Comparative Analysis: Islamic and Conventional Banking in Bangladesh

VerifiedAdded on 2020/01/23

|12

|3810

|215

Dissertation

AI Summary

This dissertation proposal presents a comparative analysis of the benefits of conventional and Islamic banking systems on the socioeconomic sustainability and development of Bangladesh. It highlights the core difference between the two systems: the prohibition of Riba (interest) in Islamic banking based on Shariah principles. The study aims to investigate the comparative advantages of each system, considering the fluctuating currency values in Bangladesh and the limitations of Islamic banking in managing exchange rate risks. The research will employ an interpretivist paradigm, an inductive approach, a qualitative study, a survey technique, and a thematic approach for data analysis. The proposal includes a detailed introduction, literature review, proposed methodology, and references, outlining the research aims, objectives, and questions, along with a discussion of ethical considerations and a proposed timeline. The study seeks to provide insights into which banking model, conventional or Islamic, better serves the socioeconomic sustainability and development of Bangladesh, culminating in recommendations for optimal lending practices.

Dissertation proposal

(A comparative analysis of the benefits of conventional and

Islamic banking on the socioeconomic sustainability and

development of Bangladesh)

1

(A comparative analysis of the benefits of conventional and

Islamic banking on the socioeconomic sustainability and

development of Bangladesh)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The main difference between conventional banking system (CBS) and Islamic Banking

System (IBS) is the restrictions on Riba based on Shariah principle. It believe that charging an

interest on money is an unjust act because taking excess amount from the borrowers against the

principle money lent out cannot be considered as justice. Henceforth, it must be eliminated from the

banking system for the justice functionality of the banking sector. In Bangladesh, the Islamic

Banking has been adopted in the year 1983 and afterwards, it founded impressive growth in Muslim

South Asian countries. Islami Bank Committee’s chairman of Bangladesh said that the future of IBS

in Bangladesh looks very bright. However, in the country, the value of Euro, Pound, US dollar and

others are keep fluctuating rapidly which has a direct impact on country’s import and export and

exporters always gain greater return from the same. In order to manage risk, country is required to

manage current fluctuation risk whilst Shariah based IBS restrict covering exchange fluctuation risk

via creating forward contracts. Thus, this is the main reason behind the decisions made to

investigate the comparative benefits of the conventional and Islamic banking system in the socio-

economic sustainability and economic development of Bangladesh. It will be performed following

interpretivism paradigm, inductive approach, qualitative study, survey technique and thematic

approach for data analysis in order to investigate the selected topic.

2

The main difference between conventional banking system (CBS) and Islamic Banking

System (IBS) is the restrictions on Riba based on Shariah principle. It believe that charging an

interest on money is an unjust act because taking excess amount from the borrowers against the

principle money lent out cannot be considered as justice. Henceforth, it must be eliminated from the

banking system for the justice functionality of the banking sector. In Bangladesh, the Islamic

Banking has been adopted in the year 1983 and afterwards, it founded impressive growth in Muslim

South Asian countries. Islami Bank Committee’s chairman of Bangladesh said that the future of IBS

in Bangladesh looks very bright. However, in the country, the value of Euro, Pound, US dollar and

others are keep fluctuating rapidly which has a direct impact on country’s import and export and

exporters always gain greater return from the same. In order to manage risk, country is required to

manage current fluctuation risk whilst Shariah based IBS restrict covering exchange fluctuation risk

via creating forward contracts. Thus, this is the main reason behind the decisions made to

investigate the comparative benefits of the conventional and Islamic banking system in the socio-

economic sustainability and economic development of Bangladesh. It will be performed following

interpretivism paradigm, inductive approach, qualitative study, survey technique and thematic

approach for data analysis in order to investigate the selected topic.

2

Table of Contents

INTRODUCTION................................................................................................................................4

Background of the study..................................................................................................................4

Statement of the problem.................................................................................................................5

Research aims and objectives..........................................................................................................5

Research questions...........................................................................................................................6

LITERATURE REVIEW.....................................................................................................................6

Conventional banking system and Islamic Banking system............................................................6

Similarities and differences in CBS and IBS...................................................................................6

Benefits of conventional and Islamic banking system in socio-economic development................7

PROPOSED METHODOLOGY..........................................................................................................8

Research philosophy........................................................................................................................8

Research approach...........................................................................................................................8

Research type...................................................................................................................................8

Data collection.................................................................................................................................8

Data analysis....................................................................................................................................9

Original contribution........................................................................................................................9

Ethical issues....................................................................................................................................9

Proposed time scale.........................................................................................................................9

REFERENCES...................................................................................................................................10

3

INTRODUCTION................................................................................................................................4

Background of the study..................................................................................................................4

Statement of the problem.................................................................................................................5

Research aims and objectives..........................................................................................................5

Research questions...........................................................................................................................6

LITERATURE REVIEW.....................................................................................................................6

Conventional banking system and Islamic Banking system............................................................6

Similarities and differences in CBS and IBS...................................................................................6

Benefits of conventional and Islamic banking system in socio-economic development................7

PROPOSED METHODOLOGY..........................................................................................................8

Research philosophy........................................................................................................................8

Research approach...........................................................................................................................8

Research type...................................................................................................................................8

Data collection.................................................................................................................................8

Data analysis....................................................................................................................................9

Original contribution........................................................................................................................9

Ethical issues....................................................................................................................................9

Proposed time scale.........................................................................................................................9

REFERENCES...................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Background of the study

Banking sector plays an inevitable role in the economic growth of every nation.

Commercialized banks are one of the most critical components or financial intermediary in the

sector which connects surplus & deficit economic agents. During the period of financial crisis,

conventional banking sector suffered many challenges and issues in the banking industry, however,

Islamic banking system greatly insulated from the same as it proven as a preventive way for the

reoccurrence of global financial crisis, depression & economic downturn. The main difference

between conventional banking system (CBS) and Islamic Banking System (IBS) is the restrictions

on Riba based on Shariah principle (Abduh and Chowdhury, 2012). It believe that charging an

interest on money is an unjust act because taking excess amount from the borrowers against the

principle money lent out cannot be considered as justice. Henceforth, it must be eliminated from the

banking system for the justice functionality of the banking sector.

Lack of strict regulatory principles & legislations, lending excessive financing without

collateral debt obligations (CBO), less rate of interest in real estate, lack of transperancy etc. were

the main reason behind failure behind crisis in 2007/2008. However, in contrast, IBS reshaped the

CBS by creating adequate lending standards, effective & strong regulatory framework, efficient

monetary system and permission to invest in toxic assets i.e. derivative proven as a successful step

which triggered the global financial crisis (Saini, Bick and Abdulla, 2011). Unlike CBS which

provide a minimum return guarantee to the depositors, in IBS, PSIA (Profit Sharing Investment

Account Holder) accepts both the risk & return in the investment without any pre-guaranteed return

via Musharakah & Mudharabah contracts (Abedifar, Molyneux and Tarazi, 2013). In addition,

Sharaih principle also provide assistance to minimize the risk of interest rate by prohibiting

accepting any monetary return in the form of interest, riba or usuary as well. In the current times,

the total assets of IBS has been reported to $920b which is expected to grow to 1.8 trillion till the

end of year 2020 in Asian countries i.e. United Arab Emirates, Qatarm,, Kuwait, Saudi Arabia etc.

In Bangladesh, the shariah based Islamic Banking gain enough popularity and growing at a steady

rate because of high Muslim community (Muhammad Awan, Shahzad Bukhar. and Iqbal, 2011).

Although, both the CBS and IBS aims at rendering banking services to the populations, however,

both these system work on different principles and regulations, therefore, the main target of the

study is to examine the comparative analysis of the benefits of both the conventional and Islamic

banking on the socioeconomic sustainability and development of Bangladesh.

4

Background of the study

Banking sector plays an inevitable role in the economic growth of every nation.

Commercialized banks are one of the most critical components or financial intermediary in the

sector which connects surplus & deficit economic agents. During the period of financial crisis,

conventional banking sector suffered many challenges and issues in the banking industry, however,

Islamic banking system greatly insulated from the same as it proven as a preventive way for the

reoccurrence of global financial crisis, depression & economic downturn. The main difference

between conventional banking system (CBS) and Islamic Banking System (IBS) is the restrictions

on Riba based on Shariah principle (Abduh and Chowdhury, 2012). It believe that charging an

interest on money is an unjust act because taking excess amount from the borrowers against the

principle money lent out cannot be considered as justice. Henceforth, it must be eliminated from the

banking system for the justice functionality of the banking sector.

Lack of strict regulatory principles & legislations, lending excessive financing without

collateral debt obligations (CBO), less rate of interest in real estate, lack of transperancy etc. were

the main reason behind failure behind crisis in 2007/2008. However, in contrast, IBS reshaped the

CBS by creating adequate lending standards, effective & strong regulatory framework, efficient

monetary system and permission to invest in toxic assets i.e. derivative proven as a successful step

which triggered the global financial crisis (Saini, Bick and Abdulla, 2011). Unlike CBS which

provide a minimum return guarantee to the depositors, in IBS, PSIA (Profit Sharing Investment

Account Holder) accepts both the risk & return in the investment without any pre-guaranteed return

via Musharakah & Mudharabah contracts (Abedifar, Molyneux and Tarazi, 2013). In addition,

Sharaih principle also provide assistance to minimize the risk of interest rate by prohibiting

accepting any monetary return in the form of interest, riba or usuary as well. In the current times,

the total assets of IBS has been reported to $920b which is expected to grow to 1.8 trillion till the

end of year 2020 in Asian countries i.e. United Arab Emirates, Qatarm,, Kuwait, Saudi Arabia etc.

In Bangladesh, the shariah based Islamic Banking gain enough popularity and growing at a steady

rate because of high Muslim community (Muhammad Awan, Shahzad Bukhar. and Iqbal, 2011).

Although, both the CBS and IBS aims at rendering banking services to the populations, however,

both these system work on different principles and regulations, therefore, the main target of the

study is to examine the comparative analysis of the benefits of both the conventional and Islamic

banking on the socioeconomic sustainability and development of Bangladesh.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Statement of the problem

In Bangladesh, the Islamic Banking has been adopted in the year 1983 and afterwards, it

founded impressive growth in Muslim South Asian countries. Islami Bank Committee’s chairman of

Bangladesh said that the future of IBS in Bangladesh looks very bright. Islami Bank Bangladesh

Ltd achieved first position in the sector in the terms of deposits, investment, import & export &

collection of remittance (Ahmad, Rustam and Dent, 2011). In accordance with the central bank,

Bank of Bangladesh, total current deposits of IBS are 25% of the total private bank deposits and

30% of total investment (Ahmad, 2010). It is expecting to grow at faster pace because Bangladesh

is the third largest country, in which, majority of Muslims to 80% (148million) of total population

residing. However, in the country, the value of Euro, Pound, US dollar and others are keep

fluctuating rapidly which has a direct impact on country’s import and export and exporters always

gain greater return from the same. In order to manage risk, country is required to manage current

fluctuation risk whilst Shariah based IBS restrict covering exchange fluctuation risk via creating

forward contracts (Bangladesh’s Islamic Banking system, 2017). It prohibits risk hedging on a

particular transaction for the currency which is supposed to be decline. Further, due to the absence

of Islamic money marks, IBs are unable to invest their fund to gain further return on it. However, on

the contrary side, several researches conducted earlier founded that in Bangaldesh, many consumers

are not interested in transacting with the IBs because they believes that only the bank name has

been changed whilst they are still practised interest charges while it was strictly restricted. Bank is

service sector which plays a vital role in the socioeconomic sustainability and economic growth and

development. Therefore, the study targeted at examining and evaluating the comparative benefits of

both the banking system, IBS and CBS in the socio-economic sustainability and country’s growth

and development.

Research aims and objectives

Aim: The focus of the investigation is to obtain deeply understanding of the benefits as well

as shortcomings of conventional and Islamic banking system for the socioeconomic development of

Bangladesh

Research objective:

1. To develop an understanding of conventional and Islamic banking in the Global and

Bangladeshi context.

2. To conduct a comparative analysis of the perceptions of conventional and Islamic banking

within the customer community.

3. To conduct a comparative analysis of conventional and Islamic banking with respect to

5

In Bangladesh, the Islamic Banking has been adopted in the year 1983 and afterwards, it

founded impressive growth in Muslim South Asian countries. Islami Bank Committee’s chairman of

Bangladesh said that the future of IBS in Bangladesh looks very bright. Islami Bank Bangladesh

Ltd achieved first position in the sector in the terms of deposits, investment, import & export &

collection of remittance (Ahmad, Rustam and Dent, 2011). In accordance with the central bank,

Bank of Bangladesh, total current deposits of IBS are 25% of the total private bank deposits and

30% of total investment (Ahmad, 2010). It is expecting to grow at faster pace because Bangladesh

is the third largest country, in which, majority of Muslims to 80% (148million) of total population

residing. However, in the country, the value of Euro, Pound, US dollar and others are keep

fluctuating rapidly which has a direct impact on country’s import and export and exporters always

gain greater return from the same. In order to manage risk, country is required to manage current

fluctuation risk whilst Shariah based IBS restrict covering exchange fluctuation risk via creating

forward contracts (Bangladesh’s Islamic Banking system, 2017). It prohibits risk hedging on a

particular transaction for the currency which is supposed to be decline. Further, due to the absence

of Islamic money marks, IBs are unable to invest their fund to gain further return on it. However, on

the contrary side, several researches conducted earlier founded that in Bangaldesh, many consumers

are not interested in transacting with the IBs because they believes that only the bank name has

been changed whilst they are still practised interest charges while it was strictly restricted. Bank is

service sector which plays a vital role in the socioeconomic sustainability and economic growth and

development. Therefore, the study targeted at examining and evaluating the comparative benefits of

both the banking system, IBS and CBS in the socio-economic sustainability and country’s growth

and development.

Research aims and objectives

Aim: The focus of the investigation is to obtain deeply understanding of the benefits as well

as shortcomings of conventional and Islamic banking system for the socioeconomic development of

Bangladesh

Research objective:

1. To develop an understanding of conventional and Islamic banking in the Global and

Bangladeshi context.

2. To conduct a comparative analysis of the perceptions of conventional and Islamic banking

within the customer community.

3. To conduct a comparative analysis of conventional and Islamic banking with respect to

5

socioeconomic advancement i.e. improving the liquidity of the “High Street” and Small and

Medium Sized Enterprises (SMEs).

4. To determine whether the socioeconomic sustainability and development of Bangladesh can be

better served by either the conventional banking model or the Islamic banking model.

5. To develop a series of recommendations on the best lending practices (conventional Versus

Islamic models) for the sustainability and socioeconomic development of the Bangladeshi

populus.

Research questions

How Conventional banking system and Islamic banking system drive benefits to the

Bangladesh in socio-economic sustainability & nation’s progress?

LITERATURE REVIEW

Conventional banking system and Islamic Banking system

According to the views of Akhter, Raza and Akram, (2011), Islamic banking system (IBS)

has been defined as a systematic regulatory framework of banking activities and operations in line

with the Islamic law based on the principle of Shariah system. It is guided, regulated and monitored

by the Islamic economics which believes that imposing interest obligations i.e. riba to the borrowers

for the money provided to them is an injustice, therefore, it must be prohibited and eliminated from

the system. The system is based on two fundamental principles that are sharing profit as well as

losses and disallowing the collection & payment of interest charges from the borrowers and to the

investors as well.

However, on the other side, Lee. and Ullah, (2011), stated that conventional banking system

(CBS) refers to a system that aims at delivering distinguish financial services i.e. deposit

acceptance, withdrawal on demand, granting loans and many others. Commercial Banks (CBs)

provides various investment products to the depositors like saving account, deposits, certificate of

deposits, time deposits, accounts checking, overdraft and others for getting maximum return. They

accept deposits and grant it to the others at some interest charges which is obviously above the

interest rate on consumer deposits and by this way, they make money. Similarly, Sun and et.al.,

(2012), studied that CBs charge high rate of interest for the monetary return from the borrowers and

provide less interest to the depositors and the net interest difference drive income and profit to the

banks.

Similarities and differences in CBS and IBS

Echchabi and Nafiu Olaniyi, (2012), stated that CBS and IBS are similar to each other as

6

Medium Sized Enterprises (SMEs).

4. To determine whether the socioeconomic sustainability and development of Bangladesh can be

better served by either the conventional banking model or the Islamic banking model.

5. To develop a series of recommendations on the best lending practices (conventional Versus

Islamic models) for the sustainability and socioeconomic development of the Bangladeshi

populus.

Research questions

How Conventional banking system and Islamic banking system drive benefits to the

Bangladesh in socio-economic sustainability & nation’s progress?

LITERATURE REVIEW

Conventional banking system and Islamic Banking system

According to the views of Akhter, Raza and Akram, (2011), Islamic banking system (IBS)

has been defined as a systematic regulatory framework of banking activities and operations in line

with the Islamic law based on the principle of Shariah system. It is guided, regulated and monitored

by the Islamic economics which believes that imposing interest obligations i.e. riba to the borrowers

for the money provided to them is an injustice, therefore, it must be prohibited and eliminated from

the system. The system is based on two fundamental principles that are sharing profit as well as

losses and disallowing the collection & payment of interest charges from the borrowers and to the

investors as well.

However, on the other side, Lee. and Ullah, (2011), stated that conventional banking system

(CBS) refers to a system that aims at delivering distinguish financial services i.e. deposit

acceptance, withdrawal on demand, granting loans and many others. Commercial Banks (CBs)

provides various investment products to the depositors like saving account, deposits, certificate of

deposits, time deposits, accounts checking, overdraft and others for getting maximum return. They

accept deposits and grant it to the others at some interest charges which is obviously above the

interest rate on consumer deposits and by this way, they make money. Similarly, Sun and et.al.,

(2012), studied that CBs charge high rate of interest for the monetary return from the borrowers and

provide less interest to the depositors and the net interest difference drive income and profit to the

banks.

Similarities and differences in CBS and IBS

Echchabi and Nafiu Olaniyi, (2012), stated that CBS and IBS are similar to each other as

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

both the systems accepts deposits from the consumers called depositors. Both the banks provide

various financial services and operate banking functions and activities like acceptance of deposits,

withdrawal facilities, loan facilities and others. Moreover, they follows same objective to serve

banking services to the consumers to satisfy their needs & demands.

However, as per the viewpoint of Hisham Yahya, Muhammad and Razak Abdul Hadi,

(2012), the key difference between CBS and IBS is that later is based on Shariah principle which

prohibits charging any kind of interest, fees and others to get excess money from the principle

amount, unlike this, CBS considers money as a commodity which can be rented out above the face

value to get excess return. In such respect, CBs charge interest taking into account the borrower’s

credit position and time value whilst IBS earn money by generating profit on trading activities. It is

because, IB operates on the basis of profit-loss sharing concept, in which, loss is shared among

parties on the basis of mode of finance i.e. Musharakah (profit/loss sharing agreement/partnership

contract), Ijarah (Leasing), Mudharabah (equity participation), Murabaha (Cost plus sale) & many

others. On the critical note, Ariff and Rosly (2011), argued that IBS is considered as an alternative

banking approach to minimize the risk of crisis reoccurrence by creating strict regulatory

framework, ethical conduct, restriction on sale of debt, investment in toxic assets i.e. derivatives,

elimination of sub-prime exposure and so on. Further, Hidayat and Abduh, (2012), commented that

CBS works on the principle of risk hedging or elimination whilst IBS works on the bearing risk

principle. CBs charges penalties also for the default of the borrower, unlike this, IBs do not charge

any penalty for such offence.

Benefits of conventional and Islamic banking system in socio-economic development

Banking system plays an important role in the growth and development of Bangladesh a

they provides security to the borrowers by accepting deposits, lends money for different duration as

per the actual requirement and also provides other financial services. Butt and et.al., (2011), studied

that CBs are the financial institutions that are limited to the monetary activities for the monetary

control in the nation, unlike it, IBs work under Shariah principle for the betterment or socio-

economic welfare. It not only aims at removal of interest charges and introduces Zakah system but

also it targets the development of balanced and just banking structure or social order which is totally

free from any kind of exploitation for the socio-economic sustainability. Thus, it follows equity

based principles for the equality treatment.

Ariff and Rosly (2011), also conducted a study and identified that in Bangladesh, Islamic

Banking has a direct responsibility of socioeconomic development by adhering with the Islamic

philosophy to attain widespread support from the service users. IBBL in Bangladesh generated

7

various financial services and operate banking functions and activities like acceptance of deposits,

withdrawal facilities, loan facilities and others. Moreover, they follows same objective to serve

banking services to the consumers to satisfy their needs & demands.

However, as per the viewpoint of Hisham Yahya, Muhammad and Razak Abdul Hadi,

(2012), the key difference between CBS and IBS is that later is based on Shariah principle which

prohibits charging any kind of interest, fees and others to get excess money from the principle

amount, unlike this, CBS considers money as a commodity which can be rented out above the face

value to get excess return. In such respect, CBs charge interest taking into account the borrower’s

credit position and time value whilst IBS earn money by generating profit on trading activities. It is

because, IB operates on the basis of profit-loss sharing concept, in which, loss is shared among

parties on the basis of mode of finance i.e. Musharakah (profit/loss sharing agreement/partnership

contract), Ijarah (Leasing), Mudharabah (equity participation), Murabaha (Cost plus sale) & many

others. On the critical note, Ariff and Rosly (2011), argued that IBS is considered as an alternative

banking approach to minimize the risk of crisis reoccurrence by creating strict regulatory

framework, ethical conduct, restriction on sale of debt, investment in toxic assets i.e. derivatives,

elimination of sub-prime exposure and so on. Further, Hidayat and Abduh, (2012), commented that

CBS works on the principle of risk hedging or elimination whilst IBS works on the bearing risk

principle. CBs charges penalties also for the default of the borrower, unlike this, IBs do not charge

any penalty for such offence.

Benefits of conventional and Islamic banking system in socio-economic development

Banking system plays an important role in the growth and development of Bangladesh a

they provides security to the borrowers by accepting deposits, lends money for different duration as

per the actual requirement and also provides other financial services. Butt and et.al., (2011), studied

that CBs are the financial institutions that are limited to the monetary activities for the monetary

control in the nation, unlike it, IBs work under Shariah principle for the betterment or socio-

economic welfare. It not only aims at removal of interest charges and introduces Zakah system but

also it targets the development of balanced and just banking structure or social order which is totally

free from any kind of exploitation for the socio-economic sustainability. Thus, it follows equity

based principles for the equality treatment.

Ariff and Rosly (2011), also conducted a study and identified that in Bangladesh, Islamic

Banking has a direct responsibility of socioeconomic development by adhering with the Islamic

philosophy to attain widespread support from the service users. IBBL in Bangladesh generated

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

employment in the country by direct or indirect ways like import-export, employment in banking

sector, industrialization and many other projects. It also makes significant contribution to the rural

economy evidencing IBBL’s Rural Development Scheme helps to maximize the standard of living

in rural areas to a large extent and promote country’s growth. Further, Green banking, ethical

principles and others maintained ecological sustainability in the economy. In despite Abedifar,

Molyneux and Tarazi (2013), small and medium sized enterprises also plays an important role in the

growth of the country, and IBS has given adequate support and importance to the sector. They

provide them funding facilities and also give an idea how potential entrepreneurs can develop their

business following Islamic principles.

PROPOSED METHODOLOGY

Research philosophy

Interpretivism philosophy will be founded suitable, in which, investigator of the study

believes in the multiplicity of reality. They follow flexible research to carry out the investigation to

study the comparative benefits of conventional as well as Islamic banking system in the economic

growth and socio-economic sustainability of Bangladesh (Silverman, 2016).

Research approach

Out of two approaches, inductive Vs deductive, inductive approach will be founded better

for the chosen research phenomena which are based on comparative analysis of the advantages that

will be drive by CBS and IBS in the growth and sustainable progress of Bangladesh.

Research type

In order to explore the advantages of both the conventional as well as Islamic banking

system in socio-economic growth and nation’s growth, qualitative investigation looks appropriate.

Thus, scholar will gather qualitative set of data to evaluate and assess the role of both the banking

system so that perfect analysis can be made that how these may be helpful in the economic

development and growth of Bangladesh (Mackey and Gass, 2015).

Data collection

It is the most important for the scholar to acquire and obtain significant amount of data

required for the chosen study. There are two methods from which data can be gathered, primary

adopts new and fresh information whereas secondary method utilizes already available information.

Here, with the proposed investigation, primary method is an appropriate study, in this; researcher

will conduct an online survey of 100 existing customers that utilize banking services. The sample

will be chosen randomly free from any biasness. Customers will be surveyed via online

8

sector, industrialization and many other projects. It also makes significant contribution to the rural

economy evidencing IBBL’s Rural Development Scheme helps to maximize the standard of living

in rural areas to a large extent and promote country’s growth. Further, Green banking, ethical

principles and others maintained ecological sustainability in the economy. In despite Abedifar,

Molyneux and Tarazi (2013), small and medium sized enterprises also plays an important role in the

growth of the country, and IBS has given adequate support and importance to the sector. They

provide them funding facilities and also give an idea how potential entrepreneurs can develop their

business following Islamic principles.

PROPOSED METHODOLOGY

Research philosophy

Interpretivism philosophy will be founded suitable, in which, investigator of the study

believes in the multiplicity of reality. They follow flexible research to carry out the investigation to

study the comparative benefits of conventional as well as Islamic banking system in the economic

growth and socio-economic sustainability of Bangladesh (Silverman, 2016).

Research approach

Out of two approaches, inductive Vs deductive, inductive approach will be founded better

for the chosen research phenomena which are based on comparative analysis of the advantages that

will be drive by CBS and IBS in the growth and sustainable progress of Bangladesh.

Research type

In order to explore the advantages of both the conventional as well as Islamic banking

system in socio-economic growth and nation’s growth, qualitative investigation looks appropriate.

Thus, scholar will gather qualitative set of data to evaluate and assess the role of both the banking

system so that perfect analysis can be made that how these may be helpful in the economic

development and growth of Bangladesh (Mackey and Gass, 2015).

Data collection

It is the most important for the scholar to acquire and obtain significant amount of data

required for the chosen study. There are two methods from which data can be gathered, primary

adopts new and fresh information whereas secondary method utilizes already available information.

Here, with the proposed investigation, primary method is an appropriate study, in this; researcher

will conduct an online survey of 100 existing customers that utilize banking services. The sample

will be chosen randomly free from any biasness. Customers will be surveyed via online

8

questionnaire from whom a set of questions will be asked to determine that why they use particular

banking services and what benefits it delivers for the growth of the Bangladesh economy.

Data analysis

In order to examine the data set, thematic approach will be used by the investigator for

examining the comparative analysis of the benefits of CBS and IBS regarding their choice of

banking selection.

Original contribution

Although many researches was performed earlier in the related area i.e. to examine both the

banks performance and others, still, no one studied the problem of comparative evaluation of the

role and importance of CBS and IBS in the socio-economic sustainability and development of the

economy. So, undoubtedly, the study will provide a significant contribution to explore and

investigate the prevailing issue in the banking sector. The study will showcase clearly the

differences in the benefits of both the banking systems, CBS or IBS (Flick, 2015). Lastly, the study

will give a set of recommendations on the lending practices under CBS versus IBS for the

socioeconomic development of Bangladesh.

Ethical issues

Confidentiality is the main ethical issue, in which, scholar will be require to keep

information confidential so that unauthorized person cannot take any kind of benefits from the

same. Secondly, responses of the selected participations also will be kept highly confidential. For

obtaining any information, investigator will get prior approval and consent from the participants,

banks and others. It will assure reliability of the data gathered and help to find out the right solution.

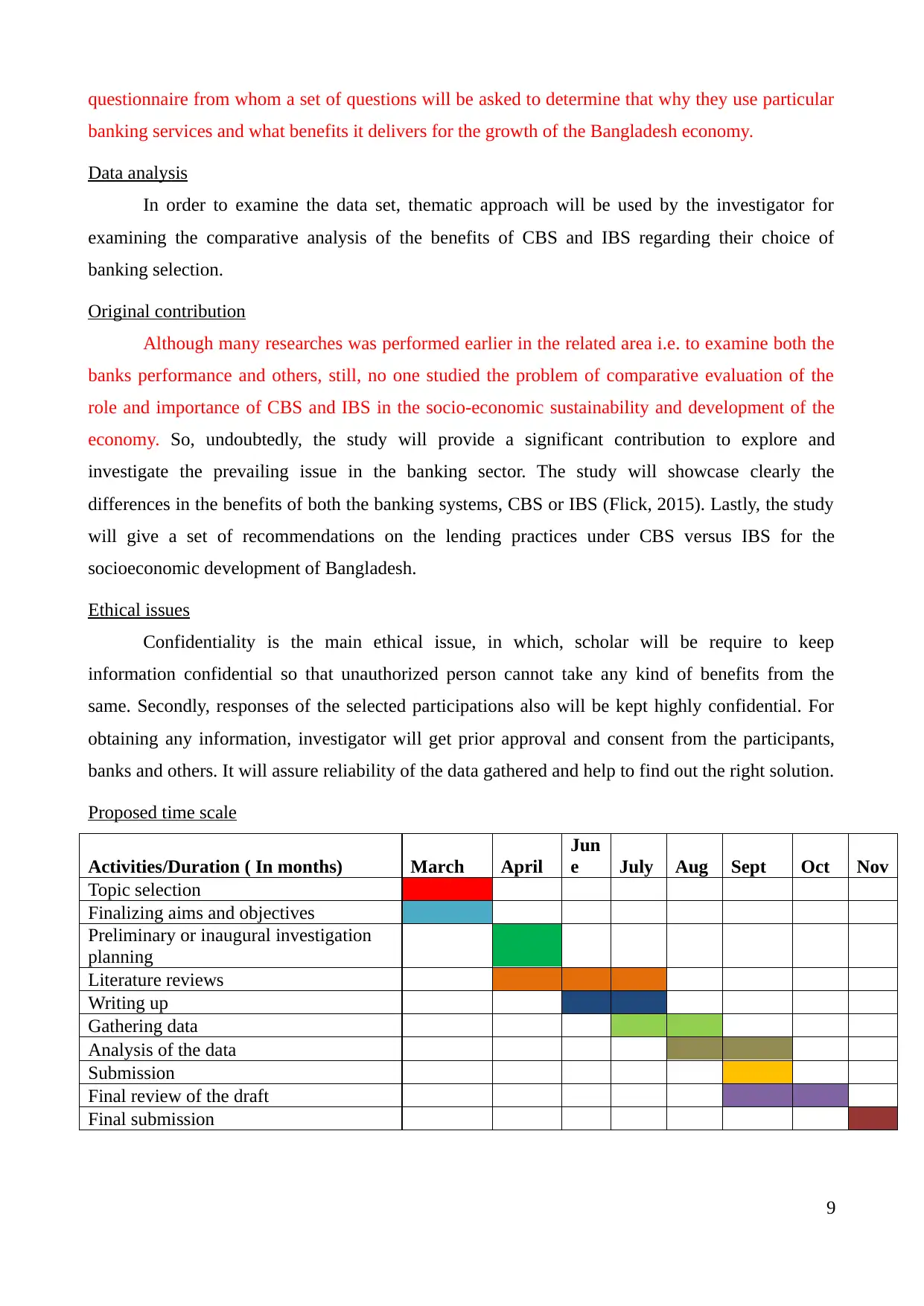

Proposed time scale

Activities/Duration ( In months) March April

Jun

e July Aug Sept Oct Nov

Topic selection

Finalizing aims and objectives

Preliminary or inaugural investigation

planning

Literature reviews

Writing up

Gathering data

Analysis of the data

Submission

Final review of the draft

Final submission

9

banking services and what benefits it delivers for the growth of the Bangladesh economy.

Data analysis

In order to examine the data set, thematic approach will be used by the investigator for

examining the comparative analysis of the benefits of CBS and IBS regarding their choice of

banking selection.

Original contribution

Although many researches was performed earlier in the related area i.e. to examine both the

banks performance and others, still, no one studied the problem of comparative evaluation of the

role and importance of CBS and IBS in the socio-economic sustainability and development of the

economy. So, undoubtedly, the study will provide a significant contribution to explore and

investigate the prevailing issue in the banking sector. The study will showcase clearly the

differences in the benefits of both the banking systems, CBS or IBS (Flick, 2015). Lastly, the study

will give a set of recommendations on the lending practices under CBS versus IBS for the

socioeconomic development of Bangladesh.

Ethical issues

Confidentiality is the main ethical issue, in which, scholar will be require to keep

information confidential so that unauthorized person cannot take any kind of benefits from the

same. Secondly, responses of the selected participations also will be kept highly confidential. For

obtaining any information, investigator will get prior approval and consent from the participants,

banks and others. It will assure reliability of the data gathered and help to find out the right solution.

Proposed time scale

Activities/Duration ( In months) March April

Jun

e July Aug Sept Oct Nov

Topic selection

Finalizing aims and objectives

Preliminary or inaugural investigation

planning

Literature reviews

Writing up

Gathering data

Analysis of the data

Submission

Final review of the draft

Final submission

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abduh, M. and Azmi Omar, M., 2012. Islamic banking and economic growth: the Indonesian

experience. International Journal of Islamic and Middle Eastern Finance and

Management. 5(1), pp.35-47.

Abduh, M. and Chowdhury, N.T., 2012. Does Islamic banking matter for economic growth in

Bangladesh. Journal of Islamic Economics, Banking and Finance. 8(3). pp.104-113.

Abedifar, P., Molyneux, P. and Tarazi, A., 2013. Risk in Islamic banking. Review of Finance, 17(6),

pp.2035-2096.

Ahmad, K., Rustam, G.A. and Dent, M.M., 2011. Brand preference in Islamic banking. Journal of

Islamic Marketing. 2(1). pp.74-82.

Akhter, W., Raza, A. and Akram, M., 2011. Efficiency and performance of Islamic Banking: The

case of Pakistan. Far East Journal of Psychology and Business. 2(2). pp.54-71.

Ariff, M. and Rosly, S.A., 2011. Islamic banking in Malaysia: unchartered waters. Asian Economic

Policy Review. 6(2). pp.301-319.

Butt, I. and et.al., 2011. Barriers to adoption of Islamic banking in Pakistan. Journal of Islamic

Marketing. 2(3). pp.259-273.

Echchabi, A. and Nafiu Olaniyi, O., 2012. Malaysian consumers' preferences for Islamic banking

attributes. International journal of social economics. 39(11). pp.859-874.

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research project.

Sage.

Hidayat, S.E. and Abduh, M., 2012. Does financial crisis give impacts on Bahrain Islamic banking

performance? A panel regression analysis. International Journal of Economics and

Finance. 4(7). p.79.

Hisham Yahya, M., Muhammad, J. and Razak Abdul Hadi, A., 2012. A comparative study on the

level of efficiency between Islamic and conventional banking systems in

Malaysia. International Journal of Islamic and Middle Eastern Finance and

Management. 5(1). pp.48-62.

Lee, K.H. and Ullah, S., 2011. Customers' attitude toward Islamic banking in

Pakistan. International Journal of Islamic and Middle Eastern Finance and Management.

4(2). pp.131-145.

11

Books and Journals

Abduh, M. and Azmi Omar, M., 2012. Islamic banking and economic growth: the Indonesian

experience. International Journal of Islamic and Middle Eastern Finance and

Management. 5(1), pp.35-47.

Abduh, M. and Chowdhury, N.T., 2012. Does Islamic banking matter for economic growth in

Bangladesh. Journal of Islamic Economics, Banking and Finance. 8(3). pp.104-113.

Abedifar, P., Molyneux, P. and Tarazi, A., 2013. Risk in Islamic banking. Review of Finance, 17(6),

pp.2035-2096.

Ahmad, K., Rustam, G.A. and Dent, M.M., 2011. Brand preference in Islamic banking. Journal of

Islamic Marketing. 2(1). pp.74-82.

Akhter, W., Raza, A. and Akram, M., 2011. Efficiency and performance of Islamic Banking: The

case of Pakistan. Far East Journal of Psychology and Business. 2(2). pp.54-71.

Ariff, M. and Rosly, S.A., 2011. Islamic banking in Malaysia: unchartered waters. Asian Economic

Policy Review. 6(2). pp.301-319.

Butt, I. and et.al., 2011. Barriers to adoption of Islamic banking in Pakistan. Journal of Islamic

Marketing. 2(3). pp.259-273.

Echchabi, A. and Nafiu Olaniyi, O., 2012. Malaysian consumers' preferences for Islamic banking

attributes. International journal of social economics. 39(11). pp.859-874.

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research project.

Sage.

Hidayat, S.E. and Abduh, M., 2012. Does financial crisis give impacts on Bahrain Islamic banking

performance? A panel regression analysis. International Journal of Economics and

Finance. 4(7). p.79.

Hisham Yahya, M., Muhammad, J. and Razak Abdul Hadi, A., 2012. A comparative study on the

level of efficiency between Islamic and conventional banking systems in

Malaysia. International Journal of Islamic and Middle Eastern Finance and

Management. 5(1). pp.48-62.

Lee, K.H. and Ullah, S., 2011. Customers' attitude toward Islamic banking in

Pakistan. International Journal of Islamic and Middle Eastern Finance and Management.

4(2). pp.131-145.

11

Mackey, A. and Gass, S.M., 2015. Second language research: Methodology and design. Routledge.

Muhammad Awan, H., Shahzad Bukhari, K. and Iqbal, A., 2011. Service quality and customer

satisfaction in the banking sector: A comparative study of conventional and Islamic banks in

Pakistan. Journal of Islamic Marketing. 2(3). pp.203-224.

Saini, Y., Bick, G. and Abdulla, L., 2011. Consumer awareness and usage of Islamic banking

products in South Africa. South African Journal of Economic and Management Sciences.

14(3), pp.298-313.

Silverman, D. ed., 2016. Qualitative research. Sage.

Sun, S. and et.al., 2012. The influence of religion on Islamic mobile phone banking services

adoption. Journal of Islamic Marketing. 3(1). pp.81-98.

Online

Ahmad, F., 2010. Islamic Banking in Bangladesh. [Online]. Available through:

http://islamicbanking.info/islamic-banking-in-bangladesh/. [Accessed on 23rd March 2017].

Bangladesh’s Islamic Banking system. 2017. [Online]. Available through:

http://www.shahfoundationbd.org/hannan/article10.html. [Accessed on 23rd March 2017].

12

Muhammad Awan, H., Shahzad Bukhari, K. and Iqbal, A., 2011. Service quality and customer

satisfaction in the banking sector: A comparative study of conventional and Islamic banks in

Pakistan. Journal of Islamic Marketing. 2(3). pp.203-224.

Saini, Y., Bick, G. and Abdulla, L., 2011. Consumer awareness and usage of Islamic banking

products in South Africa. South African Journal of Economic and Management Sciences.

14(3), pp.298-313.

Silverman, D. ed., 2016. Qualitative research. Sage.

Sun, S. and et.al., 2012. The influence of religion on Islamic mobile phone banking services

adoption. Journal of Islamic Marketing. 3(1). pp.81-98.

Online

Ahmad, F., 2010. Islamic Banking in Bangladesh. [Online]. Available through:

http://islamicbanking.info/islamic-banking-in-bangladesh/. [Accessed on 23rd March 2017].

Bangladesh’s Islamic Banking system. 2017. [Online]. Available through:

http://www.shahfoundationbd.org/hannan/article10.html. [Accessed on 23rd March 2017].

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.