Assignment III: Islamic and Conventional Banking Resilience Analysis

VerifiedAdded on 2022/09/15

|10

|1351

|15

Report

AI Summary

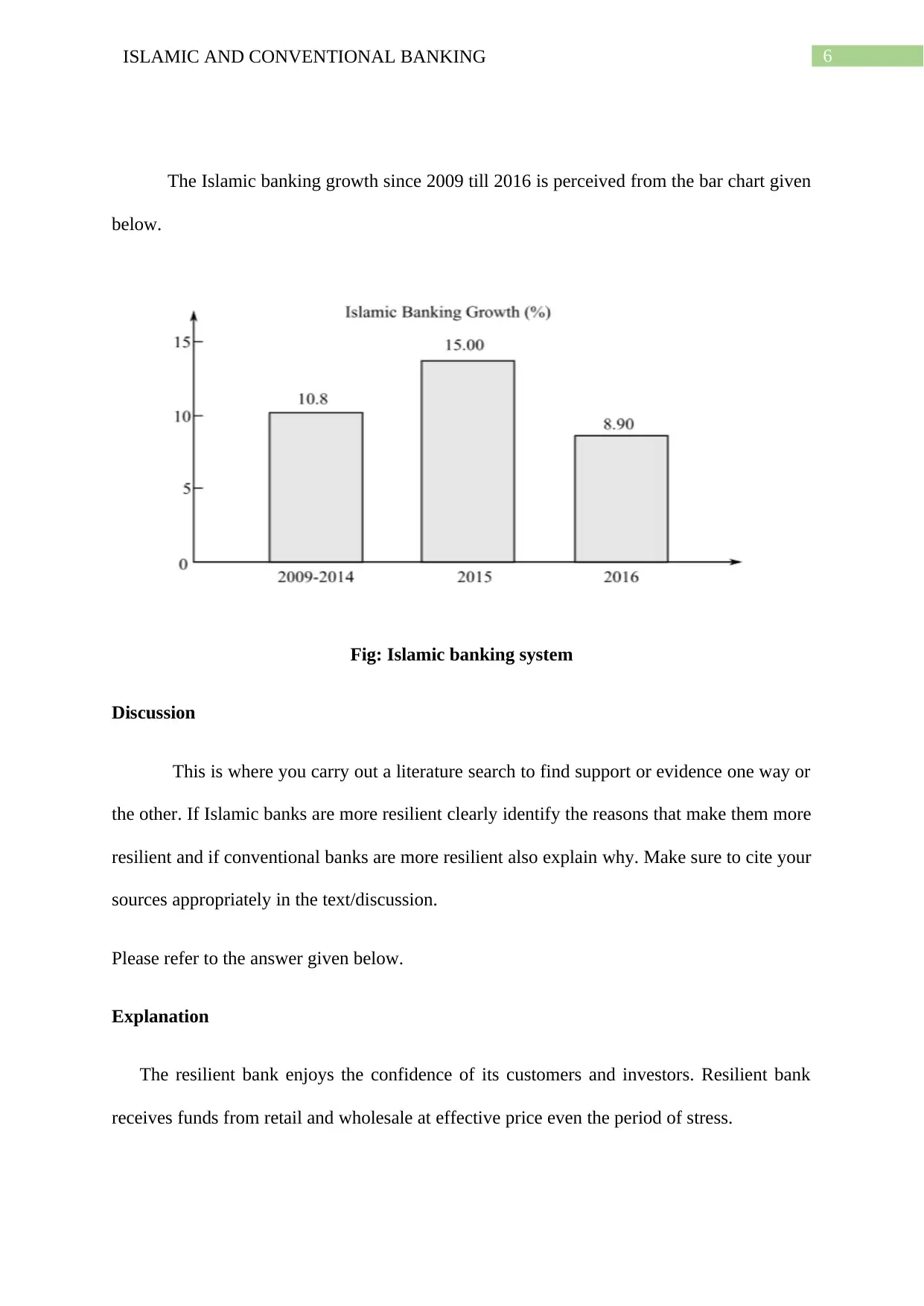

This report provides a comprehensive comparison between Islamic and conventional banking systems, focusing on their resilience during financial crises. It begins with an introduction to Islamic banking, highlighting its principles and key differences from conventional banking, including the prohibition of interest and the use of equity participation. The report then delves into the growth of Islamic banking globally, with a specific focus on the UAE as a pioneer in this sector. The core of the report involves a literature search to assess the resilience of Islamic banks compared to conventional banks during financial crises, supported by figures and charts that display the growth of Islamic banking assets. The discussion section analyzes the factors contributing to the resilience of each type of bank, citing relevant sources. The report also includes an overview of various Islamic financial instruments such as Murabahah, Ljarah, Sukuk, Musharakah, and Mudarabah. The findings suggest that while Islamic banks may be less liquid in the short term, they often demonstrate greater resilience in the long term due to their focus on real assets, strategic locations, and less exposure to the factors that caused conventional bank failures. The report concludes with a summary of key findings, providing a clear comparison of the two systems and highlighting the strengths of Islamic banking in maintaining investor trust.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.