Report on Evaluating Fund Raising Through IPO on ASX: FINA6000

VerifiedAdded on 2023/01/23

|19

|3766

|52

Report

AI Summary

This report provides a detailed analysis of Initial Public Offerings (IPOs) on the Australian Securities Exchange (ASX). It examines the fund-raising process, focusing on companies like Virtus Health, GDI Property, and Carsales.com, evaluating their performance before and after their IPOs. The report investigates the utilization of funds raised, assessing whether they were used for their intended purposes. It also compares the cost-effectiveness of IPOs versus debt financing, calculating the cost of equity using the Capital Asset Pricing Model (CAPM). Furthermore, the report explores factors related to IPO underpricing, the impact of the economy on cyclical stocks, and the objectives of issuing an IPO. The analysis includes tables and calculations to support the findings, providing a comprehensive overview of the IPO process and its implications for financial performance and investment decisions. The report also touches on the four puzzles identified in academic literature concerning IPOs: high costs, underpricing, cyclical nature, and medium to long-term performance.

Running head: EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Evaluating the Fung Raising through an IPO

Name of Student:

Name of the University:

Author Note

Evaluating the Fung Raising through an IPO

Name of Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Executive summary

The aim of this report is to understand the process of capital raising by an Australian

companies through the issue of IPO and evaluate whether those fund has been utilized for the

purpose of the for which they have been raised. The report also discusses the objective of an

IPO, like conversion of private capital to the public and vice versa. The report also assessed

the performance of cyclical stock in the economy, i.e. how they can be useful in balancing the

performance of the portfolio in the period of recession and in the economic growth. At the

end of the report a concluding remarks has been added on the performance of the share price

issued through an IPO in a long and short run.

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Executive summary

The aim of this report is to understand the process of capital raising by an Australian

companies through the issue of IPO and evaluate whether those fund has been utilized for the

purpose of the for which they have been raised. The report also discusses the objective of an

IPO, like conversion of private capital to the public and vice versa. The report also assessed

the performance of cyclical stock in the economy, i.e. how they can be useful in balancing the

performance of the portfolio in the period of recession and in the economic growth. At the

end of the report a concluding remarks has been added on the performance of the share price

issued through an IPO in a long and short run.

2

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Table of Contents

Introduction................................................................................................................................3

Answer to part (A).....................................................................................................................3

Answer to part (B)......................................................................................................................6

Answer to part (C)......................................................................................................................8

Answer to part (D).....................................................................................................................9

Answer to part (E)....................................................................................................................11

Answer to part (F)....................................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Table of Contents

Introduction................................................................................................................................3

Answer to part (A).....................................................................................................................3

Answer to part (B)......................................................................................................................6

Answer to part (C)......................................................................................................................8

Answer to part (D).....................................................................................................................9

Answer to part (E)....................................................................................................................11

Answer to part (F)....................................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Introduction

The purpose of this report is to understand the funding of the capital through an IPO

on the ASX. For this purpose, three public company has been taken like virtus health, GDI

property, carsales.com has been taken to evaluate their performance before and after the IPO.

It is also evaluated that whether the funds which has been raised to do the project, have been

utilized for the same purpose. Further it is also examined whether the IPO are costly way of

raising the long term finance for the corporation.

For this purpose the cost of equity has been calculated using CAPM approach and it

is compared with interest of long term debt, to evaluate the cost effectiveness. The report

further discusses the effect of the cyclical stock in managing the portfolio in the period of

recession and the economic boom. At the end of the report, different objectives of an IPO are

examined like conversion of private to public company and many others.

Answer to part (A)

Identification of Company Listed on the ASX with an IPO for an Amount of more than $ 100

Million.

Virtus Health

This company is related to the Health care sector, the business of the company is to

provide assisted reproductive services in Australia and Ireland, the corporation is expanding

is business presence in UK, Denmark and Singapore. The company has come up with an IPO

of 346.5 million USD in the year 2013 in the month of June. However the company can only

raise 310 million USD (Bewley, 2013).

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Introduction

The purpose of this report is to understand the funding of the capital through an IPO

on the ASX. For this purpose, three public company has been taken like virtus health, GDI

property, carsales.com has been taken to evaluate their performance before and after the IPO.

It is also evaluated that whether the funds which has been raised to do the project, have been

utilized for the same purpose. Further it is also examined whether the IPO are costly way of

raising the long term finance for the corporation.

For this purpose the cost of equity has been calculated using CAPM approach and it

is compared with interest of long term debt, to evaluate the cost effectiveness. The report

further discusses the effect of the cyclical stock in managing the portfolio in the period of

recession and the economic boom. At the end of the report, different objectives of an IPO are

examined like conversion of private to public company and many others.

Answer to part (A)

Identification of Company Listed on the ASX with an IPO for an Amount of more than $ 100

Million.

Virtus Health

This company is related to the Health care sector, the business of the company is to

provide assisted reproductive services in Australia and Ireland, the corporation is expanding

is business presence in UK, Denmark and Singapore. The company has come up with an IPO

of 346.5 million USD in the year 2013 in the month of June. However the company can only

raise 310 million USD (Bewley, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

The purpose of the Raising the fund is to supplement its business operation of assisted

reproduction technique. The company has utilized the fund amount in expanding its foot print

at the global level. The company is providing the quality services by establishing fertility

clinics, Day hospital and diagnostic center across the country (Brusov, Filatova, & Orekhova,

2013).

Some of the major acquisition made by the company in the following years are given below

Acquisition of Aagaard Fertility Clinic, Aarhus Denmark on 1st Dec 2016.

Acquisition of Canberra fertility center as on 20 may 2016.

Acquisition of the second Irish fertility clinic 24 December 2016 for 6 million Euro.

Acquisition of majority stake in Irish IVF provider for 15.49 million Euro as on 30

may 2014 (Carey,Fang & Zhang, 2016).

GDI Property

The Second Chosen Company is GDI Property which is property and fund

management group, the company has issued its IPO in the year December 2013, the company

raises an amount of USD 287 million. The company raised such amount to support its real

estate project like leasing and Syndication of office and commercial properties (Chatalova,

How, & Verhoeven, 2016).

Carsales.com

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

The purpose of the Raising the fund is to supplement its business operation of assisted

reproduction technique. The company has utilized the fund amount in expanding its foot print

at the global level. The company is providing the quality services by establishing fertility

clinics, Day hospital and diagnostic center across the country (Brusov, Filatova, & Orekhova,

2013).

Some of the major acquisition made by the company in the following years are given below

Acquisition of Aagaard Fertility Clinic, Aarhus Denmark on 1st Dec 2016.

Acquisition of Canberra fertility center as on 20 may 2016.

Acquisition of the second Irish fertility clinic 24 December 2016 for 6 million Euro.

Acquisition of majority stake in Irish IVF provider for 15.49 million Euro as on 30

may 2014 (Carey,Fang & Zhang, 2016).

GDI Property

The Second Chosen Company is GDI Property which is property and fund

management group, the company has issued its IPO in the year December 2013, the company

raises an amount of USD 287 million. The company raised such amount to support its real

estate project like leasing and Syndication of office and commercial properties (Chatalova,

How, & Verhoeven, 2016).

Carsales.com

5

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

The next company which got selected is from the automobiles sector named

carssales.com. The company is Australia largest platform of the sale and buying of used car,

automobiles. This is Australia one of the leading website for the advertisement of the used

automobiles.

The company performance has shown a tremendous growth 17 % in the reported

revenue of $235 million, the company has increased its international exposure in the foreign

market, strong reported revenue growth, the company has made several acquisition like SK

Encar, Excellent international look through revenue growth of 79% with good organic growth

in all international businesses on a constant currency basis (Ding, 2016).

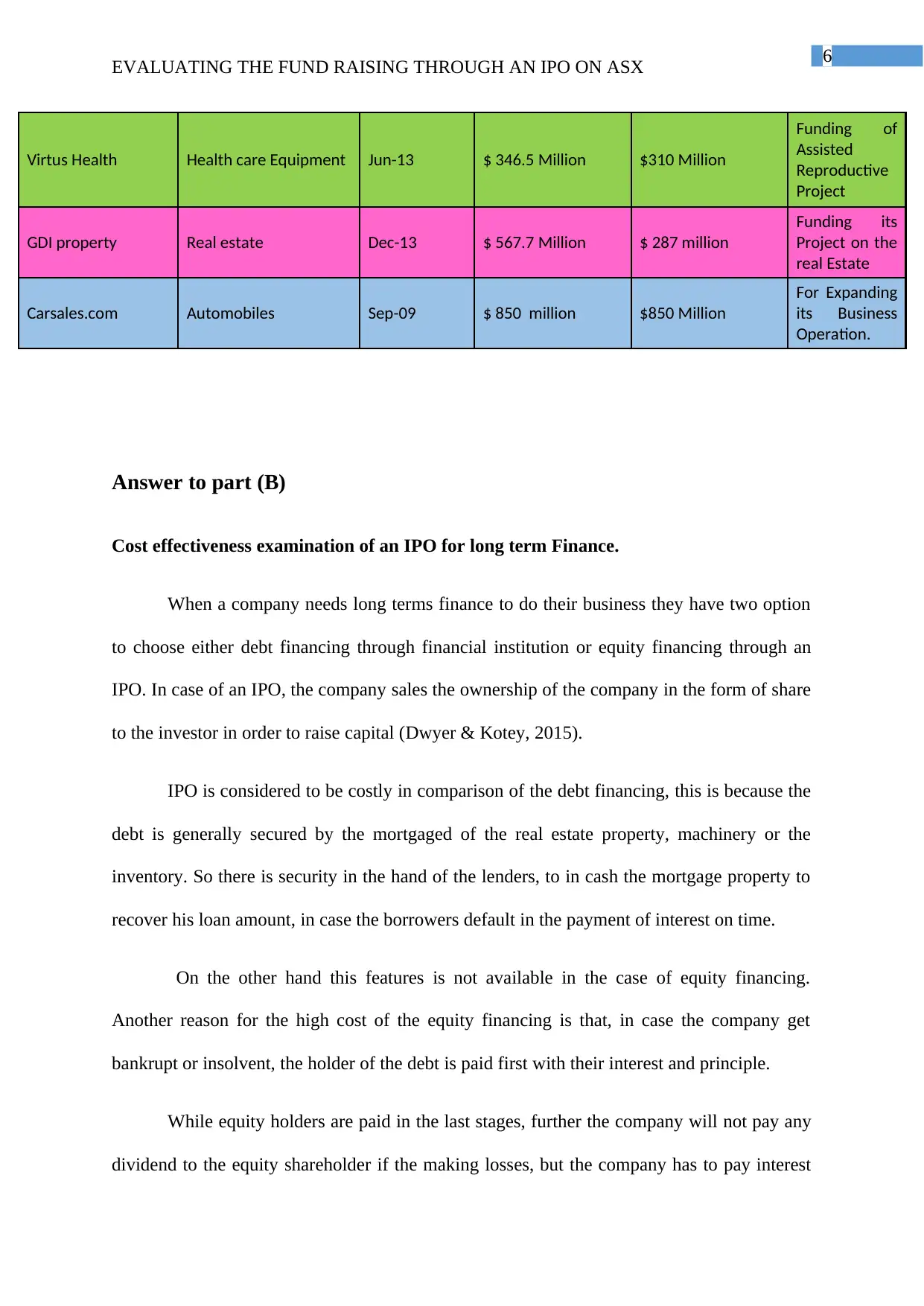

Table showing the different IPO of the company from the different sectors.

Company Name Industry Date of IPO Amount intended

to raise

Amount Actually

raised

The purpose

of the funds

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

The next company which got selected is from the automobiles sector named

carssales.com. The company is Australia largest platform of the sale and buying of used car,

automobiles. This is Australia one of the leading website for the advertisement of the used

automobiles.

The company performance has shown a tremendous growth 17 % in the reported

revenue of $235 million, the company has increased its international exposure in the foreign

market, strong reported revenue growth, the company has made several acquisition like SK

Encar, Excellent international look through revenue growth of 79% with good organic growth

in all international businesses on a constant currency basis (Ding, 2016).

Table showing the different IPO of the company from the different sectors.

Company Name Industry Date of IPO Amount intended

to raise

Amount Actually

raised

The purpose

of the funds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Virtus Health Health care Equipment Jun-13 $ 346.5 Million $310 Million

Funding of

Assisted

Reproductive

Project

GDI property Real estate Dec-13 $ 567.7 Million $ 287 million

Funding its

Project on the

real Estate

Carsales.com Automobiles Sep-09 $ 850 million $850 Million

For Expanding

its Business

Operation.

Answer to part (B)

Cost effectiveness examination of an IPO for long term Finance.

When a company needs long terms finance to do their business they have two option

to choose either debt financing through financial institution or equity financing through an

IPO. In case of an IPO, the company sales the ownership of the company in the form of share

to the investor in order to raise capital (Dwyer & Kotey, 2015).

IPO is considered to be costly in comparison of the debt financing, this is because the

debt is generally secured by the mortgaged of the real estate property, machinery or the

inventory. So there is security in the hand of the lenders, to in cash the mortgage property to

recover his loan amount, in case the borrowers default in the payment of interest on time.

On the other hand this features is not available in the case of equity financing.

Another reason for the high cost of the equity financing is that, in case the company get

bankrupt or insolvent, the holder of the debt is paid first with their interest and principle.

While equity holders are paid in the last stages, further the company will not pay any

dividend to the equity shareholder if the making losses, but the company has to pay interest

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Virtus Health Health care Equipment Jun-13 $ 346.5 Million $310 Million

Funding of

Assisted

Reproductive

Project

GDI property Real estate Dec-13 $ 567.7 Million $ 287 million

Funding its

Project on the

real Estate

Carsales.com Automobiles Sep-09 $ 850 million $850 Million

For Expanding

its Business

Operation.

Answer to part (B)

Cost effectiveness examination of an IPO for long term Finance.

When a company needs long terms finance to do their business they have two option

to choose either debt financing through financial institution or equity financing through an

IPO. In case of an IPO, the company sales the ownership of the company in the form of share

to the investor in order to raise capital (Dwyer & Kotey, 2015).

IPO is considered to be costly in comparison of the debt financing, this is because the

debt is generally secured by the mortgaged of the real estate property, machinery or the

inventory. So there is security in the hand of the lenders, to in cash the mortgage property to

recover his loan amount, in case the borrowers default in the payment of interest on time.

On the other hand this features is not available in the case of equity financing.

Another reason for the high cost of the equity financing is that, in case the company get

bankrupt or insolvent, the holder of the debt is paid first with their interest and principle.

While equity holders are paid in the last stages, further the company will not pay any

dividend to the equity shareholder if the making losses, but the company has to pay interest

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

on the loan to the lender or the banks, even in the case of the loss. Therefore it can be said

that IPO are the expensive process of securing the long term sources of finance (Graham, &

Harvey, 2018).

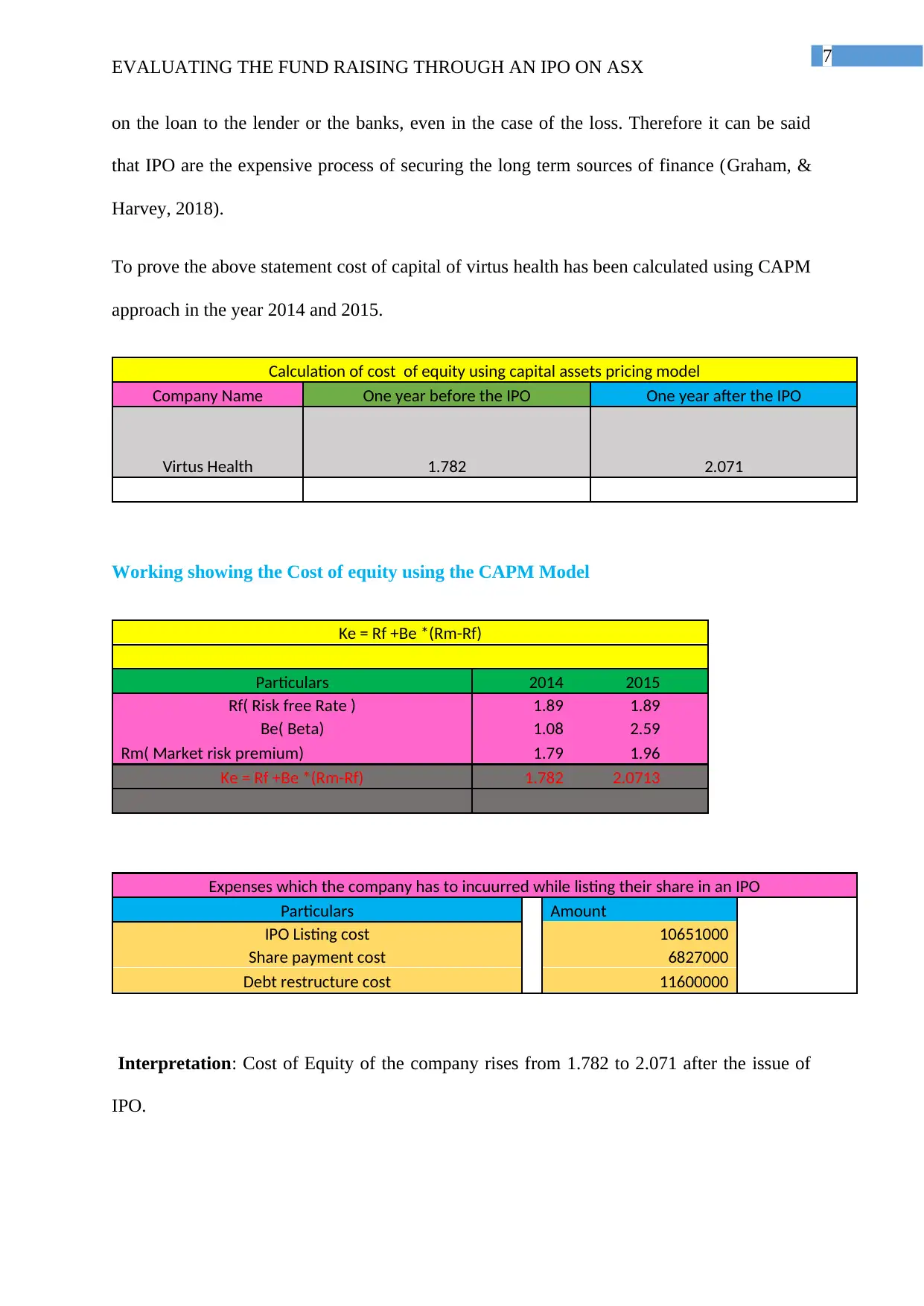

To prove the above statement cost of capital of virtus health has been calculated using CAPM

approach in the year 2014 and 2015.

Calculation of cost of equity using capital assets pricing model

Company Name One year before the IPO One year after the IPO

Virtus Health 1.782 2.071

Working showing the Cost of equity using the CAPM Model

Ke = Rf +Be *(Rm-Rf)

Particulars 2014 2015

Rf( Risk free Rate ) 1.89 1.89

Be( Beta) 1.08 2.59

Rm( Market risk premium) 1.79 1.96

Ke = Rf +Be *(Rm-Rf) 1.782 2.0713

Expenses which the company has to incuurred while listing their share in an IPO

Particulars Amount

IPO Listing cost 10651000

Share payment cost 6827000

Debt restructure cost 11600000

Interpretation: Cost of Equity of the company rises from 1.782 to 2.071 after the issue of

IPO.

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

on the loan to the lender or the banks, even in the case of the loss. Therefore it can be said

that IPO are the expensive process of securing the long term sources of finance (Graham, &

Harvey, 2018).

To prove the above statement cost of capital of virtus health has been calculated using CAPM

approach in the year 2014 and 2015.

Calculation of cost of equity using capital assets pricing model

Company Name One year before the IPO One year after the IPO

Virtus Health 1.782 2.071

Working showing the Cost of equity using the CAPM Model

Ke = Rf +Be *(Rm-Rf)

Particulars 2014 2015

Rf( Risk free Rate ) 1.89 1.89

Be( Beta) 1.08 2.59

Rm( Market risk premium) 1.79 1.96

Ke = Rf +Be *(Rm-Rf) 1.782 2.0713

Expenses which the company has to incuurred while listing their share in an IPO

Particulars Amount

IPO Listing cost 10651000

Share payment cost 6827000

Debt restructure cost 11600000

Interpretation: Cost of Equity of the company rises from 1.782 to 2.071 after the issue of

IPO.

8

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Answer to part (C)

Factor related to the Underpricing of share in an IPO.

Underpricing is basically the listing of the company share in an IPO below its market

value. A company share is considered to be trading at underpriced, when the offer price of the

stock was lower than the first day trading price of the share (Handa, & Singh, 2014). When a

company bring the IPO of the share, their aim is to raise more capital from the public, by

issuing the minimum number of share. This can only happen when the price of the share is

offered high and the general public have confidence in the business of the company.

On the other hand promoter or the investment banker of the company whose objective

is to float more number of share of the company in the IPO to reach the general masses and

book a handsome amount of profit on the company share by the fluctuation in the share price.

So the investment banker aims to float the share at lower price in order to earn maximum

commission and the profit (Hughes & Mester, 2013).

Determining the share price of the company on the IPO depends upon the several

factors and one such factors include quantitative factors. Which include reviewing the

financial position of the company bringing IPO, like the investment banker analysis the firm

financial cash flow, income statement, balance sheet. In an IPO the share price of the

company depends broadly on two factors like company present earning and the expected

earnings growth. Therefore its can said that the company share price in an IPO differs from

company to company based on their fundamental, business operation, market position and

many more.

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Answer to part (C)

Factor related to the Underpricing of share in an IPO.

Underpricing is basically the listing of the company share in an IPO below its market

value. A company share is considered to be trading at underpriced, when the offer price of the

stock was lower than the first day trading price of the share (Handa, & Singh, 2014). When a

company bring the IPO of the share, their aim is to raise more capital from the public, by

issuing the minimum number of share. This can only happen when the price of the share is

offered high and the general public have confidence in the business of the company.

On the other hand promoter or the investment banker of the company whose objective

is to float more number of share of the company in the IPO to reach the general masses and

book a handsome amount of profit on the company share by the fluctuation in the share price.

So the investment banker aims to float the share at lower price in order to earn maximum

commission and the profit (Hughes & Mester, 2013).

Determining the share price of the company on the IPO depends upon the several

factors and one such factors include quantitative factors. Which include reviewing the

financial position of the company bringing IPO, like the investment banker analysis the firm

financial cash flow, income statement, balance sheet. In an IPO the share price of the

company depends broadly on two factors like company present earning and the expected

earnings growth. Therefore its can said that the company share price in an IPO differs from

company to company based on their fundamental, business operation, market position and

many more.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

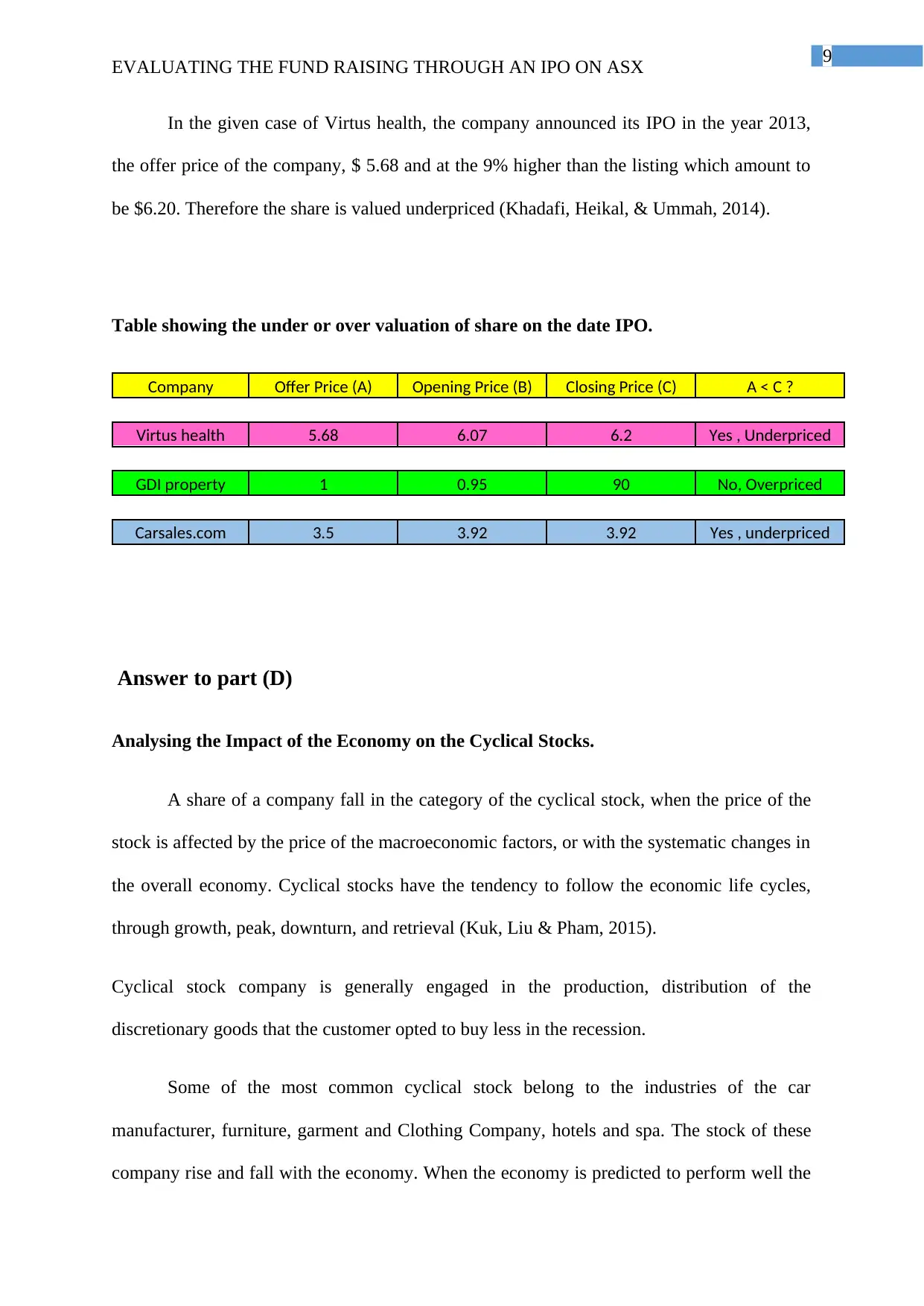

In the given case of Virtus health, the company announced its IPO in the year 2013,

the offer price of the company, $ 5.68 and at the 9% higher than the listing which amount to

be $6.20. Therefore the share is valued underpriced (Khadafi, Heikal, & Ummah, 2014).

Table showing the under or over valuation of share on the date IPO.

Company Offer Price (A) Opening Price (B) Closing Price (C) A < C ?

Virtus health 5.68 6.07 6.2 Yes , Underpriced

GDI property 1 0.95 90 No, Overpriced

Carsales.com 3.5 3.92 3.92 Yes , underpriced

Answer to part (D)

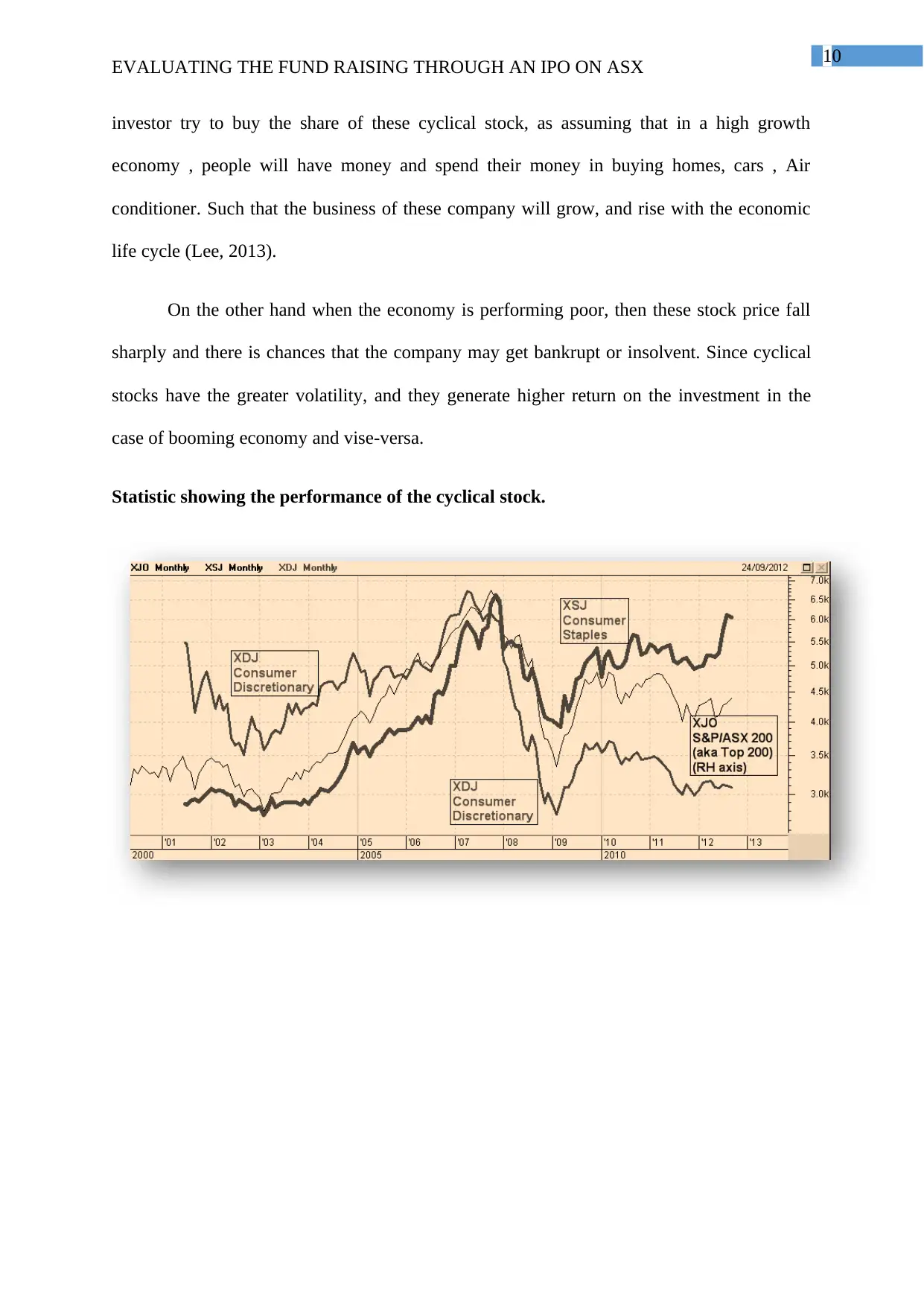

Analysing the Impact of the Economy on the Cyclical Stocks.

A share of a company fall in the category of the cyclical stock, when the price of the

stock is affected by the price of the macroeconomic factors, or with the systematic changes in

the overall economy. Cyclical stocks have the tendency to follow the economic life cycles,

through growth, peak, downturn, and retrieval (Kuk, Liu & Pham, 2015).

Cyclical stock company is generally engaged in the production, distribution of the

discretionary goods that the customer opted to buy less in the recession.

Some of the most common cyclical stock belong to the industries of the car

manufacturer, furniture, garment and Clothing Company, hotels and spa. The stock of these

company rise and fall with the economy. When the economy is predicted to perform well the

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

In the given case of Virtus health, the company announced its IPO in the year 2013,

the offer price of the company, $ 5.68 and at the 9% higher than the listing which amount to

be $6.20. Therefore the share is valued underpriced (Khadafi, Heikal, & Ummah, 2014).

Table showing the under or over valuation of share on the date IPO.

Company Offer Price (A) Opening Price (B) Closing Price (C) A < C ?

Virtus health 5.68 6.07 6.2 Yes , Underpriced

GDI property 1 0.95 90 No, Overpriced

Carsales.com 3.5 3.92 3.92 Yes , underpriced

Answer to part (D)

Analysing the Impact of the Economy on the Cyclical Stocks.

A share of a company fall in the category of the cyclical stock, when the price of the

stock is affected by the price of the macroeconomic factors, or with the systematic changes in

the overall economy. Cyclical stocks have the tendency to follow the economic life cycles,

through growth, peak, downturn, and retrieval (Kuk, Liu & Pham, 2015).

Cyclical stock company is generally engaged in the production, distribution of the

discretionary goods that the customer opted to buy less in the recession.

Some of the most common cyclical stock belong to the industries of the car

manufacturer, furniture, garment and Clothing Company, hotels and spa. The stock of these

company rise and fall with the economy. When the economy is predicted to perform well the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

investor try to buy the share of these cyclical stock, as assuming that in a high growth

economy , people will have money and spend their money in buying homes, cars , Air

conditioner. Such that the business of these company will grow, and rise with the economic

life cycle (Lee, 2013).

On the other hand when the economy is performing poor, then these stock price fall

sharply and there is chances that the company may get bankrupt or insolvent. Since cyclical

stocks have the greater volatility, and they generate higher return on the investment in the

case of booming economy and vise-versa.

Statistic showing the performance of the cyclical stock.

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

investor try to buy the share of these cyclical stock, as assuming that in a high growth

economy , people will have money and spend their money in buying homes, cars , Air

conditioner. Such that the business of these company will grow, and rise with the economic

life cycle (Lee, 2013).

On the other hand when the economy is performing poor, then these stock price fall

sharply and there is chances that the company may get bankrupt or insolvent. Since cyclical

stocks have the greater volatility, and they generate higher return on the investment in the

case of booming economy and vise-versa.

Statistic showing the performance of the cyclical stock.

11

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Answer to part (E)

There can be several objective of issuing an IPO, some of the reasons could be to convert

a private company to public or converting back the public to private company. However there

can be some other objective as for the issue of an IPO (Lukanima, & Swaray, 2013).

The company can use the fund for the research and development, funding of the

heavy expenditure project, or in the settlement of their long-term debt.

Increased in the public awareness about the company business, which ultimately lead

to the increase in the market share of the company.

IPO is the best way for many venture capitalist to sell their shareholding in the

company. Generally venture capitalist objective is to track a potential startup, fund

them with the necessary capital for their business, and ultimately sale their holding in

the company in an IPO to earn huge profit (Mayur, 2017).

However there are certain disadvantages the company has to face while listing their share in

the IPO. Some of them listed below.

EVALUATING THE FUND RAISING THROUGH AN IPO ON ASX

Answer to part (E)

There can be several objective of issuing an IPO, some of the reasons could be to convert

a private company to public or converting back the public to private company. However there

can be some other objective as for the issue of an IPO (Lukanima, & Swaray, 2013).

The company can use the fund for the research and development, funding of the

heavy expenditure project, or in the settlement of their long-term debt.

Increased in the public awareness about the company business, which ultimately lead

to the increase in the market share of the company.

IPO is the best way for many venture capitalist to sell their shareholding in the

company. Generally venture capitalist objective is to track a potential startup, fund

them with the necessary capital for their business, and ultimately sale their holding in

the company in an IPO to earn huge profit (Mayur, 2017).

However there are certain disadvantages the company has to face while listing their share in

the IPO. Some of them listed below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.