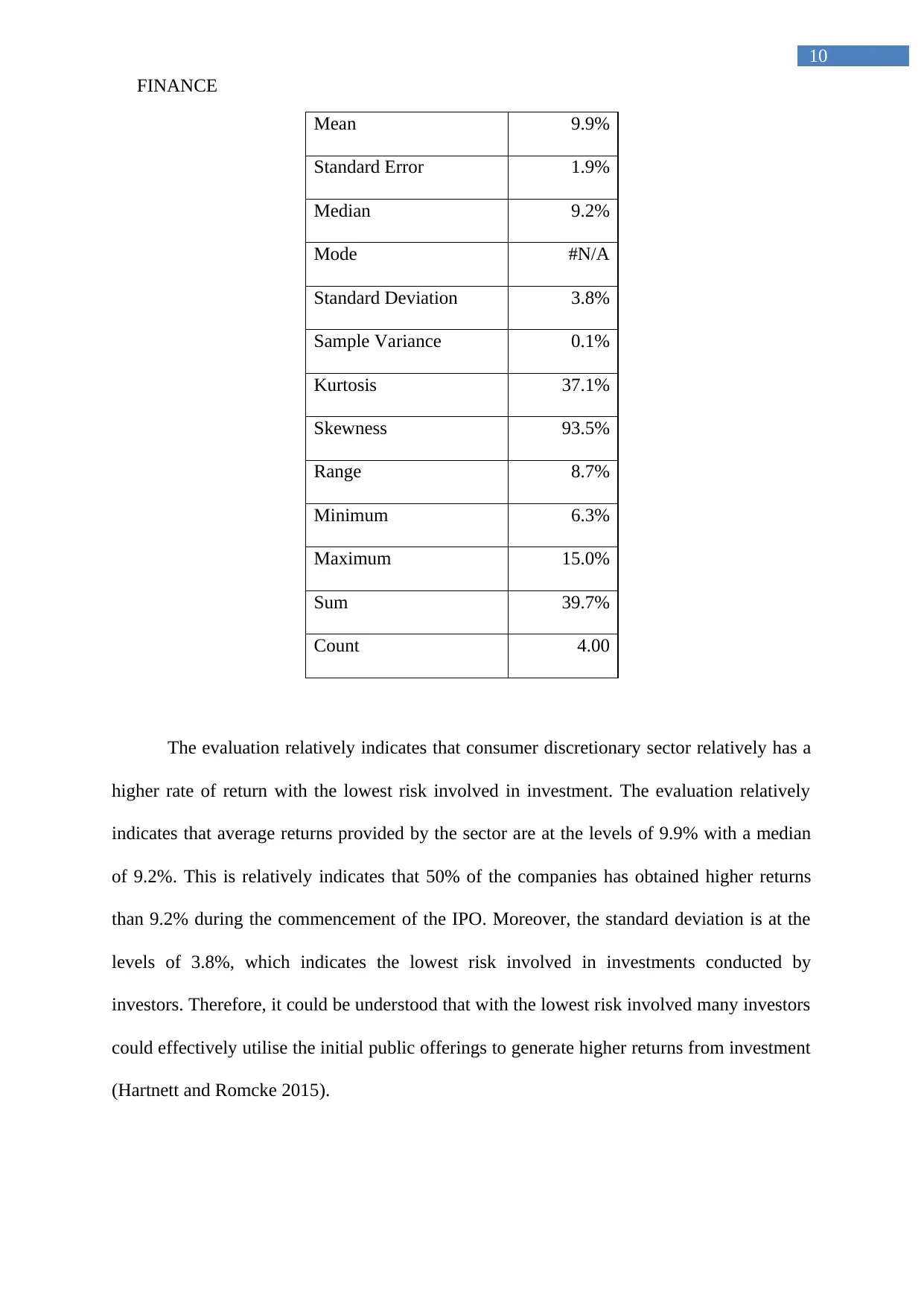

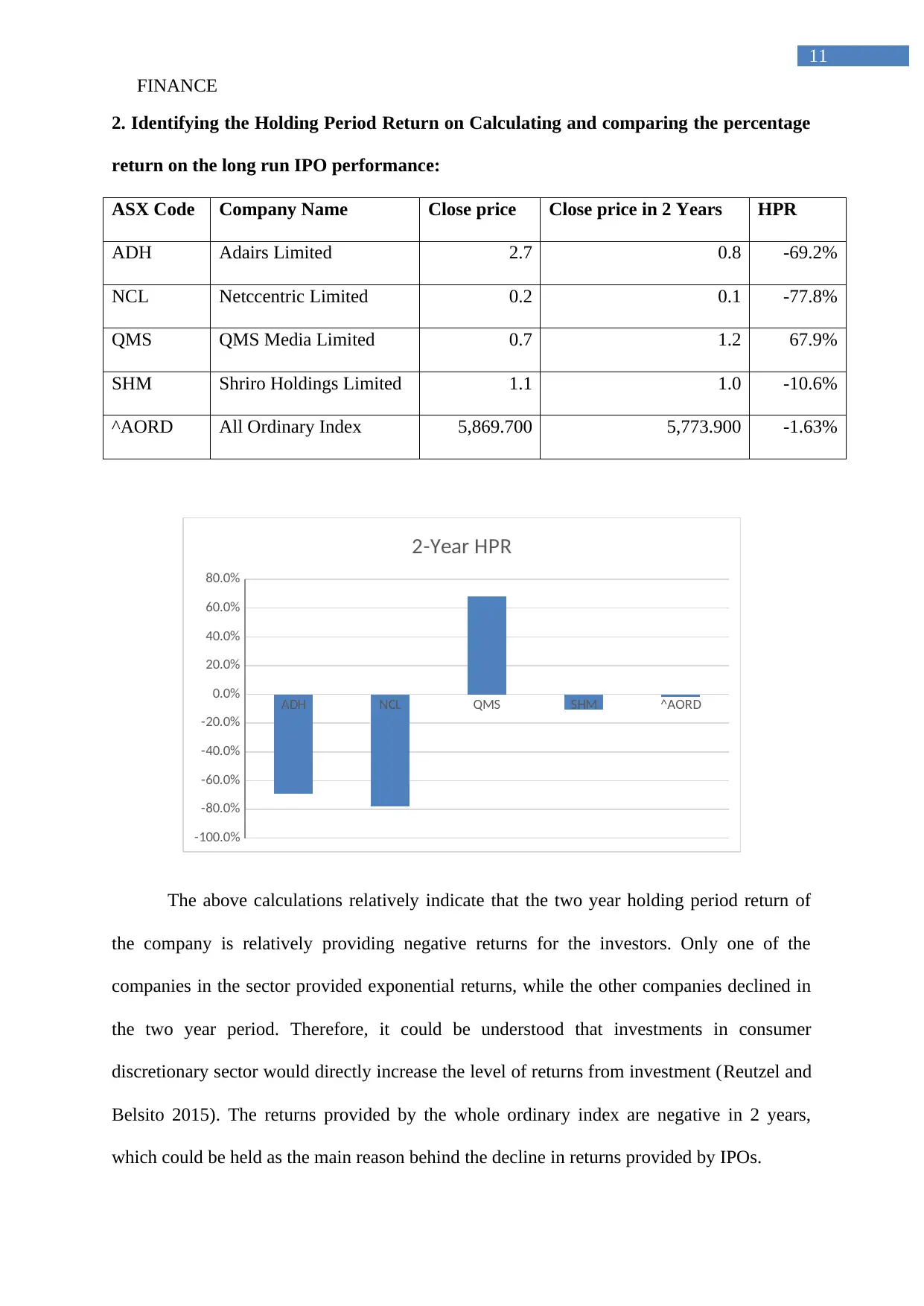

This report provides a comprehensive analysis of Initial Public Offerings (IPOs) in the Australian market, examining the initial returns generated from various sectors, including Real Estate, Telecommunications, Financials, Healthcare, Information Technology, and Consumer Discretionary. The report utilizes descriptive statistics to evaluate the performance of IPOs from April to July 2015, highlighting mean, median, standard deviation, and other relevant metrics. Furthermore, it identifies the Holding Period Return (HPR) over a two-year period for selected companies, comparing their performance against the All Ordinaries Index. The report also delves into the phenomenon of IPO underpricing, exploring the information asymmetry and behavioral theories that contribute to this practice in both the Australian and US markets, referencing empirical research from Hong Kong. The analysis aims to provide insights into the risks and returns associated with IPO investments, offering valuable information for investors and financial analysts.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.